Key Insights

The Global Lead Acid Aircraft Battery Market is projected to reach $1.61 billion by 2033, expanding at a Compound Annual Growth Rate (CAGR) of 8.3% from 2025 to 2033. This growth is driven by sustained demand for reliable, cost-effective power in commercial, military, and general aviation. Despite advancements in lithium-ion technology, lead-acid batteries maintain a strong market presence due to their proven safety, reliability, and lower initial cost. Increased global air traffic, new aircraft production, and ongoing fleet maintenance further bolster this positive trajectory. The military sector's consistent need for durable power solutions in demanding environments also acts as a significant growth catalyst.

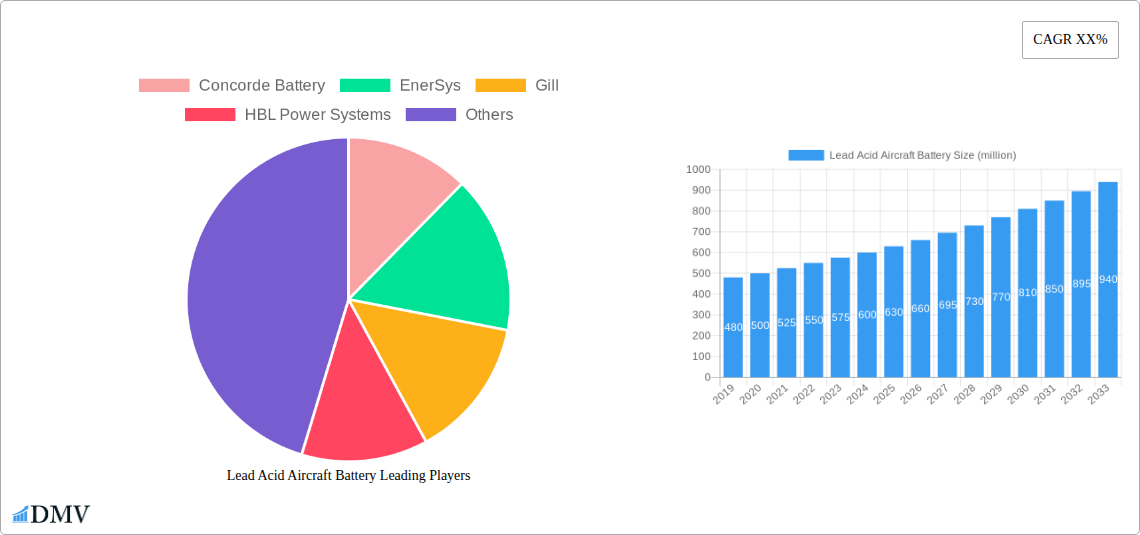

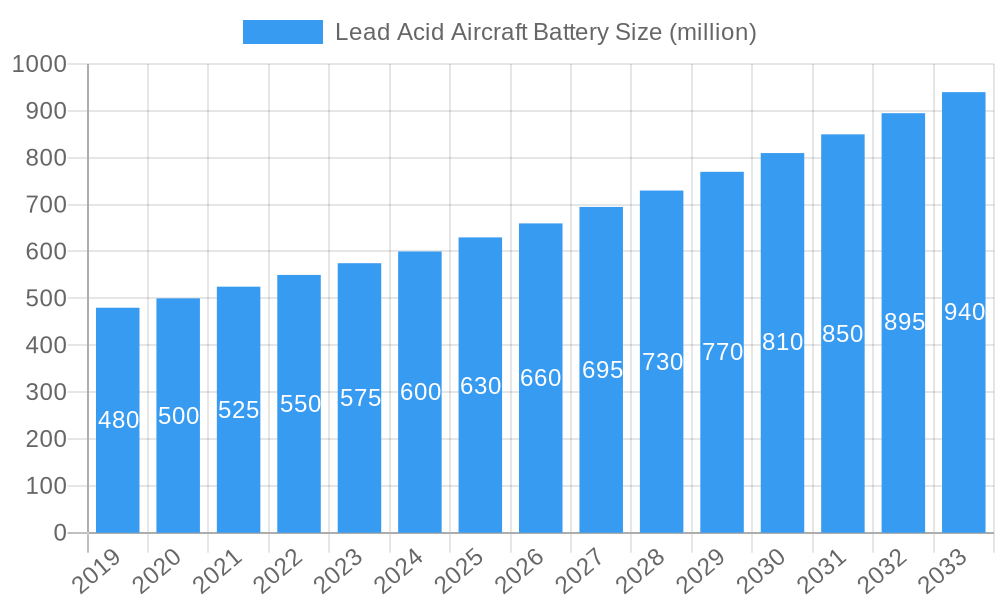

Lead Acid Aircraft Battery Market Size (In Billion)

The lead-acid aircraft battery market is adapting through design improvements for enhanced energy density and lifespan, alongside a commitment to sustainable manufacturing and recycling. Demand for specialized batteries for applications like Auxiliary Power Units (APUs) and starting systems remains strong. Key challenges include the inherent weight and energy density limitations compared to newer chemistries, potentially affecting aircraft performance. While environmental regulations regarding lead disposal are managed through existing recycling infrastructure, they remain an ongoing consideration. However, the established global supply chain and cost-effectiveness of lead-acid solutions ensure their continued market relevance.

Lead Acid Aircraft Battery Company Market Share

Lead Acid Aircraft Battery Market Composition & Trends

The global Lead Acid Aircraft Battery market is characterized by a moderately concentrated landscape, with key players such as Concorde Battery, EnerSys, Gill, and HBL Power Systems holding significant market shares. Innovation in this sector is primarily driven by the relentless pursuit of enhanced safety, extended service life, and improved energy density. Regulatory frameworks, particularly those from aviation authorities like the FAA and EASA, play a crucial role in dictating product standards, maintenance protocols, and material sourcing. While advancements in lithium-ion technologies present a long-term threat, lead-acid batteries continue to benefit from their established reliability, cost-effectiveness, and a mature supply chain, making them a persistent substitute for certain applications. End-user profiles encompass a broad spectrum of aviation operations, from commercial airlines and cargo carriers to general aviation and military applications, each with distinct performance and certification requirements. Mergers and acquisitions (M&A) activity within the industry has been limited but strategic, focusing on consolidating expertise and expanding market reach. For instance, M&A deals in the broader aerospace battery sector have seen valuations in the hundreds of millions. The market share distribution is estimated to be: Concorde Battery at approximately 35%, EnerSys at 25%, Gill at 20%, and HBL Power Systems at 15%, with the remaining 5% held by smaller regional manufacturers.

- Innovation Catalysts: Enhanced safety features, extended cycle life, improved power-to-weight ratios, and compliance with stringent aviation regulations.

- Regulatory Landscapes: FAA, EASA, and other national aviation authorities dictate design, testing, and operational standards.

- Substitute Products: Lithium-ion batteries, while offering higher energy density, face certification hurdles and higher initial costs for certain aircraft types.

- End-User Profiles: Commercial aviation (airlines, cargo), general aviation (private aircraft), military aviation, and regional air transport.

- M&A Activities: Focused on strategic partnerships and acquisitions to enhance technological capabilities and market penetration. Recent significant deals in related aerospace component markets have reached values exceeding one hundred million.

Lead Acid Aircraft Battery Industry Evolution

The Lead Acid Aircraft Battery industry has undergone a remarkable evolution, demonstrating resilience and adaptability in the face of technological shifts and evolving aviation demands. Throughout the historical period of 2019–2024, the market witnessed steady growth, driven by the consistent demand from existing aircraft fleets and the gradual expansion of air travel. This period was marked by incremental improvements in lead-acid battery technology, focusing on enhanced reliability and cost optimization. The base year, 2025, serves as a pivotal point, reflecting a mature market where established players maintain dominance while nascent trends begin to shape future trajectories. Market growth trajectories have been largely influenced by the operational lifecycles of aircraft and the replacement cycles of batteries. For instance, the average lifespan of a lead-acid aircraft battery is around 5 to 7 years, necessitating a continuous replacement market. Technological advancements have concentrated on improving charge retention, reducing weight through optimized designs and materials, and developing more robust internal structures to withstand the harsh operating conditions of aviation. Battery management systems (BMS) have also seen integration, offering enhanced monitoring and predictive maintenance capabilities, thereby extending battery life and improving safety. Shifting consumer demands, particularly from airlines, have increasingly focused on Total Cost of Ownership (TCO), where the initial purchase price, maintenance costs, and operational lifespan are all critical factors. This has further cemented the position of lead-acid batteries in segments where their proven track record and cost-effectiveness outweigh the higher upfront investment of newer technologies. Adoption metrics show a consistent replacement rate of approximately 90% for lead-acid batteries in older aircraft models, with a slower but steady adoption of advanced chemistries in new aircraft programs. The forecast period of 2025–2033 projects continued, albeit moderate, growth, as the vast existing fleet of aircraft relies on these proven power solutions. Market growth rates have averaged around 3-4% annually in recent years, and this trend is expected to continue. The industry's evolution is a testament to its ability to refine a mature technology to meet contemporary aviation needs, ensuring operational efficiency and safety across diverse aircraft segments. The value chain, from raw material sourcing to end-of-life recycling, has also seen optimization, contributing to the sustainability and economic viability of lead-acid aircraft batteries.

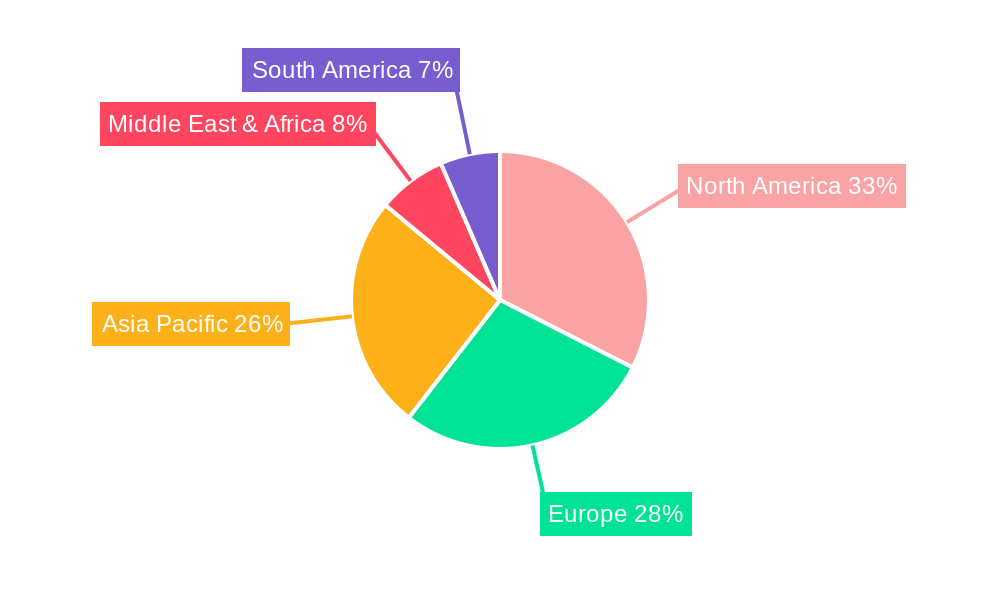

Leading Regions, Countries, or Segments in Lead Acid Aircraft Battery

North America currently stands as the dominant region in the Lead Acid Aircraft Battery market, driven by its expansive commercial aviation sector, a significant general aviation fleet, and substantial military investments. The United States, in particular, is a powerhouse, housing the largest number of aircraft globally and a robust aerospace manufacturing ecosystem. This dominance is further amplified by stringent safety regulations that, while demanding, favor proven and certified technologies like lead-acid batteries for many applications. The country’s extensive network of airports and maintenance, repair, and overhaul (MRO) facilities ensures a continuous demand for battery replacements and services, contributing to market stability.

Within the broader Lead Acid Aircraft Battery market, the Application segment of Commercial Aviation represents the most significant driver of demand. Commercial airlines operate vast fleets requiring reliable and cost-effective power solutions for their extensive flight operations. These operators prioritize longevity, safety certification, and predictable maintenance schedules, all areas where lead-acid batteries excel. The sheer volume of commercial aircraft operations globally fuels a consistent need for battery replacements, solidifying this segment's leadership.

The Type segment of Vented Lead-Acid Batteries is also a leading contributor to market value. These batteries are widely favored for their robustness, tolerance to deep discharge cycles, and lower cost of ownership compared to some sealed alternatives. Their established track record in aviation, coupled with ongoing refinements in their design and manufacturing processes, ensures their continued prevalence.

Key Drivers in North America and Commercial Aviation Application:

- Investment Trends: Sustained investments in aircraft fleet modernization and maintenance by major airlines, alongside government funding for military aviation upgrades. Over the historical period, investments in new aircraft orders alone have reached hundreds of billions of dollars.

- Regulatory Support: Proactive regulatory frameworks that emphasize safety and performance standards, which lead-acid batteries have consistently met for decades, fostering confidence among operators.

- Mature Aerospace Ecosystem: A well-established aerospace supply chain, including battery manufacturers, distributors, and MRO providers, facilitates efficient product delivery and support.

- High Aircraft Utilization Rates: Commercial aircraft operate for extended periods, leading to more frequent battery replacement cycles, thus driving consistent demand.

- Cost-Effectiveness: The lower initial purchase price and proven longevity of lead-acid batteries offer a compelling economic proposition for fleet operators.

The dominance of these regions and segments is expected to persist through the forecast period, although the growth rates may moderate as newer technologies gain traction in specific niche applications or new aircraft platforms. The inherent advantages of lead-acid technology in terms of reliability and cost will continue to underpin its strong market position.

Lead Acid Aircraft Battery Product Innovations

Product innovations in the Lead Acid Aircraft Battery sector primarily focus on enhancing existing capabilities rather than radical departures. Manufacturers are investing in advanced plate alloys and improved separator materials to extend battery lifespan and increase cycle life, pushing it beyond the current average of several thousand cycles. Enhanced internal construction techniques are being employed to improve vibration resistance, a critical factor in the demanding aviation environment. Furthermore, some innovations aim at reducing the overall weight of the battery, offering marginal but valuable fuel efficiency gains for aircraft. These advancements ensure that lead-acid batteries remain a competitive and reliable power source, delivering critical performance metrics such as reliable starting power even in extreme temperatures and consistent voltage output throughout the flight duration. The unique selling proposition remains their unparalleled cost-effectiveness and proven reliability, making them indispensable for many aviation applications.

Propelling Factors for Lead Acid Aircraft Battery Growth

Several key factors are propelling the growth of the Lead Acid Aircraft Battery market. Firstly, the sheer size and continued operation of the global aircraft fleet, particularly older models and general aviation aircraft, create a consistent demand for replacement batteries. Secondly, the inherent cost-effectiveness of lead-acid technology, in terms of both initial purchase price and total cost of ownership, remains a significant advantage for budget-conscious operators. Thirdly, the proven reliability and long service life of these batteries, coupled with established safety certifications, instill confidence in aviation authorities and end-users. Finally, ongoing incremental technological improvements, such as enhanced plate designs and more durable casings, contribute to their sustained competitiveness.

Obstacles in the Lead Acid Aircraft Battery Market

Despite its strengths, the Lead Acid Aircraft Battery market faces certain obstacles. Foremost among these is the increasing competition from advanced battery chemistries, particularly lithium-ion, which offer higher energy density and lighter weight, albeit at a higher cost and with different certification challenges. Stringent environmental regulations concerning the disposal and recycling of lead-acid batteries also pose compliance challenges and add to operational costs. Supply chain disruptions, especially for key raw materials like lead, can impact production volumes and pricing. Furthermore, the perceived lower energy density compared to newer technologies limits their suitability for certain high-performance or next-generation aircraft applications, representing a significant restraint on market expansion.

Future Opportunities in Lead Acid Aircraft Battery

Emerging opportunities for Lead Acid Aircraft Batteries lie in the development of more specialized formulations and designs tailored to specific aviation niches. The increasing demand for sustainable aviation fuels (SAFs) and the potential for hybridization in smaller aircraft could present opportunities for lead-acid batteries as part of a broader power management system. Furthermore, the continuous growth in emerging markets for aviation, particularly in Asia and Africa, where cost-sensitivity is high, will continue to drive demand for these reliable and affordable power solutions. Advancements in battery management systems specifically for lead-acid chemistries could also unlock new possibilities for performance optimization and predictive maintenance, extending their operational lifespan and appeal.

Major Players in the Lead Acid Aircraft Battery Ecosystem

- Concorde Battery

- EnerSys

- Gill

- HBL Power Systems

Key Developments in Lead Acid Aircraft Battery Industry

- 2023 September: Concorde Battery launches its latest generation of sealed lead-acid aircraft batteries, offering enhanced performance and reduced maintenance requirements.

- 2022 December: EnerSys announces a strategic partnership with a major European aircraft MRO provider to expand its service network for lead-acid aircraft batteries.

- 2021 July: Gill Batteries introduces a new lightweight design for its vented lead-acid aircraft batteries, achieving a 5% weight reduction without compromising performance.

- 2020 March: HBL Power Systems secures a significant contract to supply lead-acid aircraft batteries for a new regional jet program, highlighting continued demand for established chemistries.

- 2019 November: Industry-wide focus intensifies on battery recycling initiatives, with manufacturers exploring more sustainable end-of-life solutions for lead-acid aircraft batteries.

Strategic Lead Acid Aircraft Battery Market Forecast

The strategic Lead Acid Aircraft Battery market forecast anticipates sustained demand, primarily driven by the vast existing global aircraft fleet and the economic advantages offered by this mature technology. While incremental innovation will continue to enhance performance and longevity, the core strength of lead-acid batteries will remain their unparalleled cost-effectiveness and proven reliability. Opportunities are expected to emerge from developing markets and specialized aviation applications where higher energy density is not the paramount requirement. The market will likely see continued consolidation and strategic partnerships among key players to optimize production and distribution. The forecast suggests moderate but steady growth throughout the study period, ensuring lead-acid batteries remain a crucial component of the aviation power landscape.

Lead Acid Aircraft Battery Segmentation

- 1. Application

- 2. Types

Lead Acid Aircraft Battery Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Lead Acid Aircraft Battery Regional Market Share

Geographic Coverage of Lead Acid Aircraft Battery

Lead Acid Aircraft Battery REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 6. Global Lead Acid Aircraft Battery Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.2. Market Analysis, Insights and Forecast - by Types

- 7. North America Lead Acid Aircraft Battery Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.2. Market Analysis, Insights and Forecast - by Types

- 8. South America Lead Acid Aircraft Battery Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.2. Market Analysis, Insights and Forecast - by Types

- 9. Europe Lead Acid Aircraft Battery Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.2. Market Analysis, Insights and Forecast - by Types

- 10. Middle East & Africa Lead Acid Aircraft Battery Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.2. Market Analysis, Insights and Forecast - by Types

- 11. Asia Pacific Lead Acid Aircraft Battery Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.2. Market Analysis, Insights and Forecast - by Types

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Concorde Battery

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 EnerSys

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Gill

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 HBL Power Systems

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.1 Concorde Battery

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Lead Acid Aircraft Battery Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Lead Acid Aircraft Battery Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Lead Acid Aircraft Battery Revenue (billion), by Application 2025 & 2033

- Figure 4: North America Lead Acid Aircraft Battery Volume (K), by Application 2025 & 2033

- Figure 5: North America Lead Acid Aircraft Battery Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Lead Acid Aircraft Battery Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Lead Acid Aircraft Battery Revenue (billion), by Types 2025 & 2033

- Figure 8: North America Lead Acid Aircraft Battery Volume (K), by Types 2025 & 2033

- Figure 9: North America Lead Acid Aircraft Battery Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Lead Acid Aircraft Battery Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Lead Acid Aircraft Battery Revenue (billion), by Country 2025 & 2033

- Figure 12: North America Lead Acid Aircraft Battery Volume (K), by Country 2025 & 2033

- Figure 13: North America Lead Acid Aircraft Battery Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Lead Acid Aircraft Battery Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Lead Acid Aircraft Battery Revenue (billion), by Application 2025 & 2033

- Figure 16: South America Lead Acid Aircraft Battery Volume (K), by Application 2025 & 2033

- Figure 17: South America Lead Acid Aircraft Battery Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Lead Acid Aircraft Battery Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Lead Acid Aircraft Battery Revenue (billion), by Types 2025 & 2033

- Figure 20: South America Lead Acid Aircraft Battery Volume (K), by Types 2025 & 2033

- Figure 21: South America Lead Acid Aircraft Battery Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Lead Acid Aircraft Battery Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Lead Acid Aircraft Battery Revenue (billion), by Country 2025 & 2033

- Figure 24: South America Lead Acid Aircraft Battery Volume (K), by Country 2025 & 2033

- Figure 25: South America Lead Acid Aircraft Battery Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Lead Acid Aircraft Battery Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Lead Acid Aircraft Battery Revenue (billion), by Application 2025 & 2033

- Figure 28: Europe Lead Acid Aircraft Battery Volume (K), by Application 2025 & 2033

- Figure 29: Europe Lead Acid Aircraft Battery Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Lead Acid Aircraft Battery Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Lead Acid Aircraft Battery Revenue (billion), by Types 2025 & 2033

- Figure 32: Europe Lead Acid Aircraft Battery Volume (K), by Types 2025 & 2033

- Figure 33: Europe Lead Acid Aircraft Battery Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Lead Acid Aircraft Battery Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Lead Acid Aircraft Battery Revenue (billion), by Country 2025 & 2033

- Figure 36: Europe Lead Acid Aircraft Battery Volume (K), by Country 2025 & 2033

- Figure 37: Europe Lead Acid Aircraft Battery Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Lead Acid Aircraft Battery Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Lead Acid Aircraft Battery Revenue (billion), by Application 2025 & 2033

- Figure 40: Middle East & Africa Lead Acid Aircraft Battery Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Lead Acid Aircraft Battery Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Lead Acid Aircraft Battery Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Lead Acid Aircraft Battery Revenue (billion), by Types 2025 & 2033

- Figure 44: Middle East & Africa Lead Acid Aircraft Battery Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Lead Acid Aircraft Battery Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Lead Acid Aircraft Battery Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Lead Acid Aircraft Battery Revenue (billion), by Country 2025 & 2033

- Figure 48: Middle East & Africa Lead Acid Aircraft Battery Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Lead Acid Aircraft Battery Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Lead Acid Aircraft Battery Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Lead Acid Aircraft Battery Revenue (billion), by Application 2025 & 2033

- Figure 52: Asia Pacific Lead Acid Aircraft Battery Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Lead Acid Aircraft Battery Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Lead Acid Aircraft Battery Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Lead Acid Aircraft Battery Revenue (billion), by Types 2025 & 2033

- Figure 56: Asia Pacific Lead Acid Aircraft Battery Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Lead Acid Aircraft Battery Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Lead Acid Aircraft Battery Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Lead Acid Aircraft Battery Revenue (billion), by Country 2025 & 2033

- Figure 60: Asia Pacific Lead Acid Aircraft Battery Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Lead Acid Aircraft Battery Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Lead Acid Aircraft Battery Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Lead Acid Aircraft Battery Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Lead Acid Aircraft Battery Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Lead Acid Aircraft Battery Revenue billion Forecast, by Types 2020 & 2033

- Table 4: Global Lead Acid Aircraft Battery Volume K Forecast, by Types 2020 & 2033

- Table 5: Global Lead Acid Aircraft Battery Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Lead Acid Aircraft Battery Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Lead Acid Aircraft Battery Revenue billion Forecast, by Application 2020 & 2033

- Table 8: Global Lead Acid Aircraft Battery Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Lead Acid Aircraft Battery Revenue billion Forecast, by Types 2020 & 2033

- Table 10: Global Lead Acid Aircraft Battery Volume K Forecast, by Types 2020 & 2033

- Table 11: Global Lead Acid Aircraft Battery Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global Lead Acid Aircraft Battery Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Lead Acid Aircraft Battery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United States Lead Acid Aircraft Battery Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Lead Acid Aircraft Battery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Lead Acid Aircraft Battery Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Lead Acid Aircraft Battery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Mexico Lead Acid Aircraft Battery Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Lead Acid Aircraft Battery Revenue billion Forecast, by Application 2020 & 2033

- Table 20: Global Lead Acid Aircraft Battery Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Lead Acid Aircraft Battery Revenue billion Forecast, by Types 2020 & 2033

- Table 22: Global Lead Acid Aircraft Battery Volume K Forecast, by Types 2020 & 2033

- Table 23: Global Lead Acid Aircraft Battery Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global Lead Acid Aircraft Battery Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Lead Acid Aircraft Battery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Brazil Lead Acid Aircraft Battery Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Lead Acid Aircraft Battery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Argentina Lead Acid Aircraft Battery Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Lead Acid Aircraft Battery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Lead Acid Aircraft Battery Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Lead Acid Aircraft Battery Revenue billion Forecast, by Application 2020 & 2033

- Table 32: Global Lead Acid Aircraft Battery Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Lead Acid Aircraft Battery Revenue billion Forecast, by Types 2020 & 2033

- Table 34: Global Lead Acid Aircraft Battery Volume K Forecast, by Types 2020 & 2033

- Table 35: Global Lead Acid Aircraft Battery Revenue billion Forecast, by Country 2020 & 2033

- Table 36: Global Lead Acid Aircraft Battery Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Lead Acid Aircraft Battery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Lead Acid Aircraft Battery Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Lead Acid Aircraft Battery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Germany Lead Acid Aircraft Battery Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Lead Acid Aircraft Battery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: France Lead Acid Aircraft Battery Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Lead Acid Aircraft Battery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Italy Lead Acid Aircraft Battery Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Lead Acid Aircraft Battery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Spain Lead Acid Aircraft Battery Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Lead Acid Aircraft Battery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Russia Lead Acid Aircraft Battery Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Lead Acid Aircraft Battery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: Benelux Lead Acid Aircraft Battery Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Lead Acid Aircraft Battery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Nordics Lead Acid Aircraft Battery Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Lead Acid Aircraft Battery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Lead Acid Aircraft Battery Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Lead Acid Aircraft Battery Revenue billion Forecast, by Application 2020 & 2033

- Table 56: Global Lead Acid Aircraft Battery Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Lead Acid Aircraft Battery Revenue billion Forecast, by Types 2020 & 2033

- Table 58: Global Lead Acid Aircraft Battery Volume K Forecast, by Types 2020 & 2033

- Table 59: Global Lead Acid Aircraft Battery Revenue billion Forecast, by Country 2020 & 2033

- Table 60: Global Lead Acid Aircraft Battery Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Lead Acid Aircraft Battery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Turkey Lead Acid Aircraft Battery Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Lead Acid Aircraft Battery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Israel Lead Acid Aircraft Battery Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Lead Acid Aircraft Battery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: GCC Lead Acid Aircraft Battery Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Lead Acid Aircraft Battery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 68: North Africa Lead Acid Aircraft Battery Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Lead Acid Aircraft Battery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 70: South Africa Lead Acid Aircraft Battery Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Lead Acid Aircraft Battery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Lead Acid Aircraft Battery Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Lead Acid Aircraft Battery Revenue billion Forecast, by Application 2020 & 2033

- Table 74: Global Lead Acid Aircraft Battery Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Lead Acid Aircraft Battery Revenue billion Forecast, by Types 2020 & 2033

- Table 76: Global Lead Acid Aircraft Battery Volume K Forecast, by Types 2020 & 2033

- Table 77: Global Lead Acid Aircraft Battery Revenue billion Forecast, by Country 2020 & 2033

- Table 78: Global Lead Acid Aircraft Battery Volume K Forecast, by Country 2020 & 2033

- Table 79: China Lead Acid Aircraft Battery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 80: China Lead Acid Aircraft Battery Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Lead Acid Aircraft Battery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 82: India Lead Acid Aircraft Battery Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Lead Acid Aircraft Battery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 84: Japan Lead Acid Aircraft Battery Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Lead Acid Aircraft Battery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 86: South Korea Lead Acid Aircraft Battery Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Lead Acid Aircraft Battery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Lead Acid Aircraft Battery Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Lead Acid Aircraft Battery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 90: Oceania Lead Acid Aircraft Battery Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Lead Acid Aircraft Battery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Lead Acid Aircraft Battery Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Lead Acid Aircraft Battery?

The projected CAGR is approximately 8.3%.

2. Which companies are prominent players in the Lead Acid Aircraft Battery?

Key companies in the market include Concorde Battery, EnerSys, Gill, HBL Power Systems.

3. What are the main segments of the Lead Acid Aircraft Battery?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.61 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4350.00, USD 6525.00, and USD 8700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Lead Acid Aircraft Battery," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Lead Acid Aircraft Battery report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Lead Acid Aircraft Battery?

To stay informed about further developments, trends, and reports in the Lead Acid Aircraft Battery, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence