Key Insights

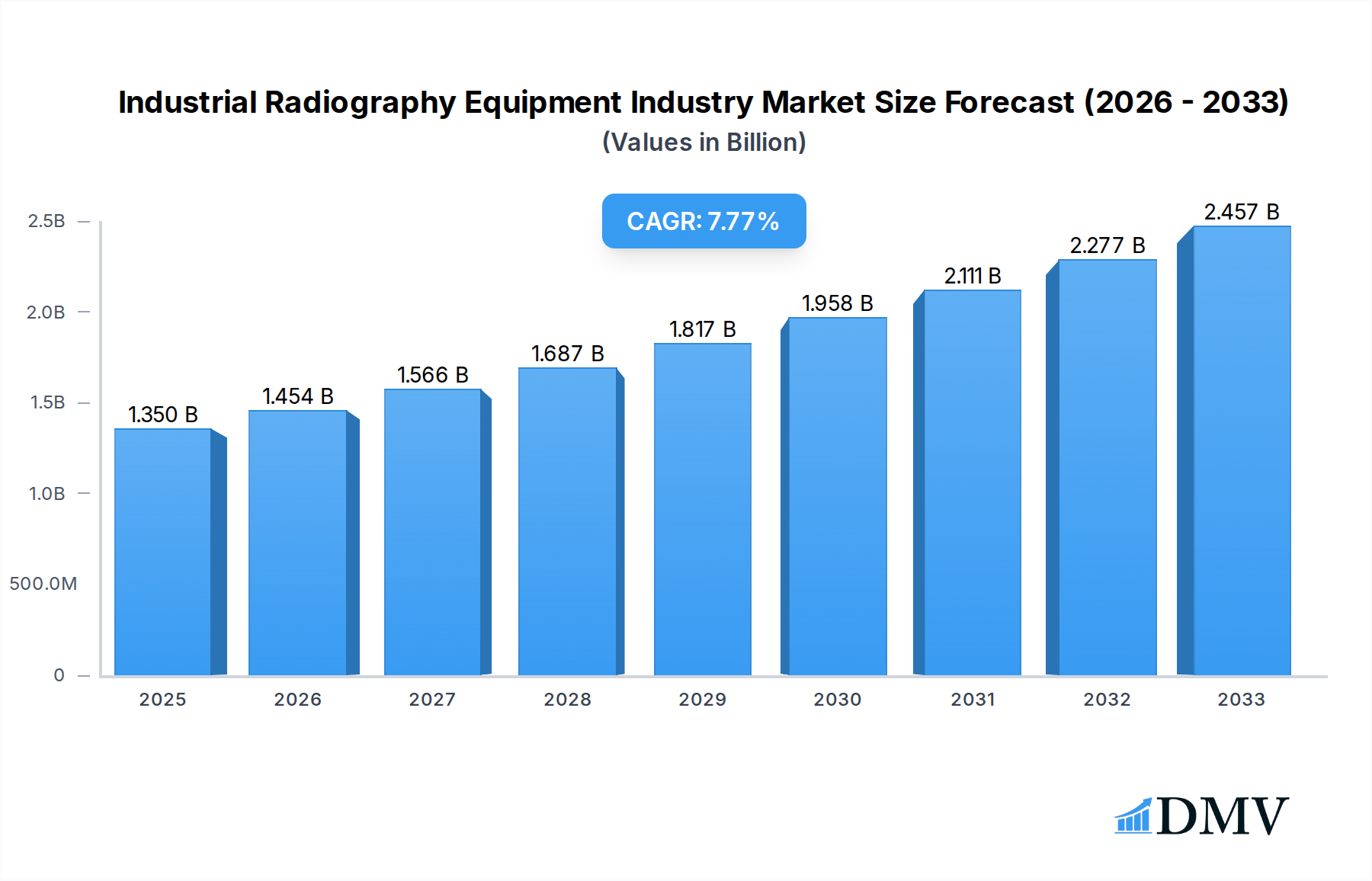

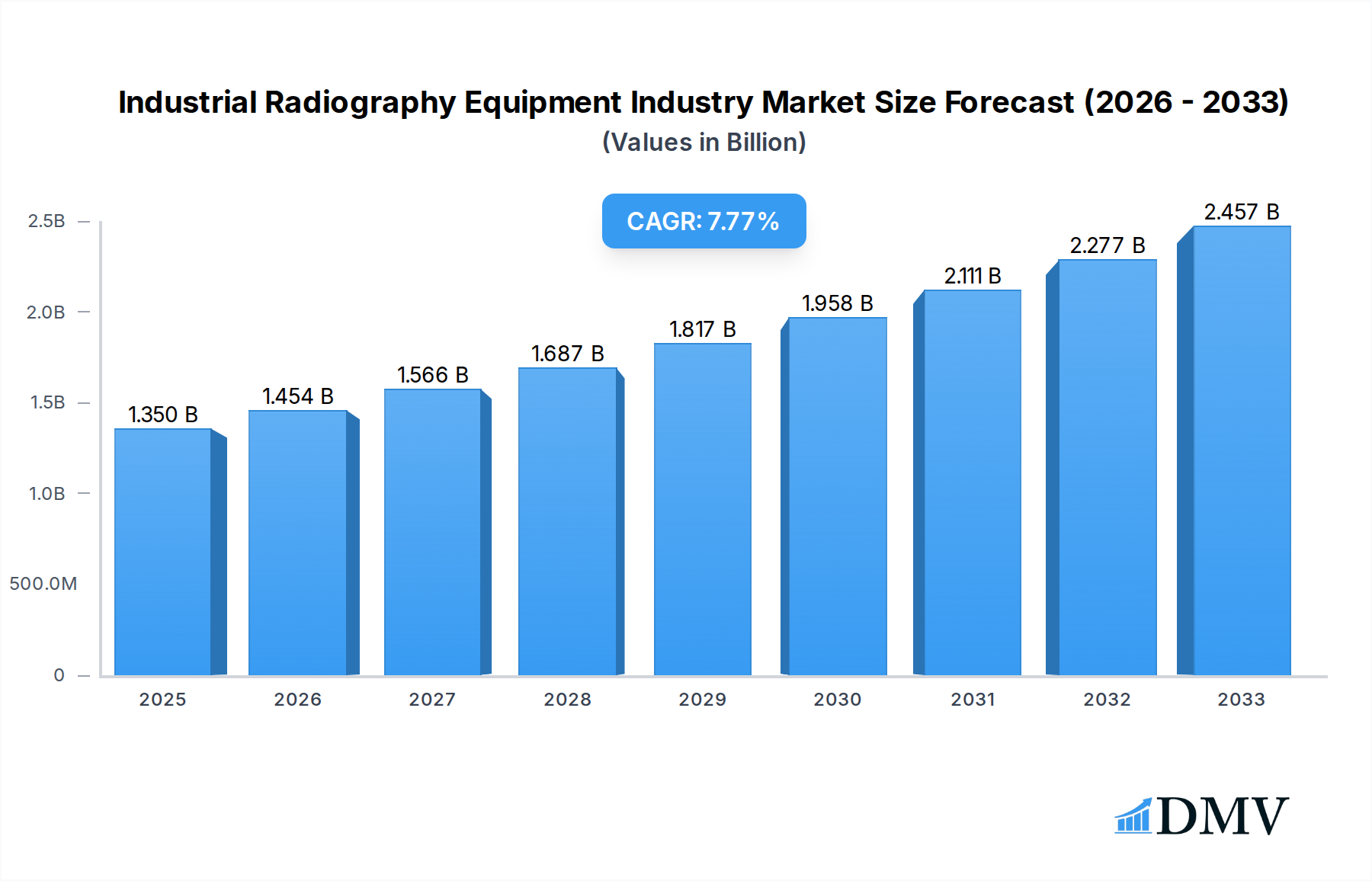

The Industrial Radiography Equipment market is poised for robust expansion, projected to reach a significant $1.35 billion in 2025 with a compound annual growth rate (CAGR) of 8.6% through 2033. This impressive growth is fueled by an increasing demand for non-destructive testing (NDT) across a diverse range of industries. Advanced technologies like Computed Radiography (CR) and Direct Radiography (DR) are gaining traction due to their enhanced imaging capabilities, faster inspection times, and reduced waste, driving adoption in sectors such as Aerospace and Defense, Petrochemical and Gas, and Energy and Power. The inherent need for quality assurance, safety compliance, and defect detection in critical infrastructure and high-value components underpins the market's upward trajectory. Furthermore, the ongoing development of portable and automated radiography systems is expanding accessibility and efficiency, making these solutions viable for a broader spectrum of applications, from manufacturing quality control to construction site inspections.

Industrial Radiography Equipment Industry Market Size (In Billion)

The market's upward momentum is further bolstered by strategic investments in research and development by leading players, focusing on improved resolution, digital integration, and sophisticated data analysis software. Key drivers include stringent regulatory frameworks mandating rigorous inspection protocols, the growing complexity of manufactured components requiring precise defect identification, and the increasing emphasis on predictive maintenance to minimize operational downtime and costs. While the market benefits from these powerful growth drivers, potential restraints such as the initial high cost of advanced equipment and the need for skilled personnel for operation and interpretation warrant consideration. Nevertheless, the continuous innovation in radiography technologies, coupled with the expanding application areas and growing awareness of the benefits of NDT, ensures a dynamic and thriving market landscape for industrial radiography equipment in the coming years.

Industrial Radiography Equipment Industry Company Market Share

This comprehensive report offers an in-depth analysis of the Industrial Radiography Equipment Industry, providing critical insights into market dynamics, technological advancements, and future growth trajectories. Covering the period from 2019 to 2033, with a base and estimated year of 2025, this study is an indispensable resource for stakeholders seeking to understand and capitalize on the evolving landscape of non-destructive testing (NDT) solutions. The report delves into market segmentation by technology and end-user industries, highlights key players, and forecasts market expansion, driven by innovations in Computed Radiography (CR), Direct Radiography (DR), and Computed Tomography (CT). The global market for industrial radiography equipment is projected to reach a valuation exceeding $5.5 billion by 2025, with robust growth anticipated across sectors like Aerospace and Defense, Petrochemical and Gas, and Energy and Power.

Industrial Radiography Equipment Industry Market Composition & Trends

The Industrial Radiography Equipment Industry is characterized by a moderate to high level of market concentration, with a few dominant players and a growing number of niche innovators. Market share distribution sees key entities like Baker Hughes, Hitachi Ltd., and Canon Medical Systems Corporation holding significant positions, particularly in the advanced Computed Tomography segment. Innovation catalysts are primarily driven by the relentless pursuit of higher resolution, faster imaging, and portable solutions, fueled by investments in research and development exceeding $500 million annually across leading companies. The regulatory landscape, though evolving, generally supports the adoption of advanced NDT technologies to ensure safety and quality standards across critical industries. Substitute products, such as ultrasonic testing and eddy current testing, pose a competitive challenge, but the unique imaging capabilities of industrial radiography in defect characterization remain paramount. End-user profiles range from large-scale industrial manufacturers and energy providers to specialized defense contractors and construction firms, each with specific inspection needs. Mergers and acquisition (M&A) activities, with deal values often in the range of $50 million to $500 million, are strategically shaping the market by consolidating expertise and expanding product portfolios. For instance, Bain Capital's acquisition of Evident Corporation highlights the strategic importance of this sector.

Industrial Radiography Equipment Industry Industry Evolution

The Industrial Radiography Equipment Industry has witnessed a significant evolutionary path, transitioning from traditional Film Radiography to sophisticated digital solutions like Computed Radiography (CR) and Direct Radiography (DR), with Computed Tomography (CT) emerging as a leading technology for complex defect analysis. This evolution has been propelled by a compound annual growth rate (CAGR) of approximately 7.5% over the historical period of 2019-2024, with projections indicating a sustained growth trajectory for the forecast period of 2025-2033. The adoption metrics for digital radiography systems have surged, with CR and DR systems now accounting for over 65% of the global market share, displacing traditional film-based methods due to their superior image quality, reduced processing time, and enhanced data management capabilities. The growing demand for lighter, more portable, and automated inspection equipment reflects shifting consumer demands and industry requirements, especially within the Aerospace and Defense and Automotive and Transportation sectors. Market growth trajectories are also influenced by increasing stringent safety regulations and the need for more efficient quality control in manufacturing processes, driving the demand for advanced X-ray and Gamma Ray equipment. Furthermore, investments in infrastructure development and the expansion of the Petrochemical and Gas industry, particularly in emerging economies, are significant contributors to the market's upward trend. The global market value, estimated at over $5.0 billion in the base year of 2025, is expected to surpass $8.0 billion by 2033.

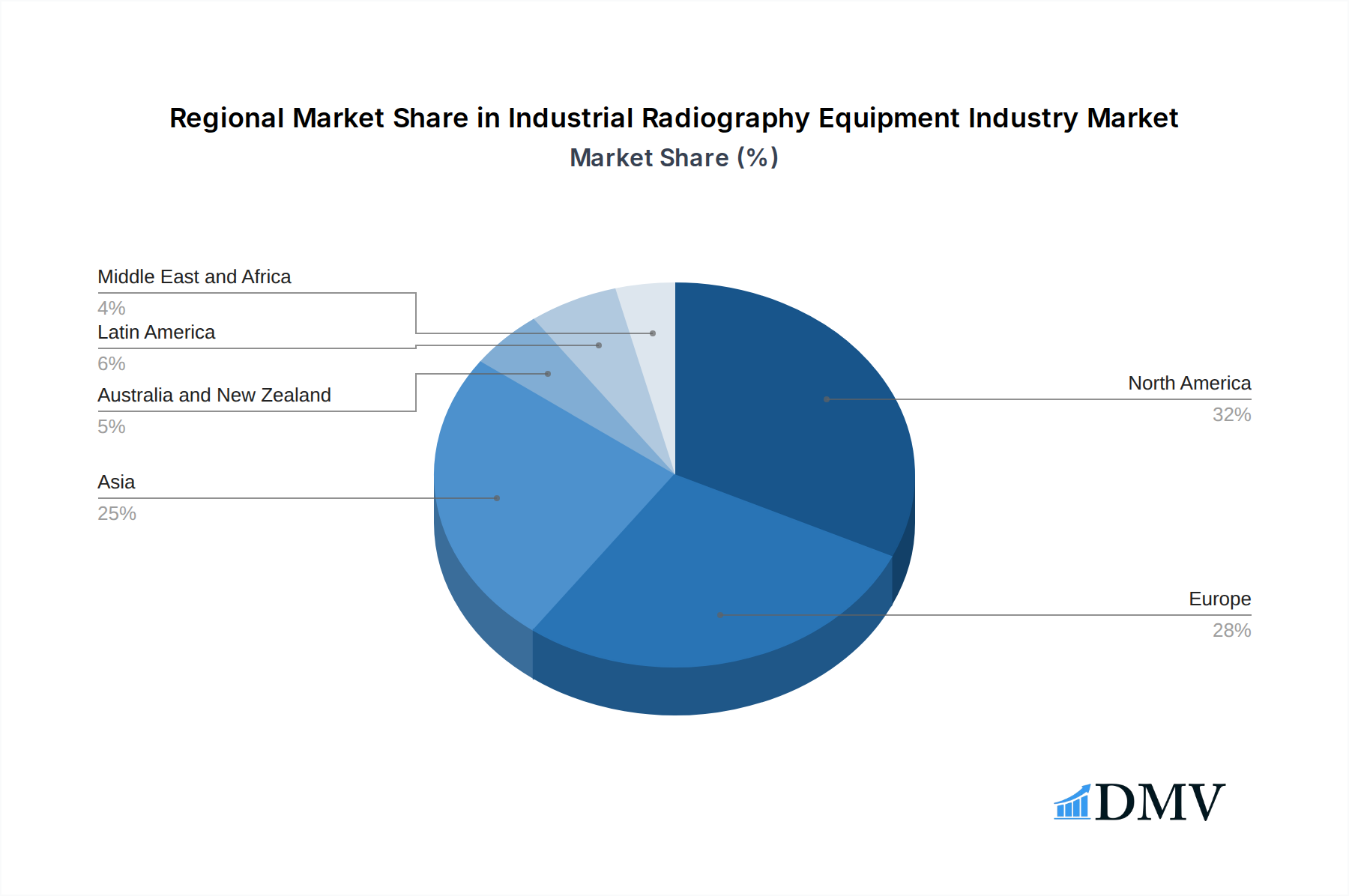

Leading Regions, Countries, or Segments in Industrial Radiography Equipment Industry

The North America region currently dominates the Industrial Radiography Equipment Industry, driven by substantial investments in the Aerospace and Defense, Petrochemical and Gas, and Energy and Power sectors, with an estimated market share of 35%. The United States, in particular, stands as a leading country due to its robust manufacturing base, stringent quality control mandates, and significant defense spending, contributing over 60% to the regional market value.

Technology Dominance: Within the technology segment, Computed Radiography (CR) and Direct Radiography (DR) hold the largest market share, estimated at 55%, owing to their widespread adoption in various industrial applications requiring detailed flaw detection and analysis. Computed Tomography (CT) is experiencing the fastest growth rate, projected at 9.2% CAGR, driven by its unparalleled ability to provide 3D imaging for complex internal defect visualization, particularly in the Aerospace and Defense and Automotive and Transportation industries. Film Radiography, while still present, is gradually declining in market share.

End-User Industry Dominance: The Aerospace and Defense sector represents a significant end-user, accounting for an estimated 25% of the market value, owing to the critical need for non-destructive inspection of aircraft components and defense equipment. The Petrochemical and Gas industry is another major consumer, utilizing radiography for the inspection of pipelines, pressure vessels, and other critical infrastructure, representing approximately 20% of the market. The Energy and Power sector also contributes substantially, with a market share of around 18%, driven by the inspection of power generation equipment and renewable energy installations. Manufacturing (including automotive) and Construction follow, with market shares of 15% and 10% respectively.

Key Drivers in Leading Regions:

- North America: High R&D spending, presence of major industry players like L3Harris Technologies Inc. and Baker Hughes, stringent regulatory frameworks for safety and quality, and significant defense contracts.

- Europe: Strong automotive and aerospace industries, supportive government initiatives for industrial modernization, and a growing emphasis on infrastructure maintenance and upgrade projects.

- Asia Pacific: Rapid industrialization, expanding manufacturing capabilities, increasing demand for energy resources, and growing adoption of advanced NDT technologies in countries like China and India, projected to witness the highest CAGR of 8.5%.

Industrial Radiography Equipment Industry Product Innovations

Recent product innovations in the Industrial Radiography Equipment Industry are centered on enhancing image resolution, reducing inspection times, and increasing portability for field applications. For instance, the development of advanced flat panel detectors (FPDs) has significantly improved the clarity and speed of Direct Radiography (DR) systems. Innovations in software algorithms are enabling more sophisticated image processing and automated defect analysis, leading to higher inspection accuracy. The introduction of compact, battery-powered portable X-ray generators and detectors by companies like Vidisco Ltd. (Aran Electronics Ltd.) is transforming field inspections, allowing for rapid deployment in challenging environments. These advancements contribute to improved performance metrics such as signal-to-noise ratio (SNR) and detection limits, making radiographic inspections more efficient and effective across diverse end-user industries.

Propelling Factors for Industrial Radiography Equipment Industry Growth

Several key factors are propelling the growth of the Industrial Radiography Equipment Industry. Firstly, the increasing demand for enhanced safety and quality control across critical sectors like Aerospace and Defense, Petrochemical and Gas, and Energy and Power mandates the use of reliable NDT solutions. Secondly, continuous technological advancements in digital radiography, particularly Computed Radiography (CR), Direct Radiography (DR), and Computed Tomography (CT), are offering superior imaging capabilities, faster processing, and more comprehensive data analysis. Thirdly, government regulations and industry standards are increasingly emphasizing non-destructive testing methods for ensuring the integrity of infrastructure and manufactured goods. Lastly, the growing global industrial manufacturing output and the expansion of energy exploration and production activities are creating sustained demand for industrial radiography equipment.

Obstacles in the Industrial Radiography Equipment Industry Market

Despite the robust growth, the Industrial Radiography Equipment Industry faces certain obstacles. High initial capital investment for advanced digital radiography systems can be a deterrent for small and medium-sized enterprises. Regulatory hurdles and the need for specialized training and certification for operators can also impede widespread adoption. Supply chain disruptions, particularly for critical components used in X-ray tubes and detectors, can impact production timelines and costs. Furthermore, the competitive pressure from alternative NDT technologies, such as ultrasonic testing and eddy current testing, necessitates continuous innovation and competitive pricing strategies. The disposal and management of outdated equipment and waste materials also present environmental and regulatory challenges.

Future Opportunities in Industrial Radiography Equipment Industry

The Industrial Radiography Equipment Industry is ripe with future opportunities. The growing emphasis on predictive maintenance and asset integrity management in aging infrastructure across the Petrochemical and Gas and Energy and Power sectors presents a significant avenue for growth. The expansion of additive manufacturing (3D printing) creates a new frontier for NDT, with radiography playing a crucial role in inspecting complex 3D printed parts. Emerging markets in Asia Pacific and Latin America, with their burgeoning industrial bases, offer substantial untapped potential. Furthermore, advancements in artificial intelligence (AI) and machine learning (ML) for automated image analysis and defect recognition are expected to revolutionize the industry, enabling faster and more accurate inspections. The development of portable, wireless, and cloud-connected radiography systems will further enhance accessibility and data sharing.

Major Players in the Industrial Radiography Equipment Industry Ecosystem

- L3Harris Technologies Inc.

- Baker Hughes

- Vidisco Ltd. (Aran Electronics Ltd.)

- Hitachi Ltd.

- Comet Holding AG

- Canon Medical Systems Corporation (Canon Inc.)

- Rigaku Corporation (Carlyle Group)

- North Star Imaging Inc.

- Carestream Health

- Carl Zeiss AG

- Evident Corporation (Bain Capital)

- Hamamatsu Photonics K K

- Durr NDT GmbH & Co Kg

- Teledyne Dalsa Inc (Teledyne Technologies)

- Fujifilm Corporation (Fujifilm Holdings Corporation)

- Nikon Metrology NV (Nikon Corporation)

Key Developments in Industrial Radiography Equipment Industry Industry

- July 2023: Canon Inc. launched the Zexirai9 digital X-ray RF system, a multi-purpose fluoroscopic table with numerous new functions and a compact design. This new digital X-ray RF system is equipped with Canon's flat panel detector (FPD) and a newly developed image processing technology; the system has been developed in consultation with medical staff, referring physicians, and engineers.

- May 2023: Nikon Metrology announced the launch of its next-generation family of X-ray computed tomography (CT) inspection systems called VOXLS (VOlumemetricX-ray Leading Solutions). It is designed for diverse inspection needs across automotive, aerospace, and academia industries - and likely for use on composite structures - the VOXLS family includes the large-volume VOXLS 40 C 450 available now and four medium-sized models coming later this year. Such initiatives by the companies in the market are expected to complement the industrial radiography market during the forecast period.

Strategic Industrial Radiography Equipment Industry Market Forecast

The strategic outlook for the Industrial Radiography Equipment Industry is exceptionally strong, driven by the confluence of technological innovation and increasing global demand for safety and quality. The forecast period of 2025–2033 anticipates sustained growth, fueled by the widespread adoption of digital radiography solutions, including Computed Radiography (CR), Direct Radiography (DR), and the rapidly expanding Computed Tomography (CT) segment. Key growth catalysts include the need for enhanced inspection capabilities in rapidly growing sectors like Aerospace and Defense and Petrochemical and Gas, alongside a global push for infrastructure modernization and stringent regulatory compliance. Future opportunities lie in the integration of AI and machine learning for automated analysis, the development of more portable and user-friendly systems, and expansion into emerging markets, positioning the industry for significant value creation and technological advancement.

Industrial Radiography Equipment Industry Segmentation

-

1. Technology

- 1.1. Film Radiography

- 1.2. Computed Radiography

- 1.3. Direct Radiography

- 1.4. Computed Tomography

-

2. End-User Industry

- 2.1. Aerospace and Defense

- 2.2. Petrochemical and Gas

- 2.3. Energy and Power

- 2.4. Construction

- 2.5. Automotive and Transportation

- 2.6. Manufacturing

- 2.7. Other End-User Industries

Industrial Radiography Equipment Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia

- 4. Australia and New Zealand

- 5. Latin America

- 6. Middle East and Africa

Industrial Radiography Equipment Industry Regional Market Share

Geographic Coverage of Industrial Radiography Equipment Industry

Industrial Radiography Equipment Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 5.1.1. Film Radiography

- 5.1.2. Computed Radiography

- 5.1.3. Direct Radiography

- 5.1.4. Computed Tomography

- 5.2. Market Analysis, Insights and Forecast - by End-User Industry

- 5.2.1. Aerospace and Defense

- 5.2.2. Petrochemical and Gas

- 5.2.3. Energy and Power

- 5.2.4. Construction

- 5.2.5. Automotive and Transportation

- 5.2.6. Manufacturing

- 5.2.7. Other End-User Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia

- 5.3.4. Australia and New Zealand

- 5.3.5. Latin America

- 5.3.6. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 6. Global Industrial Radiography Equipment Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Technology

- 6.1.1. Film Radiography

- 6.1.2. Computed Radiography

- 6.1.3. Direct Radiography

- 6.1.4. Computed Tomography

- 6.2. Market Analysis, Insights and Forecast - by End-User Industry

- 6.2.1. Aerospace and Defense

- 6.2.2. Petrochemical and Gas

- 6.2.3. Energy and Power

- 6.2.4. Construction

- 6.2.5. Automotive and Transportation

- 6.2.6. Manufacturing

- 6.2.7. Other End-User Industries

- 6.1. Market Analysis, Insights and Forecast - by Technology

- 7. North America Industrial Radiography Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Technology

- 7.1.1. Film Radiography

- 7.1.2. Computed Radiography

- 7.1.3. Direct Radiography

- 7.1.4. Computed Tomography

- 7.2. Market Analysis, Insights and Forecast - by End-User Industry

- 7.2.1. Aerospace and Defense

- 7.2.2. Petrochemical and Gas

- 7.2.3. Energy and Power

- 7.2.4. Construction

- 7.2.5. Automotive and Transportation

- 7.2.6. Manufacturing

- 7.2.7. Other End-User Industries

- 7.1. Market Analysis, Insights and Forecast - by Technology

- 8. Europe Industrial Radiography Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Technology

- 8.1.1. Film Radiography

- 8.1.2. Computed Radiography

- 8.1.3. Direct Radiography

- 8.1.4. Computed Tomography

- 8.2. Market Analysis, Insights and Forecast - by End-User Industry

- 8.2.1. Aerospace and Defense

- 8.2.2. Petrochemical and Gas

- 8.2.3. Energy and Power

- 8.2.4. Construction

- 8.2.5. Automotive and Transportation

- 8.2.6. Manufacturing

- 8.2.7. Other End-User Industries

- 8.1. Market Analysis, Insights and Forecast - by Technology

- 9. Asia Industrial Radiography Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Technology

- 9.1.1. Film Radiography

- 9.1.2. Computed Radiography

- 9.1.3. Direct Radiography

- 9.1.4. Computed Tomography

- 9.2. Market Analysis, Insights and Forecast - by End-User Industry

- 9.2.1. Aerospace and Defense

- 9.2.2. Petrochemical and Gas

- 9.2.3. Energy and Power

- 9.2.4. Construction

- 9.2.5. Automotive and Transportation

- 9.2.6. Manufacturing

- 9.2.7. Other End-User Industries

- 9.1. Market Analysis, Insights and Forecast - by Technology

- 10. Australia and New Zealand Industrial Radiography Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Technology

- 10.1.1. Film Radiography

- 10.1.2. Computed Radiography

- 10.1.3. Direct Radiography

- 10.1.4. Computed Tomography

- 10.2. Market Analysis, Insights and Forecast - by End-User Industry

- 10.2.1. Aerospace and Defense

- 10.2.2. Petrochemical and Gas

- 10.2.3. Energy and Power

- 10.2.4. Construction

- 10.2.5. Automotive and Transportation

- 10.2.6. Manufacturing

- 10.2.7. Other End-User Industries

- 10.1. Market Analysis, Insights and Forecast - by Technology

- 11. Latin America Industrial Radiography Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Technology

- 11.1.1. Film Radiography

- 11.1.2. Computed Radiography

- 11.1.3. Direct Radiography

- 11.1.4. Computed Tomography

- 11.2. Market Analysis, Insights and Forecast - by End-User Industry

- 11.2.1. Aerospace and Defense

- 11.2.2. Petrochemical and Gas

- 11.2.3. Energy and Power

- 11.2.4. Construction

- 11.2.5. Automotive and Transportation

- 11.2.6. Manufacturing

- 11.2.7. Other End-User Industries

- 11.1. Market Analysis, Insights and Forecast - by Technology

- 12. Middle East and Africa Industrial Radiography Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Technology

- 12.1.1. Film Radiography

- 12.1.2. Computed Radiography

- 12.1.3. Direct Radiography

- 12.1.4. Computed Tomography

- 12.2. Market Analysis, Insights and Forecast - by End-User Industry

- 12.2.1. Aerospace and Defense

- 12.2.2. Petrochemical and Gas

- 12.2.3. Energy and Power

- 12.2.4. Construction

- 12.2.5. Automotive and Transportation

- 12.2.6. Manufacturing

- 12.2.7. Other End-User Industries

- 12.1. Market Analysis, Insights and Forecast - by Technology

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 L3Harris Technologies Inc

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Baker Hughes

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Vidisco Ltd (Aran Electronics Ltd )

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Hitachi Ltd

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Comet Holding AG

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Canon Medical Systems Corporation (Canon Inc )

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Rigaku Corporation (Carlyle Group)

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 North Star Imaging Inc

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Carestream Health

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 Carl Zeiss AG

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.11 Evident Corporation (Bain Capital)

- 13.1.11.1. Company Overview

- 13.1.11.2. Products

- 13.1.11.3. Company Financials

- 13.1.11.4. SWOT Analysis

- 13.1.12 Hamamatsu Photonics K K

- 13.1.12.1. Company Overview

- 13.1.12.2. Products

- 13.1.12.3. Company Financials

- 13.1.12.4. SWOT Analysis

- 13.1.13 Durr NDT GmbH & Co Kg

- 13.1.13.1. Company Overview

- 13.1.13.2. Products

- 13.1.13.3. Company Financials

- 13.1.13.4. SWOT Analysis

- 13.1.14 Teledyne Dalsa Inc (Teledyne Technologies)

- 13.1.14.1. Company Overview

- 13.1.14.2. Products

- 13.1.14.3. Company Financials

- 13.1.14.4. SWOT Analysis

- 13.1.15 Fujifilm Corporation (Fujifilm Holdings Corporation)

- 13.1.15.1. Company Overview

- 13.1.15.2. Products

- 13.1.15.3. Company Financials

- 13.1.15.4. SWOT Analysis

- 13.1.16 Nikon Metrology NV (Nikon Corporation)

- 13.1.16.1. Company Overview

- 13.1.16.2. Products

- 13.1.16.3. Company Financials

- 13.1.16.4. SWOT Analysis

- 13.1.1 L3Harris Technologies Inc

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Industrial Radiography Equipment Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Industrial Radiography Equipment Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Industrial Radiography Equipment Industry Revenue (billion), by Technology 2025 & 2033

- Figure 4: North America Industrial Radiography Equipment Industry Volume (K Unit), by Technology 2025 & 2033

- Figure 5: North America Industrial Radiography Equipment Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 6: North America Industrial Radiography Equipment Industry Volume Share (%), by Technology 2025 & 2033

- Figure 7: North America Industrial Radiography Equipment Industry Revenue (billion), by End-User Industry 2025 & 2033

- Figure 8: North America Industrial Radiography Equipment Industry Volume (K Unit), by End-User Industry 2025 & 2033

- Figure 9: North America Industrial Radiography Equipment Industry Revenue Share (%), by End-User Industry 2025 & 2033

- Figure 10: North America Industrial Radiography Equipment Industry Volume Share (%), by End-User Industry 2025 & 2033

- Figure 11: North America Industrial Radiography Equipment Industry Revenue (billion), by Country 2025 & 2033

- Figure 12: North America Industrial Radiography Equipment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 13: North America Industrial Radiography Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Industrial Radiography Equipment Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: Europe Industrial Radiography Equipment Industry Revenue (billion), by Technology 2025 & 2033

- Figure 16: Europe Industrial Radiography Equipment Industry Volume (K Unit), by Technology 2025 & 2033

- Figure 17: Europe Industrial Radiography Equipment Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 18: Europe Industrial Radiography Equipment Industry Volume Share (%), by Technology 2025 & 2033

- Figure 19: Europe Industrial Radiography Equipment Industry Revenue (billion), by End-User Industry 2025 & 2033

- Figure 20: Europe Industrial Radiography Equipment Industry Volume (K Unit), by End-User Industry 2025 & 2033

- Figure 21: Europe Industrial Radiography Equipment Industry Revenue Share (%), by End-User Industry 2025 & 2033

- Figure 22: Europe Industrial Radiography Equipment Industry Volume Share (%), by End-User Industry 2025 & 2033

- Figure 23: Europe Industrial Radiography Equipment Industry Revenue (billion), by Country 2025 & 2033

- Figure 24: Europe Industrial Radiography Equipment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 25: Europe Industrial Radiography Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Europe Industrial Radiography Equipment Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Asia Industrial Radiography Equipment Industry Revenue (billion), by Technology 2025 & 2033

- Figure 28: Asia Industrial Radiography Equipment Industry Volume (K Unit), by Technology 2025 & 2033

- Figure 29: Asia Industrial Radiography Equipment Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 30: Asia Industrial Radiography Equipment Industry Volume Share (%), by Technology 2025 & 2033

- Figure 31: Asia Industrial Radiography Equipment Industry Revenue (billion), by End-User Industry 2025 & 2033

- Figure 32: Asia Industrial Radiography Equipment Industry Volume (K Unit), by End-User Industry 2025 & 2033

- Figure 33: Asia Industrial Radiography Equipment Industry Revenue Share (%), by End-User Industry 2025 & 2033

- Figure 34: Asia Industrial Radiography Equipment Industry Volume Share (%), by End-User Industry 2025 & 2033

- Figure 35: Asia Industrial Radiography Equipment Industry Revenue (billion), by Country 2025 & 2033

- Figure 36: Asia Industrial Radiography Equipment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 37: Asia Industrial Radiography Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Asia Industrial Radiography Equipment Industry Volume Share (%), by Country 2025 & 2033

- Figure 39: Australia and New Zealand Industrial Radiography Equipment Industry Revenue (billion), by Technology 2025 & 2033

- Figure 40: Australia and New Zealand Industrial Radiography Equipment Industry Volume (K Unit), by Technology 2025 & 2033

- Figure 41: Australia and New Zealand Industrial Radiography Equipment Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 42: Australia and New Zealand Industrial Radiography Equipment Industry Volume Share (%), by Technology 2025 & 2033

- Figure 43: Australia and New Zealand Industrial Radiography Equipment Industry Revenue (billion), by End-User Industry 2025 & 2033

- Figure 44: Australia and New Zealand Industrial Radiography Equipment Industry Volume (K Unit), by End-User Industry 2025 & 2033

- Figure 45: Australia and New Zealand Industrial Radiography Equipment Industry Revenue Share (%), by End-User Industry 2025 & 2033

- Figure 46: Australia and New Zealand Industrial Radiography Equipment Industry Volume Share (%), by End-User Industry 2025 & 2033

- Figure 47: Australia and New Zealand Industrial Radiography Equipment Industry Revenue (billion), by Country 2025 & 2033

- Figure 48: Australia and New Zealand Industrial Radiography Equipment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 49: Australia and New Zealand Industrial Radiography Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Australia and New Zealand Industrial Radiography Equipment Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Latin America Industrial Radiography Equipment Industry Revenue (billion), by Technology 2025 & 2033

- Figure 52: Latin America Industrial Radiography Equipment Industry Volume (K Unit), by Technology 2025 & 2033

- Figure 53: Latin America Industrial Radiography Equipment Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 54: Latin America Industrial Radiography Equipment Industry Volume Share (%), by Technology 2025 & 2033

- Figure 55: Latin America Industrial Radiography Equipment Industry Revenue (billion), by End-User Industry 2025 & 2033

- Figure 56: Latin America Industrial Radiography Equipment Industry Volume (K Unit), by End-User Industry 2025 & 2033

- Figure 57: Latin America Industrial Radiography Equipment Industry Revenue Share (%), by End-User Industry 2025 & 2033

- Figure 58: Latin America Industrial Radiography Equipment Industry Volume Share (%), by End-User Industry 2025 & 2033

- Figure 59: Latin America Industrial Radiography Equipment Industry Revenue (billion), by Country 2025 & 2033

- Figure 60: Latin America Industrial Radiography Equipment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 61: Latin America Industrial Radiography Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 62: Latin America Industrial Radiography Equipment Industry Volume Share (%), by Country 2025 & 2033

- Figure 63: Middle East and Africa Industrial Radiography Equipment Industry Revenue (billion), by Technology 2025 & 2033

- Figure 64: Middle East and Africa Industrial Radiography Equipment Industry Volume (K Unit), by Technology 2025 & 2033

- Figure 65: Middle East and Africa Industrial Radiography Equipment Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 66: Middle East and Africa Industrial Radiography Equipment Industry Volume Share (%), by Technology 2025 & 2033

- Figure 67: Middle East and Africa Industrial Radiography Equipment Industry Revenue (billion), by End-User Industry 2025 & 2033

- Figure 68: Middle East and Africa Industrial Radiography Equipment Industry Volume (K Unit), by End-User Industry 2025 & 2033

- Figure 69: Middle East and Africa Industrial Radiography Equipment Industry Revenue Share (%), by End-User Industry 2025 & 2033

- Figure 70: Middle East and Africa Industrial Radiography Equipment Industry Volume Share (%), by End-User Industry 2025 & 2033

- Figure 71: Middle East and Africa Industrial Radiography Equipment Industry Revenue (billion), by Country 2025 & 2033

- Figure 72: Middle East and Africa Industrial Radiography Equipment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 73: Middle East and Africa Industrial Radiography Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 74: Middle East and Africa Industrial Radiography Equipment Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Industrial Radiography Equipment Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 2: Global Industrial Radiography Equipment Industry Volume K Unit Forecast, by Technology 2020 & 2033

- Table 3: Global Industrial Radiography Equipment Industry Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 4: Global Industrial Radiography Equipment Industry Volume K Unit Forecast, by End-User Industry 2020 & 2033

- Table 5: Global Industrial Radiography Equipment Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Industrial Radiography Equipment Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 7: Global Industrial Radiography Equipment Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 8: Global Industrial Radiography Equipment Industry Volume K Unit Forecast, by Technology 2020 & 2033

- Table 9: Global Industrial Radiography Equipment Industry Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 10: Global Industrial Radiography Equipment Industry Volume K Unit Forecast, by End-User Industry 2020 & 2033

- Table 11: Global Industrial Radiography Equipment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global Industrial Radiography Equipment Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 13: Global Industrial Radiography Equipment Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 14: Global Industrial Radiography Equipment Industry Volume K Unit Forecast, by Technology 2020 & 2033

- Table 15: Global Industrial Radiography Equipment Industry Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 16: Global Industrial Radiography Equipment Industry Volume K Unit Forecast, by End-User Industry 2020 & 2033

- Table 17: Global Industrial Radiography Equipment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 18: Global Industrial Radiography Equipment Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 19: Global Industrial Radiography Equipment Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 20: Global Industrial Radiography Equipment Industry Volume K Unit Forecast, by Technology 2020 & 2033

- Table 21: Global Industrial Radiography Equipment Industry Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 22: Global Industrial Radiography Equipment Industry Volume K Unit Forecast, by End-User Industry 2020 & 2033

- Table 23: Global Industrial Radiography Equipment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global Industrial Radiography Equipment Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 25: Global Industrial Radiography Equipment Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 26: Global Industrial Radiography Equipment Industry Volume K Unit Forecast, by Technology 2020 & 2033

- Table 27: Global Industrial Radiography Equipment Industry Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 28: Global Industrial Radiography Equipment Industry Volume K Unit Forecast, by End-User Industry 2020 & 2033

- Table 29: Global Industrial Radiography Equipment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 30: Global Industrial Radiography Equipment Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 31: Global Industrial Radiography Equipment Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 32: Global Industrial Radiography Equipment Industry Volume K Unit Forecast, by Technology 2020 & 2033

- Table 33: Global Industrial Radiography Equipment Industry Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 34: Global Industrial Radiography Equipment Industry Volume K Unit Forecast, by End-User Industry 2020 & 2033

- Table 35: Global Industrial Radiography Equipment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 36: Global Industrial Radiography Equipment Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 37: Global Industrial Radiography Equipment Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 38: Global Industrial Radiography Equipment Industry Volume K Unit Forecast, by Technology 2020 & 2033

- Table 39: Global Industrial Radiography Equipment Industry Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 40: Global Industrial Radiography Equipment Industry Volume K Unit Forecast, by End-User Industry 2020 & 2033

- Table 41: Global Industrial Radiography Equipment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 42: Global Industrial Radiography Equipment Industry Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Industrial Radiography Equipment Industry?

The projected CAGR is approximately 8.6%.

2. Which companies are prominent players in the Industrial Radiography Equipment Industry?

Key companies in the market include L3Harris Technologies Inc, Baker Hughes, Vidisco Ltd (Aran Electronics Ltd ), Hitachi Ltd, Comet Holding AG, Canon Medical Systems Corporation (Canon Inc ), Rigaku Corporation (Carlyle Group), North Star Imaging Inc, Carestream Health, Carl Zeiss AG, Evident Corporation (Bain Capital), Hamamatsu Photonics K K, Durr NDT GmbH & Co Kg, Teledyne Dalsa Inc (Teledyne Technologies), Fujifilm Corporation (Fujifilm Holdings Corporation), Nikon Metrology NV (Nikon Corporation).

3. What are the main segments of the Industrial Radiography Equipment Industry?

The market segments include Technology, End-User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.35 billion as of 2022.

5. What are some drivers contributing to market growth?

Rising Demand From Automotive and Aerospace Industry; Augmented Accuracy of Inspection With the Integration of Advanced Software.

6. What are the notable trends driving market growth?

Aerospace and Defense to be the Largest End User.

7. Are there any restraints impacting market growth?

High Risk of Radiation Since it uses Gamma Rays. X-Rays; High Deployment Costs.

8. Can you provide examples of recent developments in the market?

July 2023: Canon Inc. launched the Zexirai9 digital X-ray RF system, a multi-purpose fluoroscopic table with many new functions and a compact design. Zexirai9 is a new digital X-ray RF system equipped with Canon's flat panel detector (FPD) and a newly developed image processing technology; the system has been developed in consultation with medical staff, referring physicians, and engineers.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Industrial Radiography Equipment Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Industrial Radiography Equipment Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Industrial Radiography Equipment Industry?

To stay informed about further developments, trends, and reports in the Industrial Radiography Equipment Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence