Key Insights

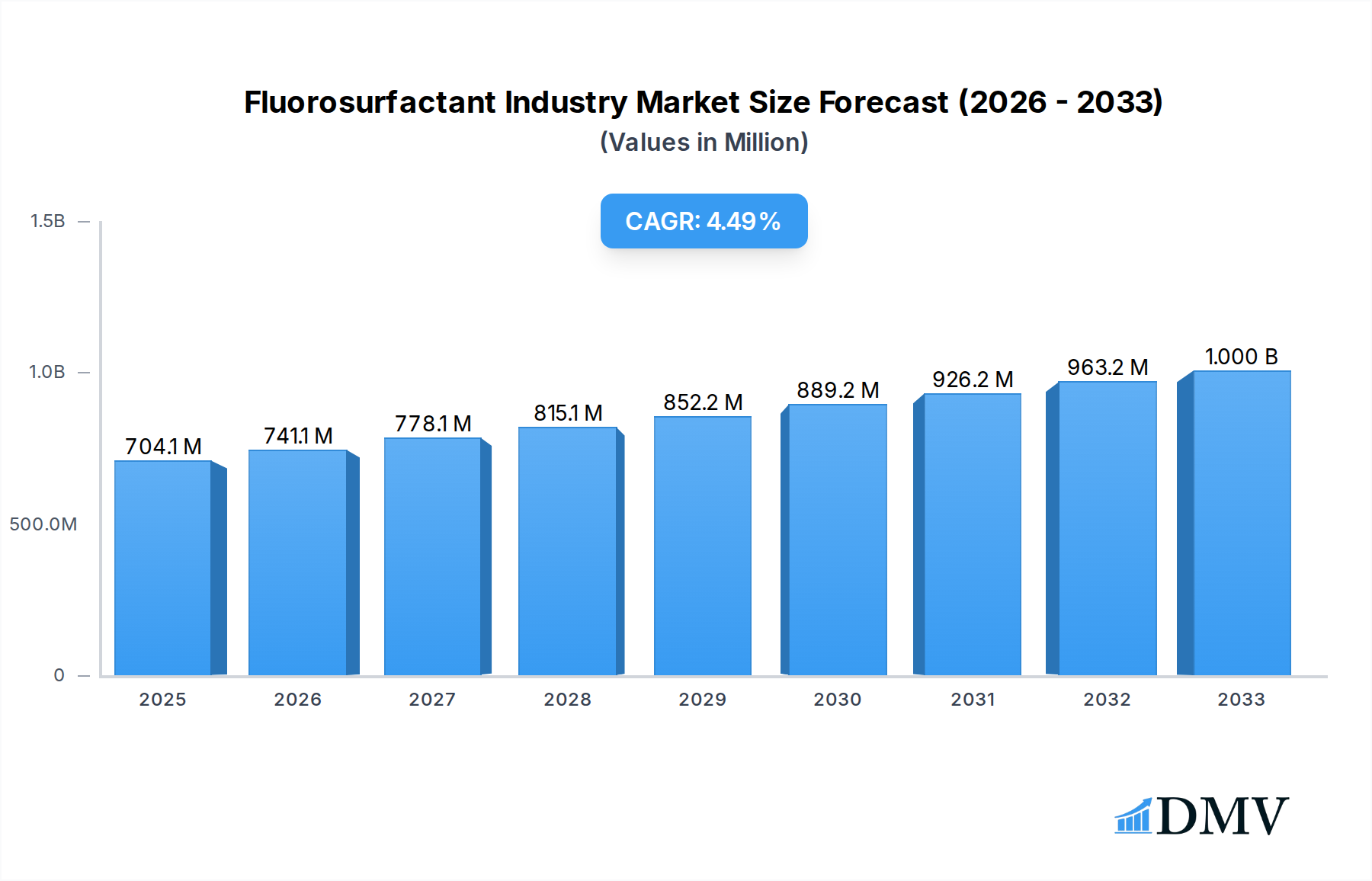

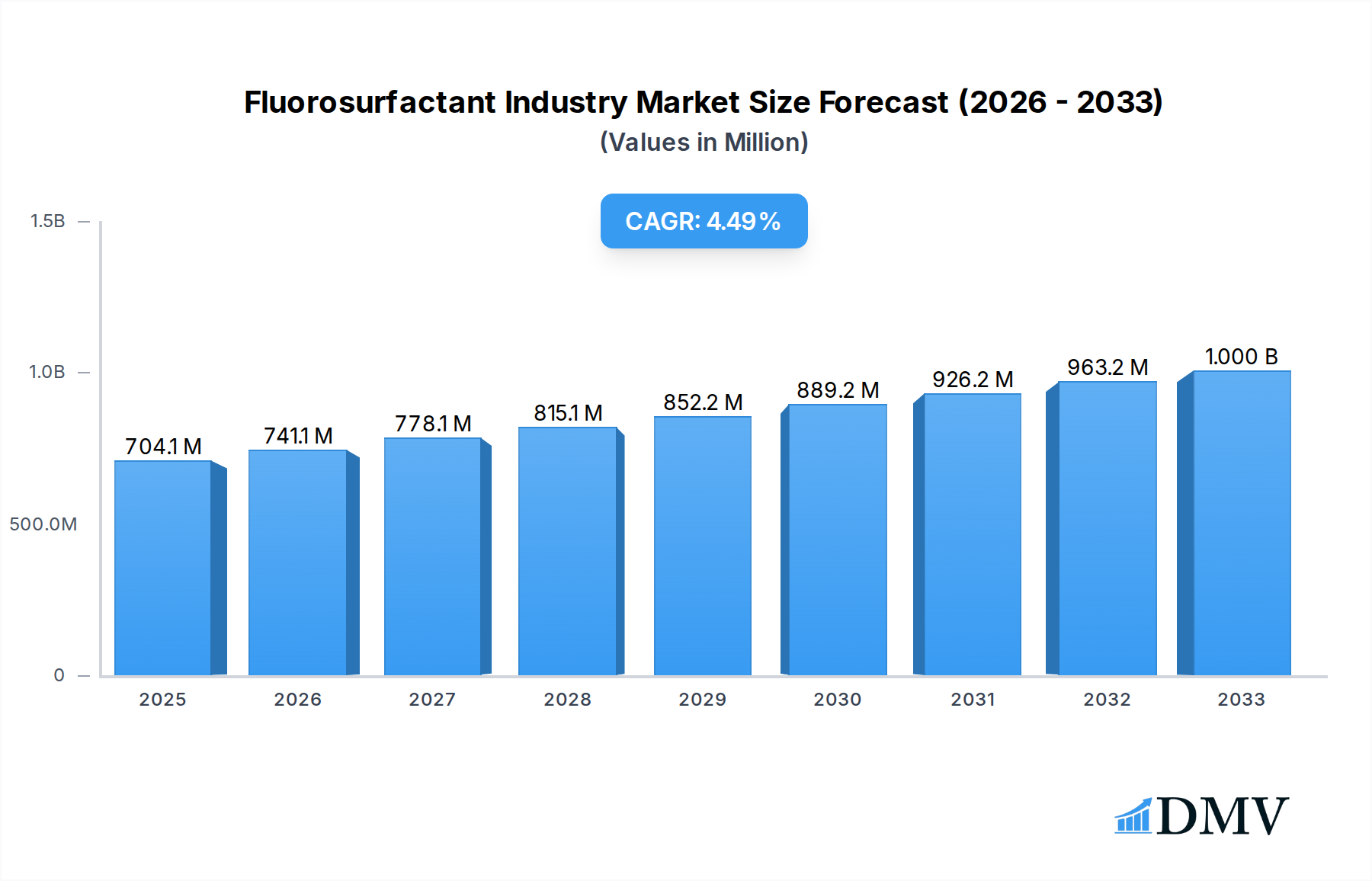

The global Fluorosurfactant market is poised for significant expansion, projected to reach $704.12 million by 2025, with a robust Compound Annual Growth Rate (CAGR) exceeding 5.00% during the forecast period of 2025-2033. This upward trajectory is primarily fueled by the escalating demand across diverse industrial applications, including paints and coatings, detergents and cleaning agents, and the oil and gas sector. The unique properties of fluorosurfactants, such as their exceptional surface tension reduction capabilities, thermal stability, and chemical inertness, make them indispensable in high-performance formulations. As industries increasingly prioritize efficiency, durability, and specialized functionalities, the adoption of fluorosurfactants is expected to witness sustained growth. Furthermore, the continuous innovation in product development and the exploration of new application areas, such as in advanced electronics and specialized automotive components, will act as significant growth accelerators.

Fluorosurfactant Industry Market Size (In Million)

The market's dynamism is also shaped by key trends that underscore its future direction. Advancements in environmentally friendlier fluorosurfactant chemistries are gaining traction as regulatory landscapes evolve. While traditional applications remain strong, emerging sectors are opening new avenues for market penetration. However, the market is not without its challenges. Stringent environmental regulations concerning per- and polyfluoroalkyl substances (PFAS), the broader category to which many fluorosurfactants belong, pose a restraint. This necessitates a focus on research and development for sustainable alternatives and improved manufacturing processes. Despite these hurdles, the intrinsic performance benefits offered by fluorosurfactants ensure their continued relevance and growth, particularly in specialized, high-value applications where performance cannot be compromised. Key players like CYTONIX, Merck KGaA, and 3M are at the forefront of innovation, driving market advancements.

Fluorosurfactant Industry Company Market Share

Fluorosurfactant Industry Market Composition & Trends

The global Fluorosurfactant market, projected to reach $5,000 Million by 2025, is characterized by a moderate to high concentration of key players, including CYTONIX, Merck KGaA, Innovative Chemical Technologies, 3M, Alfa Chemicals, The Chemours Company, MAFLON S p A, DYNAX, DIC CORPORATION, TCI EUROPE N V. Innovation remains a primary catalyst, driven by the demand for high-performance solutions in demanding applications. The regulatory landscape, particularly concerning PFAS compounds, is a significant factor influencing market dynamics and driving research into alternative chemistries. Substitute products, while emerging, often struggle to match the unique surface tension reduction properties and chemical resistance of fluorosurfactants, especially in specialized industrial sectors. End-user profiles span diverse industries, from demanding applications in Paints and Coatings and Oil and Gas to everyday use in Detergents and Cleaning Agents. M&A activities, though not always publicly disclosed in detail, are expected to continue as larger entities seek to consolidate market share and acquire innovative technologies. The M&A deal values are estimated to range from $50 Million to $500 Million as companies strategically position themselves.

Fluorosurfactant Industry Industry Evolution

The Fluorosurfactant industry has witnessed a dynamic evolution driven by relentless technological innovation and shifting end-user demands throughout the historical period of 2019-2024. The market has experienced a Compound Annual Growth Rate (CAGR) of approximately 5.5%, indicating a steady upward trajectory. Early in the study period, demand was primarily fueled by industrial applications requiring exceptional performance characteristics, such as extreme temperature resistance, low friction, and superior wetting properties. The Paints and Coatings sector, for instance, leveraged fluorosurfactants to enhance spreadability, leveling, and durability, contributing significantly to market growth. Similarly, the Oil and Gas industry utilized these chemicals in drilling fluids and enhanced oil recovery processes, where their ability to reduce interfacial tension under harsh conditions proved invaluable.

As the market matured, consumer-facing applications like Detergents and Cleaning Agents began to account for a larger share, benefiting from the enhanced cleaning efficacy and stain resistance provided by fluorosurfactants. Technological advancements have focused on improving the environmental profile of these chemicals, with a growing emphasis on shorter-chain fluorosurfactants and the development of more sustainable manufacturing processes. The introduction of new product formulations and the optimization of existing ones have allowed for broader adoption across various industries, including Adhesives, Flame Retardants, and specialized Other Applications like automotive components and electronic manufacturing. The industry's evolution is also marked by strategic responses to regulatory pressures, pushing research and development towards chemistries with reduced environmental persistence and bioaccumulation. This continuous adaptation and innovation have been crucial in sustaining the industry's growth and relevance in a rapidly changing global marketplace. The forecast period of 2025–2033 anticipates continued innovation, with a particular focus on sustainability and specialized high-performance niches.

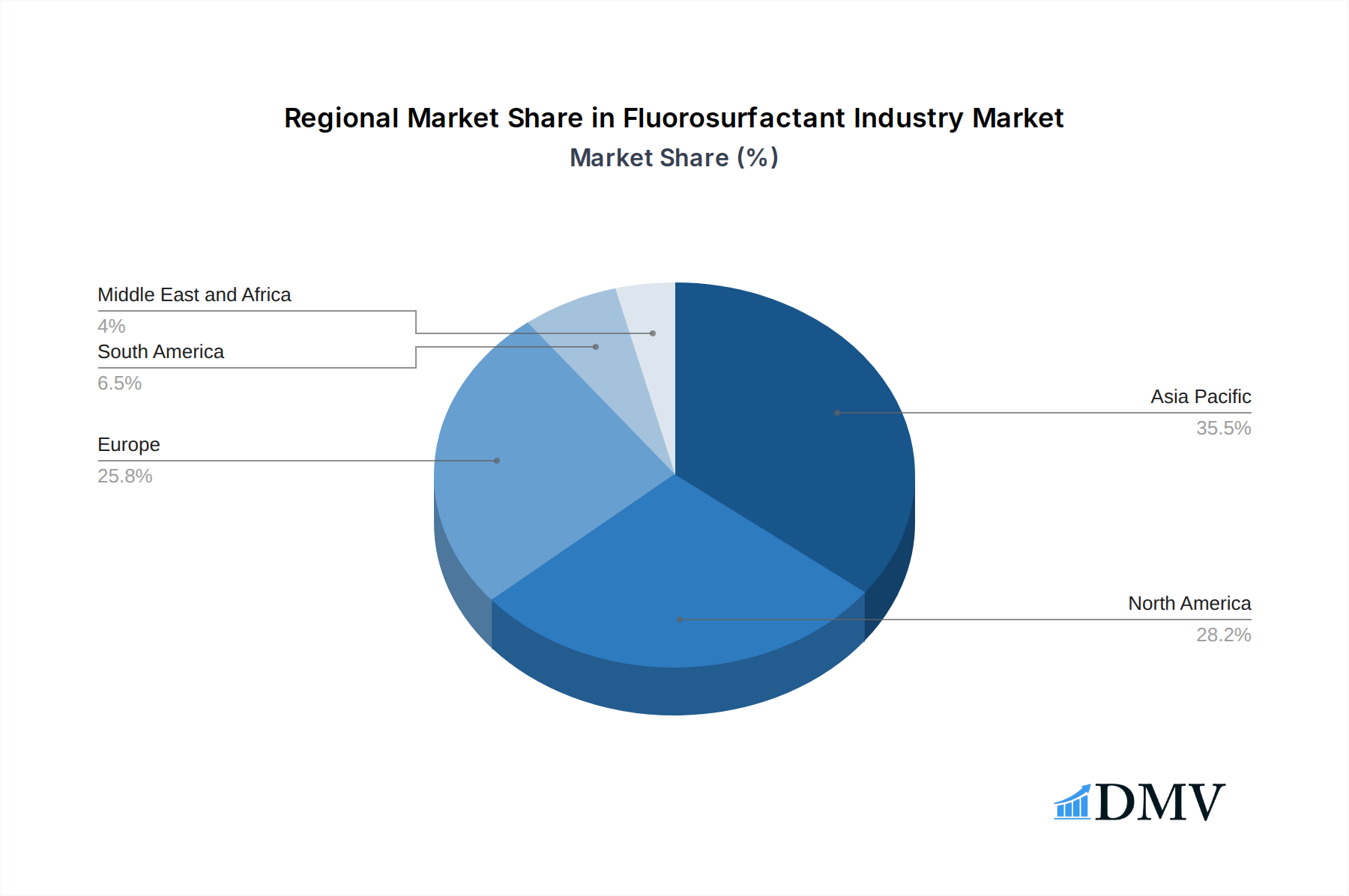

Leading Regions, Countries, or Segments in Fluorosurfactant Industry

The global Fluorosurfactant market's dominance is intricately linked to regional industrial strengths, regulatory environments, and application-specific demand. While a precise quantification of market share is complex, North America and Europe have historically been the leading regions, driven by established chemical manufacturing infrastructure and significant end-use industries. However, the Asia-Pacific region, particularly China, is experiencing rapid growth, fueled by its expanding manufacturing base and increasing investments in sectors such as electronics and automotive, which are key consumers of fluorosurfactants.

Within the Type segment, Non-ionic fluorosurfactants have consistently held a substantial market share due to their versatility and broad applicability across numerous industries. Their excellent wetting, emulsifying, and dispersing properties make them indispensable in Paints and Coatings, Detergents and Cleaning Agents, and Adhesives. Anionic fluorosurfactants also command a significant share, particularly in applications requiring strong detergency and emulsification, such as industrial cleaning solutions and fire-fighting foams. While Cationic and Amphoteric fluorosurfactants represent smaller segments, they cater to specialized applications where their unique charge characteristics are crucial, such as in specific textile treatments and personal care formulations.

In terms of Application, Paints and Coatings remain a cornerstone of the fluorosurfactant market. Their ability to improve surface properties, such as scratch resistance, stain repellency, and ease of cleaning, makes them highly sought after. The Detergents and Cleaning Agents segment is another major driver, where fluorosurfactants enhance cleaning performance and enable the formulation of low-VOC (Volatile Organic Compound) products. The Oil and Gas industry continues to be a critical application, utilizing fluorosurfactants for their effectiveness in extreme conditions. Emerging applications in Electronics (e.g., etching, semiconductor manufacturing) and Automotive (e.g., coatings, lubricants) are demonstrating substantial growth potential, contributing to the diversified demand landscape. The regulatory landscape surrounding PFAS compounds is a key factor influencing regional and segment growth, with stricter regulations potentially leading to a shift towards alternative or more sustainable fluorosurfactant chemistries in certain regions and applications.

Fluorosurfactant Industry Product Innovations

Product innovations in the Fluorosurfactant industry are largely driven by the pursuit of enhanced performance and improved environmental profiles. Companies are actively developing shorter-chain fluorosurfactants, offering comparable efficacy to longer-chain variants but with reduced persistence. Innovations focus on improved wetting, leveling, and de-aeration in paints and coatings, leading to smoother finishes and increased durability. In detergents, new formulations aim for superior stain removal and grease cutting with lower concentrations. Furthermore, advancements in encapsulation technologies are enabling controlled release of fluorosurfactant properties, optimizing their application in adhesives and specialized industrial processes. The unique selling proposition of many new products lies in their ability to deliver high-performance characteristics while addressing growing environmental concerns.

Propelling Factors for Fluorosurfactant Industry Growth

Several key factors are propelling the growth of the Fluorosurfactant industry. Technological advancements in developing more sustainable and environmentally friendly fluorosurfactant chemistries, such as shorter-chain alternatives, are opening up new market opportunities and addressing regulatory concerns. The increasing demand for high-performance materials across diverse sectors like electronics, automotive, and specialized coatings necessitates the unique properties offered by fluorosurfactants, including exceptional surface tension reduction, chemical resistance, and thermal stability. Economic growth, particularly in emerging economies, is driving increased industrial activity and consumer spending, leading to higher consumption of products that utilize fluorosurfactants. Moreover, evolving consumer preferences for durable, easy-to-clean, and high-performance products further stimulate demand.

Obstacles in the Fluorosurfactant Industry Market

Significant obstacles confront the Fluorosurfactant industry, primarily stemming from stringent regulatory scrutiny surrounding per- and polyfluoroalkyl substances (PFAS). Concerns regarding their environmental persistence and potential health impacts have led to bans and restrictions in various regions, creating a substantial barrier to market growth and necessitating costly research into alternatives. Supply chain disruptions, exacerbated by geopolitical factors and the complex manufacturing processes involved in producing fluorinated compounds, can lead to price volatility and availability issues. Furthermore, the high cost of production compared to conventional surfactants presents a competitive challenge, limiting adoption in price-sensitive applications. The ongoing regulatory pressure is estimated to impact market growth by 5-10% annually in affected regions.

Future Opportunities in Fluorosurfactant Industry

The Fluorosurfactant industry is poised for significant future opportunities driven by a confluence of factors. The growing emphasis on sustainability is spurring innovation in biodegradable and bio-based fluorosurfactant alternatives, creating new market segments. The expanding electronics and semiconductor industries present a substantial opportunity, requiring highly specialized fluorosurfactants for advanced manufacturing processes. The continued demand for high-performance coatings, adhesives, and specialty polymers in sectors like aerospace and renewable energy will also drive growth. Emerging economies with rapidly industrializing economies offer untapped markets for fluorosurfactant applications. Furthermore, advancements in material science and nanotechnology may unlock novel applications for fluorosurfactants, enhancing their performance and expanding their utility.

Major Players in the Fluorosurfactant Industry Ecosystem

- CYTONIX

- Merck KGaA

- Innovative Chemical Technologies

- 3M

- Alfa Chemicals

- The Chemours Company

- MAFLON S p A

- DYNAX

- DIC CORPORATION

- TCI EUROPE N V

Key Developments in Fluorosurfactant Industry Industry

- December 2022: 3M announced the exit of per-and polyfluoroalkyl substance (PFAS) manufacturing, signifying a major strategic shift in the industry and impacting the supply of certain fluorosurfactants. The company's commitment to discontinue the use of PFAS across its product portfolio by the end of 2025 will necessitate significant market adjustments and the adoption of alternative solutions by downstream users.

- March 2022: Alfa Chemistry launched a wide range of fluoro surfactants, including amphoteric surfactants, anionic surfactants, cationic surfactants, non-ionic surfactants, natural surfactants, and others. This launch broadens product availability and offers customers more diverse options, potentially stimulating demand and innovation within specific application segments.

Strategic Fluorosurfactant Industry Market Forecast

The Fluorosurfactant market forecast indicates continued resilience and strategic evolution, driven by ongoing technological advancements and a persistent demand for high-performance solutions. The emphasis on developing environmentally friendly and sustainable fluorosurfactant chemistries is expected to be a dominant growth catalyst, opening new avenues for market penetration. The burgeoning electronics and advanced materials sectors will continue to be significant consumers, requiring specialized fluorosurfactants for critical manufacturing processes. Furthermore, the increasing global industrialization, particularly in emerging economies, presents substantial untapped market potential. Strategic partnerships and M&A activities are likely to shape the competitive landscape, fostering consolidation and driving innovation to meet evolving regulatory requirements and consumer expectations for efficacy and sustainability.

Fluorosurfactant Industry Segmentation

-

1. Type

- 1.1. Anionic

- 1.2. Cationic

- 1.3. Non-ionic

- 1.4. Amphoteric

-

2. Application

- 2.1. Paints and Coatings

- 2.2. Detergents and Cleaning Agents

- 2.3. Oil and Gas

- 2.4. Flame Retardants

- 2.5. Adhesives

- 2.6. Other Applications (Automotive, Electronics, etc.)

Fluorosurfactant Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. France

- 3.4. Italy

- 3.5. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. Saudi Arabia

- 5.2. South Africa

- 5.3. Rest of Middle East and Africa

Fluorosurfactant Industry Regional Market Share

Geographic Coverage of Fluorosurfactant Industry

Fluorosurfactant Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of > 5.00% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Anionic

- 5.1.2. Cationic

- 5.1.3. Non-ionic

- 5.1.4. Amphoteric

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Paints and Coatings

- 5.2.2. Detergents and Cleaning Agents

- 5.2.3. Oil and Gas

- 5.2.4. Flame Retardants

- 5.2.5. Adhesives

- 5.2.6. Other Applications (Automotive, Electronics, etc.)

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.3.2. North America

- 5.3.3. Europe

- 5.3.4. South America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Fluorosurfactant Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Anionic

- 6.1.2. Cationic

- 6.1.3. Non-ionic

- 6.1.4. Amphoteric

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Paints and Coatings

- 6.2.2. Detergents and Cleaning Agents

- 6.2.3. Oil and Gas

- 6.2.4. Flame Retardants

- 6.2.5. Adhesives

- 6.2.6. Other Applications (Automotive, Electronics, etc.)

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Asia Pacific Fluorosurfactant Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Anionic

- 7.1.2. Cationic

- 7.1.3. Non-ionic

- 7.1.4. Amphoteric

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Paints and Coatings

- 7.2.2. Detergents and Cleaning Agents

- 7.2.3. Oil and Gas

- 7.2.4. Flame Retardants

- 7.2.5. Adhesives

- 7.2.6. Other Applications (Automotive, Electronics, etc.)

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. North America Fluorosurfactant Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Anionic

- 8.1.2. Cationic

- 8.1.3. Non-ionic

- 8.1.4. Amphoteric

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Paints and Coatings

- 8.2.2. Detergents and Cleaning Agents

- 8.2.3. Oil and Gas

- 8.2.4. Flame Retardants

- 8.2.5. Adhesives

- 8.2.6. Other Applications (Automotive, Electronics, etc.)

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Europe Fluorosurfactant Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Anionic

- 9.1.2. Cationic

- 9.1.3. Non-ionic

- 9.1.4. Amphoteric

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Paints and Coatings

- 9.2.2. Detergents and Cleaning Agents

- 9.2.3. Oil and Gas

- 9.2.4. Flame Retardants

- 9.2.5. Adhesives

- 9.2.6. Other Applications (Automotive, Electronics, etc.)

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. South America Fluorosurfactant Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Anionic

- 10.1.2. Cationic

- 10.1.3. Non-ionic

- 10.1.4. Amphoteric

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Paints and Coatings

- 10.2.2. Detergents and Cleaning Agents

- 10.2.3. Oil and Gas

- 10.2.4. Flame Retardants

- 10.2.5. Adhesives

- 10.2.6. Other Applications (Automotive, Electronics, etc.)

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Middle East and Africa Fluorosurfactant Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Anionic

- 11.1.2. Cationic

- 11.1.3. Non-ionic

- 11.1.4. Amphoteric

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Paints and Coatings

- 11.2.2. Detergents and Cleaning Agents

- 11.2.3. Oil and Gas

- 11.2.4. Flame Retardants

- 11.2.5. Adhesives

- 11.2.6. Other Applications (Automotive, Electronics, etc.)

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 CYTONIX

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Merck KGaA

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Innovative Chemical Technologies

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 3M

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Alfa Chemicals

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 The Chemours Company*List Not Exhaustive

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 MAFLON S p A

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 DYNAX

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 DIC CORPORATION

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 TCI EUROPE N V

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 CYTONIX

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Fluorosurfactant Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Asia Pacific Fluorosurfactant Industry Revenue (Million), by Type 2025 & 2033

- Figure 3: Asia Pacific Fluorosurfactant Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: Asia Pacific Fluorosurfactant Industry Revenue (Million), by Application 2025 & 2033

- Figure 5: Asia Pacific Fluorosurfactant Industry Revenue Share (%), by Application 2025 & 2033

- Figure 6: Asia Pacific Fluorosurfactant Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: Asia Pacific Fluorosurfactant Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: North America Fluorosurfactant Industry Revenue (Million), by Type 2025 & 2033

- Figure 9: North America Fluorosurfactant Industry Revenue Share (%), by Type 2025 & 2033

- Figure 10: North America Fluorosurfactant Industry Revenue (Million), by Application 2025 & 2033

- Figure 11: North America Fluorosurfactant Industry Revenue Share (%), by Application 2025 & 2033

- Figure 12: North America Fluorosurfactant Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: North America Fluorosurfactant Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Fluorosurfactant Industry Revenue (Million), by Type 2025 & 2033

- Figure 15: Europe Fluorosurfactant Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Europe Fluorosurfactant Industry Revenue (Million), by Application 2025 & 2033

- Figure 17: Europe Fluorosurfactant Industry Revenue Share (%), by Application 2025 & 2033

- Figure 18: Europe Fluorosurfactant Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Europe Fluorosurfactant Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: South America Fluorosurfactant Industry Revenue (Million), by Type 2025 & 2033

- Figure 21: South America Fluorosurfactant Industry Revenue Share (%), by Type 2025 & 2033

- Figure 22: South America Fluorosurfactant Industry Revenue (Million), by Application 2025 & 2033

- Figure 23: South America Fluorosurfactant Industry Revenue Share (%), by Application 2025 & 2033

- Figure 24: South America Fluorosurfactant Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: South America Fluorosurfactant Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Fluorosurfactant Industry Revenue (Million), by Type 2025 & 2033

- Figure 27: Middle East and Africa Fluorosurfactant Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: Middle East and Africa Fluorosurfactant Industry Revenue (Million), by Application 2025 & 2033

- Figure 29: Middle East and Africa Fluorosurfactant Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Middle East and Africa Fluorosurfactant Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Middle East and Africa Fluorosurfactant Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Fluorosurfactant Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Global Fluorosurfactant Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 3: Global Fluorosurfactant Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Fluorosurfactant Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 5: Global Fluorosurfactant Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 6: Global Fluorosurfactant Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: China Fluorosurfactant Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: India Fluorosurfactant Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Japan Fluorosurfactant Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: South Korea Fluorosurfactant Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Rest of Asia Pacific Fluorosurfactant Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Global Fluorosurfactant Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 13: Global Fluorosurfactant Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 14: Global Fluorosurfactant Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 15: United States Fluorosurfactant Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Canada Fluorosurfactant Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Mexico Fluorosurfactant Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Global Fluorosurfactant Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 19: Global Fluorosurfactant Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 20: Global Fluorosurfactant Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 21: Germany Fluorosurfactant Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: United Kingdom Fluorosurfactant Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: France Fluorosurfactant Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Italy Fluorosurfactant Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Rest of Europe Fluorosurfactant Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Global Fluorosurfactant Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 27: Global Fluorosurfactant Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 28: Global Fluorosurfactant Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 29: Brazil Fluorosurfactant Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Argentina Fluorosurfactant Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 31: Rest of South America Fluorosurfactant Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Global Fluorosurfactant Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 33: Global Fluorosurfactant Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 34: Global Fluorosurfactant Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 35: Saudi Arabia Fluorosurfactant Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: South Africa Fluorosurfactant Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: Rest of Middle East and Africa Fluorosurfactant Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Fluorosurfactant Industry?

The projected CAGR is approximately > 5.00%.

2. Which companies are prominent players in the Fluorosurfactant Industry?

Key companies in the market include CYTONIX, Merck KGaA, Innovative Chemical Technologies, 3M, Alfa Chemicals, The Chemours Company*List Not Exhaustive, MAFLON S p A, DYNAX, DIC CORPORATION, TCI EUROPE N V.

3. What are the main segments of the Fluorosurfactant Industry?

The market segments include Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 704.12 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand From the Paints and Coatings Industry; Increasing Application of Flurosurfactants in Oil Field; Other Drivers.

6. What are the notable trends driving market growth?

Growing Demand from the Paints and Coatings Industry.

7. Are there any restraints impacting market growth?

Higher Price Compared to Other Surfactants; Other Restraints.

8. Can you provide examples of recent developments in the market?

December 2022: 3M announced the exit of per-and polyfluoroalkyl substance (PFAS) manufacturing. The company will discontinue the use of PFAS across its product portfolio by the end of 2025.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Fluorosurfactant Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Fluorosurfactant Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Fluorosurfactant Industry?

To stay informed about further developments, trends, and reports in the Fluorosurfactant Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence