Key Insights

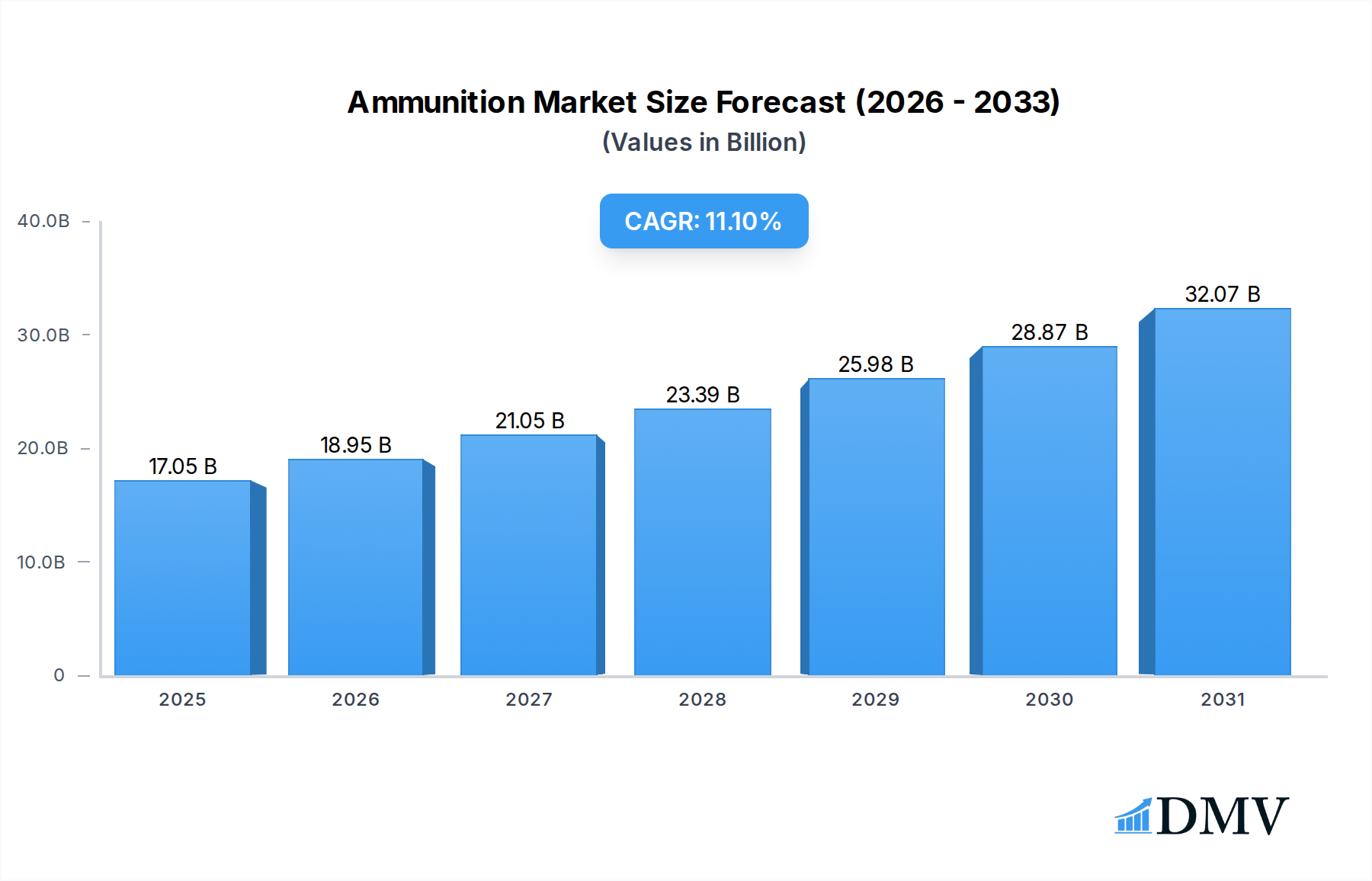

The global Ammunition Market is poised for substantial expansion, with a projected valuation reaching 15350 million by 2034. This significant growth trajectory is underpinned by a robust Compound Annual Growth Rate (CAGR) of 11.1% over the forecast period. The market's resilience and forward momentum are primarily fueled by a complex interplay of geopolitical instability, escalating global defense expenditures, and a steady increase in civilian firearm ownership driven by recreational shooting, hunting, and self-defense motives. The demand spans across various product types, including the Centerfire Ammunition Market, which continues to dominate due to its versatility and widespread application in both military and civilian sectors.

Ammunition Market Size (In Billion)

Macroeconomic tailwinds include the ongoing modernization efforts by armed forces worldwide, requiring technologically advanced and precise ammunition systems. Emerging economies are also investing heavily in upgrading their defense capabilities, thereby bolstering demand. Furthermore, innovations in manufacturing processes and material science, such as the development of lead-free and environmentally compliant ammunition, are opening new avenues for growth and attracting new consumer segments, particularly within the Sporting Ammunition Market. The continuous evolution of firearm technologies also necessitates corresponding advancements in ammunition, ensuring compatibility and enhancing performance. While stringent regulatory frameworks and raw material price volatility present notable challenges, strategic investments in R&D and diversified supply chains are enabling market participants to mitigate these risks. The outlook for the Ammunition Market remains highly positive, driven by persistent security concerns, evolving defense doctrines, and a strong global interest in shooting sports and personal protection, making it a pivotal segment within the broader Chemicals & Materials category.

Ammunition Company Market Share

The global Ammunition Market's expansion is further supported by the increasing global demand for Small Arms Market products, as these firearms require a constant supply of ammunition for training, defense, and recreational activities. Manufacturers are focusing on optimizing production and integrating advanced materials to meet the diverse needs of end-users ranging from armed forces to civilian enthusiasts. The robust growth observed across different segments, including the Rimfire Ammunition Market, underscores the comprehensive nature of demand, ensuring sustained opportunities for stakeholders in the coming decade.

The Dominant 'Armed Forces' Segment in Ammunition Market

The 'Armed Forces' end-user segment stands as the unequivocal dominant force within the global Ammunition Market, commanding the largest revenue share and exerting significant influence over market dynamics. This supremacy is fundamentally rooted in the indispensable role of ammunition in national defense, military operations, and extensive training regimens conducted by defense establishments across the globe. Governments consistently allocate substantial portions of their budgets to defense spending, driven by geopolitical tensions, border security concerns, counter-terrorism efforts, and the imperative to modernize military arsenals. This sustained and often escalating expenditure directly translates into massive procurement contracts for a wide array of ammunition types, from small caliber rounds for personal firearms to large caliber munitions for artillery and armored vehicles.

Within this segment, the demand for Centerfire Ammunition Market products is particularly prominent, serving as the backbone for most military rifles, machine guns, and pistols. The operational requirements of armed forces necessitate a consistent supply of high-performance, reliable ammunition capable of functioning across diverse environmental conditions. This includes specialized ammunition for various combat scenarios, such as armor-piercing, tracer, and incendiary rounds. Furthermore, the extensive training protocols for military personnel, which often involve live-fire exercises, contribute substantially to the consumption of ammunition. These training requirements alone represent a significant and non-negotiable demand driver, ensuring a steady baseline for the Ammunition Market.

Key players in the Ammunition Market, such as Northrop Grumman Corporation, General Dynamics Corporation, and BAE Systems PLC, are heavily integrated into the defense supply chain, developing and manufacturing advanced ammunition solutions tailored specifically for military applications. Their deep expertise in defense technologies and established relationships with national governments solidify their dominant positions. The segment's share is not merely growing but also consolidating, as fewer, larger manufacturers with sophisticated R&D capabilities and robust production capacities tend to secure major long-term contracts. This consolidation is further spurred by the stringent quality control standards, certification processes, and security clearances required for defense suppliers, creating high barriers to entry for smaller players. Innovations driven by military requirements often trickle down to other segments, influencing the broader Ammunition Market landscape. For instance, enhanced ballistic performance or improved material durability developed for military use often finds applications in the Sporting Ammunition Market and law enforcement sectors, showcasing the profound ripple effect of the 'Armed Forces' segment's dominance.

Key Market Drivers and Constraints in Ammunition Market

The Ammunition Market's trajectory is shaped by a confluence of potent drivers and inherent constraints, each influencing demand and supply dynamics. A primary driver is the pervasive geopolitical instability and escalating defense expenditures globally. Recent conflicts and heightened regional tensions, such as those observed in Eastern Europe and parts of the Middle East, have prompted nations to significantly increase their defense budgets. For instance, NATO member states are increasingly committing to spending at least 2% of their GDP on defense, directly stimulating demand for Military Ammunition Market products. This surge in spending translates into large-scale procurement contracts for various calibers and specialized munitions, thereby driving the Ammunition Market forward.

Another significant driver is the growing trend of civilian firearm ownership for self-defense, hunting, and sport shooting. In regions like North America, the demand for firearms and related ammunition, including the Centerfire Ammunition Market and Rimfire Ammunition Market, remains robust. This is often influenced by socio-political factors and personal safety concerns, leading to sustained purchases by civilian users. The expansion of shooting sports and recreational hunting activities also contributes substantially to the Sporting Ammunition Market, creating a consistent revenue stream for manufacturers.

However, the Ammunition Market faces notable constraints, chief among them being stringent governmental regulations and gun control laws. Countries across Europe and North America often implement strict legislation regarding ammunition sales, types, and possession, which can limit market access and consumer purchasing power. For instance, restrictions on certain projectile types or magazine capacities can directly impact product development and sales volumes. Furthermore, volatility in raw material prices poses a continuous challenge. Essential materials like copper, lead, brass, and the Specialty Chemicals Market components used in Primers Market and Propellants Market are subject to global commodity price fluctuations. Spikes in these prices can compress profit margins for manufacturers and lead to higher end-product costs, potentially dampening demand.

Environmental concerns surrounding lead toxicity also act as a constraint, driving the development and adoption of lead-free ammunition alternatives. While this presents an opportunity for innovation, the transition requires significant R&D investment and can face consumer resistance due to potential performance differences or higher costs compared to traditional lead-based ammunition. These intertwined drivers and constraints necessitate strategic agility from market players to capitalize on opportunities while mitigating risks.

Competitive Ecosystem of Ammunition Market

The Ammunition Market is characterized by a mix of established defense contractors, specialized ammunition manufacturers, and diverse private companies, all vying for market share through product innovation, strategic partnerships, and global distribution networks.

- Ammo Inc.: This company focuses on a broad spectrum of ammunition products for military, law enforcement, and civilian markets, with a strategic emphasis on expanding its manufacturing capabilities and intellectual property portfolio, particularly in the U.S. consumer sector.

- Arsenal JSCo.: A key player primarily based in Bulgaria, Arsenal JSCo. specializes in military ammunition and weaponry, offering a wide range of small and medium-caliber ammunition to global defense clients and supporting diverse armed forces requirements.

- BAE Systems PLC: As a multinational defense, security, and aerospace company, BAE Systems PLC produces various forms of ammunition, often integrated into their larger defense systems, focusing on advanced munitions for naval, land, and air platforms.

- CBC Global Ammunition: A major international force, CBC Global Ammunition, encompassing brands like Magtech, Sellier & Bellot, and MEN, provides a comprehensive range of small and medium-caliber ammunition for military, law enforcement, and civilian applications worldwide.

- Denel SOC Ltd.: A South African state-owned aerospace and defense technology conglomerate, Denel SOC Ltd. is involved in the design, development, and manufacture of a broad array of ammunition and missile systems for defense forces.

- Northrop Grumman Corporation: This global aerospace and defense technology company contributes to the Ammunition Market through its advanced weapons systems and munitions, focusing on precision and effectiveness for military operations across multiple domains.

- General Dynamics Corporation: A diversified aerospace and defense company, General Dynamics Corporation manufactures various types of ammunition, including tank rounds, artillery shells, and small caliber ammunition, supporting U.S. and allied militaries.

- Hanwha Corporation: As a South Korean conglomerate, Hanwha Corporation has a significant defense division that produces a wide range of ammunition, from small arms munitions to large caliber artillery shells, playing a crucial role in regional defense.

- Hornady Manufacturing, Inc.: Renowned for its focus on the civilian and law enforcement markets, Hornady Manufacturing, Inc. specializes in high-quality rifle and pistol ammunition, reloading components, and ballistics research, catering to precision shooters and hunters.

- Leonardo S.p.A.: An Italian multinational, Leonardo S.p.A. provides comprehensive defense solutions, including advanced ammunition and weapon systems, with a strong presence in European and international defense markets.

- Nammo AS: A leading Nordic defense company, Nammo AS specializes in ammunition, rocket motors, and other energetic materials, providing innovative and high-performance solutions for defense and civilian sectors globally.

- Poongsan Corporation: A South Korean company, Poongsan Corporation is a significant producer of both copper products and defense items, including a wide variety of ammunition, serving both domestic and international markets.

- MESKO S.A.: A Polish defense company, MESKO S.A. is a major producer of small, medium, and large caliber ammunition, as well as missile systems, predominantly serving the Polish Armed Forces and international export clients.

Recent Developments & Milestones in Ammunition Market

Recent years have seen dynamic shifts and strategic advancements within the Ammunition Market, reflecting ongoing geopolitical changes, technological innovation, and evolving consumer demands.

- Q1 2024: A leading global defense contractor secured a multi-year contract worth several hundred million dollars for the supply of advanced 5.56mm and 7.62mm Military Ammunition Market to a major North American defense force, emphasizing continued modernization of infantry capabilities.

- Q4 2023: Several manufacturers introduced new lines of lead-free Centerfire Ammunition Market and Rimfire Ammunition Market, driven by environmental regulations and a growing demand from the Sporting Ammunition Market for eco-friendly alternatives. These products typically feature non-toxic primers and projectiles.

- Q3 2023: An acquisition occurred in the Propellants Market, where a prominent ammunition producer acquired a specialized manufacturer of energetic materials to enhance vertical integration and secure supply chains for advanced propellants.

- Q2 2023: A European consortium announced a significant partnership focused on developing 'smart' ammunition technologies, integrating sensors and guidance systems into artillery shells to improve precision and reduce collateral damage in conflict zones.

- Q1 2023: Regulatory approvals were granted in several jurisdictions for new polymer-cased ammunition, aimed at reducing the weight of carried ammunition for soldiers and law enforcement personnel, signaling a shift towards lighter, more efficient designs.

- Q4 2022: A major investment was made into automated ammunition manufacturing facilities in Southeast Asia, aimed at increasing production capacity and efficiency to meet rising regional demand for both civilian and defense applications.

- Q3 2022: Collaboration agreements were forged between ammunition manufacturers and university research departments to explore novel materials and manufacturing processes for Primers Market and other critical components, focusing on enhanced reliability and reduced environmental impact.

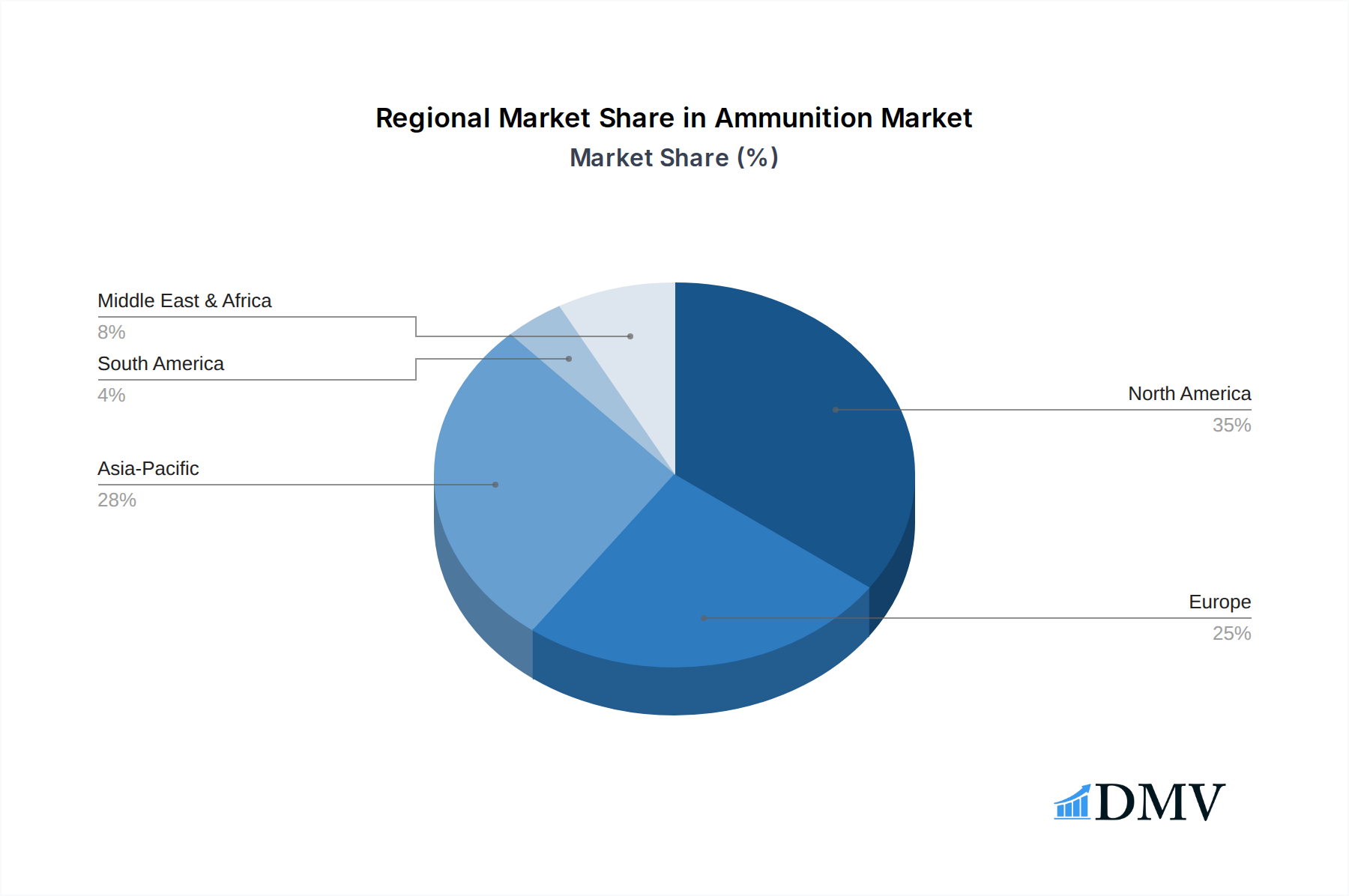

Regional Market Breakdown for Ammunition Market

The global Ammunition Market exhibits significant regional variations, influenced by defense spending, regulatory environments, geopolitical stability, and civilian firearm ownership trends. Analyzing at least four key regions provides insight into these diverse dynamics.

North America remains a cornerstone of the Ammunition Market, characterized by its mature defense industry and a substantial civilian market. The United States, in particular, drives significant demand across both the Military Ammunition Market and Sporting Ammunition Market. Civilian ownership for hunting, sport shooting, and self-defense ensures consistent demand for the Centerfire Ammunition Market and Rimfire Ammunition Market. Innovations in lead-free ammunition and advanced manufacturing techniques also find early adoption here. While specific regional CAGR data is not provided, the region typically maintains a stable, high-value share, supported by robust domestic production and export capabilities.

Asia Pacific is projected to be the fastest-growing region in the Ammunition Market. This growth is propelled by escalating defense budgets, military modernization programs, and increasing geopolitical tensions, particularly in countries like China, India, and South Korea. These nations are heavily investing in upgrading their armed forces, leading to a surge in demand for all calibers of ammunition. Furthermore, expanding law enforcement agencies and a growing, albeit regulated, civilian market in some countries contribute to this rapid expansion. The region is seeing significant investments in domestic ammunition manufacturing to achieve self-sufficiency.

Europe represents a complex and diverse Ammunition Market. Western European countries often have stringent gun control laws, impacting the civilian sector, but defense spending, especially in Eastern Europe, has seen a resurgence due to regional security concerns. Countries like Russia, Germany, France, and the UK are major producers and consumers, focusing on advanced munitions, environmentally compliant options, and maintaining strategic reserves. The demand for Specialty Chemicals Market components for ammunition is also strong in Europe due to significant R&D in materials.

Middle East & Africa (MEA) experiences significant demand for ammunition, primarily driven by ongoing conflicts, internal security challenges, and counter-terrorism efforts. Many countries in this region rely heavily on imports to meet their defense needs, making it a critical market for global suppliers. The demand is often for standard military calibers, with less emphasis on advanced or recreational ammunition. While growth can be volatile due to geopolitical factors, the persistent need for security ensures a foundational level of demand.

Overall, while North America and Europe represent mature, high-value markets with established players in the Small Arms Market and associated ammunition production, Asia Pacific is the key growth engine, poised to significantly reshape the global Ammunition Market landscape over the next decade.

Ammunition Regional Market Share

Investment & Funding Activity in Ammunition Market

Investment and funding activity within the Ammunition Market over the past 2-3 years has largely been characterized by strategic mergers and acquisitions, capital injections into manufacturing expansion, and targeted R&D funding aimed at technological advancement and sustainability. The sector has witnessed a trend where larger defense contractors and ammunition manufacturers are acquiring smaller, specialized technology firms, particularly those focused on advanced materials, digital manufacturing, or innovative propellant technologies. For instance, the acquisition of a company specializing in next-generation Propellants Market or Primers Market technologies by a major player can secure supply chains and integrate cutting-edge research into product lines.

Venture funding, while not as prevalent as in high-tech sectors, has shown interest in startups developing disruptive ammunition technologies. This includes companies innovating in areas such as caseless ammunition, smart ammunition with integrated sensors, or advanced non-lethal solutions. These investments are typically smaller but carry high potential for long-term impact on the Ammunition Market. The primary motivation for such funding is to capitalize on the increasing demand for high-performance and specialized ammunition across military, law enforcement, and civilian sectors.

Strategic partnerships have also been crucial. Collaborations between ammunition manufacturers and academic institutions or research organizations are common for exploring novel materials, improving ballistic performance, and addressing environmental concerns, such as the push for lead-free alternatives in the Sporting Ammunition Market. Governments, too, are playing a role through defense contracts that often include significant R&D clauses, effectively providing funding for innovation in the Military Ammunition Market. The sub-segments attracting the most capital are those promising enhanced precision, reduced weight, increased safety, and environmental compliance. Manufacturing automation and capacity expansion are also key areas of investment, as producers strive to meet fluctuating global demand and improve efficiency in the production of products like those for the Centerfire Ammunition Market and Rimfire Ammunition Market.

Technology Innovation Trajectory in Ammunition Market

The Ammunition Market is undergoing a significant transformation driven by several disruptive emerging technologies, fundamentally altering performance capabilities, manufacturing processes, and environmental impact. Two of the most prominent innovation trajectories are Smart Ammunition and Precision Guided Munitions (PGMs) and the rapid evolution towards Lead-Free and Environmentally Compliant Ammunition.

Smart Ammunition and PGMs: This technology represents a paradigm shift, moving beyond traditional ballistic principles to incorporate advanced electronics, sensors, and guidance systems directly into projectiles. Examples include guided artillery shells, mortar rounds, and increasingly, smaller caliber rifle ammunition with advanced target tracking capabilities. Adoption timelines for these technologies vary; large-caliber PGMs are already deployed by advanced militaries, while smaller, 'smart' rifle ammunition is still in advanced R&D and early prototyping phases, with potential broader adoption within the next 5-10 years. R&D investment levels are high, driven by military requirements for enhanced accuracy, reduced collateral damage, and improved soldier effectiveness. These innovations threaten incumbent business models focused purely on mass production of conventional ammunition, as they demand new expertise in microelectronics, software, and systems integration. Manufacturers in the Military Ammunition Market and those contributing to the Small Arms Market must either acquire these capabilities or partner with tech firms.

Lead-Free and Environmentally Compliant Ammunition: Driven by increasing environmental regulations concerning lead toxicity and growing ecological awareness, especially within the Sporting Ammunition Market, the shift towards lead-free materials is accelerating. This involves replacing lead projectiles with copper, brass, steel, or composite alternatives, and substituting lead styphnate Primers Market with lead-free equivalents. Adoption timelines are already active, with many jurisdictions either mandating or strongly encouraging the use of lead-free ammunition in specific hunting grounds or shooting ranges. R&D investment focuses on maintaining ballistic performance and ensuring cost-effectiveness comparable to traditional ammunition. This trend primarily reinforces incumbent business models that adapt quickly by investing in new material science and manufacturing processes. However, it threatens those unwilling or unable to transition, as they risk losing market share due to non-compliance or lack of competitive product offerings. The development of advanced Propellants Market that burn cleaner and more efficiently also falls under this umbrella, contributing to a greener and safer Ammunition Market overall.

Ammunition Segmentation

-

1. Product Type

- 1.1. Centerfire Ammunition

- 1.2. Rimfire Ammunition

- 1.3. Shotgun Ammunition

-

2. Caliber

- 2.1. Small Caliber

- 2.2. Medium Caliber

- 2.3. Large Caliber

-

3. Material

- 3.1. Brass

- 3.2. Steel

- 3.3. Lead

- 3.4. Aluminum

- 3.5. Composites

-

4. Platform

- 4.1. Land

- 4.2. Naval

- 4.3. Airborne

-

5. End User

- 5.1. Armed Forces

- 5.2. Homeland Security Agencies

- 5.3. Police & Law Enforcement Agencies

- 5.4. Civilian Users

Ammunition Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Ammunition Regional Market Share

Geographic Coverage of Ammunition

Ammunition REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Centerfire Ammunition

- 5.1.2. Rimfire Ammunition

- 5.1.3. Shotgun Ammunition

- 5.2. Market Analysis, Insights and Forecast - by Caliber

- 5.2.1. Small Caliber

- 5.2.2. Medium Caliber

- 5.2.3. Large Caliber

- 5.3. Market Analysis, Insights and Forecast - by Material

- 5.3.1. Brass

- 5.3.2. Steel

- 5.3.3. Lead

- 5.3.4. Aluminum

- 5.3.5. Composites

- 5.4. Market Analysis, Insights and Forecast - by Platform

- 5.4.1. Land

- 5.4.2. Naval

- 5.4.3. Airborne

- 5.5. Market Analysis, Insights and Forecast - by End User

- 5.5.1. Armed Forces

- 5.5.2. Homeland Security Agencies

- 5.5.3. Police & Law Enforcement Agencies

- 5.5.4. Civilian Users

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. North America

- 5.6.2. South America

- 5.6.3. Europe

- 5.6.4. Middle East & Africa

- 5.6.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Global Ammunition Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Centerfire Ammunition

- 6.1.2. Rimfire Ammunition

- 6.1.3. Shotgun Ammunition

- 6.2. Market Analysis, Insights and Forecast - by Caliber

- 6.2.1. Small Caliber

- 6.2.2. Medium Caliber

- 6.2.3. Large Caliber

- 6.3. Market Analysis, Insights and Forecast - by Material

- 6.3.1. Brass

- 6.3.2. Steel

- 6.3.3. Lead

- 6.3.4. Aluminum

- 6.3.5. Composites

- 6.4. Market Analysis, Insights and Forecast - by Platform

- 6.4.1. Land

- 6.4.2. Naval

- 6.4.3. Airborne

- 6.5. Market Analysis, Insights and Forecast - by End User

- 6.5.1. Armed Forces

- 6.5.2. Homeland Security Agencies

- 6.5.3. Police & Law Enforcement Agencies

- 6.5.4. Civilian Users

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. North America Ammunition Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Centerfire Ammunition

- 7.1.2. Rimfire Ammunition

- 7.1.3. Shotgun Ammunition

- 7.2. Market Analysis, Insights and Forecast - by Caliber

- 7.2.1. Small Caliber

- 7.2.2. Medium Caliber

- 7.2.3. Large Caliber

- 7.3. Market Analysis, Insights and Forecast - by Material

- 7.3.1. Brass

- 7.3.2. Steel

- 7.3.3. Lead

- 7.3.4. Aluminum

- 7.3.5. Composites

- 7.4. Market Analysis, Insights and Forecast - by Platform

- 7.4.1. Land

- 7.4.2. Naval

- 7.4.3. Airborne

- 7.5. Market Analysis, Insights and Forecast - by End User

- 7.5.1. Armed Forces

- 7.5.2. Homeland Security Agencies

- 7.5.3. Police & Law Enforcement Agencies

- 7.5.4. Civilian Users

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. South America Ammunition Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Centerfire Ammunition

- 8.1.2. Rimfire Ammunition

- 8.1.3. Shotgun Ammunition

- 8.2. Market Analysis, Insights and Forecast - by Caliber

- 8.2.1. Small Caliber

- 8.2.2. Medium Caliber

- 8.2.3. Large Caliber

- 8.3. Market Analysis, Insights and Forecast - by Material

- 8.3.1. Brass

- 8.3.2. Steel

- 8.3.3. Lead

- 8.3.4. Aluminum

- 8.3.5. Composites

- 8.4. Market Analysis, Insights and Forecast - by Platform

- 8.4.1. Land

- 8.4.2. Naval

- 8.4.3. Airborne

- 8.5. Market Analysis, Insights and Forecast - by End User

- 8.5.1. Armed Forces

- 8.5.2. Homeland Security Agencies

- 8.5.3. Police & Law Enforcement Agencies

- 8.5.4. Civilian Users

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Europe Ammunition Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Centerfire Ammunition

- 9.1.2. Rimfire Ammunition

- 9.1.3. Shotgun Ammunition

- 9.2. Market Analysis, Insights and Forecast - by Caliber

- 9.2.1. Small Caliber

- 9.2.2. Medium Caliber

- 9.2.3. Large Caliber

- 9.3. Market Analysis, Insights and Forecast - by Material

- 9.3.1. Brass

- 9.3.2. Steel

- 9.3.3. Lead

- 9.3.4. Aluminum

- 9.3.5. Composites

- 9.4. Market Analysis, Insights and Forecast - by Platform

- 9.4.1. Land

- 9.4.2. Naval

- 9.4.3. Airborne

- 9.5. Market Analysis, Insights and Forecast - by End User

- 9.5.1. Armed Forces

- 9.5.2. Homeland Security Agencies

- 9.5.3. Police & Law Enforcement Agencies

- 9.5.4. Civilian Users

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. Middle East & Africa Ammunition Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Centerfire Ammunition

- 10.1.2. Rimfire Ammunition

- 10.1.3. Shotgun Ammunition

- 10.2. Market Analysis, Insights and Forecast - by Caliber

- 10.2.1. Small Caliber

- 10.2.2. Medium Caliber

- 10.2.3. Large Caliber

- 10.3. Market Analysis, Insights and Forecast - by Material

- 10.3.1. Brass

- 10.3.2. Steel

- 10.3.3. Lead

- 10.3.4. Aluminum

- 10.3.5. Composites

- 10.4. Market Analysis, Insights and Forecast - by Platform

- 10.4.1. Land

- 10.4.2. Naval

- 10.4.3. Airborne

- 10.5. Market Analysis, Insights and Forecast - by End User

- 10.5.1. Armed Forces

- 10.5.2. Homeland Security Agencies

- 10.5.3. Police & Law Enforcement Agencies

- 10.5.4. Civilian Users

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. Asia Pacific Ammunition Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Centerfire Ammunition

- 11.1.2. Rimfire Ammunition

- 11.1.3. Shotgun Ammunition

- 11.2. Market Analysis, Insights and Forecast - by Caliber

- 11.2.1. Small Caliber

- 11.2.2. Medium Caliber

- 11.2.3. Large Caliber

- 11.3. Market Analysis, Insights and Forecast - by Material

- 11.3.1. Brass

- 11.3.2. Steel

- 11.3.3. Lead

- 11.3.4. Aluminum

- 11.3.5. Composites

- 11.4. Market Analysis, Insights and Forecast - by Platform

- 11.4.1. Land

- 11.4.2. Naval

- 11.4.3. Airborne

- 11.5. Market Analysis, Insights and Forecast - by End User

- 11.5.1. Armed Forces

- 11.5.2. Homeland Security Agencies

- 11.5.3. Police & Law Enforcement Agencies

- 11.5.4. Civilian Users

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Ammo Inc.

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Arsenal JSCo.

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 BAE Systems PLC

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 CBC Global Ammunition

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Denel SOC Ltd.

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Northrop Grumman Corporation

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 General Dynamics Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Hanwha Corporation

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Hornady Manufacturing Inc.

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Leonardo S.p.A.

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Nammo AS

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Poongsan Corporation

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 MESKO S.A.

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Others

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 Ammo Inc.

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Ammunition Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Ammunition Revenue (million), by Product Type 2025 & 2033

- Figure 3: North America Ammunition Revenue Share (%), by Product Type 2025 & 2033

- Figure 4: North America Ammunition Revenue (million), by Caliber 2025 & 2033

- Figure 5: North America Ammunition Revenue Share (%), by Caliber 2025 & 2033

- Figure 6: North America Ammunition Revenue (million), by Material 2025 & 2033

- Figure 7: North America Ammunition Revenue Share (%), by Material 2025 & 2033

- Figure 8: North America Ammunition Revenue (million), by Platform 2025 & 2033

- Figure 9: North America Ammunition Revenue Share (%), by Platform 2025 & 2033

- Figure 10: North America Ammunition Revenue (million), by End User 2025 & 2033

- Figure 11: North America Ammunition Revenue Share (%), by End User 2025 & 2033

- Figure 12: North America Ammunition Revenue (million), by Country 2025 & 2033

- Figure 13: North America Ammunition Revenue Share (%), by Country 2025 & 2033

- Figure 14: South America Ammunition Revenue (million), by Product Type 2025 & 2033

- Figure 15: South America Ammunition Revenue Share (%), by Product Type 2025 & 2033

- Figure 16: South America Ammunition Revenue (million), by Caliber 2025 & 2033

- Figure 17: South America Ammunition Revenue Share (%), by Caliber 2025 & 2033

- Figure 18: South America Ammunition Revenue (million), by Material 2025 & 2033

- Figure 19: South America Ammunition Revenue Share (%), by Material 2025 & 2033

- Figure 20: South America Ammunition Revenue (million), by Platform 2025 & 2033

- Figure 21: South America Ammunition Revenue Share (%), by Platform 2025 & 2033

- Figure 22: South America Ammunition Revenue (million), by End User 2025 & 2033

- Figure 23: South America Ammunition Revenue Share (%), by End User 2025 & 2033

- Figure 24: South America Ammunition Revenue (million), by Country 2025 & 2033

- Figure 25: South America Ammunition Revenue Share (%), by Country 2025 & 2033

- Figure 26: Europe Ammunition Revenue (million), by Product Type 2025 & 2033

- Figure 27: Europe Ammunition Revenue Share (%), by Product Type 2025 & 2033

- Figure 28: Europe Ammunition Revenue (million), by Caliber 2025 & 2033

- Figure 29: Europe Ammunition Revenue Share (%), by Caliber 2025 & 2033

- Figure 30: Europe Ammunition Revenue (million), by Material 2025 & 2033

- Figure 31: Europe Ammunition Revenue Share (%), by Material 2025 & 2033

- Figure 32: Europe Ammunition Revenue (million), by Platform 2025 & 2033

- Figure 33: Europe Ammunition Revenue Share (%), by Platform 2025 & 2033

- Figure 34: Europe Ammunition Revenue (million), by End User 2025 & 2033

- Figure 35: Europe Ammunition Revenue Share (%), by End User 2025 & 2033

- Figure 36: Europe Ammunition Revenue (million), by Country 2025 & 2033

- Figure 37: Europe Ammunition Revenue Share (%), by Country 2025 & 2033

- Figure 38: Middle East & Africa Ammunition Revenue (million), by Product Type 2025 & 2033

- Figure 39: Middle East & Africa Ammunition Revenue Share (%), by Product Type 2025 & 2033

- Figure 40: Middle East & Africa Ammunition Revenue (million), by Caliber 2025 & 2033

- Figure 41: Middle East & Africa Ammunition Revenue Share (%), by Caliber 2025 & 2033

- Figure 42: Middle East & Africa Ammunition Revenue (million), by Material 2025 & 2033

- Figure 43: Middle East & Africa Ammunition Revenue Share (%), by Material 2025 & 2033

- Figure 44: Middle East & Africa Ammunition Revenue (million), by Platform 2025 & 2033

- Figure 45: Middle East & Africa Ammunition Revenue Share (%), by Platform 2025 & 2033

- Figure 46: Middle East & Africa Ammunition Revenue (million), by End User 2025 & 2033

- Figure 47: Middle East & Africa Ammunition Revenue Share (%), by End User 2025 & 2033

- Figure 48: Middle East & Africa Ammunition Revenue (million), by Country 2025 & 2033

- Figure 49: Middle East & Africa Ammunition Revenue Share (%), by Country 2025 & 2033

- Figure 50: Asia Pacific Ammunition Revenue (million), by Product Type 2025 & 2033

- Figure 51: Asia Pacific Ammunition Revenue Share (%), by Product Type 2025 & 2033

- Figure 52: Asia Pacific Ammunition Revenue (million), by Caliber 2025 & 2033

- Figure 53: Asia Pacific Ammunition Revenue Share (%), by Caliber 2025 & 2033

- Figure 54: Asia Pacific Ammunition Revenue (million), by Material 2025 & 2033

- Figure 55: Asia Pacific Ammunition Revenue Share (%), by Material 2025 & 2033

- Figure 56: Asia Pacific Ammunition Revenue (million), by Platform 2025 & 2033

- Figure 57: Asia Pacific Ammunition Revenue Share (%), by Platform 2025 & 2033

- Figure 58: Asia Pacific Ammunition Revenue (million), by End User 2025 & 2033

- Figure 59: Asia Pacific Ammunition Revenue Share (%), by End User 2025 & 2033

- Figure 60: Asia Pacific Ammunition Revenue (million), by Country 2025 & 2033

- Figure 61: Asia Pacific Ammunition Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Ammunition Revenue million Forecast, by Product Type 2020 & 2033

- Table 2: Global Ammunition Revenue million Forecast, by Caliber 2020 & 2033

- Table 3: Global Ammunition Revenue million Forecast, by Material 2020 & 2033

- Table 4: Global Ammunition Revenue million Forecast, by Platform 2020 & 2033

- Table 5: Global Ammunition Revenue million Forecast, by End User 2020 & 2033

- Table 6: Global Ammunition Revenue million Forecast, by Region 2020 & 2033

- Table 7: Global Ammunition Revenue million Forecast, by Product Type 2020 & 2033

- Table 8: Global Ammunition Revenue million Forecast, by Caliber 2020 & 2033

- Table 9: Global Ammunition Revenue million Forecast, by Material 2020 & 2033

- Table 10: Global Ammunition Revenue million Forecast, by Platform 2020 & 2033

- Table 11: Global Ammunition Revenue million Forecast, by End User 2020 & 2033

- Table 12: Global Ammunition Revenue million Forecast, by Country 2020 & 2033

- Table 13: United States Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Canada Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Mexico Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Ammunition Revenue million Forecast, by Product Type 2020 & 2033

- Table 17: Global Ammunition Revenue million Forecast, by Caliber 2020 & 2033

- Table 18: Global Ammunition Revenue million Forecast, by Material 2020 & 2033

- Table 19: Global Ammunition Revenue million Forecast, by Platform 2020 & 2033

- Table 20: Global Ammunition Revenue million Forecast, by End User 2020 & 2033

- Table 21: Global Ammunition Revenue million Forecast, by Country 2020 & 2033

- Table 22: Brazil Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Argentina Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Rest of South America Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Global Ammunition Revenue million Forecast, by Product Type 2020 & 2033

- Table 26: Global Ammunition Revenue million Forecast, by Caliber 2020 & 2033

- Table 27: Global Ammunition Revenue million Forecast, by Material 2020 & 2033

- Table 28: Global Ammunition Revenue million Forecast, by Platform 2020 & 2033

- Table 29: Global Ammunition Revenue million Forecast, by End User 2020 & 2033

- Table 30: Global Ammunition Revenue million Forecast, by Country 2020 & 2033

- Table 31: United Kingdom Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Germany Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: France Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: Italy Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: Spain Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Russia Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Benelux Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 38: Nordics Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 39: Rest of Europe Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 40: Global Ammunition Revenue million Forecast, by Product Type 2020 & 2033

- Table 41: Global Ammunition Revenue million Forecast, by Caliber 2020 & 2033

- Table 42: Global Ammunition Revenue million Forecast, by Material 2020 & 2033

- Table 43: Global Ammunition Revenue million Forecast, by Platform 2020 & 2033

- Table 44: Global Ammunition Revenue million Forecast, by End User 2020 & 2033

- Table 45: Global Ammunition Revenue million Forecast, by Country 2020 & 2033

- Table 46: Turkey Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 47: Israel Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 48: GCC Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 49: North Africa Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 50: South Africa Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 51: Rest of Middle East & Africa Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 52: Global Ammunition Revenue million Forecast, by Product Type 2020 & 2033

- Table 53: Global Ammunition Revenue million Forecast, by Caliber 2020 & 2033

- Table 54: Global Ammunition Revenue million Forecast, by Material 2020 & 2033

- Table 55: Global Ammunition Revenue million Forecast, by Platform 2020 & 2033

- Table 56: Global Ammunition Revenue million Forecast, by End User 2020 & 2033

- Table 57: Global Ammunition Revenue million Forecast, by Country 2020 & 2033

- Table 58: China Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 59: India Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 60: Japan Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 61: South Korea Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 62: ASEAN Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 63: Oceania Ammunition Revenue (million) Forecast, by Application 2020 & 2033

- Table 64: Rest of Asia Pacific Ammunition Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Ammunition?

The projected CAGR is approximately 11.1%.

2. Which companies are prominent players in the Ammunition?

Key companies in the market include Ammo Inc., Arsenal JSCo., BAE Systems PLC, CBC Global Ammunition, Denel SOC Ltd., Northrop Grumman Corporation, General Dynamics Corporation, Hanwha Corporation, Hornady Manufacturing, Inc., Leonardo S.p.A., Nammo AS, Poongsan Corporation, MESKO S.A., Others.

3. What are the main segments of the Ammunition?

The market segments include Product Type, Caliber, Material, Platform, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 15350 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5900.00, USD 8850.00, and USD 11800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Ammunition," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Ammunition report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Ammunition?

To stay informed about further developments, trends, and reports in the Ammunition, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence