Key Insights

The global Refractory Market is poised for significant growth, projected to reach an estimated USD 35.77 billion in 2025. Driven by the insatiable demand from the iron and steel sector, which constitutes a substantial portion of end-user consumption, the market is expected to expand at a robust Compound Annual Growth Rate (CAGR) of 4.62% throughout the forecast period of 2025-2033. This upward trajectory is further fueled by the burgeoning energy and chemicals industry, alongside the non-ferrous metals sector, both of which rely heavily on high-performance refractory materials for their high-temperature processes. Technological advancements in refractory production, leading to enhanced durability, thermal resistance, and energy efficiency, are also key enablers of this market expansion. Companies are increasingly focusing on developing specialized refractory products tailored to specific industrial needs, fostering innovation and creating new market opportunities.

Refractory Market Market Size (In Billion)

The market's growth, however, is not without its challenges. Increasing raw material costs and stringent environmental regulations concerning the production and disposal of certain refractory materials are identified as key restraints. Despite these headwinds, the market is witnessing a strong trend towards the adoption of advanced refractory solutions, including non-clay refractories like magnesia, zirconia, and silicon carbide bricks, which offer superior performance in extreme conditions. The Asia Pacific region, led by China and India, is anticipated to maintain its dominance, owing to rapid industrialization and infrastructure development. Strategic collaborations, mergers, and acquisitions among leading players like RHI Magnesita GmbH, Imerys, and Saint-Gobain are shaping the competitive landscape, as they strive to expand their global reach and product portfolios.

Refractory Market Company Market Share

This in-depth report provides an authoritative analysis of the global refractory market, a critical sector underpinning numerous industrial giants including Iron and Steel, Energy and Chemicals, and Non-ferrous Metals. Examining the market from 2019 to 2033, with a base and estimated year of 2025, this study offers invaluable insights into market composition, trends, industry evolution, and future projections. With a projected market size expected to reach trillions of dollars, this report is indispensable for stakeholders seeking to navigate the complexities of this dynamic industry and capitalize on emerging opportunities within the global refractory materials landscape.

Refractory Market Market Composition & Trends

The refractory market exhibits a moderately concentrated structure, with leading players like RHI Magnesita GmbH, Imerys, and Saint-Gobain holding significant market share. Innovation is largely driven by advancements in material science, particularly in the development of high-performance non-clay refractories such as magnesite, zirconia brick, and silica brick, catering to increasingly demanding industrial applications. Regulatory landscapes, primarily focused on environmental sustainability and emission control, are pushing manufacturers towards greener production methods and advanced recycling initiatives for refractory products. Substitute products, though limited in the high-temperature applications where refractories excel, are a constant consideration, driving the need for superior performance and cost-effectiveness. End-user profiles are diverse, with the Iron and Steel industry remaining the largest consumer, followed by Cement, Ceramic, and Glass manufacturing. Mergers and acquisitions (M&A) are a significant trend, with major deals like RHI Magnesita GmbH's acquisition of Dalmia Bharat Refractories Limited's Indian business (valued in the hundreds of millions of dollars) reshaping the competitive landscape. The aggregate value of M&A activities in the refractory industry is projected to surpass billions of dollars over the study period, indicating a strong drive towards consolidation and market expansion.

- Market Concentration: Moderately concentrated with key players dominating.

- Innovation Catalysts: Material science advancements, demand for high-temperature performance, and sustainability initiatives.

- Regulatory Landscapes: Focus on environmental standards, emissions reduction, and circular economy principles.

- Substitute Products: Limited direct substitutes in extreme heat applications; focus on performance enhancement and cost competitiveness.

- End-User Profiles: Dominated by Iron and Steel, followed by Cement, Ceramic, Glass, Energy & Chemicals, and Non-ferrous Metals.

- M&A Activities: Significant consolidation and strategic acquisitions to expand capacity and product portfolios.

Refractory Market Industry Evolution

The refractory market has undergone a profound evolution, driven by technological advancements and evolving industrial demands. Over the historical period (2019–2024), the market witnessed a steady growth trajectory, averaging a CAGR of approximately 4.5%, with an estimated market size exceeding tens of billions of dollars by the end of this period. This growth was primarily fueled by increased production in key end-user industries such as Iron and Steel, which accounts for over 60% of global refractory consumption. Technological advancements have been pivotal, with a shift from traditional clay refractories like fireclay and high alumina to more sophisticated non-clay refractory solutions. The development of advanced magnesite-carbon bricks, zirconia-based refractories, and silica bricks has enabled industries to operate at higher temperatures and with greater efficiency, leading to reduced energy consumption and improved product quality. The adoption of advanced manufacturing techniques, including automation and sophisticated quality control systems, has further enhanced the performance and reliability of refractory materials.

During the base year 2025, the market is estimated to be valued at over fifty billion dollars, with a projected growth rate of 5.2% through the forecast period (2025–2033). This sustained expansion is attributed to several factors. Firstly, the ongoing industrialization in emerging economies, particularly in Asia, continues to drive demand for construction materials and manufacturing equipment, both of which rely heavily on refractories. Secondly, the increasing focus on energy efficiency and emissions reduction across industries is spurring innovation in refractory materials that can withstand extreme conditions and prolong equipment lifespan. For instance, the development of lightweight, insulating refractories is crucial for improving energy efficiency in furnaces and kilns. Thirdly, the growing demand for advanced materials in sectors like aerospace and renewable energy (e.g., in solar thermal systems) presents new avenues for growth. The Energy and Chemicals sector, with its continuous need for high-performance linings in chemical reactors and power plants, is expected to exhibit significant growth. Furthermore, the trend towards specialty refractories, designed for specific applications with unique thermal and chemical resistance properties, is gaining momentum. The market's evolution is also shaped by environmental regulations, pushing manufacturers towards sustainable practices, including the development of recyclable refractories and the reduction of carbon footprints in their production processes. The increasing complexity of industrial processes necessitates continuous R&D investment, ensuring that the refractory market remains at the forefront of material innovation and industrial support, with an estimated annual market expansion in the tens of billions of dollars throughout the forecast period.

Leading Regions, Countries, or Segments in Refractory Market

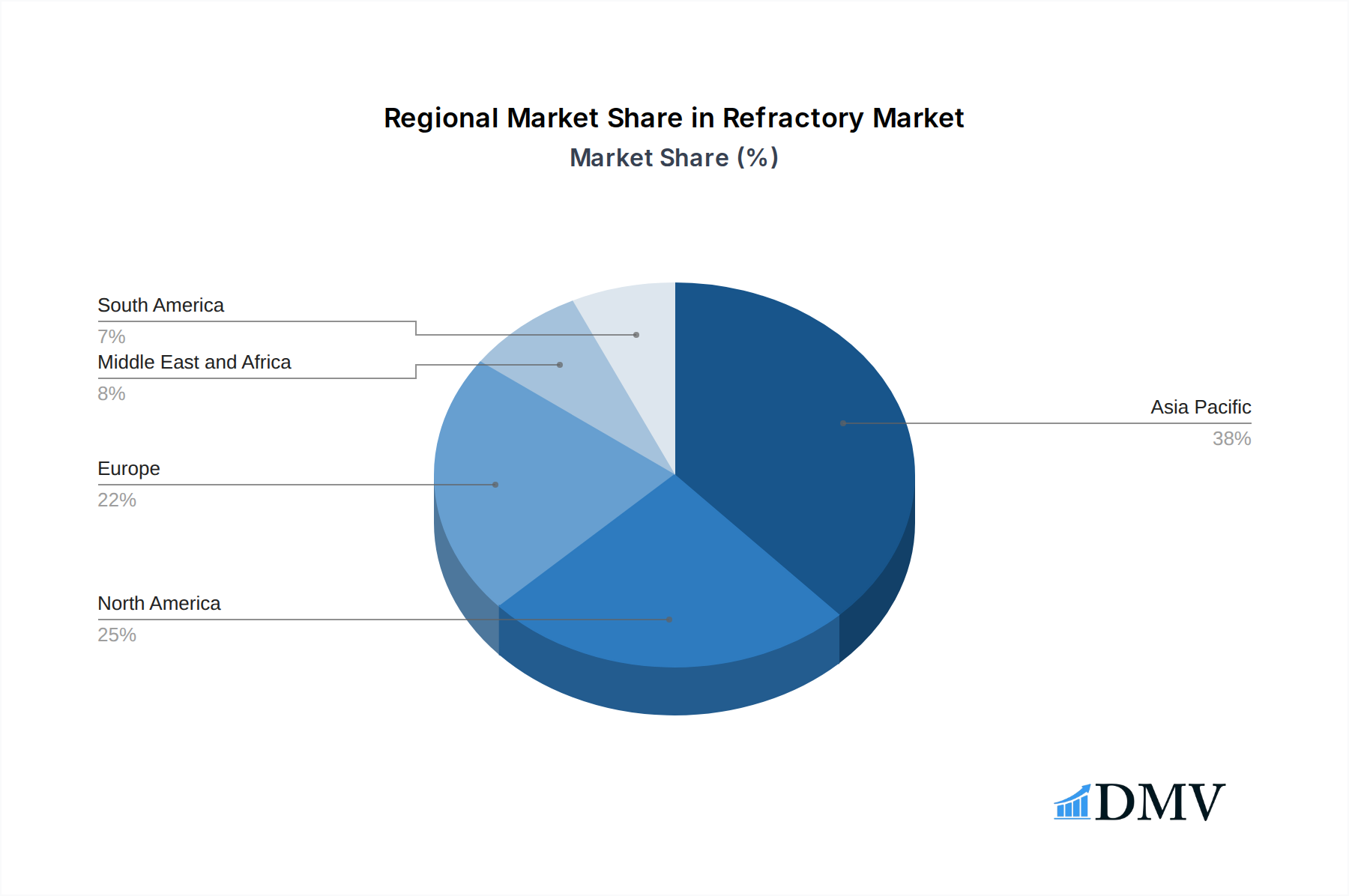

The refractory market is characterized by regional dominance and segment-specific growth. Asia-Pacific, led by China, stands as the largest and fastest-growing region, driven by its colossal Iron and Steel production capacity, robust Cement and Ceramic manufacturing sectors, and substantial investments in infrastructure. The region's market share is estimated at over 50% of the global refractory market.

Within product types, Non-clay Refractory segments, particularly magnesite and zirconia brick, are experiencing rapid growth due to their superior performance at extremely high temperatures and resistance to chemical corrosion. Magnesite refractories are indispensable in the production of steel, while zirconia brick finds critical applications in glass furnaces and non-ferrous metal smelting. The Iron and Steel end-user industry remains the dominant consumer of refractories globally, accounting for approximately 65% of the market. This is due to the sheer volume of steel produced and the high wear and tear experienced by furnaces and ladles. However, the Energy and Chemicals sector is showing promising growth, fueled by the demand for high-performance refractories in petrochemical plants, power generation facilities, and the burgeoning hydrogen production industry.

- Dominant Region: Asia-Pacific, particularly China, owing to massive industrial output and infrastructure development.

- Key Drivers:

- Largest global producer and consumer of Iron and Steel.

- Rapid expansion of Cement, Ceramic, and Glass manufacturing.

- Significant government initiatives and foreign investment in industrial sectors.

- Growing demand for advanced refractories in emerging technologies.

- Key Drivers:

- Dominant Product Type: Non-clay Refractory, with Magnesite and Zirconia Brick leading the pack.

- Key Drivers:

- Superior high-temperature performance and chemical resistance.

- Essential for critical processes in Iron and Steel, Glass, and Non-ferrous Metals industries.

- Continuous innovation in material composition and manufacturing for enhanced durability.

- Key Drivers:

- Dominant End-user Industry: Iron and Steel, due to high-temperature operational demands and vast production volumes.

- Key Drivers:

- Global reliance on steel for construction, automotive, and infrastructure.

- Intense operational conditions requiring robust refractory linings for furnaces, converters, and ladles.

- Technological advancements in steelmaking processes demanding more resilient refractory solutions.

- Key Drivers:

- Emerging Segments: Growth in Energy and Chemicals for specialized applications, and increasing demand for Insulating refractories to improve energy efficiency across all end-user industries.

The dominance of these segments and regions is further reinforced by substantial investments in research and development, strategic partnerships, and the increasing adoption of advanced refractory technologies. Regulatory support for industrial expansion and environmental compliance in key regions also plays a crucial role in shaping market dynamics.

Refractory Market Product Innovations

Product innovation in the refractory market is intensely focused on enhancing thermal shock resistance, extending service life, and improving energy efficiency. Recent developments include the introduction of novel fused cast refractories with enhanced corrosion resistance for the glass industry and advanced magnesia-carbon bricks incorporating nano-materials for superior performance in steelmaking. The application of advanced ceramic matrix composites (CMCs) is also gaining traction for extremely demanding environments. These innovations are crucial for meeting the stringent requirements of modern industrial processes, leading to reduced downtime, lower operating costs, and a smaller environmental footprint.

Propelling Factors for Refractory Market Growth

The global refractory market is experiencing robust growth, propelled by several interconnected factors. The sustained expansion of key end-user industries, most notably Iron and Steel and Cement production, is a primary driver. Increased industrialization and infrastructure development in emerging economies, particularly in Asia and Africa, are creating a burgeoning demand for refractory materials. Technological advancements in manufacturing processes are leading to the development of higher-performance refractories with improved durability and energy efficiency, allowing industries to operate at higher temperatures and achieve greater productivity. Furthermore, stringent environmental regulations are indirectly fostering growth by encouraging the adoption of advanced refractories that minimize emissions and energy consumption. Government initiatives aimed at boosting manufacturing and construction sectors worldwide also contribute significantly to this upward trend.

Obstacles in the Refractory Market Market

Despite its strong growth trajectory, the refractory market faces several significant obstacles. Fluctuations in raw material prices, particularly for key components like bauxite, magnesia, and graphite, can impact profit margins and necessitate pricing adjustments. Supply chain disruptions, exacerbated by geopolitical events and logistical challenges, can lead to material shortages and production delays. The highly competitive nature of the market, with numerous players vying for market share, can exert downward pressure on prices. Moreover, the stringent environmental regulations, while driving innovation, also impose compliance costs and can necessitate substantial investment in cleaner production technologies. The cyclical nature of some end-user industries, such as Iron and Steel, can also lead to volatility in demand.

Future Opportunities in Refractory Market

The refractory market is ripe with emerging opportunities. The increasing demand for refractories in the Energy and Chemicals sector, driven by the growth of petrochemicals, power generation, and the burgeoning hydrogen economy, presents a significant avenue for expansion. The development of advanced refractories for high-temperature applications in renewable energy technologies, such as solar thermal power plants and advanced battery manufacturing, is another promising area. The circular economy trend is also creating opportunities for businesses focused on the recycling and regeneration of used refractories, reducing waste and resource dependency. Furthermore, the continued industrialization of developing nations will sustain the demand for traditional refractory applications, while growing interest in specialized refractories for niche applications in aerospace and defense sectors offers further potential for market diversification and growth, with global market expansion expected to reach tens of billions of dollars annually.

Major Players in the Refractory Market Ecosystem

- Chosun Refractories

- Harbisonwalker International

- IFGL Refractories Ltd

- Imerys

- Intocast AG

- Krosaki Harima Corporation

- Magnezit Group

- Minerals Technologies Inc

- Morgan Advanced Materials

- Puyang Refractories Group Co Ltd

- Refratechnik

- RHI Magnesita GmbH

- Saint-Gobain

- Shinagawa Refractories Co Ltd

- Vesuvius

Key Developments in Refractory Market Industry

- January 2023: RHI Magnesita GmbH announced the completion of its acquisition of Dalmia Bharat Refractories Limited's (DBRL) Indian refractory business. This acquisition is expected to add almost 300,000 tons of capacity annually to the existing production footprint in India, enhancing the company's business in the studied market.

- December 2022: Shinagawa Refractories Co. Ltd (Shinagawa) acquired the Brazilian refractory business and alumina-based wear-resistant ceramics business from Compagnie de Saint-Gobain S.A. (Saint-Gobain) in the United States. This acquisition was expected to help the company to enhance its product portfolio in the coming years.

- April 2022: Saint-Gobain acquired Monofrax, based in New York, and a manufacturer of fused cast refractories. This strategic move was expected to strengthen the company's position in the American market.

Strategic Refractory Market Market Forecast

The refractory market is poised for sustained and significant growth through 2033, driven by ongoing industrial expansion, technological advancements, and increasing demand for high-performance materials. The projected market expansion, estimated to add tens of billions of dollars annually, will be fueled by the robust Iron and Steel, Cement, and Energy and Chemicals sectors. Innovations in non-clay refractories, particularly magnesite and zirconia, coupled with a growing emphasis on energy efficiency and sustainable production, will shape future market dynamics. Strategic acquisitions and expansions by major players, along with the growing adoption of specialty refractories in emerging industries, are expected to further consolidate market position and unlock new revenue streams, solidifying the essential role of refractories in global industrial development.

Refractory Market Segmentation

-

1. Product Type

-

1.1. Non-clay Refractory

- 1.1.1. Magnesit

- 1.1.2. Zirconia Brick

- 1.1.3. Silica Brick

- 1.1.4. Chromite Brick

- 1.1.5. Other Product Types (Carbides, Silicates)

-

1.2. Clay Refractory

- 1.2.1. High Alumina

- 1.2.2. Fireclay

- 1.2.3. Insulating

-

1.1. Non-clay Refractory

-

2. End-user Industry

- 2.1. Iron and Steel

- 2.2. Energy and Chemicals

- 2.3. Non-ferrous Metals

- 2.4. Cement

- 2.5. Ceramic

- 2.6. Glass

- 2.7. Other End-user Industries

Refractory Market Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. Italy

- 3.4. France

- 3.5. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. Saudi Arabia

- 5.2. South Africa

- 5.3. Rest of Middle East and Africa

Refractory Market Regional Market Share

Geographic Coverage of Refractory Market

Refractory Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Non-clay Refractory

- 5.1.1.1. Magnesit

- 5.1.1.2. Zirconia Brick

- 5.1.1.3. Silica Brick

- 5.1.1.4. Chromite Brick

- 5.1.1.5. Other Product Types (Carbides, Silicates)

- 5.1.2. Clay Refractory

- 5.1.2.1. High Alumina

- 5.1.2.2. Fireclay

- 5.1.2.3. Insulating

- 5.1.1. Non-clay Refractory

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Iron and Steel

- 5.2.2. Energy and Chemicals

- 5.2.3. Non-ferrous Metals

- 5.2.4. Cement

- 5.2.5. Ceramic

- 5.2.6. Glass

- 5.2.7. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.3.2. North America

- 5.3.3. Europe

- 5.3.4. South America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Global Refractory Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Non-clay Refractory

- 6.1.1.1. Magnesit

- 6.1.1.2. Zirconia Brick

- 6.1.1.3. Silica Brick

- 6.1.1.4. Chromite Brick

- 6.1.1.5. Other Product Types (Carbides, Silicates)

- 6.1.2. Clay Refractory

- 6.1.2.1. High Alumina

- 6.1.2.2. Fireclay

- 6.1.2.3. Insulating

- 6.1.1. Non-clay Refractory

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Iron and Steel

- 6.2.2. Energy and Chemicals

- 6.2.3. Non-ferrous Metals

- 6.2.4. Cement

- 6.2.5. Ceramic

- 6.2.6. Glass

- 6.2.7. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Asia Pacific Refractory Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Non-clay Refractory

- 7.1.1.1. Magnesit

- 7.1.1.2. Zirconia Brick

- 7.1.1.3. Silica Brick

- 7.1.1.4. Chromite Brick

- 7.1.1.5. Other Product Types (Carbides, Silicates)

- 7.1.2. Clay Refractory

- 7.1.2.1. High Alumina

- 7.1.2.2. Fireclay

- 7.1.2.3. Insulating

- 7.1.1. Non-clay Refractory

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Iron and Steel

- 7.2.2. Energy and Chemicals

- 7.2.3. Non-ferrous Metals

- 7.2.4. Cement

- 7.2.5. Ceramic

- 7.2.6. Glass

- 7.2.7. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. North America Refractory Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Non-clay Refractory

- 8.1.1.1. Magnesit

- 8.1.1.2. Zirconia Brick

- 8.1.1.3. Silica Brick

- 8.1.1.4. Chromite Brick

- 8.1.1.5. Other Product Types (Carbides, Silicates)

- 8.1.2. Clay Refractory

- 8.1.2.1. High Alumina

- 8.1.2.2. Fireclay

- 8.1.2.3. Insulating

- 8.1.1. Non-clay Refractory

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Iron and Steel

- 8.2.2. Energy and Chemicals

- 8.2.3. Non-ferrous Metals

- 8.2.4. Cement

- 8.2.5. Ceramic

- 8.2.6. Glass

- 8.2.7. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Europe Refractory Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Non-clay Refractory

- 9.1.1.1. Magnesit

- 9.1.1.2. Zirconia Brick

- 9.1.1.3. Silica Brick

- 9.1.1.4. Chromite Brick

- 9.1.1.5. Other Product Types (Carbides, Silicates)

- 9.1.2. Clay Refractory

- 9.1.2.1. High Alumina

- 9.1.2.2. Fireclay

- 9.1.2.3. Insulating

- 9.1.1. Non-clay Refractory

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Iron and Steel

- 9.2.2. Energy and Chemicals

- 9.2.3. Non-ferrous Metals

- 9.2.4. Cement

- 9.2.5. Ceramic

- 9.2.6. Glass

- 9.2.7. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. South America Refractory Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Non-clay Refractory

- 10.1.1.1. Magnesit

- 10.1.1.2. Zirconia Brick

- 10.1.1.3. Silica Brick

- 10.1.1.4. Chromite Brick

- 10.1.1.5. Other Product Types (Carbides, Silicates)

- 10.1.2. Clay Refractory

- 10.1.2.1. High Alumina

- 10.1.2.2. Fireclay

- 10.1.2.3. Insulating

- 10.1.1. Non-clay Refractory

- 10.2. Market Analysis, Insights and Forecast - by End-user Industry

- 10.2.1. Iron and Steel

- 10.2.2. Energy and Chemicals

- 10.2.3. Non-ferrous Metals

- 10.2.4. Cement

- 10.2.5. Ceramic

- 10.2.6. Glass

- 10.2.7. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. Middle East and Africa Refractory Market Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Non-clay Refractory

- 11.1.1.1. Magnesit

- 11.1.1.2. Zirconia Brick

- 11.1.1.3. Silica Brick

- 11.1.1.4. Chromite Brick

- 11.1.1.5. Other Product Types (Carbides, Silicates)

- 11.1.2. Clay Refractory

- 11.1.2.1. High Alumina

- 11.1.2.2. Fireclay

- 11.1.2.3. Insulating

- 11.1.1. Non-clay Refractory

- 11.2. Market Analysis, Insights and Forecast - by End-user Industry

- 11.2.1. Iron and Steel

- 11.2.2. Energy and Chemicals

- 11.2.3. Non-ferrous Metals

- 11.2.4. Cement

- 11.2.5. Ceramic

- 11.2.6. Glass

- 11.2.7. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Chosun Refractories

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Harbisonwalker International

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 IFGL Refractories Ltd

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Imerys

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Intocast AG

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Krosaki Harima Corporation

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Magnezit Group

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Minerals Technologies Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Morgan Advanced Materials

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Puyang Refractories Group Co Ltd

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Refratechnik

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 RHI Magnesita GmbH

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Saint-Gobain

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Shinagawa Refractories Co Ltd

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Vesuvius*List Not Exhaustive

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 Chosun Refractories

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Refractory Market Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Asia Pacific Refractory Market Revenue (billion), by Product Type 2025 & 2033

- Figure 3: Asia Pacific Refractory Market Revenue Share (%), by Product Type 2025 & 2033

- Figure 4: Asia Pacific Refractory Market Revenue (billion), by End-user Industry 2025 & 2033

- Figure 5: Asia Pacific Refractory Market Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 6: Asia Pacific Refractory Market Revenue (billion), by Country 2025 & 2033

- Figure 7: Asia Pacific Refractory Market Revenue Share (%), by Country 2025 & 2033

- Figure 8: North America Refractory Market Revenue (billion), by Product Type 2025 & 2033

- Figure 9: North America Refractory Market Revenue Share (%), by Product Type 2025 & 2033

- Figure 10: North America Refractory Market Revenue (billion), by End-user Industry 2025 & 2033

- Figure 11: North America Refractory Market Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 12: North America Refractory Market Revenue (billion), by Country 2025 & 2033

- Figure 13: North America Refractory Market Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Refractory Market Revenue (billion), by Product Type 2025 & 2033

- Figure 15: Europe Refractory Market Revenue Share (%), by Product Type 2025 & 2033

- Figure 16: Europe Refractory Market Revenue (billion), by End-user Industry 2025 & 2033

- Figure 17: Europe Refractory Market Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 18: Europe Refractory Market Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Refractory Market Revenue Share (%), by Country 2025 & 2033

- Figure 20: South America Refractory Market Revenue (billion), by Product Type 2025 & 2033

- Figure 21: South America Refractory Market Revenue Share (%), by Product Type 2025 & 2033

- Figure 22: South America Refractory Market Revenue (billion), by End-user Industry 2025 & 2033

- Figure 23: South America Refractory Market Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 24: South America Refractory Market Revenue (billion), by Country 2025 & 2033

- Figure 25: South America Refractory Market Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Refractory Market Revenue (billion), by Product Type 2025 & 2033

- Figure 27: Middle East and Africa Refractory Market Revenue Share (%), by Product Type 2025 & 2033

- Figure 28: Middle East and Africa Refractory Market Revenue (billion), by End-user Industry 2025 & 2033

- Figure 29: Middle East and Africa Refractory Market Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 30: Middle East and Africa Refractory Market Revenue (billion), by Country 2025 & 2033

- Figure 31: Middle East and Africa Refractory Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Refractory Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 2: Global Refractory Market Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 3: Global Refractory Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Refractory Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 5: Global Refractory Market Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 6: Global Refractory Market Revenue billion Forecast, by Country 2020 & 2033

- Table 7: China Refractory Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: India Refractory Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Japan Refractory Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: South Korea Refractory Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Rest of Asia Pacific Refractory Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Global Refractory Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 13: Global Refractory Market Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 14: Global Refractory Market Revenue billion Forecast, by Country 2020 & 2033

- Table 15: United States Refractory Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Refractory Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Mexico Refractory Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Global Refractory Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 19: Global Refractory Market Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 20: Global Refractory Market Revenue billion Forecast, by Country 2020 & 2033

- Table 21: Germany Refractory Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: United Kingdom Refractory Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Italy Refractory Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: France Refractory Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Rest of Europe Refractory Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Global Refractory Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 27: Global Refractory Market Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 28: Global Refractory Market Revenue billion Forecast, by Country 2020 & 2033

- Table 29: Brazil Refractory Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Argentina Refractory Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Rest of South America Refractory Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Global Refractory Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 33: Global Refractory Market Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 34: Global Refractory Market Revenue billion Forecast, by Country 2020 & 2033

- Table 35: Saudi Arabia Refractory Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: South Africa Refractory Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Rest of Middle East and Africa Refractory Market Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Refractory Market?

The projected CAGR is approximately 9.5%.

2. Which companies are prominent players in the Refractory Market?

Key companies in the market include Chosun Refractories, Harbisonwalker International, IFGL Refractories Ltd, Imerys, Intocast AG, Krosaki Harima Corporation, Magnezit Group, Minerals Technologies Inc, Morgan Advanced Materials, Puyang Refractories Group Co Ltd, Refratechnik, RHI Magnesita GmbH, Saint-Gobain, Shinagawa Refractories Co Ltd, Vesuvius*List Not Exhaustive.

3. What are the main segments of the Refractory Market?

The market segments include Product Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 47.88 billion as of 2022.

5. What are some drivers contributing to market growth?

Continuous Usage of Refractories in the Iron and Steel Industry; Increase in the Production of Non-ferrous Metals.

6. What are the notable trends driving market growth?

Increasing Demand from the Iron and Steel Industry.

7. Are there any restraints impacting market growth?

Continuous Usage of Refractories in the Iron and Steel Industry; Increase in the Production of Non-ferrous Metals.

8. Can you provide examples of recent developments in the market?

January 2023: RHI Magnesita GmbH announced the completion of its acquisition of Dalmia Bharat Refractories Limited's (DBRL) Indian refractory business is expected to add almost 300,000 tons of capacity annually to the existing production footprint in India, enhancing the company's business in the studied market.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Refractory Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Refractory Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Refractory Market?

To stay informed about further developments, trends, and reports in the Refractory Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence