Key Insights

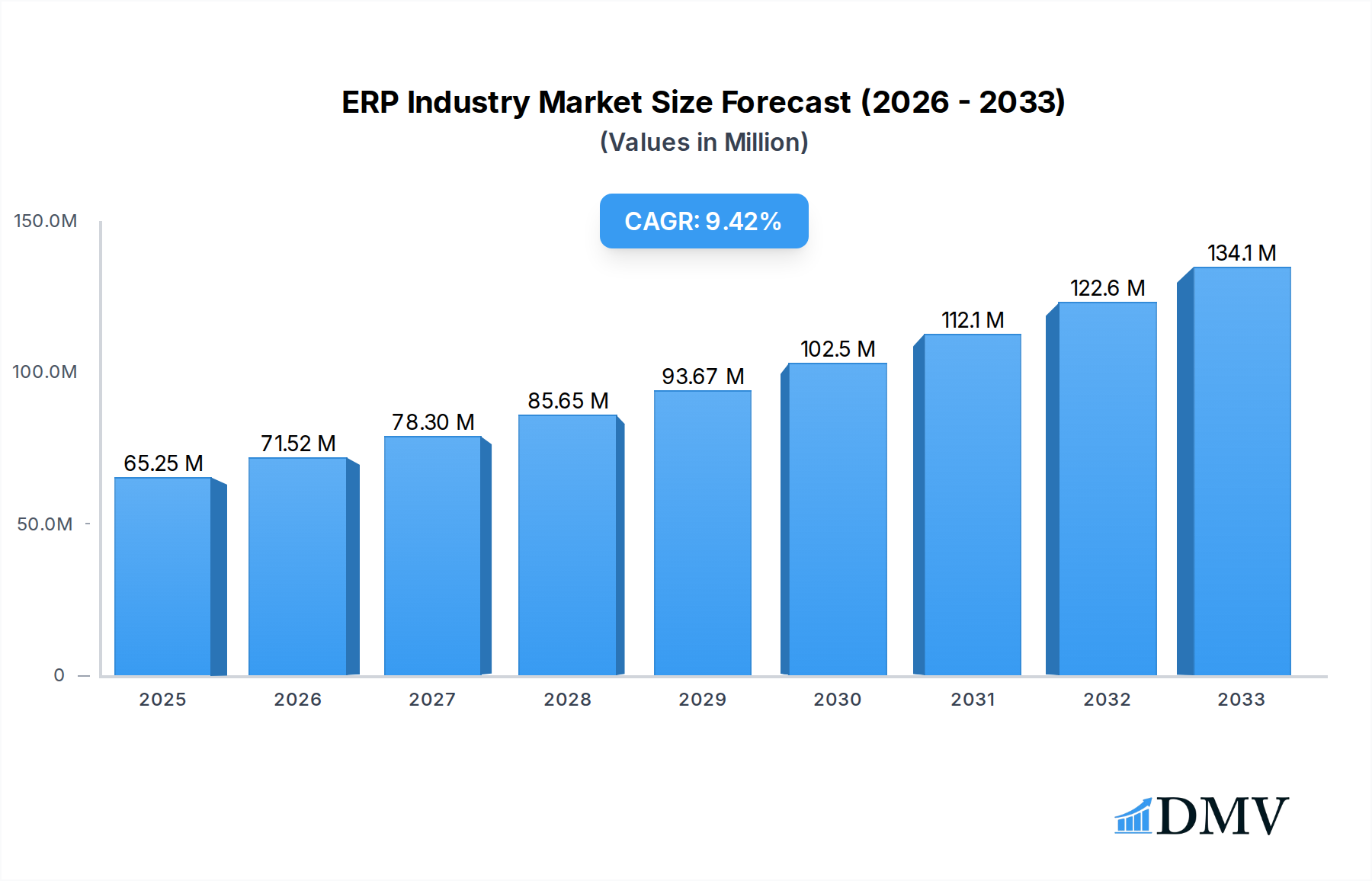

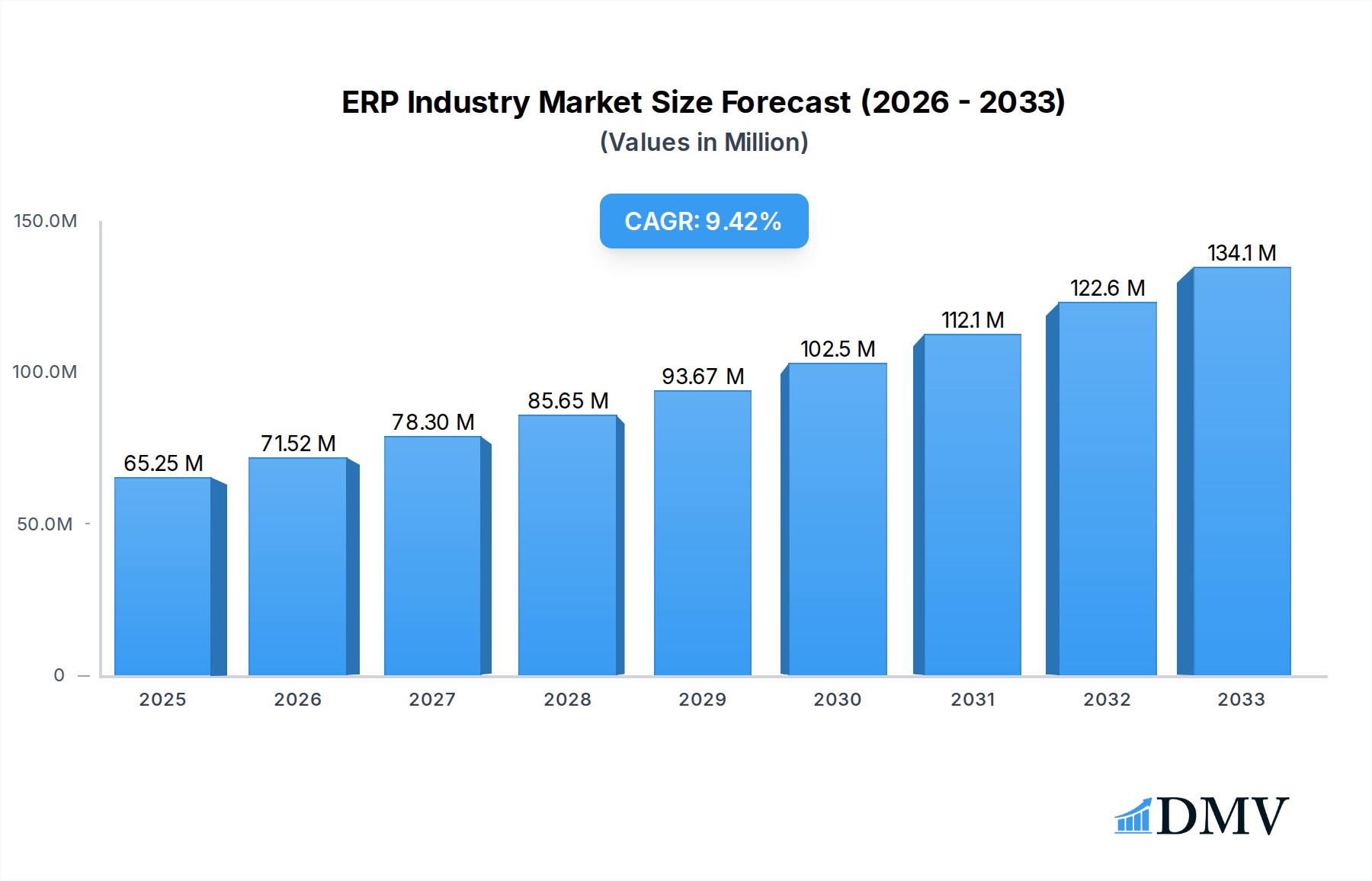

The Enterprise Resource Planning (ERP) market is poised for robust expansion, projected to reach $65.25 million by 2025, with a compelling Compound Annual Growth Rate (CAGR) of 9.76% during the forecast period of 2025-2033. This significant growth is being propelled by several key drivers, including the increasing demand for cloud-based ERP solutions, the need for enhanced operational efficiency and data-driven decision-making across organizations, and the growing adoption of digital transformation initiatives. The market is witnessing a strong surge in demand for integrated solutions that streamline core business processes such as finance, human resources, supply chain management, and marketing. Small and medium-sized enterprises (SMEs) are increasingly recognizing the value of ERP systems in optimizing their operations and competing effectively with larger players, contributing significantly to market penetration. Furthermore, the continuous innovation in ERP software, incorporating advanced technologies like artificial intelligence (AI) and machine learning (ML), is further fueling its adoption by offering predictive analytics and automated workflows.

ERP Industry Market Size (In Million)

The ERP market is segmented across various dimensions, reflecting its widespread applicability. In terms of Offering, the market is characterized by a strong preference for Solutions, which encompass the comprehensive software packages, and Services, including implementation, customization, and support, crucial for maximizing ERP benefits. Functionally, HR, Supply Chain, and Finance are dominant segments, underscoring their critical role in any enterprise. The Deployment model is tilting towards Hybrid and Cloud-based solutions, offering flexibility and scalability, while On-premise deployments continue to hold a presence, particularly for organizations with specific security and customization needs. The Industry Verticals are demonstrating widespread adoption, with BFSI, IT and Telecom, Retail and E-commerce, and Manufacturing leading the charge due to their complex operational requirements. Leading companies like SAP SE, Oracle Corporation, Microsoft Corporation, and IBM are at the forefront of innovation, driving market competition and offering advanced ERP capabilities to a diverse global clientele.

ERP Industry Company Market Share

ERP Industry Market Composition & Trends

The Enterprise Resource Planning (ERP) industry is characterized by a dynamic market composition with significant concentration among a few dominant players, while also fostering a vibrant ecosystem of specialized providers. Innovation is primarily catalyzed by the relentless pursuit of digital transformation, cloud adoption, and the integration of advanced technologies like AI and machine learning. The regulatory landscape, particularly concerning data privacy (e.g., GDPR, CCPA) and industry-specific compliance, exerts a considerable influence on ERP solution development and deployment strategies. Substitute products, while not direct replacements, include fragmented best-of-breed solutions and highly customized legacy systems that enterprises may still leverage. End-user profiles span the entire organizational spectrum, from Small and Medium Enterprises (SMEs) seeking cost-effective, scalable solutions to Large Enterprises demanding robust, comprehensive suites that integrate complex global operations. Mergers and Acquisitions (M&A) activities continue to shape the market, with strategic consolidations aimed at expanding product portfolios, gaining market share, and acquiring specialized technological capabilities. For instance, recent M&A activities have seen valuations in the hundreds of millions to several billion dollars, reflecting the strategic importance of ERP solutions in modern business operations. The market share distribution reveals a significant portion held by established giants, with niche players carving out substantial segments through focused offerings.

ERP Industry Industry Evolution

The evolution of the ERP industry has been a remarkable journey, marked by continuous adaptation and innovation to meet the ever-changing demands of businesses. From its early days of on-premise, monolithic systems designed for large corporations, the ERP market has undergone a profound transformation. The advent of cloud computing has been a pivotal force, democratizing access to sophisticated ERP functionalities for businesses of all sizes. This shift has dramatically accelerated market growth trajectories, with cloud ERP deployments now often outpacing traditional on-premise installations. Technological advancements have been relentless. Initially, ERP systems focused on integrating core business functions like finance, HR, and manufacturing. However, the scope has expanded significantly to encompass sophisticated supply chain management, customer relationship management (CRM), business intelligence, and advanced analytics. The integration of Artificial Intelligence (AI) and Machine Learning (ML) is now a defining characteristic, enabling predictive analytics, automation of routine tasks, and more intelligent decision-making. Consumer demand has also evolved. Businesses now expect ERP solutions to be user-friendly, mobile-accessible, and capable of real-time data processing. The demand for seamless integration with other business applications and a flexible, modular approach to implementation has become paramount. This has led to the rise of modular ERP systems and industry-specific solutions that cater to the unique needs of verticals like BFSI, manufacturing, and retail. The adoption metrics for cloud ERP solutions have seen a compound annual growth rate (CAGR) in the double digits over the past decade, with current projections indicating continued strong growth. The market is projected to reach well over several hundred billion dollars by the end of the forecast period, driven by ongoing digital transformation initiatives across all sectors.

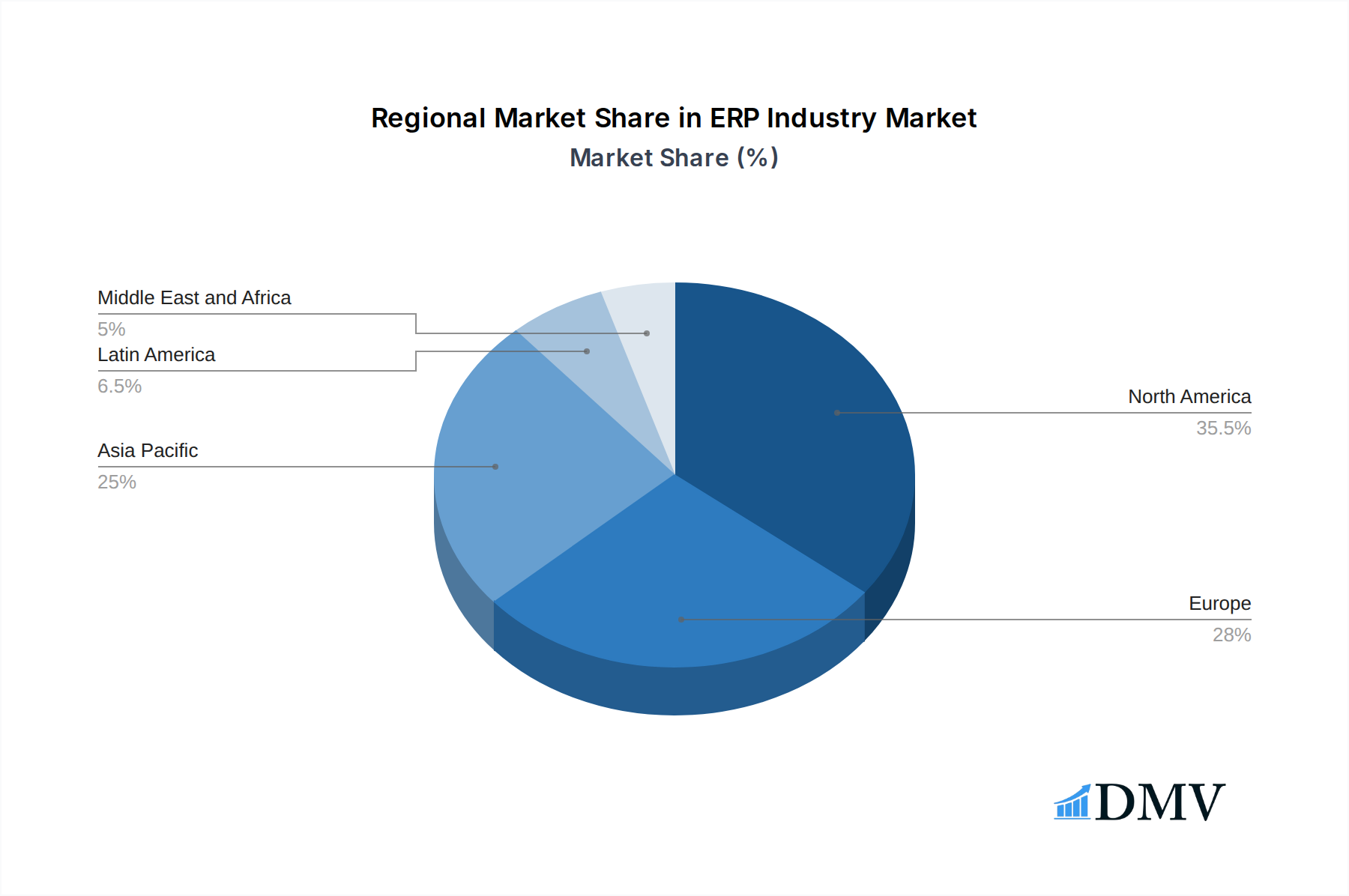

Leading Regions, Countries, or Segments in ERP Industry

The ERP industry exhibits distinct leadership across various geographical regions and business segments, driven by a confluence of economic, technological, and regulatory factors. North America, particularly the United States, consistently emerges as a dominant region due to its mature technological infrastructure, high adoption rate of advanced business solutions, and a substantial concentration of Large Enterprises investing heavily in digital transformation. The significant presence of major ERP vendors like Microsoft Corporation, Oracle Corporation, and SAP SE further solidifies its leadership position.

Within the Offering segment, Solutions generally lead over Services, reflecting the increasing demand for comprehensive, integrated ERP software packages. However, the demand for implementation, customization, and ongoing support Services remains robust, especially for complex deployments in Large Enterprises.

In terms of Function, Finance and Supply Chain management are consistently the most adopted modules, being the core pillars of operational efficiency and profitability for most businesses. HR functions are also critical, with increasing emphasis on talent management and employee experience.

The Deployment landscape is increasingly tilting towards Hybrid models, offering a balance between the scalability and cost-effectiveness of cloud solutions and the control and security offered by On-premise deployments, especially for sensitive data or highly regulated industries. While cloud-native solutions are gaining significant traction, hybrid remains a strategic choice for many organizations.

The Organization Size segment sees both Small and Medium Enterprises (SMEs) and Large Enterprises as significant contributors. SMEs are increasingly adopting cloud-based ERP solutions to gain competitive advantages previously accessible only to larger corporations, often driven by affordability and ease of implementation. Large Enterprises, on the other hand, continue to drive high-value deals with complex, customized implementations tailored to their intricate global operations.

Across Industry Verticals, the BFSI (Banking, Financial Services, and Insurance) sector is a major adopter, driven by stringent regulatory compliance requirements, the need for robust transaction processing, and a focus on enhanced customer service. The Manufacturing sector is another key driver, demanding comprehensive solutions for production planning, inventory management, and supply chain optimization. The Retail and E-commerce sector is rapidly adopting ERP systems to manage complex inventory, omnichannel sales, and customer data.

- Key Drivers in North America:

- High R&D investment in ERP technologies.

- Strong government support for digital transformation initiatives.

- Presence of a large talent pool skilled in ERP implementation and management.

- High disposable income among businesses for technology upgrades.

- Key Drivers in BFSI:

- Mandatory compliance with financial regulations.

- Need for real-time transaction processing and fraud detection.

- Demand for personalized customer experiences and financial advisory services.

- Key Drivers in Manufacturing:

- Pressure to optimize production efficiency and reduce costs.

- Complex supply chain management and global logistics.

- Increasing adoption of Industry 4.0 technologies.

ERP Industry Product Innovations

Recent product innovations in the ERP industry are largely driven by the integration of cutting-edge technologies. Artificial Intelligence (AI) and Machine Learning (ML) are revolutionizing ERP capabilities, enabling predictive analytics for demand forecasting, intelligent automation of repetitive tasks, and personalized user experiences. For instance, Microsoft's Dynamics 365 Copilot empowers users with AI-driven insights and task automation across various business functions. Oracle's continued investment in its Fusion Cloud ERP, exemplified by its partnership with Mastercard, showcases innovations in automating complex financial transactions and enhancing B2B payment processes. These advancements translate to improved operational efficiency, reduced errors, and a more agile business environment. Unique selling propositions now include enhanced interoperability, robust cybersecurity features, and adaptable, modular architectures that allow businesses to scale and customize their ERP solutions as their needs evolve.

Propelling Factors for ERP Industry Growth

Several key factors are propelling the ERP industry's growth. The accelerating pace of digital transformation across all business sectors is a primary driver, as organizations seek to streamline operations, improve decision-making, and enhance customer experiences. The increasing adoption of cloud computing offers scalable, flexible, and cost-effective ERP solutions, broadening market access. Furthermore, the rise of AI and machine learning is enabling more intelligent automation, predictive analytics, and personalized user interactions, adding significant value. Industry-specific ERP solutions are also catering to the unique needs of verticals, driving adoption. Economic recovery and business expansion initiatives post-pandemic are further fueling investment in robust enterprise systems.

Obstacles in the ERP Industry Market

Despite its robust growth, the ERP industry faces several obstacles. The high cost of implementation, particularly for comprehensive solutions in Large Enterprises, can be a significant barrier. Navigating complex regulatory compliance, especially in highly regulated industries like BFSI and healthcare, requires substantial investment and expertise. The inherent complexity of integrating ERP systems with existing legacy infrastructure and diverse business processes can lead to project delays and cost overruns. Furthermore, a shortage of skilled ERP professionals for implementation and ongoing management poses a challenge. Data security and privacy concerns, especially with the increasing reliance on cloud-based solutions, also require continuous attention and investment.

Future Opportunities in ERP Industry

The ERP industry is poised for significant future opportunities. The ongoing expansion of cloud-native ERP solutions, offering enhanced scalability and accessibility, presents a substantial growth avenue. The further integration of advanced AI and machine learning capabilities for predictive analytics, hyper-automation, and personalized user experiences will unlock new levels of efficiency and business insight. Emerging markets, particularly in developing economies, represent untapped potential as businesses in these regions increasingly adopt digital technologies. The growing demand for industry-specific ERP solutions tailored to niche verticals and the increasing focus on sustainability and ESG (Environmental, Social, and Governance) reporting integrated within ERP systems also offer promising avenues for innovation and market expansion.

Major Players in the ERP Industry Ecosystem

- Infor Inc

- Adobe

- FIS

- Microsoft Corporation

- Sage Group PLC

- Constellation Software

- Intuit

- Oracle Corporation

- SAP SE

- IBM

Key Developments in ERP Industry Industry

- September 2023: Oracle and Mastercard announced a new partnership to help enterprise customers automate end-to-end business-to-business (B2B) payment transactions. This collaboration connects Oracle Fusion Cloud Enterprise Resource Planning (ERP) directly with banks, streamlining and automating B2B finance and payment processes. The partnership leverages Mastercard’s virtual card platform to expedite financial transactions for Oracle’s corporate customers and enable banks to offer value-added services within Oracle Cloud ERP, addressing the challenge of disparate data, systems, and processes hindering efficient inter-company transactions.

- March 2023: Microsoft Corporation introduced Microsoft Dynamics 365 Copilot, positioning it as the world's first copilot in CRM and ERP. This innovation brings next-generation AI to every line of business, aiming to reduce repetitive tasks for workers, aligning with a survey indicating that nearly 9 out of 10 workers hope to use AI for this purpose. Dynamics 365 Copilot empowers workers across sales, service, marketing, operations, and supply chain roles with AI tools, allowing them to focus more on valuable aspects of their jobs.

Strategic ERP Industry Market Forecast

The strategic ERP industry market forecast anticipates robust growth, primarily driven by the ongoing digital transformation imperative across global businesses. The continued migration towards cloud-based ERP solutions will fuel market expansion, offering greater flexibility, scalability, and cost-effectiveness. The integration of advanced AI and machine learning capabilities is projected to revolutionize operational efficiency, predictive analytics, and personalized user experiences, becoming a key differentiator. Emerging markets present significant untapped potential, as businesses in these regions increasingly embrace modern enterprise solutions. Furthermore, the growing demand for industry-specific ERP modules and the increasing focus on sustainability reporting integrated within ERP systems will open new avenues for market penetration and innovation. The market is expected to witness sustained double-digit CAGR, reaching substantial valuations by the end of the forecast period.

ERP Industry Segmentation

-

1. Offering

- 1.1. Solutions

- 1.2. Services

-

2. Function

- 2.1. HR

- 2.2. Supply Chain

- 2.3. Finance

- 2.4. Marketing

- 2.5. Other Functions

-

3. Deployment

- 3.1. On-premise

- 3.2. Hybrid

-

4. Organization Size

- 4.1. Small and Medium Enterprises

- 4.2. Large Enterprises

-

5. Industry Verticals

-

5.1. BFSI

- 5.1.1. Use Cases

- 5.2. IT and Telecom

- 5.3. Government

- 5.4. Retail and E-commerce

- 5.5. Manufacturing

- 5.6. Oil, Gas, and Energy

- 5.7. Other Industry Verticals

-

5.1. BFSI

ERP Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

ERP Industry Regional Market Share

Geographic Coverage of ERP Industry

ERP Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.76% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Offering

- 5.1.1. Solutions

- 5.1.2. Services

- 5.2. Market Analysis, Insights and Forecast - by Function

- 5.2.1. HR

- 5.2.2. Supply Chain

- 5.2.3. Finance

- 5.2.4. Marketing

- 5.2.5. Other Functions

- 5.3. Market Analysis, Insights and Forecast - by Deployment

- 5.3.1. On-premise

- 5.3.2. Hybrid

- 5.4. Market Analysis, Insights and Forecast - by Organization Size

- 5.4.1. Small and Medium Enterprises

- 5.4.2. Large Enterprises

- 5.5. Market Analysis, Insights and Forecast - by Industry Verticals

- 5.5.1. BFSI

- 5.5.1.1. Use Cases

- 5.5.2. IT and Telecom

- 5.5.3. Government

- 5.5.4. Retail and E-commerce

- 5.5.5. Manufacturing

- 5.5.6. Oil, Gas, and Energy

- 5.5.7. Other Industry Verticals

- 5.5.1. BFSI

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. North America

- 5.6.2. Europe

- 5.6.3. Asia Pacific

- 5.6.4. Latin America

- 5.6.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Offering

- 6. Global ERP Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Offering

- 6.1.1. Solutions

- 6.1.2. Services

- 6.2. Market Analysis, Insights and Forecast - by Function

- 6.2.1. HR

- 6.2.2. Supply Chain

- 6.2.3. Finance

- 6.2.4. Marketing

- 6.2.5. Other Functions

- 6.3. Market Analysis, Insights and Forecast - by Deployment

- 6.3.1. On-premise

- 6.3.2. Hybrid

- 6.4. Market Analysis, Insights and Forecast - by Organization Size

- 6.4.1. Small and Medium Enterprises

- 6.4.2. Large Enterprises

- 6.5. Market Analysis, Insights and Forecast - by Industry Verticals

- 6.5.1. BFSI

- 6.5.1.1. Use Cases

- 6.5.2. IT and Telecom

- 6.5.3. Government

- 6.5.4. Retail and E-commerce

- 6.5.5. Manufacturing

- 6.5.6. Oil, Gas, and Energy

- 6.5.7. Other Industry Verticals

- 6.5.1. BFSI

- 6.1. Market Analysis, Insights and Forecast - by Offering

- 7. North America ERP Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Offering

- 7.1.1. Solutions

- 7.1.2. Services

- 7.2. Market Analysis, Insights and Forecast - by Function

- 7.2.1. HR

- 7.2.2. Supply Chain

- 7.2.3. Finance

- 7.2.4. Marketing

- 7.2.5. Other Functions

- 7.3. Market Analysis, Insights and Forecast - by Deployment

- 7.3.1. On-premise

- 7.3.2. Hybrid

- 7.4. Market Analysis, Insights and Forecast - by Organization Size

- 7.4.1. Small and Medium Enterprises

- 7.4.2. Large Enterprises

- 7.5. Market Analysis, Insights and Forecast - by Industry Verticals

- 7.5.1. BFSI

- 7.5.1.1. Use Cases

- 7.5.2. IT and Telecom

- 7.5.3. Government

- 7.5.4. Retail and E-commerce

- 7.5.5. Manufacturing

- 7.5.6. Oil, Gas, and Energy

- 7.5.7. Other Industry Verticals

- 7.5.1. BFSI

- 7.1. Market Analysis, Insights and Forecast - by Offering

- 8. Europe ERP Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Offering

- 8.1.1. Solutions

- 8.1.2. Services

- 8.2. Market Analysis, Insights and Forecast - by Function

- 8.2.1. HR

- 8.2.2. Supply Chain

- 8.2.3. Finance

- 8.2.4. Marketing

- 8.2.5. Other Functions

- 8.3. Market Analysis, Insights and Forecast - by Deployment

- 8.3.1. On-premise

- 8.3.2. Hybrid

- 8.4. Market Analysis, Insights and Forecast - by Organization Size

- 8.4.1. Small and Medium Enterprises

- 8.4.2. Large Enterprises

- 8.5. Market Analysis, Insights and Forecast - by Industry Verticals

- 8.5.1. BFSI

- 8.5.1.1. Use Cases

- 8.5.2. IT and Telecom

- 8.5.3. Government

- 8.5.4. Retail and E-commerce

- 8.5.5. Manufacturing

- 8.5.6. Oil, Gas, and Energy

- 8.5.7. Other Industry Verticals

- 8.5.1. BFSI

- 8.1. Market Analysis, Insights and Forecast - by Offering

- 9. Asia Pacific ERP Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Offering

- 9.1.1. Solutions

- 9.1.2. Services

- 9.2. Market Analysis, Insights and Forecast - by Function

- 9.2.1. HR

- 9.2.2. Supply Chain

- 9.2.3. Finance

- 9.2.4. Marketing

- 9.2.5. Other Functions

- 9.3. Market Analysis, Insights and Forecast - by Deployment

- 9.3.1. On-premise

- 9.3.2. Hybrid

- 9.4. Market Analysis, Insights and Forecast - by Organization Size

- 9.4.1. Small and Medium Enterprises

- 9.4.2. Large Enterprises

- 9.5. Market Analysis, Insights and Forecast - by Industry Verticals

- 9.5.1. BFSI

- 9.5.1.1. Use Cases

- 9.5.2. IT and Telecom

- 9.5.3. Government

- 9.5.4. Retail and E-commerce

- 9.5.5. Manufacturing

- 9.5.6. Oil, Gas, and Energy

- 9.5.7. Other Industry Verticals

- 9.5.1. BFSI

- 9.1. Market Analysis, Insights and Forecast - by Offering

- 10. Latin America ERP Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Offering

- 10.1.1. Solutions

- 10.1.2. Services

- 10.2. Market Analysis, Insights and Forecast - by Function

- 10.2.1. HR

- 10.2.2. Supply Chain

- 10.2.3. Finance

- 10.2.4. Marketing

- 10.2.5. Other Functions

- 10.3. Market Analysis, Insights and Forecast - by Deployment

- 10.3.1. On-premise

- 10.3.2. Hybrid

- 10.4. Market Analysis, Insights and Forecast - by Organization Size

- 10.4.1. Small and Medium Enterprises

- 10.4.2. Large Enterprises

- 10.5. Market Analysis, Insights and Forecast - by Industry Verticals

- 10.5.1. BFSI

- 10.5.1.1. Use Cases

- 10.5.2. IT and Telecom

- 10.5.3. Government

- 10.5.4. Retail and E-commerce

- 10.5.5. Manufacturing

- 10.5.6. Oil, Gas, and Energy

- 10.5.7. Other Industry Verticals

- 10.5.1. BFSI

- 10.1. Market Analysis, Insights and Forecast - by Offering

- 11. Middle East and Africa ERP Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Offering

- 11.1.1. Solutions

- 11.1.2. Services

- 11.2. Market Analysis, Insights and Forecast - by Function

- 11.2.1. HR

- 11.2.2. Supply Chain

- 11.2.3. Finance

- 11.2.4. Marketing

- 11.2.5. Other Functions

- 11.3. Market Analysis, Insights and Forecast - by Deployment

- 11.3.1. On-premise

- 11.3.2. Hybrid

- 11.4. Market Analysis, Insights and Forecast - by Organization Size

- 11.4.1. Small and Medium Enterprises

- 11.4.2. Large Enterprises

- 11.5. Market Analysis, Insights and Forecast - by Industry Verticals

- 11.5.1. BFSI

- 11.5.1.1. Use Cases

- 11.5.2. IT and Telecom

- 11.5.3. Government

- 11.5.4. Retail and E-commerce

- 11.5.5. Manufacturing

- 11.5.6. Oil, Gas, and Energy

- 11.5.7. Other Industry Verticals

- 11.5.1. BFSI

- 11.1. Market Analysis, Insights and Forecast - by Offering

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Infor Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Adobe

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 FIS

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Microsoft Corporation

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Sage Group PLC*List Not Exhaustive

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Constellation Software

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Intuit

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Oracle Corporation

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 SAP SE

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 IBM

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Infor Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global ERP Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America ERP Industry Revenue (Million), by Offering 2025 & 2033

- Figure 3: North America ERP Industry Revenue Share (%), by Offering 2025 & 2033

- Figure 4: North America ERP Industry Revenue (Million), by Function 2025 & 2033

- Figure 5: North America ERP Industry Revenue Share (%), by Function 2025 & 2033

- Figure 6: North America ERP Industry Revenue (Million), by Deployment 2025 & 2033

- Figure 7: North America ERP Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 8: North America ERP Industry Revenue (Million), by Organization Size 2025 & 2033

- Figure 9: North America ERP Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 10: North America ERP Industry Revenue (Million), by Industry Verticals 2025 & 2033

- Figure 11: North America ERP Industry Revenue Share (%), by Industry Verticals 2025 & 2033

- Figure 12: North America ERP Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: North America ERP Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe ERP Industry Revenue (Million), by Offering 2025 & 2033

- Figure 15: Europe ERP Industry Revenue Share (%), by Offering 2025 & 2033

- Figure 16: Europe ERP Industry Revenue (Million), by Function 2025 & 2033

- Figure 17: Europe ERP Industry Revenue Share (%), by Function 2025 & 2033

- Figure 18: Europe ERP Industry Revenue (Million), by Deployment 2025 & 2033

- Figure 19: Europe ERP Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 20: Europe ERP Industry Revenue (Million), by Organization Size 2025 & 2033

- Figure 21: Europe ERP Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 22: Europe ERP Industry Revenue (Million), by Industry Verticals 2025 & 2033

- Figure 23: Europe ERP Industry Revenue Share (%), by Industry Verticals 2025 & 2033

- Figure 24: Europe ERP Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Europe ERP Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific ERP Industry Revenue (Million), by Offering 2025 & 2033

- Figure 27: Asia Pacific ERP Industry Revenue Share (%), by Offering 2025 & 2033

- Figure 28: Asia Pacific ERP Industry Revenue (Million), by Function 2025 & 2033

- Figure 29: Asia Pacific ERP Industry Revenue Share (%), by Function 2025 & 2033

- Figure 30: Asia Pacific ERP Industry Revenue (Million), by Deployment 2025 & 2033

- Figure 31: Asia Pacific ERP Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 32: Asia Pacific ERP Industry Revenue (Million), by Organization Size 2025 & 2033

- Figure 33: Asia Pacific ERP Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 34: Asia Pacific ERP Industry Revenue (Million), by Industry Verticals 2025 & 2033

- Figure 35: Asia Pacific ERP Industry Revenue Share (%), by Industry Verticals 2025 & 2033

- Figure 36: Asia Pacific ERP Industry Revenue (Million), by Country 2025 & 2033

- Figure 37: Asia Pacific ERP Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Latin America ERP Industry Revenue (Million), by Offering 2025 & 2033

- Figure 39: Latin America ERP Industry Revenue Share (%), by Offering 2025 & 2033

- Figure 40: Latin America ERP Industry Revenue (Million), by Function 2025 & 2033

- Figure 41: Latin America ERP Industry Revenue Share (%), by Function 2025 & 2033

- Figure 42: Latin America ERP Industry Revenue (Million), by Deployment 2025 & 2033

- Figure 43: Latin America ERP Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 44: Latin America ERP Industry Revenue (Million), by Organization Size 2025 & 2033

- Figure 45: Latin America ERP Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 46: Latin America ERP Industry Revenue (Million), by Industry Verticals 2025 & 2033

- Figure 47: Latin America ERP Industry Revenue Share (%), by Industry Verticals 2025 & 2033

- Figure 48: Latin America ERP Industry Revenue (Million), by Country 2025 & 2033

- Figure 49: Latin America ERP Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East and Africa ERP Industry Revenue (Million), by Offering 2025 & 2033

- Figure 51: Middle East and Africa ERP Industry Revenue Share (%), by Offering 2025 & 2033

- Figure 52: Middle East and Africa ERP Industry Revenue (Million), by Function 2025 & 2033

- Figure 53: Middle East and Africa ERP Industry Revenue Share (%), by Function 2025 & 2033

- Figure 54: Middle East and Africa ERP Industry Revenue (Million), by Deployment 2025 & 2033

- Figure 55: Middle East and Africa ERP Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 56: Middle East and Africa ERP Industry Revenue (Million), by Organization Size 2025 & 2033

- Figure 57: Middle East and Africa ERP Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 58: Middle East and Africa ERP Industry Revenue (Million), by Industry Verticals 2025 & 2033

- Figure 59: Middle East and Africa ERP Industry Revenue Share (%), by Industry Verticals 2025 & 2033

- Figure 60: Middle East and Africa ERP Industry Revenue (Million), by Country 2025 & 2033

- Figure 61: Middle East and Africa ERP Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global ERP Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 2: Global ERP Industry Revenue Million Forecast, by Function 2020 & 2033

- Table 3: Global ERP Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 4: Global ERP Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 5: Global ERP Industry Revenue Million Forecast, by Industry Verticals 2020 & 2033

- Table 6: Global ERP Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 7: Global ERP Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 8: Global ERP Industry Revenue Million Forecast, by Function 2020 & 2033

- Table 9: Global ERP Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 10: Global ERP Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 11: Global ERP Industry Revenue Million Forecast, by Industry Verticals 2020 & 2033

- Table 12: Global ERP Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Global ERP Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 14: Global ERP Industry Revenue Million Forecast, by Function 2020 & 2033

- Table 15: Global ERP Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 16: Global ERP Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 17: Global ERP Industry Revenue Million Forecast, by Industry Verticals 2020 & 2033

- Table 18: Global ERP Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 19: Global ERP Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 20: Global ERP Industry Revenue Million Forecast, by Function 2020 & 2033

- Table 21: Global ERP Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 22: Global ERP Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 23: Global ERP Industry Revenue Million Forecast, by Industry Verticals 2020 & 2033

- Table 24: Global ERP Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 25: Global ERP Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 26: Global ERP Industry Revenue Million Forecast, by Function 2020 & 2033

- Table 27: Global ERP Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 28: Global ERP Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 29: Global ERP Industry Revenue Million Forecast, by Industry Verticals 2020 & 2033

- Table 30: Global ERP Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 31: Global ERP Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 32: Global ERP Industry Revenue Million Forecast, by Function 2020 & 2033

- Table 33: Global ERP Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 34: Global ERP Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 35: Global ERP Industry Revenue Million Forecast, by Industry Verticals 2020 & 2033

- Table 36: Global ERP Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the ERP Industry?

The projected CAGR is approximately 9.76%.

2. Which companies are prominent players in the ERP Industry?

Key companies in the market include Infor Inc, Adobe, FIS, Microsoft Corporation, Sage Group PLC*List Not Exhaustive, Constellation Software, Intuit, Oracle Corporation, SAP SE, IBM.

3. What are the main segments of the ERP Industry?

The market segments include Offering, Function, Deployment, Organization Size, Industry Verticals.

4. Can you provide details about the market size?

The market size is estimated to be USD 65.25 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Demand for Customer Centric Approach; Rapid Increase in Cloud and Mobile Application; Increase in Adoption of Data-intensive Approach and Decisions.

6. What are the notable trends driving market growth?

Large Enterprises to Witness Highest Market Growth.

7. Are there any restraints impacting market growth?

; Lack of End-to-end Solutions; Lack of Techniques that allow Seamless IT systems and Application Integration.

8. Can you provide examples of recent developments in the market?

September 2023 - Oracle and Mastercard announced a new partnership to help enterprise customers automate end-to-end business-to-business (B2B) payment transactions. The partnership lets Oracle directly connect Oracle Fusion Cloud Enterprise Resource Planning (ERP) with banks to streamline and automate the B2B finance and payment process. Moreover, many companies desire simpler commercial payment experiences. Yet, disparate data, systems, and processes across the ecosystem hinder enterprises and their suppliers from transacting efficiently. To address these challenges and enable organizations to connect and share information across all trading parties, Oracle aims to leverage Mastercard’s innovative virtual card platform to help expedite end-to-end financial transactions for Oracle’s corporate customers and enable banks to offer value-added services inside Oracle Cloud ERP.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "ERP Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the ERP Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the ERP Industry?

To stay informed about further developments, trends, and reports in the ERP Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence