Key Insights

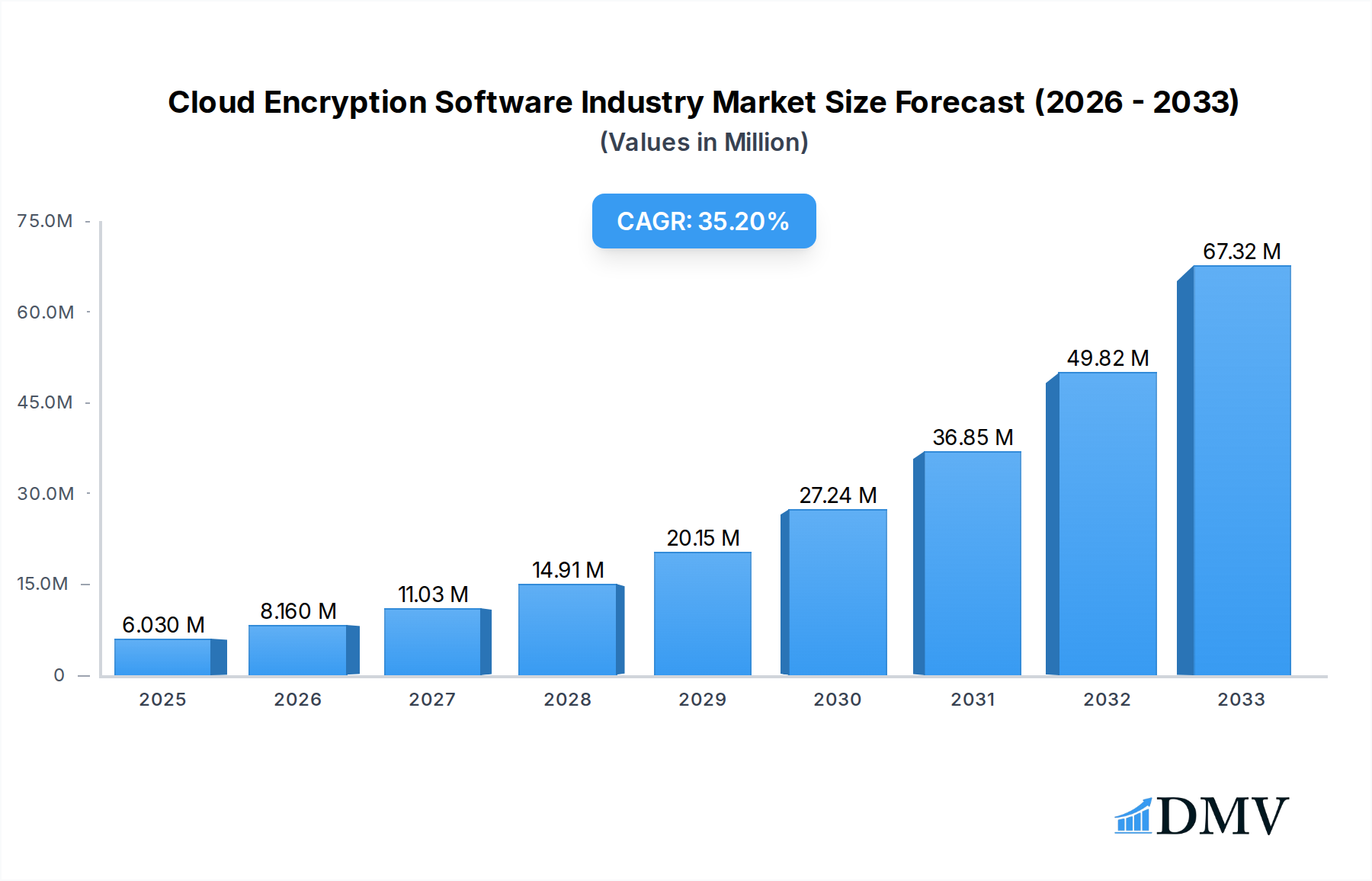

The global Cloud Encryption Software market is experiencing robust expansion, projected to reach $6.03 Million by 2025, driven by an exceptional CAGR of 35.23% over the forecast period of 2025-2033. This significant growth is primarily fueled by the escalating adoption of cloud services across diverse industries and the increasing imperative for robust data security and privacy. Organizations of all sizes, from Small and Medium-sized Enterprises (SMEs) to Large Enterprises, are prioritizing cloud encryption solutions to protect sensitive information from ever-evolving cyber threats. The market's trajectory is further bolstered by the growing awareness of regulatory compliance requirements, such as GDPR and CCPA, which mandate stringent data protection measures. Professional services and managed services are key offerings within this segment, assisting businesses in implementing and managing complex encryption strategies effectively.

Cloud Encryption Software Industry Market Size (In Million)

The Cloud Encryption Software market is characterized by a dynamic interplay of drivers and restraints. Key growth drivers include the burgeoning demand for data-at-rest and data-in-transit encryption, the proliferation of sophisticated cyberattacks, and the increasing adoption of hybrid and multi-cloud environments. Industry verticals like IT & Telecommunication, BFSI, Healthcare, and Entertainment & Media are leading the charge in adopting these solutions due to the highly sensitive nature of their data. While the market presents immense opportunities, restraints such as the complexity of integration, potential performance overheads, and the scarcity of skilled cybersecurity professionals could pose challenges. However, ongoing advancements in encryption technologies, including advancements in key management and cryptographic algorithms, are continuously mitigating these challenges and shaping the market's future landscape. Prominent players like Sophos, Hitachi Vantara, and Google LLC are instrumental in driving innovation and market expansion through their comprehensive offerings and strategic partnerships.

Cloud Encryption Software Industry Company Market Share

The global cloud encryption software market is characterized by a dynamic and evolving landscape, driven by escalating cybersecurity threats and stringent data privacy regulations. Market concentration remains moderately fragmented, with a mix of established cybersecurity giants and specialized cloud security vendors vying for dominance. Innovation is a key differentiator, with companies actively investing in advanced encryption techniques, key management solutions, and seamless integration with hybrid and multi-cloud environments. Regulatory landscapes, including GDPR, CCPA, and HIPAA, are powerful catalysts, compelling organizations across all verticals to adopt robust cloud encryption solutions to ensure compliance and protect sensitive data. Substitute products, such as on-premise encryption solutions, are gradually losing ground to the flexibility and scalability offered by cloud-based alternatives. End-user profiles span across Small and Medium-sized Enterprises (SMEs) seeking cost-effective and user-friendly solutions to Large Enterprises requiring comprehensive, enterprise-grade security and granular control. Merger and acquisition (M&A) activities are prevalent as larger players aim to expand their cloud security portfolios and acquire innovative technologies. Notable M&A deal values in recent years have ranged from tens of millions to hundreds of millions of dollars, reflecting the strategic importance of this sector. Market share distribution shows a gradual shift towards vendors offering comprehensive encryption-as-a-service models and robust key management capabilities.

Cloud Encryption Software Industry Industry Evolution

The cloud encryption software industry has witnessed a significant evolutionary journey, transforming from basic data protection mechanisms to sophisticated, integrated security ecosystems. Over the historical period (2019–2024), the market experienced steady growth, fueled by the increasing adoption of cloud computing services by businesses of all sizes. Early adoption was primarily driven by the need for basic data-at-rest and data-in-transit encryption. However, as cloud infrastructure matured and data breaches became more frequent and sophisticated, the demand shifted towards more advanced security features.

During the base year (2025), the market is projected to reach an estimated value of $XX Billion. The study period (2019–2033) encapsulates a transformative phase where cloud encryption software has become an indispensable component of any robust cybersecurity strategy. The forecast period (2025–2033) is anticipated to see accelerated growth, with an estimated Compound Annual Growth Rate (CAGR) of XX%. This surge will be propelled by several key factors:

- Technological Advancements: The evolution of encryption algorithms, including advancements in homomorphic encryption and post-quantum cryptography, is enhancing data security even while data is being processed. The rise of client-side encryption, where data is encrypted on the user's device before being uploaded to the cloud, has gained significant traction. Solutions like Utimaco's u.trust LAN Crypt Cloud exemplify this trend, offering easy-to-use file encryption as-a-service to protect sensitive data regardless of its storage location.

- Shifting Consumer Demands: End-users, particularly in regulated industries like healthcare and finance, are increasingly demanding verifiable data security and privacy. This has led to a greater emphasis on transparent encryption processes, robust key management, and granular access controls. The demand for encryption solutions that seamlessly integrate with existing cloud platforms (e.g., AWS, Azure, Google Cloud) and offer simplified management interfaces is also on the rise.

- Regulatory Pressures: A continuous stream of evolving data privacy regulations globally has been a primary growth driver. Organizations are compelled to invest in cloud encryption software to meet compliance requirements, avoid hefty fines, and maintain customer trust.

- Hybrid and Multi-Cloud Adoption: The widespread adoption of hybrid and multi-cloud strategies by enterprises necessitates sophisticated encryption solutions capable of managing data security across diverse environments. This has spurred innovation in unified key management and cross-platform encryption capabilities. The recent announcement by HPE regarding new solutions across HPE GreenLake, including HPE GreenLake Block Storage for Amazon Web Services (AWS), underscores the industry's focus on simplifying data and workload management across hybrid cloud environments, including robust storage encryption.

The market's evolution is also marked by increasing specialization, with vendors offering tailored solutions for specific industry verticals and organization sizes. The integration of encryption with other security functions, such as data loss prevention (DLP) and identity and access management (IAM), is becoming a standard offering. The trajectory clearly indicates a future where cloud encryption software is not merely a security tool but a foundational element of cloud infrastructure, enabling businesses to leverage the full potential of cloud computing securely and compliantly.

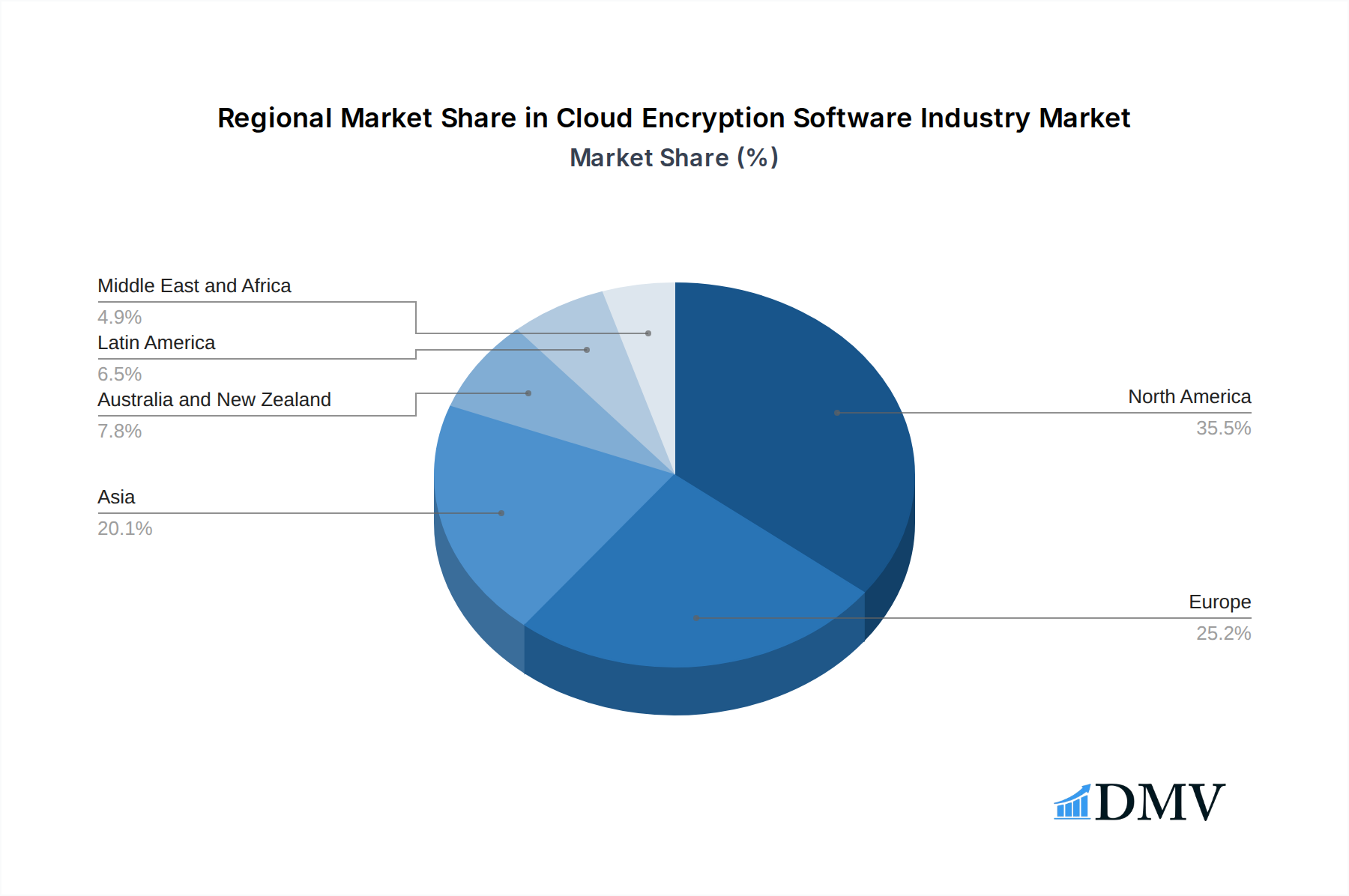

Leading Regions, Countries, or Segments in Cloud Encryption Software Industry

North America currently leads the global cloud encryption software market, driven by a confluence of factors that foster rapid adoption and innovation. The region's advanced technological infrastructure, high concentration of large enterprises, and stringent regulatory environment are key contributors to its dominance. Specifically, the United States, with its thriving tech industry and significant investments in cybersecurity, stands out as a primary market.

Within North America, the dominance can be attributed to several key drivers across various segments:

Organization Size:

- Large Enterprises: These organizations are at the forefront of cloud encryption adoption due to their vast datasets, complex IT infrastructures, and greater exposure to sophisticated cyber threats. Their ability to invest in comprehensive, enterprise-grade solutions, including professional and managed services, solidifies their impact. Companies like Google LLC, Hewlett Packard Enterprise, and Symantec Corporation are key players catering to this segment.

- SMEs: While historically slower to adopt advanced security solutions, SMEs are increasingly recognizing the necessity of cloud encryption due to the escalating threat landscape and the growing availability of user-friendly and cost-effective solutions. The affordability and scalability of cloud-based encryption software are making it accessible for this segment.

Service:

- Managed Services: The growing complexity of cloud security and the shortage of skilled cybersecurity professionals have propelled the demand for managed encryption services. Organizations are outsourcing the management and monitoring of their encryption solutions to specialized providers, ensuring continuous protection and compliance. This trend is particularly strong in North America.

- Professional Services: Implementation, configuration, and ongoing support services remain critical for large enterprises to ensure optimal deployment and integration of cloud encryption software with their existing systems.

Industry Vertical:

- IT & Telecommunication: This sector, being a primary adopter of cloud technologies, also leads in the demand for advanced cloud encryption to secure their own infrastructure and customer data.

- BFSI (Banking, Financial Services, and Insurance): Highly regulated and dealing with sensitive financial data, the BFSI sector is a significant driver of cloud encryption adoption. Compliance with regulations like PCI DSS and stringent data privacy laws necessitates robust encryption solutions.

- Healthcare: The increasing digitization of health records and the sensitive nature of Protected Health Information (PHI) make healthcare a critical vertical for cloud encryption. HIPAA compliance mandates strong data protection measures.

- Retail: With the rise of e-commerce and the increasing volume of customer payment data stored and processed in the cloud, the retail sector is also a key adopter of cloud encryption solutions.

The dominance of North America is further amplified by the proactive stance of its governments and regulatory bodies in mandating data protection standards. Investments in research and development of advanced encryption technologies by North American companies, such as Sophos and Trend Micro, also contribute to the region's leadership. The presence of major cloud providers and a mature cybersecurity ecosystem creates a fertile ground for the growth and adoption of cloud encryption software. While other regions like Europe and Asia-Pacific are rapidly growing, North America's established infrastructure, regulatory enforcement, and high adoption rates currently cement its position as the leading region in the cloud encryption software industry.

Cloud Encryption Software Industry Product Innovations

Product innovation in the cloud encryption software industry is sharply focused on enhancing data security, user experience, and integration capabilities. Recent advancements include the development of intelligent key management systems that automate key rotation and lifecycle management, significantly reducing administrative overhead. Client-side encryption solutions, exemplified by Utimaco's u.trust LAN Crypt Cloud, are gaining prominence, ensuring data remains protected at the point of origin before it even enters the cloud, thereby offering unparalleled privacy. Furthermore, solutions are increasingly offering seamless integration with hybrid and multi-cloud environments, with HPE's GreenLake Block Storage for AWS showcasing advancements in managing block storage across these diverse infrastructures. Performance metrics are witnessing improvements through optimized algorithms and hardware acceleration, minimizing any potential latency impact on data access. The unique selling proposition often lies in the combination of robust encryption protocols, user-friendly interfaces, comprehensive compliance reporting, and flexible deployment options, catering to the evolving needs of organizations seeking resilient cloud data protection.

Propelling Factors for Cloud Encryption Software Industry Growth

The growth of the cloud encryption software industry is propelled by a powerful confluence of factors. The relentless surge in cyber threats, including ransomware and sophisticated data breaches, necessitates stronger data protection. The expanding adoption of cloud computing services across all business sizes and verticals fuels the demand for secure cloud storage and processing. Stringent global data privacy regulations, such as GDPR and CCPA, impose significant compliance requirements, making encryption a non-negotiable element. Furthermore, the increasing emphasis on data sovereignty and the need to protect sensitive information in multi-cloud and hybrid cloud environments are driving innovation and adoption. The evolving threat landscape, coupled with the increasing value of data, ensures a sustained demand for advanced cloud encryption solutions.

Obstacles in the Cloud Encryption Software Industry Market

Despite robust growth, the cloud encryption software industry faces several obstacles. The complexity of implementing and managing encryption, particularly key management, can be a significant barrier for SMEs with limited IT resources. The perceived cost of advanced encryption solutions, though decreasing, can still be a deterrent for some organizations. Furthermore, the evolving nature of encryption standards and the emergence of new threats require continuous investment in updates and training, which can strain budgets. Integration challenges with existing legacy systems and diverse cloud platforms can also slow down adoption. Finally, a lack of widespread cybersecurity expertise can lead to misconfigurations, undermining the effectiveness of even the best encryption software, thus creating a demand for user-friendly and expertly managed solutions.

Future Opportunities in Cloud Encryption Software Industry

The future of cloud encryption software is ripe with opportunities. The expanding adoption of AI and machine learning in cybersecurity presents a significant avenue for developing intelligent encryption solutions that can proactively detect and respond to threats. The ongoing growth of the Internet of Things (IoT) will create a massive demand for securing vast amounts of data generated by connected devices. The development and widespread adoption of post-quantum cryptography will be crucial for protecting data against future quantum computing threats, opening up a new frontier for encryption innovation. Furthermore, the increasing demand for zero-trust security architectures will drive the integration of encryption as a fundamental layer of data protection. Emerging markets and the continuous need for regulatory compliance will also continue to fuel market expansion.

Major Players in the Cloud Encryption Software Industry Ecosystem

- Sophos

- Hitachi Vantara

- Google LLC

- Voltage Security Inc

- Trend Micro

- Ciphercloud

- Hewlett Packard Enterprise

- Safenet

- Boxcryptor

- CyberArk

- Symantec Corporation

Key Developments in Cloud Encryption Software Industry Industry

- May 2024 - HPE announced new solutions across the HPE GreenLake cloud to simplify how enterprises manage and optimize their storage, data and workloads across on-prem and public cloud environments. New or expanded offerings include HPE GreenLake Block Storage for Amazon Web Services (AWS), a new software-defined storage offering to seamlessly manage block storage across hybrid cloud environments.

- November 2023 - Utimaco launch of its new easy-to-use file encryption as-a-service management solution, u.trust LAN Crypt Cloud, to protect sensitive and business-critical data against unauthorized access. Client-side encryption ensures that data remains protected, regardless of its storage location, whether on-premises or in the cloud.

Strategic Cloud Encryption Software Industry Market Forecast

The strategic forecast for the cloud encryption software market indicates sustained robust growth driven by an increasing reliance on cloud services and a heightened awareness of cybersecurity imperatives. The continuous evolution of cyber threats, coupled with stringent regulatory landscapes worldwide, will act as a primary catalyst, compelling organizations to invest in advanced encryption solutions. Opportunities in emerging technologies like AI-driven encryption and solutions for the burgeoning IoT ecosystem will further shape market dynamics. The market's future is characterized by a strong emphasis on integrated security platforms, user-friendly management interfaces, and comprehensive data protection across hybrid and multi-cloud environments, ensuring that cloud encryption software remains an indispensable component of modern digital infrastructure.

Cloud Encryption Software Industry Segmentation

-

1. Organization Size

- 1.1. SMEs

- 1.2. Large Enterprises

-

2. Service

- 2.1. Professional Services

- 2.2. Managed Services

-

3. Industry Vertical

- 3.1. IT & Telecommunication

- 3.2. BFSI

- 3.3. Healthcare

- 3.4. Entertainment and Media

- 3.5. Retail

- 3.6. Education

- 3.7. Other Industry Verticals

Cloud Encryption Software Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia

- 4. Australia and New Zealand

- 5. Latin America

- 6. Middle East and Africa

Cloud Encryption Software Industry Regional Market Share

Geographic Coverage of Cloud Encryption Software Industry

Cloud Encryption Software Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 35.23% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Organization Size

- 5.1.1. SMEs

- 5.1.2. Large Enterprises

- 5.2. Market Analysis, Insights and Forecast - by Service

- 5.2.1. Professional Services

- 5.2.2. Managed Services

- 5.3. Market Analysis, Insights and Forecast - by Industry Vertical

- 5.3.1. IT & Telecommunication

- 5.3.2. BFSI

- 5.3.3. Healthcare

- 5.3.4. Entertainment and Media

- 5.3.5. Retail

- 5.3.6. Education

- 5.3.7. Other Industry Verticals

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia

- 5.4.4. Australia and New Zealand

- 5.4.5. Latin America

- 5.4.6. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Organization Size

- 6. Global Cloud Encryption Software Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Organization Size

- 6.1.1. SMEs

- 6.1.2. Large Enterprises

- 6.2. Market Analysis, Insights and Forecast - by Service

- 6.2.1. Professional Services

- 6.2.2. Managed Services

- 6.3. Market Analysis, Insights and Forecast - by Industry Vertical

- 6.3.1. IT & Telecommunication

- 6.3.2. BFSI

- 6.3.3. Healthcare

- 6.3.4. Entertainment and Media

- 6.3.5. Retail

- 6.3.6. Education

- 6.3.7. Other Industry Verticals

- 6.1. Market Analysis, Insights and Forecast - by Organization Size

- 7. North America Cloud Encryption Software Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Organization Size

- 7.1.1. SMEs

- 7.1.2. Large Enterprises

- 7.2. Market Analysis, Insights and Forecast - by Service

- 7.2.1. Professional Services

- 7.2.2. Managed Services

- 7.3. Market Analysis, Insights and Forecast - by Industry Vertical

- 7.3.1. IT & Telecommunication

- 7.3.2. BFSI

- 7.3.3. Healthcare

- 7.3.4. Entertainment and Media

- 7.3.5. Retail

- 7.3.6. Education

- 7.3.7. Other Industry Verticals

- 7.1. Market Analysis, Insights and Forecast - by Organization Size

- 8. Europe Cloud Encryption Software Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Organization Size

- 8.1.1. SMEs

- 8.1.2. Large Enterprises

- 8.2. Market Analysis, Insights and Forecast - by Service

- 8.2.1. Professional Services

- 8.2.2. Managed Services

- 8.3. Market Analysis, Insights and Forecast - by Industry Vertical

- 8.3.1. IT & Telecommunication

- 8.3.2. BFSI

- 8.3.3. Healthcare

- 8.3.4. Entertainment and Media

- 8.3.5. Retail

- 8.3.6. Education

- 8.3.7. Other Industry Verticals

- 8.1. Market Analysis, Insights and Forecast - by Organization Size

- 9. Asia Cloud Encryption Software Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Organization Size

- 9.1.1. SMEs

- 9.1.2. Large Enterprises

- 9.2. Market Analysis, Insights and Forecast - by Service

- 9.2.1. Professional Services

- 9.2.2. Managed Services

- 9.3. Market Analysis, Insights and Forecast - by Industry Vertical

- 9.3.1. IT & Telecommunication

- 9.3.2. BFSI

- 9.3.3. Healthcare

- 9.3.4. Entertainment and Media

- 9.3.5. Retail

- 9.3.6. Education

- 9.3.7. Other Industry Verticals

- 9.1. Market Analysis, Insights and Forecast - by Organization Size

- 10. Australia and New Zealand Cloud Encryption Software Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Organization Size

- 10.1.1. SMEs

- 10.1.2. Large Enterprises

- 10.2. Market Analysis, Insights and Forecast - by Service

- 10.2.1. Professional Services

- 10.2.2. Managed Services

- 10.3. Market Analysis, Insights and Forecast - by Industry Vertical

- 10.3.1. IT & Telecommunication

- 10.3.2. BFSI

- 10.3.3. Healthcare

- 10.3.4. Entertainment and Media

- 10.3.5. Retail

- 10.3.6. Education

- 10.3.7. Other Industry Verticals

- 10.1. Market Analysis, Insights and Forecast - by Organization Size

- 11. Latin America Cloud Encryption Software Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Organization Size

- 11.1.1. SMEs

- 11.1.2. Large Enterprises

- 11.2. Market Analysis, Insights and Forecast - by Service

- 11.2.1. Professional Services

- 11.2.2. Managed Services

- 11.3. Market Analysis, Insights and Forecast - by Industry Vertical

- 11.3.1. IT & Telecommunication

- 11.3.2. BFSI

- 11.3.3. Healthcare

- 11.3.4. Entertainment and Media

- 11.3.5. Retail

- 11.3.6. Education

- 11.3.7. Other Industry Verticals

- 11.1. Market Analysis, Insights and Forecast - by Organization Size

- 12. Middle East and Africa Cloud Encryption Software Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Organization Size

- 12.1.1. SMEs

- 12.1.2. Large Enterprises

- 12.2. Market Analysis, Insights and Forecast - by Service

- 12.2.1. Professional Services

- 12.2.2. Managed Services

- 12.3. Market Analysis, Insights and Forecast - by Industry Vertical

- 12.3.1. IT & Telecommunication

- 12.3.2. BFSI

- 12.3.3. Healthcare

- 12.3.4. Entertainment and Media

- 12.3.5. Retail

- 12.3.6. Education

- 12.3.7. Other Industry Verticals

- 12.1. Market Analysis, Insights and Forecast - by Organization Size

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Sophos

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Hitachi Vantara

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Google LLC

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Voltage Security Inc

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Trend Micro

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Ciphercloud

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Hewlett Packard Enterprise

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Safenet

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Boxcryptor*List Not Exhaustive

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 CyberArk

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.11 Symantec Corporation

- 13.1.11.1. Company Overview

- 13.1.11.2. Products

- 13.1.11.3. Company Financials

- 13.1.11.4. SWOT Analysis

- 13.1.1 Sophos

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Cloud Encryption Software Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Cloud Encryption Software Industry Revenue (Million), by Organization Size 2025 & 2033

- Figure 3: North America Cloud Encryption Software Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 4: North America Cloud Encryption Software Industry Revenue (Million), by Service 2025 & 2033

- Figure 5: North America Cloud Encryption Software Industry Revenue Share (%), by Service 2025 & 2033

- Figure 6: North America Cloud Encryption Software Industry Revenue (Million), by Industry Vertical 2025 & 2033

- Figure 7: North America Cloud Encryption Software Industry Revenue Share (%), by Industry Vertical 2025 & 2033

- Figure 8: North America Cloud Encryption Software Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: North America Cloud Encryption Software Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Cloud Encryption Software Industry Revenue (Million), by Organization Size 2025 & 2033

- Figure 11: Europe Cloud Encryption Software Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 12: Europe Cloud Encryption Software Industry Revenue (Million), by Service 2025 & 2033

- Figure 13: Europe Cloud Encryption Software Industry Revenue Share (%), by Service 2025 & 2033

- Figure 14: Europe Cloud Encryption Software Industry Revenue (Million), by Industry Vertical 2025 & 2033

- Figure 15: Europe Cloud Encryption Software Industry Revenue Share (%), by Industry Vertical 2025 & 2033

- Figure 16: Europe Cloud Encryption Software Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Europe Cloud Encryption Software Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Cloud Encryption Software Industry Revenue (Million), by Organization Size 2025 & 2033

- Figure 19: Asia Cloud Encryption Software Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 20: Asia Cloud Encryption Software Industry Revenue (Million), by Service 2025 & 2033

- Figure 21: Asia Cloud Encryption Software Industry Revenue Share (%), by Service 2025 & 2033

- Figure 22: Asia Cloud Encryption Software Industry Revenue (Million), by Industry Vertical 2025 & 2033

- Figure 23: Asia Cloud Encryption Software Industry Revenue Share (%), by Industry Vertical 2025 & 2033

- Figure 24: Asia Cloud Encryption Software Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Asia Cloud Encryption Software Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Australia and New Zealand Cloud Encryption Software Industry Revenue (Million), by Organization Size 2025 & 2033

- Figure 27: Australia and New Zealand Cloud Encryption Software Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 28: Australia and New Zealand Cloud Encryption Software Industry Revenue (Million), by Service 2025 & 2033

- Figure 29: Australia and New Zealand Cloud Encryption Software Industry Revenue Share (%), by Service 2025 & 2033

- Figure 30: Australia and New Zealand Cloud Encryption Software Industry Revenue (Million), by Industry Vertical 2025 & 2033

- Figure 31: Australia and New Zealand Cloud Encryption Software Industry Revenue Share (%), by Industry Vertical 2025 & 2033

- Figure 32: Australia and New Zealand Cloud Encryption Software Industry Revenue (Million), by Country 2025 & 2033

- Figure 33: Australia and New Zealand Cloud Encryption Software Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Latin America Cloud Encryption Software Industry Revenue (Million), by Organization Size 2025 & 2033

- Figure 35: Latin America Cloud Encryption Software Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 36: Latin America Cloud Encryption Software Industry Revenue (Million), by Service 2025 & 2033

- Figure 37: Latin America Cloud Encryption Software Industry Revenue Share (%), by Service 2025 & 2033

- Figure 38: Latin America Cloud Encryption Software Industry Revenue (Million), by Industry Vertical 2025 & 2033

- Figure 39: Latin America Cloud Encryption Software Industry Revenue Share (%), by Industry Vertical 2025 & 2033

- Figure 40: Latin America Cloud Encryption Software Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: Latin America Cloud Encryption Software Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: Middle East and Africa Cloud Encryption Software Industry Revenue (Million), by Organization Size 2025 & 2033

- Figure 43: Middle East and Africa Cloud Encryption Software Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 44: Middle East and Africa Cloud Encryption Software Industry Revenue (Million), by Service 2025 & 2033

- Figure 45: Middle East and Africa Cloud Encryption Software Industry Revenue Share (%), by Service 2025 & 2033

- Figure 46: Middle East and Africa Cloud Encryption Software Industry Revenue (Million), by Industry Vertical 2025 & 2033

- Figure 47: Middle East and Africa Cloud Encryption Software Industry Revenue Share (%), by Industry Vertical 2025 & 2033

- Figure 48: Middle East and Africa Cloud Encryption Software Industry Revenue (Million), by Country 2025 & 2033

- Figure 49: Middle East and Africa Cloud Encryption Software Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Cloud Encryption Software Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 2: Global Cloud Encryption Software Industry Revenue Million Forecast, by Service 2020 & 2033

- Table 3: Global Cloud Encryption Software Industry Revenue Million Forecast, by Industry Vertical 2020 & 2033

- Table 4: Global Cloud Encryption Software Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Cloud Encryption Software Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 6: Global Cloud Encryption Software Industry Revenue Million Forecast, by Service 2020 & 2033

- Table 7: Global Cloud Encryption Software Industry Revenue Million Forecast, by Industry Vertical 2020 & 2033

- Table 8: Global Cloud Encryption Software Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: Global Cloud Encryption Software Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 10: Global Cloud Encryption Software Industry Revenue Million Forecast, by Service 2020 & 2033

- Table 11: Global Cloud Encryption Software Industry Revenue Million Forecast, by Industry Vertical 2020 & 2033

- Table 12: Global Cloud Encryption Software Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Global Cloud Encryption Software Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 14: Global Cloud Encryption Software Industry Revenue Million Forecast, by Service 2020 & 2033

- Table 15: Global Cloud Encryption Software Industry Revenue Million Forecast, by Industry Vertical 2020 & 2033

- Table 16: Global Cloud Encryption Software Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 17: Global Cloud Encryption Software Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 18: Global Cloud Encryption Software Industry Revenue Million Forecast, by Service 2020 & 2033

- Table 19: Global Cloud Encryption Software Industry Revenue Million Forecast, by Industry Vertical 2020 & 2033

- Table 20: Global Cloud Encryption Software Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 21: Global Cloud Encryption Software Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 22: Global Cloud Encryption Software Industry Revenue Million Forecast, by Service 2020 & 2033

- Table 23: Global Cloud Encryption Software Industry Revenue Million Forecast, by Industry Vertical 2020 & 2033

- Table 24: Global Cloud Encryption Software Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 25: Global Cloud Encryption Software Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 26: Global Cloud Encryption Software Industry Revenue Million Forecast, by Service 2020 & 2033

- Table 27: Global Cloud Encryption Software Industry Revenue Million Forecast, by Industry Vertical 2020 & 2033

- Table 28: Global Cloud Encryption Software Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Cloud Encryption Software Industry?

The projected CAGR is approximately 35.23%.

2. Which companies are prominent players in the Cloud Encryption Software Industry?

Key companies in the market include Sophos, Hitachi Vantara, Google LLC, Voltage Security Inc, Trend Micro, Ciphercloud, Hewlett Packard Enterprise, Safenet, Boxcryptor*List Not Exhaustive, CyberArk, Symantec Corporation.

3. What are the main segments of the Cloud Encryption Software Industry?

The market segments include Organization Size, Service, Industry Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.03 Million as of 2022.

5. What are some drivers contributing to market growth?

Regulatory Standards Related to Data Transfer and its Security; Growing Volume of Strength of Cyber Attacks and Mobile Theft.

6. What are the notable trends driving market growth?

IT & Telecommunication Segment to Witness High Growth.

7. Are there any restraints impacting market growth?

Rise in Organizational Overhead Expenses.

8. Can you provide examples of recent developments in the market?

May 2024 - HPE announced new solutions across the HPE GreenLake cloud to simplify how enterprises manage and optimize their storage, data and workloads across on-prem and public cloud environments. New or expanded offerings include HPE GreenLake Block Storage for Amazon Web Services (AWS), a new software-defined storage offering to seamlessly manage block storage across hybrid cloud environments.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Cloud Encryption Software Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Cloud Encryption Software Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Cloud Encryption Software Industry?

To stay informed about further developments, trends, and reports in the Cloud Encryption Software Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence