Key Insights

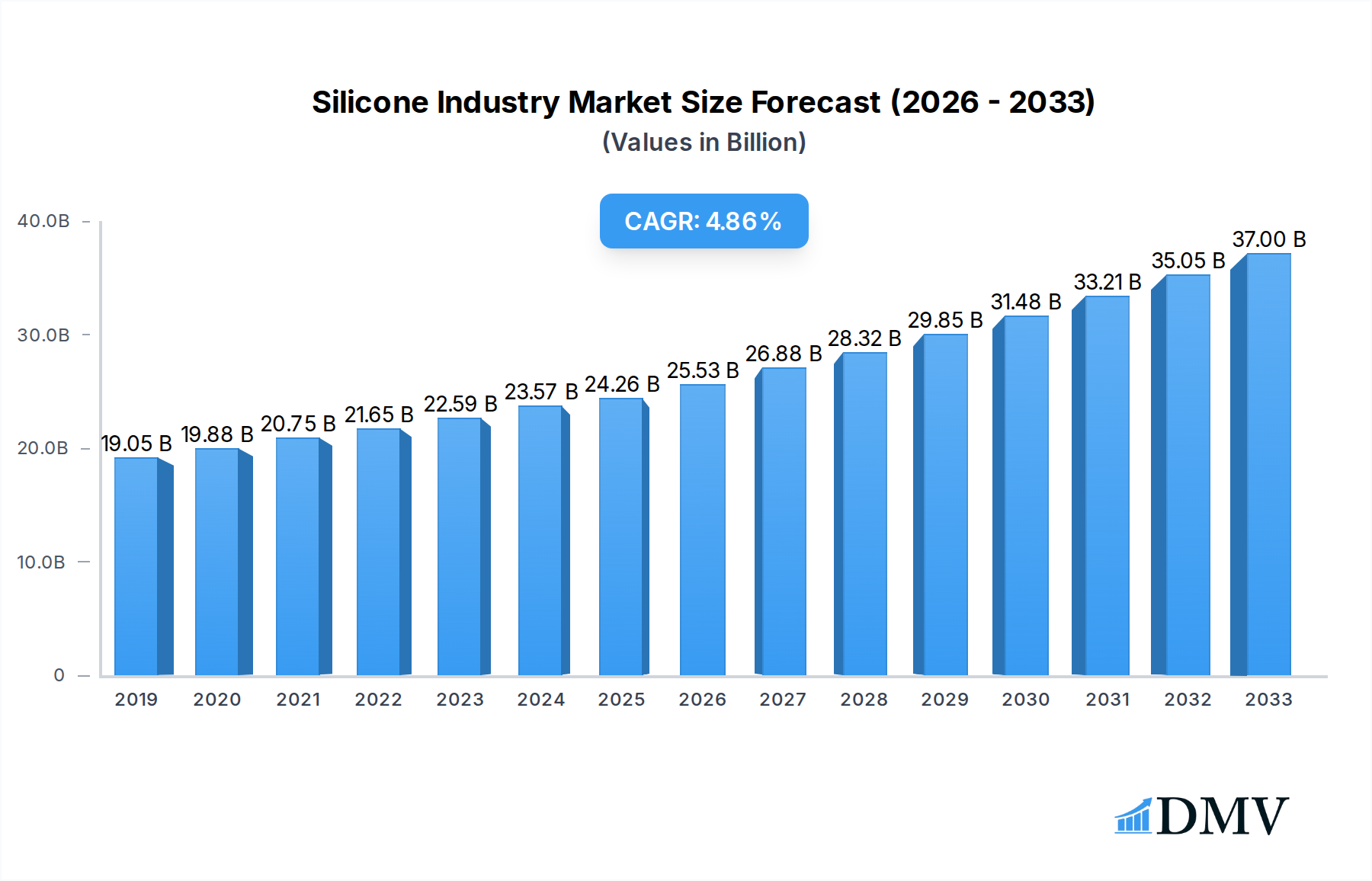

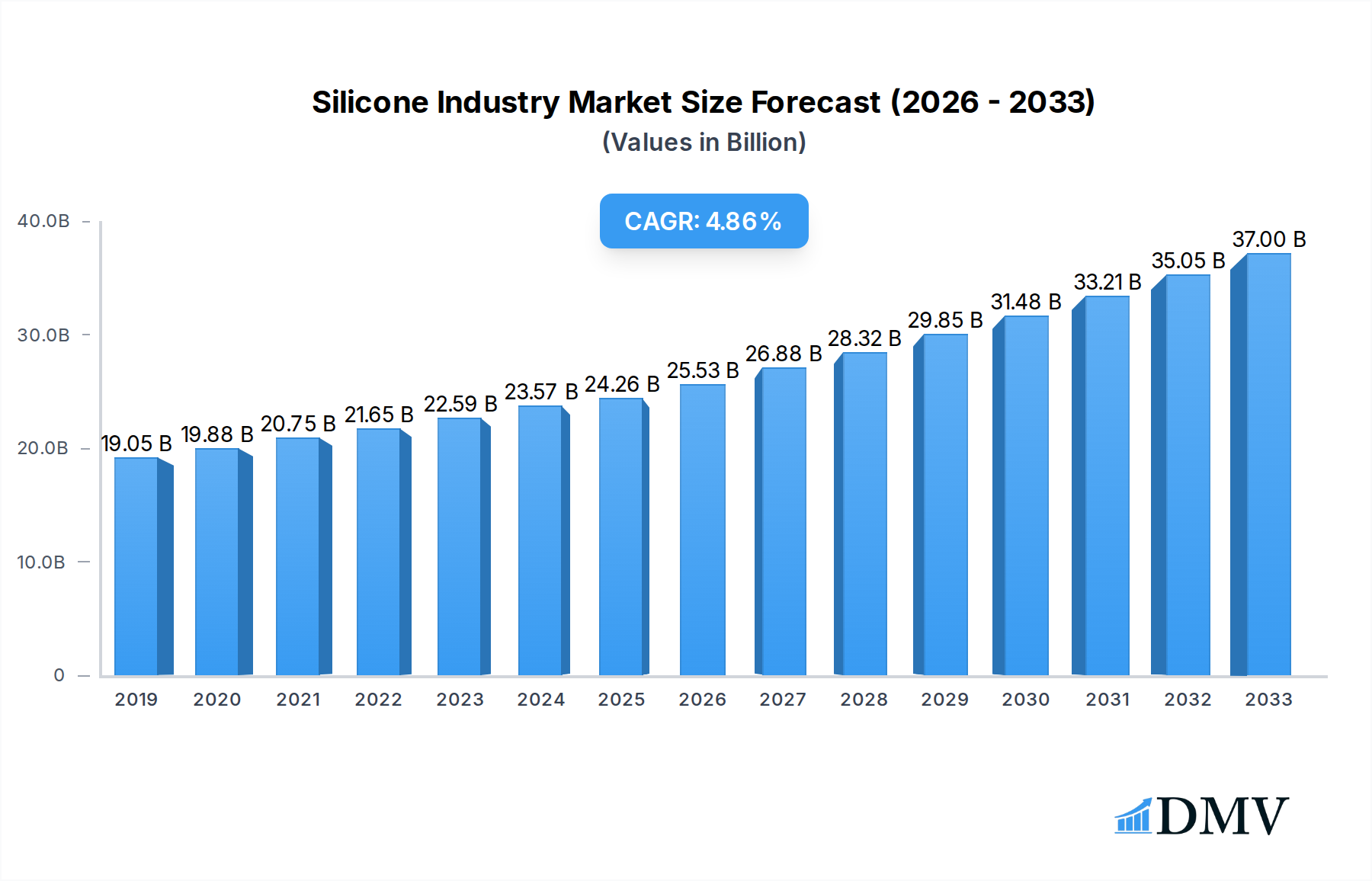

The global Silicone Industry is poised for robust expansion, projected to reach a market size of USD 24.26 billion by 2025, with a compelling Compound Annual Growth Rate (CAGR) of 5.4% from 2019 to 2033. This significant growth is underpinned by a confluence of powerful drivers, chief among them the escalating demand for advanced materials across key sectors. The automotive industry's push towards lighter, more fuel-efficient vehicles, coupled with increasing adoption of electric mobility, fuels the need for high-performance silicones in components like seals, gaskets, and adhesives. Similarly, the burgeoning construction sector, particularly in emerging economies, leverages silicones for their superior durability, weather resistance, and energy-efficient properties in sealants, coatings, and insulation. Furthermore, the rapid evolution of the electronics industry, with its constant innovation in smaller, more powerful devices, demands specialized silicones for encapsulation, thermal management, and dielectric applications. The healthcare sector's growing reliance on biocompatible silicone materials for medical devices, implants, and drug delivery systems also significantly contributes to market dynamism.

Silicone Industry Market Size (In Billion)

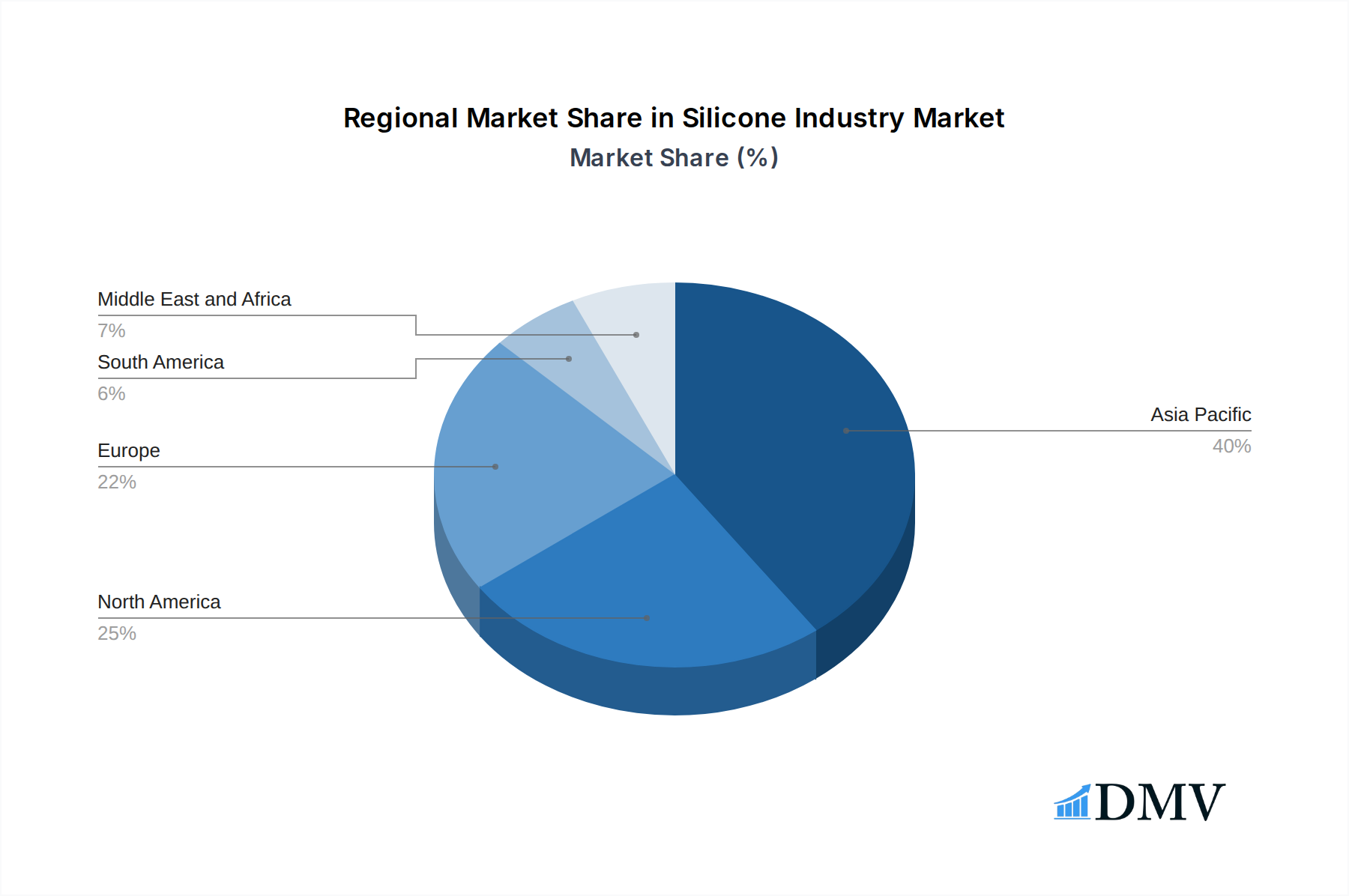

The industry's trajectory is further shaped by evolving trends and strategic responses to market dynamics. The increasing focus on sustainability is driving the development of eco-friendly silicone formulations and advanced recycling technologies. Innovations in specialty silicones, offering enhanced properties like higher temperature resistance, improved flexibility, and advanced adhesion, are opening new application avenues. Conversely, while the market enjoys strong growth, it is not without its challenges. Fluctuations in raw material prices, particularly silicon metal, can impact production costs and profit margins. Intense competition among established players and emerging manufacturers necessitates continuous innovation and cost optimization. Regional market dynamics reveal a strong dominance and growth potential in Asia Pacific, driven by China's extensive manufacturing capabilities and robust industrial expansion, followed by North America and Europe, which continue to be significant markets for high-value silicone applications.

Silicone Industry Company Market Share

Dive deep into the dynamic global silicone industry with this comprehensive report. Covering the period from 2019 to 2033, with a base and estimated year of 2025, this analysis provides unparalleled insights into market composition, evolution, leading segments, and future opportunities. Uncover the impact of key industry developments, strategic player initiatives, and critical growth drivers that are shaping the multi-billion dollar silicone market. This report is essential for stakeholders seeking to capitalize on emerging trends in silicone applications, elastomers, fluids, resins, and advanced silicone materials.

Silicone Industry Market Composition & Trends

The global silicone industry is characterized by a moderately concentrated market, driven by continuous innovation in high-performance silicones and stringent regulatory environments. Key innovation catalysts include the increasing demand for sustainable materials, advancements in silicone chemistry, and the growing adoption of silicones in high-growth sectors. Substitute products, while present, often struggle to match the unique properties of silicones, such as thermal stability, flexibility, and biocompatibility. End-user profiles reveal significant contributions from the transportation, construction materials, electronics, and healthcare sectors, each with evolving requirements for specialized silicone solutions. Mergers and acquisitions (M&A) activity remains a significant aspect of market consolidation, with several multi-billion dollar deals shaping the competitive landscape.

- Market Share Distribution: Dominant players hold substantial market share, but emerging companies are actively innovating to capture niche segments.

- M&A Deal Values: Significant multi-billion dollar transactions underscore the strategic importance and investment potential within the silicone sector.

- Regulatory Impact: Evolving environmental and safety regulations are influencing product development and manufacturing processes, particularly for specialty silicones.

- Substitute Products: While polymers like polyurethane and TPEs offer alternatives, they often fall short in critical performance areas, maintaining silicone's competitive edge.

- End-User Dominance: The transportation and electronics sectors are key demand drivers, with projected growth of XX% and XX% respectively.

Silicone Industry Industry Evolution

The silicone industry has witnessed remarkable evolution, driven by a confluence of technological advancements, shifting consumer demands, and expanding application frontiers. Over the historical period (2019-2024) and into the forecast period (2025-2033), the market has consistently demonstrated robust growth trajectories. This expansion is fueled by the inherent versatility of silicones, enabling their integration into increasingly sophisticated products and processes. Technological innovations have centered on developing advanced silicone formulations with enhanced properties like superior adhesion, increased durability, and improved thermal resistance. The adoption of silicones in megatrends such as electromobility, renewable energies, and personalized healthcare has been particularly noteworthy. Consumer demand for safer, more durable, and environmentally friendly products has further propelled the market, encouraging manufacturers to invest in research and development for sustainable silicone solutions. Market growth rates have consistently outperformed the broader chemical industry, with a projected Compound Annual Growth Rate (CAGR) of XX% between 2025 and 2033. This sustained growth is indicative of the indispensable role silicones play across diverse industries. The increasing complexity of end-user requirements, from lightweight materials in automotive to biocompatible components in medical devices, necessitates continuous innovation in silicone chemistry and processing. For instance, the development of medical-grade silicones has revolutionized implantable devices and drug delivery systems, showcasing the profound impact of technological progress. Furthermore, the push for energy efficiency in buildings and the development of advanced electronic components have also created substantial demand for specialized silicone sealants, coatings, and encapsulants. The industry's ability to adapt to these evolving needs underscores its resilience and forward-looking approach.

Leading Regions, Countries, or Segments in Silicone Industry

The global silicone industry is experiencing significant growth across various regions and segments, with Asia Pacific emerging as a dominant force. This leadership is attributed to robust manufacturing capabilities, expanding industrial bases, and increasing adoption of silicone-based products in rapidly growing economies. Within the Form segmentation, elastomers continue to hold a commanding market share due to their widespread use in automotive, construction, and consumer goods, projected to account for over XX% of the market value by 2025. Fluids also represent a significant segment, driven by applications in personal care, healthcare, and industrial lubricants.

Dominant Region: Asia Pacific:

- Key Drivers: High manufacturing output, increasing domestic consumption, favorable government policies supporting industrial development, and substantial investments in infrastructure and technology.

- Market Penetration: Strong presence of key manufacturers and a growing demand for silicones in diverse applications, including textiles, coatings, and electronics.

- Investment Trends: Significant capital expenditure by leading companies to expand production capacities and develop localized solutions.

Leading Segment (Form): Elastomers:

- Key Drivers: High demand from the automotive sector for components like seals, gaskets, and hoses, and the construction industry for sealants and adhesives.

- Performance Metrics: Superior flexibility, durability, and resistance to extreme temperatures make them indispensable.

- Growth Projections: Expected to grow at a CAGR of XX% during the forecast period.

Leading Segment (End User): Transportation:

- Key Drivers: Increasing production of electric vehicles (EVs) requiring advanced thermal management and sealing solutions, lightweighting initiatives, and demand for durable components.

- Application Trends: Silicones used in battery pack encapsulation, EV charging systems, and interior components for enhanced safety and comfort.

- Market Impact: The automotive sector's reliance on high-performance silicones solidifies its position as a primary demand generator.

Emerging Segment: Healthcare:

- Key Drivers: Growing demand for biocompatible materials in medical devices, implants, and drug delivery systems, driven by an aging global population and advancements in medical technology.

- Innovation Focus: Development of specialized medical-grade silicones with enhanced antimicrobial properties and improved patient comfort.

- Regulatory Support: Stringent quality and safety standards are being met by silicone manufacturers to cater to this critical sector.

Silicone Industry Product Innovations

The silicone industry is a hotbed of innovation, with continuous advancements in product development and application. Recent breakthroughs include the launch of highly adhesive silicone gels designed for intricate electronic component fixation, crucial for the miniaturization and efficiency of modern devices. Furthermore, the development of advanced silicone elastomers with superior flame retardancy and thermal conductivity is revolutionizing applications in electric vehicle battery systems and renewable energy infrastructure. Innovations in bio-compatible silicones are also expanding their role in the healthcare sector, enabling the creation of more advanced and patient-friendly medical devices and wound care solutions. These product innovations are directly addressing megatrends like electromobility and the increasing demand for sustainable and high-performance materials.

Propelling Factors for Silicone Industry Growth

The silicone industry's growth is propelled by a synergistic interplay of technological, economic, and regulatory influences. Key growth drivers include the accelerating adoption of silicones in burgeoning sectors like electric vehicles (EVs) and renewable energy infrastructure, demanding advanced thermal management and sealing solutions. Technological advancements in silicone chemistry, leading to enhanced properties such as superior heat resistance, flexibility, and biocompatibility, are continuously expanding application possibilities. Economic factors, including rising disposable incomes and industrialization in emerging economies, are fueling demand for silicone-based consumer products and construction materials. Regulatory support for sustainability and energy efficiency also plays a crucial role, encouraging the use of durable and eco-friendly silicone alternatives.

- Electromobility & Renewable Energy: Demand for advanced thermal management and sealing solutions.

- Technological Advancements: Development of high-performance, specialized silicone formulations.

- Growing Disposable Incomes: Increased demand for consumer products incorporating silicones.

- Sustainability Initiatives: Preference for durable and eco-friendly materials in construction and manufacturing.

Obstacles in the Silicone Industry Market

Despite its robust growth, the silicone industry faces several obstacles that can temper its expansion. Volatile raw material prices, particularly for silicon metal, can significantly impact production costs and profit margins. Stringent environmental regulations concerning the production and disposal of certain silicone precursors and by-products can increase compliance costs and necessitate the adoption of more complex manufacturing processes. Furthermore, supply chain disruptions, exacerbated by geopolitical events and logistical challenges, can lead to production delays and increased lead times for critical silicone materials. Intense competition from both established players and emerging low-cost manufacturers can also exert downward pressure on pricing and profitability.

- Raw Material Price Volatility: Fluctuations in silicon metal prices directly affect manufacturing costs.

- Regulatory Hurdles: Increasing compliance costs and stricter environmental standards for production.

- Supply Chain Disruptions: Geopolitical events and logistical challenges impacting material availability.

- Intense Competition: Pressure from both established and emerging players impacting pricing.

Future Opportunities in Silicone Industry

The silicone industry is poised for significant future growth, driven by emerging opportunities across various sectors. The burgeoning demand for advanced materials in electric vehicles (EVs), including battery thermal management systems and lightweight components, presents a substantial growth avenue. The expansion of renewable energy infrastructure, such as solar panels and wind turbines, will also require specialized silicone sealants and encapsulants. Furthermore, the increasing focus on sustainable construction practices and energy-efficient buildings will drive demand for high-performance silicone coatings and sealants. The growing healthcare sector's need for biocompatible materials for medical devices, implants, and advanced drug delivery systems offers another promising frontier. Innovations in 3D printing with silicone will also unlock new applications and manufacturing possibilities.

- Electric Vehicle Revolution: Advanced thermal management and lightweighting solutions.

- Renewable Energy Expansion: Demand for durable sealants and encapsulants in solar and wind technologies.

- Sustainable Construction: Growth in energy-efficient building materials and coatings.

- Healthcare Advancements: Increased use of biocompatible materials in medical devices.

- 3D Printing with Silicone: Novel applications and manufacturing techniques.

Major Players in the Silicone Industry Ecosystem

- BRB International (PETRONAS Chemicals Group Berhad)

- CHT Germany GmbH

- Dow

- DyStar Singapore Pte Ltd

- Elkem ASA

- Evonik Industries AG

- Hoshine Silicon Industry Co Ltd

- Jiangsu Mingzhu Silicone Rubber Material Co Ltd

- KANEKA CORPORATION

- Mitsubishi Chemical Corporation

- Momentive

- Shin-Etsu Chemical Co Ltd

- Wacker Chemie AG

- Wynca Tinyo Silicone Co Ltd

- Zhejiang Sucon Silicone Co Ltd

Key Developments in Silicone Industry Industry

- January 2024: Wacker Chemie AG announced plans to expand its European silicone specialties business and production operations with a new site in Karlovy Vary, Czech Republic, aimed at addressing megatrends like electromobility and renewable energies. Production is slated to begin by the end of 2025.

- November 2023: Wacker Chemie AG launched SILPURAN 2124, a highly adhesive silicone gel for electronic component fixation. This product is also suitable for atraumatic wound dressings and wearable devices.

- October 2022: Elkem ASA inaugurated a new specialized facility in Timberland Court, spanning over 18,000 sq. ft, to manufacture high-purity medical silicone materials for the MedTech and Pharma markets.

Strategic Silicone Industry Market Forecast

The strategic outlook for the silicone industry is overwhelmingly positive, driven by persistent innovation and the indispensable role silicones play in addressing global megatrends. The forecast period (2025-2033) is expected to witness continued robust growth, propelled by advancements in specialty silicones for electric vehicles, renewable energy solutions, and cutting-edge healthcare applications. Market potential is further amplified by the increasing demand for sustainable and high-performance materials across construction, electronics, and consumer goods. The industry's ability to adapt to evolving regulatory landscapes and its commitment to developing novel silicone formulations will be critical in capitalizing on emerging opportunities and solidifying its position as a cornerstone of modern industrial development, with the silicone market value projected to reach trillions of dollars.

Silicone Industry Segmentation

-

1. Form

- 1.1. Elastomers

- 1.2. Fluids

- 1.3. Resins

- 1.4. Other Forms

-

2. End User

- 2.1. Transportation

- 2.2. Construction Materials

- 2.3. Electronics

- 2.4. Healthcare

- 2.5. Industrial Processes

- 2.6. Personal Care and Consumer Products

- 2.7. Other End Users (Textiles and Coatings)

Silicone Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Thailand

- 1.6. Malaysia

- 1.7. Indonesia

- 1.8. Vietnam

- 1.9. ASEAN Countries

- 1.10. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. Italy

- 3.4. France

- 3.5. Spain

- 3.6. Turkey

- 3.7. Russia

- 3.8. NORDIC

- 3.9. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Colombia

- 4.4. Rest of South America

-

5. Middle East and Africa

- 5.1. Saudi Arabia

- 5.2. South Africa

- 5.3. Nigeria

- 5.4. Qatar

- 5.5. Egypt

- 5.6. United Arab Emirates

- 5.7. Rest of Middle East and Africa

Silicone Industry Regional Market Share

Geographic Coverage of Silicone Industry

Silicone Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Form

- 5.1.1. Elastomers

- 5.1.2. Fluids

- 5.1.3. Resins

- 5.1.4. Other Forms

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Transportation

- 5.2.2. Construction Materials

- 5.2.3. Electronics

- 5.2.4. Healthcare

- 5.2.5. Industrial Processes

- 5.2.6. Personal Care and Consumer Products

- 5.2.7. Other End Users (Textiles and Coatings)

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.3.2. North America

- 5.3.3. Europe

- 5.3.4. South America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Form

- 6. Global Silicone Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Form

- 6.1.1. Elastomers

- 6.1.2. Fluids

- 6.1.3. Resins

- 6.1.4. Other Forms

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Transportation

- 6.2.2. Construction Materials

- 6.2.3. Electronics

- 6.2.4. Healthcare

- 6.2.5. Industrial Processes

- 6.2.6. Personal Care and Consumer Products

- 6.2.7. Other End Users (Textiles and Coatings)

- 6.1. Market Analysis, Insights and Forecast - by Form

- 7. Asia Pacific Silicone Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Form

- 7.1.1. Elastomers

- 7.1.2. Fluids

- 7.1.3. Resins

- 7.1.4. Other Forms

- 7.2. Market Analysis, Insights and Forecast - by End User

- 7.2.1. Transportation

- 7.2.2. Construction Materials

- 7.2.3. Electronics

- 7.2.4. Healthcare

- 7.2.5. Industrial Processes

- 7.2.6. Personal Care and Consumer Products

- 7.2.7. Other End Users (Textiles and Coatings)

- 7.1. Market Analysis, Insights and Forecast - by Form

- 8. North America Silicone Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Form

- 8.1.1. Elastomers

- 8.1.2. Fluids

- 8.1.3. Resins

- 8.1.4. Other Forms

- 8.2. Market Analysis, Insights and Forecast - by End User

- 8.2.1. Transportation

- 8.2.2. Construction Materials

- 8.2.3. Electronics

- 8.2.4. Healthcare

- 8.2.5. Industrial Processes

- 8.2.6. Personal Care and Consumer Products

- 8.2.7. Other End Users (Textiles and Coatings)

- 8.1. Market Analysis, Insights and Forecast - by Form

- 9. Europe Silicone Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Form

- 9.1.1. Elastomers

- 9.1.2. Fluids

- 9.1.3. Resins

- 9.1.4. Other Forms

- 9.2. Market Analysis, Insights and Forecast - by End User

- 9.2.1. Transportation

- 9.2.2. Construction Materials

- 9.2.3. Electronics

- 9.2.4. Healthcare

- 9.2.5. Industrial Processes

- 9.2.6. Personal Care and Consumer Products

- 9.2.7. Other End Users (Textiles and Coatings)

- 9.1. Market Analysis, Insights and Forecast - by Form

- 10. South America Silicone Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Form

- 10.1.1. Elastomers

- 10.1.2. Fluids

- 10.1.3. Resins

- 10.1.4. Other Forms

- 10.2. Market Analysis, Insights and Forecast - by End User

- 10.2.1. Transportation

- 10.2.2. Construction Materials

- 10.2.3. Electronics

- 10.2.4. Healthcare

- 10.2.5. Industrial Processes

- 10.2.6. Personal Care and Consumer Products

- 10.2.7. Other End Users (Textiles and Coatings)

- 10.1. Market Analysis, Insights and Forecast - by Form

- 11. Middle East and Africa Silicone Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Form

- 11.1.1. Elastomers

- 11.1.2. Fluids

- 11.1.3. Resins

- 11.1.4. Other Forms

- 11.2. Market Analysis, Insights and Forecast - by End User

- 11.2.1. Transportation

- 11.2.2. Construction Materials

- 11.2.3. Electronics

- 11.2.4. Healthcare

- 11.2.5. Industrial Processes

- 11.2.6. Personal Care and Consumer Products

- 11.2.7. Other End Users (Textiles and Coatings)

- 11.1. Market Analysis, Insights and Forecast - by Form

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 BRB International (PETRONAS Chemicals Group Berhad)

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 CHT Germany GmbH

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Dow

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 DyStar Singapore Pte Ltd

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Elkem ASA

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Evonik Industries AG

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Hoshine Silicon Industry Co Ltd

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Jiangsu Mingzhu Silicone Rubber Material Co Ltd

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 KANEKA CORPORATION

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Mitsubishi Chemical Corporation

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Momentive

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Shin-Etsu Chemical Co Ltd

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Wacker Chemie AG

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Wynca Tinyo Silicone Co Ltd

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Zhejiang Sucon Silicone Co Ltd*List Not Exhaustive

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 BRB International (PETRONAS Chemicals Group Berhad)

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Silicone Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Asia Pacific Silicone Industry Revenue (billion), by Form 2025 & 2033

- Figure 3: Asia Pacific Silicone Industry Revenue Share (%), by Form 2025 & 2033

- Figure 4: Asia Pacific Silicone Industry Revenue (billion), by End User 2025 & 2033

- Figure 5: Asia Pacific Silicone Industry Revenue Share (%), by End User 2025 & 2033

- Figure 6: Asia Pacific Silicone Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: Asia Pacific Silicone Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: North America Silicone Industry Revenue (billion), by Form 2025 & 2033

- Figure 9: North America Silicone Industry Revenue Share (%), by Form 2025 & 2033

- Figure 10: North America Silicone Industry Revenue (billion), by End User 2025 & 2033

- Figure 11: North America Silicone Industry Revenue Share (%), by End User 2025 & 2033

- Figure 12: North America Silicone Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: North America Silicone Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Silicone Industry Revenue (billion), by Form 2025 & 2033

- Figure 15: Europe Silicone Industry Revenue Share (%), by Form 2025 & 2033

- Figure 16: Europe Silicone Industry Revenue (billion), by End User 2025 & 2033

- Figure 17: Europe Silicone Industry Revenue Share (%), by End User 2025 & 2033

- Figure 18: Europe Silicone Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Silicone Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: South America Silicone Industry Revenue (billion), by Form 2025 & 2033

- Figure 21: South America Silicone Industry Revenue Share (%), by Form 2025 & 2033

- Figure 22: South America Silicone Industry Revenue (billion), by End User 2025 & 2033

- Figure 23: South America Silicone Industry Revenue Share (%), by End User 2025 & 2033

- Figure 24: South America Silicone Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: South America Silicone Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Silicone Industry Revenue (billion), by Form 2025 & 2033

- Figure 27: Middle East and Africa Silicone Industry Revenue Share (%), by Form 2025 & 2033

- Figure 28: Middle East and Africa Silicone Industry Revenue (billion), by End User 2025 & 2033

- Figure 29: Middle East and Africa Silicone Industry Revenue Share (%), by End User 2025 & 2033

- Figure 30: Middle East and Africa Silicone Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Middle East and Africa Silicone Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Silicone Industry Revenue billion Forecast, by Form 2020 & 2033

- Table 2: Global Silicone Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 3: Global Silicone Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Silicone Industry Revenue billion Forecast, by Form 2020 & 2033

- Table 5: Global Silicone Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 6: Global Silicone Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: China Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: India Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Japan Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: South Korea Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Thailand Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Malaysia Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Indonesia Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Vietnam Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: ASEAN Countries Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Rest of Asia Pacific Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Global Silicone Industry Revenue billion Forecast, by Form 2020 & 2033

- Table 18: Global Silicone Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 19: Global Silicone Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 20: United States Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Canada Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Mexico Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Global Silicone Industry Revenue billion Forecast, by Form 2020 & 2033

- Table 24: Global Silicone Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 25: Global Silicone Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 26: Germany Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: United Kingdom Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Italy Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: France Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Spain Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Turkey Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Russia Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: NORDIC Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Rest of Europe Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: Global Silicone Industry Revenue billion Forecast, by Form 2020 & 2033

- Table 36: Global Silicone Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 37: Global Silicone Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 38: Brazil Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: Argentina Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Colombia Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: Rest of South America Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Global Silicone Industry Revenue billion Forecast, by Form 2020 & 2033

- Table 43: Global Silicone Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 44: Global Silicone Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 45: Saudi Arabia Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: South Africa Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 47: Nigeria Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Qatar Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 49: Egypt Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: United Arab Emirates Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 51: Rest of Middle East and Africa Silicone Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Silicone Industry?

The projected CAGR is approximately 5.4%.

2. Which companies are prominent players in the Silicone Industry?

Key companies in the market include BRB International (PETRONAS Chemicals Group Berhad), CHT Germany GmbH, Dow, DyStar Singapore Pte Ltd, Elkem ASA, Evonik Industries AG, Hoshine Silicon Industry Co Ltd, Jiangsu Mingzhu Silicone Rubber Material Co Ltd, KANEKA CORPORATION, Mitsubishi Chemical Corporation, Momentive, Shin-Etsu Chemical Co Ltd, Wacker Chemie AG, Wynca Tinyo Silicone Co Ltd, Zhejiang Sucon Silicone Co Ltd*List Not Exhaustive.

3. What are the main segments of the Silicone Industry?

The market segments include Form, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 24.26 billion as of 2022.

5. What are some drivers contributing to market growth?

Rising Application in Automotive Industry; Increasing Usage in Healthcare Industry; Growing Demand from Power Transmission and Distribution.

6. What are the notable trends driving market growth?

The Industrial Processes Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

Rising Application in Automotive Industry; Increasing Usage in Healthcare Industry; Growing Demand from Power Transmission and Distribution.

8. Can you provide examples of recent developments in the market?

January 2024: Wacker Chemie AG planned to expand its European silicone specialties business and production operations. This new silicone production site will be built in Karlovy Vary in the Czech Republic. This expansion is intended to overcome the megatrends such as electromobility and renewable energies. The production is expected to start at the end of 2025.November 2023: Wacker Chemie AG launched SILPURAN 2124. It is a highly adhesive silicone gel for fixing electronic components. This adhesive is suitable for the production of adhesive layers that are required for atraumatic wound dressings and for fixing wearables and other devices worn on the skin.October 2022: Elkem ASA opened a new specialized facility in Timberland Court. The new facility spans over 18,000 sq. ft and will manufacture high-purity medical silicone materials to meet the demands of the MedTech and Pharma markets.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Silicone Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Silicone Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Silicone Industry?

To stay informed about further developments, trends, and reports in the Silicone Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence