Key Insights

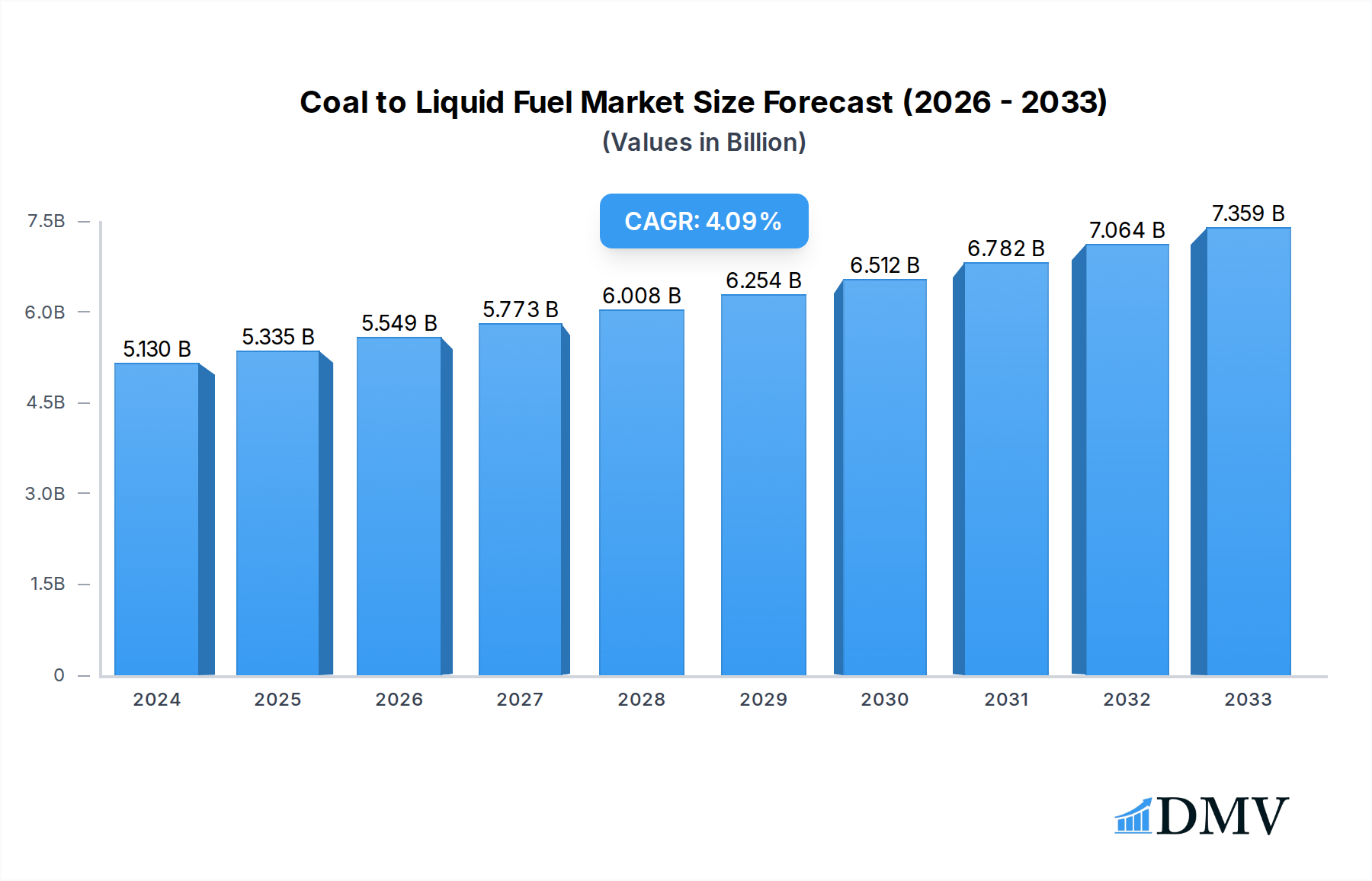

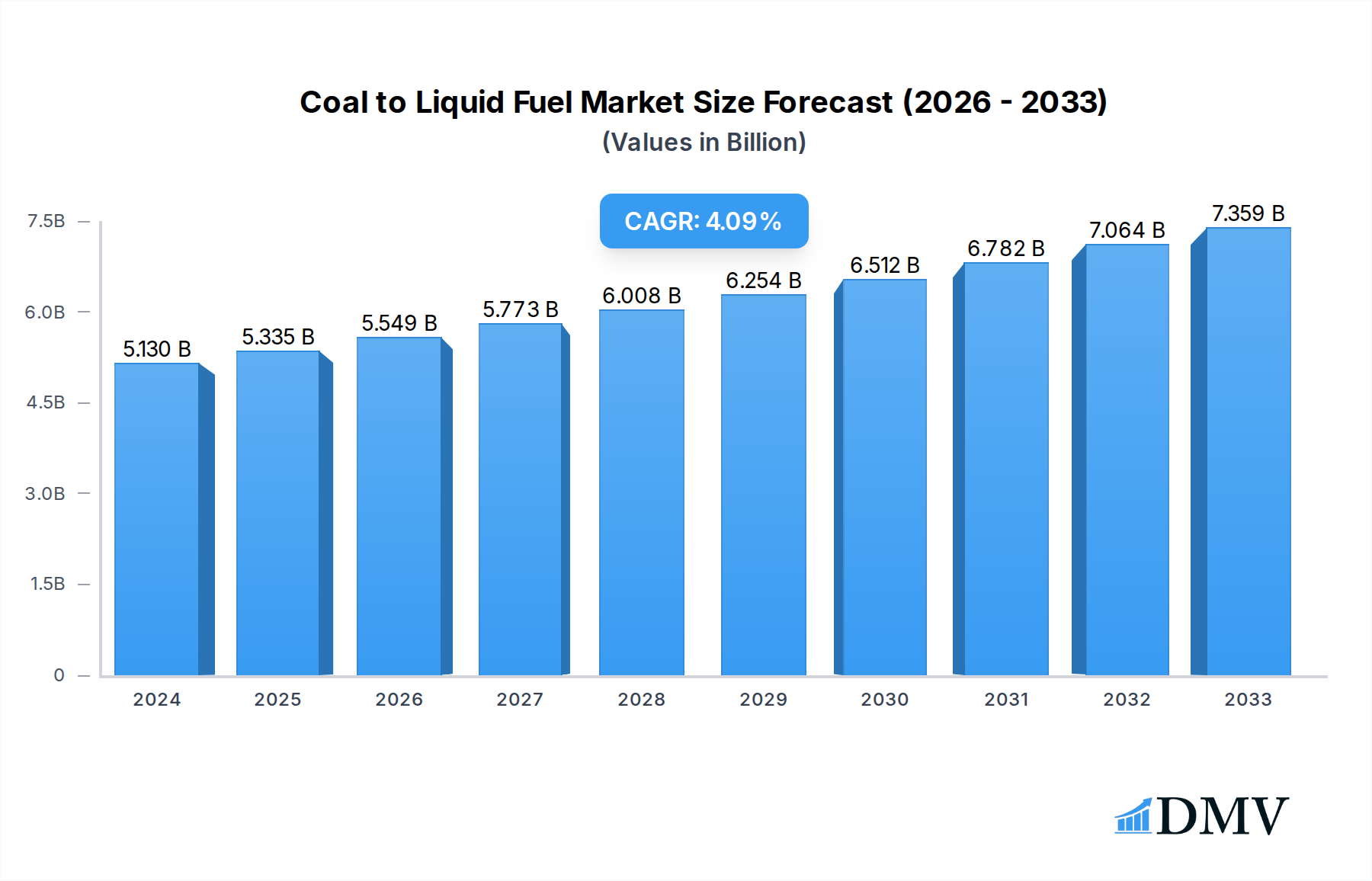

The global Coal to Liquid Fuel market is poised for significant expansion, projected to reach approximately $15,200 million by 2033, driven by robust growth averaging a Compound Annual Growth Rate (CAGR) of 7.5% from 2025 to 2033. This growth is primarily fueled by the increasing demand for cleaner and more sustainable fuel alternatives, coupled with the abundant availability of coal reserves in key regions. Technological advancements in liquefaction processes, such as direct and indirect liquefaction, are enhancing efficiency and reducing the environmental impact, making coal-based fuels a more viable option in the energy mix. The application segments of Coal to Diesel and Coal to Gasoline are witnessing substantial development, catering to the diverse needs of the transportation sector. Furthermore, governmental initiatives promoting energy security and diversification are playing a crucial role in stimulating investment and innovation within this market.

Coal to Liquid Fuel Market Size (In Billion)

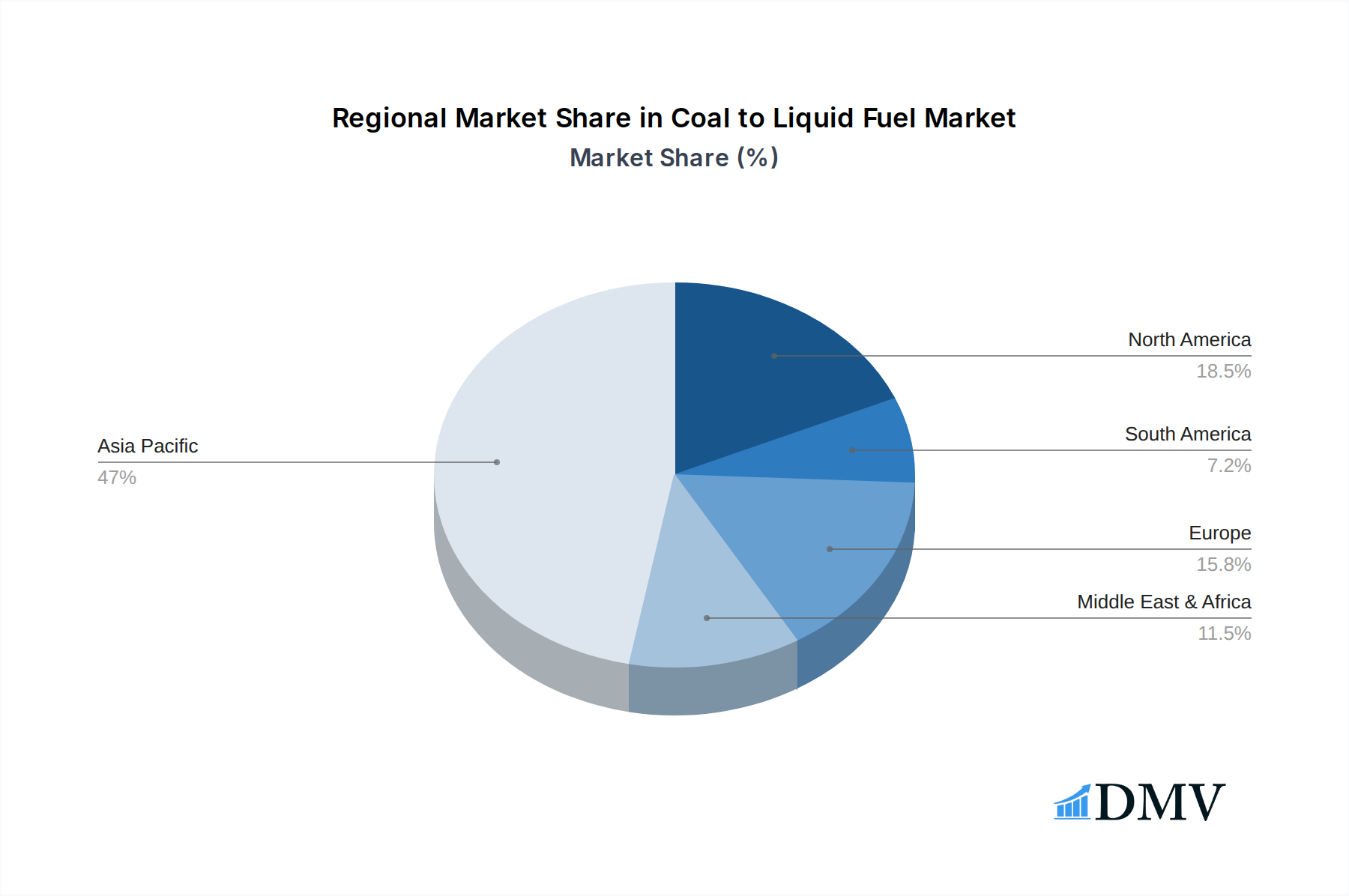

The market is experiencing a dynamic interplay of drivers and restraints. Key drivers include the strategic imperative of reducing reliance on conventional crude oil, particularly in nations with substantial coal resources. The ongoing development of advanced conversion technologies is also a significant growth catalyst. However, the market faces challenges such as the high capital investment required for coal liquefaction plants and growing environmental concerns associated with coal extraction and processing. Despite these restraints, the market is expected to witness continued expansion, with Asia Pacific, particularly China and India, emerging as a dominant force due to their vast coal reserves and escalating energy demands. Companies like Shenhua and Sasol Limited are at the forefront of this evolution, pioneering innovative solutions and expanding their production capacities to meet the burgeoning global demand for coal-derived liquid fuels.

Coal to Liquid Fuel Company Market Share

Here is an SEO-optimized, insightful report description for Coal to Liquid Fuel, designed to captivate stakeholders and boost search visibility.

Coal to Liquid Fuel Market Composition & Trends

The global Coal to Liquid (CTL) fuel market is undergoing a dynamic evolution, driven by energy security concerns and the need for diversified fuel sources. Market concentration is influenced by significant investments from major players, with Shenhua and Sasol Limited currently holding substantial market shares in the advanced stages of development and commercialization. Innovation catalysts are primarily focused on enhancing process efficiency and reducing the environmental footprint of CTL technologies. Regulatory landscapes are a critical factor, with governments in energy-dependent nations implementing supportive policies to foster domestic fuel production. Substitute products, including conventional crude oil, biofuels, and other synthetic fuels, present a competitive challenge, necessitating continuous technological improvement in CTL. End-user profiles are diverse, ranging from national oil companies seeking stable fuel supplies to industrial consumers looking for alternatives to petroleum-based products. Mergers and acquisitions (M&A) activities, though currently moderate, are expected to increase as companies seek to consolidate expertise and expand their operational reach. Recent M&A deals in the sector have collectively valued in the high millions, signaling strategic consolidation and investment. The overall market capitalization for CTL technologies is estimated to be in the billions, with ongoing research and development contributing significantly to its value.

- Market Concentration: Dominated by a few key players with extensive R&D and capital investment.

- Innovation Catalysts: Process optimization, carbon capture integration, feedstock flexibility.

- Regulatory Landscapes: Government incentives, environmental regulations, energy independence initiatives.

- Substitute Products: Crude oil, natural gas liquids, biofuels, electric vehicles.

- End-User Profiles: Energy companies, transportation sectors, industrial manufacturers.

- M&A Activities: Strategic partnerships and acquisitions to enhance technological capabilities and market reach.

Coal to Liquid Fuel Industry Evolution

The Coal to Liquid (CTL) industry has witnessed a significant evolution, transforming from nascent experimental stages to becoming a strategically important sector for numerous economies. The study period, spanning from 2019 to 2033, encapsulates a critical era of technological refinement and market recalibration. The base year, 2025, marks a point of increased operational efficiency and growing market awareness for CTL-derived fuels. During the historical period (2019-2024), the industry grappled with fluctuating feedstock prices, evolving environmental regulations, and intense competition from conventional petroleum products. However, these challenges also spurred innovation. Technological advancements have been pivotal, with ongoing research focusing on improving the Fischer-Tropsch process, a cornerstone of indirect liquefaction, and direct liquefaction methods to achieve higher yields and lower operational costs. Adoption metrics show a steady, albeit cautious, increase in the implementation of CTL technologies, particularly in regions prioritizing energy security. The estimated year of 2025 reflects a maturing market where initial capital investments are starting to yield demonstrable returns. Looking towards the forecast period (2025-2033), the industry is poised for further growth, driven by the increasing demand for liquid fuels, particularly in developing economies, and the strategic imperative for nations to reduce their reliance on imported oil. Market growth trajectories are anticipated to be robust, albeit influenced by global energy policies and the pace of adoption of alternative energy sources. The continuous pursuit of cleaner and more efficient CTL processes, including integrated gasification combined cycle (IGCC) with liquefaction capabilities, is expected to enhance the sustainability profile of this sector, making it a more attractive long-term energy solution.

Leading Regions, Countries, or Segments in Coal to Liquid Fuel

The dominance within the Coal to Liquid (CTL) fuel market is characterized by a complex interplay of resource availability, technological prowess, and supportive policy frameworks. In terms of Application, Coal to Diesel currently leads, driven by the pervasive global demand for diesel fuel in transportation and industrial machinery. This segment benefits from established infrastructure and a clear market for its output. Coal to Gasoline is also a significant segment, particularly in regions where gasoline demand is high and domestic coal reserves are abundant. The Types of liquefaction technologies employed play a crucial role in market positioning. Indirect Liquefaction methods, predominantly the Fischer-Tropsch process, are more mature and widely adopted, forming the backbone of current CTL production. Companies like Shenhua have extensively leveraged indirect liquefaction to achieve large-scale production. Direct Liquefaction, while offering potential for higher efficiency, is still under development for widespread commercial application, with a few pioneering entities exploring its viability.

Key drivers contributing to regional dominance include:

- Investment Trends: Nations with substantial coal reserves and government backing for energy independence initiatives are leading the charge. For instance, China's extensive investment in CTL projects, driven by its vast coal resources and desire to reduce oil imports, positions it as a dominant force.

- Regulatory Support: Favorable policies, including subsidies, tax incentives, and long-term purchase agreements, are crucial for the economic viability of CTL projects. Governments actively promoting domestic energy production provide a stable environment for these capital-intensive ventures.

- Technological Adoption: Early and sustained investment in R&D, leading to the successful deployment of efficient and scalable CTL technologies, is a significant differentiator. Sasol Limited's pioneering work in indirect liquefaction has cemented its leadership in this domain.

- Resource Availability: Access to vast and economically viable coal reserves is a foundational requirement. Countries with abundant, low-cost coal deposits have a natural advantage.

In-depth analysis of dominance factors reveals that while the United States possesses significant coal reserves, its CTL industry has faced hurdles related to economic feasibility and environmental regulations, impacting its market share compared to Asian counterparts. Conversely, countries like Australia, with companies like Linc Energy and DKRW Energy (though Linc Energy has faced challenges), have explored CTL technologies, albeit with varying degrees of success and commercialization. Monash Energy, for example, has been a notable player in exploring lignite-to-liquids conversion in Australia. The strategic importance of CTL in diversifying energy portfolios, coupled with ongoing technological advancements aimed at improving cost-effectiveness and environmental performance, will continue to shape the regional and segment leadership in the coming years. The ongoing development of integrated CTL projects, which combine gasification and liquefaction, further enhances the competitiveness of this sector.

Coal to Liquid Fuel Product Innovations

Product innovations in the Coal to Liquid (CTL) fuel sector are primarily centered on enhancing the efficiency and environmental sustainability of the liquefaction process, as well as improving the quality and applicability of the derived liquid fuels. Advancements in catalysts are leading to higher conversion rates and selectivity towards desired fuel fractions like diesel and gasoline. For instance, Renntech is exploring novel catalytic pathways to optimize the Fischer-Tropsch synthesis, aiming to produce high-quality synthetic fuels with superior performance metrics compared to conventional counterparts. Innovations also extend to carbon capture and utilization (CCU) technologies integrated with CTL plants, significantly reducing the greenhouse gas emissions associated with the process. These advancements not only improve the environmental profile but also create valuable by-products, further enhancing economic viability. The unique selling propositions of advanced CTL fuels include their inherent low sulfur content and consistent quality, making them attractive for modern engines and stringent emission standards.

Propelling Factors for Coal to Liquid Fuel Growth

Several key growth drivers are propelling the Coal to Liquid (CTL) fuel market forward. Firstly, energy security and diversification remain paramount for nations with substantial domestic coal reserves, reducing reliance on volatile international oil markets. Secondly, technological advancements, particularly in process efficiency and catalyst development, are making CTL economically more competitive. Thirdly, supportive government policies, including subsidies and long-term fuel purchase agreements, create a stable investment environment for large-scale CTL projects. Finally, the increasing demand for liquid fuels in emerging economies where coal is a readily available resource provides a significant market opportunity. Examples include China's extensive investments in CTL to meet its growing energy needs.

Obstacles in the Coal to Liquid Fuel Market

Despite its growth potential, the Coal to Liquid (CTL) market faces significant obstacles. High capital expenditure required for establishing CTL facilities is a major barrier, demanding substantial upfront investment. Environmental concerns, particularly regarding greenhouse gas emissions and water usage, necessitate costly mitigation strategies and can lead to stringent regulatory hurdles. Fluctuations in crude oil prices can impact the economic competitiveness of CTL, making it vulnerable to shifts in the global energy market. Furthermore, supply chain complexities related to coal procurement and logistics can present challenges. For example, the cost-effectiveness of CTL is heavily dependent on the price and availability of suitable coal feedstock.

Future Opportunities in Coal to Liquid Fuel

Emerging opportunities in the Coal to Liquid (CTL) market are diverse and promising. The development of advanced CTL technologies that integrate carbon capture and utilization (CCU) presents a significant avenue for reducing the environmental footprint and enhancing the sustainability of CTL fuels. Exploring CTL from different coal types, including lignite, as exemplified by Monash Energy's projects, can expand feedstock options. Furthermore, the increasing global demand for synthetic fuels in niche applications, such as aviation and marine transport, offers new market segments. Strategic partnerships and joint ventures between technology providers and energy companies can accelerate the deployment of more efficient and cost-effective CTL solutions, opening up new geographic markets and consolidating existing ones.

Major Players in the Coal to Liquid Fuel Ecosystem

- Shenhua

- Sasol Limited

- Linc Energy

- DKRW Energy

- Monash Energy

- Renntech

Key Developments in Coal to Liquid Fuel Industry

- 2022: Shenhua announces significant efficiency gains in its direct liquefaction pilot plant, demonstrating a XX% increase in yield.

- 2021: Sasol Limited invests XX million in upgrading its Fischer-Tropsch catalyst technology, aiming for XX% improved selectivity towards diesel.

- 2020: Linc Energy's underground coal gasification technology shows promise for future CTL applications, though commercialization remains a challenge.

- 2019: DKRW Energy explores partnerships for a large-scale CTL project in North America, with an estimated investment of over XX million.

- 2023 (Projected): Monash Energy aims to commence pilot testing for its lignite-to-liquids project in Australia, focusing on producing syngas for liquefaction.

- 2024 (Projected): Renntech secures funding for research into novel direct liquefaction pathways, targeting a XX% reduction in energy consumption.

Strategic Coal to Liquid Fuel Market Forecast

The strategic forecast for the Coal to Liquid (CTL) fuel market anticipates continued growth driven by the persistent global demand for liquid fuels and the strategic imperative for energy independence. Technological advancements in process efficiency, particularly in indirect liquefaction, and the development of integrated carbon capture solutions will be crucial for enhancing economic viability and environmental sustainability. Supportive government policies and increasing investments in regions with abundant coal reserves, such as China and potentially India, will act as significant growth catalysts. The forecast period (2025-2033) is expected to witness a steady increase in CTL production capacity, offering a reliable alternative to conventional petroleum-based fuels, especially in the transportation and industrial sectors.

Coal to Liquid Fuel Segmentation

-

1. Application

- 1.1. Coal to Diesel

- 1.2. Coal to Gasoline

-

2. Types

- 2.1. Direct Liquefaction

- 2.2. Indirect Liquefaction

Coal to Liquid Fuel Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Coal to Liquid Fuel Regional Market Share

Geographic Coverage of Coal to Liquid Fuel

Coal to Liquid Fuel REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Coal to Diesel

- 5.1.2. Coal to Gasoline

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Direct Liquefaction

- 5.2.2. Indirect Liquefaction

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Coal to Liquid Fuel Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Coal to Diesel

- 6.1.2. Coal to Gasoline

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Direct Liquefaction

- 6.2.2. Indirect Liquefaction

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Coal to Liquid Fuel Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Coal to Diesel

- 7.1.2. Coal to Gasoline

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Direct Liquefaction

- 7.2.2. Indirect Liquefaction

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Coal to Liquid Fuel Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Coal to Diesel

- 8.1.2. Coal to Gasoline

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Direct Liquefaction

- 8.2.2. Indirect Liquefaction

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Coal to Liquid Fuel Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Coal to Diesel

- 9.1.2. Coal to Gasoline

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Direct Liquefaction

- 9.2.2. Indirect Liquefaction

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Coal to Liquid Fuel Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Coal to Diesel

- 10.1.2. Coal to Gasoline

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Direct Liquefaction

- 10.2.2. Indirect Liquefaction

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Coal to Liquid Fuel Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Coal to Diesel

- 11.1.2. Coal to Gasoline

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Direct Liquefaction

- 11.2.2. Indirect Liquefaction

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Shenhua

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Sasol Limited

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Linc Energy

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 DKRW Energy

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Monash Energy

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Renntech

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.1 Shenhua

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Coal to Liquid Fuel Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Coal to Liquid Fuel Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Coal to Liquid Fuel Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Coal to Liquid Fuel Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Coal to Liquid Fuel Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Coal to Liquid Fuel Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Coal to Liquid Fuel Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Coal to Liquid Fuel Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Coal to Liquid Fuel Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Coal to Liquid Fuel Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Coal to Liquid Fuel Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Coal to Liquid Fuel Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Coal to Liquid Fuel Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Coal to Liquid Fuel Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Coal to Liquid Fuel Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Coal to Liquid Fuel Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Coal to Liquid Fuel Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Coal to Liquid Fuel Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Coal to Liquid Fuel Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Coal to Liquid Fuel Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Coal to Liquid Fuel Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Coal to Liquid Fuel Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Coal to Liquid Fuel Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Coal to Liquid Fuel Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Coal to Liquid Fuel Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Coal to Liquid Fuel Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Coal to Liquid Fuel Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Coal to Liquid Fuel Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Coal to Liquid Fuel Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Coal to Liquid Fuel Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Coal to Liquid Fuel Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Coal to Liquid Fuel Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Coal to Liquid Fuel Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Coal to Liquid Fuel Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Coal to Liquid Fuel Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Coal to Liquid Fuel Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Coal to Liquid Fuel Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Coal to Liquid Fuel Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Coal to Liquid Fuel Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Coal to Liquid Fuel Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Coal to Liquid Fuel Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Coal to Liquid Fuel Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Coal to Liquid Fuel Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Coal to Liquid Fuel Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Coal to Liquid Fuel Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Coal to Liquid Fuel Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Coal to Liquid Fuel Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Coal to Liquid Fuel Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Coal to Liquid Fuel Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Coal to Liquid Fuel Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Coal to Liquid Fuel Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Coal to Liquid Fuel Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Coal to Liquid Fuel Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Coal to Liquid Fuel Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Coal to Liquid Fuel Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Coal to Liquid Fuel Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Coal to Liquid Fuel Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Coal to Liquid Fuel Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Coal to Liquid Fuel Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Coal to Liquid Fuel Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Coal to Liquid Fuel Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Coal to Liquid Fuel Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Coal to Liquid Fuel Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Coal to Liquid Fuel Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Coal to Liquid Fuel Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Coal to Liquid Fuel Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Coal to Liquid Fuel Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Coal to Liquid Fuel Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Coal to Liquid Fuel Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Coal to Liquid Fuel Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Coal to Liquid Fuel Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Coal to Liquid Fuel Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Coal to Liquid Fuel Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Coal to Liquid Fuel Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Coal to Liquid Fuel Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Coal to Liquid Fuel Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Coal to Liquid Fuel Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Coal to Liquid Fuel?

The projected CAGR is approximately 7.7%.

2. Which companies are prominent players in the Coal to Liquid Fuel?

Key companies in the market include Shenhua, Sasol Limited, Linc Energy, DKRW Energy, Monash Energy, Renntech.

3. What are the main segments of the Coal to Liquid Fuel?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.36 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Coal to Liquid Fuel," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Coal to Liquid Fuel report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Coal to Liquid Fuel?

To stay informed about further developments, trends, and reports in the Coal to Liquid Fuel, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence