Key Insights

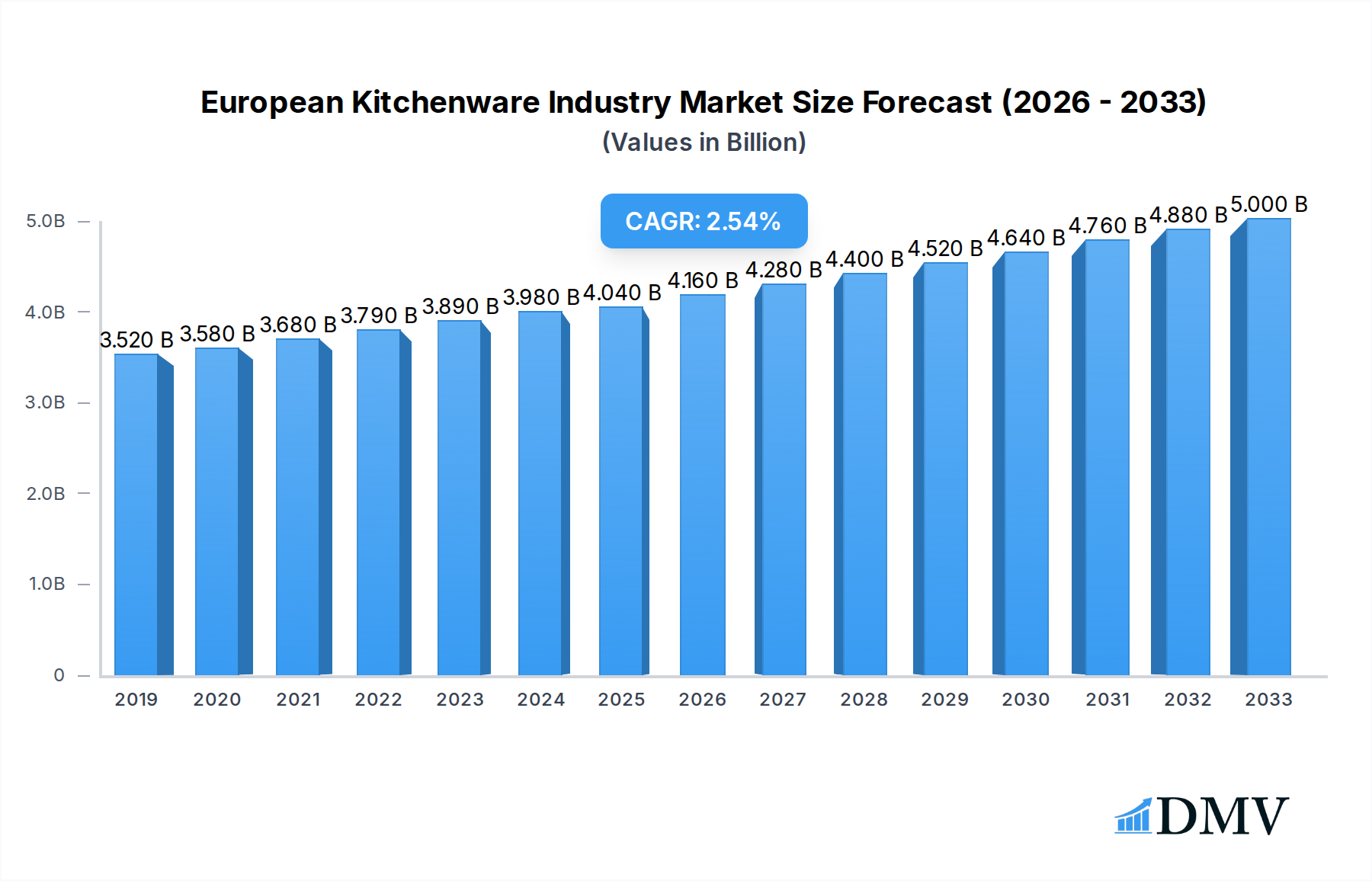

The European Kitchenware Industry is poised for steady growth, with an estimated market size of 4040 million in 2025. Projected to expand at a Compound Annual Growth Rate (CAGR) of 3.17% through 2033, this dynamic sector is being propelled by several key drivers. A significant factor is the increasing consumer focus on home cooking and culinary exploration, fueled by the popularity of cooking shows, social media trends, and a growing awareness of healthy eating. This has led to a higher demand for premium, durable, and aesthetically pleasing kitchenware. Furthermore, rising disposable incomes across various European nations contribute to consumers' willingness to invest in higher-quality cookware and kitchen tools, enhancing their cooking experience and kitchen aesthetics. The segment for cooking tools is experiencing robust demand, reflecting this trend.

European Kitchenware Industry Market Size (In Billion)

However, the industry is not without its challenges. The rise of private label brands and intense price competition from budget-friendly options can put pressure on profit margins for established players. Moreover, fluctuating raw material costs, particularly for stainless steel and aluminum, can impact manufacturing expenses and ultimately product pricing. Despite these restraints, innovation remains a key differentiator. Brands are increasingly focusing on developing energy-efficient cookware, non-stick surfaces with improved durability, and smart kitchen gadgets that integrate technology. The online distribution channel is rapidly gaining traction, offering convenience and wider product selection to consumers, while specialty stores cater to enthusiasts seeking high-performance and niche products. Stainless steel and aluminum continue to dominate material preferences due to their durability and performance, but interest in sustainable and eco-friendly materials is on the rise.

European Kitchenware Industry Company Market Share

European Kitchenware Industry Market Composition & Trends

The European kitchenware market exhibits a moderately concentrated landscape, with several global powerhouses and established regional players vying for market share. Innovation is a significant catalyst, driven by increasing consumer demand for convenience, durability, and aesthetically pleasing designs. Sustainability is also emerging as a key differentiator, with manufacturers investing in eco-friendly materials and production processes. The regulatory environment, particularly concerning food-grade materials and product safety standards within the EU, plays a crucial role in shaping market entry and product development. Substitute products, such as direct-to-consumer online brands and private label offerings, present a growing challenge to traditional retail channels. End-user profiles are diverse, ranging from budget-conscious households to culinary enthusiasts seeking premium performance. Mergers and acquisitions (M&A) activity, while not at extreme levels, is present as companies strategically consolidate to expand their product portfolios and geographic reach. The overall market share distribution sees established brands like Cuisinart and Le Creuset holding significant portions, complemented by specialized manufacturers and emerging direct-to-consumer brands. M&A deal values, though variable, often reflect strategic imperatives such as acquiring new technologies or market access.

- Market Concentration: Moderately concentrated with a mix of global and regional leaders.

- Innovation Catalysts: Demand for convenience, durability, aesthetics, and sustainability.

- Regulatory Landscape: Stringent EU regulations on product safety and material compliance.

- Substitute Products: Growing influence of online DTC brands and private labels.

- End-User Profiles: Diverse, from budget-conscious to premium culinary enthusiasts.

- M&A Activities: Strategic consolidations for portfolio expansion and market access.

European Kitchenware Industry Industry Evolution

The European kitchenware industry has undergone a remarkable evolution over the Historical Period (2019–2024), characterized by dynamic growth trajectories and a continuous influx of technological advancements. This period witnessed a significant shift in consumer preferences, moving beyond basic functionality to prioritize durability, ergonomic design, and advanced cooking capabilities. The Base Year of 2025 marks a pivotal point where these evolving demands have firmly taken root, shaping product development and market strategies. The Study Period (2019–2033) encompasses a comprehensive view of this transformation, from initial post-pandemic recovery trends to projected future innovations. Throughout the Forecast Period (2025–2033), the industry is expected to maintain a robust growth trajectory, fueled by increasing disposable incomes, a rising interest in home cooking, and the growing influence of social media showcasing culinary expertise. Technological advancements have been instrumental, with the integration of smart features in cookware, improved non-stick coatings, and the use of more sustainable materials gaining traction. For instance, the adoption rate of induction-compatible cookware has seen a substantial increase, reflecting the growing prevalence of induction hobs across European households. Similarly, the demand for lightweight yet durable materials like advanced aluminum alloys has surged, improving user experience. The penetration of online retail channels has revolutionized distribution, allowing smaller brands to reach a wider audience and forcing traditional retailers to adapt their strategies. This digital transformation has also facilitated a greater demand for personalized and niche kitchenware products, catering to specific dietary needs or cooking styles. Furthermore, the industry has responded to increasing environmental consciousness by investing in product lifecycle assessments and the development of recyclable or biodegradable components, a trend that is projected to accelerate significantly in the coming years. The overall market size is estimated to have grown by approximately 6% annually during the historical period, with projections indicating a similar or slightly higher growth rate in the forecast period. The market size in 2024 is estimated at over 20 billion Euros, with a projected growth to over 40 billion Euros by 2033.

Leading Regions, Countries, or Segments in European Kitchenware Industry

Within the diverse European kitchenware industry, the Product Segment of Pots and Pans consistently emerges as the dominant force, driving significant market share and consumer demand. This category, encompassing a vast array of cooking vessels, from everyday frying pans to specialized stockpots, forms the bedrock of kitchen utility. The Material Segment of Stainless Steel also holds a commanding position, prized for its durability, non-reactivity, and aesthetic appeal, making it a preferred choice for both professional chefs and home cooks. The Distribution Channel of Hypermarkets and Supermarkets continues to be a crucial avenue for reaching a broad consumer base, offering convenience and accessibility for everyday purchases.

Dominance Factors for Pots and Pans:

- Ubiquitous Necessity: Pots and pans are fundamental to virtually every cooking activity, ensuring constant demand.

- Diverse Product Range: The segment caters to a wide spectrum of cooking needs, from basic frying to complex simmering and boiling.

- Innovation Hub: Manufacturers continuously innovate within this segment, introducing new coatings, designs, and functionalities to attract consumers.

- Brand Loyalty & Perception: Established brands in this segment have cultivated strong brand loyalty, often associated with quality and performance.

Dominance Factors for Stainless Steel:

- Superior Durability and Longevity: Stainless steel cookware is known for its ability to withstand high temperatures and resist corrosion, leading to a longer product lifespan.

- Food Safety and Non-Reactivity: It does not react with acidic foods, preserving the flavor and integrity of ingredients.

- Ease of Maintenance: Stainless steel is relatively easy to clean and maintain, appealing to busy consumers.

- Versatility in Cooking: It is compatible with most stovetop types, including induction, and can often be used in ovens.

- Premium Aesthetic Appeal: The sleek and polished finish of stainless steel often aligns with modern kitchen aesthetics.

Dominance Factors for Hypermarkets and Supermarkets:

- Mass Market Reach: These channels provide access to the largest consumer demographic across Europe.

- Convenience and Impulse Purchases: Consumers can easily pick up kitchenware items during their regular grocery shopping.

- Competitive Pricing Strategies: The presence of multiple brands allows for price competition, attracting budget-conscious shoppers.

- Promotional Activities: Supermarkets frequently run promotions and discounts, driving sales volume for kitchenware.

While other segments like specialty stores and online channels are growing, the core demand for essential cooking items, particularly pots and pans made from stainless steel, distributed through mass-market retail, solidifies their leading positions in the European Kitchenware Industry. The market size for Pots and Pans is estimated at over 15 billion Euros in 2025, with Stainless Steel accounting for over 10 billion Euros of that value.

European Kitchenware Industry Product Innovations

The European kitchenware industry is experiencing a surge in product innovations, driven by a desire for enhanced user experience and greater sustainability. Advanced non-stick coatings are now more durable and PFOA-free, offering healthier cooking options. Smart cookware integrating Bluetooth connectivity allows users to monitor cooking temperatures and times via smartphone apps, revolutionizing precision cooking. The development of energy-efficient materials and designs, such as induction-compatible bases and lighter-weight yet robust alloys, is also a significant trend. Innovations in modular kitchenware, allowing for multi-functional use and space-saving storage, are catering to increasingly smaller living spaces across Europe. Performance metrics such as heat distribution uniformity, scratch resistance of coatings, and overall product lifespan are key areas of focus for R&D, ensuring consumers receive high-quality, long-lasting products. The market size for innovative kitchenware products is projected to grow at a CAGR of 7% from 2025-2033.

Propelling Factors for European Kitchenware Industry Growth

Several key factors are propelling the growth of the European kitchenware industry. Firstly, a growing consumer interest in home cooking, influenced by social media trends and a desire for healthier eating habits, is a significant driver. Secondly, technological advancements leading to innovative, convenient, and durable products, such as smart cookware and energy-efficient materials, are attracting consumers. Thirdly, rising disposable incomes across many European nations allow for greater expenditure on premium and aesthetically pleasing kitchenware. Finally, increasing awareness of health and sustainability is pushing demand for eco-friendly materials and safer cooking surfaces, creating new market opportunities for conscious brands. The market size for sustainable kitchenware is predicted to reach over 8 billion Euros by 2033.

- Rising Home Cooking Trend: Increased engagement in culinary activities at home.

- Technological Innovations: Introduction of smart features, advanced materials, and improved performance.

- Economic Growth & Disposable Income: Higher spending power enabling purchases of premium kitchenware.

- Health & Sustainability Focus: Demand for non-toxic, eco-friendly, and durable products.

Obstacles in the European Kitchenware Industry Market

Despite robust growth, the European kitchenware industry faces several obstacles. Intensifying competition from both established brands and emerging online retailers, particularly those offering lower price points, puts pressure on profit margins. Fluctuations in raw material prices, such as the cost of stainless steel and aluminum, can significantly impact manufacturing costs and product pricing. Stringent EU regulations concerning product safety, material sourcing, and environmental impact, while ensuring quality, can also increase compliance costs and slow down product development. Furthermore, supply chain disruptions, as experienced in recent years, can lead to delays in production and delivery, affecting market availability. The economic uncertainty in some European regions can also dampen consumer spending on non-essential items. Quantifiable impacts include potential increases of up to 10% in production costs due to raw material price volatility.

- Intense Competition: Price wars and market saturation from numerous players.

- Raw Material Price Volatility: Unpredictable costs impacting manufacturing and retail prices.

- Regulatory Compliance Burden: Increased costs and time for meeting EU standards.

- Supply Chain Vulnerabilities: Potential for delays and shortages affecting product availability.

- Economic Uncertainty: Dampened consumer spending on discretionary kitchenware.

Future Opportunities in European Kitchenware Industry

The European kitchenware industry is poised for significant future opportunities. The growing demand for smart kitchen appliances and integrated technology presents a major avenue for innovation and market penetration. The increasing consumer preference for sustainable and eco-friendly products opens doors for brands focusing on recycled materials, biodegradable components, and ethical production practices. Expansion into emerging markets within Eastern Europe offers untapped potential for growth. Furthermore, the rise of personalized and artisanal kitchenware caters to niche consumer segments seeking unique and high-quality items. The growth of online direct-to-consumer (DTC) sales channels continues to provide opportunities for brands to build direct relationships with customers and control their brand narrative. The market size for smart kitchenware is projected to reach over 5 billion Euros by 2033.

- Smart Kitchen Technology Integration: Development and adoption of connected kitchenware.

- Sustainable & Eco-Friendly Products: Focus on recycled materials, energy efficiency, and ethical sourcing.

- Emerging European Markets: Expansion into regions with growing consumer bases.

- Personalized & Artisanal Offerings: Catering to niche markets with unique products.

- Direct-to-Consumer (DTC) Channel Growth: Leveraging online platforms for direct sales and customer engagement.

Major Players in the European Kitchenware Industry Ecosystem

- Uno Casa

- Viking Cookware

- Cuisinart

- Le Creuset

- Bialetti

- Abbio

- Calphalon

- All-Clad

Key Developments in European Kitchenware Industry Industry

- February 2023: Crucible Cookware, a leading manufacturer and supplier of high-quality kitchenware, announced it had signed a contract with DHL for shipping its products within the European Union (EU). DHL is one of the leading logistics companies. This new partnership will allow Crucible Cookware to provide its customers with faster and more efficient shipping options for their orders. This development is expected to enhance customer satisfaction and streamline logistics for Crucible Cookware, potentially increasing its market competitiveness within the EU.

- February 2023: A new range of bakeware with a reduced environmental impact is launched by market leader Guardini. They partnered with ArcelorMittal, one of the leading steel and mining companies, coated steel manufacturer Cooper Coated Coil (CCC), and coatings manufacturer ILAG. This initiative by Guardini highlights the growing industry trend towards sustainability, showcasing a collaborative effort to produce eco-conscious kitchenware.

Strategic European Kitchenware Industry Market Forecast

The strategic forecast for the European kitchenware industry is exceptionally promising, driven by a confluence of evolving consumer behaviors and technological advancements. The persistent growth in home cooking, coupled with an increasing demand for high-performance, durable, and aesthetically pleasing kitchen tools, forms the bedrock of this positive outlook. Innovation in smart kitchen technology and sustainable materials will unlock new market segments and capture the interest of eco-conscious consumers. The Forecast Period (2025–2033) is expected to witness substantial growth, with opportunities arising from expanding distribution channels, particularly online, and the continued exploration of premium product offerings. The market size is projected to reach over 40 billion Euros by 2033, indicating a strong CAGR of approximately 6.5%.

European Kitchenware Industry Segmentation

-

1. Product

- 1.1. Pots and Pans

- 1.2. Cooking Racks

- 1.3. Cooking Tools

- 1.4. Microwave Cookware

- 1.5. Pressure Cookers

-

2. Material

- 2.1. Stainless Steel

- 2.2. Aluminium

- 2.3. Glass

- 2.4. Other Materials

-

3. Distribution Channel

- 3.1. Hypermarkets and Supermarkets

- 3.2. Specialty Store

- 3.3. Online

- 3.4. Other Distribution Channels

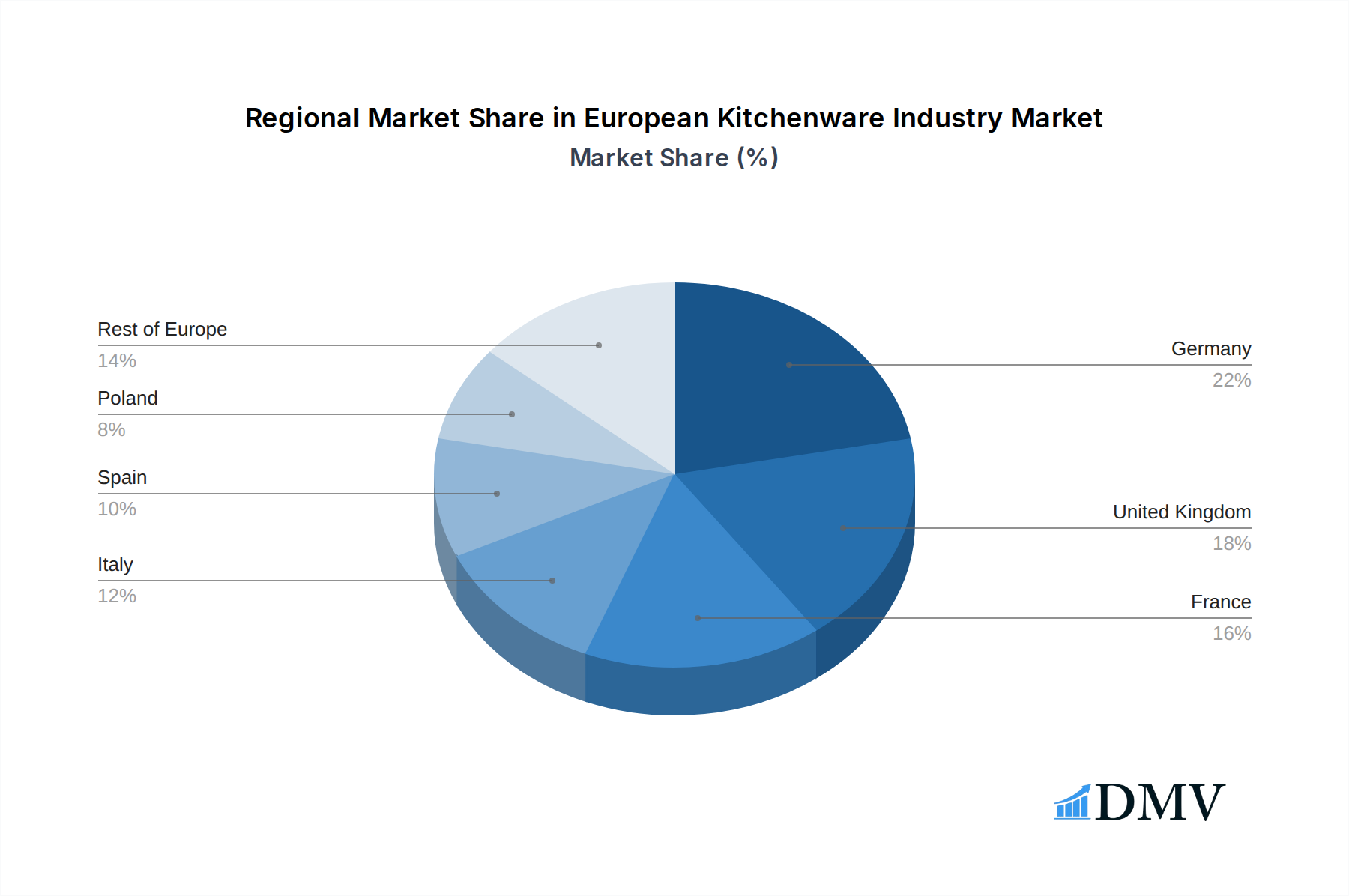

European Kitchenware Industry Segmentation By Geography

- 1. Germany

- 2. United Kingdom

- 3. France

- 4. Poland

- 5. Italy

- 6. Rest of Europe

European Kitchenware Industry Regional Market Share

Geographic Coverage of European Kitchenware Industry

European Kitchenware Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.17% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Pots and Pans

- 5.1.2. Cooking Racks

- 5.1.3. Cooking Tools

- 5.1.4. Microwave Cookware

- 5.1.5. Pressure Cookers

- 5.2. Market Analysis, Insights and Forecast - by Material

- 5.2.1. Stainless Steel

- 5.2.2. Aluminium

- 5.2.3. Glass

- 5.2.4. Other Materials

- 5.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.3.1. Hypermarkets and Supermarkets

- 5.3.2. Specialty Store

- 5.3.3. Online

- 5.3.4. Other Distribution Channels

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Germany

- 5.4.2. United Kingdom

- 5.4.3. France

- 5.4.4. Poland

- 5.4.5. Italy

- 5.4.6. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. European Kitchenware Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product

- 6.1.1. Pots and Pans

- 6.1.2. Cooking Racks

- 6.1.3. Cooking Tools

- 6.1.4. Microwave Cookware

- 6.1.5. Pressure Cookers

- 6.2. Market Analysis, Insights and Forecast - by Material

- 6.2.1. Stainless Steel

- 6.2.2. Aluminium

- 6.2.3. Glass

- 6.2.4. Other Materials

- 6.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.3.1. Hypermarkets and Supermarkets

- 6.3.2. Specialty Store

- 6.3.3. Online

- 6.3.4. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Product

- 7. Germany European Kitchenware Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product

- 7.1.1. Pots and Pans

- 7.1.2. Cooking Racks

- 7.1.3. Cooking Tools

- 7.1.4. Microwave Cookware

- 7.1.5. Pressure Cookers

- 7.2. Market Analysis, Insights and Forecast - by Material

- 7.2.1. Stainless Steel

- 7.2.2. Aluminium

- 7.2.3. Glass

- 7.2.4. Other Materials

- 7.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.3.1. Hypermarkets and Supermarkets

- 7.3.2. Specialty Store

- 7.3.3. Online

- 7.3.4. Other Distribution Channels

- 7.1. Market Analysis, Insights and Forecast - by Product

- 8. United Kingdom European Kitchenware Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product

- 8.1.1. Pots and Pans

- 8.1.2. Cooking Racks

- 8.1.3. Cooking Tools

- 8.1.4. Microwave Cookware

- 8.1.5. Pressure Cookers

- 8.2. Market Analysis, Insights and Forecast - by Material

- 8.2.1. Stainless Steel

- 8.2.2. Aluminium

- 8.2.3. Glass

- 8.2.4. Other Materials

- 8.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.3.1. Hypermarkets and Supermarkets

- 8.3.2. Specialty Store

- 8.3.3. Online

- 8.3.4. Other Distribution Channels

- 8.1. Market Analysis, Insights and Forecast - by Product

- 9. France European Kitchenware Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product

- 9.1.1. Pots and Pans

- 9.1.2. Cooking Racks

- 9.1.3. Cooking Tools

- 9.1.4. Microwave Cookware

- 9.1.5. Pressure Cookers

- 9.2. Market Analysis, Insights and Forecast - by Material

- 9.2.1. Stainless Steel

- 9.2.2. Aluminium

- 9.2.3. Glass

- 9.2.4. Other Materials

- 9.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.3.1. Hypermarkets and Supermarkets

- 9.3.2. Specialty Store

- 9.3.3. Online

- 9.3.4. Other Distribution Channels

- 9.1. Market Analysis, Insights and Forecast - by Product

- 10. Poland European Kitchenware Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product

- 10.1.1. Pots and Pans

- 10.1.2. Cooking Racks

- 10.1.3. Cooking Tools

- 10.1.4. Microwave Cookware

- 10.1.5. Pressure Cookers

- 10.2. Market Analysis, Insights and Forecast - by Material

- 10.2.1. Stainless Steel

- 10.2.2. Aluminium

- 10.2.3. Glass

- 10.2.4. Other Materials

- 10.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.3.1. Hypermarkets and Supermarkets

- 10.3.2. Specialty Store

- 10.3.3. Online

- 10.3.4. Other Distribution Channels

- 10.1. Market Analysis, Insights and Forecast - by Product

- 11. Italy European Kitchenware Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product

- 11.1.1. Pots and Pans

- 11.1.2. Cooking Racks

- 11.1.3. Cooking Tools

- 11.1.4. Microwave Cookware

- 11.1.5. Pressure Cookers

- 11.2. Market Analysis, Insights and Forecast - by Material

- 11.2.1. Stainless Steel

- 11.2.2. Aluminium

- 11.2.3. Glass

- 11.2.4. Other Materials

- 11.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.3.1. Hypermarkets and Supermarkets

- 11.3.2. Specialty Store

- 11.3.3. Online

- 11.3.4. Other Distribution Channels

- 11.1. Market Analysis, Insights and Forecast - by Product

- 12. Rest of Europe European Kitchenware Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Product

- 12.1.1. Pots and Pans

- 12.1.2. Cooking Racks

- 12.1.3. Cooking Tools

- 12.1.4. Microwave Cookware

- 12.1.5. Pressure Cookers

- 12.2. Market Analysis, Insights and Forecast - by Material

- 12.2.1. Stainless Steel

- 12.2.2. Aluminium

- 12.2.3. Glass

- 12.2.4. Other Materials

- 12.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 12.3.1. Hypermarkets and Supermarkets

- 12.3.2. Specialty Store

- 12.3.3. Online

- 12.3.4. Other Distribution Channels

- 12.1. Market Analysis, Insights and Forecast - by Product

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Uno Casa**List Not Exhaustive

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Viking Cookware

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Cuisinart

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Le Creuset

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Bialetti

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Abbio

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Calphalon

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 All-Clad

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.1 Uno Casa**List Not Exhaustive

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: European Kitchenware Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: European Kitchenware Industry Share (%) by Company 2025

List of Tables

- Table 1: European Kitchenware Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 2: European Kitchenware Industry Revenue Million Forecast, by Material 2020 & 2033

- Table 3: European Kitchenware Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 4: European Kitchenware Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: European Kitchenware Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 6: European Kitchenware Industry Revenue Million Forecast, by Material 2020 & 2033

- Table 7: European Kitchenware Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 8: European Kitchenware Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: European Kitchenware Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 10: European Kitchenware Industry Revenue Million Forecast, by Material 2020 & 2033

- Table 11: European Kitchenware Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 12: European Kitchenware Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: European Kitchenware Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 14: European Kitchenware Industry Revenue Million Forecast, by Material 2020 & 2033

- Table 15: European Kitchenware Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 16: European Kitchenware Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 17: European Kitchenware Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 18: European Kitchenware Industry Revenue Million Forecast, by Material 2020 & 2033

- Table 19: European Kitchenware Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 20: European Kitchenware Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 21: European Kitchenware Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 22: European Kitchenware Industry Revenue Million Forecast, by Material 2020 & 2033

- Table 23: European Kitchenware Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 24: European Kitchenware Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 25: European Kitchenware Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 26: European Kitchenware Industry Revenue Million Forecast, by Material 2020 & 2033

- Table 27: European Kitchenware Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 28: European Kitchenware Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the European Kitchenware Industry?

The projected CAGR is approximately 3.17%.

2. Which companies are prominent players in the European Kitchenware Industry?

Key companies in the market include Uno Casa**List Not Exhaustive, Viking Cookware, Cuisinart, Le Creuset, Bialetti, Abbio, Calphalon, All-Clad.

3. What are the main segments of the European Kitchenware Industry?

The market segments include Product, Material, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 4.04 Million as of 2022.

5. What are some drivers contributing to market growth?

Rise in Household Disposable Income; Rise in Sales of Washing Machines and Refrigerators.

6. What are the notable trends driving market growth?

Non-Stick Cookware is Dominating the Cookware Industry.

7. Are there any restraints impacting market growth?

Increase in Price of Major Appliances Post Covid; Supply Chain Disruptions in Market with Rising Geopolitical Issues.

8. Can you provide examples of recent developments in the market?

February 2023: Crucible Cookware, a leading manufacturer and supplier of high-quality kitchenware, announced it had signed a contract with DHL for shipping its products within the European Union (EU). DHL is one of the leading logistics companies. This new partnership will allow Crucible Cookware to provide its customers with faster and more efficient shipping options for their orders.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "European Kitchenware Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the European Kitchenware Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the European Kitchenware Industry?

To stay informed about further developments, trends, and reports in the European Kitchenware Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence