Key Insights

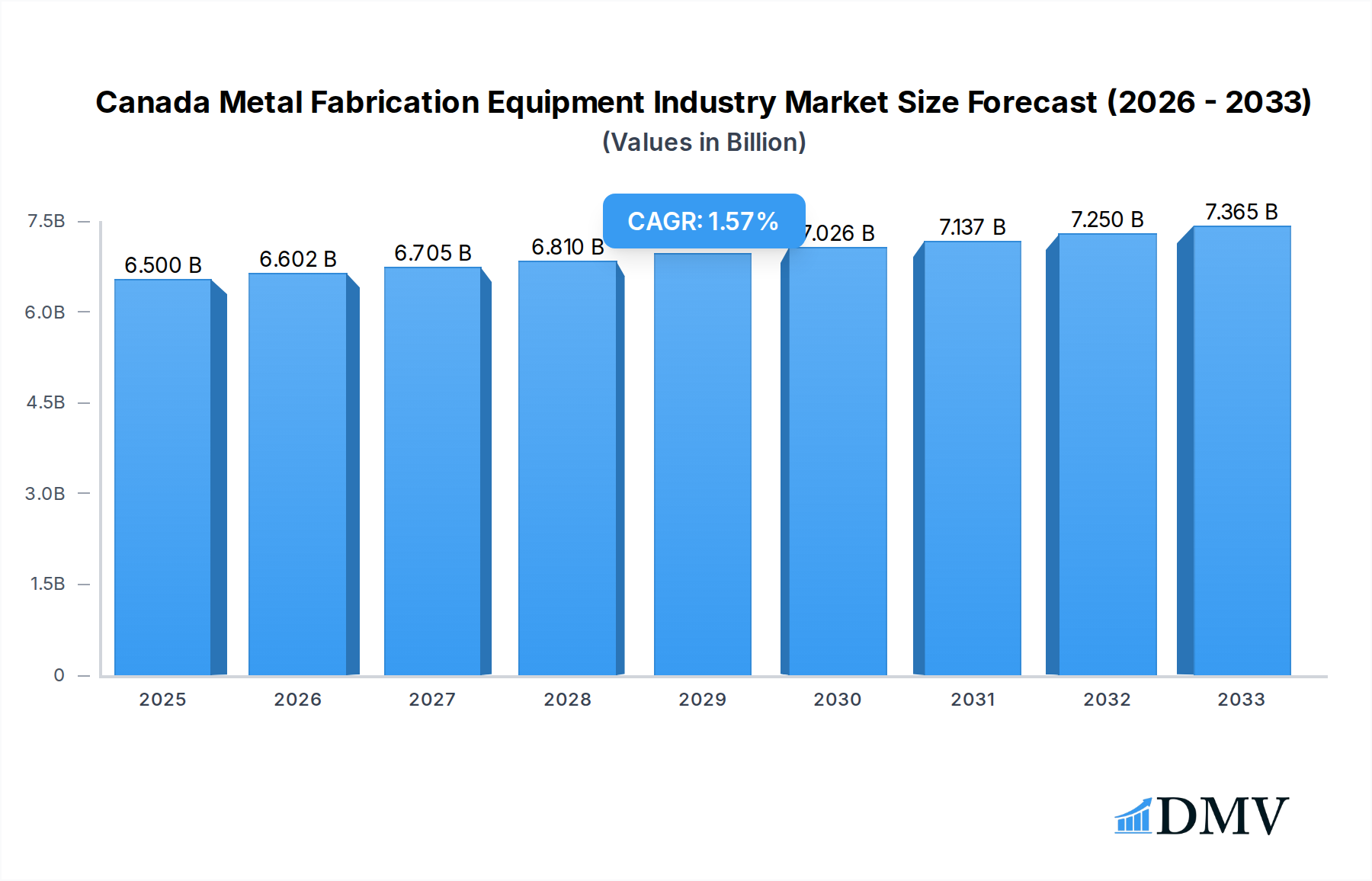

The Canada Metal Fabrication Equipment market is poised for steady growth, projected to reach $6.5 billion by 2025. With a Compound Annual Growth Rate (CAGR) of 1.6% from 2019 to 2033, the industry demonstrates resilience and consistent expansion. This growth is primarily propelled by significant investments in infrastructure projects across sectors like construction and power generation, alongside a robust manufacturing base that continues to demand advanced fabrication solutions. The increasing adoption of automation in manufacturing processes, driven by the need for enhanced efficiency, precision, and cost-effectiveness, serves as a key catalyst. Furthermore, the ongoing modernization of existing industrial facilities and the emergence of new energy projects are creating sustained demand for high-performance metal fabrication machinery.

Canada Metal Fabrication Equipment Industry Market Size (In Billion)

Despite the positive outlook, the market faces certain constraints. The high initial capital investment required for sophisticated metal fabrication equipment can be a barrier for smaller enterprises. Additionally, fluctuations in raw material prices, particularly for metals like steel and aluminum, can impact project budgets and equipment purchasing decisions. Nevertheless, the market is witnessing a strong trend towards smart manufacturing and Industry 4.0 integration, with companies focusing on equipment that offers advanced digital capabilities, real-time monitoring, and predictive maintenance. Innovations in machining and cutting technologies, alongside advancements in automated welding and forming processes, are expected to shape the competitive landscape. Key end-user industries like manufacturing, oil and gas, and power & utilities are anticipated to drive demand, while the services segment, including maintenance and repair, will play a crucial role in supporting the installed base of equipment.

Canada Metal Fabrication Equipment Industry Company Market Share

Canada Metal Fabrication Equipment Industry Market Composition & Trends

The Canadian metal fabrication equipment industry, valued at an estimated USD XXX billion in 2025, is characterized by a dynamic and evolving market. Market concentration is moderate, with a significant presence of both established multinational corporations and specialized domestic players. Innovation is a key catalyst, driven by the relentless pursuit of enhanced efficiency, precision, and automation in manufacturing processes. Regulatory landscapes, while generally supportive of industrial growth, can present varying compliance requirements across different provinces. Substitute products, though present in some niche applications, are largely outpaced by the specialized capabilities of modern fabrication equipment. End-user profiles span a diverse range of sectors, with manufacturing forming the largest segment, followed closely by construction and oil and gas. Mergers and acquisitions (M&A) activities are a notable trend, aimed at consolidating market share, expanding technological capabilities, and achieving economies of scale. M&A deal values are projected to reach USD XXX billion in the forecast period.

- Market Concentration: Moderate, with a mix of large enterprises and SMEs.

- Innovation Drivers: Automation, precision engineering, advanced materials.

- End-User Dominance: Manufacturing sector accounts for approximately XX% of demand.

- M&A Focus: Market consolidation, technology acquisition, geographical expansion.

Canada Metal Fabrication Equipment Industry Industry Evolution

The Canada metal fabrication equipment industry has undergone significant evolution from 2019 to the present, and its trajectory from 2025 to 2033 promises continued innovation and growth. Throughout the historical period (2019-2024), the industry witnessed a steady increase in demand, fueled by robust activity in the construction, manufacturing, and resource sectors. Technological advancements have been a primary driver, with the adoption of automated machinery, advanced welding techniques, and sophisticated cutting technologies becoming increasingly prevalent. This shift has been spurred by a desire for higher productivity, improved product quality, and reduced labor costs. The base year of 2025 marks a pivotal point, with the market anticipated to reach USD XXX billion. The forecast period (2025-2033) is expected to see a compound annual growth rate (CAGR) of approximately XX%, driven by a confluence of factors including government initiatives promoting domestic manufacturing, ongoing infrastructure development projects, and the persistent need for sophisticated metal components across a multitude of industries.

Consumer demand has also played a crucial role in shaping the industry's evolution. As end-user industries require more complex and customized metal products, the demand for versatile and high-precision fabrication equipment has surged. This has led to a greater emphasis on research and development, with companies investing heavily in developing intelligent systems, robotic integration, and advanced software for design and manufacturing. The adoption of Industry 4.0 principles, including the Internet of Things (IoT) and artificial intelligence (AI), is increasingly influencing the design and functionality of metal fabrication equipment, enabling real-time monitoring, predictive maintenance, and optimized production workflows. Furthermore, a growing emphasis on sustainability and energy efficiency within end-user industries is prompting fabricators to seek equipment that minimizes waste and energy consumption, driving innovation in these areas. The industry's resilience, demonstrated through navigating global economic fluctuations and supply chain challenges, underscores its fundamental importance to the Canadian economy. By 2033, the market is projected to reach an impressive USD XXX billion, reflecting sustained investment and technological progression.

Leading Regions, Countries, or Segments in Canada Metal Fabrication Equipment Industry

Within the Canada metal fabrication equipment industry, several segments and end-user industries exhibit significant dominance, shaping market dynamics and investment trends. From a Service Type perspective, Machining and Cutting services represent a cornerstone, commanding a substantial market share due to the fundamental requirement for precision shaping and material removal across virtually all manufacturing and construction applications. This segment’s dominance is underpinned by the continuous demand for high-precision components in sectors like aerospace, automotive, and heavy machinery.

- Machining and Cutting Dominance: Driven by the need for precision in high-value manufacturing, including aerospace, automotive, and medical device fabrication. Investment in advanced CNC machinery and multi-axis machining centers is a key indicator.

In terms of Product Type, Automatic fabrication equipment is witnessing the most rapid growth and is increasingly defining leadership. The push for higher throughput, consistent quality, and reduced operational costs is propelling the adoption of automated solutions.

- Automatic Equipment Ascendancy: Fueled by Industry 4.0 adoption, robotic integration, and the demand for high-volume, high-precision production. Government incentives for automation and technological upgrades further bolster this segment.

The End User Industry landscape clearly positions Manufacturing as the leading sector, accounting for an estimated XX% of the market's demand. This broad category encompasses diverse sub-sectors like automotive, aerospace, heavy machinery, and consumer goods, all of which rely heavily on sophisticated metal fabrication. The Construction industry also presents a substantial and growing market, driven by infrastructure projects and commercial development.

- Manufacturing Sector Leadership: Encompasses automotive, aerospace, general manufacturing, and industrial equipment, all requiring advanced fabrication capabilities for component production.

- Construction Industry Growth: Significant investment in infrastructure projects, commercial buildings, and residential development fuels demand for structural steel and specialized fabricated components.

Geographically, Ontario consistently emerges as the leading region for metal fabrication equipment due to its concentrated industrial base, particularly in automotive and advanced manufacturing. Its well-developed infrastructure, skilled workforce, and proximity to key markets further solidify its position.

- Ontario's Dominance: A hub for advanced manufacturing, automotive production, and R&D, attracting significant investment in fabrication technologies. Strong provincial support for manufacturing innovation.

Canada Metal Fabrication Equipment Industry Product Innovations

Product innovations in the Canada metal fabrication equipment industry are increasingly focused on intelligent automation, enhanced precision, and sustainable operation. The introduction of AI-powered robotic welding systems, offering adaptive path planning and real-time quality control, is revolutionizing efficiency. Advanced laser cutting machines with higher power density and multi-axis capabilities enable intricate designs and faster processing of diverse materials. Furthermore, the development of collaborative robots (cobots) allows for seamless integration with human operators, boosting productivity in complex assembly tasks. These innovations are critical for meeting the evolving demands of end-user industries for customized, high-performance metal components.

Propelling Factors for Canada Metal Fabrication Equipment Industry Growth

Several key factors are propelling the growth of the Canada metal fabrication equipment industry. Technologically, the relentless drive towards automation, digitalization (Industry 4.0), and advanced manufacturing techniques is creating demand for sophisticated machinery. Economically, significant government investment in infrastructure projects and initiatives aimed at revitalizing domestic manufacturing are boosting capital expenditure. Regulatory influences, such as those promoting advanced manufacturing and export competitiveness, also play a crucial role in fostering industry expansion.

- Technological Advancements: Industry 4.0 adoption, AI integration, robotics, and automation.

- Economic Stimulus: Government infrastructure spending and manufacturing support programs.

- Regulatory Support: Policies promoting innovation, competitiveness, and job creation in advanced manufacturing.

Obstacles in the Canada Metal Fabrication Equipment Industry Market

Despite strong growth prospects, the Canada metal fabrication equipment industry faces several obstacles. Regulatory challenges related to environmental standards and labor regulations can increase operational costs. Supply chain disruptions, as witnessed globally, can lead to material shortages and extended lead times for critical components, impacting production schedules and cost-effectiveness. Intense competitive pressures, both domestically and internationally, necessitate continuous investment in R&D and process optimization to maintain market share and profitability.

- Regulatory Hurdles: Evolving environmental and safety compliance requirements.

- Supply Chain Volatility: Material availability and logistics challenges impacting lead times.

- Competitive Landscape: Intense pricing pressure and the need for constant innovation.

Future Opportunities in Canada Metal Fabrication Equipment Industry

Emerging opportunities in the Canada metal fabrication equipment industry lie in the growing demand for specialized fabrication solutions for renewable energy sectors, such as wind turbine component manufacturing. The continued adoption of Industry 4.0 technologies presents a significant opportunity for companies offering smart, interconnected equipment and advanced software solutions. Furthermore, the trend towards increased reshoring of manufacturing activities creates a demand for modern, efficient fabrication capabilities within Canada.

- Renewable Energy Sector Expansion: Fabrication for wind, solar, and other green energy infrastructure.

- Smart Manufacturing Solutions: Demand for IoT-enabled equipment and data analytics platforms.

- Reshoring Initiatives: Opportunities for domestic manufacturers to meet increased local demand.

Major Players in the Canada Metal Fabrication Equipment Industry Ecosystem

- BTD Manufacturing

- Colfax

- Komaspec

- Matcor Matsu Group Inc

- Sandvik Mining and Construction Canada Inc

- STANDARD IRON & WIRE WORKS INC

- TRUMPF Canada Inc

- Atlas Copco

- AMADA Canada

- DMG MORI Canada

Key Developments in Canada Metal Fabrication Equipment Industry Industry

- February 2022: Arrow Machine and Fabrication Group of Guelph, Ontario, announced the acquisition of Steelcraft, a Kitchener, Ontario, steel design, engineering, and fabrication firm. This acquisition expands Arrow's global customer base and manufacturing footprint. It also further promotes the company's strategy of partnering with leading operator-run machining and fabrication organizations to leverage their collective capabilities, solve customer problems, and develop deeper supply chain interactions.

- January 2022: Ag Growth International Inc. (AGI) completed the acquisition of Eastern Fabricators, Prince Edward Island, Canada. Eastern specializes in the engineering, design, fabrication, and installation of stainless-steel equipment and systems for food processors. Eastern operates three facilities in Canada, with two in Prince Edward Island and one in Ontario.

Strategic Canada Metal Fabrication Equipment Industry Market Forecast

The strategic forecast for the Canada metal fabrication equipment industry anticipates sustained growth driven by ongoing technological advancements and robust demand from key end-user sectors. The increasing adoption of automation and smart manufacturing technologies will continue to be a primary growth catalyst, enhancing productivity and precision. Emerging opportunities in sectors like renewable energy and the potential for increased reshoring of manufacturing will further bolster market expansion. Investments in advanced machinery and a focus on innovative solutions will be critical for stakeholders to capitalize on the projected market potential, reaching an estimated USD XXX billion by 2033.

Canada Metal Fabrication Equipment Industry Segmentation

-

1. Service Type

- 1.1. Machining and Cutting

- 1.2. Forming

- 1.3. Welding

- 1.4. Other Service Type

-

2. Product Type

- 2.1. Automatic

- 2.2. Semi-automatic

- 2.3. Manual

-

3. End User Industry

- 3.1. Manufacturing

- 3.2. Power and Utilities

- 3.3. Construction

- 3.4. Oil and Gas

- 3.5. Other End-user Industries

Canada Metal Fabrication Equipment Industry Segmentation By Geography

- 1. Canada

Canada Metal Fabrication Equipment Industry Regional Market Share

Geographic Coverage of Canada Metal Fabrication Equipment Industry

Canada Metal Fabrication Equipment Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 1.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Service Type

- 5.1.1. Machining and Cutting

- 5.1.2. Forming

- 5.1.3. Welding

- 5.1.4. Other Service Type

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Automatic

- 5.2.2. Semi-automatic

- 5.2.3. Manual

- 5.3. Market Analysis, Insights and Forecast - by End User Industry

- 5.3.1. Manufacturing

- 5.3.2. Power and Utilities

- 5.3.3. Construction

- 5.3.4. Oil and Gas

- 5.3.5. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Canada

- 5.1. Market Analysis, Insights and Forecast - by Service Type

- 6. Canada Metal Fabrication Equipment Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Service Type

- 6.1.1. Machining and Cutting

- 6.1.2. Forming

- 6.1.3. Welding

- 6.1.4. Other Service Type

- 6.2. Market Analysis, Insights and Forecast - by Product Type

- 6.2.1. Automatic

- 6.2.2. Semi-automatic

- 6.2.3. Manual

- 6.3. Market Analysis, Insights and Forecast - by End User Industry

- 6.3.1. Manufacturing

- 6.3.2. Power and Utilities

- 6.3.3. Construction

- 6.3.4. Oil and Gas

- 6.3.5. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Service Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 BTD Manufacturing

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Colfax

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Komaspec

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Matcor Matsu Group Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Sandvik Mining and Construction Canada Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 STANDARD IRON & WIRE WORKS INC

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 TRUMPF Canada Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Atlas Copco

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 AMADA Canada

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 DMG MORI Canada**List Not Exhaustive

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 BTD Manufacturing

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Canada Metal Fabrication Equipment Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Canada Metal Fabrication Equipment Industry Share (%) by Company 2025

List of Tables

- Table 1: Canada Metal Fabrication Equipment Industry Revenue billion Forecast, by Service Type 2020 & 2033

- Table 2: Canada Metal Fabrication Equipment Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 3: Canada Metal Fabrication Equipment Industry Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 4: Canada Metal Fabrication Equipment Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Canada Metal Fabrication Equipment Industry Revenue billion Forecast, by Service Type 2020 & 2033

- Table 6: Canada Metal Fabrication Equipment Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 7: Canada Metal Fabrication Equipment Industry Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 8: Canada Metal Fabrication Equipment Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Canada Metal Fabrication Equipment Industry?

The projected CAGR is approximately 1.6%.

2. Which companies are prominent players in the Canada Metal Fabrication Equipment Industry?

Key companies in the market include BTD Manufacturing, Colfax, Komaspec, Matcor Matsu Group Inc, Sandvik Mining and Construction Canada Inc, STANDARD IRON & WIRE WORKS INC, TRUMPF Canada Inc, Atlas Copco, AMADA Canada, DMG MORI Canada**List Not Exhaustive.

3. What are the main segments of the Canada Metal Fabrication Equipment Industry?

The market segments include Service Type, Product Type, End User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.5 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Construction Industry Offers Immense Demand for the Metal Fabrication Equipment.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

February 2022: Arrow Machine and Fabrication Group of Guelph, Ontario, announced the acquisition of Steelcraft, a Kitchener, Ontario, steel design, engineering, and fabrication firm. This acquisition expands Arrow's global customer base and manufacturing footprint. It also further promotes the company's strategy of partnering with leading operator-run machining and fabrication organizations to leverage their collective capabilities, solve customer problems, and develop deeper supply chain interactions.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Canada Metal Fabrication Equipment Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Canada Metal Fabrication Equipment Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Canada Metal Fabrication Equipment Industry?

To stay informed about further developments, trends, and reports in the Canada Metal Fabrication Equipment Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence