Key Insights

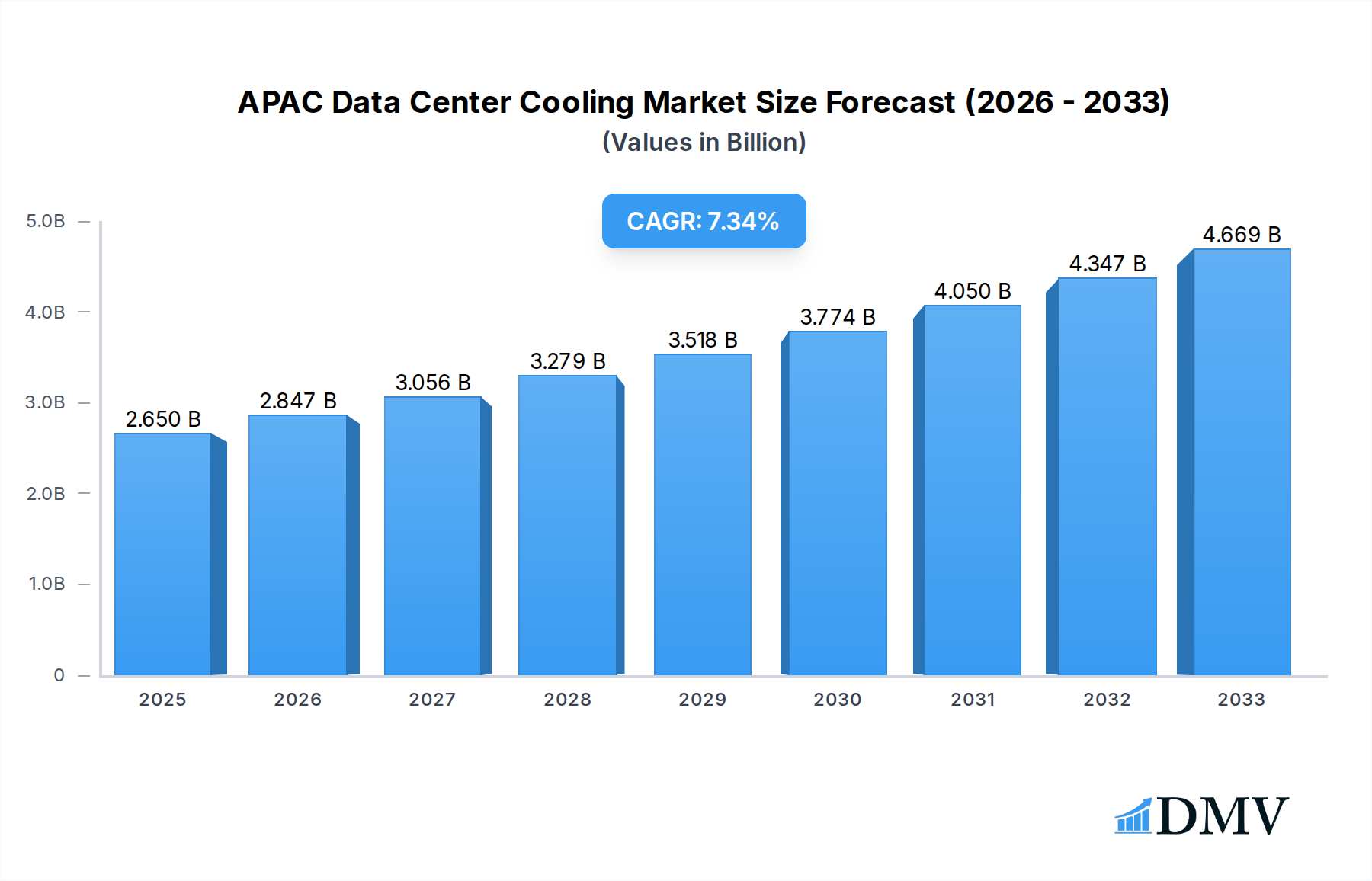

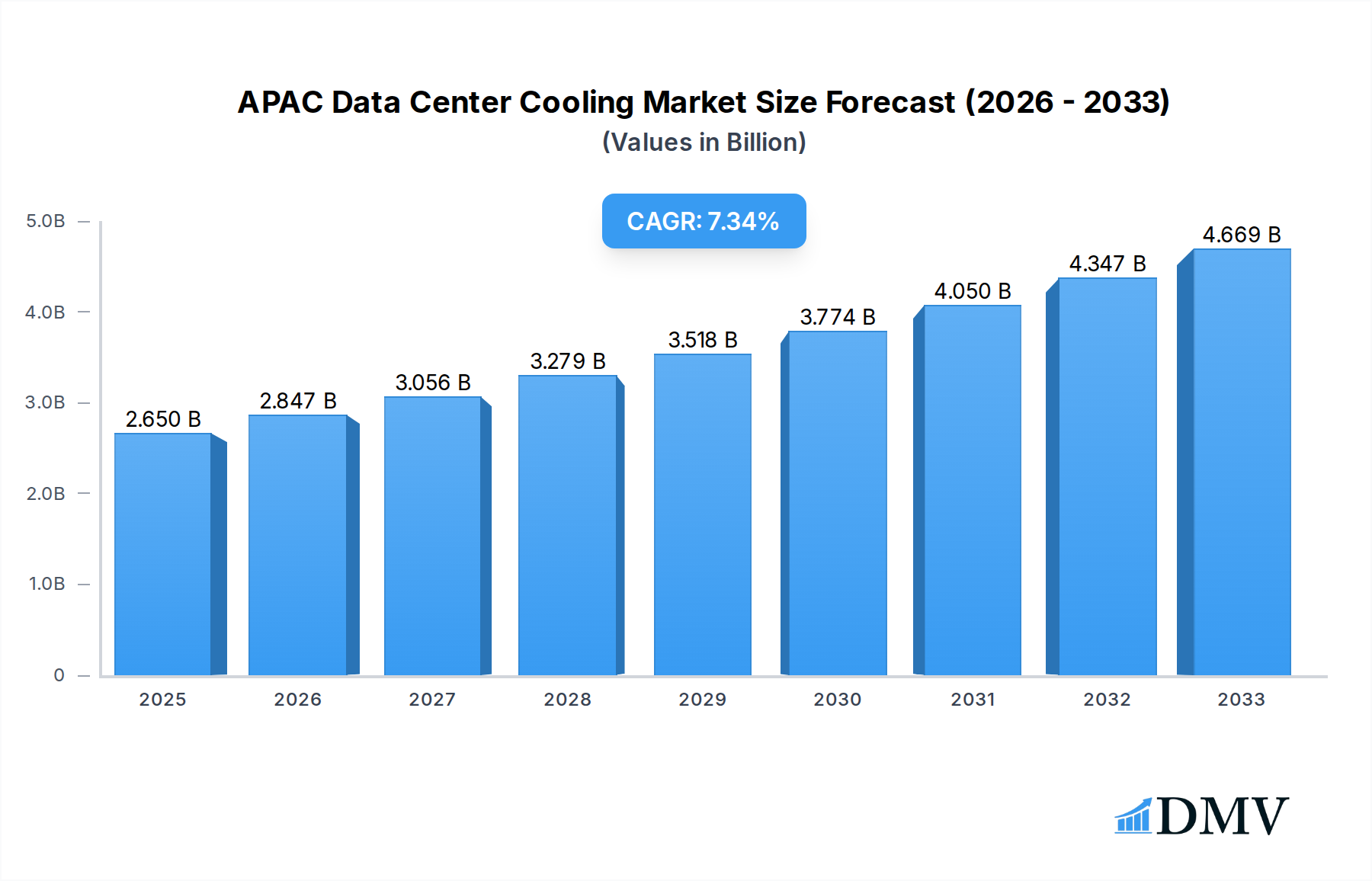

The APAC Data Center Cooling market is poised for significant expansion, with a current market size estimated at $2.65 Billion in the base year 2025. This robust growth is driven by the region's escalating demand for data processing power, fueled by rapid digitalization, the proliferation of cloud computing, and the burgeoning adoption of AI and IoT technologies. The increasing density of IT equipment within data centers necessitates advanced cooling solutions to maintain optimal operating temperatures and prevent performance degradation. Key growth drivers include the continuous build-out of hyperscale and colocation data centers across major economies like China and India, alongside a growing emphasis on energy efficiency and sustainability in data center operations. The market is expected to witness a Compound Annual Growth Rate (CAGR) of 7.40% throughout the forecast period, reaching an estimated value of $4.36 Billion by 2033. This expansion is further supported by government initiatives promoting digital infrastructure development and the increasing adoption of advanced cooling technologies such as liquid-based cooling solutions to address the thermal challenges of high-performance computing.

APAC Data Center Cooling Market Market Size (In Billion)

The competitive landscape of the APAC Data Center Cooling market is characterized by a blend of established global players and emerging regional manufacturers, all vying for market share through innovation and strategic partnerships. The market is segmented into air-based and liquid-based cooling systems, with both categories witnessing substantial adoption. Air-based cooling, including technologies like CRAH, chillers, and economizers, continues to be a foundational element, particularly for existing infrastructure. However, the surge in demand for high-density computing is accelerating the adoption of liquid-based cooling, such as immersion cooling and direct-to-chip solutions, which offer superior thermal management capabilities. Key end-user verticals driving this demand include the IT & Telecom sector, a consistent high consumer of data center resources, followed by the Retail & Consumer Goods, Healthcare, and Media & Entertainment industries, all of which are increasingly reliant on digital infrastructure. North America, Europe, and Asia Pacific are the dominant regional markets, with the latter expected to exhibit the fastest growth due to its expanding digital economy and significant investments in data center infrastructure.

APAC Data Center Cooling Market Company Market Share

This in-depth report provides a strategic analysis of the APAC Data Center Cooling Market, offering unparalleled insights into its current landscape, historical performance, and future trajectory. Designed for data center operators, infrastructure providers, IT professionals, and investors, this research delves deep into market dynamics, technological advancements, and regional growth catalysts. We project the APAC Data Center Cooling Market to reach USD XX Billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of XX% during the forecast period (2025–2033).

APAC Data Center Cooling Market Market Composition & Trends

The APAC Data Center Cooling Market is characterized by a moderately concentrated landscape, with key players like Vertiv Group Corp, Schneider Electric SE, and Daikin Industries Limited holding significant market share. Innovation catalysts are primarily driven by the escalating demand for high-density computing, the proliferation of AI and machine learning workloads, and the increasing adoption of advanced cooling technologies. Regulatory landscapes are evolving, with a growing emphasis on energy efficiency and sustainability initiatives across various APAC nations, influencing the adoption of eco-friendly cooling solutions. Substitute products, while present in the form of legacy cooling systems, are progressively being phased out in favor of more efficient and technologically advanced alternatives. End-user profiles span a diverse range, from hyperscale cloud providers to colocation facilities and enterprise data centers, each with unique cooling requirements. Mergers and acquisitions (M&A) activities are on the rise, with strategic consolidations aimed at expanding market reach and technological portfolios, with recent deals valued in the hundreds of millions. Market share distribution indicates a strong preference for air-based cooling, particularly CRAH units, but liquid-based cooling solutions are rapidly gaining traction.

APAC Data Center Cooling Market Industry Evolution

The APAC Data Center Cooling Market has witnessed a remarkable evolution over the historical period (2019–2024) and is poised for accelerated growth through 2033. This evolution is fundamentally driven by the exponential increase in data generation and processing demands, fueled by digital transformation initiatives, the expansion of 5G networks, and the burgeoning Internet of Things (IoT) ecosystem across the region. The initial growth trajectory was anchored by traditional air-based cooling solutions, including Computer Room Air Handlers (CRAH), chillers, and economizers, which provided reliable and cost-effective cooling for established data centers. However, the surging power densities within modern data centers, driven by high-performance computing (HPC) and AI/ML applications, have necessitated a paradigm shift towards more sophisticated and efficient cooling methodologies.

Technological advancements have been a pivotal force in shaping the industry. The introduction of liquid-based cooling solutions, such as direct-to-chip cooling and immersion cooling, represents a significant leap forward. These technologies offer superior heat dissipation capabilities, enabling data centers to operate at higher densities and achieve unprecedented energy efficiency. For instance, direct-to-chip cooling can reduce the thermal resistance between components and the cooling medium by up to 90% compared to traditional air cooling, leading to substantial energy savings and improved performance. Immersion cooling, in its single-phase and two-phase variants, further enhances efficiency by directly submerging server components in a dielectric fluid, providing uniform temperature distribution and eliminating the need for energy-intensive fans.

Shifting consumer demands, particularly the growing awareness and stringent requirements for sustainability and reduced environmental impact, are also reshaping the market. Data center operators are increasingly prioritizing solutions that minimize energy consumption and carbon footprint. This has led to a surge in demand for free cooling techniques, such as economizers, which leverage ambient air to cool data centers when conditions permit, and advanced adiabatic cooling systems. The adoption metrics for these sustainable solutions are projected to grow by over XX% annually in the coming years. Furthermore, the increasing complexity of data center designs, including modular and edge data centers, demands flexible and scalable cooling architectures, further driving innovation. The base year (2025) marks a critical juncture where hybrid cooling strategies, integrating both air and liquid-based approaches, are becoming mainstream, catering to the diverse needs of the rapidly expanding APAC digital infrastructure.

Leading Regions, Countries, or Segments in APAC Data Center Cooling Market

The dominance within the APAC Data Center Cooling Market is multifaceted, with specific regions, countries, and segments exhibiting exceptional growth and adoption.

Dominant Segments:

- Air-based Cooling:

- CRAH (Computer Room Air Handler): Continues to be a foundational technology, especially for existing infrastructure and mid-density deployments. Its widespread adoption is driven by established infrastructure, ease of maintenance, and cost-effectiveness for many applications. Key drivers include the large number of legacy data centers requiring upgrades and the ongoing expansion of colocation facilities across emerging economies.

- Chiller and Economizer Systems: Essential for large-scale and hyperscale data centers, chiller systems coupled with economizers offer significant energy savings in suitable climates. The increasing number of hyperscale data center builds in countries like China and Singapore, which can leverage free cooling opportunities for a substantial portion of the year, fuels their dominance. Investment trends in advanced chiller technologies that utilize refrigerants with lower Global Warming Potential (GWP) are also a significant factor.

- Liquid-based Cooling:

- Direct-to-Chip Cooling: This segment is experiencing the most rapid growth. It is critical for high-density racks supporting AI, HPC, and GPU-intensive workloads. Countries investing heavily in AI research and development, such as South Korea and Japan, are leading the adoption of direct-to-chip solutions. Performance metrics such as reduced latency and increased compute efficiency are key drivers.

- Immersion Cooling: While still a nascent but rapidly expanding segment, immersion cooling offers unparalleled thermal management for extremely high-density environments. Its adoption is driven by specialized applications in sectors requiring extreme computational power. The projected growth rate for immersion cooling is estimated to be over XX% annually.

- Rear-Door Heat Exchanger: Serves as an efficient supplemental cooling solution for high-density racks, bridging the gap between air and full liquid immersion. Its adoption is driven by the need for targeted and efficient heat removal in specific rack configurations.

Dominant End-user Verticals:

- IT & Telecom: This vertical remains the largest consumer of data center cooling solutions due to the continuous expansion of cloud infrastructure, 5G deployment, and digital services. The insatiable demand for data processing power and storage necessitates robust and scalable cooling. Investment in new data center construction and upgrades by major telecommunication companies and cloud providers is a primary driver.

- Federal & Institutional Agencies: Governments across APAC are investing heavily in digital infrastructure for smart city initiatives, defense, and public services, driving demand for secure and efficient data center cooling. Regulatory support for digital transformation and data sovereignty further bolsters this segment.

Leading Regions and Countries:

- China: Dominates the APAC market due to its massive data center expansion, rapid adoption of advanced technologies, and significant investments in AI and HPC. Government initiatives promoting digital infrastructure and the sheer scale of its IT & Telecom sector are key drivers.

- Japan: A mature market with a strong focus on technological innovation and energy efficiency, leading in the adoption of advanced liquid cooling solutions and eco-friendly technologies. Its established manufacturing base and R&D capabilities contribute to its leadership.

- Singapore: A regional hub for data centers, benefiting from strategic location, favorable business environment, and government support for digital infrastructure. Its focus on sustainability and high-density computing is driving demand for advanced cooling.

- South Korea: A leader in AI and HPC research, driving demand for high-performance liquid cooling solutions. Significant investments in next-generation computing infrastructure are propelling this market.

APAC Data Center Cooling Market Product Innovations

Product innovations in the APAC Data Center Cooling Market are primarily focused on enhancing energy efficiency, improving cooling capacity for high-density applications, and enabling greater sustainability. Direct-to-chip liquid cooling solutions, such as those offering microchannel cold plates, are revolutionizing heat dissipation by bringing cooling closer to the heat source, reducing thermal resistance by over 85%. Immersion cooling technologies are advancing with more efficient dielectric fluids and modular designs, enabling rapid deployment for extreme density requirements. Advanced CRAH units are incorporating variable speed drives and intelligent controls for optimized airflow and energy consumption, achieving up to 30% energy savings. Rear-door heat exchangers are evolving with higher heat removal capacities and quieter operation. These innovations are driven by the need to support next-generation processors and GPUs, reduce operational expenditure (OPEX), and meet stringent environmental regulations.

Propelling Factors for APAC Data Center Cooling Market Growth

The APAC Data Center Cooling Market is propelled by several key factors. The relentless surge in data consumption and generation, driven by 5G, IoT, and AI adoption, necessitates robust and scalable data center infrastructure. Government initiatives promoting digital transformation and smart cities across the region are accelerating data center construction and modernization. The growing trend towards high-density computing for AI, machine learning, and HPC workloads demands advanced cooling solutions that can efficiently dissipate heat. Furthermore, an increasing emphasis on energy efficiency and sustainability is driving the adoption of eco-friendly cooling technologies, such as free cooling and liquid-based solutions, to reduce operational costs and environmental impact. The expansion of cloud computing services and the rise of edge computing are also contributing significantly to market growth.

Obstacles in the APAC Data Center Cooling Market Market

Despite robust growth, the APAC Data Center Cooling Market faces several obstacles. The high initial capital expenditure associated with advanced cooling technologies, particularly liquid-based solutions, can be a deterrent for some smaller enterprises. Navigating diverse and evolving regulatory landscapes across different APAC countries can create compliance challenges. Supply chain disruptions, as witnessed during recent global events, can impact the availability and cost of critical components. Moreover, the skilled workforce required for the installation, operation, and maintenance of sophisticated cooling systems is in high demand, leading to potential talent shortages. Intense competition among existing and new players can also put pressure on pricing and profit margins.

Future Opportunities in APAC Data Center Cooling Market

Emerging opportunities in the APAC Data Center Cooling Market are abundant. The rapid growth of AI and HPC applications presents a significant opportunity for the widespread adoption of liquid cooling solutions, including immersion and direct-to-chip technologies. The expansion of edge data centers, driven by the need for low latency processing for IoT and autonomous systems, will create demand for compact and efficient cooling solutions. The increasing focus on sustainability and the circular economy will drive innovation in energy-efficient cooling, heat reuse technologies, and eco-friendly refrigerants. Furthermore, the development of smart data centers with integrated AI-powered cooling management systems offers avenues for enhanced operational efficiency and predictive maintenance. The untapped potential in emerging economies within APAC also presents substantial growth opportunities.

Major Players in the APAC Data Center Cooling Market Ecosystem

- Eaton Corporation plc

- Munters Group

- Mitsubishi Electric Corporation

- Schneider Electric SE

- Rittal Gmbh & Co KG

- Johnson Controls Inc

- Stulz GmbH

- Vertiv Group Corp

- Asetek A/S

- Daikin Industries Limited

Key Developments in APAC Data Center Cooling Market Industry

- 2023 Q4: Vertiv Group Corp launched an advanced liquid cooling solution for high-density racks, enhancing performance for AI workloads.

- 2023 Q3: Schneider Electric SE expanded its EcoStruxure™ for Data Centers portfolio with enhanced cooling management capabilities, emphasizing energy efficiency.

- 2023 Q2: Daikin Industries Limited announced strategic partnerships to boost its presence in the liquid cooling segment for data centers in Southeast Asia.

- 2023 Q1: Mitsubishi Electric Corporation showcased its latest energy-efficient chiller technology designed for data center applications at a major industry exhibition.

- 2022 Q4: Munters Group acquired a company specializing in advanced heat exchanger technology, strengthening its offerings for data center thermal management.

- 2022 Q3: Eaton Corporation plc introduced new uninterruptible power supply (UPS) systems integrated with advanced cooling monitoring for improved data center resilience.

- 2022 Q2: Rittal Gmbh & Co KG expanded its liquid cooling solutions portfolio to cater to the increasing demand for high-density computing.

- 2022 Q1: Johnson Controls Inc unveiled a new suite of intelligent building management solutions for data centers, including optimized cooling controls.

- 2021 Q4: Stulz GmbH introduced innovative adiabatic cooling systems for enhanced energy savings in data center operations.

- 2021 Q3: Asetek A/S reported significant growth in its data center segment, driven by the adoption of its direct-to-chip cooling solutions.

Strategic APAC Data Center Cooling Market Market Forecast

The strategic APAC Data Center Cooling Market forecast indicates sustained robust growth, primarily driven by the insatiable demand for data processing and storage, fueled by AI, 5G, and the digital economy. Key growth catalysts include ongoing investments in hyperscale and edge data centers, coupled with a strong push towards energy efficiency and sustainability. The increasing adoption of advanced liquid cooling technologies, such as direct-to-chip and immersion cooling, will be crucial in managing the thermal challenges posed by high-density computing. Furthermore, supportive government policies and a growing awareness of environmental impact will continue to propel the market towards greener and more intelligent cooling solutions. The market is expected to witness significant innovation and strategic partnerships, shaping a dynamic and evolving landscape.

APAC Data Center Cooling Market Segmentation

-

1. Cooli

-

1.1. Air-based Cooling

- 1.1.1. CRAH

- 1.1.2. Chiller and Economizer

- 1.1.3. Cooling

- 1.1.4. Others

-

1.2. Liquid-based Cooling

- 1.2.1. Immersion Cooling

- 1.2.2. Direct-to-Chip Cooling

- 1.2.3. Rear-Door Heat Exchanger

-

1.1. Air-based Cooling

-

2. End-user Vertical

- 2.1. IT & Telecom

- 2.2. Retail & Consumer Goods

- 2.3. Healthcare

- 2.4. Media & Entertainment

- 2.5. Federal & Institutional agencies

- 2.6. Other end-users

APAC Data Center Cooling Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

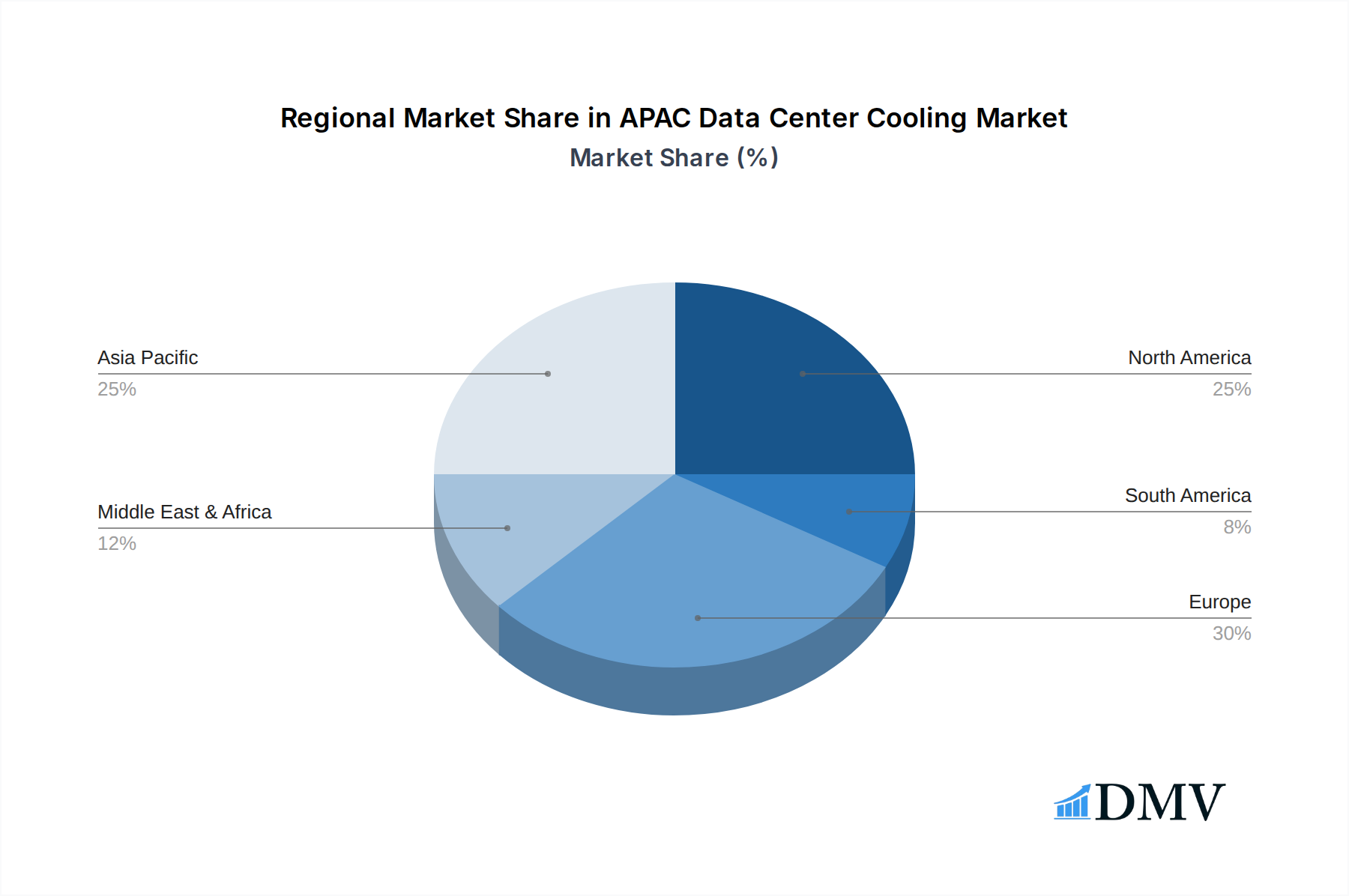

APAC Data Center Cooling Market Regional Market Share

Geographic Coverage of APAC Data Center Cooling Market

APAC Data Center Cooling Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.40% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Cooli

- 5.1.1. Air-based Cooling

- 5.1.1.1. CRAH

- 5.1.1.2. Chiller and Economizer

- 5.1.1.3. Cooling

- 5.1.1.4. Others

- 5.1.2. Liquid-based Cooling

- 5.1.2.1. Immersion Cooling

- 5.1.2.2. Direct-to-Chip Cooling

- 5.1.2.3. Rear-Door Heat Exchanger

- 5.1.1. Air-based Cooling

- 5.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 5.2.1. IT & Telecom

- 5.2.2. Retail & Consumer Goods

- 5.2.3. Healthcare

- 5.2.4. Media & Entertainment

- 5.2.5. Federal & Institutional agencies

- 5.2.6. Other end-users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Cooli

- 6. Global APAC Data Center Cooling Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Cooli

- 6.1.1. Air-based Cooling

- 6.1.1.1. CRAH

- 6.1.1.2. Chiller and Economizer

- 6.1.1.3. Cooling

- 6.1.1.4. Others

- 6.1.2. Liquid-based Cooling

- 6.1.2.1. Immersion Cooling

- 6.1.2.2. Direct-to-Chip Cooling

- 6.1.2.3. Rear-Door Heat Exchanger

- 6.1.1. Air-based Cooling

- 6.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 6.2.1. IT & Telecom

- 6.2.2. Retail & Consumer Goods

- 6.2.3. Healthcare

- 6.2.4. Media & Entertainment

- 6.2.5. Federal & Institutional agencies

- 6.2.6. Other end-users

- 6.1. Market Analysis, Insights and Forecast - by Cooli

- 7. North America APAC Data Center Cooling Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Cooli

- 7.1.1. Air-based Cooling

- 7.1.1.1. CRAH

- 7.1.1.2. Chiller and Economizer

- 7.1.1.3. Cooling

- 7.1.1.4. Others

- 7.1.2. Liquid-based Cooling

- 7.1.2.1. Immersion Cooling

- 7.1.2.2. Direct-to-Chip Cooling

- 7.1.2.3. Rear-Door Heat Exchanger

- 7.1.1. Air-based Cooling

- 7.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 7.2.1. IT & Telecom

- 7.2.2. Retail & Consumer Goods

- 7.2.3. Healthcare

- 7.2.4. Media & Entertainment

- 7.2.5. Federal & Institutional agencies

- 7.2.6. Other end-users

- 7.1. Market Analysis, Insights and Forecast - by Cooli

- 8. South America APAC Data Center Cooling Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Cooli

- 8.1.1. Air-based Cooling

- 8.1.1.1. CRAH

- 8.1.1.2. Chiller and Economizer

- 8.1.1.3. Cooling

- 8.1.1.4. Others

- 8.1.2. Liquid-based Cooling

- 8.1.2.1. Immersion Cooling

- 8.1.2.2. Direct-to-Chip Cooling

- 8.1.2.3. Rear-Door Heat Exchanger

- 8.1.1. Air-based Cooling

- 8.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 8.2.1. IT & Telecom

- 8.2.2. Retail & Consumer Goods

- 8.2.3. Healthcare

- 8.2.4. Media & Entertainment

- 8.2.5. Federal & Institutional agencies

- 8.2.6. Other end-users

- 8.1. Market Analysis, Insights and Forecast - by Cooli

- 9. Europe APAC Data Center Cooling Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Cooli

- 9.1.1. Air-based Cooling

- 9.1.1.1. CRAH

- 9.1.1.2. Chiller and Economizer

- 9.1.1.3. Cooling

- 9.1.1.4. Others

- 9.1.2. Liquid-based Cooling

- 9.1.2.1. Immersion Cooling

- 9.1.2.2. Direct-to-Chip Cooling

- 9.1.2.3. Rear-Door Heat Exchanger

- 9.1.1. Air-based Cooling

- 9.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 9.2.1. IT & Telecom

- 9.2.2. Retail & Consumer Goods

- 9.2.3. Healthcare

- 9.2.4. Media & Entertainment

- 9.2.5. Federal & Institutional agencies

- 9.2.6. Other end-users

- 9.1. Market Analysis, Insights and Forecast - by Cooli

- 10. Middle East & Africa APAC Data Center Cooling Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Cooli

- 10.1.1. Air-based Cooling

- 10.1.1.1. CRAH

- 10.1.1.2. Chiller and Economizer

- 10.1.1.3. Cooling

- 10.1.1.4. Others

- 10.1.2. Liquid-based Cooling

- 10.1.2.1. Immersion Cooling

- 10.1.2.2. Direct-to-Chip Cooling

- 10.1.2.3. Rear-Door Heat Exchanger

- 10.1.1. Air-based Cooling

- 10.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 10.2.1. IT & Telecom

- 10.2.2. Retail & Consumer Goods

- 10.2.3. Healthcare

- 10.2.4. Media & Entertainment

- 10.2.5. Federal & Institutional agencies

- 10.2.6. Other end-users

- 10.1. Market Analysis, Insights and Forecast - by Cooli

- 11. Asia Pacific APAC Data Center Cooling Market Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Cooli

- 11.1.1. Air-based Cooling

- 11.1.1.1. CRAH

- 11.1.1.2. Chiller and Economizer

- 11.1.1.3. Cooling

- 11.1.1.4. Others

- 11.1.2. Liquid-based Cooling

- 11.1.2.1. Immersion Cooling

- 11.1.2.2. Direct-to-Chip Cooling

- 11.1.2.3. Rear-Door Heat Exchanger

- 11.1.1. Air-based Cooling

- 11.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 11.2.1. IT & Telecom

- 11.2.2. Retail & Consumer Goods

- 11.2.3. Healthcare

- 11.2.4. Media & Entertainment

- 11.2.5. Federal & Institutional agencies

- 11.2.6. Other end-users

- 11.1. Market Analysis, Insights and Forecast - by Cooli

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Eaton Corporation plc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Munters Group

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Mitsubishi Electric Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Schneider Electric SE

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Rittal Gmbh & Co KG

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Johnson Controls Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Stulz GmbH

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Vertiv Group Corp

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Asetek A/

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Daikin Industries Limited

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Eaton Corporation plc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global APAC Data Center Cooling Market Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America APAC Data Center Cooling Market Revenue (Million), by Cooli 2025 & 2033

- Figure 3: North America APAC Data Center Cooling Market Revenue Share (%), by Cooli 2025 & 2033

- Figure 4: North America APAC Data Center Cooling Market Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 5: North America APAC Data Center Cooling Market Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 6: North America APAC Data Center Cooling Market Revenue (Million), by Country 2025 & 2033

- Figure 7: North America APAC Data Center Cooling Market Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America APAC Data Center Cooling Market Revenue (Million), by Cooli 2025 & 2033

- Figure 9: South America APAC Data Center Cooling Market Revenue Share (%), by Cooli 2025 & 2033

- Figure 10: South America APAC Data Center Cooling Market Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 11: South America APAC Data Center Cooling Market Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 12: South America APAC Data Center Cooling Market Revenue (Million), by Country 2025 & 2033

- Figure 13: South America APAC Data Center Cooling Market Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe APAC Data Center Cooling Market Revenue (Million), by Cooli 2025 & 2033

- Figure 15: Europe APAC Data Center Cooling Market Revenue Share (%), by Cooli 2025 & 2033

- Figure 16: Europe APAC Data Center Cooling Market Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 17: Europe APAC Data Center Cooling Market Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 18: Europe APAC Data Center Cooling Market Revenue (Million), by Country 2025 & 2033

- Figure 19: Europe APAC Data Center Cooling Market Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa APAC Data Center Cooling Market Revenue (Million), by Cooli 2025 & 2033

- Figure 21: Middle East & Africa APAC Data Center Cooling Market Revenue Share (%), by Cooli 2025 & 2033

- Figure 22: Middle East & Africa APAC Data Center Cooling Market Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 23: Middle East & Africa APAC Data Center Cooling Market Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 24: Middle East & Africa APAC Data Center Cooling Market Revenue (Million), by Country 2025 & 2033

- Figure 25: Middle East & Africa APAC Data Center Cooling Market Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific APAC Data Center Cooling Market Revenue (Million), by Cooli 2025 & 2033

- Figure 27: Asia Pacific APAC Data Center Cooling Market Revenue Share (%), by Cooli 2025 & 2033

- Figure 28: Asia Pacific APAC Data Center Cooling Market Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 29: Asia Pacific APAC Data Center Cooling Market Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 30: Asia Pacific APAC Data Center Cooling Market Revenue (Million), by Country 2025 & 2033

- Figure 31: Asia Pacific APAC Data Center Cooling Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global APAC Data Center Cooling Market Revenue Million Forecast, by Cooli 2020 & 2033

- Table 2: Global APAC Data Center Cooling Market Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 3: Global APAC Data Center Cooling Market Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global APAC Data Center Cooling Market Revenue Million Forecast, by Cooli 2020 & 2033

- Table 5: Global APAC Data Center Cooling Market Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 6: Global APAC Data Center Cooling Market Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States APAC Data Center Cooling Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada APAC Data Center Cooling Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Mexico APAC Data Center Cooling Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Global APAC Data Center Cooling Market Revenue Million Forecast, by Cooli 2020 & 2033

- Table 11: Global APAC Data Center Cooling Market Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 12: Global APAC Data Center Cooling Market Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Brazil APAC Data Center Cooling Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Argentina APAC Data Center Cooling Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America APAC Data Center Cooling Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Global APAC Data Center Cooling Market Revenue Million Forecast, by Cooli 2020 & 2033

- Table 17: Global APAC Data Center Cooling Market Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 18: Global APAC Data Center Cooling Market Revenue Million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom APAC Data Center Cooling Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Germany APAC Data Center Cooling Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: France APAC Data Center Cooling Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Italy APAC Data Center Cooling Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Spain APAC Data Center Cooling Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Russia APAC Data Center Cooling Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Benelux APAC Data Center Cooling Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Nordics APAC Data Center Cooling Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe APAC Data Center Cooling Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Global APAC Data Center Cooling Market Revenue Million Forecast, by Cooli 2020 & 2033

- Table 29: Global APAC Data Center Cooling Market Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 30: Global APAC Data Center Cooling Market Revenue Million Forecast, by Country 2020 & 2033

- Table 31: Turkey APAC Data Center Cooling Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Israel APAC Data Center Cooling Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 33: GCC APAC Data Center Cooling Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: North Africa APAC Data Center Cooling Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: South Africa APAC Data Center Cooling Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa APAC Data Center Cooling Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: Global APAC Data Center Cooling Market Revenue Million Forecast, by Cooli 2020 & 2033

- Table 38: Global APAC Data Center Cooling Market Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 39: Global APAC Data Center Cooling Market Revenue Million Forecast, by Country 2020 & 2033

- Table 40: China APAC Data Center Cooling Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 41: India APAC Data Center Cooling Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Japan APAC Data Center Cooling Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 43: South Korea APAC Data Center Cooling Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN APAC Data Center Cooling Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 45: Oceania APAC Data Center Cooling Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific APAC Data Center Cooling Market Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the APAC Data Center Cooling Market?

The projected CAGR is approximately 7.40%.

2. Which companies are prominent players in the APAC Data Center Cooling Market?

Key companies in the market include Eaton Corporation plc, Munters Group, Mitsubishi Electric Corporation, Schneider Electric SE, Rittal Gmbh & Co KG, Johnson Controls Inc, Stulz GmbH, Vertiv Group Corp, Asetek A/, Daikin Industries Limited.

3. What are the main segments of the APAC Data Center Cooling Market?

The market segments include Cooli, End-user Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.65 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Volume of Digital Data; Emergence of Green Data Centers.

6. What are the notable trends driving market growth?

Information Technology Industry to Witness Highest Growth.

7. Are there any restraints impacting market growth?

Costs. Adaptability Requirements. and Power Outages.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "APAC Data Center Cooling Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the APAC Data Center Cooling Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the APAC Data Center Cooling Market?

To stay informed about further developments, trends, and reports in the APAC Data Center Cooling Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence