Key Insights

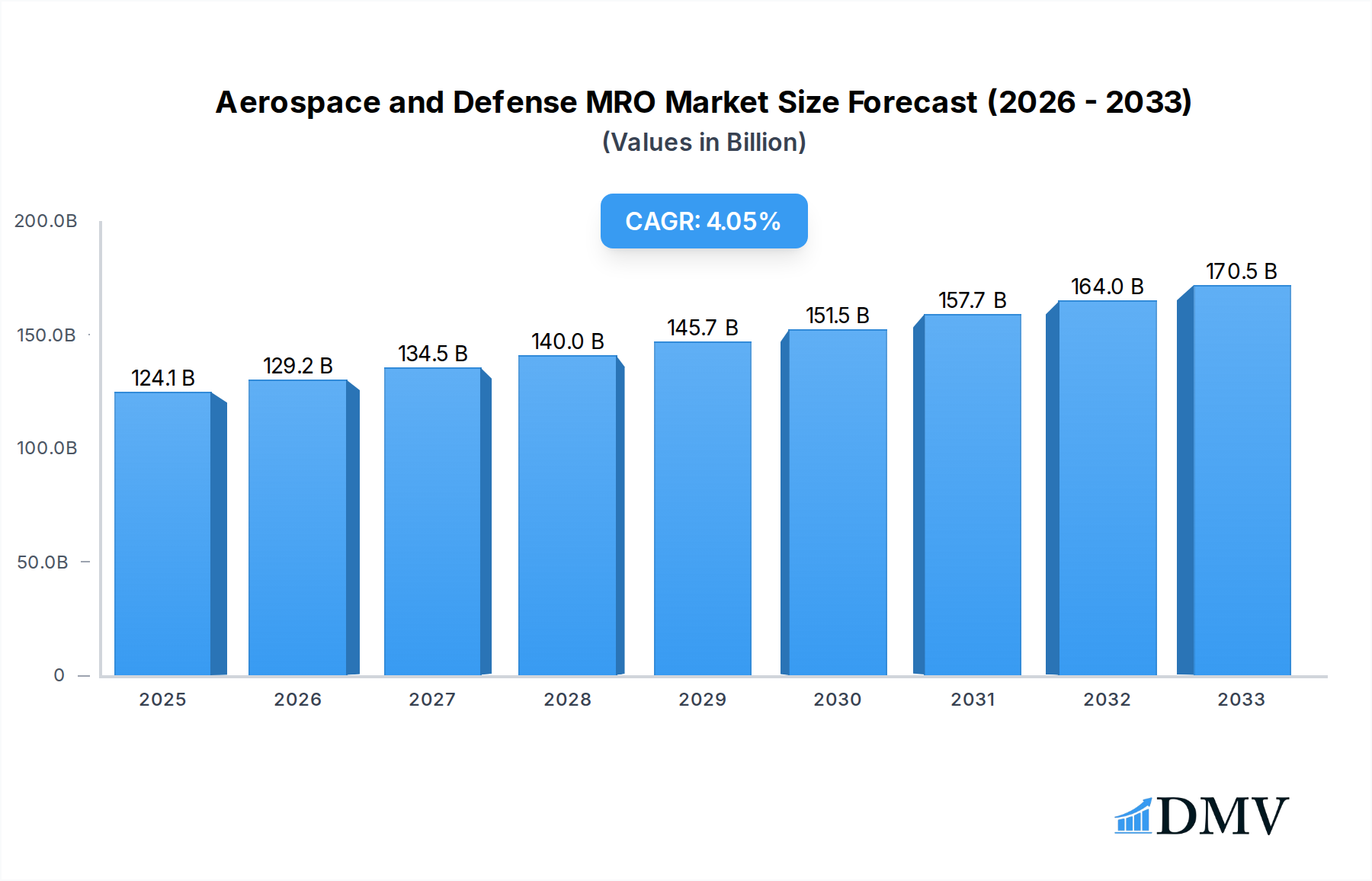

The global Aerospace and Defense (A&D) Maintenance, Repair, and Overhaul (MRO) market is poised for significant expansion, projected to reach an estimated $124,100 million by 2025, with a robust Compound Annual Growth Rate (CAGR) of 4.2% through 2033. This growth is underpinned by several critical drivers, most notably the increasing global demand for air travel, which is fueling fleet expansion and consequently driving the need for regular maintenance and component servicing. The continued aging of commercial aircraft fleets worldwide necessitates extensive MRO activities, as older planes require more frequent and complex repairs to ensure airworthiness and operational efficiency. Furthermore, advancements in aviation technology, including the introduction of new aircraft models with sophisticated systems, are creating specialized MRO opportunities, demanding highly skilled technicians and advanced diagnostic tools. The emphasis on fleet modernization and the integration of next-generation aircraft also contribute to market dynamics, requiring tailored MRO solutions for these advanced platforms.

Aerospace and Defense MRO Market Size (In Billion)

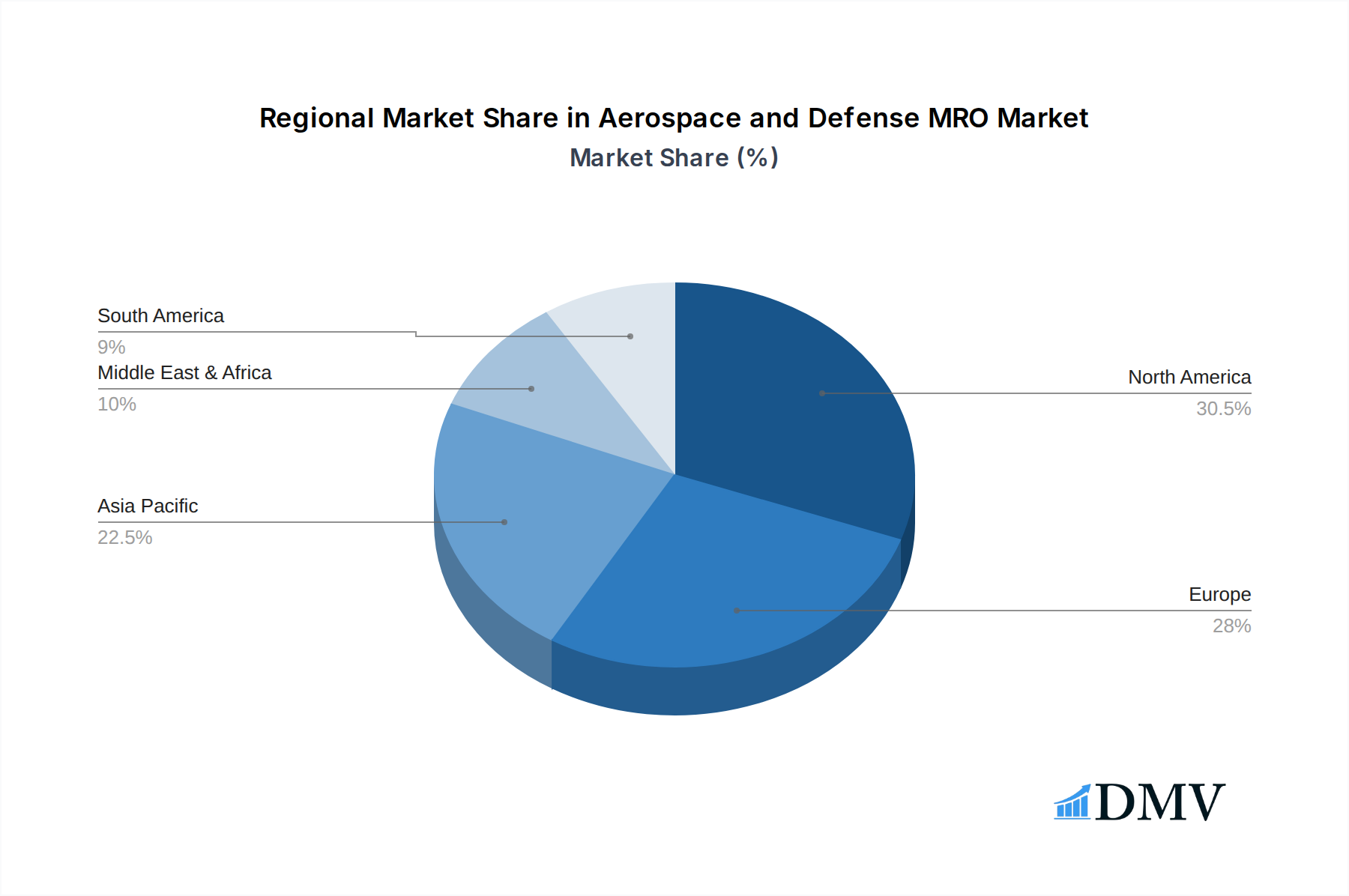

The A&D MRO market is characterized by diverse segments, with the Engine segment holding a dominant position due to its high cost and complexity, followed by Components, Airframe, and Line maintenance. Geographically, North America and Europe currently lead the market, driven by well-established aviation infrastructures and a high density of commercial and military fleets. However, the Asia Pacific region is emerging as a key growth engine, propelled by a rapidly expanding aviation sector, increasing airline investments, and the growth of low-cost carriers. Emerging economies in the Middle East and Africa are also demonstrating substantial growth potential. Despite these positive trends, the market faces certain restraints, including a shortage of skilled MRO technicians and escalating labor costs, which can impact operational efficiency and profitability. Additionally, the high capital investment required for state-of-the-art MRO facilities and technologies can act as a barrier to entry for smaller players.

Aerospace and Defense MRO Company Market Share

This comprehensive market research report delves deep into the global Aerospace and Defense MRO (Maintenance, Repair, and Overhaul) sector, providing a critical analysis of its current landscape and future trajectory. Covering a study period from 2019 to 2033, with a base and estimated year of 2025, this report offers invaluable insights for stakeholders, investors, and industry professionals. The forecast period extends from 2025 to 2033, building upon the historical data from 2019 to 2024.

Aerospace and Defense MRO Market Composition & Trends

The Aerospace and Defense MRO market is characterized by a dynamic interplay of established giants and emerging players, with significant market share distribution concentrated among key companies. Innovation is a potent catalyst, driven by the relentless pursuit of efficiency, safety, and advanced technologies in aircraft and defense systems maintenance. Regulatory landscapes, including stringent FAA, EASA, and defense-specific mandates, significantly shape operational protocols and investment decisions. Substitute products, such as advanced repair techniques and component remanufacturing, are increasingly influencing traditional overhaul services. End-user profiles range from major airlines and cargo carriers to defense forces and private aviation operators, each with distinct MRO requirements. Mergers and acquisitions (M&A) are a recurring theme, with recent deal values in the multi-million dollar range, consolidating market power and expanding service portfolios. For instance, the total M&A deal value in the sector is estimated to be in the hundreds of millions. The market exhibits a moderate concentration, with the top 5 companies holding approximately 60% of the global market share. Key M&A activities have included acquisitions focused on expanding engine MRO capabilities and digital maintenance solutions.

- Market Share Distribution: Top 5 companies hold an estimated 60% of the market.

- Innovation Catalysts: Digitalization, predictive maintenance, sustainable MRO solutions.

- Regulatory Landscapes: EASA, FAA, ITAR, and national defense regulations.

- Substitute Products: Advanced composite repair, 3D printed parts, component life extension programs.

- End-User Profiles: Commercial airlines (Narrow Body Aircraft, Wide Body Aircraft, Regional Aircraft), defense organizations, MRO service providers.

- M&A Deal Values: Multi-million dollar transactions, focused on strategic acquisitions and capacity expansion.

Aerospace and Defense MRO Industry Evolution

The Aerospace and Defense MRO industry has witnessed a remarkable evolution, marked by consistent market growth trajectories fueled by an expanding global aviation fleet and increasing defense spending. Technological advancements have been pivotal, with the adoption of AI-powered predictive maintenance, augmented reality for technician training, and sophisticated diagnostic tools revolutionizing repair processes. This evolution has also been shaped by shifting consumer demands, primarily driven by airlines’ focus on cost optimization, reduced downtime, and enhanced aircraft availability. The industry is moving towards more specialized and integrated MRO solutions. For example, the adoption rate of digital twin technology in MRO is projected to reach over 70% by 2030. The overall market growth rate for Aerospace and Defense MRO is projected to be around 4.5% annually during the forecast period. The shift from reactive to proactive maintenance strategies is a defining trend. Furthermore, the increasing complexity of modern aircraft, featuring advanced avionics and composite materials, necessitates continuous investment in specialized MRO capabilities. The industry is also responding to the growing imperative for sustainable MRO practices, including environmentally friendly cleaning agents and waste reduction initiatives. The global Aerospace MRO market size is estimated to be in the tens of billions of dollars, with steady growth anticipated.

Leading Regions, Countries, or Segments in Aerospace and Defense MRO

The Aerospace and Defense MRO market is significantly influenced by regional dynamics and the dominance of specific application and type segments. North America currently leads the global market, driven by a robust commercial aviation sector, a substantial defense budget, and a well-established MRO infrastructure. The United States, in particular, stands out as a dominant country due to the presence of major airlines, leading MRO providers like AAR Corp. and Delta TechOps, and significant defense contracts. Within application segments, Narrow Body Aircraft MRO commands a substantial share due to the high volume of these aircraft in global fleets and their frequent utilization, leading to consistent maintenance needs. Simultaneously, Wide Body Aircraft MRO is a high-value segment, often involving complex overhauls and component repairs.

In terms of MRO types, Engine MRO represents the largest and most critical segment, given the high cost and complexity of engine maintenance, with companies like GE Aviation, Rolls-Royce, and MTU Maintenance being key players. Components MRO is also a significant area, encompassing a wide array of systems and parts. The Airframe segment continues to be essential for structural integrity and longevity. Line maintenance, crucial for day-to-day operational readiness, also contributes significantly to the overall MRO market. Investment trends in these segments are robust, supported by a growing global passenger and cargo demand. Regulatory support, particularly concerning safety and airworthiness standards, underpins the consistent demand for these MRO services. The increasing fleet size of narrow-body aircraft, projected to grow by over 20% in the next decade, further solidifies its leading position.

- Dominant Region: North America, with the United States as a key country.

- Leading Application Segment: Narrow Body Aircraft MRO, driven by fleet size and utilization.

- High-Value Application Segment: Wide Body Aircraft MRO, requiring complex overhauls.

- Dominant MRO Type: Engine MRO, due to cost and complexity.

- Key Drivers for Dominance:

- Investment Trends: Significant capital deployment in engine overhaul facilities and component repair capabilities.

- Regulatory Support: Stringent safety and airworthiness standards driving demand for compliant MRO services.

- Fleet Size and Utilization: High operational tempo of narrow-body aircraft necessitates frequent maintenance.

- Technological Advancements: Investment in advanced diagnostic and repair technologies.

- Defense Spending: Continued government investment in military aircraft MRO.

Aerospace and Defense MRO Product Innovations

The Aerospace and Defense MRO market is experiencing a surge in product innovations aimed at enhancing efficiency, reducing turnaround times, and improving sustainability. Key advancements include the development of advanced composite repair kits, enabling quicker and more cost-effective structural repairs on modern aircraft. Predictive maintenance software, powered by machine learning and AI, is revolutionizing diagnostics, allowing for proactive identification of potential issues and minimizing unscheduled downtime. Furthermore, the emergence of digital twin technology provides virtual replicas of aircraft components, facilitating remote monitoring and troubleshooting. Additive manufacturing (3D printing) is also gaining traction for producing specialized MRO parts, offering faster lead times and customized solutions. These innovations contribute to significant performance improvements, such as an estimated 15% reduction in maintenance turn-around times and a 10% decrease in unscheduled maintenance events.

Propelling Factors for Aerospace and Defense MRO Growth

Several key factors are propelling the growth of the Aerospace and Defense MRO market. The ever-increasing global fleet size, particularly of commercial aircraft, directly translates to higher demand for maintenance services. Robust defense spending worldwide, driven by geopolitical dynamics and the need for advanced military capabilities, also fuels substantial MRO requirements for defense platforms. Technological advancements, such as AI-driven predictive maintenance and digital twins, are enhancing efficiency and creating new service opportunities. Furthermore, evolving regulatory requirements, emphasizing stringent safety and airworthiness standards, necessitate continuous investment in MRO expertise and infrastructure. The growing demand for sustainable MRO solutions also presents a significant growth avenue, encouraging the development of eco-friendly repair processes and materials.

- Increasing Global Fleet Size: Expansion of commercial and cargo aircraft fleets.

- Rising Defense Spending: Governments investing in military readiness and modernization.

- Technological Advancements: AI, IoT, AR/VR driving efficiency and new service models.

- Stringent Regulatory Frameworks: Emphasis on safety and airworthiness driving compliance-based MRO.

- Demand for Sustainable MRO: Growing focus on environmental impact and eco-friendly practices.

Obstacles in the Aerospace and Defense MRO Market

Despite robust growth, the Aerospace and Defense MRO market faces several significant obstacles. Stringent and evolving regulatory landscapes, particularly in aviation safety, can lead to increased compliance costs and longer approval cycles for new repair processes. Supply chain disruptions, exacerbated by global events and geopolitical tensions, can impact the availability of critical spare parts and raw materials, leading to production delays and increased costs. Intense competitive pressures among MRO providers, especially for lucrative engine and component overhaul contracts, can lead to price erosion. The shortage of skilled aviation technicians and engineers, a persistent global challenge, also poses a significant restraint on market expansion. Furthermore, the high capital investment required for advanced MRO facilities and technologies can be a barrier for smaller players. The cost of compliance with new environmental regulations is also a growing concern.

Future Opportunities in Aerospace and Defense MRO

The Aerospace and Defense MRO market is ripe with future opportunities, driven by emerging trends and technological breakthroughs. The growing demand for sustainable aviation fuels (SAFs) and the push for environmentally friendly MRO practices present a significant growth area. The increasing integration of digitalization and Industry 4.0 principles into MRO operations, including advanced data analytics and blockchain for supply chain transparency, offers avenues for innovation and efficiency gains. The expansion of air cargo operations globally creates sustained demand for freighter aircraft MRO. The development of new aircraft technologies, such as electric and hybrid-electric propulsion systems, will necessitate the development of specialized MRO capabilities and expertise, opening up new market segments. Furthermore, the growing defense sector in emerging economies presents untapped markets for MRO services.

Major Players in the Aerospace and Defense MRO Ecosystem

- GE Aviation

- Airbus

- Lufthansa Technik

- AFI KLM E&M

- MTU Maintenance

- Rolls-Royce

- AAR Corp.

- ST Aerospace

- SR Technics (Mubadala Aerospace)

- SIA Engineering

- Delta TechOps

- Haeco

- JAL Engineering

- Ameco Beijing

- Pratt & Whitney

- ANA

- Korean Air

- Iberia Maintenance

Key Developments in Aerospace and Defense MRO Industry

- 2023/September: GE Aviation and RTX (formerly Raytheon Technologies) announce plans for a joint venture combining their engine businesses, creating a powerhouse in engine MRO.

- 2023/July: Lufthansa Technik launches a new digital platform for component MRO, enhancing efficiency and transparency.

- 2023/April: Rolls-Royce invests in new sustainable MRO technologies to reduce environmental impact.

- 2022/December: AAR Corp. secures a multi-year component support agreement with a major cargo airline, highlighting the growing cargo MRO demand.

- 2022/October: AFI KLM E&M expands its narrow-body aircraft MRO capabilities with a new facility.

- 2022/June: ST Aerospace announces advancements in its composite repair capabilities, addressing the growing need for advanced material maintenance.

- 2021/November: Pratt & Whitney partners with an emerging market airline to provide comprehensive engine MRO services.

- 2021/May: SIA Engineering inaugurates a new dedicated facility for wide-body aircraft component MRO.

- 2020/March: MTU Maintenance announces significant expansion of its overhaul capacity for next-generation aircraft engines.

- 2020/January: Haeco invests in new technologies for airframe maintenance, focusing on digitalization and automation.

Strategic Aerospace and Defense MRO Market Forecast

The strategic forecast for the Aerospace and Defense MRO market is exceptionally positive, driven by sustained growth in the global aviation fleet, increasing defense expenditures, and rapid technological innovation. Future opportunities lie in the expansion of sustainable MRO solutions, the adoption of advanced digital tools for predictive maintenance, and the development of specialized services for new aircraft technologies. The market is poised for significant expansion, with projected growth rates expected to exceed 4.5% annually over the forecast period. Investment in next-generation MRO capabilities, particularly in engine and component services, will be crucial for capturing market share. The market potential is immense, estimated to reach several tens of billions of dollars by the end of the forecast period, presenting substantial opportunities for stakeholders who can adapt to evolving industry demands and technological advancements.

Aerospace and Defense MRO Segmentation

-

1. Application

- 1.1. Narrow Body Aircraft

- 1.2. Wide Body Aircraft

- 1.3. Regional Aircraft

- 1.4. Others

-

2. Types

- 2.1. Engine

- 2.2. Components

- 2.3. Airframe

- 2.4. Line

Aerospace and Defense MRO Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Aerospace and Defense MRO Regional Market Share

Geographic Coverage of Aerospace and Defense MRO

Aerospace and Defense MRO REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Narrow Body Aircraft

- 5.1.2. Wide Body Aircraft

- 5.1.3. Regional Aircraft

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Engine

- 5.2.2. Components

- 5.2.3. Airframe

- 5.2.4. Line

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Aerospace and Defense MRO Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Narrow Body Aircraft

- 6.1.2. Wide Body Aircraft

- 6.1.3. Regional Aircraft

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Engine

- 6.2.2. Components

- 6.2.3. Airframe

- 6.2.4. Line

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Aerospace and Defense MRO Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Narrow Body Aircraft

- 7.1.2. Wide Body Aircraft

- 7.1.3. Regional Aircraft

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Engine

- 7.2.2. Components

- 7.2.3. Airframe

- 7.2.4. Line

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Aerospace and Defense MRO Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Narrow Body Aircraft

- 8.1.2. Wide Body Aircraft

- 8.1.3. Regional Aircraft

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Engine

- 8.2.2. Components

- 8.2.3. Airframe

- 8.2.4. Line

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Aerospace and Defense MRO Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Narrow Body Aircraft

- 9.1.2. Wide Body Aircraft

- 9.1.3. Regional Aircraft

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Engine

- 9.2.2. Components

- 9.2.3. Airframe

- 9.2.4. Line

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Aerospace and Defense MRO Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Narrow Body Aircraft

- 10.1.2. Wide Body Aircraft

- 10.1.3. Regional Aircraft

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Engine

- 10.2.2. Components

- 10.2.3. Airframe

- 10.2.4. Line

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Aerospace and Defense MRO Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Narrow Body Aircraft

- 11.1.2. Wide Body Aircraft

- 11.1.3. Regional Aircraft

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Engine

- 11.2.2. Components

- 11.2.3. Airframe

- 11.2.4. Line

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 GE Aviation

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Airbus

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Lufthansa Technik

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 AFI KLM E&M

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 MTU Maintenance

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Rolls-Royce

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 AAR Corp.

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 ST Aerospace

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 SR Technics (Mubadala Aerospace)

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 SIA Engineering

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Delta TechOps

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Haeco

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 JAL Engineering

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Ameco Beijing

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Pratt & Whitney

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 ANA

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Korean Air

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 Iberia Maintenance

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.1 GE Aviation

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Aerospace and Defense MRO Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Aerospace and Defense MRO Revenue (million), by Application 2025 & 2033

- Figure 3: North America Aerospace and Defense MRO Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Aerospace and Defense MRO Revenue (million), by Types 2025 & 2033

- Figure 5: North America Aerospace and Defense MRO Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Aerospace and Defense MRO Revenue (million), by Country 2025 & 2033

- Figure 7: North America Aerospace and Defense MRO Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Aerospace and Defense MRO Revenue (million), by Application 2025 & 2033

- Figure 9: South America Aerospace and Defense MRO Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Aerospace and Defense MRO Revenue (million), by Types 2025 & 2033

- Figure 11: South America Aerospace and Defense MRO Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Aerospace and Defense MRO Revenue (million), by Country 2025 & 2033

- Figure 13: South America Aerospace and Defense MRO Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Aerospace and Defense MRO Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Aerospace and Defense MRO Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Aerospace and Defense MRO Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Aerospace and Defense MRO Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Aerospace and Defense MRO Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Aerospace and Defense MRO Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Aerospace and Defense MRO Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Aerospace and Defense MRO Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Aerospace and Defense MRO Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Aerospace and Defense MRO Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Aerospace and Defense MRO Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Aerospace and Defense MRO Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Aerospace and Defense MRO Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Aerospace and Defense MRO Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Aerospace and Defense MRO Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Aerospace and Defense MRO Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Aerospace and Defense MRO Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Aerospace and Defense MRO Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Aerospace and Defense MRO Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Aerospace and Defense MRO Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Aerospace and Defense MRO Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Aerospace and Defense MRO Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Aerospace and Defense MRO Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Aerospace and Defense MRO Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Aerospace and Defense MRO Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Aerospace and Defense MRO Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Aerospace and Defense MRO Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Aerospace and Defense MRO Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Aerospace and Defense MRO Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Aerospace and Defense MRO Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Aerospace and Defense MRO Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Aerospace and Defense MRO Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Aerospace and Defense MRO Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Aerospace and Defense MRO Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Aerospace and Defense MRO Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Aerospace and Defense MRO Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Aerospace and Defense MRO Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Aerospace and Defense MRO Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Aerospace and Defense MRO Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Aerospace and Defense MRO Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Aerospace and Defense MRO Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Aerospace and Defense MRO Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Aerospace and Defense MRO Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Aerospace and Defense MRO Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Aerospace and Defense MRO Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Aerospace and Defense MRO Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Aerospace and Defense MRO Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Aerospace and Defense MRO Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Aerospace and Defense MRO Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Aerospace and Defense MRO Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Aerospace and Defense MRO Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Aerospace and Defense MRO Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Aerospace and Defense MRO Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Aerospace and Defense MRO Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Aerospace and Defense MRO Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Aerospace and Defense MRO Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Aerospace and Defense MRO Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Aerospace and Defense MRO Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Aerospace and Defense MRO Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Aerospace and Defense MRO Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Aerospace and Defense MRO Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Aerospace and Defense MRO Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Aerospace and Defense MRO Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Aerospace and Defense MRO Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Aerospace and Defense MRO?

The projected CAGR is approximately 4.2%.

2. Which companies are prominent players in the Aerospace and Defense MRO?

Key companies in the market include GE Aviation, Airbus, Lufthansa Technik, AFI KLM E&M, MTU Maintenance, Rolls-Royce, AAR Corp., ST Aerospace, SR Technics (Mubadala Aerospace), SIA Engineering, Delta TechOps, Haeco, JAL Engineering, Ameco Beijing, Pratt & Whitney, ANA, Korean Air, Iberia Maintenance.

3. What are the main segments of the Aerospace and Defense MRO?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 124100 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5600.00, USD 8400.00, and USD 11200.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Aerospace and Defense MRO," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Aerospace and Defense MRO report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Aerospace and Defense MRO?

To stay informed about further developments, trends, and reports in the Aerospace and Defense MRO, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence