Key Insights

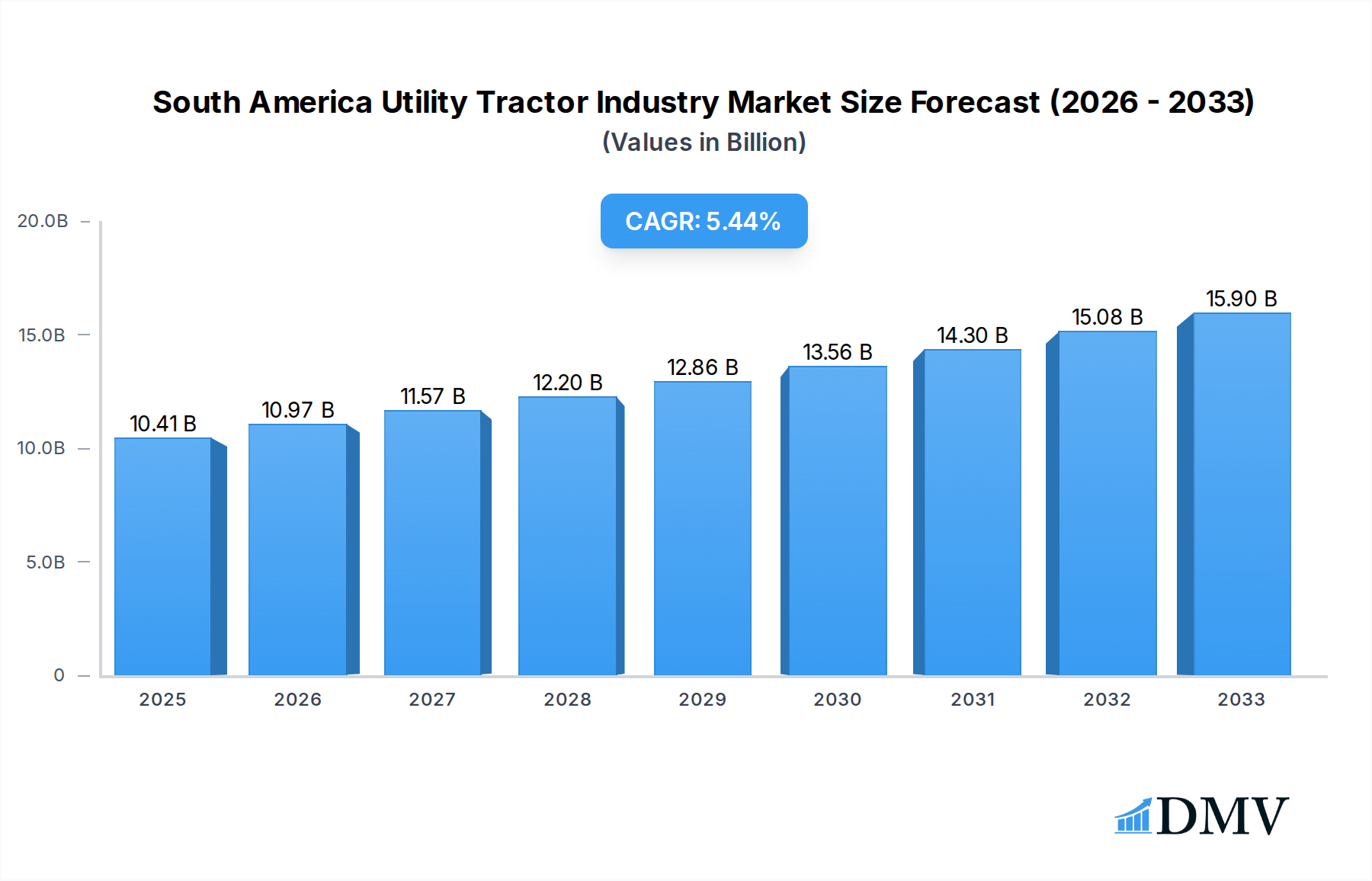

The South American utility tractor market is poised for significant expansion, with an estimated market size of USD 10.41 billion in 2025. This growth is driven by a projected Compound Annual Growth Rate (CAGR) of 5.4% from 2019 to 2033, indicating a robust and sustained upward trajectory. Key drivers for this expansion include the increasing adoption of modern farming techniques, the growing need for enhanced agricultural productivity to feed a rising population, and government initiatives aimed at modernizing the agricultural sector across key nations like Brazil and Argentina. Furthermore, technological advancements in utility tractors, such as GPS guidance, precision farming capabilities, and more fuel-efficient engines, are attracting greater investment and adoption by farmers seeking to optimize their operations and yields. The region's diverse agricultural landscape, ranging from large-scale commercial farming to smallholder operations, necessitates a variety of utility tractor solutions, further fueling market demand.

South America Utility Tractor Industry Market Size (In Billion)

While the market is strong, certain factors could influence its growth trajectory. Evolving economic conditions and currency fluctuations within South American countries can impact purchasing power and investment in new machinery. Additionally, the availability and cost of credit for farmers, along with logistical challenges in reaching remote agricultural areas, present potential restraints. However, the overarching trend towards mechanization and the pursuit of greater efficiency in agriculture are expected to outweigh these challenges. The market segmentation reveals a strong focus on production and consumption analysis, with significant attention also paid to import and export dynamics, and price trends. Companies like CNH Global NV, Mahindra & Mahindra Ltd, and Deere & Company are key players actively shaping this landscape through innovation and strategic market penetration.

South America Utility Tractor Industry Company Market Share

South America Utility Tractor Industry Market Composition & Trends

The South America utility tractor market exhibits a dynamic landscape, shaped by significant innovation catalysts and evolving regulatory frameworks. Market concentration is moderate, with key players vying for substantial market share. CNH Global NV, Deere & Company, and AGCO Corp currently lead, their collective market share estimated at over 50 billion USD in 2025. The industry's growth is propelled by agricultural mechanization initiatives and government support for modern farming practices. Identifying and understanding end-user profiles, from large-scale commercial farms to smaller family holdings, is crucial for targeted product development and marketing strategies. The demand for versatile, fuel-efficient, and technologically advanced utility tractors is on the rise, influencing new product development and adoption rates. Potential substitute products, such as advanced ride-on mowers and specialized compact equipment, are present but generally cater to niche applications and do not pose a significant threat to the core utility tractor market. Mergers and acquisitions (M&A) activities are expected to play a role in consolidating the market, with projected M&A deal values reaching several billion USD by 2033. These strategic moves will likely focus on acquiring innovative technologies, expanding geographical reach, and enhancing product portfolios to meet the growing demands for sustainable and efficient agricultural machinery across South America.

- Market Share Distribution (Estimated 2025):

- CNH Global NV: 18 billion USD

- Deere & Company: 15 billion USD

- AGCO Corp: 12 billion USD

- Mahindra & Mahindra Ltd: 7 billion USD

- International Tractors Limited: 6 billion USD

- Tractors and Farm Equipment Limited (TAFE): 5 billion USD

- Claas KGaA mbH: 4 billion USD

- Kubota Agricultural Machinery: 3 billion USD

- Massey Ferguson: 2 billion USD

- M&A Deal Values (Projected 2025-2033): Expected to reach approximately 10 billion USD.

South America Utility Tractor Industry Industry Evolution

The South America utility tractor industry has undergone a significant transformation, evolving from basic mechanization to sophisticated agricultural solutions. The study period of 2019–2033 encompasses a robust growth trajectory, driven by increasing agricultural output demands, government incentives for farm modernization, and a growing understanding of the economic benefits of advanced machinery. In the base year of 2025, the market is valued at an estimated 80 billion USD, reflecting a compound annual growth rate (CAGR) of approximately 5.5% from the historical period of 2019–2024. Technological advancements have been a cornerstone of this evolution. We've witnessed the integration of GPS guidance systems, precision farming technologies, and telematics, enhancing operational efficiency and reducing resource wastage. These innovations are critical for improving crop yields and optimizing farm management practices. Shifting consumer demands, particularly from large agricultural conglomerates and progressive medium-sized farms, are pushing for tractors with higher horsepower, greater fuel efficiency, enhanced operator comfort, and advanced connectivity features. The forecast period of 2025–2033 is expected to see continued growth, fueled by the adoption of electric and hybrid tractor technologies, further automation, and the increasing demand for sustainable agricultural practices. The rise of digital agriculture platforms, which integrate tractor data with other farm management systems, is also a key trend shaping the industry's future. This evolution is not merely about hardware; it’s about providing comprehensive solutions that enhance productivity, profitability, and sustainability for South American farmers.

Leading Regions, Countries, or Segments in South America Utility Tractor Industry

The dominance within the South America utility tractor industry is intricately linked to specific segments and key geographical areas, showcasing a strong correlation between agricultural output, economic development, and market penetration.

Production Analysis:

Brazil emerges as the undisputed leader in production, contributing over 40% of the total utility tractor output in South America. This dominance is attributed to its vast agricultural land, significant global exports of commodities like soybeans and corn, and a well-established manufacturing base. Argentina follows, with its substantial grain production and a growing focus on mechanized farming, accounting for approximately 25% of the regional production.

- Key Drivers for Production Dominance:

- Vast Agricultural Land: Extensive arable land in Brazil and Argentina supports large-scale tractor deployment.

- Export-Oriented Agriculture: High demand for agricultural exports necessitates efficient and high-volume production.

- Government Support: Policies promoting domestic manufacturing and agricultural modernization.

- Presence of Key Manufacturers: Several major global and local players have manufacturing facilities in these countries.

Consumption Analysis:

Brazil also leads in consumption, mirroring its production prowess and the sheer scale of its agricultural operations. The demand here is driven by large commercial farms and the continuous need for advanced machinery to maximize output. Argentina is the second-largest consumer, with its significant beef and grain industries requiring robust tractor fleets.

- Key Drivers for Consumption Dominance:

- Large Farm Holdings: The prevalence of large-scale agribusinesses requires substantial tractor investment.

- Technological Adoption: Farmers in these regions are increasingly adopting advanced tractors for precision agriculture.

- Profitability of Agriculture: Strong agricultural commodity prices support investment in new machinery.

Import Market Analysis (Value & Volume):

While Brazil and Argentina are major producers, other countries like Colombia, Peru, and Chile, with developing agricultural sectors and specific crop demands (e.g., coffee, fruits), represent significant import markets for utility tractors. These nations often import specialized models or units not domestically manufactured. The import market in 2025 is estimated at 10 billion USD.

- Key Drivers for Import Market Dominance:

- Specialized Crop Requirements: Demand for tractors suited for specific terrains and crops.

- Limited Domestic Production: Countries with smaller manufacturing bases rely on imports.

- Technological Gaps: Imports fill the need for advanced features not yet widely produced locally.

Export Market Analysis (Value & Volume):

Brazil and Argentina are also the largest exporters of utility tractors within South America, primarily shipping to neighboring countries and also to other global agricultural hubs. Their competitive pricing and production capacity make them key players in the international export arena. The export market value in 2025 is estimated at 8 billion USD.

- Key Drivers for Export Market Dominance:

- Competitive Pricing: Economies of scale in production allow for competitive export prices.

- Established Trade Networks: Strong existing trade relationships within South America and beyond.

- Product Quality and Innovation: Continuous investment in R&D ensures export-ready products.

Price Trend Analysis:

Price trends for utility tractors in South America are influenced by a combination of production costs, currency exchange rates, import duties, and market demand. While prices have seen a steady increase due to inflation and rising component costs, the market for utility tractors in the estimated year of 2025 is expected to be in the range of 25,000 USD to 70,000 USD per unit, depending on horsepower and features. The overall market value for utility tractors is projected to reach 95 billion USD by 2033.

- Key Factors Influencing Price Trends:

- Raw Material Costs: Fluctuations in steel, rubber, and engine component prices.

- Technological Advancements: Integration of high-tech features often leads to higher price points.

- Exchange Rates: Impact of local currency fluctuations against the US dollar.

- Demand-Supply Dynamics: High demand can lead to price increases, while oversupply can result in competitive pricing.

South America Utility Tractor Industry Product Innovations

The South America utility tractor industry is witnessing a surge in product innovations, driven by the need for enhanced efficiency, sustainability, and operator comfort. Companies are focusing on developing tractors with higher horsepower-to-weight ratios, improved fuel efficiency through advanced engine technology, and enhanced maneuverability for diverse terrains. The integration of telematics and GPS guidance systems is becoming standard, enabling precision farming applications like variable rate application of fertilizers and precise row planting, leading to an estimated 15% increase in crop yield for early adopters. Innovations in operator cabins, such as ergonomic seating, advanced climate control, and intuitive digital interfaces, are also a key focus, reducing operator fatigue and improving productivity. The development of compact and versatile utility tractors suitable for smaller farms and specialized agricultural tasks, along with early-stage research into electric and hybrid powertrains, represents the next frontier in product development. These advancements are critical for addressing the evolving needs of South American agriculture.

Propelling Factors for South America Utility Tractor Industry Growth

Several interconnected factors are propelling the growth of the South America utility tractor industry. A primary driver is the increasing demand for food security and agricultural exports, necessitating higher crop yields and more efficient farming practices. Government initiatives promoting agricultural mechanization, coupled with subsidies and favorable financing options for farmers, are significantly boosting tractor adoption rates. Technological advancements, including the integration of GPS, precision farming tools, and telematics, are enhancing operational efficiency and driving demand for modern utility tractors. Furthermore, the growing trend of consolidation among agricultural landholdings is leading to larger-scale operations that require more powerful and sophisticated machinery, estimated to drive market growth by an additional 3% annually.

Obstacles in the South America Utility Tractor Industry Market

Despite the robust growth, the South America utility tractor industry faces several significant obstacles. High upfront costs for advanced utility tractors can be a major barrier, particularly for small and medium-sized farmers who often have limited access to financing. Fluctuating currency exchange rates and economic instability in some South American countries can also impact purchasing power and the affordability of imported machinery, leading to an estimated 10% slowdown in adoption during periods of volatility. Supply chain disruptions, exacerbated by global logistics challenges and local infrastructure limitations, can lead to extended delivery times and increased costs. Furthermore, intense competition among global and local manufacturers, while beneficial for consumers, can exert downward pressure on profit margins.

Future Opportunities in South America Utility Tractor Industry

The future of the South America utility tractor industry presents numerous promising opportunities. The increasing adoption of precision agriculture technologies offers a significant avenue for growth, as farmers seek to optimize resource usage and improve yields. The growing demand for sustainable and eco-friendly farming methods is creating opportunities for the development and adoption of electric and hybrid utility tractors, which are projected to capture a 10% market share by 2033. Emerging markets within South America, with developing agricultural sectors, represent untapped potential for market expansion. Furthermore, the increasing focus on data analytics and farm management software, integrated with tractor telematics, opens doors for service-based revenue streams and value-added solutions for farmers.

Major Players in the South America Utility Tractor Industry Ecosystem

- CNH Global NV

- International Tractors Limited

- AGCO Corp

- Mahindra & Mahindra Ltd

- Tractors and Farm Equipment Limited (TAFE)

- Claas KGaA mbH

- Kubota Agricultural Machinery

- Massey Ferguson

- Deere & Company

Key Developments in South America Utility Tractor Industry Industry

- 2023 October: AGCO Corp announces strategic expansion of its manufacturing facility in Brazil to meet growing regional demand for utility tractors.

- 2023 November: Mahindra & Mahindra Ltd launches a new range of fuel-efficient utility tractors tailored for the South American market, focusing on affordability and performance.

- 2024 January: Deere & Company introduces advanced telematics solutions for its utility tractor fleet in South America, enabling enhanced fleet management and predictive maintenance.

- 2024 March: CNH Global NV announces a partnership with a leading Latin American agricultural technology provider to integrate smart farming solutions into its tractor offerings.

- 2024 May: Tractors and Farm Equipment Limited (TAFE) expands its distribution network in Colombia, aiming to increase its market share in the country's growing agricultural sector.

- 2024 July: Kubota Agricultural Machinery showcases its latest compact utility tractor models at a major agricultural expo in Argentina, targeting the needs of smaller farm operations.

- 2024 September: Claas KGaA mbH invests in research and development for alternative fuel powertrains for utility tractors, anticipating future market shifts towards sustainability.

Strategic South America Utility Tractor Industry Market Forecast

The South America utility tractor industry is poised for substantial growth, driven by a confluence of factors including increasing agricultural output, supportive government policies, and continuous technological innovation. The estimated market value of 95 billion USD by 2033 reflects a robust CAGR of approximately 5.5% from the base year of 2025. Key growth catalysts include the expanding adoption of precision agriculture, which enhances farm productivity and resource efficiency, and the emerging demand for sustainable technologies like electric and hybrid tractors. Investments in R&D, coupled with strategic partnerships and potential M&A activities, will further shape the competitive landscape, ensuring that manufacturers remain agile and responsive to the evolving needs of the region's dynamic agricultural sector. The outlook for the South America utility tractor market remains highly optimistic, with significant opportunities for market expansion and technological advancement.

South America Utility Tractor Industry Segmentation

- 1. Production Analysis

- 2. Consumption Analysis

- 3. Import Market Analysis (Value & Volume)

- 4. Export Market Analysis (Value & Volume)

- 5. Price Trend Analysis

South America Utility Tractor Industry Segmentation By Geography

-

1. South America

- 1.1. Brazil

- 1.2. Argentina

- 1.3. Chile

- 1.4. Colombia

- 1.5. Peru

- 1.6. Venezuela

- 1.7. Ecuador

- 1.8. Bolivia

- 1.9. Paraguay

- 1.10. Uruguay

South America Utility Tractor Industry Regional Market Share

Geographic Coverage of South America Utility Tractor Industry

South America Utility Tractor Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Production Analysis

- 5.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 5.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 5.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 5.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. South America

- 6. South America Utility Tractor Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Production Analysis

- 6.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 6.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 6.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 6.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 CNH Global NV

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 International Tractors Limited

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 AGCO Cor

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Mahindra & Mahindra Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Tractors and Farm Equipment Limited (TAFE)

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Claas KGaA mbH

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Kubota Agricultural Machinery

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Massey Ferguson

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Deere & Company

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 CNH Global NV

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: South America Utility Tractor Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: South America Utility Tractor Industry Share (%) by Company 2025

List of Tables

- Table 1: South America Utility Tractor Industry Revenue billion Forecast, by Production Analysis 2020 & 2033

- Table 2: South America Utility Tractor Industry Volume Kiloton Forecast, by Production Analysis 2020 & 2033

- Table 3: South America Utility Tractor Industry Revenue billion Forecast, by Consumption Analysis 2020 & 2033

- Table 4: South America Utility Tractor Industry Volume Kiloton Forecast, by Consumption Analysis 2020 & 2033

- Table 5: South America Utility Tractor Industry Revenue billion Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 6: South America Utility Tractor Industry Volume Kiloton Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 7: South America Utility Tractor Industry Revenue billion Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 8: South America Utility Tractor Industry Volume Kiloton Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 9: South America Utility Tractor Industry Revenue billion Forecast, by Price Trend Analysis 2020 & 2033

- Table 10: South America Utility Tractor Industry Volume Kiloton Forecast, by Price Trend Analysis 2020 & 2033

- Table 11: South America Utility Tractor Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 12: South America Utility Tractor Industry Volume Kiloton Forecast, by Region 2020 & 2033

- Table 13: South America Utility Tractor Industry Revenue billion Forecast, by Production Analysis 2020 & 2033

- Table 14: South America Utility Tractor Industry Volume Kiloton Forecast, by Production Analysis 2020 & 2033

- Table 15: South America Utility Tractor Industry Revenue billion Forecast, by Consumption Analysis 2020 & 2033

- Table 16: South America Utility Tractor Industry Volume Kiloton Forecast, by Consumption Analysis 2020 & 2033

- Table 17: South America Utility Tractor Industry Revenue billion Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 18: South America Utility Tractor Industry Volume Kiloton Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 19: South America Utility Tractor Industry Revenue billion Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 20: South America Utility Tractor Industry Volume Kiloton Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 21: South America Utility Tractor Industry Revenue billion Forecast, by Price Trend Analysis 2020 & 2033

- Table 22: South America Utility Tractor Industry Volume Kiloton Forecast, by Price Trend Analysis 2020 & 2033

- Table 23: South America Utility Tractor Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 24: South America Utility Tractor Industry Volume Kiloton Forecast, by Country 2020 & 2033

- Table 25: Brazil South America Utility Tractor Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Brazil South America Utility Tractor Industry Volume (Kiloton) Forecast, by Application 2020 & 2033

- Table 27: Argentina South America Utility Tractor Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Argentina South America Utility Tractor Industry Volume (Kiloton) Forecast, by Application 2020 & 2033

- Table 29: Chile South America Utility Tractor Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Chile South America Utility Tractor Industry Volume (Kiloton) Forecast, by Application 2020 & 2033

- Table 31: Colombia South America Utility Tractor Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Colombia South America Utility Tractor Industry Volume (Kiloton) Forecast, by Application 2020 & 2033

- Table 33: Peru South America Utility Tractor Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Peru South America Utility Tractor Industry Volume (Kiloton) Forecast, by Application 2020 & 2033

- Table 35: Venezuela South America Utility Tractor Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Venezuela South America Utility Tractor Industry Volume (Kiloton) Forecast, by Application 2020 & 2033

- Table 37: Ecuador South America Utility Tractor Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Ecuador South America Utility Tractor Industry Volume (Kiloton) Forecast, by Application 2020 & 2033

- Table 39: Bolivia South America Utility Tractor Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Bolivia South America Utility Tractor Industry Volume (Kiloton) Forecast, by Application 2020 & 2033

- Table 41: Paraguay South America Utility Tractor Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Paraguay South America Utility Tractor Industry Volume (Kiloton) Forecast, by Application 2020 & 2033

- Table 43: Uruguay South America Utility Tractor Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Uruguay South America Utility Tractor Industry Volume (Kiloton) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the South America Utility Tractor Industry?

The projected CAGR is approximately 5.4%.

2. Which companies are prominent players in the South America Utility Tractor Industry?

Key companies in the market include CNH Global NV, International Tractors Limited, AGCO Cor, Mahindra & Mahindra Ltd, Tractors and Farm Equipment Limited (TAFE), Claas KGaA mbH, Kubota Agricultural Machinery, Massey Ferguson, Deere & Company.

3. What are the main segments of the South America Utility Tractor Industry?

The market segments include Production Analysis, Consumption Analysis, Import Market Analysis (Value & Volume), Export Market Analysis (Value & Volume), Price Trend Analysis.

4. Can you provide details about the market size?

The market size is estimated to be USD 10.41 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Legalization of Cannabis; Growing Focus on Health Benefits of Cannabis.

6. What are the notable trends driving market growth?

Rising Labour Scarcity and Wages.

7. Are there any restraints impacting market growth?

Lack of Data on Dosages and Results; Lack of Access to Financial Assistance.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in Kiloton.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "South America Utility Tractor Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the South America Utility Tractor Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the South America Utility Tractor Industry?

To stay informed about further developments, trends, and reports in the South America Utility Tractor Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence