Key Insights

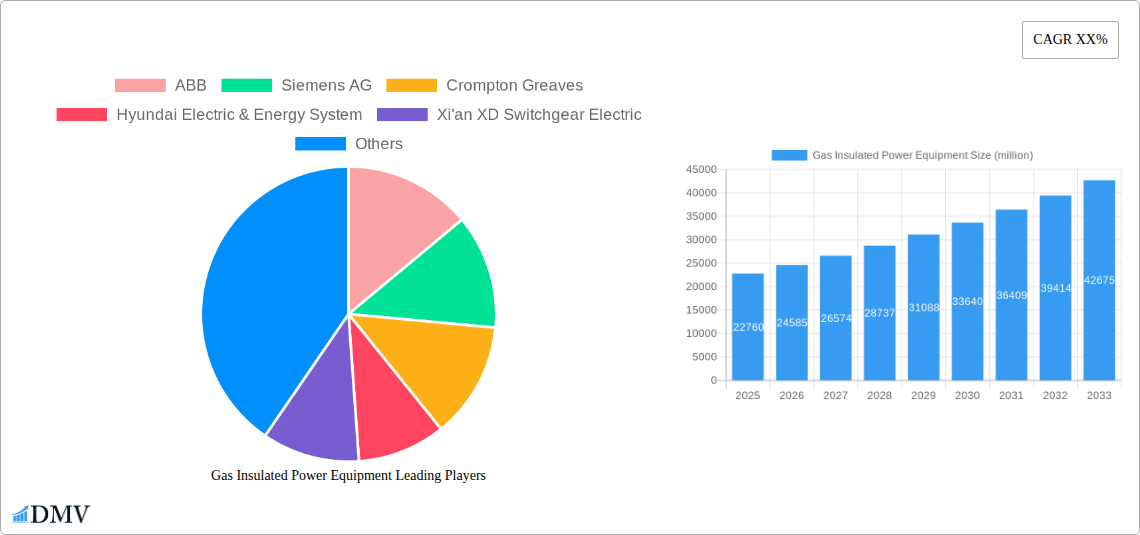

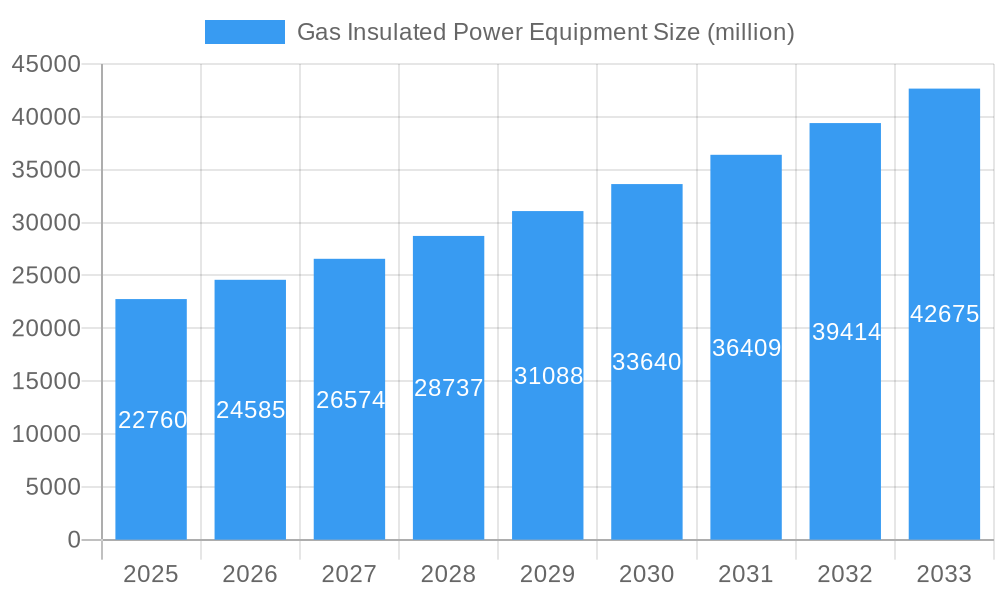

The global Gas Insulated Power Equipment market is poised for significant expansion, projected to reach $22.76 billion in 2025. This robust growth is driven by an accelerating Compound Annual Growth Rate (CAGR) of 8.06%, indicating a sustained upward trajectory throughout the forecast period of 2025-2033. The increasing demand for reliable and efficient power transmission and distribution systems, coupled with the continuous upgrade of aging grid infrastructure, forms the bedrock of this market's expansion. Furthermore, the global push towards renewable energy integration, which often necessitates advanced grid solutions for stability and control, is a substantial contributor. High-Voltage Direct Current (HVDC) and High-Voltage Alternating Current (HVAC) applications are expected to be the primary consumers of these advanced gas-insulated power equipment, highlighting the critical role they play in modernizing electrical grids and facilitating the seamless flow of electricity.

Gas Insulated Power Equipment Market Size (In Billion)

The market's dynamism is further fueled by technological advancements and a growing preference for Gas Insulated Switchgear (GIS) and Gas Insulated Transmission Lines (GITL) due to their superior performance, reduced footprint, and enhanced safety features compared to traditional air-insulated equipment. Leading players such as ABB, Siemens AG, and Schneider Electric are at the forefront of innovation, investing heavily in research and development to introduce more compact, environmentally friendly, and digitally integrated solutions. While the market benefits from strong demand drivers, potential challenges such as the high initial cost of gas-insulated equipment and the availability of skilled labor for installation and maintenance could moderate growth. However, the long-term benefits in terms of operational efficiency, reduced maintenance, and environmental compliance are expected to outweigh these concerns, ensuring a healthy market outlook. The Asia Pacific region, particularly China and India, is anticipated to be a major growth engine, owing to rapid industrialization and substantial investments in power infrastructure.

Gas Insulated Power Equipment Company Market Share

Here is an SEO-optimized and insightful report description for Gas Insulated Power Equipment, incorporating all your specified details and adhering to formatting requirements.

Gas Insulated Power Equipment Market Composition & Trends

This comprehensive report delves into the intricate market composition and evolving trends of the global Gas Insulated Power Equipment market, valued at an estimated $XXX billion in the base year of 2025. The market analysis explores key aspects including market concentration, identifying leading players such as ABB, Siemens AG, Crompton Greaves, Hyundai Electric & Energy System, Xi'an XD Switchgear Electric, Meidensha Corporation, Schneider Electric, and Larsen & Toubro, which collectively hold an estimated XX% market share. Innovation catalysts are rigorously examined, with a particular focus on advancements in SF6 alternatives and modular designs. The regulatory landscape is dissected, highlighting the impact of environmental regulations and grid modernization initiatives on market dynamics. Substitute products, while limited in high-voltage applications, are assessed for their potential impact on specific segments. End-user profiles reveal a strong reliance on utilities and renewable energy developers, driving demand for reliable and compact power transmission solutions. Mergers and Acquisitions (M&A) activities are a significant feature, with an estimated $XXX billion in M&A deals projected during the historical period (2019-2024), indicating strategic consolidation and expansion within the industry.

- Market Share Distribution: Dominant players collectively hold an estimated XX% of the global market.

- M&A Deal Value: Estimated $XXX billion in M&A deals recorded from 2019-2024.

- Innovation Focus: Development of eco-friendly insulating gases and compact substation designs.

- End-User Dominance: Utilities and renewable energy developers represent over XX% of the customer base.

Gas Insulated Power Equipment Industry Evolution

The Gas Insulated Power Equipment industry has witnessed a remarkable evolution, driven by the escalating demand for efficient, reliable, and compact power transmission and distribution solutions. The study period, spanning from 2019 to 2033, with a base year of 2025, illustrates a dynamic growth trajectory shaped by technological advancements, stringent environmental regulations, and the global push towards grid modernization and renewable energy integration. During the historical period (2019-2024), the market experienced a Compound Annual Growth Rate (CAGR) of approximately XX%, fueled by significant investments in upgrading aging electrical infrastructure and expanding power grids in emerging economies. The estimated market size for 2025 is pegged at $XXX billion, with projections indicating a robust CAGR of XX% during the forecast period (2025-2033).

Technological advancements have been pivotal in this evolution. The transition from traditional air-insulated substations to Gas Insulated Switchgear (GIS) and Gas Insulated Lines (GIL) offers substantial benefits, including reduced footprint, enhanced safety, lower maintenance, and improved reliability, crucial for urban environments and space-constrained locations. The development and adoption of High-Voltage Direct Current (HVDC) technology, particularly for long-distance power transmission and interconnections, have further propelled the demand for specialized gas-insulated equipment capable of handling higher voltage levels with greater efficiency and minimal losses. The increasing integration of renewable energy sources like solar and wind, often located in remote areas, necessitates robust and efficient transmission networks, a domain where Gas Insulated Power Equipment excels.

Shifting consumer demands, primarily from utility companies and industrial sectors, emphasize the need for solutions that minimize environmental impact, reduce operational costs, and ensure uninterrupted power supply. The growing concern over greenhouse gas emissions has spurred research and development into alternative insulating gases to SF6 (sulfur hexafluoride), which, despite its excellent dielectric properties, has a high global warming potential. While SF6 remains the dominant insulating gas, the market is actively exploring and testing alternatives like nitrogen-based mixtures, CO2-based mixtures, and vacuum interrupter technology for certain applications, indicating a significant shift towards sustainability. The increasing complexity of power grids, with the rise of smart grid technologies and distributed energy resources, also demands more sophisticated and compact switchgear and transmission solutions, which gas-insulated equipment is well-positioned to provide. The forecast period (2025-2033) is expected to witness accelerated adoption of these advanced technologies, driven by government incentives, infrastructure development projects, and the continuous pursuit of operational excellence and environmental responsibility within the power sector. The overall industry evolution is characterized by a strong emphasis on performance, sustainability, and adaptability to the evolving energy landscape.

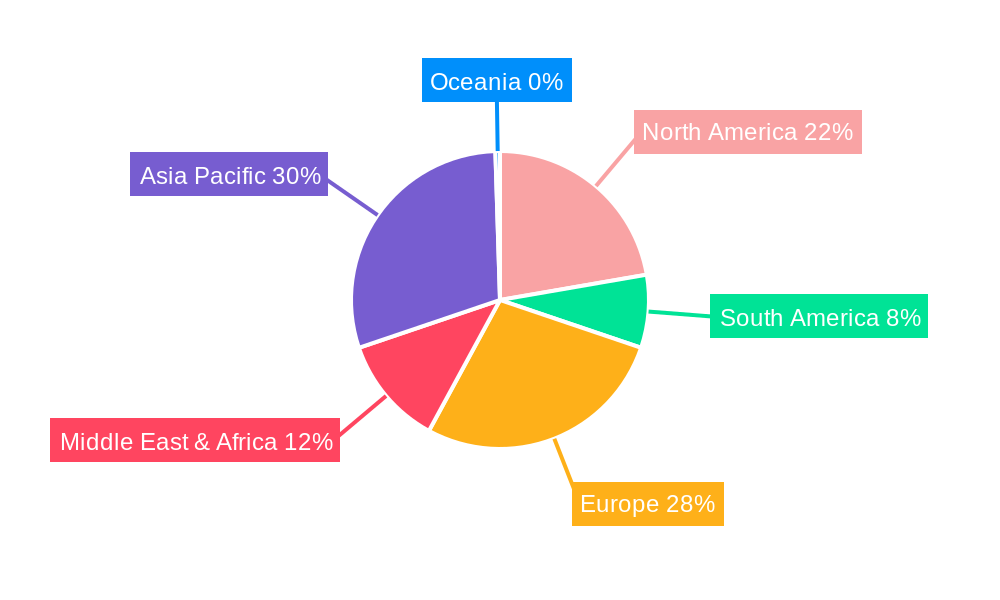

Leading Regions, Countries, or Segments in Gas Insulated Power Equipment

The global Gas Insulated Power Equipment market exhibits distinct regional dominance and segment-specific growth, driven by varying economic factors, infrastructure development needs, and regulatory frameworks. In terms of application, HVAC (High-Voltage Alternating Current) segments continue to represent the largest share of the market, largely due to existing grid infrastructure and widespread demand for AC power transmission and distribution. However, the HVDC (High-Voltage Direct Current) segment is experiencing rapid growth, fueled by long-distance power transmission projects, integration of remote renewable energy sources, and the need for efficient intercontinental grid connections. This segment is projected to witness a higher CAGR during the forecast period.

Regionally, Asia Pacific stands out as the leading market for Gas Insulated Power Equipment. This dominance is attributable to several key drivers:

- Massive Infrastructure Investment: Countries like China and India are undertaking unprecedented investments in expanding and modernizing their power grids to meet burgeoning energy demands, driven by rapid industrialization and urbanization. This includes significant deployments of Gas Insulated Switchgear (GIS) and Gas Insulated Transmission lines (GIL) in densely populated urban centers and critical industrial zones where space is at a premium.

- Renewable Energy Integration: The region is a global leader in renewable energy deployment, particularly solar and wind power. Connecting these often remote generation sites to the national grid requires efficient and high-capacity transmission solutions, a role effectively filled by gas-insulated equipment.

- Technological Advancement and Manufacturing Hubs: Asia Pacific is also a major manufacturing hub for electrical equipment, with several key players like Hyundai Electric & Energy System and Xi'an XD Switchgear Electric based in the region, contributing to competitive pricing and technological innovation.

- Government Support and Favorable Policies: Governments across the Asia Pacific region are actively promoting grid modernization and the adoption of advanced power transmission technologies through supportive policies, subsidies, and long-term development plans.

Within the "Types" of gas-insulated equipment, Switchgear holds the largest market share, comprising the majority of installations in substations worldwide. Gas Insulated Transmission lines (GIL) are also gaining traction, particularly for high-capacity urban underground transmission and cross-border connections, offering an alternative to traditional underground cables. The "Other" category, which may include specialized components or emerging technologies, is expected to see steady growth as innovation continues. The combination of high demand for AC power, increasing adoption of HVDC for specific applications, and the substantial infrastructure development in Asia Pacific positions these segments and regions at the forefront of the Gas Insulated Power Equipment market's growth trajectory.

Gas Insulated Power Equipment Product Innovations

Product innovations in Gas Insulated Power Equipment are predominantly focused on enhancing environmental sustainability, improving operational efficiency, and miniaturizing designs. A significant breakthrough involves the development of SF6-free or reduced SF6 content insulating gas mixtures, such as those incorporating nitrogen, CO2, or novel fluoronitrile-based compounds. These alternatives aim to significantly lower the Global Warming Potential (GWP) while maintaining comparable dielectric strength and arc-quenching capabilities. ABB, for instance, has pioneered SF6-free switchgear solutions, demonstrating their viability in demanding applications. Furthermore, advancements in vacuum interrupter technology integrated into gas-insulated switchgear are enhancing safety and reliability by eliminating the need for traditional arc-quenching gases in certain components. The design of more compact and modular Gas Insulated Switchgear (GIS) and Gas Insulated Transmission lines (GIL) is another critical innovation, enabling easier installation, reduced footprint for urban substations, and enhanced flexibility for grid expansion. Performance metrics are continually being optimized, with a focus on extending the operational lifespan of equipment, reducing partial discharge levels, and improving thermal management, all contributing to lower total cost of ownership for utilities and grid operators.

Propelling Factors for Gas Insulated Power Equipment Growth

The growth of the Gas Insulated Power Equipment market is propelled by a confluence of technological, economic, and regulatory factors. Technologically, the inherent advantages of gas-insulated systems—compact size, enhanced safety, and superior reliability—make them indispensable for modernizing and expanding power grids. The increasing demand for renewable energy integration necessitates efficient, high-capacity transmission solutions, a niche where gas-insulated equipment excels. Economically, rapid urbanization and industrialization, particularly in emerging economies, drive significant investment in power infrastructure, favoring space-saving and robust solutions. Regulatory mandates focused on grid reliability, reduced environmental impact, and energy efficiency also play a crucial role. For example, stringent regulations on greenhouse gas emissions are accelerating the development and adoption of SF6 alternatives, fostering innovation and market expansion.

Obstacles in the Gas Insulated Power Equipment Market

Despite robust growth prospects, the Gas Insulated Power Equipment market faces several obstacles. A primary restraint is the high initial cost of gas-insulated equipment compared to traditional air-insulated alternatives, which can be a deterrent for cost-sensitive projects. The environmental concerns surrounding SF6, a potent greenhouse gas, continue to be a challenge, driving the need for research and adoption of costly alternatives, and necessitating stringent handling and recycling protocols. Supply chain disruptions, as witnessed in recent global events, can impact the availability of critical components and raw materials, leading to project delays and increased costs. Furthermore, the specialized knowledge and training required for the installation, operation, and maintenance of gas-insulated systems can pose a barrier to entry for some utilities.

Future Opportunities in Gas Insulated Power Equipment

Emerging opportunities in the Gas Insulated Power Equipment market are substantial and diverse. The ongoing transition to a greener energy future presents a significant avenue for growth, with the development and deployment of SF6-free alternatives gaining momentum. The expanding smart grid ecosystem, requiring advanced and compact solutions for distributed energy resources and microgrids, offers new application areas. Increased investment in High-Voltage Direct Current (HVDC) transmission lines for long-distance power transfer and grid interconnections will continue to drive demand for specialized gas-insulated components. Moreover, the rehabilitation and upgrading of aging electrical infrastructure worldwide present a constant need for reliable and efficient power transmission equipment, favoring the durable and low-maintenance characteristics of gas-insulated systems.

Major Players in the Gas Insulated Power Equipment Ecosystem

- ABB

- Siemens AG

- Crompton Greaves

- Hyundai Electric & Energy System

- Xi'an XD Switchgear Electric

- Meidensha Corporation

- Schneider Electric

- Larsen & Toubro

Key Developments in Gas Insulated Power Equipment Industry

- 2024: ABB launches a new generation of SF6-free Gas Insulated Switchgear (GIS) for medium-voltage applications, significantly reducing environmental impact.

- 2023: Siemens AG secures a major contract for Gas Insulated Switchgear (GIS) for a large offshore wind farm in Europe, highlighting the growing role in renewable energy infrastructure.

- 2023: Hyundai Electric & Energy System announces significant advancements in the development of high-voltage gas-insulated transformers with improved thermal management.

- 2022: Schneider Electric expands its portfolio of gas-insulated solutions for smart grid applications, emphasizing modularity and digital integration.

- 2022: Xi'an XD Switchgear Electric completes a major project involving Gas Insulated Transmission lines (GIL) for a critical urban power corridor in China.

- 2021: Meidensha Corporation showcases innovative SF6 alternative gas mixtures for high-voltage applications, targeting a lower global warming potential.

- 2021: Larsen & Toubro secures a substantial order for Gas Insulated Switchgear (GIS) for a new substation in India, underscoring regional market strength.

- 2020: Several industry players collaborate on research initiatives to standardize testing procedures for SF6-free insulating gases.

Strategic Gas Insulated Power Equipment Market Forecast

The strategic Gas Insulated Power Equipment market forecast anticipates sustained robust growth driven by critical demand for grid modernization, renewable energy integration, and urbanization. Key growth catalysts include ongoing technological advancements in SF6 alternatives, offering environmentally conscious solutions that align with global sustainability goals. The increasing adoption of High-Voltage Direct Current (HVDC) transmission for long-distance energy transfer and the expansion of smart grid technologies will further fuel market expansion, requiring compact and highly reliable power transmission equipment. Infrastructure development initiatives across emerging economies, coupled with the global push to upgrade aging electrical networks, represent a significant and consistent demand driver. The market's potential is further amplified by the inherent advantages of gas-insulated equipment, such as its reduced footprint, enhanced safety, and extended lifespan, making it a preferred choice for critical power infrastructure investments.

Gas Insulated Power Equipment Segmentation

-

1. Application

- 1.1. HVDC(High-Voltage Direct Current)

- 1.2. HVAC(High-Voltage Alternating Current)

-

2. Types

- 2.1. Switchgear

- 2.2. Gas Insulated Transmission lines

- 2.3. Other

Gas Insulated Power Equipment Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Gas Insulated Power Equipment Regional Market Share

Geographic Coverage of Gas Insulated Power Equipment

Gas Insulated Power Equipment REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. HVDC(High-Voltage Direct Current)

- 5.1.2. HVAC(High-Voltage Alternating Current)

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Switchgear

- 5.2.2. Gas Insulated Transmission lines

- 5.2.3. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Gas Insulated Power Equipment Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. HVDC(High-Voltage Direct Current)

- 6.1.2. HVAC(High-Voltage Alternating Current)

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Switchgear

- 6.2.2. Gas Insulated Transmission lines

- 6.2.3. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Gas Insulated Power Equipment Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. HVDC(High-Voltage Direct Current)

- 7.1.2. HVAC(High-Voltage Alternating Current)

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Switchgear

- 7.2.2. Gas Insulated Transmission lines

- 7.2.3. Other

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Gas Insulated Power Equipment Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. HVDC(High-Voltage Direct Current)

- 8.1.2. HVAC(High-Voltage Alternating Current)

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Switchgear

- 8.2.2. Gas Insulated Transmission lines

- 8.2.3. Other

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Gas Insulated Power Equipment Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. HVDC(High-Voltage Direct Current)

- 9.1.2. HVAC(High-Voltage Alternating Current)

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Switchgear

- 9.2.2. Gas Insulated Transmission lines

- 9.2.3. Other

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Gas Insulated Power Equipment Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. HVDC(High-Voltage Direct Current)

- 10.1.2. HVAC(High-Voltage Alternating Current)

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Switchgear

- 10.2.2. Gas Insulated Transmission lines

- 10.2.3. Other

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Gas Insulated Power Equipment Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. HVDC(High-Voltage Direct Current)

- 11.1.2. HVAC(High-Voltage Alternating Current)

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Switchgear

- 11.2.2. Gas Insulated Transmission lines

- 11.2.3. Other

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 ABB

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Siemens AG

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Crompton Greaves

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Hyundai Electric & Energy System

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Xi'an XD Switchgear Electric

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Meidensha Corporation

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Schneider Electric

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Larsen & Toubro

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.1 ABB

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Gas Insulated Power Equipment Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Gas Insulated Power Equipment Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Gas Insulated Power Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Gas Insulated Power Equipment Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Gas Insulated Power Equipment Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Gas Insulated Power Equipment Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Gas Insulated Power Equipment Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Gas Insulated Power Equipment Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Gas Insulated Power Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Gas Insulated Power Equipment Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Gas Insulated Power Equipment Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Gas Insulated Power Equipment Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Gas Insulated Power Equipment Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Gas Insulated Power Equipment Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Gas Insulated Power Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Gas Insulated Power Equipment Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Gas Insulated Power Equipment Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Gas Insulated Power Equipment Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Gas Insulated Power Equipment Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Gas Insulated Power Equipment Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Gas Insulated Power Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Gas Insulated Power Equipment Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Gas Insulated Power Equipment Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Gas Insulated Power Equipment Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Gas Insulated Power Equipment Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Gas Insulated Power Equipment Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Gas Insulated Power Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Gas Insulated Power Equipment Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Gas Insulated Power Equipment Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Gas Insulated Power Equipment Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Gas Insulated Power Equipment Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Gas Insulated Power Equipment Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Gas Insulated Power Equipment Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Gas Insulated Power Equipment Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Gas Insulated Power Equipment Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Gas Insulated Power Equipment Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Gas Insulated Power Equipment Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Gas Insulated Power Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Gas Insulated Power Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Gas Insulated Power Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Gas Insulated Power Equipment Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Gas Insulated Power Equipment Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Gas Insulated Power Equipment Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Gas Insulated Power Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Gas Insulated Power Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Gas Insulated Power Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Gas Insulated Power Equipment Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Gas Insulated Power Equipment Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Gas Insulated Power Equipment Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Gas Insulated Power Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Gas Insulated Power Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Gas Insulated Power Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Gas Insulated Power Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Gas Insulated Power Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Gas Insulated Power Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Gas Insulated Power Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Gas Insulated Power Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Gas Insulated Power Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Gas Insulated Power Equipment Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Gas Insulated Power Equipment Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Gas Insulated Power Equipment Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Gas Insulated Power Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Gas Insulated Power Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Gas Insulated Power Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Gas Insulated Power Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Gas Insulated Power Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Gas Insulated Power Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Gas Insulated Power Equipment Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Gas Insulated Power Equipment Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Gas Insulated Power Equipment Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Gas Insulated Power Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Gas Insulated Power Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Gas Insulated Power Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Gas Insulated Power Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Gas Insulated Power Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Gas Insulated Power Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Gas Insulated Power Equipment Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Gas Insulated Power Equipment?

The projected CAGR is approximately 8%.

2. Which companies are prominent players in the Gas Insulated Power Equipment?

Key companies in the market include ABB, Siemens AG, Crompton Greaves, Hyundai Electric & Energy System, Xi'an XD Switchgear Electric, Meidensha Corporation, Schneider Electric, Larsen & Toubro.

3. What are the main segments of the Gas Insulated Power Equipment?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 29.1 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Gas Insulated Power Equipment," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Gas Insulated Power Equipment report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Gas Insulated Power Equipment?

To stay informed about further developments, trends, and reports in the Gas Insulated Power Equipment, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence