Key Insights

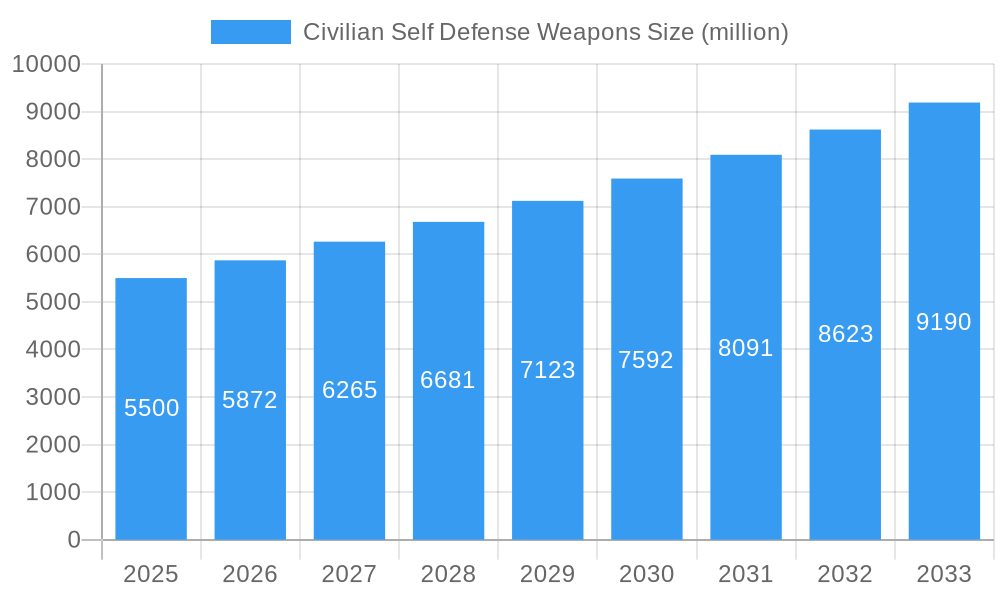

The global Civilian Self Defense Weapons market is projected for substantial growth, anticipated to reach USD 3.96 billion by 2025. This expansion is driven by a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. Key growth drivers include rising personal safety concerns in urban and suburban areas, increasing crime rates, and a growing consumer awareness of self-protection rights. Technological advancements are introducing more sophisticated, user-friendly, and less lethal self-defense options, broadening market appeal across demographics. Enhanced disposable incomes in developing economies are also contributing to increased investment in personal security.

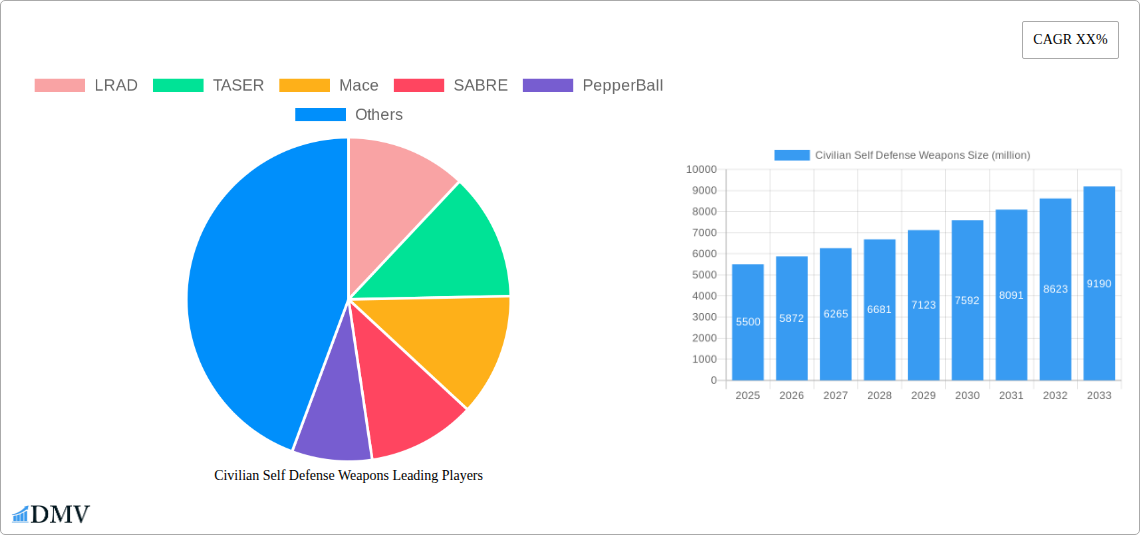

Civilian Self Defense Weapons Market Size (In Billion)

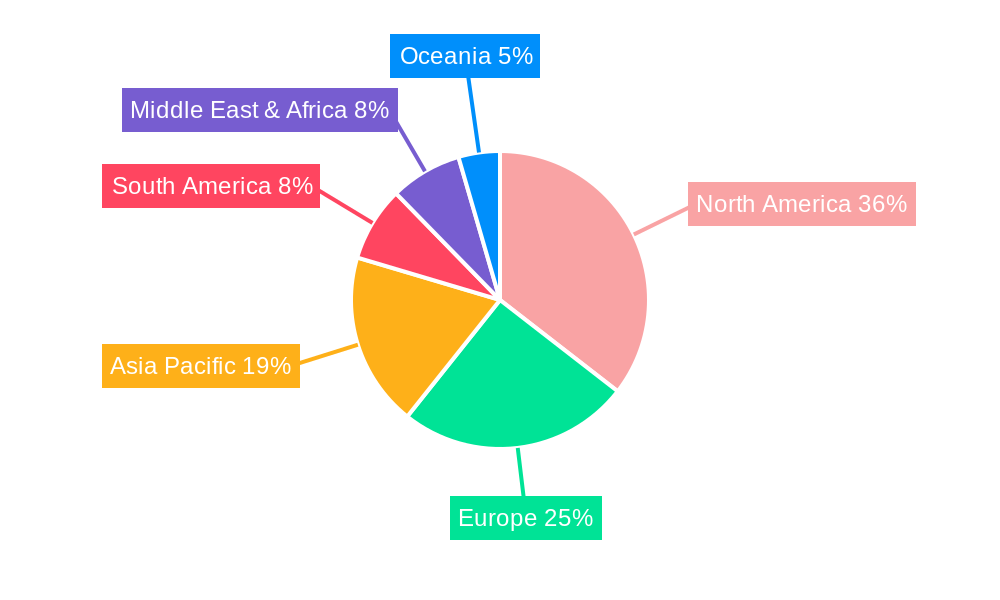

Market segmentation highlights significant demand within specific applications and product types. The Women and Children segments are expected to show robust growth, influenced by heightened vulnerability concerns. Students also represent an expanding consumer base due to campus safety considerations. In terms of product types, Stun Guns and Pepper Spray devices are anticipated to capture a dominant market share, attributed to their perceived efficacy, widespread legality, and ease of use. Self-defense integrated lighting devices are also gaining popularity. Leading companies like TASER, SABRE, and Mace are actively innovating and expanding their offerings in response to evolving consumer needs, fostering a competitive environment that benefits consumers with improved products and pricing. Geographically, North America currently leads the market, supported by established safety measures and high consumer adoption. Asia Pacific and Europe present significant growth opportunities driven by urbanization and an increasing emphasis on personal security.

Civilian Self Defense Weapons Company Market Share

Civilian Self Defense Weapons Market Composition & Trends

The civilian self-defense weapons market, a critical sector for personal safety, is characterized by a dynamic interplay of innovation, regulatory oversight, and evolving consumer needs. Market concentration is moderate, with key players like TASER, Mace, and SABRE holding significant shares, yet a growing number of specialized manufacturers are emerging. Innovation catalysts are primarily driven by advancements in less-lethal technologies, aiming for enhanced effectiveness and reduced risk of severe harm. Regulatory landscapes vary globally, influencing product availability and consumer adoption; for instance, regulations surrounding stun guns and pepper spray differ significantly between regions. Substitute products, such as personal alarms and high-visibility safety apps, also present competition, though their efficacy is often perceived as complementary rather than direct replacements for tangible self-defense tools. End-user profiles are diverse, encompassing women seeking protection, parents concerned for their children's safety, students on campuses, and a broad spectrum of "others" prioritizing personal security. Mergers and acquisitions (M&A) activities are notable, with an estimated aggregate deal value in the low millions of dollars, indicating consolidation and strategic expansion. For example, Safariland's acquisitions have broadened its personal defense portfolio. The market share distribution sees established brands like TASER commanding a substantial portion, estimated at over 30 million dollars in revenue, followed by Mace and SABRE, each contributing tens of millions. Emerging companies are carving out niches, particularly in specialized lighting devices and advanced less-lethal projectile systems.

- Market Share Distribution: Leading companies like TASER, Mace, and SABRE collectively hold an estimated 60% of the global market.

- M&A Deal Value: Estimated aggregate deal value for M&A activities in the historical period was approximately $XX million.

- Innovation Focus: Continued investment in miniaturization, improved battery life, and non-lethal payload delivery systems.

- Regulatory Impact: Growing awareness and lobbying efforts surrounding self-defense rights are shaping product development and market access.

Civilian Self Defense Weapons Industry Evolution

The civilian self-defense weapons industry has undergone a significant evolution, transforming from a niche market to a mainstream sector driven by increasing global security concerns and technological advancements. Over the study period from 2019 to 2033, the market has witnessed consistent growth trajectories, with the base year of 2025 showing robust activity and the forecast period projecting sustained expansion. In the historical period of 2019–2024, the market experienced an average annual growth rate of approximately 7.5%, fueled by a confluence of factors including rising crime rates in certain urban areas, heightened awareness of personal safety, and a growing proactive approach to self-protection by individuals and families. Technological advancements have been a cornerstone of this evolution. The shift from more traditional, potentially lethal options to a wider array of less-lethal and non-lethal devices has been a defining characteristic. Companies like TASER have consistently innovated with their electroshock weapons, enhancing features such as data logging and remote incapacitation capabilities, contributing to an estimated market segment value of over $500 million in 2025. Similarly, advancements in chemical irritant technology by brands like Mace and SABRE have led to more effective and safer formulations, with their combined market share estimated to be around $300 million in 2025. PepperBall, with its less-lethal projectile systems, has also gained traction, particularly in situations requiring area denial or incapacitation from a distance, contributing an estimated $100 million to the market in 2025.

Shifting consumer demands have played a pivotal role in shaping product development and market strategies. There's a discernible trend towards user-friendly, discreet, and highly portable self-defense tools. For women, in particular, demand for compact and easy-to-deploy items like pepper spray, stun guns disguised as everyday objects, and personal safety alarms has surged. This demographic represents a significant consumer segment, with an estimated spending of over $400 million on self-defense products annually. The market for children's safety, while more focused on monitoring and communication devices, also sees a demand for simple, deterrent-focused items like personal alarms, albeit with a much smaller market value estimated at around $50 million. Students, facing concerns related to campus safety, are significant consumers of personal alarms, pepper spray, and less-lethal keychain devices. The "Others" segment, encompassing individuals concerned about home security, travelers, and those in professions requiring personal protection, also contributes substantially to market growth, with an estimated collective spending exceeding $600 million in 2025. AMTEC Less Lethal and Safariland have also expanded their offerings to cater to these diverse needs, focusing on integrated solutions and professional-grade equipment. The adoption metrics for new technologies, such as smart self-defense devices that can alert emergency services, are steadily increasing, projected to reach over 15% adoption by 2028. The overall industry growth rate is expected to remain robust, averaging around 8% annually through the forecast period, driven by continued innovation and a persistent societal emphasis on personal security.

Leading Regions, Countries, or Segments in Civilian Self Defense Weapons

North America, particularly the United States, stands as the dominant region in the civilian self-defense weapons market. This dominance is underpinned by a strong cultural emphasis on individual rights, including the right to self-defense, coupled with a robust regulatory framework that, while varied, generally permits a wide range of personal safety devices. Investment trends within the region are substantial, with significant capital flowing into research and development of less-lethal technologies and a robust consumer base willing to invest in personal security. Regulatory support, while involving strict adherence to specific product classifications and sales channels, has also fostered a mature market for reputable manufacturers like TASER, Mace, and SABRE. The estimated market value for North America in 2025 is projected to exceed $1.5 billion.

Within the broader "Application" segment, "Others" represents the largest consumer group, encompassing individuals of all ages concerned with home security, personal safety during travel, and those in professions that may expose them to risk. This segment's spending is estimated to be over $600 million in 2025. "Women" constitute another substantial segment, with an estimated market value of over $400 million in 2025, driven by specific safety concerns and a preference for compact, easy-to-use devices. "Students," while a smaller segment in terms of absolute spending, exhibit a high adoption rate of specific products like personal alarms and keychain pepper spray, with an estimated market value of around $150 million. "Children," though primarily associated with protective gear and monitoring systems, also represent a niche with some demand for deterrent devices, contributing an estimated $50 million.

In terms of "Types" of civilian self-defense weapons, "Stun Guns" and "Pepper Spray/Pepper Balls" are leading segments, collectively accounting for over 50% of the market in 2025, with estimated values of over $500 million and $400 million respectively. The "Lighting Devices" segment, particularly tactical flashlights with strobe functions and defensive capabilities, is experiencing significant growth, estimated at over $200 million. "Knives," traditionally a prominent category, maintain a steady market presence, estimated at over $150 million, with a focus on concealed and tactical designs. "Others," which includes personal alarms, batons, and emerging technologies, comprises the remaining market share, with batons estimated at over $100 million and emerging technologies showing strong growth potential.

- Dominant Region: North America, with the United States as a key market.

- Leading Application Segment: "Others" (general public safety concerns).

- Key Application Segment Growth: Significant demand from "Women" seeking personal protection.

- Dominant Weapon Type: Stun Guns and Pepper Spray.

- Emerging Weapon Type Growth: Tactical lighting devices with self-defense features.

- Investment Trends: High R&D spending in less-lethal technologies within North America.

- Regulatory Landscape: Favorable but regulated market access for key product types.

Civilian Self Defense Weapons Product Innovations

Product innovation in civilian self-defense weapons is rapidly advancing, focusing on enhanced efficacy, safety, and user-friendliness. Key advancements include the integration of smart technologies, such as GPS tracking and emergency alert systems in devices like TASER's civilian models and specialized alarms from Oxley Group. PepperBall's projectile technology continues to evolve, offering more precise and less-lethal incapacitation options. Piexon's non-toxic jet spray technology represents a significant innovation in pepper spray delivery. Kimber America is exploring innovative designs in defensive tools that blend practicality with concealability. Safariland is focusing on integrated systems that combine various self-defense elements. Lighting devices are increasingly incorporating blinding strobe functions and robust construction for defensive impact.

Propelling Factors for Civilian Self Defense Weapons Growth

The civilian self-defense weapons market is propelled by a confluence of factors. Increasing global concerns regarding personal safety and crime rates are a primary driver, leading individuals to seek effective means of protection. Technological advancements in less-lethal and non-lethal technologies, such as improved stun gun effectiveness and safer, more potent pepper spray formulations from Mace and SABRE, are making these options more attractive and accessible. Regulatory shifts in some regions, recognizing the right to self-defense, are also contributing to market expansion. Economic factors, including a growing disposable income among target demographics, allow for greater investment in personal security devices. Furthermore, a rising awareness and emphasis on personal responsibility for safety, amplified by media coverage and social trends, encourage proactive self-defense measures. The market is also benefiting from the introduction of innovative products by companies like AMTEC Less Lethal, offering diverse solutions for various scenarios.

Obstacles in the Civilian Self Defense Weapons Market

Despite robust growth, the civilian self-defense weapons market faces several obstacles. Stringent and inconsistent regulations across different countries and even within regions can hinder market penetration and product availability, leading to an estimated compliance cost of $XX million annually for manufacturers. The perception of certain self-defense weapons as dangerous or potentially lethal can lead to public apprehension and resistance, impacting adoption rates. Supply chain disruptions, exacerbated by geopolitical events and raw material shortages, can affect production timelines and increase costs, potentially adding millions to manufacturing expenses. Intense competitive pressures from both established brands and emerging players necessitate continuous innovation and aggressive pricing strategies. Furthermore, the ethical debate surrounding the proliferation of any weapon, even non-lethal, can create societal friction.

Future Opportunities in Civilian Self Defense Weapons

Emerging opportunities in the civilian self-defense weapons market are abundant, driven by ongoing technological advancements and evolving consumer needs. The integration of artificial intelligence and biometric security features into self-defense devices presents a significant avenue for growth. The development of discreet, aesthetically pleasing, and multi-functional self-defense tools tailored for specific demographics, such as women and the elderly, offers niche market potential. Expansion into emerging economies with rising disposable incomes and increasing security concerns provides substantial untapped markets. Advancements in non-lethal projectile technology, such as those pioneered by PepperBall and Piexon, offer opportunities for innovation in crowd control and personal defense applications. Furthermore, the growing demand for smart home security systems that integrate personal defense solutions creates a synergistic market for connected devices.

Major Players in the Civilian Self Defense Weapons Ecosystem

- LRAD

- TASER

- Mace

- SABRE

- PepperBall

- AMTEC Less Lethal

- Safariland

- Piexon

- Kimber America

- Oxley Group

- Salt Supply

Key Developments in Civilian Self Defense Weapons Industry

- 2023 January: TASER introduces a new civilian model with enhanced connectivity features and data logging capabilities, aiming for wider adoption.

- 2023 March: Mace Security International launches a new line of compact, high-strength pepper gels designed for discreet carry.

- 2023 July: SABRE enhances its Smart Pepper Spray technology, allowing for optional integration with personal safety apps.

- 2023 October: PepperBall unveils a new generation of less-lethal projectiles with improved accuracy and reduced impact force for civilian use.

- 2024 February: Piexon introduces a non-toxic, water-based irritant spray alternative in select markets.

- 2024 May: Safariland announces strategic partnerships to integrate its self-defense products with emerging smart security platforms.

- 2024 August: Oxley Group showcases advanced LED flashlight designs with integrated defensive capabilities for the civilian market.

- 2025 January: Kimber America hints at innovative concealed carry solutions incorporating self-defense functionalities.

- 2025 March: AMTEC Less Lethal expands its product portfolio with a focus on integrated less-lethal solutions for diverse environments.

Strategic Civilian Self Defense Weapons Market Forecast

The strategic civilian self-defense weapons market is poised for significant growth, driven by a robust demand for enhanced personal security solutions and continuous technological innovation. Key growth catalysts include the increasing adoption of less-lethal technologies, the development of smart and connected self-defense devices, and the expansion into emerging markets. Future opportunities lie in creating user-friendly, discreet, and highly effective products that cater to a diverse range of applications, from women's personal safety to student security. The market potential remains substantial, estimated to reach over $5 billion by 2033, fueled by a proactive approach to personal safety and a strong consumer willingness to invest in reliable self-defense tools.

Civilian Self Defense Weapons Segmentation

-

1. Application

- 1.1. Woman

- 1.2. Children

- 1.3. Students

- 1.4. Others

-

2. Types

- 2.1. Lighting Devices

- 2.2. Knives

- 2.3. Batons

- 2.4. Stun Guns

- 2.5. Others

Civilian Self Defense Weapons Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Civilian Self Defense Weapons Regional Market Share

Geographic Coverage of Civilian Self Defense Weapons

Civilian Self Defense Weapons REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Civilian Self Defense Weapons Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Woman

- 5.1.2. Children

- 5.1.3. Students

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Lighting Devices

- 5.2.2. Knives

- 5.2.3. Batons

- 5.2.4. Stun Guns

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Civilian Self Defense Weapons Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Woman

- 6.1.2. Children

- 6.1.3. Students

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Lighting Devices

- 6.2.2. Knives

- 6.2.3. Batons

- 6.2.4. Stun Guns

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Civilian Self Defense Weapons Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Woman

- 7.1.2. Children

- 7.1.3. Students

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Lighting Devices

- 7.2.2. Knives

- 7.2.3. Batons

- 7.2.4. Stun Guns

- 7.2.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Civilian Self Defense Weapons Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Woman

- 8.1.2. Children

- 8.1.3. Students

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Lighting Devices

- 8.2.2. Knives

- 8.2.3. Batons

- 8.2.4. Stun Guns

- 8.2.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Civilian Self Defense Weapons Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Woman

- 9.1.2. Children

- 9.1.3. Students

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Lighting Devices

- 9.2.2. Knives

- 9.2.3. Batons

- 9.2.4. Stun Guns

- 9.2.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Civilian Self Defense Weapons Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Woman

- 10.1.2. Children

- 10.1.3. Students

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Lighting Devices

- 10.2.2. Knives

- 10.2.3. Batons

- 10.2.4. Stun Guns

- 10.2.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 LRAD

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 TASER

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Mace

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 SABRE

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 PepperBall

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 AMTEC Less Lethal

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Safariland

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Piexon

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Kimber America

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Oxley Group

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Salt Supply

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 LRAD

List of Figures

- Figure 1: Global Civilian Self Defense Weapons Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Civilian Self Defense Weapons Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Civilian Self Defense Weapons Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Civilian Self Defense Weapons Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Civilian Self Defense Weapons Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Civilian Self Defense Weapons Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Civilian Self Defense Weapons Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Civilian Self Defense Weapons Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Civilian Self Defense Weapons Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Civilian Self Defense Weapons Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Civilian Self Defense Weapons Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Civilian Self Defense Weapons Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Civilian Self Defense Weapons Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Civilian Self Defense Weapons Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Civilian Self Defense Weapons Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Civilian Self Defense Weapons Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Civilian Self Defense Weapons Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Civilian Self Defense Weapons Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Civilian Self Defense Weapons Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Civilian Self Defense Weapons Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Civilian Self Defense Weapons Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Civilian Self Defense Weapons Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Civilian Self Defense Weapons Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Civilian Self Defense Weapons Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Civilian Self Defense Weapons Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Civilian Self Defense Weapons Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Civilian Self Defense Weapons Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Civilian Self Defense Weapons Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Civilian Self Defense Weapons Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Civilian Self Defense Weapons Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Civilian Self Defense Weapons Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Civilian Self Defense Weapons Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Civilian Self Defense Weapons Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Civilian Self Defense Weapons Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Civilian Self Defense Weapons Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Civilian Self Defense Weapons Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Civilian Self Defense Weapons Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Civilian Self Defense Weapons Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Civilian Self Defense Weapons Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Civilian Self Defense Weapons Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Civilian Self Defense Weapons Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Civilian Self Defense Weapons Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Civilian Self Defense Weapons Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Civilian Self Defense Weapons Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Civilian Self Defense Weapons Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Civilian Self Defense Weapons Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Civilian Self Defense Weapons Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Civilian Self Defense Weapons Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Civilian Self Defense Weapons Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Civilian Self Defense Weapons Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Civilian Self Defense Weapons Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Civilian Self Defense Weapons Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Civilian Self Defense Weapons Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Civilian Self Defense Weapons Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Civilian Self Defense Weapons Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Civilian Self Defense Weapons Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Civilian Self Defense Weapons Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Civilian Self Defense Weapons Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Civilian Self Defense Weapons Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Civilian Self Defense Weapons Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Civilian Self Defense Weapons Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Civilian Self Defense Weapons Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Civilian Self Defense Weapons Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Civilian Self Defense Weapons Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Civilian Self Defense Weapons Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Civilian Self Defense Weapons Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Civilian Self Defense Weapons Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Civilian Self Defense Weapons Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Civilian Self Defense Weapons Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Civilian Self Defense Weapons Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Civilian Self Defense Weapons Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Civilian Self Defense Weapons Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Civilian Self Defense Weapons Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Civilian Self Defense Weapons Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Civilian Self Defense Weapons Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Civilian Self Defense Weapons Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Civilian Self Defense Weapons Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Civilian Self Defense Weapons?

The projected CAGR is approximately 6.8%.

2. Which companies are prominent players in the Civilian Self Defense Weapons?

Key companies in the market include LRAD, TASER, Mace, SABRE, PepperBall, AMTEC Less Lethal, Safariland, Piexon, Kimber America, Oxley Group, Salt Supply.

3. What are the main segments of the Civilian Self Defense Weapons?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.96 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Civilian Self Defense Weapons," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Civilian Self Defense Weapons report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Civilian Self Defense Weapons?

To stay informed about further developments, trends, and reports in the Civilian Self Defense Weapons, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence