Key Insights

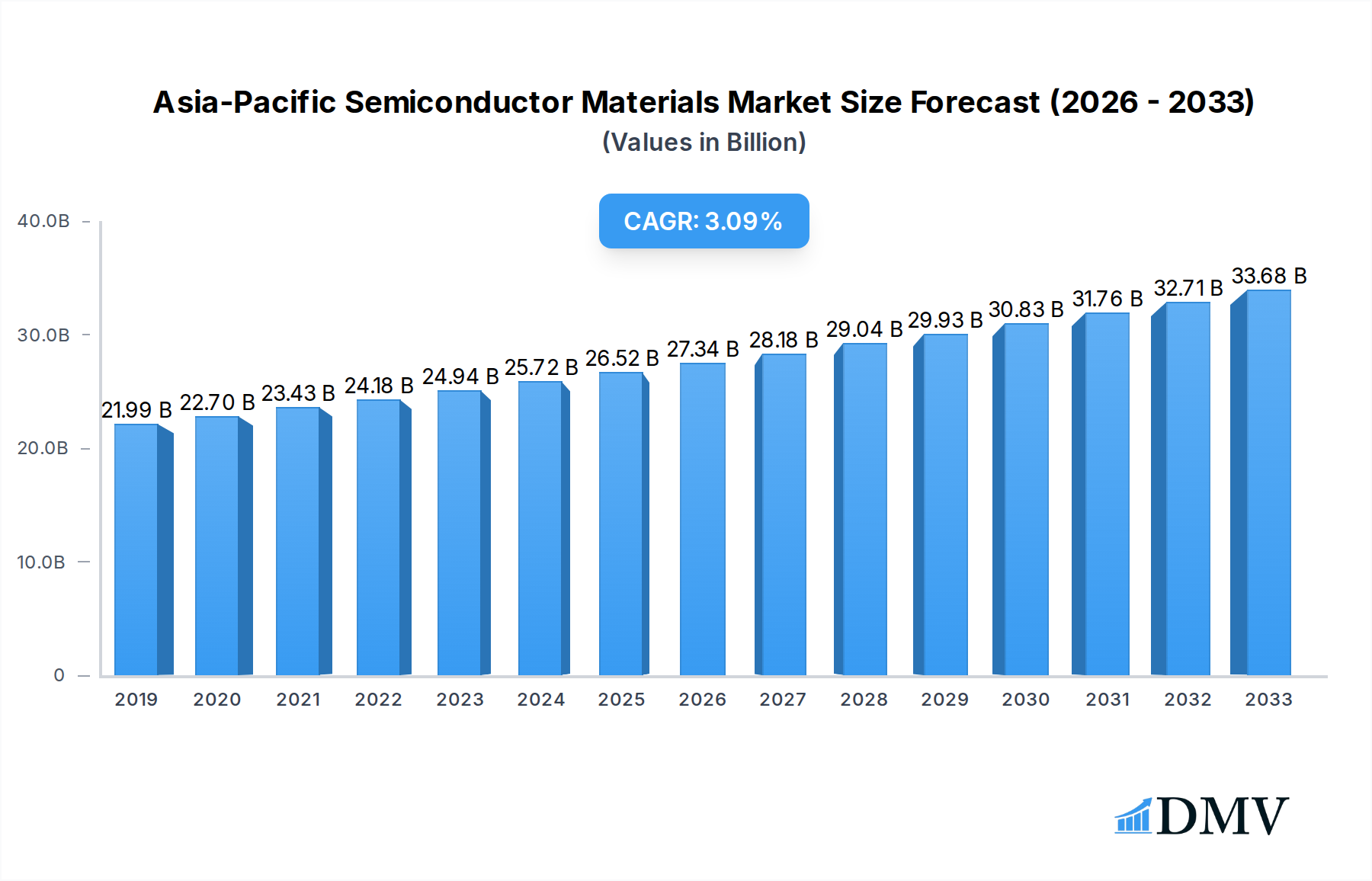

The Asia-Pacific semiconductor materials market is poised for robust expansion, projected to reach a significant $26.08 million by 2025. This growth is underpinned by a healthy Compound Annual Growth Rate (CAGR) of 3.40% between 2019 and 2033, indicating a consistent upward trajectory. The market is fueled by escalating demand from key end-user industries, particularly consumer electronics and telecommunications, which are experiencing rapid innovation and consumer adoption of new technologies. The automotive sector's increasing reliance on advanced semiconductor components for features like autonomous driving and in-car entertainment, alongside the energy and utility sector's growing need for efficient power management solutions, further contribute to this demand. Manufacturing applications, including advanced fabrication and packaging processes, are also vital drivers, as the region continues to be a global hub for semiconductor production.

Asia-Pacific Semiconductor Materials Market Market Size (In Billion)

Key material segments like Silicon Carbide (SiC) and Gallium Manganese Arsenide (GaAs) are expected to witness substantial adoption due to their superior performance characteristics in high-power and high-frequency applications, respectively. While the market benefits from strong drivers, potential restraints such as supply chain volatilities and geopolitical uncertainties require careful navigation. Emerging trends like the increasing integration of advanced materials for next-generation semiconductor devices, the drive towards miniaturization, and the growing emphasis on sustainable manufacturing practices will shape the market landscape. Companies like UTAC Holdings Ltd, Sumitomo Chemical Co Ltd, and Intel Corporation are actively investing in research and development to capitalize on these trends and maintain a competitive edge in this dynamic market. The Asia-Pacific region, with its established manufacturing infrastructure and burgeoning technological ecosystem, is set to remain the dominant force in the global semiconductor materials arena.

Asia-Pacific Semiconductor Materials Market Company Market Share

Asia-Pacific Semiconductor Materials Market Report: Growth, Innovations, and Future Outlook (2019-2033)

Gain unparalleled insights into the dynamic Asia-Pacific semiconductor materials market, a pivotal sector driving global technological advancement. This comprehensive report navigates the intricate landscape of silicon carbide (SiC), gallium arsenide (GaAs), copper indium gallium selenide (CIGS), molybdenum disulfide (MoS), and bismuth telluride (Bi2Te3) materials. Delve into their critical roles in fabrication and packaging processes, influencing key end-user industries such as consumer electronics, telecommunication, manufacturing, automotive, and energy & utility. With a study period spanning 2019–2033, a base year of 2025, and a robust forecast period of 2025–2033, this report provides critical data for strategic decision-making. Explore market trends, competitive dynamics, and emerging opportunities to stay ahead in this rapidly evolving market.

Asia-Pacific Semiconductor Materials Market Market Composition & Trends

The Asia-Pacific semiconductor materials market exhibits a moderate to high concentration, with a few key players dominating significant market share. Innovation is a constant catalyst, driven by relentless demand for enhanced performance and miniaturization in electronic devices. Regulatory landscapes, while varying across nations, are increasingly geared towards fostering domestic semiconductor production and R&D, exemplified by initiatives like India's 'Aatmanirbhar Bharat' program. The threat of substitute products is relatively low for advanced materials like SiC and GaAs due to their unique performance characteristics, but competition from evolving materials within existing categories remains a factor. End-user profiles are diverse, ranging from high-volume consumer electronics manufacturers to specialized automotive and telecommunication equipment providers. Merger and acquisition (M&A) activities are strategic, aimed at consolidating market position, acquiring cutting-edge technologies, or expanding geographical reach. The total M&A deal value in the semiconductor materials sector globally exceeded an estimated $50,000 Million in the past five years, with a significant portion influenced by Asia-Pacific's strategic importance.

- Market Share Distribution: Dominated by a few major material suppliers with specialized expertise.

- Innovation Catalysts: Miniaturization trends, 5G deployment, electric vehicle adoption, and AI advancements.

- Regulatory Landscape: Government incentives for domestic manufacturing and R&D, export controls on advanced technologies.

- Substitute Products: Limited for high-performance applications, but material optimization and cost-reduction efforts are ongoing.

- End-User Profiles: Varied, from high-volume consumer electronics to niche industrial and automotive applications.

- M&A Activities: Focused on technology acquisition, vertical integration, and market expansion.

Asia-Pacific Semiconductor Materials Market Industry Evolution

The Asia-Pacific semiconductor materials market has witnessed remarkable evolution, driven by a confluence of technological breakthroughs, escalating demand from burgeoning end-user industries, and strategic government initiatives. Over the historical period (2019–2024), the market experienced robust growth, propelled by the relentless digital transformation across various sectors. The advent of 5G technology, the rapid expansion of the Internet of Things (IoT), and the increasing sophistication of artificial intelligence (AI) have significantly amplified the need for advanced semiconductor materials. Specifically, the demand for materials like Silicon Carbide (SiC) has surged due to its superior thermal conductivity and high-voltage capabilities, making it indispensable for electric vehicles (EVs) and renewable energy applications. Gallium Arsenide (GaAs) continues to be a critical material for high-frequency applications in telecommunications and consumer electronics, supporting the performance demands of next-generation devices.

The growth trajectory has been further bolstered by substantial investments in semiconductor manufacturing infrastructure across the Asia-Pacific region. Countries like China, South Korea, Taiwan, and Japan are at the forefront of this expansion, attracting global semiconductor players and fostering local innovation. Technological advancements have focused on improving material purity, reducing defects, and developing novel material compositions to meet the ever-increasing performance requirements of integrated circuits. This includes innovations in wafer fabrication techniques, deposition processes, and the development of new materials for advanced packaging solutions. Consumer demand has shifted towards more powerful, energy-efficient, and feature-rich electronic devices, directly translating into a higher demand for sophisticated semiconductor components and, consequently, the materials used to produce them. The forecast period (2025–2033) is projected to see continued accelerated growth, with an estimated Compound Annual Growth Rate (CAGR) of approximately 12-15%, driven by emerging technologies such as AI accelerators, advanced automotive electronics, and the continued build-out of global communication networks. Adoption metrics for SiC, for instance, are expected to see a substantial increase, with its market share in power electronics projected to grow significantly from an estimated 15% in 2025 to over 30% by 2033. Similarly, the demand for high-purity chemicals for semiconductor manufacturing, as exemplified by Sumitomo Chemical's capacity expansion, underscores the industry's commitment to meeting the escalating quality and volume requirements.

Leading Regions, Countries, or Segments in Asia-Pacific Semiconductor Materials Market

The Asia-Pacific semiconductor materials market is a complex ecosystem with distinct regional and segmental leadership, driven by a combination of robust industrial policies, significant R&D investments, and the presence of major global manufacturers. Among the material segments, Silicon Carbide (SiC) is emerging as a dominant force, particularly in its application within the automotive and energy & utility sectors. The escalating demand for electric vehicles (EVs) and the ongoing transition to renewable energy sources necessitate the high-performance capabilities of SiC in power electronics, such as inverters and power modules, where its superior thermal conductivity and voltage handling far surpass traditional silicon. This has led to substantial investments in SiC wafer production and downstream integration across the region.

Geographically, East Asia, encompassing countries like China, South Korea, Japan, and Taiwan, stands out as the undisputed leader in the Asia-Pacific semiconductor materials market. These nations are home to the world's largest semiconductor manufacturing hubs and possess sophisticated supply chains.

- Dominant Region: East Asia (China, South Korea, Japan, Taiwan)

- Key Drivers: Massive domestic semiconductor manufacturing capacity, government support for the industry through subsidies and favorable policies, a strong ecosystem of material suppliers and research institutions, and substantial demand from the consumer electronics and telecommunication sectors.

- Analysis: Taiwan's foundry leadership, South Korea's dominance in memory chips, and China's rapid expansion in all facets of semiconductor production contribute significantly to the region's supremacy. These countries are not only consumers of semiconductor materials but are also increasingly becoming producers, with companies actively investing in material R&D and production capabilities.

Within the Application segment, Fabrication remains the largest contributor, as it encompasses the core processes of creating semiconductor chips. However, the Packaging segment is experiencing rapid growth, driven by the need for advanced packaging solutions that enhance performance, reduce form factor, and improve thermal management for increasingly complex chips.

- Dominant Application Segment: Fabrication

- Analysis: The foundational processes of wafer fabrication, including photolithography, etching, and deposition, consume a vast array of specialized materials. The sheer volume of chip production globally necessitates continuous innovation and supply of these essential fabrication materials.

The End-user Industry landscape is highly diversified, but Consumer Electronics continues to be the largest consumer of semiconductor materials, followed closely by the Telecommunication sector. The burgeoning Automotive industry, with its increasing integration of sophisticated electronic systems for autonomous driving, advanced driver-assistance systems (ADAS), and powertrain management, is a rapidly growing driver for semiconductor materials, especially SiC and advanced packaging solutions.

- Leading End-User Industry: Consumer Electronics

- Analysis: The insatiable global demand for smartphones, laptops, televisions, and other smart devices ensures a sustained high demand for semiconductor materials. The rapid upgrade cycles and the introduction of new features constantly fuel the need for advanced and cost-effective semiconductor components.

The strategic importance of Silicon Carbide (SiC) as a material segment, coupled with the manufacturing prowess of East Asian countries, and the consistent demand from Consumer Electronics, forms the bedrock of leadership in the Asia-Pacific semiconductor materials market.

Asia-Pacific Semiconductor Materials Market Product Innovations

Product innovations in the Asia-Pacific semiconductor materials market are intensely focused on enhancing performance, enabling miniaturization, and improving energy efficiency. Key advancements include the development of ultra-high purity chemicals with ppb-level impurities for advanced lithography and etching processes, crucial for sub-10nm fabrication nodes. Furthermore, innovations in Silicon Carbide (SiC) materials are yielding wafers with reduced defect densities and improved crystal quality, leading to higher device yields and reliability in high-power applications like electric vehicles. Researchers are also exploring novel Gallium Manganese Arsenide (GaAs) formulations for faster and more efficient radio-frequency (RF) devices essential for 5G and future wireless communication. The emphasis is on materials that can withstand higher operating temperatures and voltages, thereby enabling more compact and powerful electronic components across consumer electronics, telecommunications, and automotive sectors.

Propelling Factors for Asia-Pacific Semiconductor Materials Market Growth

The growth of the Asia-Pacific semiconductor materials market is propelled by a potent combination of technological advancements, robust economic trends, and supportive regulatory frameworks. The relentless pursuit of enhanced computing power, increased data processing capabilities, and the miniaturization of electronic devices across consumer electronics, telecommunications, and automotive sectors is a primary driver. The global rollout of 5G networks, the proliferation of Artificial Intelligence (AI) and Machine Learning (ML) applications, and the accelerating adoption of electric vehicles (EVs) are creating unprecedented demand for advanced semiconductor materials like Silicon Carbide (SiC) and Gallium Arsenide (GaAs). Government initiatives across key Asia-Pacific nations, such as financial incentives, tax breaks, and R&D funding aimed at bolstering domestic semiconductor manufacturing capabilities, are further catalyzing market expansion. Additionally, strategic investments by leading companies in expanding production capacity and developing next-generation materials are solidifying this growth trajectory.

Obstacles in the Asia-Pacific Semiconductor Materials Market Market

Despite its robust growth, the Asia-Pacific semiconductor materials market faces several significant obstacles. Intense global competition and pricing pressures can impact profit margins for material suppliers. Supply chain disruptions, exacerbated by geopolitical tensions and natural disasters, pose a constant threat to timely delivery and production continuity. The stringent quality control and high purity requirements for semiconductor materials necessitate substantial investment in advanced manufacturing processes and quality assurance, creating high entry barriers. Furthermore, the rapid pace of technological obsolescence means that companies must continuously invest in R&D to stay competitive, risking significant losses if new materials or processes fail to gain market traction. Regulatory complexities and trade restrictions in certain regions can also impede market access and expansion.

Future Opportunities in Asia-Pacific Semiconductor Materials Market

The Asia-Pacific semiconductor materials market is poised for significant future opportunities. The escalating demand for advanced materials in emerging applications such as AI accelerators, IoT devices, and advanced driver-assistance systems (ADAS) in the automotive sector presents a substantial growth avenue. The continued global transition towards renewable energy sources and electric mobility will drive further demand for high-performance materials like SiC for power electronics. Opportunities also lie in the development of novel materials for next-generation packaging technologies, enabling more compact and powerful electronic devices. Furthermore, government initiatives aimed at fostering domestic semiconductor ecosystems in various Asia-Pacific countries offer fertile ground for market expansion and strategic partnerships. The increasing focus on sustainability within the electronics industry also opens doors for greener material solutions and manufacturing processes.

Major Players in the Asia-Pacific Semiconductor Materials Market Ecosystem

- UTAC Holdings Ltd

- Sumitomo Chemical Co Ltd

- Indium Corporation

- Kyocera Corporation

- LG Chem Ltd

- Dow Chemical Co

- Henkel AG & Company KGAA

- BASF SE

- Showa Denko Materials Co Ltd

- Intel Corporation

Key Developments in Asia-Pacific Semiconductor Materials Market Industry

- December 2021: Intel Corporation announced its plan to establish a semiconductor manufacturing facility in India, a move aimed at bolstering the 'Aatmanirbhar Bharat' program and supporting research and innovation in the industry.

- August 2021: Sumitomo Chemical decided to expand its production capacity for high-purity chemicals for semiconductors. This expansion includes installing new production lines to double the capability for high-purity sulfuric acid at its Ehime Works in Japan and improving the capacity for high-purity ammonia water at the Iksan Plant of its subsidiary, Dongwoo Fine-Chem Co., Ltd., in South Korea. The new lines are expected to commence operations in the first half of fiscal 2024 for Ehime Works and the second half of fiscal 2023 for the Iksan Plant.

Strategic Asia-Pacific Semiconductor Materials Market Market Forecast

The strategic forecast for the Asia-Pacific semiconductor materials market is overwhelmingly positive, projecting sustained high growth driven by innovation and market demand. Key growth catalysts include the ever-increasing need for advanced materials in consumer electronics, telecommunications, and the burgeoning automotive sector, particularly for electric vehicles. The continued global push towards 5G deployment, AI integration, and the Internet of Things (IoT) will further fuel demand for specialized materials like Silicon Carbide (SiC) and Gallium Arsenide (GaAs). Government support for domestic semiconductor manufacturing and R&D across the region will act as a significant tailwind, fostering investment and technological advancement. Emerging opportunities in advanced packaging and sustainable material solutions will also contribute to the market's lucrative future, making the Asia-Pacific region a critical hub for semiconductor material innovation and supply.

Asia-Pacific Semiconductor Materials Market Segmentation

-

1. Material

- 1.1. Silicon Carbide (SiC)

- 1.2. Gallium Manganese Arsenide (GaAs)

- 1.3. Copper Indium Gallium Selenide (CIGS)

- 1.4. Molybdenum Disulfide (MoS)

- 1.5. Bismuth Telluride (Bi2Te3)

-

2. Application

- 2.1. Fabrication

- 2.2. Packaging

-

3. End-user Industry

- 3.1. Consumer Electronics

- 3.2. Telecommunication

- 3.3. Manufacturing

- 3.4. Automotive

- 3.5. Energy and Utility

- 3.6. Other End-User Industries

Asia-Pacific Semiconductor Materials Market Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. Japan

- 1.3. South Korea

- 1.4. India

- 1.5. Australia

- 1.6. New Zealand

- 1.7. Indonesia

- 1.8. Malaysia

- 1.9. Singapore

- 1.10. Thailand

- 1.11. Vietnam

- 1.12. Philippines

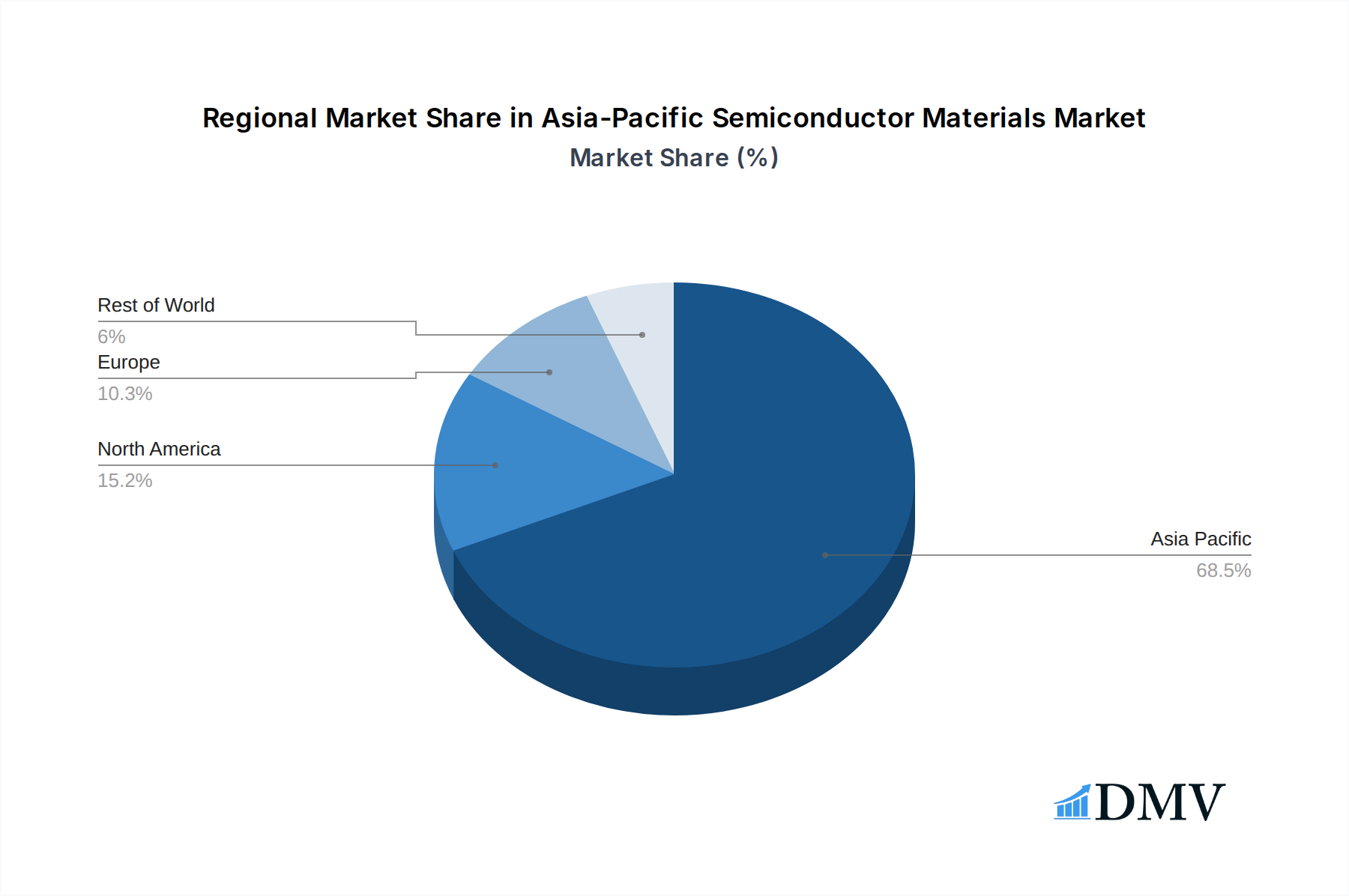

Asia-Pacific Semiconductor Materials Market Regional Market Share

Geographic Coverage of Asia-Pacific Semiconductor Materials Market

Asia-Pacific Semiconductor Materials Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.40% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material

- 5.1.1. Silicon Carbide (SiC)

- 5.1.2. Gallium Manganese Arsenide (GaAs)

- 5.1.3. Copper Indium Gallium Selenide (CIGS)

- 5.1.4. Molybdenum Disulfide (MoS)

- 5.1.5. Bismuth Telluride (Bi2Te3)

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Fabrication

- 5.2.2. Packaging

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Consumer Electronics

- 5.3.2. Telecommunication

- 5.3.3. Manufacturing

- 5.3.4. Automotive

- 5.3.5. Energy and Utility

- 5.3.6. Other End-User Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Material

- 6. Asia-Pacific Semiconductor Materials Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material

- 6.1.1. Silicon Carbide (SiC)

- 6.1.2. Gallium Manganese Arsenide (GaAs)

- 6.1.3. Copper Indium Gallium Selenide (CIGS)

- 6.1.4. Molybdenum Disulfide (MoS)

- 6.1.5. Bismuth Telluride (Bi2Te3)

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Fabrication

- 6.2.2. Packaging

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Consumer Electronics

- 6.3.2. Telecommunication

- 6.3.3. Manufacturing

- 6.3.4. Automotive

- 6.3.5. Energy and Utility

- 6.3.6. Other End-User Industries

- 6.1. Market Analysis, Insights and Forecast - by Material

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 UTAC Holdings Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Sumitomo Chemical Co Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Indium Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Kyocera Corporation

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 LG Chem Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Dow Chemical Co

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Henkel AG & Company KGAA

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 BASF SE

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Showa Denko Materials Co Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Intel Corporation

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 UTAC Holdings Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Asia-Pacific Semiconductor Materials Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Asia-Pacific Semiconductor Materials Market Share (%) by Company 2025

List of Tables

- Table 1: Asia-Pacific Semiconductor Materials Market Revenue Million Forecast, by Material 2020 & 2033

- Table 2: Asia-Pacific Semiconductor Materials Market Volume K Unit Forecast, by Material 2020 & 2033

- Table 3: Asia-Pacific Semiconductor Materials Market Revenue Million Forecast, by Application 2020 & 2033

- Table 4: Asia-Pacific Semiconductor Materials Market Volume K Unit Forecast, by Application 2020 & 2033

- Table 5: Asia-Pacific Semiconductor Materials Market Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 6: Asia-Pacific Semiconductor Materials Market Volume K Unit Forecast, by End-user Industry 2020 & 2033

- Table 7: Asia-Pacific Semiconductor Materials Market Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Asia-Pacific Semiconductor Materials Market Volume K Unit Forecast, by Region 2020 & 2033

- Table 9: Asia-Pacific Semiconductor Materials Market Revenue Million Forecast, by Material 2020 & 2033

- Table 10: Asia-Pacific Semiconductor Materials Market Volume K Unit Forecast, by Material 2020 & 2033

- Table 11: Asia-Pacific Semiconductor Materials Market Revenue Million Forecast, by Application 2020 & 2033

- Table 12: Asia-Pacific Semiconductor Materials Market Volume K Unit Forecast, by Application 2020 & 2033

- Table 13: Asia-Pacific Semiconductor Materials Market Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 14: Asia-Pacific Semiconductor Materials Market Volume K Unit Forecast, by End-user Industry 2020 & 2033

- Table 15: Asia-Pacific Semiconductor Materials Market Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Asia-Pacific Semiconductor Materials Market Volume K Unit Forecast, by Country 2020 & 2033

- Table 17: China Asia-Pacific Semiconductor Materials Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: China Asia-Pacific Semiconductor Materials Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Japan Asia-Pacific Semiconductor Materials Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Japan Asia-Pacific Semiconductor Materials Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 21: South Korea Asia-Pacific Semiconductor Materials Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: South Korea Asia-Pacific Semiconductor Materials Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 23: India Asia-Pacific Semiconductor Materials Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: India Asia-Pacific Semiconductor Materials Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 25: Australia Asia-Pacific Semiconductor Materials Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Australia Asia-Pacific Semiconductor Materials Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 27: New Zealand Asia-Pacific Semiconductor Materials Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: New Zealand Asia-Pacific Semiconductor Materials Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 29: Indonesia Asia-Pacific Semiconductor Materials Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Indonesia Asia-Pacific Semiconductor Materials Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 31: Malaysia Asia-Pacific Semiconductor Materials Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Malaysia Asia-Pacific Semiconductor Materials Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: Singapore Asia-Pacific Semiconductor Materials Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Singapore Asia-Pacific Semiconductor Materials Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 35: Thailand Asia-Pacific Semiconductor Materials Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Thailand Asia-Pacific Semiconductor Materials Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Vietnam Asia-Pacific Semiconductor Materials Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Vietnam Asia-Pacific Semiconductor Materials Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 39: Philippines Asia-Pacific Semiconductor Materials Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Philippines Asia-Pacific Semiconductor Materials Market Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia-Pacific Semiconductor Materials Market?

The projected CAGR is approximately 3.40%.

2. Which companies are prominent players in the Asia-Pacific Semiconductor Materials Market?

Key companies in the market include UTAC Holdings Ltd, Sumitomo Chemical Co Ltd, Indium Corporation, Kyocera Corporation, LG Chem Ltd, Dow Chemical Co, Henkel AG & Company KGAA, BASF SE, Showa Denko Materials Co Ltd, Intel Corporation.

3. What are the main segments of the Asia-Pacific Semiconductor Materials Market?

The market segments include Material, Application, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 26.08 Million as of 2022.

5. What are some drivers contributing to market growth?

Technological Progress and Product Innovation in Electronic Materials; Increased Demand for Consumer Electronics.

6. What are the notable trends driving market growth?

Silicon Segment to Witness Significant Growth.

7. Are there any restraints impacting market growth?

Complexity of the Manufacturing Process.

8. Can you provide examples of recent developments in the market?

December 2021: Intel Corporation announced that it would open a semiconductor manufacturing facility in India. The announcement by the company comes after Union Cabinet's recent decision on semiconductors, which will support research and innovation in the industry and enhance production, bolstering the 'Aatmanirbhar Bharat' program.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia-Pacific Semiconductor Materials Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia-Pacific Semiconductor Materials Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia-Pacific Semiconductor Materials Market?

To stay informed about further developments, trends, and reports in the Asia-Pacific Semiconductor Materials Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence