Key Insights

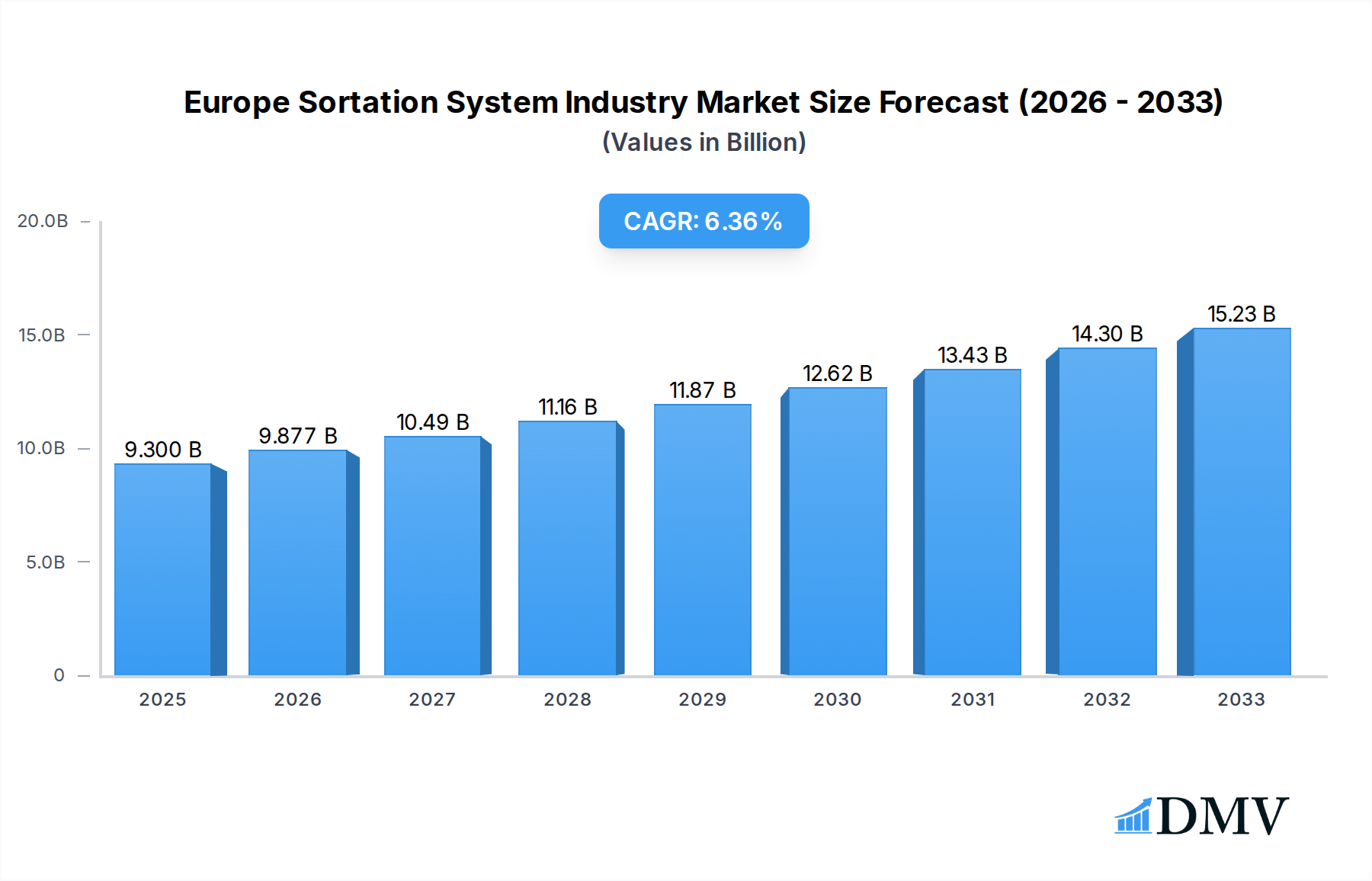

The European Sortation System Industry is poised for substantial growth, with an estimated market size of $9.3 billion in 2025 and a projected Compound Annual Growth Rate (CAGR) of 6.3% throughout the forecast period of 2025-2033. This robust expansion is primarily driven by the escalating demand for efficient and automated material handling solutions across various sectors. The e-commerce boom has significantly amplified the need for advanced sortation systems in the Post and Parcel and Retail industries, enabling faster order fulfillment and last-mile delivery. Furthermore, the increasing adoption of automation in sectors like Food and Beverages, Pharmaceuticals, and Airports to enhance operational efficiency, reduce labor costs, and minimize errors is a critical growth catalyst. Investments in modernizing logistics infrastructure and the pursuit of greater supply chain visibility are also fueling market penetration.

Europe Sortation System Industry Market Size (In Billion)

Despite the strong growth trajectory, certain factors could moderate the pace of expansion. The high initial capital investment required for sophisticated sortation systems, particularly for small and medium-sized enterprises, presents a significant barrier. Moreover, the complexity of integration with existing legacy systems and the need for skilled personnel to operate and maintain these advanced technologies pose challenges. Nevertheless, the continuous evolution of technologies such as artificial intelligence, machine learning, and robotics in sortation systems, along with strategic collaborations and mergers among key players, are expected to drive innovation and create new market opportunities, ensuring a dynamic and evolving European sortation system landscape.

Europe Sortation System Industry Company Market Share

Europe Sortation System Industry Market Composition & Trends

The European sortation system industry is characterized by a dynamic market structure driven by increasing demand for automated logistics solutions across diverse end-user segments. The market is moderately concentrated, with key players like Murata Machinery Ltd, TGW Systems Inc, Interroll Holding AG, Vanderlande Industries Nederland BV, Fives Group, Bastian Solutions Inc, Siemens AG, Viastore Systems Gmbh, KNAPP AG, Honeywell Intelligrated, Dematic Corp (KION Group), Daifuku Co Ltd, and Beumer Group GmbH holding significant market share. Innovation catalysts include the relentless pursuit of operational efficiency, labor cost reduction, and the growing complexity of supply chains, particularly in e-commerce. Regulatory landscapes, while not overtly restrictive, emphasize safety standards and data privacy, influencing system design and implementation. Substitute products, such as manual sorting or simpler conveyor systems, are gradually being phased out due to their inherent inefficiencies for higher-volume operations. End-user profiles are diverse, spanning the high-volume needs of Post and Parcel and Retail sectors, the precision requirements of Pharmaceuticals, and the specialized demands of Food and Beverages and Airports. Mergers and acquisitions (M&A) activities, with estimated deal values in the billions of Euros, are strategically reshaping the competitive landscape as companies seek to expand their technological capabilities and market reach. The market share distribution is influenced by the adoption rates of advanced technologies like Artificial Intelligence (AI) and the Internet of Things (IoT) within sortation systems.

- Market Concentration: Moderately concentrated, with a few dominant players.

- Innovation Catalysts: Operational efficiency, labor cost reduction, e-commerce growth.

- Regulatory Influence: Focus on safety standards and data privacy.

- Substitute Products: Manual sorting, simpler conveyor systems (decreasing relevance).

- Key End-User Segments: Post and Parcel, Retail, Pharmaceuticals, Food & Beverages, Airports.

- M&A Activity: Significant, with deal values estimated in the billions of Euros.

Europe Sortation System Industry Industry Evolution

The Europe sortation system industry has witnessed a profound evolution over the historical period of 2019-2024, driven by an unprecedented surge in e-commerce and a heightened awareness of operational efficiency. This period laid a robust foundation for the projected market growth from 2025 to 2033. During the historical phase, market growth trajectories were largely shaped by the increasing need to handle a higher volume and variety of parcels, especially in the Post and Parcel and Retail sectors. Companies invested heavily in upgrading their existing infrastructure to accommodate the rapid expansion of online shopping. Technological advancements played a pivotal role, with a significant adoption of automated sorters, including cross-belt sorters, tilt-tray sorters, and increasingly, advanced robotics integrated into sortation processes. The base year of 2025 marks a crucial point where these historical trends have solidified, and the market is poised for accelerated expansion.

Shifting consumer demands, such as the expectation for faster delivery times and greater transparency in the supply chain, have further propelled the adoption of sophisticated sortation systems. This has led to a higher demand for systems capable of handling a wider range of item sizes, weights, and shapes, including fragile goods and irregular items. The Pharmaceuticals and Food and Beverages industries, with their stringent regulatory requirements and temperature-sensitive product needs, have also been significant contributors to the market's development, demanding highly specialized and accurate sortation solutions. The "Other End-user Industries" segment, encompassing sectors like manufacturing and wholesale distribution, is also demonstrating a growing interest in optimizing internal logistics through advanced sortation technologies.

The period leading up to 2025 has seen a consistent upward trend in the adoption metrics of automated sortation systems, with growth rates for sophisticated solutions often exceeding XX% year-on-year. This adoption is not merely about replacing manual labor but about enhancing throughput, reducing errors, and improving the overall speed and reliability of logistics operations. The investment in advanced sortation systems, which can range from hundreds of thousands to several million Euros per installation, has become a strategic imperative for businesses looking to maintain a competitive edge. Looking ahead to the forecast period of 2025-2033, the industry is expected to experience continued robust growth, with market expansion driven by further technological innovations, increasing labor costs, and the ongoing digitalization of supply chains across Europe. The estimated market value in 2025 is projected to be in the billions of Euros, underscoring the significant economic impact of this sector.

Leading Regions, Countries, or Segments in Europe Sortation System Industry

The Post and Parcel segment stands as the undeniable leader within the European sortation system industry. Its dominance is a direct consequence of the meteoric rise of e-commerce across the continent, a trend that has irrevocably altered logistical demands. The sheer volume of parcels processed daily necessitates highly efficient, accurate, and scalable sortation solutions, making this segment the largest consumer of advanced sortation technologies. Investment trends within this segment are consistently high, with postal operators and large logistics providers continually upgrading their infrastructure to meet ever-increasing throughput requirements and to reduce delivery times.

- Dominant Segment: Post and Parcel.

- Key Drivers for Dominance:

- E-commerce Growth: Unprecedented surge in online retail driving parcel volumes.

- High Throughput Demands: Need for rapid and accurate sorting of millions of items daily.

- Labor Cost Optimization: Automation is critical to manage rising labor expenses.

- Technological Adoption: Early and widespread adoption of advanced automated sortation systems.

- Network Expansion: Continuous investment in new hubs and upgrades to existing facilities.

The regulatory support in this sector, while not a direct subsidy, is geared towards facilitating efficient trade and logistics, indirectly benefiting the sortation system market. Furthermore, the competitive landscape within the Post and Parcel segment is intense, compelling companies to invest in cutting-edge technology to maintain market share and operational efficiency. The integration of AI and machine learning for optimized routing and sorting decisions is becoming standard practice.

While Post and Parcel leads, other segments like Retail are also significant growth drivers. The retail sector, especially with the convergence of online and brick-and-mortar operations (omnichannel retail), requires sophisticated sortation for both forward and reverse logistics. This involves sorting goods for direct customer delivery, for store replenishment, and for returns management, all demanding flexible and adaptable sortation systems. The Food and Beverages and Pharmaceuticals segments, while smaller in volume, represent high-value markets due to their specialized requirements for temperature control, hygiene, and precision sorting. Airports, for their baggage handling needs, and the "Other End-user Industries" also contribute to the overall market size, albeit with their unique operational challenges and technological preferences. However, the sheer volume and continuous investment from the Post and Parcel sector firmly establish it as the primary engine driving the European sortation system industry forward. The total market size for sortation systems in Europe is projected to reach billions of Euros by 2025, with the Post and Parcel segment constituting a substantial portion of this value.

Europe Sortation System Industry Product Innovations

The Europe sortation system industry is continually evolving with groundbreaking product innovations designed to enhance efficiency, flexibility, and scalability. Key advancements include the integration of Artificial Intelligence (AI) and Machine Learning (ML) for predictive maintenance and optimized sorting paths, significantly reducing downtime and improving throughput. Modular sortation systems are gaining traction, allowing businesses to easily scale operations up or down based on demand fluctuations, a crucial advantage in the volatile e-commerce landscape. High-speed sorters, capable of processing thousands of items per hour, are becoming standard, alongside sophisticated vision systems for accurate item identification and dimensioning. Furthermore, the development of specialized sorters for unique items, such as flat items, polybags, and fragile goods, addresses the growing diversity of products handled by logistics operations. These innovations are not just about speed but also about precision, reducing errors and damage, ultimately leading to substantial cost savings and improved customer satisfaction across industries like Post and Parcel, Retail, and Food and Beverages.

Propelling Factors for Europe Sortation System Industry Growth

The European sortation system industry's growth is propelled by a confluence of powerful factors. The relentless expansion of e-commerce is the primary driver, demanding faster and more efficient parcel handling. Increasing labor costs across Europe are incentivizing businesses to invest in automation to reduce operational expenses and mitigate labor shortages. Technological advancements, particularly in AI, robotics, and IoT, are enabling the development of smarter, more agile, and cost-effective sortation solutions. Stringent regulatory requirements for supply chain transparency and efficiency, coupled with a growing emphasis on sustainability and reduced carbon footprints in logistics, further encourage the adoption of optimized sorting processes that minimize waste and energy consumption. The need for enhanced operational accuracy and reduced error rates in complex supply chains also plays a crucial role.

- E-commerce Growth: Exponential increase in online shopping driving parcel volumes.

- Rising Labor Costs: Automation offers a solution to mitigate increasing operational expenses.

- Technological Advancements: Innovations in AI, robotics, and IoT enabling smarter systems.

- Regulatory Push: Demand for efficiency, transparency, and sustainability in logistics.

- Accuracy and Error Reduction: Minimizing mistakes in high-volume sorting operations.

Obstacles in the Europe Sortation System Industry Market

Despite robust growth, the Europe sortation system industry faces several significant obstacles. The high initial capital investment required for sophisticated automated systems can be a barrier for smaller enterprises. Supply chain disruptions, including shortages of key components and increased lead times for manufacturing, can impact project timelines and the availability of new installations. Navigating complex and sometimes fragmented regulatory landscapes across different European countries can pose challenges for system integration and compliance. Furthermore, the need for skilled personnel to operate and maintain these advanced systems creates a demand that can be difficult to meet, exacerbating labor concerns. Competitive pressures, while driving innovation, also lead to pricing challenges, potentially impacting profit margins for manufacturers and integrators.

- High Initial Capital Investment: Significant upfront costs for advanced automation.

- Supply Chain Disruptions: Component shortages and extended lead times affecting deployment.

- Regulatory Fragmentation: Navigating varying regulations across European nations.

- Skilled Labor Shortage: Difficulty in finding qualified personnel for operation and maintenance.

- Intense Competition: Price pressures impacting profitability.

Future Opportunities in Europe Sortation System Industry

The Europe sortation system industry is ripe with future opportunities. The continued growth of e-commerce, particularly in emerging markets within Europe and in specialized niches like same-day delivery, will fuel demand for high-speed and intelligent sorting solutions. The increasing adoption of Industry 4.0 principles and the Industrial Internet of Things (IIoT) will lead to the development of even more interconnected and data-driven sortation systems, offering predictive analytics and real-time optimization. The expansion into new end-user segments, such as pharmaceutical cold chain logistics and specialized industrial manufacturing, presents untapped potential. Furthermore, the growing focus on reverse logistics and sustainability offers opportunities for innovative sortation systems designed for efficient returns processing and waste reduction. The development of more adaptable and flexible systems capable of handling a wider variety of unconventional package types will also be a key area for growth.

- Continued E-commerce Expansion: Ongoing demand from online retail and faster delivery models.

- Industry 4.0 Integration: Development of data-driven, interconnected, and intelligent systems.

- Emerging End-User Markets: Growth in specialized logistics for pharmaceuticals, manufacturing, and more.

- Reverse Logistics & Sustainability: Opportunities in efficient returns processing and waste minimization.

- Adaptable System Development: Solutions for diverse and unconventional package types.

Major Players in the Europe Sortation System Industry Ecosystem

- Murata Machinery Ltd

- TGW Systems Inc

- Interroll Holding AG

- Vanderlande Industries Nederland BV

- Fives Group

- Bastian Solutions Inc

- Siemens AG

- Viastore Systems Gmbh

- KNAPP AG

- Honeywell Intelligrated

- Dematic Corp (KION Group)

- Daifuku Co Ltd

- Beumer Group GmbH

Key Developments in Europe Sortation System Industry Industry

- July 2022: BEUMER launched its new BG Line Sorter and BG Pouch System, which utilizes next-generation technology to deliver enhanced flexibility and scalability for mid-size-volume operations. The BG Line Sorter solution extends parcel and material handling operations by helping them sort a wide range of items while utilizing a modular design to ensure flexibility and optimize the use of space.

- May 2022: OPEX Corporation participated for the first time in LogiMAT, Europe's largest international trade show for intralogistics solutions and process management. OPEX's automation experts conducted continuous live demonstrations of the company's Sure Sort sorting system and showcased all of OPEX's warehouse automation solutions designed to help businesses thrive.

Strategic Europe Sortation System Industry Market Forecast

The strategic forecast for the Europe sortation system industry anticipates sustained and significant growth driven by the persistent expansion of e-commerce and the ongoing digital transformation of logistics operations. Key market potential lies in the increasing demand for highly automated and intelligent sortation solutions that can adapt to fluctuating volumes and diverse product types. The integration of advanced technologies such as AI, machine learning, and robotics will be crucial in enhancing operational efficiency, reducing errors, and optimizing supply chain performance. Furthermore, the growing emphasis on sustainability and the need to minimize the environmental impact of logistics will drive the adoption of energy-efficient and waste-reducing sortation systems. Investments in upgrading existing infrastructure and developing new, state-of-the-art facilities will continue to be a dominant trend, ensuring that the European market remains at the forefront of sortation technology innovation and implementation, with an estimated market value projected to reach billions of Euros in the coming years.

Europe Sortation System Industry Segmentation

-

1. End User

- 1.1. Post and Parcel

- 1.2. Airport

- 1.3. Food and Beverages

- 1.4. Retail

- 1.5. Pharmaceuticals

- 1.6. Other End-user Industries

Europe Sortation System Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

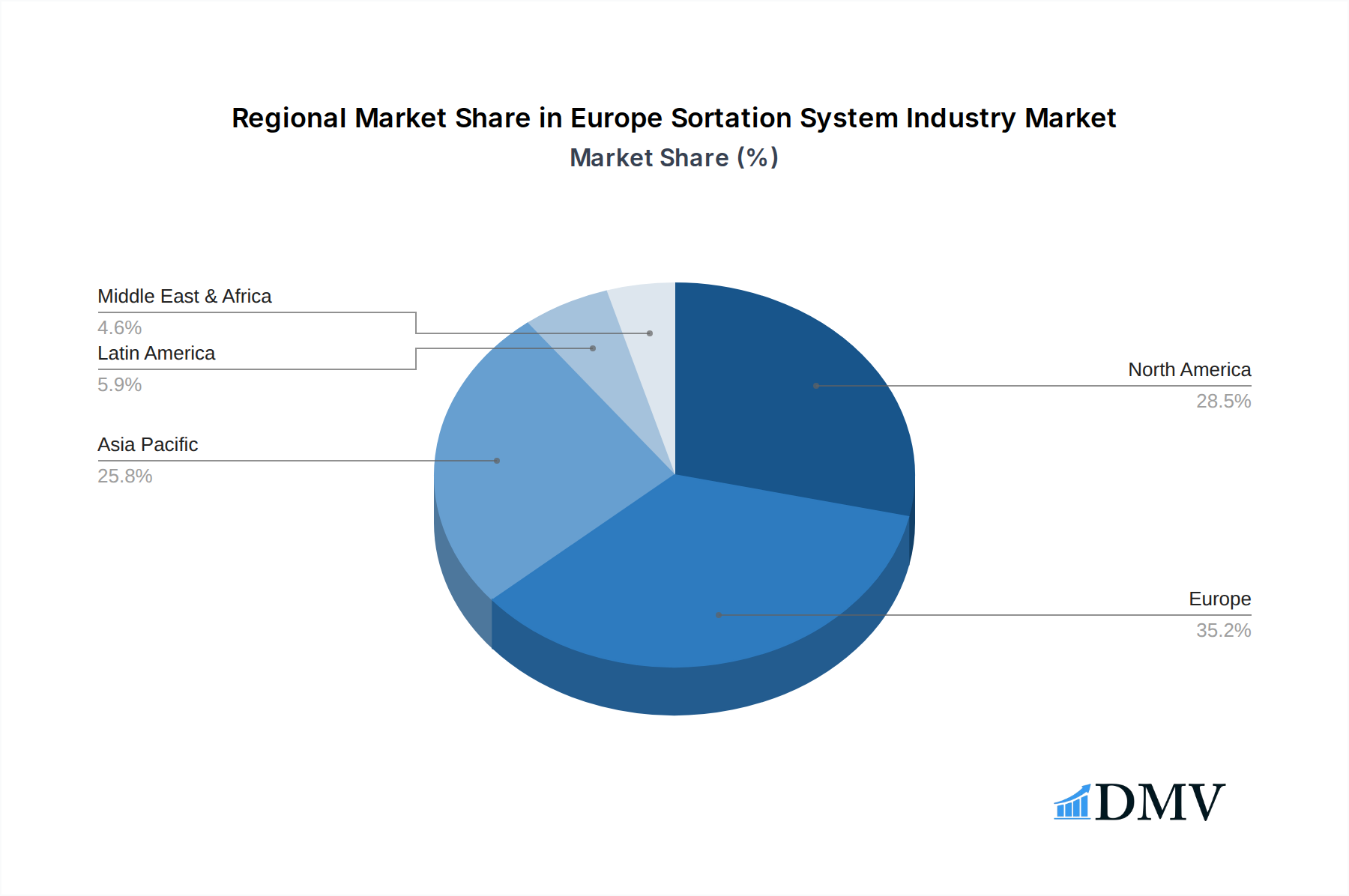

Europe Sortation System Industry Regional Market Share

Geographic Coverage of Europe Sortation System Industry

Europe Sortation System Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by End User

- 5.1.1. Post and Parcel

- 5.1.2. Airport

- 5.1.3. Food and Beverages

- 5.1.4. Retail

- 5.1.5. Pharmaceuticals

- 5.1.6. Other End-user Industries

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by End User

- 6. Europe Sortation System Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by End User

- 6.1.1. Post and Parcel

- 6.1.2. Airport

- 6.1.3. Food and Beverages

- 6.1.4. Retail

- 6.1.5. Pharmaceuticals

- 6.1.6. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by End User

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Murata Machinery Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 TGW Systems Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Interroll Holding AG

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Vanderlande Industries Nederland BV

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Fives Group

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Bastian Solutions Inc

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Siemens AG

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Viastore Systems Gmbh

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 KNAPP AG*List Not Exhaustive

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Honeywell Intelligrated

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Dematic Corp (KION Group)

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Daifuku Co Ltd

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Beumer Group GmbH

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.1 Murata Machinery Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Sortation System Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe Sortation System Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Sortation System Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 2: Europe Sortation System Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Europe Sortation System Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 4: Europe Sortation System Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 5: United Kingdom Europe Sortation System Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 6: Germany Europe Sortation System Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 7: France Europe Sortation System Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Italy Europe Sortation System Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Spain Europe Sortation System Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Netherlands Europe Sortation System Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Belgium Europe Sortation System Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Sweden Europe Sortation System Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Norway Europe Sortation System Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Poland Europe Sortation System Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Denmark Europe Sortation System Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Sortation System Industry?

The projected CAGR is approximately 6.3%.

2. Which companies are prominent players in the Europe Sortation System Industry?

Key companies in the market include Murata Machinery Ltd, TGW Systems Inc, Interroll Holding AG, Vanderlande Industries Nederland BV, Fives Group, Bastian Solutions Inc, Siemens AG, Viastore Systems Gmbh, KNAPP AG*List Not Exhaustive, Honeywell Intelligrated, Dematic Corp (KION Group), Daifuku Co Ltd, Beumer Group GmbH.

3. What are the main segments of the Europe Sortation System Industry?

The market segments include End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 9.3 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Improving Order Accuracy and SKU Proliferation; Increasing Concerns About Labor Costs and Industrial Automation; Growth in E-commerce.

6. What are the notable trends driving market growth?

The Post and Parcel Segment is Expected to Drive the Market's Growth.

7. Are there any restraints impacting market growth?

High Deployment and Maintenance Costs; Real-time Technical Challenges and the Need for Skilled Workforce.

8. Can you provide examples of recent developments in the market?

July 2022 - BEUMER launched its new BG Line Sorter and BG Pouch System, which utilizes next-generation technology to deliver enhanced flexibility and scalability for mid-size-volume operations. As claimed by the company, the BG Line Sorter solution extends the parcel and material handling operations by helping them sort a wide range of items while utilizing a modular design to ensure flexibility and optimize the use of space.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Sortation System Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Sortation System Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Sortation System Industry?

To stay informed about further developments, trends, and reports in the Europe Sortation System Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence