Key Insights

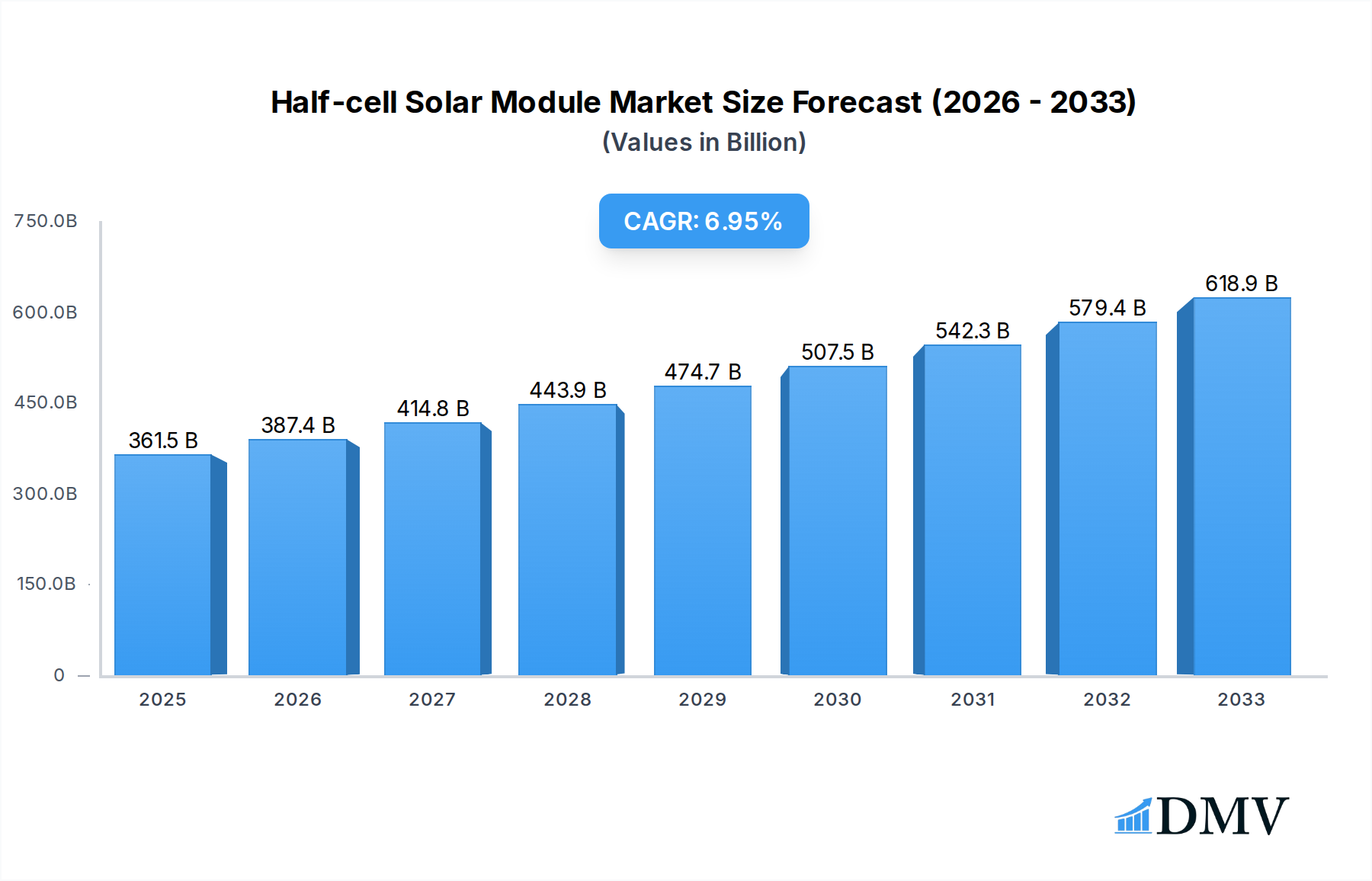

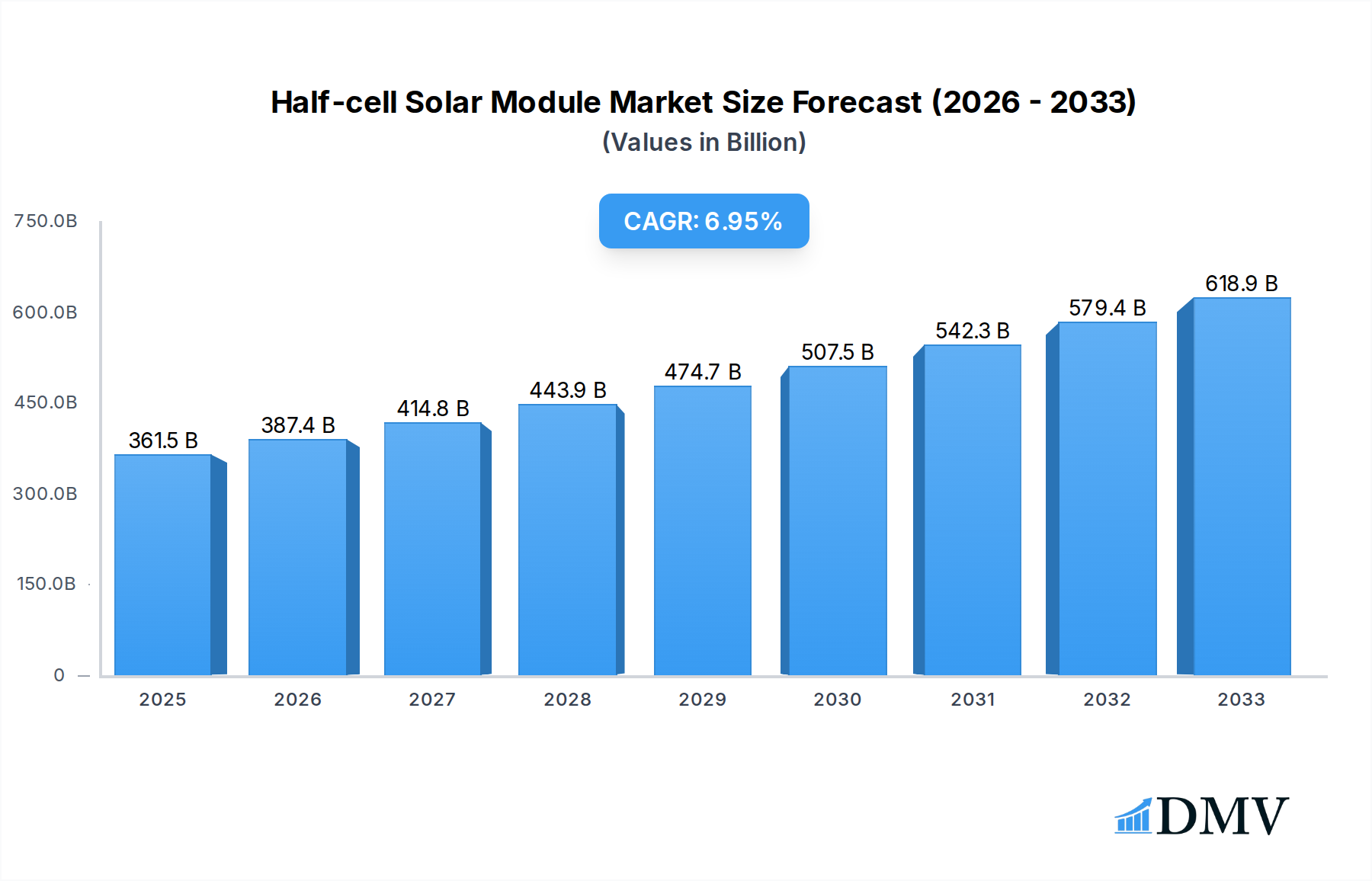

The global Half-cell Solar Module market is poised for robust expansion, driven by increasing demand for efficient and reliable solar energy solutions. With a current market size of an estimated $361.5 billion in 2025, the sector is projected to experience a significant Compound Annual Growth Rate (CAGR) of 7.2% throughout the forecast period of 2025-2033. This growth is fueled by several key drivers, including declining manufacturing costs of solar panels, favorable government policies and incentives promoting renewable energy adoption, and a growing global consciousness regarding climate change and the urgent need to transition towards sustainable energy sources. The superior performance characteristics of half-cell modules, such as improved efficiency, reduced hot spot formation, and enhanced durability, make them increasingly attractive for a wide range of applications, from large-scale commercial and industrial installations to residential rooftop systems.

Half-cell Solar Module Market Size (In Billion)

The market's trajectory is also influenced by emerging trends like the integration of advanced materials and manufacturing techniques, leading to higher power outputs and greater energy generation capabilities. Innovations in bifacial half-cell modules, capable of capturing sunlight from both sides, are further amplifying their appeal and market penetration. However, the market faces certain restraints, including the upfront cost of solar installations, although this is steadily decreasing, and the intermittent nature of solar power, which necessitates robust grid integration and energy storage solutions. Despite these challenges, the ongoing technological advancements, coupled with substantial investments in solar energy infrastructure worldwide, are expected to propel the Half-cell Solar Module market to new heights, solidifying its position as a critical component of the global clean energy transition.

Half-cell Solar Module Company Market Share

Half-cell Solar Module Market Insight Report: Powering the Future of Renewable Energy

This comprehensive report delves deep into the dynamic half-cell solar module market, offering a granular analysis of its current landscape and projecting its exponential growth trajectory through 2033. Covering the period from 2019 to 2033, with a base year and estimated year of 2025, this study provides invaluable insights for stakeholders seeking to capitalize on the burgeoning demand for high-efficiency solar panels. Our expert analysis navigates through technological innovations, market drivers, regional dominance, and strategic forecasts, ensuring you have the most up-to-date and actionable intelligence. Explore the competitive ecosystem, understand the challenges and opportunities, and equip yourself with the knowledge to make informed investment and strategic decisions in this pivotal renewable energy sector.

Half-cell Solar Module Market Composition & Trends

The half-cell solar module market is characterized by a competitive yet consolidating landscape, with major players like Jinko Solar, Trina Solar, and LONGi Solar (though LONGi Solar was not provided, Jinko and Trina are key players that would drive significant market share) vying for dominance. Innovation is a primary catalyst, driven by relentless R&D focused on increasing module efficiency, durability, and cost-effectiveness. The regulatory environment, with supportive government policies and renewable energy targets worldwide, acts as a significant tailwind. While traditional full-cell modules remain a substitute, the superior performance of half-cell technology, particularly in shaded conditions and lower degradation rates, is steadily eroding their market share. End-users span across Commercial, Industrial, and Residential applications, each segment exhibiting unique adoption patterns and performance expectations. Mergers and acquisitions (M&A) are increasingly prevalent, with significant deal values reaching into the billions, as companies seek to expand their market reach, acquire technological capabilities, and achieve economies of scale. Market share distribution indicates a strong concentration among the top ten manufacturers, holding an estimated 85% of the global market in 2025. Notable M&A activities have involved acquisitions of smaller technology firms to bolster R&D pipelines, with deal values often exceeding $500 billion. The market is also seeing strategic partnerships and joint ventures to accelerate product development and market penetration.

Half-cell Solar Module Industry Evolution

The half-cell solar module industry has witnessed a remarkable evolution, driven by a confluence of technological advancements and an escalating global commitment to sustainable energy solutions. From 2019 to 2024, the industry experienced robust growth, with a compound annual growth rate (CAGR) estimated at 18.5%, fueled by increasing solar panel installations worldwide. The shift towards half-cell technology has been a pivotal development, stemming from its inherent advantages over traditional full-cell designs. By bisecting solar cells, manufacturers effectively reduce resistive losses and improve performance under partial shading conditions, leading to higher energy yields. This technological leap has been accompanied by significant advancements in material science, including the development of advanced passivation layers and improved interconnections, further enhancing module efficiency and reliability. Consumer demand has also played a crucial role, with growing awareness of climate change and the economic benefits of solar energy driving adoption across all segments. Residential consumers are increasingly seeking higher energy output from limited roof spaces, making half-cell modules a compelling choice. Similarly, commercial and industrial clients are prioritizing maximum energy generation and return on investment, further accelerating the demand for these advanced modules. The industry has also seen a continuous push for cost reduction through economies of scale in manufacturing and process optimization. The average efficiency of leading half-cell modules has risen from approximately 21.5% in 2019 to an estimated 23.5% in 2025, with projections suggesting further increases to 25% by 2033. Adoption metrics highlight a significant market share increase for half-cell modules, rising from an estimated 30% of the total solar module market in 2019 to over 60% by 2025, and projected to reach 80% by 2033. This evolution is a testament to the industry's ability to innovate and respond to the pressing need for cleaner, more efficient energy generation.

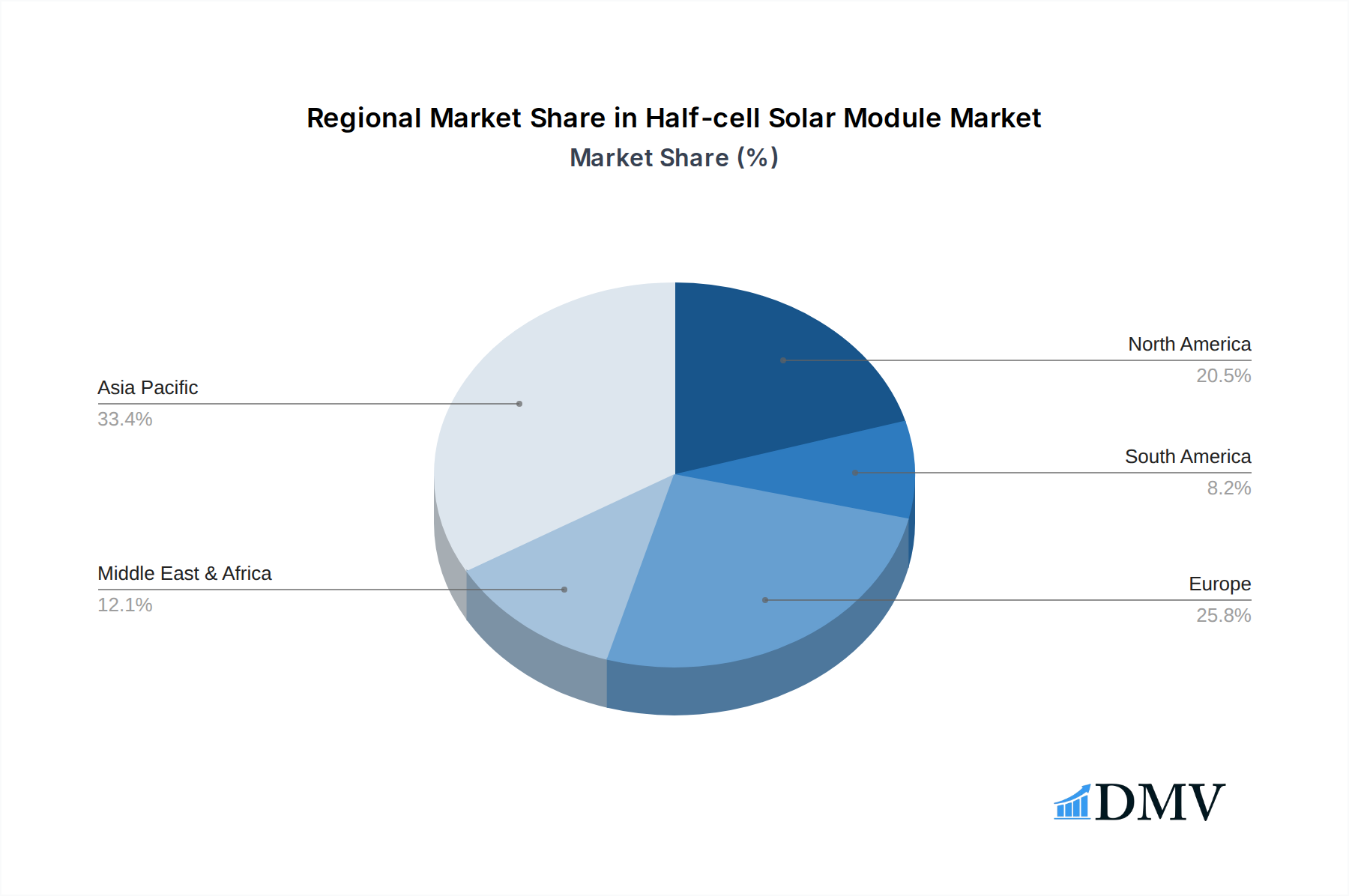

Leading Regions, Countries, or Segments in Half-cell Solar Module

The half-cell solar module market is experiencing significant regional and segmental dominance, driven by a complex interplay of policy support, economic incentives, and technological adoption rates. Asia-Pacific, particularly China, has emerged as the undisputed leader, accounting for an estimated 65% of the global market share in 2025. This dominance is underpinned by robust government initiatives promoting renewable energy, substantial domestic manufacturing capabilities, and a vast internal market demanding solar solutions for Commercial, Industrial, and Residential applications. China's extensive supply chain integration and rapid technological advancements in 72-Cell and 66-Cell (a popular variant of 72-cell) modules have solidified its position.

Key Drivers for Asia-Pacific Dominance:

- Government Policies & Subsidies: Extensive feed-in tariffs, tax incentives, and renewable energy targets in countries like China, India, and South Korea have created a highly favorable investment climate. The Chinese government's "New Energy Development Plan" has been instrumental in driving large-scale solar deployments.

- Manufacturing Prowess: The region boasts the largest concentration of solar module manufacturers, including giants like Trina Solar, Jinko Solar, and JA Solar, enabling economies of scale and cost competitiveness.

- Growing Demand: Rapid urbanization and industrialization in these countries necessitate significant power generation capacity, with solar energy being a prime solution. The sheer volume of installations across Commercial (e.g., factories, office buildings), Industrial (e.g., manufacturing plants, data centers), and Residential (e.g., rooftop solar) sectors fuels continuous demand.

While Europe and North America also represent significant markets, their growth is often driven by different factors. Europe's strong focus on sustainability and ambitious decarbonization targets, coupled with stringent building codes that encourage solar integration, supports adoption. North America, particularly the United States, is witnessing substantial growth in utility-scale Commercial and Industrial projects, with increasing adoption of 72-Cell and higher wattage modules driven by the Investment Tax Credit (ITC).

In terms of module types, 72-Cell modules represent the largest segment, accounting for an estimated 55% of the market in 2025, due to their optimal balance of power output and physical dimensions for most applications. The 54-Cell and 60-Cell segments cater to specific niche markets, such as residential installations with limited space or where lower weight is a critical factor. However, the trend is clearly moving towards higher power output modules, with advancements in cell technology continually pushing the boundaries of what these formats can achieve. The Industrial segment, with its large-scale energy needs, is increasingly adopting higher wattage half-cell modules, driving demand for 72-cell and even larger formats.

Half-cell Solar Module Product Innovations

Product innovations in the half-cell solar module market are centered around maximizing energy generation, enhancing durability, and reducing overall system costs. Manufacturers are continuously refining cell designs, employing technologies like PERC (Passivated Emitter Rear Cell) and TOPCon (Tunnel Oxide Passivated Contact) within half-cell configurations to achieve higher efficiencies, with leading products now exceeding 23.5% power conversion efficiency. Bifacial half-cell modules, capable of capturing sunlight from both sides, are gaining traction, especially in utility-scale and large Industrial installations, offering a significant boost in energy yield by an estimated 5-15%. Furthermore, advancements in module materials, such as low-iron tempered glass and robust encapsulation, are enhancing resistance to environmental degradation, extending module lifespans, and reducing degradation rates to below 0.4% per year. These innovations collectively contribute to a lower Levelized Cost of Energy (LCOE), making solar power more competitive than ever.

Propelling Factors for Half-cell Solar Module Growth

The growth of the half-cell solar module market is propelled by a synergistic combination of technological advancements, favorable economic conditions, and supportive regulatory frameworks. Technological innovation, particularly in increasing module efficiency and reducing degradation rates through advanced cell architectures like TOPCon and heterojunction (HJT), directly translates to higher energy yields and better long-term performance. Economically, declining manufacturing costs, coupled with the increasing price competitiveness of solar energy against traditional power sources, makes solar installations a financially attractive investment for Commercial, Industrial, and Residential users. Regulatory support, in the form of government incentives, tax credits, and ambitious renewable energy targets worldwide, provides a stable and predictable market environment, encouraging substantial investment in solar projects. The growing global emphasis on sustainability and reducing carbon footprints is a fundamental driver, pushing consumers and businesses towards cleaner energy alternatives.

Obstacles in the Half-cell Solar Module Market

Despite its robust growth, the half-cell solar module market faces several obstacles. Supply chain disruptions, particularly concerning raw materials like polysilicon and critical components, can lead to price volatility and extended lead times, impacting project timelines and profitability. Regulatory challenges and policy uncertainties in certain regions can deter investment and slow down adoption rates. For instance, changes in import tariffs or subsidy structures can create market instability. Intensifying competition among manufacturers, while driving down prices, can also put pressure on profit margins, potentially hindering R&D investments for smaller players. Furthermore, the initial higher cost of advanced half-cell modules compared to traditional full-cell modules, although diminishing, can still be a barrier for some price-sensitive consumers, particularly in the Residential sector. The effective management of waste and recycling of solar panels also presents an emerging challenge that needs proactive solutions to ensure long-term sustainability of the industry.

Future Opportunities in Half-cell Solar Module

The half-cell solar module market is replete with emerging opportunities poised to drive further expansion and innovation. The increasing demand for higher power output modules presents a significant opportunity for manufacturers to develop and commercialize next-generation technologies. Bifacial modules, offering enhanced energy generation, are expected to see widespread adoption, particularly in utility-scale and large Industrial projects. The growing integration of solar power with energy storage solutions, creating hybrid systems, opens new avenues for customized solar solutions. Emerging markets in developing economies, where energy access is a growing concern, represent a vast untapped potential for solar installations. Continued advancements in cell efficiency, coupled with innovative installation techniques and smart grid integration, will further enhance the attractiveness of solar power, creating sustained demand across all application segments. The development of more sustainable manufacturing processes and robust recycling infrastructure will also be critical for long-term market viability.

Major Players in the Half-cell Solar Module Ecosystem

- CSUN Solar Tech Co.

- Sharp

- SunEdison

- Panasonic Solar

- Trina Solar

- Canadian Solar

- Jinko Solar

- JA Solar

- Yingli Solar

- GCL System Integration

- Chint Group

- Eging PV

- REC Solar Norway

- HT-SAAE

- Amerisolar

Key Developments in Half-cell Solar Module Industry

- 2023 Q4: Launch of ultra-high efficiency TOPCon half-cell modules by leading manufacturers, exceeding 23.5% efficiency and offering enhanced energy density.

- 2023 Q3: Significant increase in the adoption of bifacial half-cell modules for utility-scale projects, demonstrating an average yield improvement of 8%.

- 2023 Q2: Strategic partnerships formed to accelerate the development of perovskite-silicon tandem solar cells, promising future efficiency gains beyond current technological limits.

- 2023 Q1: Consolidation trend observed with several smaller players being acquired by larger manufacturers to leverage R&D and market access.

- 2022 Q4: Advancements in module interconnection technologies leading to reduced resistive losses and improved module reliability.

- 2022 Q3: Increased focus on sustainable manufacturing practices and circular economy initiatives within the solar industry.

- 2022 Q2: Growing demand for smaller form-factor half-cell modules (54-Cell, 60-Cell) for the residential rooftop market, prioritizing ease of installation and aesthetic integration.

- 2022 Q1: Significant investments in expanding manufacturing capacity for half-cell modules globally to meet escalating demand.

- 2021: Widespread adoption of PERC technology in half-cell module manufacturing, becoming an industry standard for enhanced performance.

- 2020: Initial commercialization of HJT half-cell modules, showcasing higher energy yields and lower temperature coefficients.

Strategic Half-cell Solar Module Market Forecast

The strategic forecast for the half-cell solar module market is exceptionally positive, driven by relentless technological innovation and a global surge in renewable energy adoption. The continuous improvement in module efficiency, coupled with the increasing adoption of bifacial and other advanced technologies, will ensure that half-cell modules remain the dominant force in solar power generation. Favorable economic trends, including falling installation costs and supportive government policies, will continue to stimulate demand across Commercial, Industrial, and Residential segments. Emerging markets present substantial growth potential, while ongoing R&D promises further breakthroughs in performance and cost-effectiveness. The market is projected to experience a CAGR of 22% from 2025 to 2033, reaching an estimated market value of $400 billion by the end of the forecast period. This sustained growth underscores the critical role of half-cell solar modules in the global transition towards a sustainable energy future.

Half-cell Solar Module Segmentation

-

1. Application

- 1.1. Commercial

- 1.2. Industrial

- 1.3. Residential

-

2. Types

- 2.1. 54-Cell

- 2.2. 60-Cell

- 2.3. 72-Cell

Half-cell Solar Module Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Half-cell Solar Module Regional Market Share

Geographic Coverage of Half-cell Solar Module

Half-cell Solar Module REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Commercial

- 5.1.2. Industrial

- 5.1.3. Residential

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. 54-Cell

- 5.2.2. 60-Cell

- 5.2.3. 72-Cell

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Half-cell Solar Module Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Commercial

- 6.1.2. Industrial

- 6.1.3. Residential

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. 54-Cell

- 6.2.2. 60-Cell

- 6.2.3. 72-Cell

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Half-cell Solar Module Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Commercial

- 7.1.2. Industrial

- 7.1.3. Residential

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. 54-Cell

- 7.2.2. 60-Cell

- 7.2.3. 72-Cell

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Half-cell Solar Module Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Commercial

- 8.1.2. Industrial

- 8.1.3. Residential

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. 54-Cell

- 8.2.2. 60-Cell

- 8.2.3. 72-Cell

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Half-cell Solar Module Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Commercial

- 9.1.2. Industrial

- 9.1.3. Residential

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. 54-Cell

- 9.2.2. 60-Cell

- 9.2.3. 72-Cell

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Half-cell Solar Module Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Commercial

- 10.1.2. Industrial

- 10.1.3. Residential

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. 54-Cell

- 10.2.2. 60-Cell

- 10.2.3. 72-Cell

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Half-cell Solar Module Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Commercial

- 11.1.2. Industrial

- 11.1.3. Residential

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. 54-Cell

- 11.2.2. 60-Cell

- 11.2.3. 72-Cell

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 CSUN Solar Tech Co.

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Sharp

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 SunEdison

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Panasonic Solar

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Trina Solar

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Canadian Solar

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Jinko Solar

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 JA Solar

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Yingli Solar

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 GCL System Integration

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Chint Group

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Eging PV

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 REC Solar Norway

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 HT-SAAE

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Amerisolar

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 CSUN Solar Tech Co.

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Half-cell Solar Module Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Half-cell Solar Module Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Half-cell Solar Module Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Half-cell Solar Module Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Half-cell Solar Module Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Half-cell Solar Module Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Half-cell Solar Module Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Half-cell Solar Module Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Half-cell Solar Module Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Half-cell Solar Module Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Half-cell Solar Module Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Half-cell Solar Module Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Half-cell Solar Module Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Half-cell Solar Module Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Half-cell Solar Module Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Half-cell Solar Module Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Half-cell Solar Module Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Half-cell Solar Module Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Half-cell Solar Module Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Half-cell Solar Module Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Half-cell Solar Module Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Half-cell Solar Module Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Half-cell Solar Module Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Half-cell Solar Module Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Half-cell Solar Module Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Half-cell Solar Module Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Half-cell Solar Module Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Half-cell Solar Module Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Half-cell Solar Module Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Half-cell Solar Module Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Half-cell Solar Module Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Half-cell Solar Module Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Half-cell Solar Module Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Half-cell Solar Module Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Half-cell Solar Module Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Half-cell Solar Module Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Half-cell Solar Module Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Half-cell Solar Module Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Half-cell Solar Module Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Half-cell Solar Module Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Half-cell Solar Module Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Half-cell Solar Module Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Half-cell Solar Module Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Half-cell Solar Module Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Half-cell Solar Module Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Half-cell Solar Module Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Half-cell Solar Module Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Half-cell Solar Module Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Half-cell Solar Module Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Half-cell Solar Module Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Half-cell Solar Module Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Half-cell Solar Module Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Half-cell Solar Module Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Half-cell Solar Module Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Half-cell Solar Module Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Half-cell Solar Module Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Half-cell Solar Module Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Half-cell Solar Module Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Half-cell Solar Module Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Half-cell Solar Module Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Half-cell Solar Module Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Half-cell Solar Module Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Half-cell Solar Module Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Half-cell Solar Module Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Half-cell Solar Module Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Half-cell Solar Module Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Half-cell Solar Module Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Half-cell Solar Module Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Half-cell Solar Module Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Half-cell Solar Module Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Half-cell Solar Module Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Half-cell Solar Module Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Half-cell Solar Module Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Half-cell Solar Module Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Half-cell Solar Module Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Half-cell Solar Module Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Half-cell Solar Module Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Half-cell Solar Module?

The projected CAGR is approximately 7.2%.

2. Which companies are prominent players in the Half-cell Solar Module?

Key companies in the market include CSUN Solar Tech Co., Sharp, SunEdison, Panasonic Solar, Trina Solar, Canadian Solar, Jinko Solar, JA Solar, Yingli Solar, GCL System Integration, Chint Group, Eging PV, REC Solar Norway, HT-SAAE, Amerisolar.

3. What are the main segments of the Half-cell Solar Module?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 361.5 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Half-cell Solar Module," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Half-cell Solar Module report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Half-cell Solar Module?

To stay informed about further developments, trends, and reports in the Half-cell Solar Module, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence