Key Insights

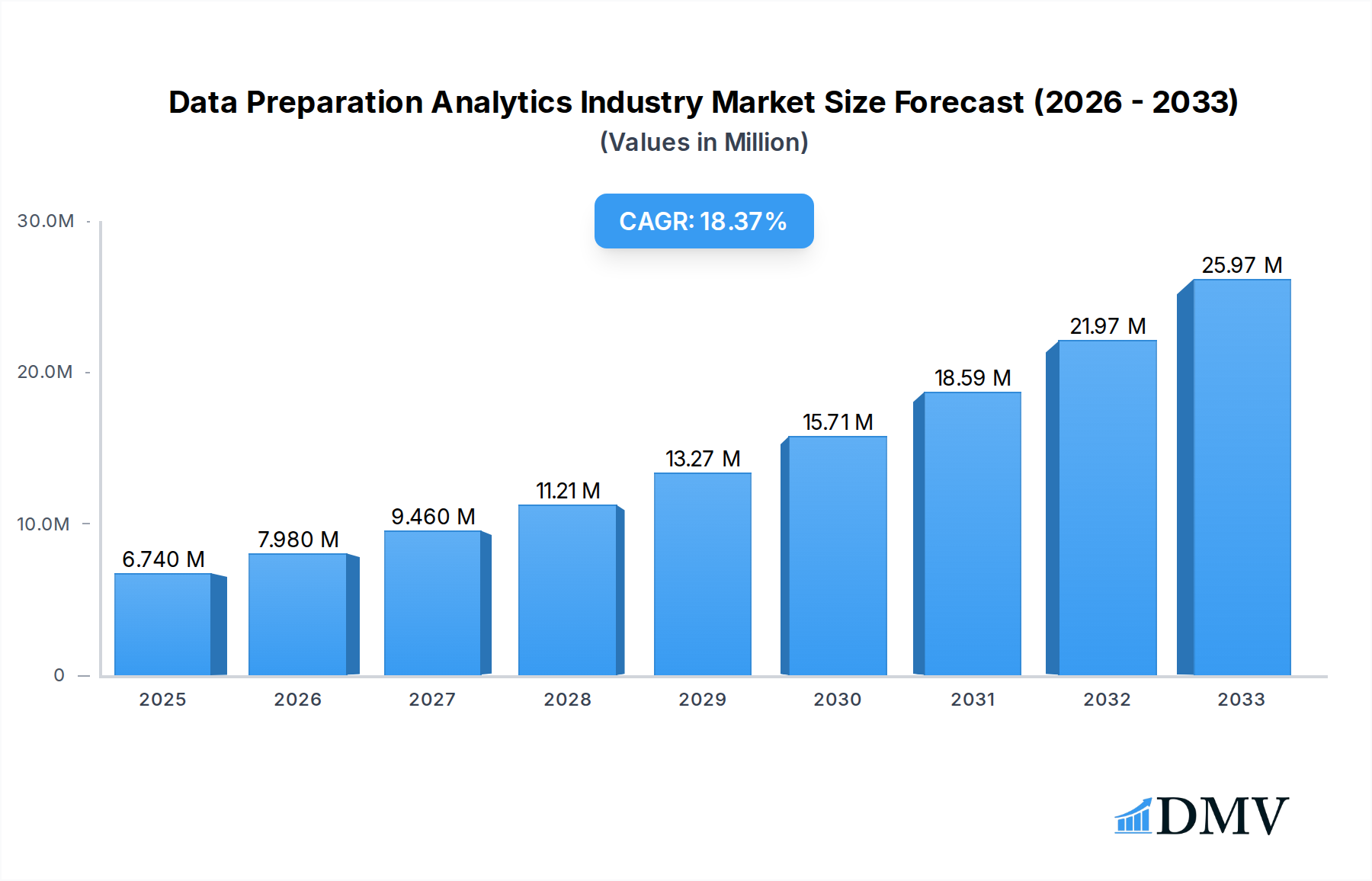

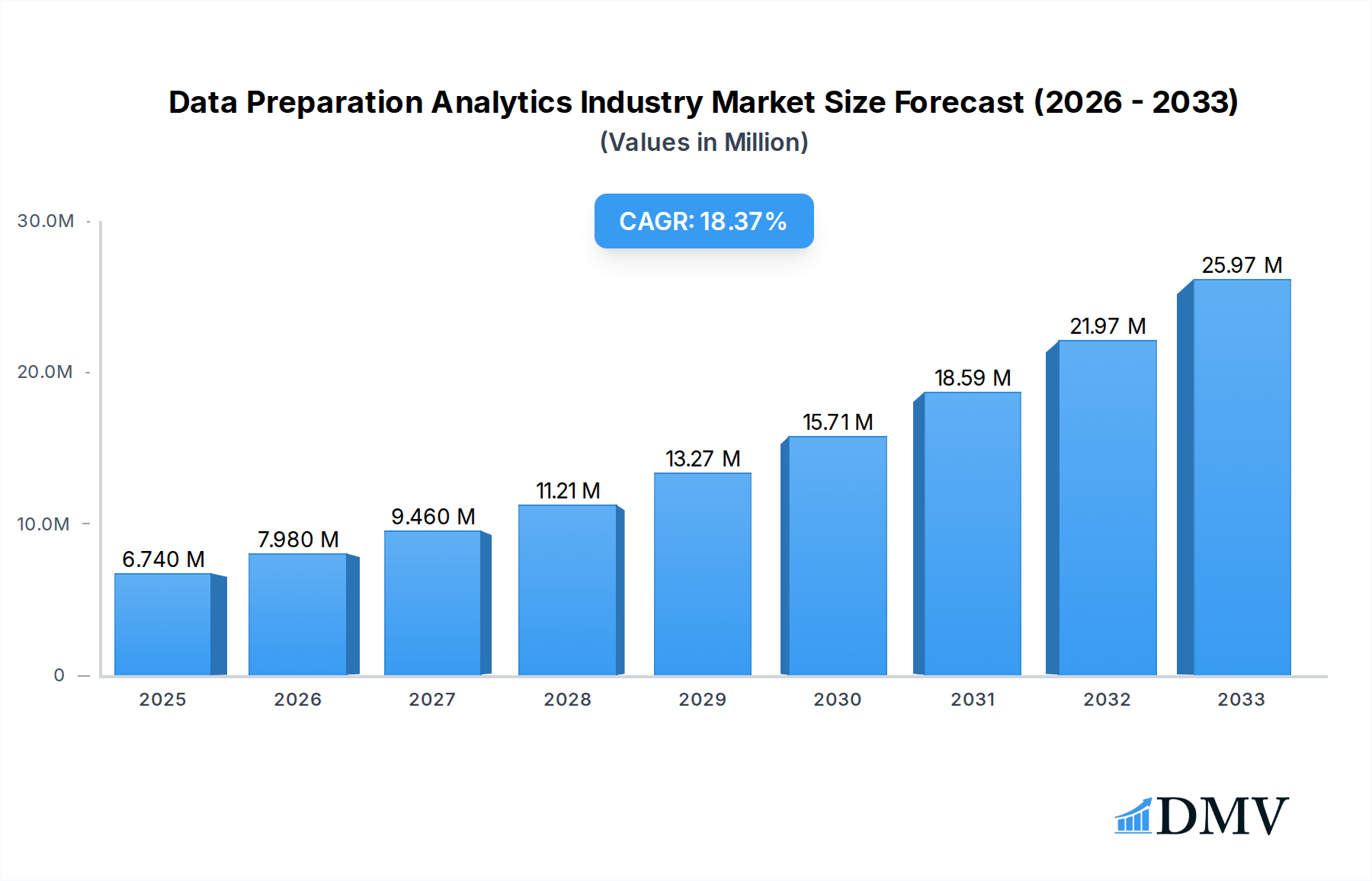

The Data Preparation Analytics Industry is poised for remarkable expansion, currently valued at $6.74 million and projected to grow at a robust compound annual growth rate (CAGR) of 18.74% during the forecast period of 2025-2033. This significant surge is propelled by the increasing volume and complexity of data generated across all sectors, necessitating efficient and effective tools for data cleansing, transformation, and enrichment. The growing recognition of data as a critical business asset, coupled with the demand for advanced analytics to drive strategic decision-making, is a primary driver. Furthermore, the proliferation of big data technologies and the escalating adoption of cloud-based solutions are fueling this growth by making data preparation more accessible and scalable. The industry is witnessing a significant shift towards cloud-based deployment models, offering greater flexibility and cost-effectiveness for businesses of all sizes. Small and Medium Enterprises (SMEs), in particular, are increasingly leveraging these solutions to gain a competitive edge, while large enterprises are focusing on integrating advanced data preparation capabilities into their existing big data ecosystems.

Data Preparation Analytics Industry Market Size (In Million)

The competitive landscape is characterized by the presence of established technology giants and specialized data preparation solution providers, all vying for market share through product innovation and strategic partnerships. Key players such as SAS Institute Inc., IBM Corporation, Oracle Corporation, and Informatica LLC are actively investing in R&D to enhance their offerings with AI-driven capabilities and broader data source connectivity. The BFSI, Healthcare, and Retail sectors are leading the charge in adopting data preparation analytics due to their data-intensive nature and the critical need for accurate insights for fraud detection, patient care optimization, and personalized customer experiences. While the market presents immense opportunities, potential restraints include data security and privacy concerns, the complexity of integrating new tools with legacy systems, and a shortage of skilled data professionals. Nevertheless, the overarching trend towards data-driven operations and the continuous evolution of data preparation technologies suggest a dynamic and high-growth trajectory for the Data Preparation Analytics Industry.

Data Preparation Analytics Industry Company Market Share

Data Preparation Analytics Industry Market Composition & Trends

The global Data Preparation Analytics market is experiencing robust expansion, driven by the escalating need for clean, structured data to fuel advanced analytics and AI initiatives. Market concentration is moderate, with several key players vying for dominance. Innovation is primarily focused on automating complex data wrangling processes, enhancing data quality, and enabling self-service data preparation for a broader user base. Regulatory landscapes, particularly data privacy laws like GDPR and CCPA, are indirectly influencing the market by emphasizing the importance of data governance and compliance, which data preparation tools facilitate. Substitute products, such as manual data cleaning methods or less sophisticated ETL tools, are progressively being outpaced by the efficiency and intelligence offered by dedicated data preparation platforms. End-user profiles are diverse, encompassing data scientists, business analysts, and citizen data scientists across all enterprise sizes. Mergers and acquisitions (M&A) are active, with Alteryx's strategic investment in MANTA for $50 Million in December 2022 signifying a trend towards enhancing data lineage capabilities within the ecosystem. The overall market share distribution is a dynamic interplay of established giants and agile innovators, with the market size projected to reach $XX Billion by 2033.

- Market Concentration: Moderate, with a mix of established enterprise vendors and specialized data preparation players.

- Innovation Catalysts: AI/ML integration, self-service analytics, data governance, and cloud-native solutions.

- Regulatory Landscapes: Data privacy and compliance mandates (e.g., GDPR, CCPA) are pushing for robust data governance and quality.

- Substitute Products: Manual data cleaning, basic ETL tools, and spreadsheets are being phased out due to inefficiency.

- End-User Profiles: Data scientists, business analysts, citizen data scientists, IT professionals.

- M&A Activities: Active, with a focus on strengthening data lineage, AI capabilities, and cloud integration. Example: Alteryx investment in MANTA ($50 Million).

Data Preparation Analytics Industry Industry Evolution

The Data Preparation Analytics industry has undergone a significant evolution, transforming from rudimentary data cleansing utilities into sophisticated, AI-powered platforms integral to modern data ecosystems. The historical period from 2019 to 2024 has witnessed an exponential surge in data generation, compelling organizations across all sectors to invest heavily in tools that can effectively manage, cleanse, and transform this deluge of information. Early in this period, the focus was largely on Extract, Transform, Load (ETL) processes, often requiring significant technical expertise and manual intervention. However, the advent of cloud computing and the democratization of data analytics have shifted the paradigm. The base year of 2025 marks a pivotal point where data preparation has transitioned from a back-office IT function to a strategic business enabler. The forecast period, from 2025 to 2033, is expected to see continued rapid growth, fueled by advancements in machine learning, natural language processing (NLP), and automated data discovery.

Technological advancements have been a primary driver of this evolution. The integration of AI and machine learning has enabled automated data profiling, anomaly detection, and intelligent data transformations, drastically reducing the time and effort required for data preparation. This has allowed organizations to move faster from raw data to actionable insights, a crucial competitive advantage in today's data-driven economy. For instance, features like intelligent suggestions for data cleaning and data augmentation are becoming standard. Adoption metrics have steadily climbed, with a significant portion of enterprises reporting increased reliance on dedicated data preparation tools. The market growth trajectory has been impressive, with compound annual growth rates (CAGR) consistently exceeding 15% during the historical period and projected to remain robust.

Shifting consumer and business demands have also played a critical role. As businesses strive for greater agility and faster decision-making, the need for self-service data preparation capabilities has become paramount. This empowers business users, often referred to as citizen data scientists, to prepare data for their specific analytical needs without constant reliance on IT departments. This decentralization of data preparation tasks has opened up new markets and expanded the user base for data preparation solutions. Furthermore, the increasing complexity of data sources, including structured, semi-structured, and unstructured data from various cloud and on-premise systems, necessitates advanced preparation capabilities that can handle this diversity seamlessly. The market size, estimated at $XX Billion in 2025, is on track to reach $XX Billion by 2033, reflecting this sustained growth and the increasing strategic importance of data preparation in the global analytics landscape.

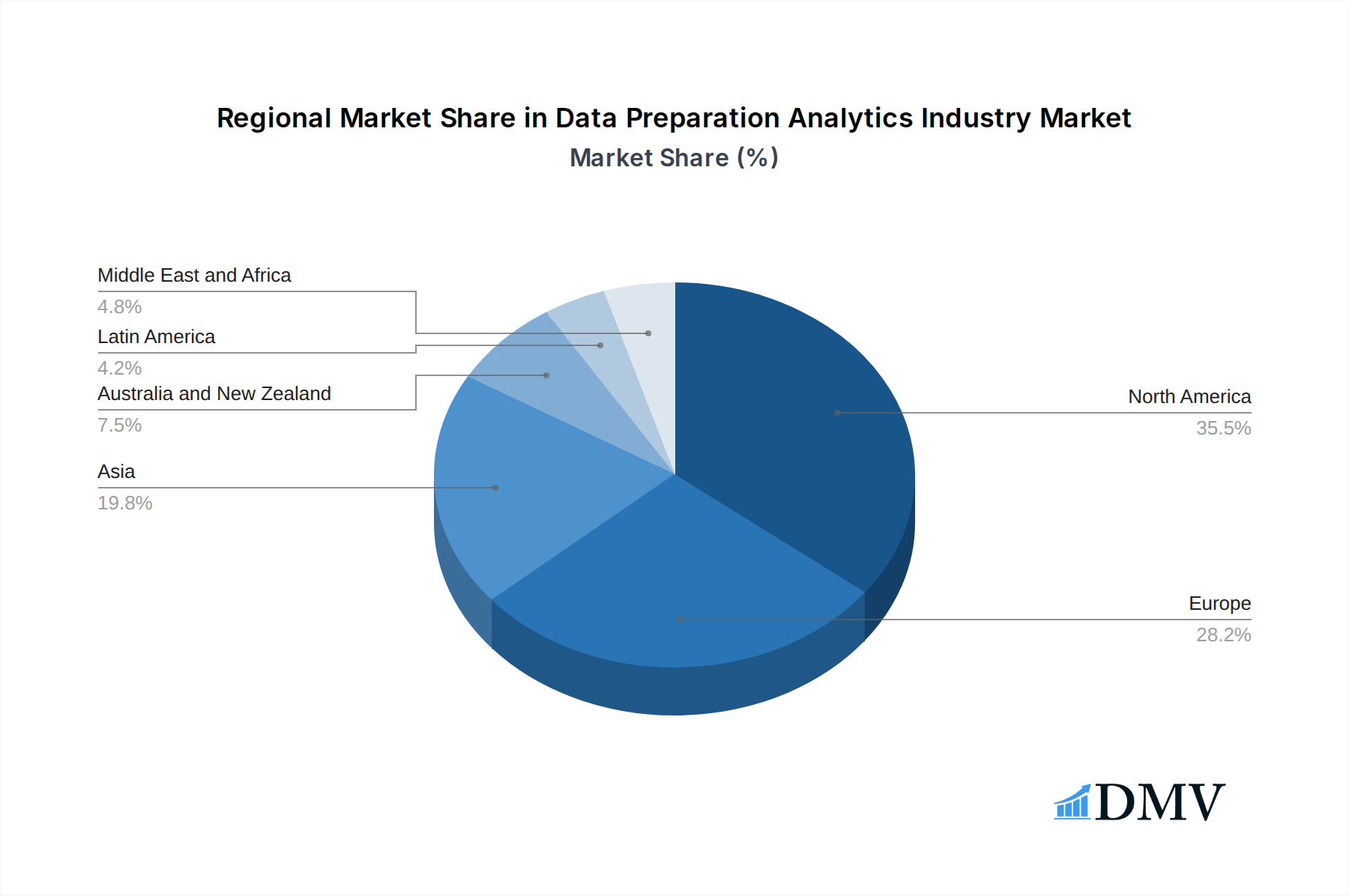

Leading Regions, Countries, or Segments in Data Preparation Analytics Industry

The Data Preparation Analytics industry is witnessing significant regional dominance and segment-specific growth. North America, particularly the United States, stands out as the leading region due to its early adoption of advanced analytics technologies, a strong presence of major technology vendors, and a robust ecosystem of data-intensive industries. The prevalence of cloud-based deployments is a dominant trend, with businesses increasingly leveraging the scalability, flexibility, and cost-effectiveness of cloud infrastructure for their data preparation needs. This segment is expected to grow at a CAGR of XX% during the forecast period.

Within the deployment segment, cloud-based solutions are outperforming on-premise deployments, which are gradually declining in market share, though still significant for highly regulated industries or organizations with existing on-premise investments. Key drivers for cloud adoption include the ease of integration with other cloud-based analytics platforms, reduced IT overhead, and the ability to access cutting-edge features and updates more readily.

Analyzing enterprise size, Large Enterprises represent the largest segment, driven by their substantial data volumes, complex analytical requirements, and the financial resources to invest in advanced data preparation solutions. However, Small and Medium Enterprises (SMEs) are emerging as a high-growth segment, fueled by the increasing availability of more affordable, cloud-based, and user-friendly data preparation tools that enable them to compete with larger organizations by leveraging data insights.

The BFSI (Banking, Financial Services, and Insurance) sector is a primary end-user vertical, owing to the critical need for accurate and compliant data for risk management, fraud detection, customer analytics, and regulatory reporting. The stringent data governance requirements within BFSI necessitate robust data preparation capabilities. Other significant end-user verticals include Healthcare, driven by the demand for data analysis in patient care, research, and operational efficiency, and IT and Telecommunication, which relies heavily on data for network optimization, customer churn prediction, and service improvement. Manufacturing is also a growing segment, utilizing data preparation for supply chain optimization, predictive maintenance, and quality control.

- Leading Region: North America, driven by technological adoption and industry diversity.

- Dominant Deployment: Cloud-based solutions, offering scalability and flexibility.

- Key Drivers: Cost-effectiveness, seamless integration, rapid access to innovations.

- Market Share Growth: Projected to capture XX% of the market by 2033.

- Leading Enterprise Size: Large Enterprises, due to extensive data needs and analytical sophistication.

- Sub-segment Trend: SMEs showing rapid growth with accessible cloud solutions.

- Key End-User Vertical: BFSI, driven by regulatory compliance and complex analytical needs.

- Sub-vertical Growth: Healthcare and IT & Telecommunication are rapidly expanding.

- Investment Trends: Increased investment in cloud infrastructure and AI-powered data preparation tools across all segments.

- Regulatory Support: Favorable regulatory environments in North America and Europe encouraging data governance, indirectly boosting data preparation adoption.

Data Preparation Analytics Industry Product Innovations

Product innovation in the Data Preparation Analytics industry is rapidly advancing, focusing on intelligent automation and enhanced user experience. Key advancements include AI-driven data profiling to automatically identify data quality issues and suggest remedies, as well as natural language querying (NLQ) capabilities that empower business users to interact with data more intuitively. Machine learning algorithms are increasingly being embedded to predict data transformations, automate data cleansing, and even suggest data enrichment strategies, significantly reducing manual effort and accelerating time-to-insight. Technologies like enhanced data lineage tracking are providing greater transparency and auditability, crucial for compliance. Performance metrics are showing improvements in processing speeds for large datasets, with real-time data preparation becoming more prevalent. Unique selling propositions often lie in the seamless integration with existing data ecosystems, the breadth of connectors to various data sources, and the ability to cater to both expert data scientists and less technical business users through intuitive graphical interfaces and guided workflows.

Propelling Factors for Data Preparation Analytics Industry Growth

The growth of the Data Preparation Analytics industry is propelled by several key factors. The exponential increase in data volume, velocity, and variety generated by businesses worldwide necessitates sophisticated tools to manage and derive value. The growing adoption of Artificial Intelligence (AI) and Machine Learning (ML) across industries relies heavily on clean and well-structured data, making data preparation a foundational step. Furthermore, the increasing demand for real-time analytics and business intelligence for faster decision-making drives the need for efficient data preparation processes. Government initiatives promoting digital transformation and the emphasis on data-driven decision-making also contribute significantly. The proliferation of cloud computing services has made advanced data preparation tools more accessible and affordable.

- Big Data Explosion: Increasing data volumes and complexity across all sectors.

- AI/ML Adoption: The indispensable need for clean data to train and deploy AI/ML models.

- Demand for Real-Time Insights: Businesses require immediate access to actionable data for agile decision-making.

- Digital Transformation Initiatives: Government and organizational pushes towards data-centric operations.

- Cloud Computing Accessibility: Lowered barriers to entry for sophisticated data preparation solutions.

Obstacles in the Data Preparation Analytics Industry Market

Despite its robust growth, the Data Preparation Analytics market faces certain obstacles. The complexity of integrating diverse data sources and legacy systems can be a significant challenge for organizations, requiring substantial IT resources and expertise. Data security and privacy concerns, especially with the increasing stringency of regulations like GDPR and CCPA, can lead to hesitancy in adopting cloud-based solutions or sharing sensitive data, impacting adoption rates. The shortage of skilled data professionals capable of effectively utilizing advanced data preparation tools also presents a barrier. Moreover, the initial cost of implementing comprehensive data preparation solutions, although decreasing with cloud offerings, can still be a deterrent for smaller businesses. The competitive landscape, while fostering innovation, can also lead to market fragmentation and confusion for buyers trying to select the most suitable solution.

Future Opportunities in Data Preparation Analytics Industry

The future of the Data Preparation Analytics industry is ripe with opportunities. The burgeoning field of edge computing presents a new frontier, requiring data preparation capabilities at the source of data generation. The continued advancement of AI and ML will lead to even more autonomous and intelligent data preparation tools, capable of self-learning and adapting to evolving data landscapes. The increasing demand for augmented analytics, where data preparation is seamlessly integrated into the analytical workflow, offers significant growth potential. Expansion into emerging markets with growing data analytics adoption will provide new revenue streams. Furthermore, the development of specialized data preparation solutions for niche industries, such as genomics or IoT, will unlock new market segments. The growing trend of data democratization will also fuel demand for user-friendly, self-service data preparation tools.

Major Players in the Data Preparation Analytics Industry Ecosystem

- SAS Institute Inc

- Unifi Software Inc

- IBM Corporation

- Microstrategy Inc

- Paxata Inc

- ClearStory Data Inc

- Alteryx Inc

- Oracle Corporation

- Rapid Insight Inc

- Informatica LLC

- Tableau Software LLC (Salesforce com Inc)

- SAP SE

- Qlik Technologies Inc QlikTech International AB

Key Developments in Data Preparation Analytics Industry Industry

- December 2022: Alteryx, Inc., the Analytics Automation company, announced a strategic investment in MANTA, the data lineage company. MANTA enables businesses to achieve complete visibility into the most complex data environments. With this investment from Alteryx Ventures, the company can bolster product innovation, expand its partner ecosystem, and grow in key markets.

- November 2022: Amazon Web Services (AWS) announced a series of new features for Amazon QuickSight, the cloud computing giant's analytics platform. The update includes new query, forecasting, and data preparation features, adding functionality to QuickSight Q, a natural language query (NLQ) tool.

Strategic Data Preparation Analytics Industry Market Forecast

The strategic outlook for the Data Preparation Analytics industry is exceptionally positive, driven by an undeniable and escalating need for efficient, accurate, and accessible data. The convergence of AI, cloud computing, and the ever-increasing volume of global data continues to be the primary growth catalyst. As businesses across all verticals recognize data as their most valuable asset, the demand for sophisticated data preparation tools that empower both technical and non-technical users will only intensify. The forecast period of 2025–2033 is expected to witness sustained double-digit growth, fueled by innovations in automated data discovery, intelligent cleansing, and seamless integration with advanced analytics and AI platforms. Emerging markets and specialized industry applications will offer significant untapped potential, ensuring a dynamic and expanding market landscape for years to come.

Data Preparation Analytics Industry Segmentation

-

1. Deployment

- 1.1. On-premise

- 1.2. Cloud-based

-

2. Enterprise Size

- 2.1. Small and Medium Enterprises (SMEs)

- 2.2. Large Enterprises

-

3. End-user Vertical

- 3.1. BFSI

- 3.2. Healthcare

- 3.3. Retail

- 3.4. Manufacturing

- 3.5. IT and Telecommunication

- 3.6. Other End-user Verticals

Data Preparation Analytics Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia

- 4. Australia and New Zealand

- 5. Latin America

- 6. Middle East and Africa

Data Preparation Analytics Industry Regional Market Share

Geographic Coverage of Data Preparation Analytics Industry

Data Preparation Analytics Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 18.74% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Deployment

- 5.1.1. On-premise

- 5.1.2. Cloud-based

- 5.2. Market Analysis, Insights and Forecast - by Enterprise Size

- 5.2.1. Small and Medium Enterprises (SMEs)

- 5.2.2. Large Enterprises

- 5.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 5.3.1. BFSI

- 5.3.2. Healthcare

- 5.3.3. Retail

- 5.3.4. Manufacturing

- 5.3.5. IT and Telecommunication

- 5.3.6. Other End-user Verticals

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia

- 5.4.4. Australia and New Zealand

- 5.4.5. Latin America

- 5.4.6. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Deployment

- 6. Global Data Preparation Analytics Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Deployment

- 6.1.1. On-premise

- 6.1.2. Cloud-based

- 6.2. Market Analysis, Insights and Forecast - by Enterprise Size

- 6.2.1. Small and Medium Enterprises (SMEs)

- 6.2.2. Large Enterprises

- 6.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 6.3.1. BFSI

- 6.3.2. Healthcare

- 6.3.3. Retail

- 6.3.4. Manufacturing

- 6.3.5. IT and Telecommunication

- 6.3.6. Other End-user Verticals

- 6.1. Market Analysis, Insights and Forecast - by Deployment

- 7. North America Data Preparation Analytics Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Deployment

- 7.1.1. On-premise

- 7.1.2. Cloud-based

- 7.2. Market Analysis, Insights and Forecast - by Enterprise Size

- 7.2.1. Small and Medium Enterprises (SMEs)

- 7.2.2. Large Enterprises

- 7.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 7.3.1. BFSI

- 7.3.2. Healthcare

- 7.3.3. Retail

- 7.3.4. Manufacturing

- 7.3.5. IT and Telecommunication

- 7.3.6. Other End-user Verticals

- 7.1. Market Analysis, Insights and Forecast - by Deployment

- 8. Europe Data Preparation Analytics Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Deployment

- 8.1.1. On-premise

- 8.1.2. Cloud-based

- 8.2. Market Analysis, Insights and Forecast - by Enterprise Size

- 8.2.1. Small and Medium Enterprises (SMEs)

- 8.2.2. Large Enterprises

- 8.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 8.3.1. BFSI

- 8.3.2. Healthcare

- 8.3.3. Retail

- 8.3.4. Manufacturing

- 8.3.5. IT and Telecommunication

- 8.3.6. Other End-user Verticals

- 8.1. Market Analysis, Insights and Forecast - by Deployment

- 9. Asia Data Preparation Analytics Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Deployment

- 9.1.1. On-premise

- 9.1.2. Cloud-based

- 9.2. Market Analysis, Insights and Forecast - by Enterprise Size

- 9.2.1. Small and Medium Enterprises (SMEs)

- 9.2.2. Large Enterprises

- 9.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 9.3.1. BFSI

- 9.3.2. Healthcare

- 9.3.3. Retail

- 9.3.4. Manufacturing

- 9.3.5. IT and Telecommunication

- 9.3.6. Other End-user Verticals

- 9.1. Market Analysis, Insights and Forecast - by Deployment

- 10. Australia and New Zealand Data Preparation Analytics Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Deployment

- 10.1.1. On-premise

- 10.1.2. Cloud-based

- 10.2. Market Analysis, Insights and Forecast - by Enterprise Size

- 10.2.1. Small and Medium Enterprises (SMEs)

- 10.2.2. Large Enterprises

- 10.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 10.3.1. BFSI

- 10.3.2. Healthcare

- 10.3.3. Retail

- 10.3.4. Manufacturing

- 10.3.5. IT and Telecommunication

- 10.3.6. Other End-user Verticals

- 10.1. Market Analysis, Insights and Forecast - by Deployment

- 11. Latin America Data Preparation Analytics Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Deployment

- 11.1.1. On-premise

- 11.1.2. Cloud-based

- 11.2. Market Analysis, Insights and Forecast - by Enterprise Size

- 11.2.1. Small and Medium Enterprises (SMEs)

- 11.2.2. Large Enterprises

- 11.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 11.3.1. BFSI

- 11.3.2. Healthcare

- 11.3.3. Retail

- 11.3.4. Manufacturing

- 11.3.5. IT and Telecommunication

- 11.3.6. Other End-user Verticals

- 11.1. Market Analysis, Insights and Forecast - by Deployment

- 12. Middle East and Africa Data Preparation Analytics Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Deployment

- 12.1.1. On-premise

- 12.1.2. Cloud-based

- 12.2. Market Analysis, Insights and Forecast - by Enterprise Size

- 12.2.1. Small and Medium Enterprises (SMEs)

- 12.2.2. Large Enterprises

- 12.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 12.3.1. BFSI

- 12.3.2. Healthcare

- 12.3.3. Retail

- 12.3.4. Manufacturing

- 12.3.5. IT and Telecommunication

- 12.3.6. Other End-user Verticals

- 12.1. Market Analysis, Insights and Forecast - by Deployment

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 SAS Institute Inc

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Unifi Software Inc

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 IBM Corporation

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Microstrategy Inc

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Paxata Inc

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 ClearStory Data Inc

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Alteryx Inc

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Oracle Corporation*List Not Exhaustive

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Rapid Insight Inc

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 Informatica LLC

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.11 Tableau Software LLC (Salesforce com Inc )

- 13.1.11.1. Company Overview

- 13.1.11.2. Products

- 13.1.11.3. Company Financials

- 13.1.11.4. SWOT Analysis

- 13.1.12 SAP SE

- 13.1.12.1. Company Overview

- 13.1.12.2. Products

- 13.1.12.3. Company Financials

- 13.1.12.4. SWOT Analysis

- 13.1.13 Qlik Technologies Inc QlikTech International AB

- 13.1.13.1. Company Overview

- 13.1.13.2. Products

- 13.1.13.3. Company Financials

- 13.1.13.4. SWOT Analysis

- 13.1.1 SAS Institute Inc

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Data Preparation Analytics Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Data Preparation Analytics Industry Revenue (Million), by Deployment 2025 & 2033

- Figure 3: North America Data Preparation Analytics Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 4: North America Data Preparation Analytics Industry Revenue (Million), by Enterprise Size 2025 & 2033

- Figure 5: North America Data Preparation Analytics Industry Revenue Share (%), by Enterprise Size 2025 & 2033

- Figure 6: North America Data Preparation Analytics Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 7: North America Data Preparation Analytics Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 8: North America Data Preparation Analytics Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: North America Data Preparation Analytics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Data Preparation Analytics Industry Revenue (Million), by Deployment 2025 & 2033

- Figure 11: Europe Data Preparation Analytics Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 12: Europe Data Preparation Analytics Industry Revenue (Million), by Enterprise Size 2025 & 2033

- Figure 13: Europe Data Preparation Analytics Industry Revenue Share (%), by Enterprise Size 2025 & 2033

- Figure 14: Europe Data Preparation Analytics Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 15: Europe Data Preparation Analytics Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 16: Europe Data Preparation Analytics Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Europe Data Preparation Analytics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Data Preparation Analytics Industry Revenue (Million), by Deployment 2025 & 2033

- Figure 19: Asia Data Preparation Analytics Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 20: Asia Data Preparation Analytics Industry Revenue (Million), by Enterprise Size 2025 & 2033

- Figure 21: Asia Data Preparation Analytics Industry Revenue Share (%), by Enterprise Size 2025 & 2033

- Figure 22: Asia Data Preparation Analytics Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 23: Asia Data Preparation Analytics Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 24: Asia Data Preparation Analytics Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Asia Data Preparation Analytics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Australia and New Zealand Data Preparation Analytics Industry Revenue (Million), by Deployment 2025 & 2033

- Figure 27: Australia and New Zealand Data Preparation Analytics Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 28: Australia and New Zealand Data Preparation Analytics Industry Revenue (Million), by Enterprise Size 2025 & 2033

- Figure 29: Australia and New Zealand Data Preparation Analytics Industry Revenue Share (%), by Enterprise Size 2025 & 2033

- Figure 30: Australia and New Zealand Data Preparation Analytics Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 31: Australia and New Zealand Data Preparation Analytics Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 32: Australia and New Zealand Data Preparation Analytics Industry Revenue (Million), by Country 2025 & 2033

- Figure 33: Australia and New Zealand Data Preparation Analytics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Latin America Data Preparation Analytics Industry Revenue (Million), by Deployment 2025 & 2033

- Figure 35: Latin America Data Preparation Analytics Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 36: Latin America Data Preparation Analytics Industry Revenue (Million), by Enterprise Size 2025 & 2033

- Figure 37: Latin America Data Preparation Analytics Industry Revenue Share (%), by Enterprise Size 2025 & 2033

- Figure 38: Latin America Data Preparation Analytics Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 39: Latin America Data Preparation Analytics Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 40: Latin America Data Preparation Analytics Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: Latin America Data Preparation Analytics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: Middle East and Africa Data Preparation Analytics Industry Revenue (Million), by Deployment 2025 & 2033

- Figure 43: Middle East and Africa Data Preparation Analytics Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 44: Middle East and Africa Data Preparation Analytics Industry Revenue (Million), by Enterprise Size 2025 & 2033

- Figure 45: Middle East and Africa Data Preparation Analytics Industry Revenue Share (%), by Enterprise Size 2025 & 2033

- Figure 46: Middle East and Africa Data Preparation Analytics Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 47: Middle East and Africa Data Preparation Analytics Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 48: Middle East and Africa Data Preparation Analytics Industry Revenue (Million), by Country 2025 & 2033

- Figure 49: Middle East and Africa Data Preparation Analytics Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Data Preparation Analytics Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 2: Global Data Preparation Analytics Industry Revenue Million Forecast, by Enterprise Size 2020 & 2033

- Table 3: Global Data Preparation Analytics Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 4: Global Data Preparation Analytics Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Data Preparation Analytics Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 6: Global Data Preparation Analytics Industry Revenue Million Forecast, by Enterprise Size 2020 & 2033

- Table 7: Global Data Preparation Analytics Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 8: Global Data Preparation Analytics Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: Global Data Preparation Analytics Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 10: Global Data Preparation Analytics Industry Revenue Million Forecast, by Enterprise Size 2020 & 2033

- Table 11: Global Data Preparation Analytics Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 12: Global Data Preparation Analytics Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Global Data Preparation Analytics Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 14: Global Data Preparation Analytics Industry Revenue Million Forecast, by Enterprise Size 2020 & 2033

- Table 15: Global Data Preparation Analytics Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 16: Global Data Preparation Analytics Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 17: Global Data Preparation Analytics Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 18: Global Data Preparation Analytics Industry Revenue Million Forecast, by Enterprise Size 2020 & 2033

- Table 19: Global Data Preparation Analytics Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 20: Global Data Preparation Analytics Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 21: Global Data Preparation Analytics Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 22: Global Data Preparation Analytics Industry Revenue Million Forecast, by Enterprise Size 2020 & 2033

- Table 23: Global Data Preparation Analytics Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 24: Global Data Preparation Analytics Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 25: Global Data Preparation Analytics Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 26: Global Data Preparation Analytics Industry Revenue Million Forecast, by Enterprise Size 2020 & 2033

- Table 27: Global Data Preparation Analytics Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 28: Global Data Preparation Analytics Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Data Preparation Analytics Industry?

The projected CAGR is approximately 18.74%.

2. Which companies are prominent players in the Data Preparation Analytics Industry?

Key companies in the market include SAS Institute Inc, Unifi Software Inc, IBM Corporation, Microstrategy Inc, Paxata Inc, ClearStory Data Inc, Alteryx Inc, Oracle Corporation*List Not Exhaustive, Rapid Insight Inc, Informatica LLC, Tableau Software LLC (Salesforce com Inc ), SAP SE, Qlik Technologies Inc QlikTech International AB.

3. What are the main segments of the Data Preparation Analytics Industry?

The market segments include Deployment, Enterprise Size, End-user Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.74 Million as of 2022.

5. What are some drivers contributing to market growth?

Demand for Self-service Data Preparation Tools; Increasing Demand for Data Analytics.

6. What are the notable trends driving market growth?

IT and Telecom Segment is Expected to Hold a Significant Market Share.

7. Are there any restraints impacting market growth?

Limited Budgets and Low Investments owing to Complexities and Associated Risks..

8. Can you provide examples of recent developments in the market?

December 2022: Alteryx, Inc., the Analytics Automation company, announced a strategic investment in MANTA, the data lineage company. MANTA enables businesses to achieve complete visibility into the most complex data environments. With this investment from Alteryx Ventures, the company can bolster product innovation, expand its partner ecosystem, and grow in key markets.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Data Preparation Analytics Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Data Preparation Analytics Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Data Preparation Analytics Industry?

To stay informed about further developments, trends, and reports in the Data Preparation Analytics Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence