Key Insights

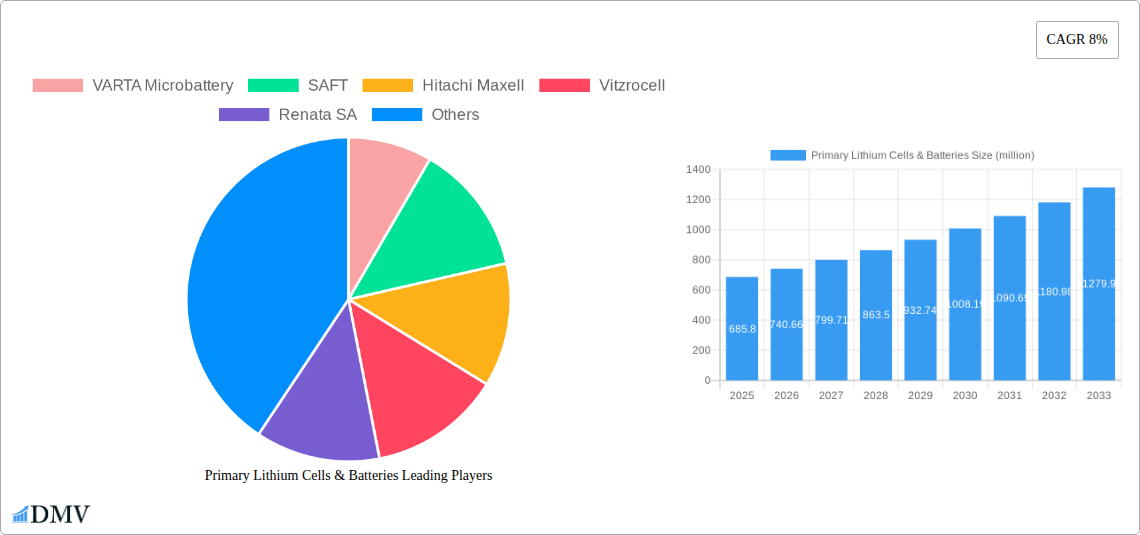

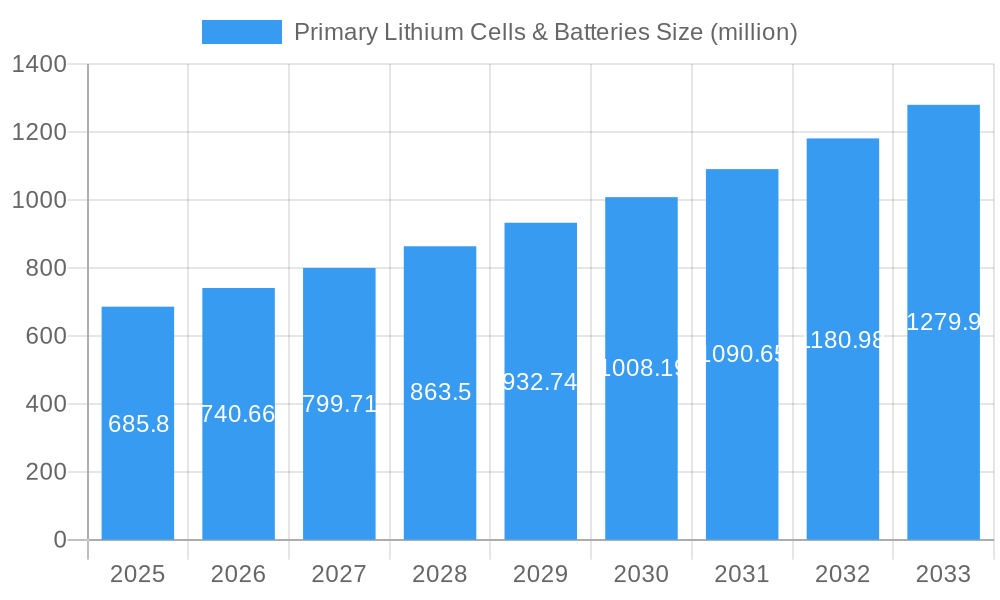

The global market for Primary Lithium Cells & Batteries is poised for significant expansion, projected to reach an estimated $685.8 million in 2025 and exhibit a robust Compound Annual Growth Rate (CAGR) of 8% through 2033. This dynamic growth is propelled by an increasing demand for high-performance, long-lasting power sources across a multitude of applications. Key drivers include the pervasive adoption of Tire Pressure Monitoring Systems (TPMS) in automotive safety, the growing sophistication of Remote Keyless Entry (RKE) systems, and the expanding integration of these batteries in metering devices, intelligent security systems, and a wide array of consumer electronics. The inherent advantages of primary lithium batteries, such as their high energy density, extended shelf life, wide operating temperature range, and superior reliability, make them the preferred choice for applications where frequent replacement or recharging is impractical or undesirable. This technological superiority ensures their continued relevance and market penetration.

Primary Lithium Cells & Batteries Market Size (In Million)

Furthermore, the market is characterized by ongoing innovation in battery chemistries, with Li-MnO2 and Li-SOCl2 chemistries currently dominating due to their balanced performance and cost-effectiveness. However, emerging applications are likely to spur advancements in other types like Li-SO2, catering to niche requirements for extreme environments or exceptionally high power bursts. Geographically, the Asia Pacific region, led by China and Japan, is expected to be a dominant force, driven by its substantial manufacturing capabilities and burgeoning consumer electronics sector. North America and Europe, with their advanced automotive industries and increasing focus on smart security solutions, will also represent substantial market shares. Restraints such as stringent environmental regulations regarding battery disposal and the emergence of rechargeable alternatives in some segments could pose challenges, but the inherent advantages of primary lithium cells in specific, high-value applications will ensure sustained market vitality. Leading companies like VARTA Microbattery, SAFT, and Hitachi Maxell are actively investing in research and development to enhance performance and sustainability, further shaping the market landscape.

Primary Lithium Cells & Batteries Company Market Share

Primary Lithium Cells & Batteries Market Report: Comprehensive Analysis & Future Outlook (2019-2033)

This in-depth report provides a strategic analysis of the global Primary Lithium Cells & Batteries market, a critical component driving innovation across numerous high-growth sectors. Delving into market dynamics from 2019 to 2033, with a base year of 2025 and a robust forecast period of 2025-2033, this research offers unparalleled insights for stakeholders. Explore market composition, industry evolution, regional dominance, product innovations, growth drivers, obstacles, and future opportunities, supported by a comprehensive list of major players and key industry developments. Unlock strategic intelligence for market penetration and investment.

Primary Lithium Cells & Batteries Market Composition & Trends

The primary lithium battery market exhibits moderate concentration, with key players like VARTA Microbattery, SAFT, Hitachi Maxell, Vitzrocell, Renata SA, Gold Peak, EVE Energy, Huiderui Lithium Battery, FDK CORP., and Ultralife holding significant market share. Innovation is primarily driven by advancements in energy density, leakage prevention, and extended shelf life, crucial for TPMS (Tire Pressure Monitoring Systems), RKE (Remote Keyless Entry), smart metering, and intelligent security applications. The regulatory landscape is evolving, with a focus on safety standards and environmental compliance, impacting the production and disposal of these Li-MnO2 and Li-SOCl2 batteries. Substitute products, such as advanced alkaline and silver-oxide batteries, pose a competitive threat in certain lower-end applications, but the superior energy density of lithium chemistries maintains their dominance in power-critical and long-life applications. End-user profiles range from automotive manufacturers and utility companies to consumer electronics brands and industrial equipment suppliers. Mergers and acquisitions (M&A) activity is moderate, with recent transactions valued in the tens of millions, consolidating market presence and expanding technological portfolios. For instance, strategic acquisitions focused on enhancing Li-SO2 battery production capabilities for specialized military and medical devices have been observed, contributing to a market share distribution where advanced chemistries like Li-SOCl2 capture approximately 35% of the market, followed by Li-MnO2 at 30%, with Others comprising the remaining 35%. M&A deal values are projected to reach an aggregate of $50 million during the forecast period, signifying consolidation and strategic expansion.

Primary Lithium Cells & Batteries Industry Evolution

The primary lithium cells and batteries industry has witnessed remarkable growth and evolution over the historical period (2019-2024) and is poised for continued expansion through 2033. The market trajectory is characterized by a Compound Annual Growth Rate (CAGR) of approximately 7.5% from 2019 to 2024, driven by increasing demand for compact, long-lasting, and reliable power sources. Technological advancements have been pivotal in this growth. Early innovations focused on enhancing energy density and operational temperature ranges for Li-MnO2 batteries, making them ideal for widespread consumer electronics and certain industrial sensors. Subsequently, the development of Li-SOCl2 (Lithium Thionyl Chloride) batteries revolutionized long-term power solutions, particularly for applications requiring minimal self-discharge, such as utility metering and advanced security systems. The introduction of Li-SO2 (Lithium Sulfur Dioxide) batteries provided high-power density for demanding applications like military equipment and specialized medical devices. Shifting consumer demands have also played a significant role. The proliferation of the Internet of Things (IoT) has spurred demand for wirelessly connected devices that require compact and efficient power, directly benefiting the primary lithium battery market. The automotive sector's increasing reliance on sophisticated electronics for TPMS and RKE systems has further fueled growth. By 2025, the market is expected to reach a valuation of $7,500 million, with projections indicating a further surge to $13,000 million by 2033. Adoption metrics for primary lithium batteries in the smart grid sector have seen a year-on-year increase of 8% from 2022 to 2024, while consumer electronics adoption has grown by 6% annually. The intelligent security segment alone is predicted to contribute an additional $1,500 million to the market by 2028, driven by the increasing need for reliable, long-term power in surveillance and alarm systems. The Others application segment, encompassing niche industrial and medical devices, is projected to grow at a CAGR of 9% due to specialized battery requirements. The Li-MnO2 type is expected to maintain a significant market share, driven by its cost-effectiveness and widespread availability, projected at around $3,000 million in revenue by 2025.

Leading Regions, Countries, or Segments in Primary Lithium Cells & Batteries

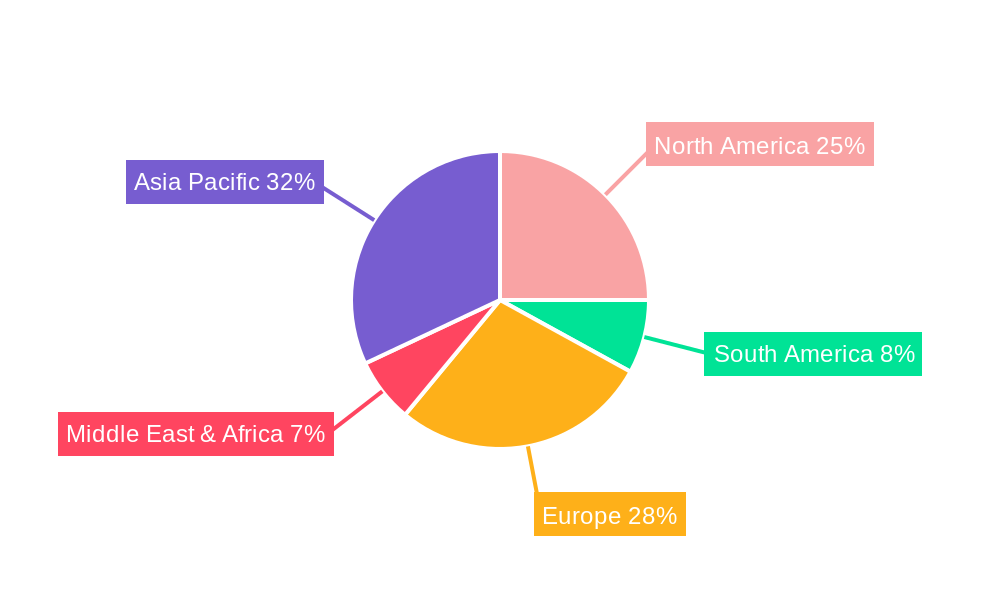

The Asia Pacific region is emerging as a dominant force in the primary lithium cells and batteries market. This leadership is underpinned by a confluence of factors, including robust manufacturing capabilities, significant government investment in battery research and development, and a rapidly expanding consumer electronics and automotive sectors. Countries like China, South Korea, and Japan are at the forefront of production and innovation.

Key Drivers for Asia Pacific Dominance:

- Manufacturing Prowess: Extensive manufacturing infrastructure and a skilled workforce enable high-volume production of primary lithium batteries at competitive costs.

- Technological Hubs: The region is home to leading technology companies that drive demand for advanced battery solutions for their consumer electronics, automotive, and emerging IoT devices.

- Government Support: Favorable government policies, including subsidies and R&D grants, accelerate the development and adoption of advanced battery technologies.

- Growing Automotive Sector: The booming automotive industry, particularly in electric and hybrid vehicles, as well as the increasing adoption of TPMS and RKE systems, significantly boosts demand.

- Smart Grid Initiatives: Aggressive smart grid implementation across several Asian nations necessitates reliable and long-lasting power sources for metering applications, further driving the demand for primary lithium batteries.

Within this dominant region, the Consumer Electronics segment, particularly for applications like portable devices, smart home devices, and wearables, is a primary driver of demand for Li-MnO2 batteries. The market share of Li-MnO2 in consumer electronics is estimated at 40% of the total segment revenue, valued at approximately $1,800 million in 2025. The intelligent security segment, powered by Li-SOCl2 and Li-MnO2 chemistries, is also experiencing substantial growth, driven by increasing concerns about safety and security in both residential and commercial spaces. This segment is projected to grow at a CAGR of 8.2% over the forecast period, reaching an estimated $2,200 million by 2033. The TPMS application, relying heavily on the longevity and reliability of Li-MnO2 batteries, is a substantial contributor, with an estimated market value of $1,000 million by 2025. Furthermore, advancements in Li-SO2 technology are finding traction in specialized industrial and defense applications, contributing to a niche but high-value segment. The "Others" application category, encompassing medical devices and industrial sensors, is also witnessing steady growth, with a projected market value of $900 million in 2025, supported by the demand for dependable, maintenance-free power sources.

Primary Lithium Cells & Batteries Product Innovations

Product innovation in primary lithium cells and batteries centers on enhancing energy density, extending operational lifespan, and improving safety characteristics. Manufacturers are actively developing high-capacity Li-MnO2 cells for longer-lasting consumer electronics and ultra-low self-discharge Li-SOCl2 batteries for mission-critical applications such as advanced metering infrastructure and remote monitoring systems. Innovations also include improved sealing technologies to prevent leakage and wider operating temperature ranges for harsh environments. For instance, recent developments in Li-SO2 batteries have achieved energy densities exceeding 500 Wh/kg, a significant leap for specialized power needs. Performance metrics like a shelf life exceeding 10-15 years for Li-SOCl2 and operational durations of over 5 years in demanding TPMS applications are becoming standard.

Propelling Factors for Primary Lithium Cells & Batteries Growth

The growth of the primary lithium battery market is propelled by several interconnected factors. The relentless expansion of the Internet of Things (IoT) ecosystem, with billions of connected devices requiring compact, long-life power solutions, is a primary catalyst. The automotive industry's increasing integration of advanced electronic systems, including TPMS and RKE, further fuels demand. Moreover, a global push towards smart grid infrastructure necessitates reliable and maintenance-free power for smart meters. Technological advancements in battery chemistry, leading to higher energy densities and extended shelf lives, are also crucial. Regulatory support for smart city initiatives and mandates for electronic metering also contribute significantly to market expansion. For example, government incentives for smart meter deployment in North America are projected to add $500 million in demand by 2028.

Obstacles in the Primary Lithium Cells & Batteries Market

Despite robust growth, the primary lithium battery market faces several obstacles. Stringent environmental regulations concerning the disposal of lithium-based batteries pose a compliance challenge for manufacturers and end-users. Supply chain disruptions, particularly concerning the availability and cost of raw materials like lithium and cobalt, can impact production volumes and pricing. Intense competition from alternative battery technologies, though often with limitations in energy density or lifespan, can exert pressure on market share in certain segments. Furthermore, the higher initial cost of primary lithium batteries compared to some conventional battery types can be a barrier for cost-sensitive applications. The market is also susceptible to fluctuations in geopolitical stability, which can affect the supply of critical raw materials, with a potential impact of 10-15% on raw material costs during periods of instability.

Future Opportunities in Primary Lithium Cells & Batteries

Emerging opportunities in the primary lithium battery market lie in the burgeoning field of advanced medical devices requiring long-term, implantable power sources. The continued miniaturization and increasing functionality of consumer electronics, such as advanced wearables and smart home sensors, will drive demand for smaller and more efficient batteries. The expansion of smart grid technology into developing nations presents a significant new market. Furthermore, research into novel lithium-based chemistries promises even higher energy densities and improved safety, opening doors for new applications in niche industrial and aerospace sectors. The development of specialized battery solutions for remote environmental monitoring systems is also a growing opportunity, estimated to contribute $700 million by 2030.

Major Players in the Primary Lithium Cells & Batteries Ecosystem

- VARTA Microbattery

- SAFT

- Hitachi Maxell

- Vitzrocell

- Renata SA

- Gold Peak

- EVE Energy

- Huiderui Lithium Battery

- FDK CORP.

- Ultralife

Key Developments in Primary Lithium Cells & Batteries Industry

- January 2024: EVE Energy launched a new generation of high-energy-density Li-MnO2 batteries, offering a 15% increase in capacity for smart meters.

- October 2023: SAFT announced a strategic partnership with a leading medical device manufacturer to develop custom Li-SOCl2 batteries for advanced implantable devices.

- July 2023: VITZROCELL introduced enhanced sealing technology for its Li-SOCl2 batteries, significantly improving leakage resistance in extreme temperatures.

- April 2023: Ultralife showcased its latest Li-SO2 batteries with improved power output for defense applications.

- December 2022: Renata SA expanded its production capacity for Li-MnO2 batteries to meet growing demand from the consumer electronics sector.

- September 2022: Hitachi Maxell announced advancements in battery materials research aimed at extending the shelf life of primary lithium cells by an additional 5 years.

Strategic Primary Lithium Cells & Batteries Market Forecast

The primary lithium cells and batteries market is poised for sustained growth, driven by ongoing technological innovation and increasing adoption across diverse sectors. The expansion of IoT devices, coupled with the automotive industry's demand for reliable electronic components, will continue to be significant growth catalysts. The global push towards smart grid infrastructure and the increasing need for long-lasting, maintenance-free power solutions in smart metering and intelligent security applications represent substantial future opportunities. Strategic investments in R&D for higher energy density and improved safety, alongside the exploration of new applications in medical and industrial domains, will shape the market's trajectory, with a projected market value of $13,000 million by 2033.

Primary Lithium Cells & Batteries Segmentation

-

1. Application

- 1.1. TPMS

- 1.2. RKE

- 1.3. Metering

- 1.4. Intelligent Security

- 1.5. Consumer Electronics

- 1.6. Others

-

2. Types

- 2.1. Li-MnO2

- 2.2. Li-SOCl2

- 2.3. Li-SO2

- 2.4. Others

Primary Lithium Cells & Batteries Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Primary Lithium Cells & Batteries Regional Market Share

Geographic Coverage of Primary Lithium Cells & Batteries

Primary Lithium Cells & Batteries REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. TPMS

- 5.1.2. RKE

- 5.1.3. Metering

- 5.1.4. Intelligent Security

- 5.1.5. Consumer Electronics

- 5.1.6. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Li-MnO2

- 5.2.2. Li-SOCl2

- 5.2.3. Li-SO2

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Primary Lithium Cells & Batteries Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. TPMS

- 6.1.2. RKE

- 6.1.3. Metering

- 6.1.4. Intelligent Security

- 6.1.5. Consumer Electronics

- 6.1.6. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Li-MnO2

- 6.2.2. Li-SOCl2

- 6.2.3. Li-SO2

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Primary Lithium Cells & Batteries Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. TPMS

- 7.1.2. RKE

- 7.1.3. Metering

- 7.1.4. Intelligent Security

- 7.1.5. Consumer Electronics

- 7.1.6. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Li-MnO2

- 7.2.2. Li-SOCl2

- 7.2.3. Li-SO2

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Primary Lithium Cells & Batteries Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. TPMS

- 8.1.2. RKE

- 8.1.3. Metering

- 8.1.4. Intelligent Security

- 8.1.5. Consumer Electronics

- 8.1.6. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Li-MnO2

- 8.2.2. Li-SOCl2

- 8.2.3. Li-SO2

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Primary Lithium Cells & Batteries Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. TPMS

- 9.1.2. RKE

- 9.1.3. Metering

- 9.1.4. Intelligent Security

- 9.1.5. Consumer Electronics

- 9.1.6. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Li-MnO2

- 9.2.2. Li-SOCl2

- 9.2.3. Li-SO2

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Primary Lithium Cells & Batteries Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. TPMS

- 10.1.2. RKE

- 10.1.3. Metering

- 10.1.4. Intelligent Security

- 10.1.5. Consumer Electronics

- 10.1.6. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Li-MnO2

- 10.2.2. Li-SOCl2

- 10.2.3. Li-SO2

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Primary Lithium Cells & Batteries Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. TPMS

- 11.1.2. RKE

- 11.1.3. Metering

- 11.1.4. Intelligent Security

- 11.1.5. Consumer Electronics

- 11.1.6. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Li-MnO2

- 11.2.2. Li-SOCl2

- 11.2.3. Li-SO2

- 11.2.4. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 VARTA Microbattery

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 SAFT

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Hitachi Maxell

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Vitzrocell

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Renata SA

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Gold Peak

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 EVE Energy

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Huiderui Lithium Battery

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 FDK CORP.

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Ultralife

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 VARTA Microbattery

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Primary Lithium Cells & Batteries Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: Global Primary Lithium Cells & Batteries Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Primary Lithium Cells & Batteries Revenue (million), by Application 2025 & 2033

- Figure 4: North America Primary Lithium Cells & Batteries Volume (K), by Application 2025 & 2033

- Figure 5: North America Primary Lithium Cells & Batteries Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Primary Lithium Cells & Batteries Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Primary Lithium Cells & Batteries Revenue (million), by Types 2025 & 2033

- Figure 8: North America Primary Lithium Cells & Batteries Volume (K), by Types 2025 & 2033

- Figure 9: North America Primary Lithium Cells & Batteries Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Primary Lithium Cells & Batteries Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Primary Lithium Cells & Batteries Revenue (million), by Country 2025 & 2033

- Figure 12: North America Primary Lithium Cells & Batteries Volume (K), by Country 2025 & 2033

- Figure 13: North America Primary Lithium Cells & Batteries Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Primary Lithium Cells & Batteries Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Primary Lithium Cells & Batteries Revenue (million), by Application 2025 & 2033

- Figure 16: South America Primary Lithium Cells & Batteries Volume (K), by Application 2025 & 2033

- Figure 17: South America Primary Lithium Cells & Batteries Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Primary Lithium Cells & Batteries Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Primary Lithium Cells & Batteries Revenue (million), by Types 2025 & 2033

- Figure 20: South America Primary Lithium Cells & Batteries Volume (K), by Types 2025 & 2033

- Figure 21: South America Primary Lithium Cells & Batteries Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Primary Lithium Cells & Batteries Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Primary Lithium Cells & Batteries Revenue (million), by Country 2025 & 2033

- Figure 24: South America Primary Lithium Cells & Batteries Volume (K), by Country 2025 & 2033

- Figure 25: South America Primary Lithium Cells & Batteries Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Primary Lithium Cells & Batteries Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Primary Lithium Cells & Batteries Revenue (million), by Application 2025 & 2033

- Figure 28: Europe Primary Lithium Cells & Batteries Volume (K), by Application 2025 & 2033

- Figure 29: Europe Primary Lithium Cells & Batteries Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Primary Lithium Cells & Batteries Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Primary Lithium Cells & Batteries Revenue (million), by Types 2025 & 2033

- Figure 32: Europe Primary Lithium Cells & Batteries Volume (K), by Types 2025 & 2033

- Figure 33: Europe Primary Lithium Cells & Batteries Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Primary Lithium Cells & Batteries Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Primary Lithium Cells & Batteries Revenue (million), by Country 2025 & 2033

- Figure 36: Europe Primary Lithium Cells & Batteries Volume (K), by Country 2025 & 2033

- Figure 37: Europe Primary Lithium Cells & Batteries Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Primary Lithium Cells & Batteries Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Primary Lithium Cells & Batteries Revenue (million), by Application 2025 & 2033

- Figure 40: Middle East & Africa Primary Lithium Cells & Batteries Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Primary Lithium Cells & Batteries Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Primary Lithium Cells & Batteries Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Primary Lithium Cells & Batteries Revenue (million), by Types 2025 & 2033

- Figure 44: Middle East & Africa Primary Lithium Cells & Batteries Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Primary Lithium Cells & Batteries Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Primary Lithium Cells & Batteries Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Primary Lithium Cells & Batteries Revenue (million), by Country 2025 & 2033

- Figure 48: Middle East & Africa Primary Lithium Cells & Batteries Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Primary Lithium Cells & Batteries Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Primary Lithium Cells & Batteries Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Primary Lithium Cells & Batteries Revenue (million), by Application 2025 & 2033

- Figure 52: Asia Pacific Primary Lithium Cells & Batteries Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Primary Lithium Cells & Batteries Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Primary Lithium Cells & Batteries Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Primary Lithium Cells & Batteries Revenue (million), by Types 2025 & 2033

- Figure 56: Asia Pacific Primary Lithium Cells & Batteries Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Primary Lithium Cells & Batteries Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Primary Lithium Cells & Batteries Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Primary Lithium Cells & Batteries Revenue (million), by Country 2025 & 2033

- Figure 60: Asia Pacific Primary Lithium Cells & Batteries Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Primary Lithium Cells & Batteries Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Primary Lithium Cells & Batteries Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Primary Lithium Cells & Batteries Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Primary Lithium Cells & Batteries Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Primary Lithium Cells & Batteries Revenue million Forecast, by Types 2020 & 2033

- Table 4: Global Primary Lithium Cells & Batteries Volume K Forecast, by Types 2020 & 2033

- Table 5: Global Primary Lithium Cells & Batteries Revenue million Forecast, by Region 2020 & 2033

- Table 6: Global Primary Lithium Cells & Batteries Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Primary Lithium Cells & Batteries Revenue million Forecast, by Application 2020 & 2033

- Table 8: Global Primary Lithium Cells & Batteries Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Primary Lithium Cells & Batteries Revenue million Forecast, by Types 2020 & 2033

- Table 10: Global Primary Lithium Cells & Batteries Volume K Forecast, by Types 2020 & 2033

- Table 11: Global Primary Lithium Cells & Batteries Revenue million Forecast, by Country 2020 & 2033

- Table 12: Global Primary Lithium Cells & Batteries Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Primary Lithium Cells & Batteries Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: United States Primary Lithium Cells & Batteries Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Primary Lithium Cells & Batteries Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Canada Primary Lithium Cells & Batteries Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Primary Lithium Cells & Batteries Revenue (million) Forecast, by Application 2020 & 2033

- Table 18: Mexico Primary Lithium Cells & Batteries Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Primary Lithium Cells & Batteries Revenue million Forecast, by Application 2020 & 2033

- Table 20: Global Primary Lithium Cells & Batteries Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Primary Lithium Cells & Batteries Revenue million Forecast, by Types 2020 & 2033

- Table 22: Global Primary Lithium Cells & Batteries Volume K Forecast, by Types 2020 & 2033

- Table 23: Global Primary Lithium Cells & Batteries Revenue million Forecast, by Country 2020 & 2033

- Table 24: Global Primary Lithium Cells & Batteries Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Primary Lithium Cells & Batteries Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Brazil Primary Lithium Cells & Batteries Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Primary Lithium Cells & Batteries Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Argentina Primary Lithium Cells & Batteries Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Primary Lithium Cells & Batteries Revenue (million) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Primary Lithium Cells & Batteries Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Primary Lithium Cells & Batteries Revenue million Forecast, by Application 2020 & 2033

- Table 32: Global Primary Lithium Cells & Batteries Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Primary Lithium Cells & Batteries Revenue million Forecast, by Types 2020 & 2033

- Table 34: Global Primary Lithium Cells & Batteries Volume K Forecast, by Types 2020 & 2033

- Table 35: Global Primary Lithium Cells & Batteries Revenue million Forecast, by Country 2020 & 2033

- Table 36: Global Primary Lithium Cells & Batteries Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Primary Lithium Cells & Batteries Revenue (million) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Primary Lithium Cells & Batteries Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Primary Lithium Cells & Batteries Revenue (million) Forecast, by Application 2020 & 2033

- Table 40: Germany Primary Lithium Cells & Batteries Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Primary Lithium Cells & Batteries Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: France Primary Lithium Cells & Batteries Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Primary Lithium Cells & Batteries Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: Italy Primary Lithium Cells & Batteries Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Primary Lithium Cells & Batteries Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Spain Primary Lithium Cells & Batteries Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Primary Lithium Cells & Batteries Revenue (million) Forecast, by Application 2020 & 2033

- Table 48: Russia Primary Lithium Cells & Batteries Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Primary Lithium Cells & Batteries Revenue (million) Forecast, by Application 2020 & 2033

- Table 50: Benelux Primary Lithium Cells & Batteries Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Primary Lithium Cells & Batteries Revenue (million) Forecast, by Application 2020 & 2033

- Table 52: Nordics Primary Lithium Cells & Batteries Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Primary Lithium Cells & Batteries Revenue (million) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Primary Lithium Cells & Batteries Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Primary Lithium Cells & Batteries Revenue million Forecast, by Application 2020 & 2033

- Table 56: Global Primary Lithium Cells & Batteries Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Primary Lithium Cells & Batteries Revenue million Forecast, by Types 2020 & 2033

- Table 58: Global Primary Lithium Cells & Batteries Volume K Forecast, by Types 2020 & 2033

- Table 59: Global Primary Lithium Cells & Batteries Revenue million Forecast, by Country 2020 & 2033

- Table 60: Global Primary Lithium Cells & Batteries Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Primary Lithium Cells & Batteries Revenue (million) Forecast, by Application 2020 & 2033

- Table 62: Turkey Primary Lithium Cells & Batteries Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Primary Lithium Cells & Batteries Revenue (million) Forecast, by Application 2020 & 2033

- Table 64: Israel Primary Lithium Cells & Batteries Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Primary Lithium Cells & Batteries Revenue (million) Forecast, by Application 2020 & 2033

- Table 66: GCC Primary Lithium Cells & Batteries Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Primary Lithium Cells & Batteries Revenue (million) Forecast, by Application 2020 & 2033

- Table 68: North Africa Primary Lithium Cells & Batteries Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Primary Lithium Cells & Batteries Revenue (million) Forecast, by Application 2020 & 2033

- Table 70: South Africa Primary Lithium Cells & Batteries Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Primary Lithium Cells & Batteries Revenue (million) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Primary Lithium Cells & Batteries Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Primary Lithium Cells & Batteries Revenue million Forecast, by Application 2020 & 2033

- Table 74: Global Primary Lithium Cells & Batteries Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Primary Lithium Cells & Batteries Revenue million Forecast, by Types 2020 & 2033

- Table 76: Global Primary Lithium Cells & Batteries Volume K Forecast, by Types 2020 & 2033

- Table 77: Global Primary Lithium Cells & Batteries Revenue million Forecast, by Country 2020 & 2033

- Table 78: Global Primary Lithium Cells & Batteries Volume K Forecast, by Country 2020 & 2033

- Table 79: China Primary Lithium Cells & Batteries Revenue (million) Forecast, by Application 2020 & 2033

- Table 80: China Primary Lithium Cells & Batteries Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Primary Lithium Cells & Batteries Revenue (million) Forecast, by Application 2020 & 2033

- Table 82: India Primary Lithium Cells & Batteries Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Primary Lithium Cells & Batteries Revenue (million) Forecast, by Application 2020 & 2033

- Table 84: Japan Primary Lithium Cells & Batteries Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Primary Lithium Cells & Batteries Revenue (million) Forecast, by Application 2020 & 2033

- Table 86: South Korea Primary Lithium Cells & Batteries Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Primary Lithium Cells & Batteries Revenue (million) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Primary Lithium Cells & Batteries Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Primary Lithium Cells & Batteries Revenue (million) Forecast, by Application 2020 & 2033

- Table 90: Oceania Primary Lithium Cells & Batteries Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Primary Lithium Cells & Batteries Revenue (million) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Primary Lithium Cells & Batteries Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Primary Lithium Cells & Batteries?

The projected CAGR is approximately 8%.

2. Which companies are prominent players in the Primary Lithium Cells & Batteries?

Key companies in the market include VARTA Microbattery, SAFT, Hitachi Maxell, Vitzrocell, Renata SA, Gold Peak, EVE Energy, Huiderui Lithium Battery, FDK CORP., Ultralife.

3. What are the main segments of the Primary Lithium Cells & Batteries?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 685.8 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Primary Lithium Cells & Batteries," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Primary Lithium Cells & Batteries report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Primary Lithium Cells & Batteries?

To stay informed about further developments, trends, and reports in the Primary Lithium Cells & Batteries, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence