Key Insights

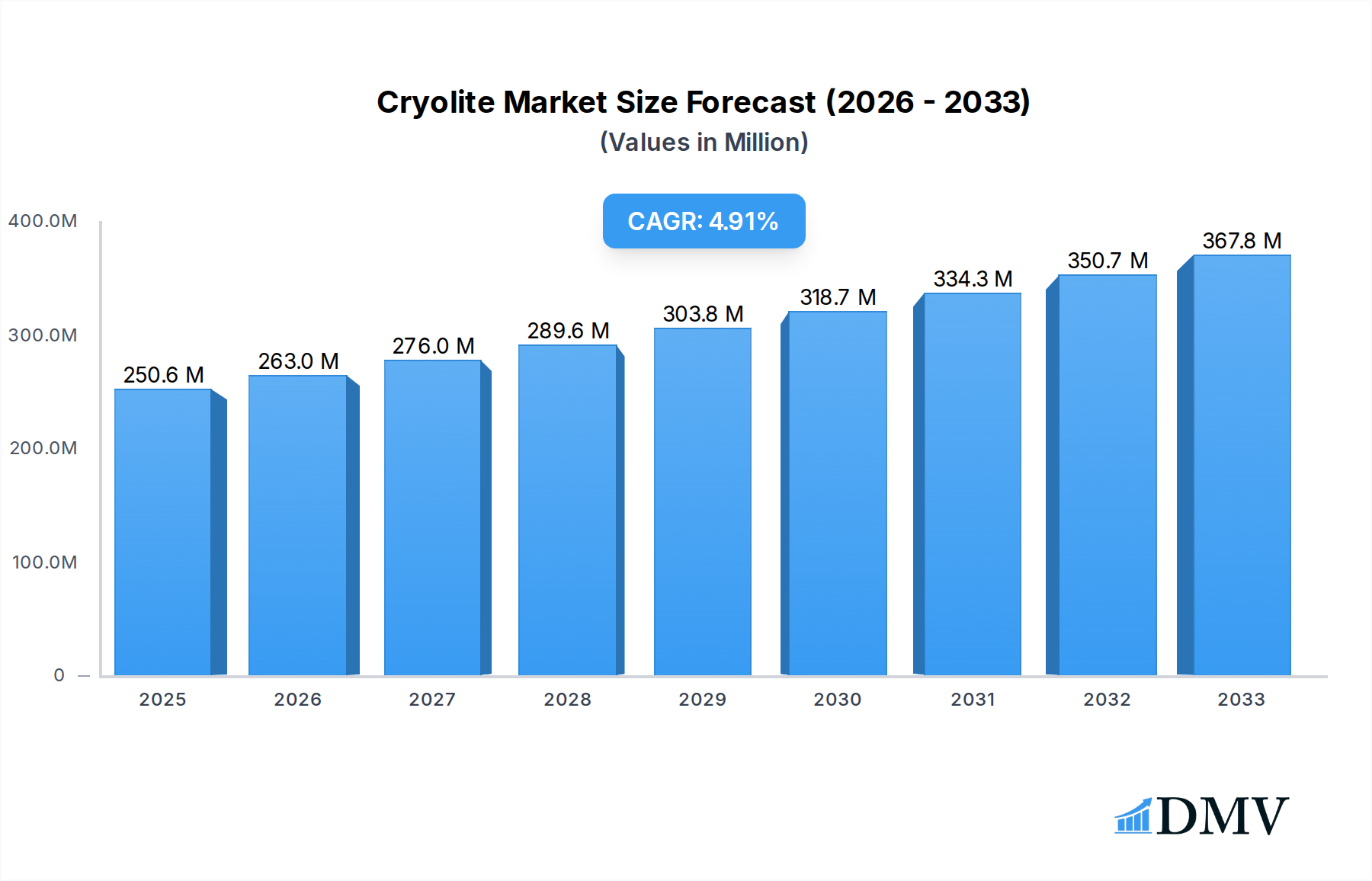

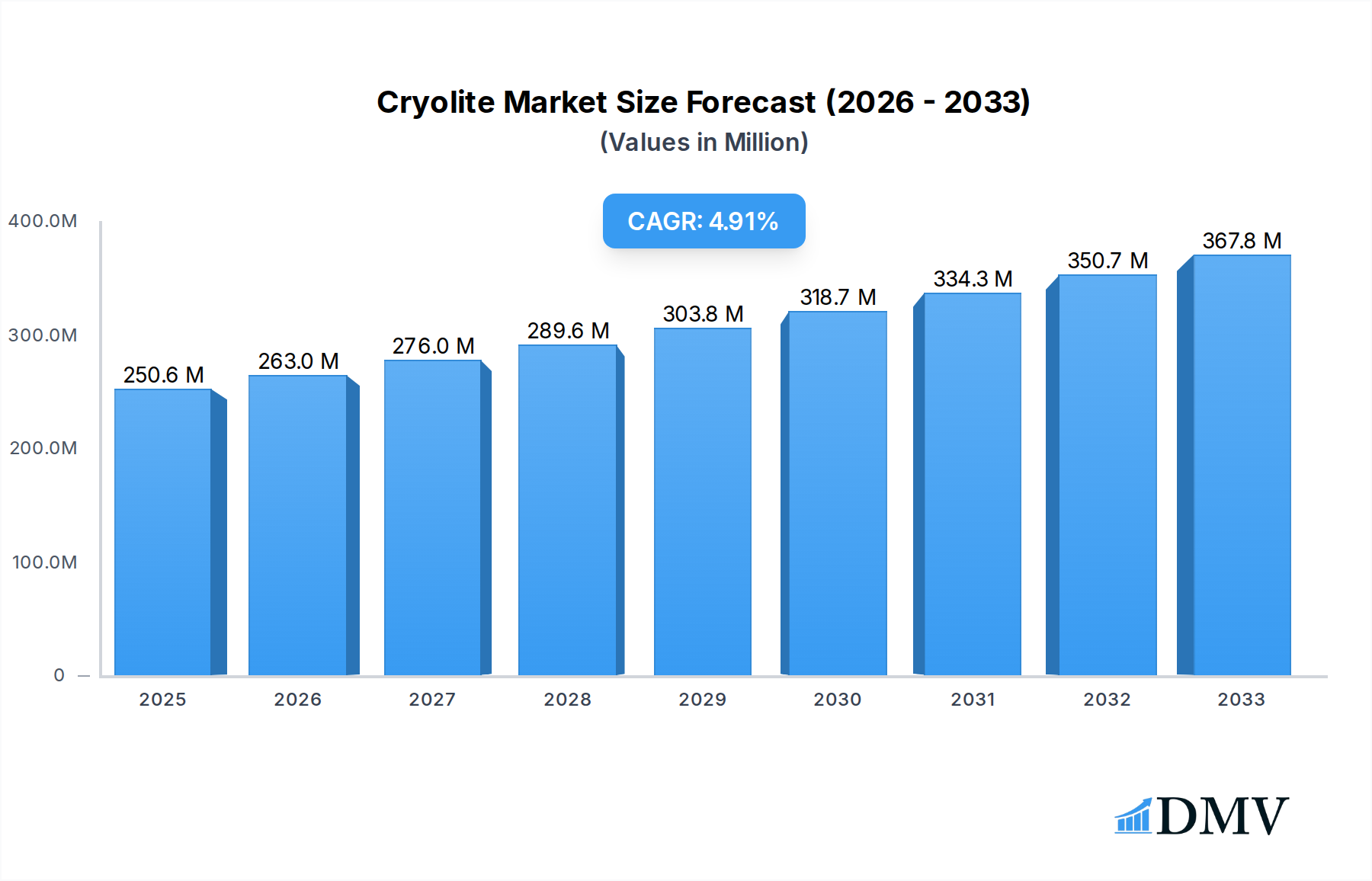

The global cryolite market is poised for robust expansion, projected to reach $250.6 million in 2025 with a Compound Annual Growth Rate (CAGR) of 4.9% through 2033. This growth is fueled by the indispensable role of cryolite as a key raw material in various industrial applications, most notably in the production of aluminum metal through the Hall-Héroult process. The increasing global demand for aluminum, driven by its widespread use in the automotive, aerospace, and construction sectors for its lightweight and durable properties, directly translates into a sustained demand for cryolite. Furthermore, its application as an opacifier in enamels, ceramics, and glass manufacturing, along with its use as a coloring agent, contributes significantly to market impetus. Emerging economies, particularly in Asia Pacific, are expected to be major growth contributors due to rapid industrialization and infrastructure development.

Cryolite Market Size (In Million)

While the primary driver remains aluminum production, the market also benefits from its unique chemical properties that lend themselves to diverse applications. The growing emphasis on sustainable manufacturing practices and the search for efficient industrial processes are likely to further solidify cryolite's position. However, the market may face certain challenges, including the volatility of raw material prices, particularly fluorspar, which is a precursor to cryolite. Stringent environmental regulations pertaining to the mining and processing of fluorides could also pose a restraint. Nevertheless, ongoing research and development into enhanced production methods and potential new applications are expected to mitigate these challenges and ensure continued market vitality. The market is segmented by application into Coloring Agent, Opacifier, and Others, and by type into Synthetic Cryolite, Pure Cryolite, and Others, with synthetic cryolite holding a dominant share.

Cryolite Company Market Share

Cryolite Market Composition & Trends

The global Cryolite market, a critical component in various industrial applications, exhibits a dynamic and evolving landscape. Market concentration is moderately fragmented, with key players vying for market share through technological innovation and strategic expansions. Innovation catalysts are primarily driven by the demand for enhanced performance in aluminum smelting, glass manufacturing, and the production of enamels and glazes. The regulatory landscape, while generally supportive of cryolite's essential functions, is increasingly focusing on environmental impact and sustainable production methods. Substitute products, such as aluminum fluoride, pose a competitive threat, particularly in certain aluminum smelting processes, but cryolite maintains a strong foothold due to its specific electrochemical properties and cost-effectiveness. End-user profiles are diverse, spanning the aluminum industry, glass and ceramics manufacturers, and specialized chemical producers. Mergers and acquisitions (M&A) activity, though not intensely high, plays a role in market consolidation and the expansion of capabilities. Recent M&A deal values have been in the range of tens to hundreds of million dollars, signifying strategic realignments and capacity enhancements within the industry. Understanding these intricate market dynamics is crucial for stakeholders seeking to navigate the cryolite market effectively.

- Market Share Distribution: While specific current figures are proprietary, analysis suggests leading companies hold significant, but not dominant, portions of the market, indicating room for new entrants and mid-tier players.

- M&A Deal Values: Past transactions have ranged from XX million to XX million USD, reflecting strategic investments in production capacity and market access.

- Innovation Focus: Research and development efforts are concentrated on improving purity levels, reducing energy consumption in production, and exploring novel applications beyond traditional uses.

- Regulatory Influence: Environmental compliance and safety standards are increasingly shaping production processes and product formulations, impacting operational costs and market entry barriers.

- Substitute Threat Analysis: The competitive advantage of alternatives like aluminum fluoride is assessed based on price volatility of raw materials and the specific technical requirements of end-user processes.

Cryolite Industry Evolution

The cryolite industry has undergone a significant transformation over the historical period of 2019–2024, and its trajectory promises continued evolution through the forecast period of 2025–2033. From 2019 to 2024, the market witnessed steady growth, largely propelled by the robust demand from the aluminum smelting sector, which accounts for a substantial portion of cryolite consumption. This period was characterized by a focus on optimizing production efficiencies and ensuring consistent quality to meet the stringent requirements of this primary application. Technological advancements during these years primarily revolved around refining synthesis processes to enhance purity and reduce energy intensity, leading to a projected estimated year value of XX million in production volume. The adoption of advanced control systems and automation in cryolite manufacturing facilities contributed to improved output and reduced operational costs, creating a more competitive market environment. Shifting consumer demands, though less direct for cryolite itself, influenced its end-use industries. For instance, the growing global demand for electric vehicles, which require lighter materials like aluminum, indirectly boosted cryolite consumption. Furthermore, increased awareness regarding sustainable manufacturing practices has spurred research into more environmentally friendly production methods and the potential for recycling cryolite-containing materials. This evolution is reflected in the market growth trajectory, which has seen a compound annual growth rate (CAGR) of approximately XX% during the historical period. Looking ahead, the forecast period of 2025–2033 is expected to see a continuation of this growth, albeit with potential moderations influenced by global economic shifts and the increasing emphasis on green technologies. The base year of 2025 is projected to set a strong foundation for this expansion, with an anticipated market size of XX million USD. The industry will likely witness further technological innovations, including potentially novel synthesis routes and enhanced purification techniques, to address evolving environmental regulations and market expectations for higher-performance materials. Consumer demand for products that utilize aluminum, such as in packaging, construction, and transportation, will remain a key driver, ensuring sustained relevance for cryolite.

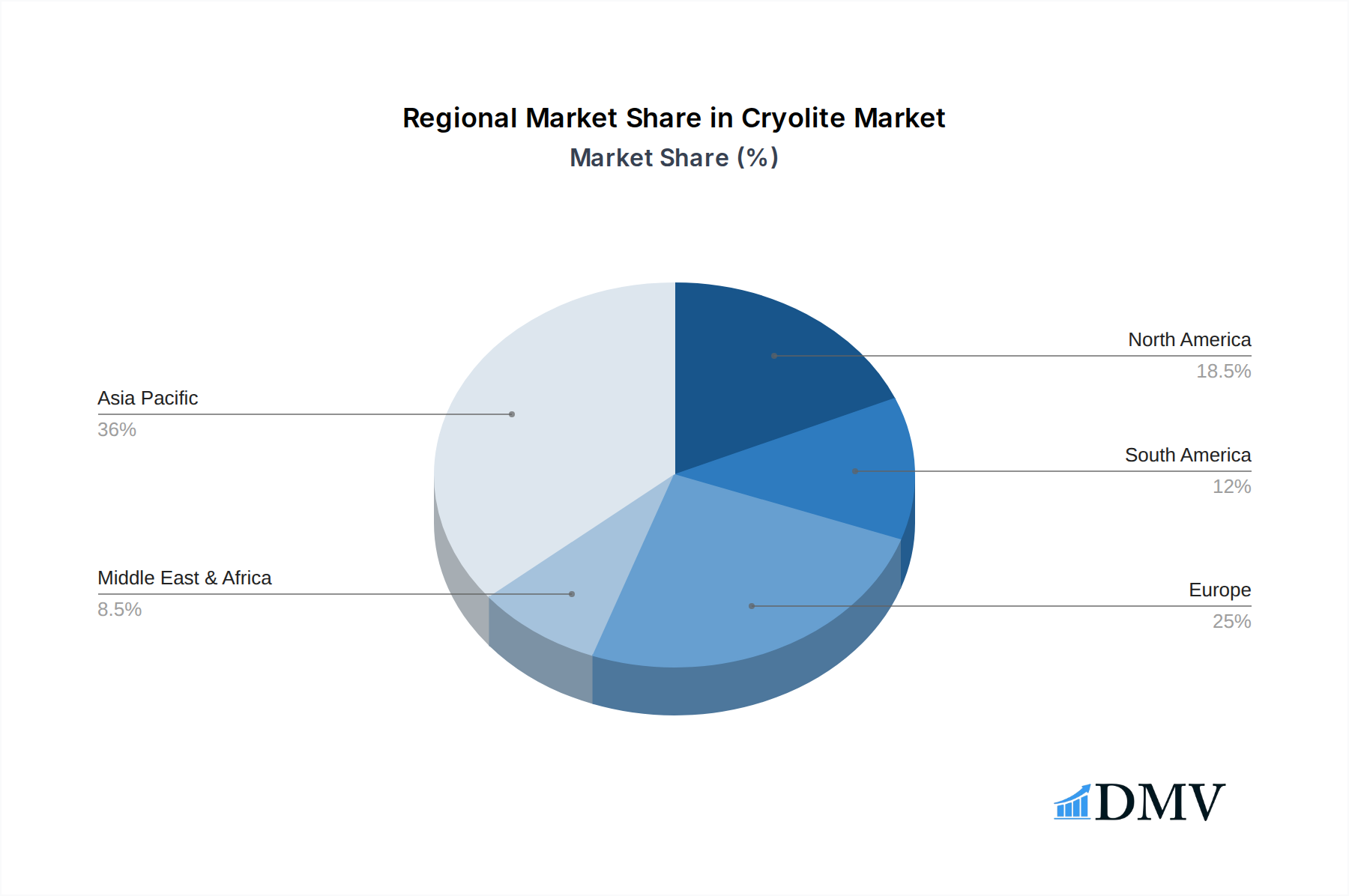

Leading Regions, Countries, or Segments in Cryolite

The global cryolite market is characterized by distinct regional strengths and segment dominance, with Asia-Pacific emerging as the undisputed leader in both production and consumption, driven by its colossal manufacturing base and burgeoning industrial sectors. Within the application segments, the Opacifier segment holds significant sway, particularly in the glass and ceramics industries, where cryolite's ability to impart whiteness and opacity is highly valued. Its use as an opacifier in enamels and glazes for sanitaryware, tableware, and industrial coatings contributes to its substantial market share. Another critical application, Coloring Agent, also plays a vital role, especially in the production of specialty glass and pigments. The demand for aesthetically pleasing and durable colored products continues to fuel growth in this area.

The dominant type of cryolite in terms of market volume and value is Synthetic Cryolite. This is primarily due to the large-scale industrial processes, especially aluminum smelting, that rely on synthesized forms to meet purity and volume requirements. Synthetic cryolite offers greater control over its chemical composition and physical properties, making it ideal for demanding industrial applications.

Key drivers for the dominance of the Asia-Pacific region include:

- Massive Aluminum Production: Countries like China are global powerhouses in aluminum smelting, which is the largest consumer of cryolite. This industrial concentration directly translates to high demand.

- Expansive Manufacturing Ecosystem: The region hosts a vast array of industries that utilize cryolite, including glass manufacturing, ceramic production, and the chemical industry, creating a diversified demand base.

- Favorable Investment Climate: Significant foreign and domestic investments in manufacturing infrastructure and technological upgrades within the Asia-Pacific region have supported the growth of cryolite production and consumption.

- Cost-Effective Production: Relatively lower manufacturing costs and readily available raw materials in some Asia-Pacific countries contribute to competitive pricing, further bolstering market dominance.

In terms of application, the dominance of the Opacifier segment is fueled by:

- Growth in Construction and Home Goods: Increasing demand for aesthetically appealing and durable building materials, sanitaryware, and household items drives the use of opacifiers in ceramics and enamels.

- Industrial Coatings: The use of cryolite-based enamels and glazes in industrial applications for corrosion resistance and decorative finishes contributes significantly to its market share.

The leadership of Synthetic Cryolite is attributed to:

- Scalability and Purity Control: Industrial processes require large volumes of cryolite with precise specifications, which synthetic production methods are best equipped to deliver.

- Cost-Effectiveness for Large-Scale Use: For high-volume applications like aluminum smelting, synthetic cryolite offers a more economical solution compared to naturally sourced alternatives.

The study period of 2019–2033, with a base year of 2025, positions the Asia-Pacific region to maintain its lead, with projected market share expansion due to continued industrial growth and technological advancements in its manufacturing sectors. The estimated year of 2025 sees this dominance firmly in place, with substantial contributions from countries like China, India, and Southeast Asian nations.

Cryolite Product Innovations

Recent product innovations in the cryolite market are centered on enhancing purity levels and developing novel formulations for specialized applications. Manufacturers are focusing on producing cryolite with fewer impurities to meet the stringent demands of high-tech industries. Advances in synthesis and purification techniques have led to the development of ultra-pure cryolite, crucial for applications in advanced optics and certain electronic components where even trace contaminants can degrade performance. Furthermore, research is exploring cryolite's potential as a component in new composite materials, aiming to leverage its unique physical and chemical properties for enhanced strength, thermal resistance, or conductivity. Performance metrics being optimized include particle size distribution for better dispersion in various matrices and improved thermal stability for high-temperature applications. The unique selling proposition of these innovations lies in their ability to unlock new market segments and provide advanced solutions beyond traditional uses, driving efficiency and performance for end-users.

Propelling Factors for Cryolite Growth

Several key factors are propelling the growth of the cryolite market. The sustained demand from the aluminum smelting industry remains a primary driver, as aluminum is increasingly used in lightweight automotive components and construction. Technological advancements in cryolite production, leading to higher purity and improved efficiency, are making it more attractive for existing and new applications. Furthermore, the growth of the glass and ceramics industries, particularly in emerging economies, significantly contributes to cryolite's demand as an opacifier and coloring agent. Favorable regulatory environments, coupled with an increasing focus on industrial development in various regions, also support market expansion.

Obstacles in the Cryolite Market

Despite positive growth prospects, the cryolite market faces several obstacles. Fluctuations in the prices of raw materials essential for cryolite production, such as fluorspar and aluminum hydroxide, can impact profitability and market stability. Stringent environmental regulations concerning the mining and processing of raw materials and the disposal of by-products can increase operational costs and pose compliance challenges. The availability and adoption of substitute materials, like aluminum fluoride in certain aluminum smelting processes, also represent a competitive pressure. Additionally, supply chain disruptions, exacerbated by geopolitical events and logistical complexities, can hinder timely delivery and impact market dynamics.

Future Opportunities in Cryolite

Emerging opportunities in the cryolite market are diverse and promising. The growing demand for high-performance materials in advanced manufacturing, including aerospace and electronics, presents a significant avenue for ultra-pure cryolite. Expansion into new geographical markets with developing industrial bases offers substantial growth potential. Furthermore, ongoing research into novel applications of cryolite, such as in specialized ceramics, refractory materials, and even as a flux in certain metallurgical processes, could unlock entirely new revenue streams. The increasing focus on sustainable technologies may also lead to opportunities in developing eco-friendlier production methods and exploring the recyclability of cryolite-containing waste streams.

Major Players in the Cryolite Ecosystem

- Do Fluoride Chemicals

- Fluorsid

- S.B. Chemicals

- Xinhai Chemicals

- Yuzhou Deyi Chemical

- Zhengzhou Flworld Chemical

- Henan Buckton Industry & Commerce

Key Developments in Cryolite Industry

- 2023/Q4: Announcement of expanded production capacity for synthetic cryolite by a leading manufacturer in Asia, aiming to meet rising global demand from the aluminum sector.

- 2023/Q3: Introduction of a new, higher-purity grade of cryolite designed for specialized glass applications, offering enhanced optical properties.

- 2022/Q2: Strategic partnership formed between two key players to invest in R&D for more sustainable cryolite production methods.

- 2021/Q1: Regulatory approval granted for enhanced environmental controls at several major cryolite production facilities, ensuring compliance with stricter emission standards.

- 2020/Q4: Launch of a new cryolite-based opacifier with improved dispersion characteristics for ceramic glazes, leading to wider adoption in the sanitaryware industry.

Strategic Cryolite Market Forecast

The strategic cryolite market forecast indicates sustained growth driven by robust demand in its core applications and emerging opportunities. The aluminum industry's continued expansion, coupled with advancements in glass and ceramic manufacturing, will ensure a steady influx of demand. Innovations in cryolite production, focusing on higher purity and reduced environmental impact, will further solidify its market position and unlock new high-value applications. The forecast period of 2025–2033 is expected to witness a CAGR of approximately XX%, with the market size projected to reach XX million USD by 2033. Strategic investments in production capacity and technological upgrades will be crucial for market players to capitalize on these future opportunities and navigate potential challenges effectively.

Cryolite Segmentation

-

1. Application

- 1.1. Coloring Agent

- 1.2. Opacifier

- 1.3. Others

-

2. Types

- 2.1. Synthetic Cryolite

- 2.2. Pure Cryolite

- 2.3. Others

Cryolite Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Cryolite Regional Market Share

Geographic Coverage of Cryolite

Cryolite REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Coloring Agent

- 5.1.2. Opacifier

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Synthetic Cryolite

- 5.2.2. Pure Cryolite

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Cryolite Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Coloring Agent

- 6.1.2. Opacifier

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Synthetic Cryolite

- 6.2.2. Pure Cryolite

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Cryolite Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Coloring Agent

- 7.1.2. Opacifier

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Synthetic Cryolite

- 7.2.2. Pure Cryolite

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Cryolite Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Coloring Agent

- 8.1.2. Opacifier

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Synthetic Cryolite

- 8.2.2. Pure Cryolite

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Cryolite Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Coloring Agent

- 9.1.2. Opacifier

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Synthetic Cryolite

- 9.2.2. Pure Cryolite

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Cryolite Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Coloring Agent

- 10.1.2. Opacifier

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Synthetic Cryolite

- 10.2.2. Pure Cryolite

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Cryolite Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Coloring Agent

- 11.1.2. Opacifier

- 11.1.3. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Synthetic Cryolite

- 11.2.2. Pure Cryolite

- 11.2.3. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Do Fluoride Chemicals

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Fluorsid

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 S.B. Chemicals

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Xinhai Chemicals

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Yuzhou Deyi Chemical

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Zhengzhou Flworld Chemical

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Henan Buckton Industry & Commerce

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.1 Do Fluoride Chemicals

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Cryolite Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Cryolite Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Cryolite Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Cryolite Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Cryolite Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Cryolite Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Cryolite Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Cryolite Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Cryolite Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Cryolite Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Cryolite Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Cryolite Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Cryolite Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Cryolite Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Cryolite Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Cryolite Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Cryolite Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Cryolite Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Cryolite Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Cryolite Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Cryolite Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Cryolite Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Cryolite Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Cryolite Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Cryolite Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Cryolite Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Cryolite Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Cryolite Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Cryolite Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Cryolite Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Cryolite Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Cryolite Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Cryolite Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Cryolite Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Cryolite Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Cryolite Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Cryolite Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Cryolite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Cryolite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Cryolite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Cryolite Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Cryolite Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Cryolite Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Cryolite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Cryolite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Cryolite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Cryolite Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Cryolite Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Cryolite Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Cryolite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Cryolite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Cryolite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Cryolite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Cryolite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Cryolite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Cryolite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Cryolite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Cryolite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Cryolite Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Cryolite Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Cryolite Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Cryolite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Cryolite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Cryolite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Cryolite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Cryolite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Cryolite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Cryolite Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Cryolite Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Cryolite Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Cryolite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Cryolite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Cryolite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Cryolite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Cryolite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Cryolite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Cryolite Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Cryolite?

The projected CAGR is approximately 4.9%.

2. Which companies are prominent players in the Cryolite?

Key companies in the market include Do Fluoride Chemicals, Fluorsid, S.B. Chemicals, Xinhai Chemicals, Yuzhou Deyi Chemical, Zhengzhou Flworld Chemical, Henan Buckton Industry & Commerce.

3. What are the main segments of the Cryolite?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Cryolite," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Cryolite report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Cryolite?

To stay informed about further developments, trends, and reports in the Cryolite, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence