Key Insights

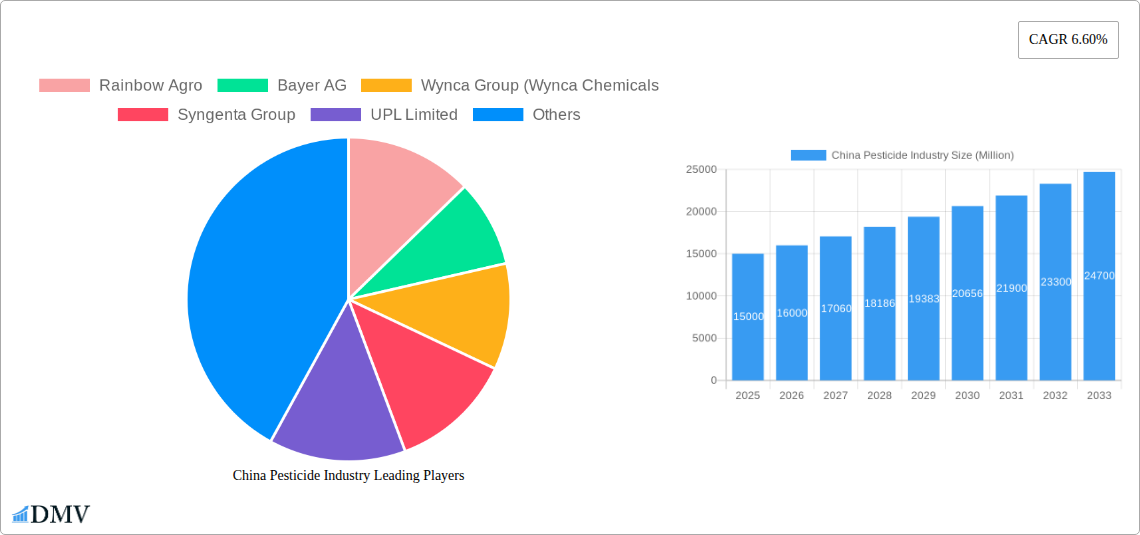

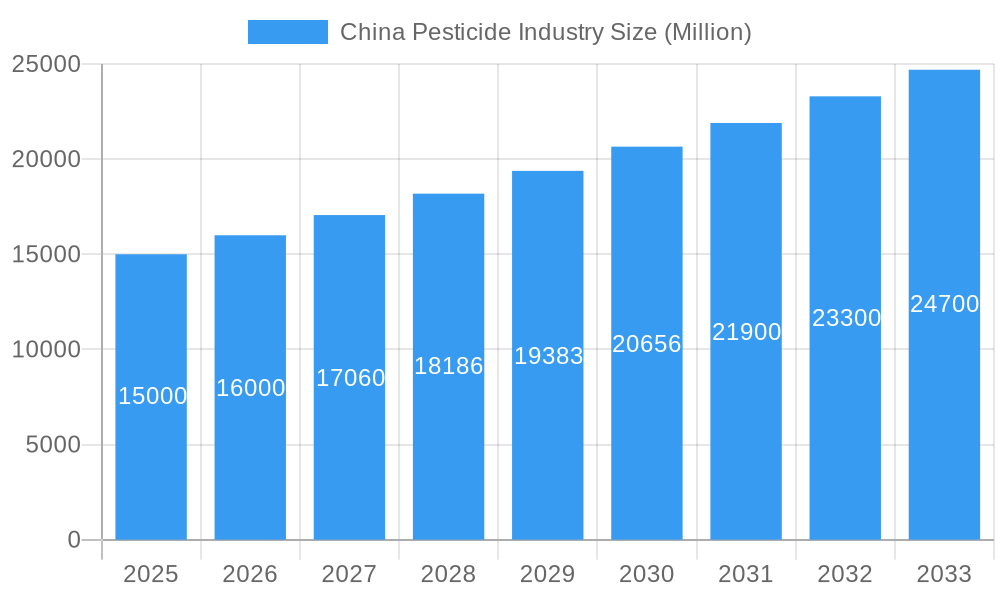

The China pesticide market is projected for significant expansion, estimated at $43.5 billion in 2025. The market is expected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% from 2025 to 2033. This growth is primarily driven by the imperative for food security in a large and developing nation, requiring enhanced crop yields and, consequently, increased pesticide utilization. The persistent presence of crop pests and diseases also fuels demand for effective pest control solutions across various pesticide categories. Furthermore, technological advancements, particularly in the development of targeted and environmentally conscious pesticide formulations, are accelerating market adoption. Key growth segments include insecticides and fungicides, vital for comprehensive crop protection. While foliar spraying and seed treatment remain dominant application methods, chemigation and soil treatment are gaining traction due to their enhanced efficiency and reduced environmental impact. Leading global players such as Bayer AG, Syngenta Group, and UPL Limited, alongside prominent domestic companies including Rainbow Agro and Jiangsu Yangnong Chemical Co Ltd, are key contributors to the market's competitive landscape. However, stringent regulatory frameworks and increasing environmental concerns pose challenges, necessitating a focus on sustainable and bio-pesticide alternatives to balance agricultural productivity with ecological preservation.

China Pesticide Industry Market Size (In Billion)

Market segmentation indicates substantial opportunities across diverse crop types, with fruits & vegetables, grains & cereals, and commercial crops representing significant segments, reflecting China's high agricultural output. Urbanization and the expansion of the landscaping sector are also boosting demand in the turf & ornamental segment. While the overall market exhibits strong growth potential, regional variations are anticipated within China, influenced by specific climatic conditions, crop patterns, and pest prevalence. The future trajectory of the Chinese pesticide market will be shaped by the ongoing need to balance agricultural productivity with a growing emphasis on sustainable and environmentally responsible practices. Continuous innovation, rigorous regulatory compliance, and a commitment to responsible pesticide application will be crucial for navigating the market's evolution in the coming years.

China Pesticide Industry Company Market Share

China Pesticide Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the China pesticide industry, offering invaluable insights for stakeholders seeking to navigate this dynamic market. The study covers the period 2019-2033, with a base year of 2025 and a forecast period of 2025-2033. The report utilizes data from the historical period (2019-2024) to project future market trends and opportunities, revealing a market valued at xx Million in 2025 and projected to reach xx Million by 2033. This report will equip you with the knowledge to make informed decisions in this crucial sector.

China Pesticide Industry Market Composition & Trends

This section delves into the intricate composition of the China pesticide market, examining market concentration, innovation drivers, regulatory frameworks, substitute product impacts, end-user behavior, and significant M&A activity. The analysis reveals a market characterized by both established players and emerging innovators.

Market Concentration: The market exhibits a moderately concentrated structure, with a few dominant players holding significant market share. Rainbow Agro, Bayer AG, and Syngenta Group are among the leading companies, collectively accounting for an estimated xx% of the market in 2025. Smaller players contribute to the remaining share.

Innovation Catalysts: Government support for sustainable agriculture and the rising demand for high-efficiency pesticides are stimulating significant product innovation. The development of biopesticides and targeted delivery systems are major trends.

Regulatory Landscape: Stringent environmental regulations and increasing scrutiny of pesticide usage are shaping industry practices and driving the adoption of more eco-friendly solutions. Compliance costs present a notable challenge for smaller players.

Substitute Products: The rise of integrated pest management (IPM) techniques and biological control agents poses a competitive challenge, but also creates opportunities for companies to develop integrated solutions.

End-User Profiles: The report profiles key end-users, including large-scale commercial farms, smallholder farmers, and government agencies, highlighting their unique needs and preferences.

M&A Activity: Significant M&A activity has shaped the market landscape. Recent deals, such as the Bayer-UPL partnership (May 2022), valued at an estimated xx Million, highlight the strategic importance of collaborations and acquisitions to expand market share and product portfolios. The average M&A deal value in the period 2019-2024 was approximately xx Million.

China Pesticide Industry Industry Evolution

This section analyzes the evolutionary trajectory of the China pesticide industry, charting market growth, technological advancements, and evolving consumer preferences. The market witnessed a Compound Annual Growth Rate (CAGR) of xx% during the 2019-2024 historical period. The forecast period (2025-2033) projects a CAGR of xx%, driven by several key factors. Technological advancements, particularly in precision agriculture and the development of next-generation pesticides, are playing a significant role in shaping market growth. The increasing adoption of technology in agriculture, coupled with the rising demand for higher crop yields and sustainable farming practices, is transforming the industry. Consumer demand is increasingly focusing on environmentally benign solutions, prompting manufacturers to prioritize biopesticides and integrated pest management systems. This shift necessitates substantial investments in research and development to meet these evolving demands. The industry has witnessed considerable innovation in formulation technologies, aiming for more efficient and targeted delivery of active ingredients. The development and registration of newer, more effective and selective active ingredients are also driving growth. The adoption of these technological advancements will play a crucial role in shaping the future trajectory of the market.

Leading Regions, Countries, or Segments in China Pesticide Industry

This section identifies the dominant regions, countries, and segments within the China pesticide market. The analysis focuses on key drivers, including investment trends and regulatory support, to explain the factors contributing to dominance.

Dominant Segments:

Function: Insecticides represent the largest segment, followed by herbicides and fungicides. The high prevalence of insect pests and weeds in major agricultural areas drives this dominance.

Application Mode: Foliar application remains the dominant method, followed by seed treatment and soil treatment. The ease and widespread adoption of foliar application contribute to its leading position.

Crop Type: Grains & Cereals and Fruits & Vegetables are the primary target crops, driven by their substantial acreage and economic importance.

Key Drivers of Segment Dominance:

- High demand: The significant acreage of these crops in China fuels the demand for corresponding pesticide types.

- Government support: Policies encouraging increased agricultural production and crop protection indirectly boost usage.

- Investment: Significant investments in research and development contribute to improving efficacy and expanding the market.

China Pesticide Industry Product Innovations

Recent innovations include the development of more targeted pesticides with reduced environmental impact. These incorporate advanced formulations that enhance efficacy, minimize off-target effects, and reduce the risk of pesticide resistance. Companies are investing heavily in biopesticides and other environmentally sustainable solutions to meet the growing demand for eco-friendly crop protection products. Performance metrics are steadily improving, with increased efficacy and reduced application rates becoming increasingly significant selling points.

Propelling Factors for China Pesticide Industry Growth

Several factors propel the growth of the China pesticide industry. Firstly, the increasing demand for food security necessitates higher crop yields, driving the need for effective pest and weed control solutions. Secondly, the government's support for agricultural modernization and sustainable agriculture initiatives fosters innovation and market expansion. Thirdly, technological advancements, such as the development of precision agriculture technologies, enable more efficient and targeted pesticide applications, minimizing environmental impact and maximizing returns for farmers.

Obstacles in the China Pesticide Industry Market

Despite the growth potential, several obstacles hinder market expansion. Stringent environmental regulations and safety standards create compliance challenges, increasing costs and restricting product availability. Supply chain disruptions, particularly with raw material sourcing, present intermittent challenges. Intense competition from both domestic and international players necessitates ongoing innovation and cost optimization.

Future Opportunities in China Pesticide Industry

Future opportunities lie in the growing adoption of sustainable agriculture practices, including integrated pest management (IPM) strategies. The rising demand for biopesticides and other eco-friendly solutions presents significant growth potential. Further expansion into emerging markets and the exploration of new crop protection technologies are crucial for sustained industry growth.

Major Players in the China Pesticide Industry Ecosystem

- Rainbow Agro

- Bayer AG

- Wynca Group (Wynca Chemicals)

- Syngenta Group

- UPL Limited

- Lianyungang Liben Crop Technology Co Ltd

- BASF SE

- FMC Corporation

- Jiangsu Yangnong Chemical Co Ltd

- Corteva Agriscience

Key Developments in China Pesticide Industry Industry

- May 2022: UPL partnered with Bayer for Spirotetramat insecticide, focusing on resistance management and difficult-to-control pests.

- August 2022: BASF and Corteva Agriscience collaborated on soybean weed control solutions.

- January 2023: Bayer partnered with Oerth Bio for eco-friendly crop protection technologies.

Strategic China Pesticide Industry Market Forecast

The China pesticide market is poised for sustained growth, driven by increasing agricultural demands, technological advancements, and government support for sustainable practices. Opportunities abound in biopesticides, precision agriculture, and integrated pest management. Continued innovation and strategic partnerships will be crucial for players to capitalize on this dynamic market's potential.

China Pesticide Industry Segmentation

- 1. Production Analysis

- 2. Consumption Analysis

- 3. Import Market Analysis (Value & Volume)

- 4. Export Market Analysis (Value & Volume)

- 5. Price Trend Analysis

China Pesticide Industry Segmentation By Geography

- 1. China

China Pesticide Industry Regional Market Share

Geographic Coverage of China Pesticide Industry

China Pesticide Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Production Analysis

- 5.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 5.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 5.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 5.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. China

- 6. China Pesticide Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Production Analysis

- 6.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 6.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 6.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 6.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Rainbow Agro

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Bayer AG

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Wynca Group (Wynca Chemicals

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Syngenta Group

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 UPL Limited

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Lianyungang Liben Crop Technology Co Ltd

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 BASF SE

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 FMC Corporation

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Jiangsu Yangnong Chemical Co Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Corteva Agriscience

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Rainbow Agro

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Pesticide Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: China Pesticide Industry Share (%) by Company 2025

List of Tables

- Table 1: China Pesticide Industry Revenue billion Forecast, by Production Analysis 2020 & 2033

- Table 2: China Pesticide Industry Revenue billion Forecast, by Consumption Analysis 2020 & 2033

- Table 3: China Pesticide Industry Revenue billion Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 4: China Pesticide Industry Revenue billion Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 5: China Pesticide Industry Revenue billion Forecast, by Price Trend Analysis 2020 & 2033

- Table 6: China Pesticide Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 7: China Pesticide Industry Revenue billion Forecast, by Production Analysis 2020 & 2033

- Table 8: China Pesticide Industry Revenue billion Forecast, by Consumption Analysis 2020 & 2033

- Table 9: China Pesticide Industry Revenue billion Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 10: China Pesticide Industry Revenue billion Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 11: China Pesticide Industry Revenue billion Forecast, by Price Trend Analysis 2020 & 2033

- Table 12: China Pesticide Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Pesticide Industry?

The projected CAGR is approximately 6.5%.

2. Which companies are prominent players in the China Pesticide Industry?

Key companies in the market include Rainbow Agro, Bayer AG, Wynca Group (Wynca Chemicals, Syngenta Group, UPL Limited, Lianyungang Liben Crop Technology Co Ltd, BASF SE, FMC Corporation, Jiangsu Yangnong Chemical Co Ltd, Corteva Agriscience.

3. What are the main segments of the China Pesticide Industry?

The market segments include Production Analysis, Consumption Analysis, Import Market Analysis (Value & Volume), Export Market Analysis (Value & Volume), Price Trend Analysis.

4. Can you provide details about the market size?

The market size is estimated to be USD 43.5 billion as of 2022.

5. What are some drivers contributing to market growth?

Demand For Landscaping Maintenance; Adoption of Green Spaces and Green Roofs.

6. What are the notable trends driving market growth?

Herbicides dominate the market.

7. Are there any restraints impacting market growth?

Shortage of Labor In Landscaping; High Maintenance Cost of Lawn Mowers.

8. Can you provide examples of recent developments in the market?

January 2023: Bayer formed a new partnership with Oerth Bio to enhance crop protection technology and create more eco-friendly crop protection solutions.August 2022: BASF and Corteva Agriscience collaborated to provide soybean farmers with the weed control of the future. By working together, BASF and Corteva aim to satisfy farmers' demand for specialized weed control solutions that are distinct from those that are currently available or being developed.May 2022: UPL partnered with Bayer for Spirotetramat insecticide to develop new pest management solutions. Through this long-term global data access and supply agreement with Bayer, specifically for addressing farmer demands regarding resistance management and difficult-to-control sucking pests, UPL will develop, register, and distribute new unique solutions, including Spirotetramat, using its experience in insecticides and worldwide research and development network.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Pesticide Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Pesticide Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Pesticide Industry?

To stay informed about further developments, trends, and reports in the China Pesticide Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence