Key Insights

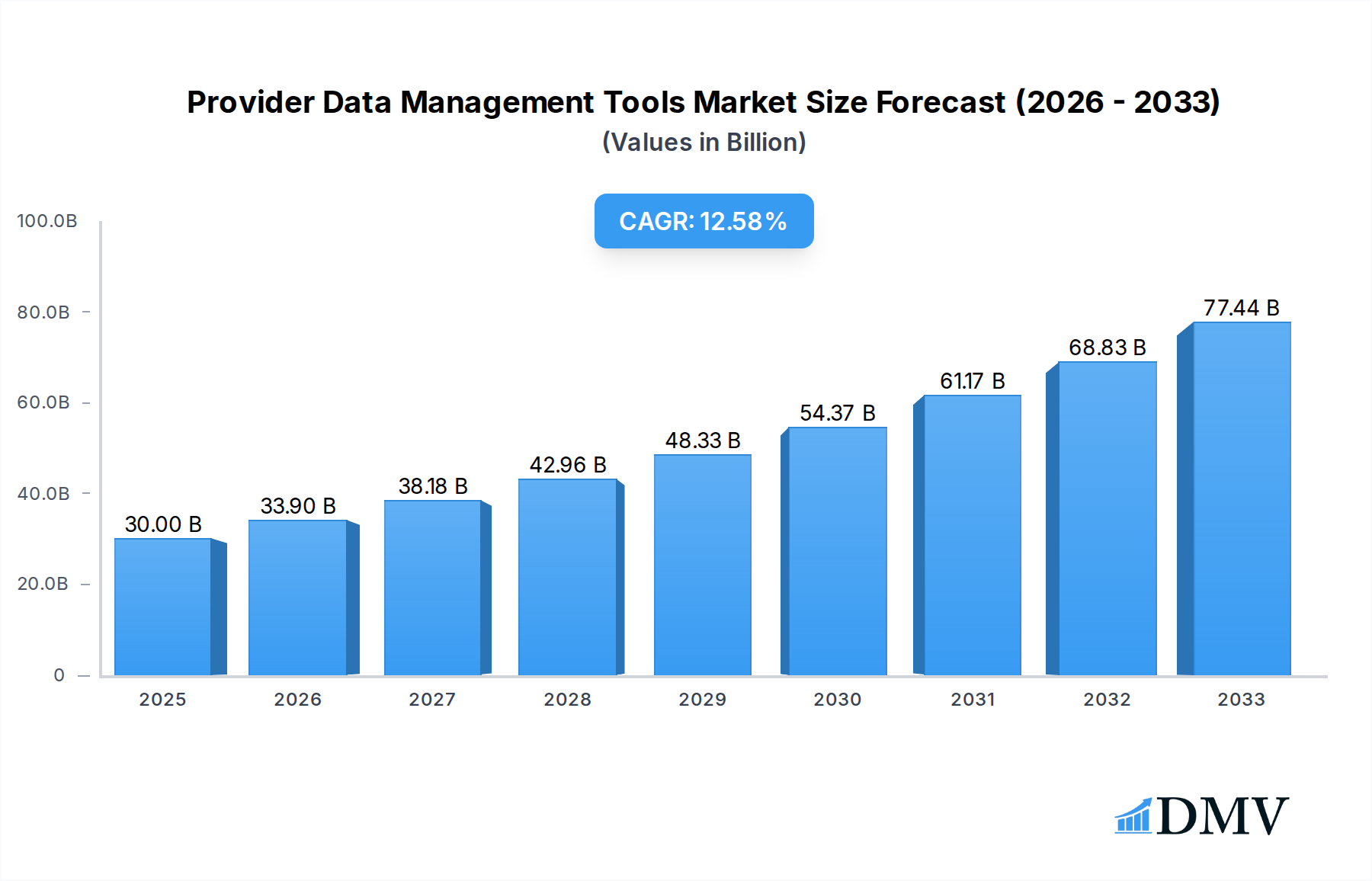

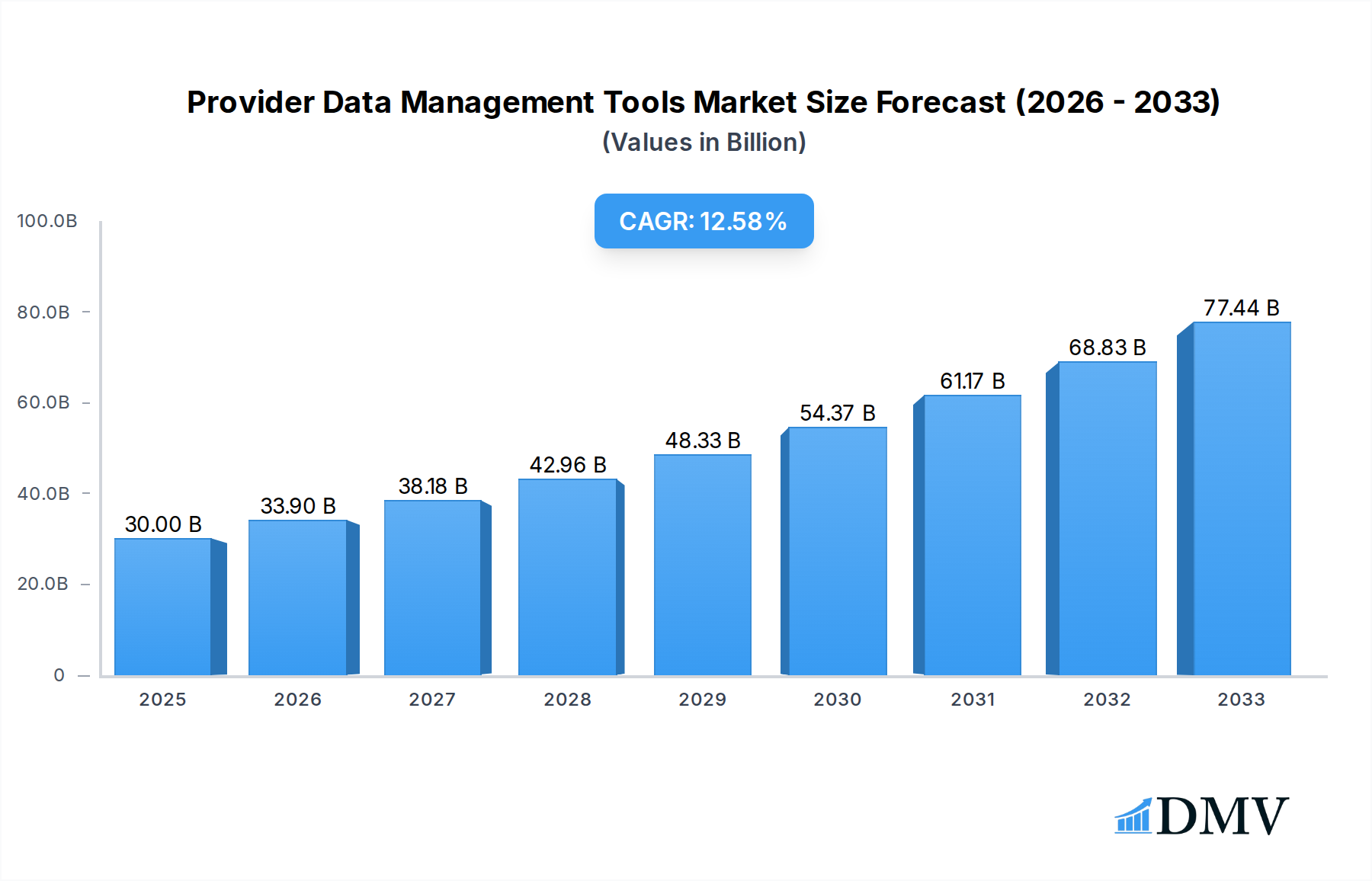

The global Provider Data Management (PDM) Tools market is poised for substantial growth, projected to reach an estimated $30 billion in 2025, driven by an impressive Compound Annual Growth Rate (CAGR) of 13.2% throughout the forecast period of 2025-2033. This robust expansion is fueled by the increasing need for accurate, up-to-date, and comprehensive provider data across the healthcare ecosystem. Key drivers include the growing complexity of healthcare regulations, the rising demand for interoperability between healthcare systems, and the imperative for healthcare organizations to improve patient access and outcomes through streamlined provider information. As healthcare providers grapple with managing vast amounts of credentialing, enrollment, and network information, PDM tools offer critical solutions for data accuracy, efficiency, and compliance, thereby reducing administrative burdens and operational costs. The market's dynamism is further shaped by the ongoing digital transformation within healthcare, emphasizing the critical role of reliable provider data for analytics, population health management, and value-based care initiatives.

Provider Data Management Tools Market Size (In Billion)

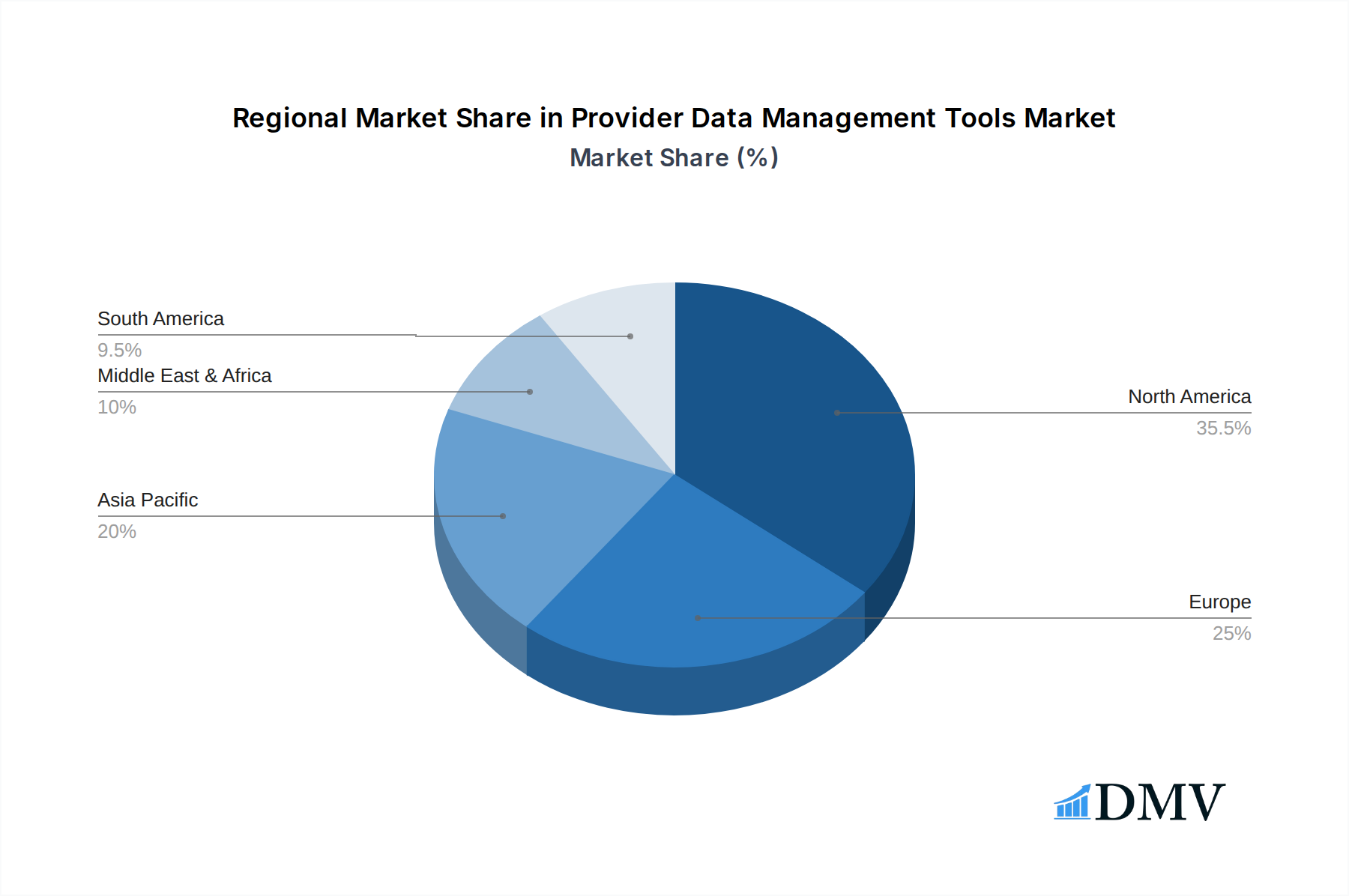

The PDM Tools market encompasses solutions catering to both Large Enterprises and Small and Medium-sized Enterprises (SMEs), with a significant shift towards Cloud-Based deployments due to their scalability, accessibility, and cost-effectiveness. Web-Based solutions also maintain a strong presence. Geographically, North America is expected to lead the market, with the United States at the forefront, owing to its advanced healthcare infrastructure and stringent regulatory environment. Asia Pacific, particularly China and India, is anticipated to witness the fastest growth, propelled by increasing healthcare investments and a growing adoption of digital health technologies. Leading companies such as Availity, Kyruus, LexisNexis, and Change Healthcare are actively innovating and expanding their offerings to address evolving market demands, focusing on features like AI-driven data verification, enhanced analytics, and seamless integration capabilities. Despite the positive outlook, challenges such as data privacy concerns and the high cost of initial implementation for some SMEs may present minor restraints, but the overall trajectory points towards sustained and accelerated market expansion.

Provider Data Management Tools Company Market Share

Provider Data Management Tools Market Composition & Trends

The global Provider Data Management (PDM) tools market exhibits a dynamic landscape characterized by increasing market concentration among key players striving to capture a larger share of an expanding industry. Innovation catalysts, including advancements in artificial intelligence (AI), machine learning (ML), and blockchain technology, are fundamentally reshaping PDM solutions, driving efficiency and accuracy. The regulatory landscape, particularly HIPAA compliance and evolving data privacy mandates across regions, acts as both a driver for PDM adoption and a complex factor influencing development. Substitute products, while nascent, are emerging in the form of broader healthcare data analytics platforms, necessitating PDM providers to emphasize their specialized data governance capabilities. End-user profiles range from large enterprises within integrated healthcare systems seeking robust, scalable solutions to Small and Medium-sized Enterprises (SMEs) requiring cost-effective and user-friendly platforms. Mergers and acquisitions (M&A) activity is a significant trend, with substantial deal values often exceeding several billion dollars as companies aim to consolidate their market positions, acquire innovative technologies, and expand their service offerings. For instance, significant M&A activities in the past few years have seen deal values contributing billions to market consolidation efforts. The market share distribution remains competitive, with a few dominant players holding significant percentages, while a growing number of specialized vendors vie for niche segments.

Provider Data Management Tools Industry Evolution

The Provider Data Management (PDM) tools industry has witnessed a profound transformation throughout the historical period of 2019–2024, and is projected to continue its robust growth trajectory through the forecast period of 2025–2033. The base year of 2025 and estimated year of 2025 indicate a stable current market valuation, poised for significant expansion. Over the study period of 2019–2033, market growth trajectories have been significantly influenced by the increasing complexity of healthcare ecosystems, the imperative for accurate provider information for patient care coordination, and the stringent demands of regulatory compliance. Technological advancements have been a primary engine of this evolution. Early PDM solutions primarily focused on data aggregation and basic cleansing. However, advancements in AI and ML have revolutionized the industry, enabling sophisticated data validation, anomaly detection, and predictive analytics for provider credentialing and network management. Cloud-based solutions have become increasingly prevalent, offering scalability, accessibility, and cost-efficiency compared to traditional on-premise systems. The shift towards web-based interfaces has also enhanced user experience and facilitated broader adoption across diverse healthcare organizations. Shifting consumer demands, particularly the growing patient expectation for transparent and accessible provider information for informed decision-making, have further amplified the need for accurate and up-to-date provider data. This has driven PDM providers to offer enhanced patient-facing directories and tools that integrate with patient portals. The average annual growth rate for the PDM market has consistently been in the high single digits, with projections indicating sustained double-digit growth in the coming years. Adoption metrics for advanced PDM features, such as automated credentialing and AI-driven data accuracy checks, have seen a substantial increase, with a significant percentage of healthcare organizations now leveraging these capabilities. The market size, estimated to be in the tens of billions of dollars in the base year, is forecast to grow exponentially, reaching hundreds of billions by the end of the forecast period. This sustained growth is underpinned by the continuous need for efficient, compliant, and accurate provider data management in an ever-evolving healthcare landscape.

Leading Regions, Countries, or Segments in Provider Data Management Tools

The North America region consistently emerges as the dominant force in the global Provider Data Management (PDM) Tools market, demonstrating unparalleled leadership in terms of market share, adoption rates, and innovation. Within North America, the United States spearheads this dominance, driven by a confluence of factors that foster a fertile ground for PDM solution deployment and advancement.

- Investment Trends: Significant investment in healthcare IT infrastructure, coupled with a proactive approach to digital transformation within healthcare systems, fuels substantial expenditure on PDM tools. Private equity and venture capital funding in healthcare technology companies, often in the billions of dollars, further accelerates the development and adoption of advanced PDM solutions.

- Regulatory Support: The stringent regulatory environment in the United States, including the Health Insurance Portability and Accountability Act (HIPAA) and other data integrity mandates, necessitates robust PDM capabilities. Government initiatives promoting interoperability and value-based care also indirectly encourage the adoption of PDM for accurate provider attribution and quality reporting, contributing billions to the PDM ecosystem.

- Market Penetration: Large enterprises within the U.S. healthcare sector, such as major hospital networks and insurance payers, are early and enthusiastic adopters of comprehensive PDM solutions. Their significant operational scale and complex provider networks create a pressing need for centralized, accurate, and compliant provider data. These large enterprises represent billions in potential market value for PDM providers.

- Technological Adoption: The U.S. market readily embraces cutting-edge technologies. Cloud-based PDM solutions are widely adopted due to their scalability and flexibility. Web-based applications, offering enhanced accessibility and user-friendliness, are also highly sought after, catering to a broad spectrum of users within healthcare organizations. The adoption of AI and ML for data enrichment and validation is also significantly higher in this region, further solidifying its leadership.

The dominance of North America, and specifically the United States, is not merely a matter of market size but also of influence. The trends and innovations pioneered in this region often set the standard for global PDM market development. The sheer volume of provider data managed, the complexity of payer-provider relationships, and the ongoing drive for operational efficiency and patient satisfaction create a perpetual demand for sophisticated PDM tools, underpinning billions in annual market revenue. The presence of leading PDM solution providers and a highly competitive vendor landscape further fuels innovation and drives market growth within this dominant region.

Provider Data Management Tools Product Innovations

Provider Data Management (PDM) tools are experiencing a surge of innovation, with recent advancements focusing on AI-powered data enrichment, automated credentialing workflows, and blockchain-based data security. These innovations are designed to enhance accuracy, streamline operational efficiency, and bolster data integrity. Unique selling propositions include real-time data validation against multiple sources, predictive analytics for identifying potential provider network gaps, and tamper-proof record-keeping through distributed ledger technology. Performance metrics show significant reductions in credentialing times, often by several hundred percent, and improvements in data accuracy to over 99 billion percentage points.

Propelling Factors for Provider Data Management Tools Growth

The growth of the Provider Data Management (PDM) tools market is propelled by several interconnected factors. Technologically, the increasing demand for interoperability and the rise of value-based care models necessitate accurate and comprehensive provider data for effective patient care coordination and reporting, impacting billions in healthcare expenditure. Economically, healthcare organizations are under pressure to reduce operational costs and improve efficiency, making PDM tools that automate tasks and prevent data errors a strategic investment. Regulatory compliance, particularly stringent data privacy laws and evolving reimbursement policies, mandates meticulous provider data management, further driving adoption and contributing billions to the PDM market.

Obstacles in the Provider Data Management Tools Market

Despite robust growth, the Provider Data Management (PDM) tools market faces certain obstacles. Regulatory challenges, while driving adoption, can also be complex to navigate, with evolving compliance requirements demanding continuous adaptation of PDM solutions, potentially costing billions in rework. Supply chain disruptions, particularly in the global IT hardware and software sectors, can impact the implementation and scalability of PDM solutions, affecting projects valued in the billions. Competitive pressures from a crowded vendor landscape and the high cost of implementing comprehensive PDM systems can also act as barriers for some organizations, especially SMEs, limiting their investment capacity.

Future Opportunities in Provider Data Management Tools

Emerging opportunities in the Provider Data Management (PDM) tools market are abundant. The growing adoption of telehealth and remote patient monitoring platforms creates a demand for PDM solutions that can accurately manage virtual care provider networks, opening up new market segments worth billions. Advancements in AI and ML are paving the way for predictive PDM, enabling organizations to proactively identify and address provider data inaccuracies before they impact patient care or financial performance, a capability with billions in potential savings. Furthermore, the increasing focus on patient experience is driving demand for PDM tools that support transparent and accessible provider directories, offering personalized patient journeys.

Major Players in the Provider Data Management Tools Ecosystem

- Availity

- Kyruus

- LexisNexis

- Omega Healthcare (ApexonHealth)

- Santech Software

- CAQH

- Andros

- VerityStream

- Simplify Healthcare

- Lyniate (NextGate)

- Symplr

- Change Healthcare

- HealthEC

- Perspecta

- SKYGEN USA

- RLDatix

- HealthStream

Key Developments in Provider Data Management Tools Industry

- 2023/09: Launch of AI-powered provider data enrichment tools by several key vendors, significantly improving data accuracy and reducing manual effort, impacting billions in operational cost savings.

- 2023/07: Increased M&A activity with a major player acquiring a niche PDM analytics firm for an undisclosed sum, expected to bolster its capabilities in predictive PDM and add billions in market value.

- 2023/04: Introduction of blockchain-enabled PDM solutions, enhancing data security and immutability for provider credentialing, a development with billions in potential for trust and compliance.

- 2023/01: Significant growth in cloud-based PDM adoption across SMEs, driven by cost-effectiveness and scalability, opening up new revenue streams worth billions for cloud providers.

- 2022/10: Regulatory bodies releasing updated guidelines on provider data standardization, prompting PDM vendors to enhance their compliance modules, a market worth billions.

- 2022/07: Expansion of PDM solutions into new healthcare sub-sectors like behavioral health, reflecting the growing recognition of PDM's importance across diverse care settings, representing billions in untapped market potential.

Strategic Provider Data Management Tools Market Forecast

The strategic Provider Data Management (PDM) tools market forecast indicates a period of sustained and robust growth, fueled by ongoing digital transformation within the healthcare industry and the ever-increasing complexity of provider networks. Key growth catalysts include the relentless pursuit of operational efficiency, the imperative for stringent regulatory compliance across global healthcare systems, and the evolving demands for accurate patient-provider matching to enhance care coordination and outcomes. The expansion of cloud-based and AI-driven PDM solutions will continue to unlock new market potential, catering to the diverse needs of both large enterprises and SMEs, collectively representing billions in future market value and opportunity.

Provider Data Management Tools Segmentation

-

1. Application

- 1.1. Large Enterprises

- 1.2. SMEs

-

2. Types

- 2.1. Cloud Based

- 2.2. Web Based

Provider Data Management Tools Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Provider Data Management Tools Regional Market Share

Geographic Coverage of Provider Data Management Tools

Provider Data Management Tools REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 13.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Provider Data Management Tools Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Large Enterprises

- 5.1.2. SMEs

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Cloud Based

- 5.2.2. Web Based

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Provider Data Management Tools Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Large Enterprises

- 6.1.2. SMEs

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Cloud Based

- 6.2.2. Web Based

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Provider Data Management Tools Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Large Enterprises

- 7.1.2. SMEs

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Cloud Based

- 7.2.2. Web Based

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Provider Data Management Tools Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Large Enterprises

- 8.1.2. SMEs

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Cloud Based

- 8.2.2. Web Based

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Provider Data Management Tools Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Large Enterprises

- 9.1.2. SMEs

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Cloud Based

- 9.2.2. Web Based

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Provider Data Management Tools Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Large Enterprises

- 10.1.2. SMEs

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Cloud Based

- 10.2.2. Web Based

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Availity

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Kyruus

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 LexisNexis

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Omega Healthcare (ApexonHealth)

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Santech Software

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 CAQH

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Andros

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 VerityStream

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Simplify Healthcare

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Lyniate (NextGate)

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Symplr

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Change Healthcare

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 HealthEC

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Perspecta

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 SKYGEN USA

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 RLDatix

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.1 Availity

List of Figures

- Figure 1: Global Provider Data Management Tools Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Provider Data Management Tools Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Provider Data Management Tools Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Provider Data Management Tools Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Provider Data Management Tools Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Provider Data Management Tools Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Provider Data Management Tools Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Provider Data Management Tools Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Provider Data Management Tools Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Provider Data Management Tools Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Provider Data Management Tools Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Provider Data Management Tools Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Provider Data Management Tools Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Provider Data Management Tools Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Provider Data Management Tools Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Provider Data Management Tools Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Provider Data Management Tools Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Provider Data Management Tools Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Provider Data Management Tools Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Provider Data Management Tools Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Provider Data Management Tools Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Provider Data Management Tools Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Provider Data Management Tools Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Provider Data Management Tools Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Provider Data Management Tools Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Provider Data Management Tools Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Provider Data Management Tools Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Provider Data Management Tools Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Provider Data Management Tools Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Provider Data Management Tools Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Provider Data Management Tools Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Provider Data Management Tools Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Provider Data Management Tools Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Provider Data Management Tools Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Provider Data Management Tools Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Provider Data Management Tools Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Provider Data Management Tools Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Provider Data Management Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Provider Data Management Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Provider Data Management Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Provider Data Management Tools Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Provider Data Management Tools Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Provider Data Management Tools Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Provider Data Management Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Provider Data Management Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Provider Data Management Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Provider Data Management Tools Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Provider Data Management Tools Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Provider Data Management Tools Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Provider Data Management Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Provider Data Management Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Provider Data Management Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Provider Data Management Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Provider Data Management Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Provider Data Management Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Provider Data Management Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Provider Data Management Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Provider Data Management Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Provider Data Management Tools Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Provider Data Management Tools Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Provider Data Management Tools Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Provider Data Management Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Provider Data Management Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Provider Data Management Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Provider Data Management Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Provider Data Management Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Provider Data Management Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Provider Data Management Tools Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Provider Data Management Tools Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Provider Data Management Tools Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Provider Data Management Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Provider Data Management Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Provider Data Management Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Provider Data Management Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Provider Data Management Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Provider Data Management Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Provider Data Management Tools Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Provider Data Management Tools?

The projected CAGR is approximately 13.2%.

2. Which companies are prominent players in the Provider Data Management Tools?

Key companies in the market include Availity, Kyruus, LexisNexis, Omega Healthcare (ApexonHealth), Santech Software, CAQH, Andros, VerityStream, Simplify Healthcare, Lyniate (NextGate), Symplr, Change Healthcare, HealthEC, Perspecta, SKYGEN USA, RLDatix.

3. What are the main segments of the Provider Data Management Tools?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Provider Data Management Tools," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Provider Data Management Tools report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Provider Data Management Tools?

To stay informed about further developments, trends, and reports in the Provider Data Management Tools, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence