Key Insights

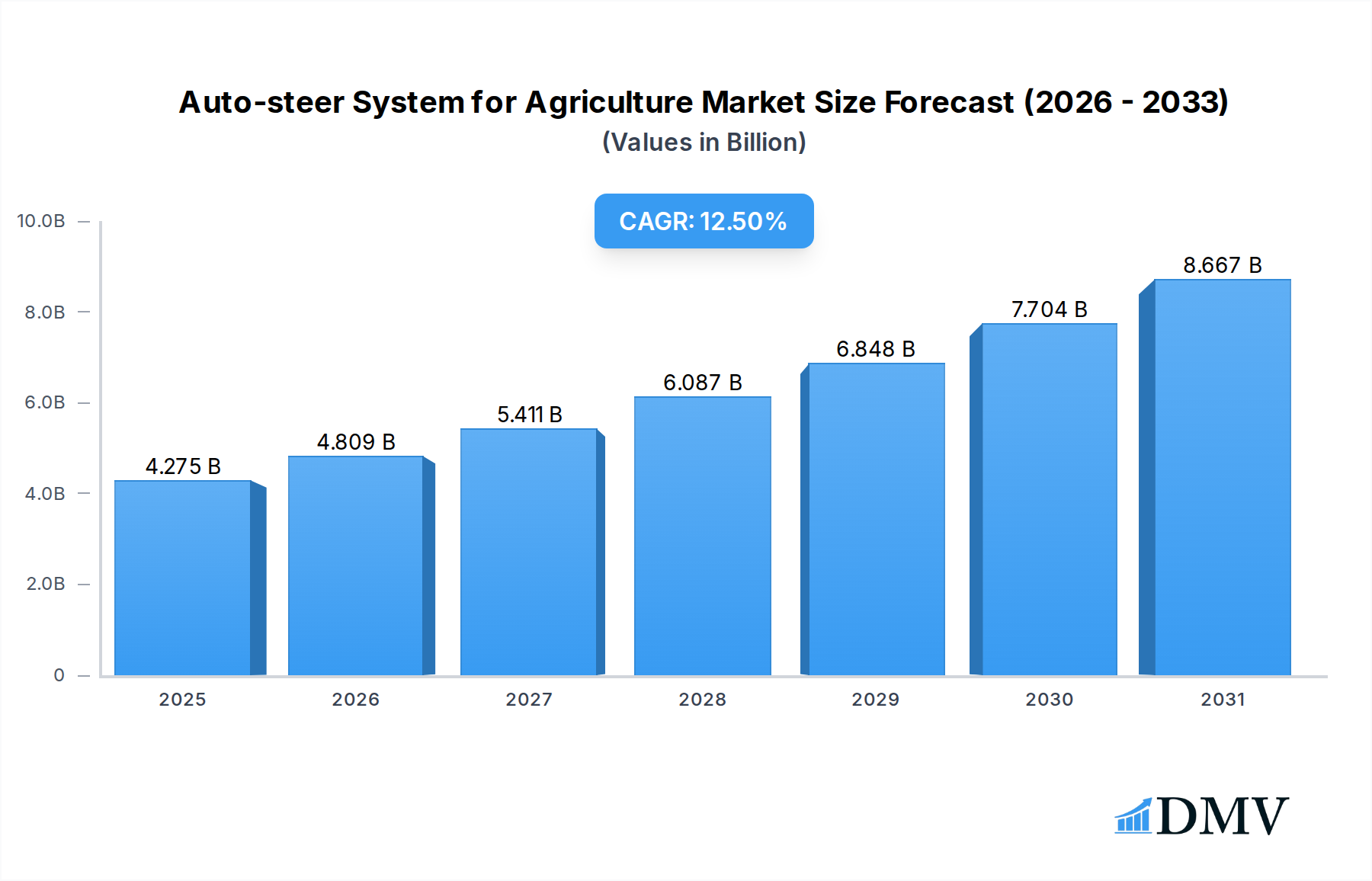

The Auto-steer System for Agriculture Market is poised for robust expansion, driven by the escalating demand for operational efficiency, enhanced precision, and sustainable farming practices globally. Valued at $3.8 billion in 2024, the market is projected to reach approximately $12.34 billion by 2034, demonstrating an impressive Compound Annual Growth Rate (CAGR) of 12.5% during the forecast period. This significant growth trajectory is underpinned by several macro tailwinds, including increasing labor shortages in the agricultural sector, the imperative to maximize land productivity, and the ongoing technological advancements transforming traditional farming.

Auto-steer System for Agriculture Market Size (In Billion)

The integration of sophisticated GNSS-based systems, RTK guidance, and sensor fusion technologies is enabling farmers to achieve sub-inch accuracy in field operations, leading to reduced input costs (fuel, seeds, fertilizers, pesticides) and improved crop yields. The overarching trend towards a more digitized and automated agricultural landscape is a primary catalyst. Furthermore, government initiatives and subsidies promoting modern farming techniques, coupled with rising awareness among farmers regarding the long-term economic and environmental benefits of precision agriculture, are fueling adoption. The evolving landscape of the Precision Agriculture Market is directly benefiting auto-steer system manufacturers as farmers seek integrated solutions.

Auto-steer System for Agriculture Company Market Share

Key demand drivers include the growing adoption of farm mechanization across developing economies, driven by population growth and food security concerns. The aftermarket segment is also experiencing strong growth, as farmers upgrade existing fleets with auto-steer capabilities, signaling a clear shift towards technology-driven farming. Despite high initial investment costs and the need for skilled operators, the compelling return on investment through optimized resource utilization and yield enhancement continues to drive market penetration. The continuous innovation in sensor technology, artificial intelligence, and real-time data analytics is expected to further refine auto-steer system functionalities, broadening their applicability across diverse crop types and farm sizes. This dynamic environment suggests sustained growth and technological evolution within the Auto-steer System for Agriculture Market over the next decade.

Hardware Component Dominance in Auto-steer System for Agriculture Market

The Hardware component segment is identified as the largest contributor to revenue within the Auto-steer System for Agriculture Market, a trend anticipated to continue throughout the forecast period. This dominance stems from the foundational necessity and inherent value of physical components that enable autonomous steering capabilities. Hardware encompasses critical elements such as GPS/GNSS Receivers, Steering Controllers, Sensors, Displays & Monitors, and Antennas. Each of these components represents a significant capital outlay and is indispensable for the functionality, accuracy, and reliability of an auto-steer system.

GPS/GNSS Receivers form the core of any auto-steer system, providing the precise positioning data essential for navigation. The increasing sophistication of these receivers, incorporating multi-frequency and multi-constellation capabilities to enhance accuracy and robustness in challenging environments, contributes significantly to their market value. The evolution from basic DGPS to highly accurate RTK-guided systems has further solidified the premium pricing and indispensable nature of these components. Leading players in this sub-segment include Trimble, Topcon Positioning Systems, and John Deere, who continuously invest in R&D to deliver cutting-edge GNSS Receivers Market solutions.

Steering Controllers are another vital hardware component, translating the positioning data into precise steering commands for the agricultural machinery. These controllers often incorporate advanced algorithms and processing capabilities to ensure smooth and accurate vehicle movement, minimizing overlaps and skips. Sensors, including gyroscopes, accelerometers, and various optical or ultrasonic sensors, play a crucial role in providing additional data for terrain compensation, obstacle detection, and implement control, thereby enhancing the overall performance and safety of the system. The rising adoption of Agricultural Sensors Market solutions contributes directly to the complexity and value of integrated hardware packages.

Displays & Monitors serve as the human-machine interface, allowing operators to visualize field maps, monitor system performance, and make adjustments. The trend towards larger, more intuitive touchscreens with advanced mapping and data logging capabilities further adds to the value of this hardware category. The cumulative cost of these sophisticated hardware elements, coupled with their long operational lifespan and the need for robustness in harsh agricultural environments, ensures that the Hardware segment maintains its leading revenue share. While software and service revenues are growing, the upfront investment in physical infrastructure remains the primary driver of market value, signifying the strategic importance of manufacturing and integrating high-quality hardware in the Auto-steer System for Agriculture Market.

Key Market Drivers and Constraints in Auto-steer System for Agriculture Market

The Auto-steer System for Agriculture Market's growth is primarily propelled by the critical need for enhanced operational efficiency and precision in farming, alongside significant economic and environmental pressures. A key driver is the global rising demand for food production due to an increasing population, which necessitates maximizing yield from existing arable land. Auto-steer systems contribute directly to this by reducing overlap and skips during planting, spraying, and harvesting, thereby optimizing input usage and improving crop uniformity. For instance, studies indicate that precision guidance can reduce fuel consumption by up to 12-15% and input waste by 5-10%.

Another significant driver is the escalating labor shortage in the agricultural sector across developed economies. Auto-steer systems automate a critical part of machine operation, reducing the need for highly skilled drivers for repetitive tasks and alleviating fatigue. This translates into increased operational hours and fewer human errors, making farming more sustainable with a smaller workforce. The increasing investment in the Agricultural Equipment Market to integrate such technologies reflects this trend.

Conversely, several constraints temper the market's full potential. The high initial investment cost associated with auto-steer systems remains a significant barrier for many individual farmers and smaller agricultural enterprises. A complete RTK-guided auto-steer system can cost upwards of $15,000-$30,000, which is a substantial outlay, particularly in regions with lower profit margins or limited access to credit. This financial hurdle often limits adoption to larger commercial farming enterprises or those with government subsidies.

Furthermore, technical complexities and the need for skilled operators to set up, calibrate, and troubleshoot these advanced systems present a challenge. While auto-steer simplifies driving, the underlying technology requires a certain level of technical proficiency. Issues related to interoperability between different manufacturers' equipment and software platforms can also hinder seamless integration and adoption. The nascent stage of the Agricultural Robotics Market adoption also means infrastructure for fully autonomous operations is still developing, which can constrain immediate widespread deployment of advanced auto-steer functionalities.

Supply Chain & Raw Material Dynamics for Auto-steer System for Agriculture Market

The supply chain for the Auto-steer System for Agriculture Market is complex, characterized by global dependencies on various electronic components, precise manufacturing processes, and specialized software development. Upstream dependencies primarily include manufacturers of high-precision electronic components such as semiconductors, microcontrollers, GPS/GNSS chipsets, and various types of sensors. The market also relies on suppliers of specialized materials for robust enclosures and cabling, designed to withstand harsh agricultural environments. The global semiconductor shortage experienced in 2020-2022 notably impacted the production timelines and costs of auto-steer systems, demonstrating the vulnerability of this supply chain to disruptions in critical component manufacturing.

Sourcing risks are prevalent due to the concentrated nature of semiconductor manufacturing in a few regions, particularly East Asia. Geopolitical tensions, trade disputes, and natural disasters in these regions can significantly impede the flow of components, leading to price volatility and extended lead times. For instance, the price of specialized silicon wafers, a fundamental raw material for chipsets, has seen upward trends, directly influencing the final cost of GNSS Receivers Market products and steering controllers.

Key inputs include rare earth elements for magnets in electric motors (used in some steering actuators), copper for wiring and circuit boards, and various polymers and alloys for system casings and mounting hardware. Price volatility for these commodities, influenced by global industrial demand, mining output, and energy costs, directly affects the manufacturing expenses. For example, fluctuations in copper prices, which have seen a general upward trend over the past few years, translate into higher production costs for wiring harnesses and connectors within auto-steer systems.

Historically, supply chain disruptions have led to production delays, increased inventory holding costs, and sometimes forced manufacturers to re-engineer products to accommodate alternative components. This market is increasingly focusing on building more resilient and diversified supply chains, including regional sourcing strategies and deeper collaboration with key component suppliers to mitigate future risks and maintain consistent product availability in the demanding Smart Farming Market.

Regulatory & Policy Landscape Shaping Auto-steer System for Agriculture Market

The Auto-steer System for Agriculture Market is influenced by a complex web of regulatory frameworks, standards, and government policies across key geographies. These regulations primarily focus on spectrum allocation for GNSS/RTK systems, safety standards for autonomous agricultural machinery, and data privacy for precision farming data. Globally, bodies like the International Organization for Standardization (ISO) establish standards for agricultural machinery safety, notably ISO 18497 for Safety of Operator Presence Detection Systems, which indirectly impacts the design and implementation of auto-steer systems as they evolve towards higher levels of autonomy.

In North America, the Federal Communications Commission (FCC) in the United States and Innovation, Science and Economic Development Canada (ISED) manage radio spectrum, ensuring that GNSS and RTK correction signals operate without interference. Recent policy discussions revolve around the use of C-band spectrum for 5G, which requires careful management to avoid interference with GPS signals, crucial for the reliable operation of auto-steer systems. State-level regulations also vary concerning the use of autonomous vehicles on public roads, though agricultural auto-steer systems primarily operate off-road. The Commercial Agriculture Market in North America benefits from incentives promoting sustainable practices, which indirectly boost auto-steer adoption.

In Europe, the EU Machinery Directive (2006/42/EC) sets essential health and safety requirements for machinery, including tractors and agricultural equipment. As auto-steer systems approach full autonomy, these directives will necessitate rigorous testing and certification processes. The European Union Agency for the Space Programme (EUSPA), managing Galileo, also plays a role in promoting GNSS adoption and developing standards. Policies related to the Common Agricultural Policy (CAP), with its emphasis on environmental sustainability and digital farming, often include subsidies or funding opportunities that can incentivize farmers to invest in precision technologies, including auto-steer systems.

Recent policy changes are increasingly focusing on data governance and privacy, particularly with the growth of connected farm equipment and Farm Management Software Market integration. Regulations like GDPR in Europe set precedents for how agricultural data, including field data collected by auto-steer systems, must be handled. This necessitates manufacturers and software providers to build robust data security and privacy features into their offerings. The regulatory landscape is continuously evolving as the technology advances, pushing towards clearer guidelines for fully autonomous agricultural operations and the safety implications thereof.

Competitive Ecosystem of Auto-steer System for Agriculture Market

The Auto-steer System for Agriculture Market is characterized by a mix of established agricultural machinery giants, specialized precision agriculture technology providers, and emerging innovators. Competition revolves around accuracy, integration capabilities, ease of use, and after-sales support.

- John Deere: A global leader in agricultural machinery, John Deere offers integrated auto-steer solutions through its StarFire receivers and AutoTrac guidance systems, deeply integrated into its extensive tractor and harvester lines, emphasizing seamless connectivity and data management within its ecosystem.

- Trimble: A pioneering force in positioning technologies, Trimble provides a comprehensive portfolio of GNSS-based auto-steer systems, including its TMX-2050 display and Autopilot steering system, serving a wide range of agricultural equipment brands through both OEM and aftermarket channels.

- Topcon Positioning Systems: Known for its advanced GNSS and optical positioning solutions, Topcon offers robust auto-steer systems like the AES-35 electric steering system and XD displays, catering to precision farming applications with a focus on high accuracy and reliability.

- Ag Leader Technology: A prominent independent provider of precision farming solutions, Ag Leader offers its SteerCommand auto-steer system, often lauded for its user-friendly interface and compatibility with diverse equipment brands, alongside comprehensive data management platforms.

- Raven Industries: Specializing in application control and precision agriculture, Raven provides auto-steer technology such as the RS1 and CR7/CR12 displays, focusing on improving the efficiency and accuracy of spraying, spreading, and planting operations.

- AgJunction: A pure-play provider of agricultural guidance and auto-steer solutions, AgJunction (now part of Kubota) develops software and hardware platforms for machine control, emphasizing open architecture and OEM partnerships for broad market reach.

- CNH Industrial: Parent company of brands like Case IH and New Holland, CNH Industrial integrates its own FMX and IntelliSteer auto-steer systems directly into its machinery, offering factory-fitted precision solutions designed for optimal performance with their equipment.

- AGCO Corporation: Manufacturer of Fendt, Massey Ferguson, and Valtra, AGCO provides its Fuse Technologies platform, which includes NovAtel-powered auto-steer systems, emphasizing connectivity and open approach to precision agriculture solutions.

- Hexagon Agriculture: A division of Hexagon AB, it offers a range of precision agriculture solutions, including auto-steer systems and software, leveraging its expertise in geospatial technology to provide accurate and efficient farming tools.

- FJDynamics: An emerging player, FJDynamics offers cost-effective auto-steer and intelligent farming solutions, focusing on expanding access to precision agriculture technology, particularly in developing markets and for smaller farms.

Recent Developments & Milestones in Auto-steer System for Agriculture Market

March 2024: John Deere unveiled enhancements to its AutoTrac guidance systems, including new features for improved headland turn performance and greater precision in uneven terrain, reflecting ongoing innovation in core auto-steer capabilities. January 2024: Trimble announced a partnership with a major agricultural OEM to integrate its advanced GNSS Receivers Market and steering control technology into new lines of tractors, expanding its OEM presence and market reach. November 2023: Topcon Positioning Systems launched its next-generation AGI-4 receiver and steering controller, featuring enhanced RTK performance and a more robust design for challenging agricultural environments, targeting increased accuracy and reliability. September 2023: Ag Leader Technology introduced new software updates for its SteerCommand system, improving compatibility with a wider range of implements and offering more intuitive user interfaces, aiming to enhance the user experience and expand interoperability. July 2023: Raven Industries acquired an AI-driven vision technology startup to integrate advanced perception capabilities into its auto-steer and application control systems, signaling a move towards more intelligent and autonomous farming solutions within the Agricultural Robotics Market. May 2023: CNH Industrial announced significant investments in its precision technology development centers, focusing on accelerating the integration of advanced auto-steer, telematics, and data analytics into its Case IH and New Holland machinery. February 2023: AGCO Corporation expanded its offerings within the Smart Farming Market by introducing new subscription-based services for its Fuse Technologies platform, providing farmers with access to enhanced auto-steer features and data management tools on a flexible model. December 2022: FJDynamics formed strategic alliances with several regional distributors in Asia Pacific to expand the availability and support for its auto-steer kits, particularly targeting small to medium-sized farms in rapidly mechanizing regions.

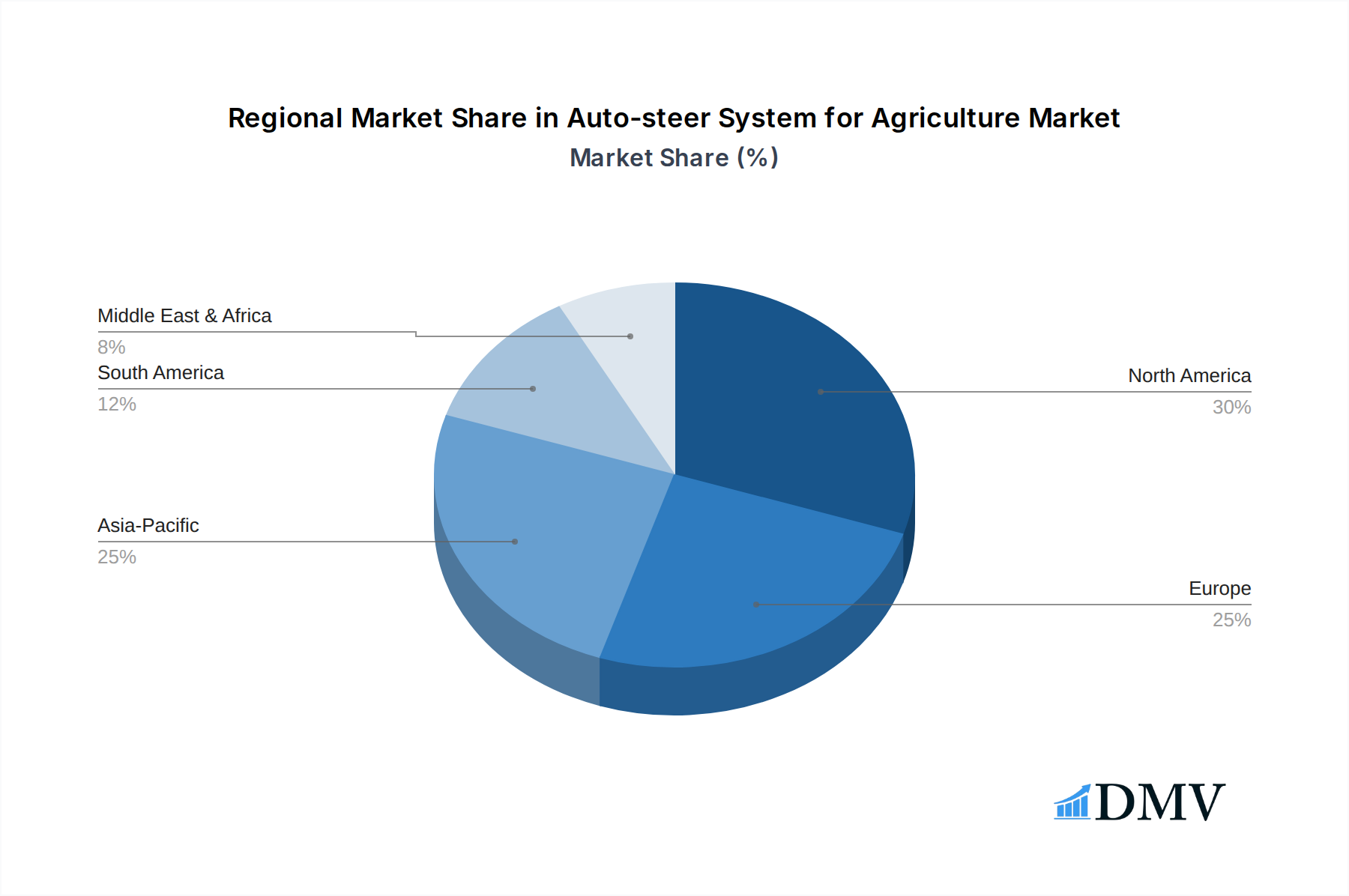

Regional Market Breakdown for Auto-steer System for Agriculture Market

The Auto-steer System for Agriculture Market exhibits distinct regional dynamics, influenced by varying levels of agricultural mechanization, farm sizes, technological adoption rates, and government support. North America, comprising the United States, Canada, and Mexico, currently holds the largest revenue share and is a mature market, driven by large-scale commercial farming enterprises that readily adopt precision agriculture technologies to optimize vast land areas. The demand in this region is propelled by a continued focus on maximizing yield, reducing input costs, and addressing labor shortages, with a strong presence of key players and an established distribution network for the Agricultural Equipment Market.

Europe also represents a significant share of the market, characterized by advanced farming practices, stringent environmental regulations, and supportive agricultural policies. Countries like Germany, France, and the UK are at the forefront of adopting auto-steer systems, driven by the need for sustainable farming and efficiency gains. The region demonstrates a steady CAGR, benefiting from early adoption and ongoing integration of smart farming solutions, particularly those offering environmental benefits.

Asia Pacific is projected to be the fastest-growing region in the Auto-steer System for Agriculture Market during the forecast period. This rapid expansion is primarily fueled by increasing mechanization in countries like China, India, and ASEAN nations, where governments are actively promoting modern farming techniques to enhance food security and improve agricultural productivity. The substantial number of small and medium-sized farms in the region presents a large untapped market, with rising disposable incomes and government subsidies making auto-steer systems more accessible. This region is seeing significant growth in demand for both OEM and aftermarket solutions, with a strong emphasis on cost-effective and easy-to-implement technologies.

South America, particularly Brazil and Argentina, also shows promising growth. These nations possess vast agricultural lands and are major global food producers. The increasing scale of farm operations and the desire to remain competitive on the global stage are driving the adoption of precision agriculture tools, including auto-steer systems. While market maturity is behind North America and Europe, the region’s high growth CAGR indicates substantial future potential.

The Middle East & Africa (MEA) region, while currently holding a smaller share, is expected to grow steadily. Initiatives to enhance food security, optimize water usage in arid regions, and modernize agricultural practices are creating opportunities for auto-steer system adoption. However, challenges such as limited infrastructure and higher initial investment costs temper its growth rate compared to other regions.

Auto-steer System for Agriculture Regional Market Share

Auto-steer System for Agriculture Segmentation

-

1. Component

-

1.1. Hardware

- 1.1.1. GPS/GNSS Receivers

- 1.1.2. Steering Controllers

- 1.1.3. Sensors

- 1.1.4. Displays & Monitors

- 1.1.5. Antennas

- 1.1.6. Others

- 1.2. Software

-

1.1. Hardware

-

2. Technology

- 2.1. GNSS-Based

- 2.2. RTK-Guided

- 2.3. Satellite-Based

- 2.4. Others

-

3. Vehicle Type

- 3.1. Tractors

- 3.2. Harvesters

- 3.3. Sprayers

- 3.4. Seeders & Planters

- 3.5. Others

-

4. Sales Channel

- 4.1. OEM

- 4.2. Aftermarket

-

5. End User

- 5.1. Individual Farmers

- 5.2. Commercial Farming Enterprises

- 5.3. Agricultural Cooperatives

- 5.4. Others

Auto-steer System for Agriculture Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Auto-steer System for Agriculture Regional Market Share

Geographic Coverage of Auto-steer System for Agriculture

Auto-steer System for Agriculture REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Component

- 5.1.1. Hardware

- 5.1.1.1. GPS/GNSS Receivers

- 5.1.1.2. Steering Controllers

- 5.1.1.3. Sensors

- 5.1.1.4. Displays & Monitors

- 5.1.1.5. Antennas

- 5.1.1.6. Others

- 5.1.2. Software

- 5.1.1. Hardware

- 5.2. Market Analysis, Insights and Forecast - by Technology

- 5.2.1. GNSS-Based

- 5.2.2. RTK-Guided

- 5.2.3. Satellite-Based

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.3.1. Tractors

- 5.3.2. Harvesters

- 5.3.3. Sprayers

- 5.3.4. Seeders & Planters

- 5.3.5. Others

- 5.4. Market Analysis, Insights and Forecast - by Sales Channel

- 5.4.1. OEM

- 5.4.2. Aftermarket

- 5.5. Market Analysis, Insights and Forecast - by End User

- 5.5.1. Individual Farmers

- 5.5.2. Commercial Farming Enterprises

- 5.5.3. Agricultural Cooperatives

- 5.5.4. Others

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. North America

- 5.6.2. South America

- 5.6.3. Europe

- 5.6.4. Middle East & Africa

- 5.6.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Component

- 6. Global Auto-steer System for Agriculture Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Component

- 6.1.1. Hardware

- 6.1.1.1. GPS/GNSS Receivers

- 6.1.1.2. Steering Controllers

- 6.1.1.3. Sensors

- 6.1.1.4. Displays & Monitors

- 6.1.1.5. Antennas

- 6.1.1.6. Others

- 6.1.2. Software

- 6.1.1. Hardware

- 6.2. Market Analysis, Insights and Forecast - by Technology

- 6.2.1. GNSS-Based

- 6.2.2. RTK-Guided

- 6.2.3. Satellite-Based

- 6.2.4. Others

- 6.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.3.1. Tractors

- 6.3.2. Harvesters

- 6.3.3. Sprayers

- 6.3.4. Seeders & Planters

- 6.3.5. Others

- 6.4. Market Analysis, Insights and Forecast - by Sales Channel

- 6.4.1. OEM

- 6.4.2. Aftermarket

- 6.5. Market Analysis, Insights and Forecast - by End User

- 6.5.1. Individual Farmers

- 6.5.2. Commercial Farming Enterprises

- 6.5.3. Agricultural Cooperatives

- 6.5.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Component

- 7. North America Auto-steer System for Agriculture Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Component

- 7.1.1. Hardware

- 7.1.1.1. GPS/GNSS Receivers

- 7.1.1.2. Steering Controllers

- 7.1.1.3. Sensors

- 7.1.1.4. Displays & Monitors

- 7.1.1.5. Antennas

- 7.1.1.6. Others

- 7.1.2. Software

- 7.1.1. Hardware

- 7.2. Market Analysis, Insights and Forecast - by Technology

- 7.2.1. GNSS-Based

- 7.2.2. RTK-Guided

- 7.2.3. Satellite-Based

- 7.2.4. Others

- 7.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 7.3.1. Tractors

- 7.3.2. Harvesters

- 7.3.3. Sprayers

- 7.3.4. Seeders & Planters

- 7.3.5. Others

- 7.4. Market Analysis, Insights and Forecast - by Sales Channel

- 7.4.1. OEM

- 7.4.2. Aftermarket

- 7.5. Market Analysis, Insights and Forecast - by End User

- 7.5.1. Individual Farmers

- 7.5.2. Commercial Farming Enterprises

- 7.5.3. Agricultural Cooperatives

- 7.5.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Component

- 8. South America Auto-steer System for Agriculture Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Component

- 8.1.1. Hardware

- 8.1.1.1. GPS/GNSS Receivers

- 8.1.1.2. Steering Controllers

- 8.1.1.3. Sensors

- 8.1.1.4. Displays & Monitors

- 8.1.1.5. Antennas

- 8.1.1.6. Others

- 8.1.2. Software

- 8.1.1. Hardware

- 8.2. Market Analysis, Insights and Forecast - by Technology

- 8.2.1. GNSS-Based

- 8.2.2. RTK-Guided

- 8.2.3. Satellite-Based

- 8.2.4. Others

- 8.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 8.3.1. Tractors

- 8.3.2. Harvesters

- 8.3.3. Sprayers

- 8.3.4. Seeders & Planters

- 8.3.5. Others

- 8.4. Market Analysis, Insights and Forecast - by Sales Channel

- 8.4.1. OEM

- 8.4.2. Aftermarket

- 8.5. Market Analysis, Insights and Forecast - by End User

- 8.5.1. Individual Farmers

- 8.5.2. Commercial Farming Enterprises

- 8.5.3. Agricultural Cooperatives

- 8.5.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Component

- 9. Europe Auto-steer System for Agriculture Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Component

- 9.1.1. Hardware

- 9.1.1.1. GPS/GNSS Receivers

- 9.1.1.2. Steering Controllers

- 9.1.1.3. Sensors

- 9.1.1.4. Displays & Monitors

- 9.1.1.5. Antennas

- 9.1.1.6. Others

- 9.1.2. Software

- 9.1.1. Hardware

- 9.2. Market Analysis, Insights and Forecast - by Technology

- 9.2.1. GNSS-Based

- 9.2.2. RTK-Guided

- 9.2.3. Satellite-Based

- 9.2.4. Others

- 9.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 9.3.1. Tractors

- 9.3.2. Harvesters

- 9.3.3. Sprayers

- 9.3.4. Seeders & Planters

- 9.3.5. Others

- 9.4. Market Analysis, Insights and Forecast - by Sales Channel

- 9.4.1. OEM

- 9.4.2. Aftermarket

- 9.5. Market Analysis, Insights and Forecast - by End User

- 9.5.1. Individual Farmers

- 9.5.2. Commercial Farming Enterprises

- 9.5.3. Agricultural Cooperatives

- 9.5.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Component

- 10. Middle East & Africa Auto-steer System for Agriculture Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Component

- 10.1.1. Hardware

- 10.1.1.1. GPS/GNSS Receivers

- 10.1.1.2. Steering Controllers

- 10.1.1.3. Sensors

- 10.1.1.4. Displays & Monitors

- 10.1.1.5. Antennas

- 10.1.1.6. Others

- 10.1.2. Software

- 10.1.1. Hardware

- 10.2. Market Analysis, Insights and Forecast - by Technology

- 10.2.1. GNSS-Based

- 10.2.2. RTK-Guided

- 10.2.3. Satellite-Based

- 10.2.4. Others

- 10.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 10.3.1. Tractors

- 10.3.2. Harvesters

- 10.3.3. Sprayers

- 10.3.4. Seeders & Planters

- 10.3.5. Others

- 10.4. Market Analysis, Insights and Forecast - by Sales Channel

- 10.4.1. OEM

- 10.4.2. Aftermarket

- 10.5. Market Analysis, Insights and Forecast - by End User

- 10.5.1. Individual Farmers

- 10.5.2. Commercial Farming Enterprises

- 10.5.3. Agricultural Cooperatives

- 10.5.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Component

- 11. Asia Pacific Auto-steer System for Agriculture Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Component

- 11.1.1. Hardware

- 11.1.1.1. GPS/GNSS Receivers

- 11.1.1.2. Steering Controllers

- 11.1.1.3. Sensors

- 11.1.1.4. Displays & Monitors

- 11.1.1.5. Antennas

- 11.1.1.6. Others

- 11.1.2. Software

- 11.1.1. Hardware

- 11.2. Market Analysis, Insights and Forecast - by Technology

- 11.2.1. GNSS-Based

- 11.2.2. RTK-Guided

- 11.2.3. Satellite-Based

- 11.2.4. Others

- 11.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 11.3.1. Tractors

- 11.3.2. Harvesters

- 11.3.3. Sprayers

- 11.3.4. Seeders & Planters

- 11.3.5. Others

- 11.4. Market Analysis, Insights and Forecast - by Sales Channel

- 11.4.1. OEM

- 11.4.2. Aftermarket

- 11.5. Market Analysis, Insights and Forecast - by End User

- 11.5.1. Individual Farmers

- 11.5.2. Commercial Farming Enterprises

- 11.5.3. Agricultural Cooperatives

- 11.5.4. Others

- 11.1. Market Analysis, Insights and Forecast - by Component

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 John Deere

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Trimble

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Topcon Positioning Systems

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Ag Leader Technology

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Raven Industries

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 AgJunction

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Patchwork

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 CNH Industrial

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 AGCO Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 FieldBee

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 ARAG

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Homburg Holland

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Sveaverken Svea Agri

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Geometer International

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Hexagon Agriculture

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Reichhardt

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Rostselmash

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 FJDynamics

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 SMAJAYU(SHENZHEN)

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.20 ComNav Technology

- 12.1.20.1. Company Overview

- 12.1.20.2. Products

- 12.1.20.3. Company Financials

- 12.1.20.4. SWOT Analysis

- 12.1.21 CP Device

- 12.1.21.1. Company Overview

- 12.1.21.2. Products

- 12.1.21.3. Company Financials

- 12.1.21.4. SWOT Analysis

- 12.1.1 John Deere

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Auto-steer System for Agriculture Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Auto-steer System for Agriculture Revenue (billion), by Component 2025 & 2033

- Figure 3: North America Auto-steer System for Agriculture Revenue Share (%), by Component 2025 & 2033

- Figure 4: North America Auto-steer System for Agriculture Revenue (billion), by Technology 2025 & 2033

- Figure 5: North America Auto-steer System for Agriculture Revenue Share (%), by Technology 2025 & 2033

- Figure 6: North America Auto-steer System for Agriculture Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 7: North America Auto-steer System for Agriculture Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 8: North America Auto-steer System for Agriculture Revenue (billion), by Sales Channel 2025 & 2033

- Figure 9: North America Auto-steer System for Agriculture Revenue Share (%), by Sales Channel 2025 & 2033

- Figure 10: North America Auto-steer System for Agriculture Revenue (billion), by End User 2025 & 2033

- Figure 11: North America Auto-steer System for Agriculture Revenue Share (%), by End User 2025 & 2033

- Figure 12: North America Auto-steer System for Agriculture Revenue (billion), by Country 2025 & 2033

- Figure 13: North America Auto-steer System for Agriculture Revenue Share (%), by Country 2025 & 2033

- Figure 14: South America Auto-steer System for Agriculture Revenue (billion), by Component 2025 & 2033

- Figure 15: South America Auto-steer System for Agriculture Revenue Share (%), by Component 2025 & 2033

- Figure 16: South America Auto-steer System for Agriculture Revenue (billion), by Technology 2025 & 2033

- Figure 17: South America Auto-steer System for Agriculture Revenue Share (%), by Technology 2025 & 2033

- Figure 18: South America Auto-steer System for Agriculture Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 19: South America Auto-steer System for Agriculture Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 20: South America Auto-steer System for Agriculture Revenue (billion), by Sales Channel 2025 & 2033

- Figure 21: South America Auto-steer System for Agriculture Revenue Share (%), by Sales Channel 2025 & 2033

- Figure 22: South America Auto-steer System for Agriculture Revenue (billion), by End User 2025 & 2033

- Figure 23: South America Auto-steer System for Agriculture Revenue Share (%), by End User 2025 & 2033

- Figure 24: South America Auto-steer System for Agriculture Revenue (billion), by Country 2025 & 2033

- Figure 25: South America Auto-steer System for Agriculture Revenue Share (%), by Country 2025 & 2033

- Figure 26: Europe Auto-steer System for Agriculture Revenue (billion), by Component 2025 & 2033

- Figure 27: Europe Auto-steer System for Agriculture Revenue Share (%), by Component 2025 & 2033

- Figure 28: Europe Auto-steer System for Agriculture Revenue (billion), by Technology 2025 & 2033

- Figure 29: Europe Auto-steer System for Agriculture Revenue Share (%), by Technology 2025 & 2033

- Figure 30: Europe Auto-steer System for Agriculture Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 31: Europe Auto-steer System for Agriculture Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 32: Europe Auto-steer System for Agriculture Revenue (billion), by Sales Channel 2025 & 2033

- Figure 33: Europe Auto-steer System for Agriculture Revenue Share (%), by Sales Channel 2025 & 2033

- Figure 34: Europe Auto-steer System for Agriculture Revenue (billion), by End User 2025 & 2033

- Figure 35: Europe Auto-steer System for Agriculture Revenue Share (%), by End User 2025 & 2033

- Figure 36: Europe Auto-steer System for Agriculture Revenue (billion), by Country 2025 & 2033

- Figure 37: Europe Auto-steer System for Agriculture Revenue Share (%), by Country 2025 & 2033

- Figure 38: Middle East & Africa Auto-steer System for Agriculture Revenue (billion), by Component 2025 & 2033

- Figure 39: Middle East & Africa Auto-steer System for Agriculture Revenue Share (%), by Component 2025 & 2033

- Figure 40: Middle East & Africa Auto-steer System for Agriculture Revenue (billion), by Technology 2025 & 2033

- Figure 41: Middle East & Africa Auto-steer System for Agriculture Revenue Share (%), by Technology 2025 & 2033

- Figure 42: Middle East & Africa Auto-steer System for Agriculture Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 43: Middle East & Africa Auto-steer System for Agriculture Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 44: Middle East & Africa Auto-steer System for Agriculture Revenue (billion), by Sales Channel 2025 & 2033

- Figure 45: Middle East & Africa Auto-steer System for Agriculture Revenue Share (%), by Sales Channel 2025 & 2033

- Figure 46: Middle East & Africa Auto-steer System for Agriculture Revenue (billion), by End User 2025 & 2033

- Figure 47: Middle East & Africa Auto-steer System for Agriculture Revenue Share (%), by End User 2025 & 2033

- Figure 48: Middle East & Africa Auto-steer System for Agriculture Revenue (billion), by Country 2025 & 2033

- Figure 49: Middle East & Africa Auto-steer System for Agriculture Revenue Share (%), by Country 2025 & 2033

- Figure 50: Asia Pacific Auto-steer System for Agriculture Revenue (billion), by Component 2025 & 2033

- Figure 51: Asia Pacific Auto-steer System for Agriculture Revenue Share (%), by Component 2025 & 2033

- Figure 52: Asia Pacific Auto-steer System for Agriculture Revenue (billion), by Technology 2025 & 2033

- Figure 53: Asia Pacific Auto-steer System for Agriculture Revenue Share (%), by Technology 2025 & 2033

- Figure 54: Asia Pacific Auto-steer System for Agriculture Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 55: Asia Pacific Auto-steer System for Agriculture Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 56: Asia Pacific Auto-steer System for Agriculture Revenue (billion), by Sales Channel 2025 & 2033

- Figure 57: Asia Pacific Auto-steer System for Agriculture Revenue Share (%), by Sales Channel 2025 & 2033

- Figure 58: Asia Pacific Auto-steer System for Agriculture Revenue (billion), by End User 2025 & 2033

- Figure 59: Asia Pacific Auto-steer System for Agriculture Revenue Share (%), by End User 2025 & 2033

- Figure 60: Asia Pacific Auto-steer System for Agriculture Revenue (billion), by Country 2025 & 2033

- Figure 61: Asia Pacific Auto-steer System for Agriculture Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Auto-steer System for Agriculture Revenue billion Forecast, by Component 2020 & 2033

- Table 2: Global Auto-steer System for Agriculture Revenue billion Forecast, by Technology 2020 & 2033

- Table 3: Global Auto-steer System for Agriculture Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 4: Global Auto-steer System for Agriculture Revenue billion Forecast, by Sales Channel 2020 & 2033

- Table 5: Global Auto-steer System for Agriculture Revenue billion Forecast, by End User 2020 & 2033

- Table 6: Global Auto-steer System for Agriculture Revenue billion Forecast, by Region 2020 & 2033

- Table 7: Global Auto-steer System for Agriculture Revenue billion Forecast, by Component 2020 & 2033

- Table 8: Global Auto-steer System for Agriculture Revenue billion Forecast, by Technology 2020 & 2033

- Table 9: Global Auto-steer System for Agriculture Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 10: Global Auto-steer System for Agriculture Revenue billion Forecast, by Sales Channel 2020 & 2033

- Table 11: Global Auto-steer System for Agriculture Revenue billion Forecast, by End User 2020 & 2033

- Table 12: Global Auto-steer System for Agriculture Revenue billion Forecast, by Country 2020 & 2033

- Table 13: United States Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Canada Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Mexico Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Auto-steer System for Agriculture Revenue billion Forecast, by Component 2020 & 2033

- Table 17: Global Auto-steer System for Agriculture Revenue billion Forecast, by Technology 2020 & 2033

- Table 18: Global Auto-steer System for Agriculture Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 19: Global Auto-steer System for Agriculture Revenue billion Forecast, by Sales Channel 2020 & 2033

- Table 20: Global Auto-steer System for Agriculture Revenue billion Forecast, by End User 2020 & 2033

- Table 21: Global Auto-steer System for Agriculture Revenue billion Forecast, by Country 2020 & 2033

- Table 22: Brazil Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Argentina Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Rest of South America Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Global Auto-steer System for Agriculture Revenue billion Forecast, by Component 2020 & 2033

- Table 26: Global Auto-steer System for Agriculture Revenue billion Forecast, by Technology 2020 & 2033

- Table 27: Global Auto-steer System for Agriculture Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 28: Global Auto-steer System for Agriculture Revenue billion Forecast, by Sales Channel 2020 & 2033

- Table 29: Global Auto-steer System for Agriculture Revenue billion Forecast, by End User 2020 & 2033

- Table 30: Global Auto-steer System for Agriculture Revenue billion Forecast, by Country 2020 & 2033

- Table 31: United Kingdom Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Germany Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: France Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Italy Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: Spain Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Russia Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Benelux Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Nordics Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: Rest of Europe Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Global Auto-steer System for Agriculture Revenue billion Forecast, by Component 2020 & 2033

- Table 41: Global Auto-steer System for Agriculture Revenue billion Forecast, by Technology 2020 & 2033

- Table 42: Global Auto-steer System for Agriculture Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 43: Global Auto-steer System for Agriculture Revenue billion Forecast, by Sales Channel 2020 & 2033

- Table 44: Global Auto-steer System for Agriculture Revenue billion Forecast, by End User 2020 & 2033

- Table 45: Global Auto-steer System for Agriculture Revenue billion Forecast, by Country 2020 & 2033

- Table 46: Turkey Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 47: Israel Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: GCC Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 49: North Africa Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: South Africa Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 51: Rest of Middle East & Africa Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Global Auto-steer System for Agriculture Revenue billion Forecast, by Component 2020 & 2033

- Table 53: Global Auto-steer System for Agriculture Revenue billion Forecast, by Technology 2020 & 2033

- Table 54: Global Auto-steer System for Agriculture Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 55: Global Auto-steer System for Agriculture Revenue billion Forecast, by Sales Channel 2020 & 2033

- Table 56: Global Auto-steer System for Agriculture Revenue billion Forecast, by End User 2020 & 2033

- Table 57: Global Auto-steer System for Agriculture Revenue billion Forecast, by Country 2020 & 2033

- Table 58: China Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 59: India Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 60: Japan Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 61: South Korea Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: ASEAN Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 63: Oceania Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Rest of Asia Pacific Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Auto-steer System for Agriculture?

The projected CAGR is approximately 12.5%.

2. Which companies are prominent players in the Auto-steer System for Agriculture?

Key companies in the market include John Deere, Trimble, Topcon Positioning Systems, Ag Leader Technology, Raven Industries, AgJunction, Patchwork, CNH Industrial, AGCO Corporation, FieldBee, ARAG, Homburg Holland, Sveaverken Svea Agri, Geometer International, Hexagon Agriculture, Reichhardt, Rostselmash, FJDynamics, SMAJAYU(SHENZHEN), ComNav Technology, CP Device.

3. What are the main segments of the Auto-steer System for Agriculture?

The market segments include Component, Technology, Vehicle Type, Sales Channel, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.8 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Auto-steer System for Agriculture," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Auto-steer System for Agriculture report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Auto-steer System for Agriculture?

To stay informed about further developments, trends, and reports in the Auto-steer System for Agriculture, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence