Key Insights

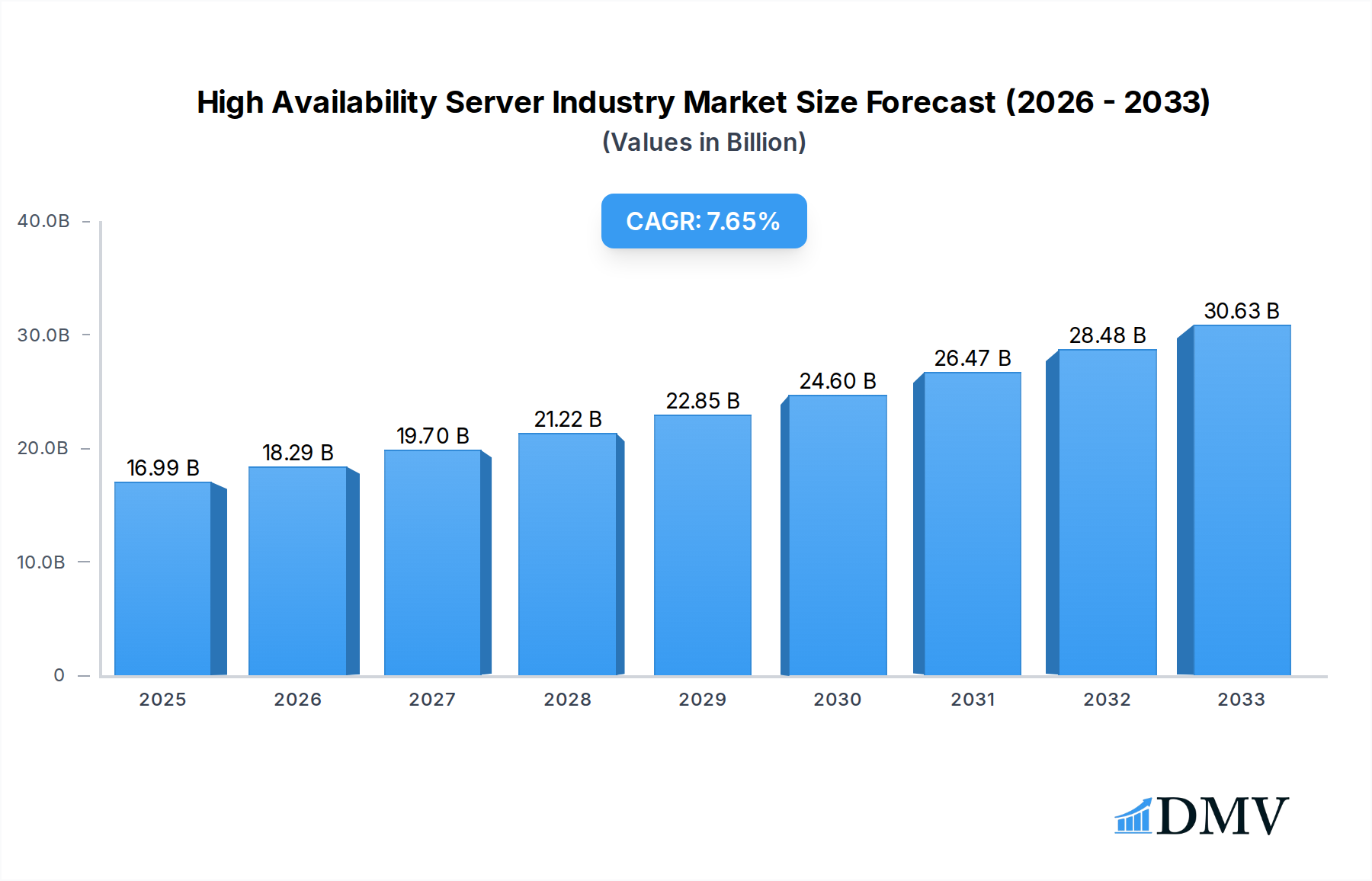

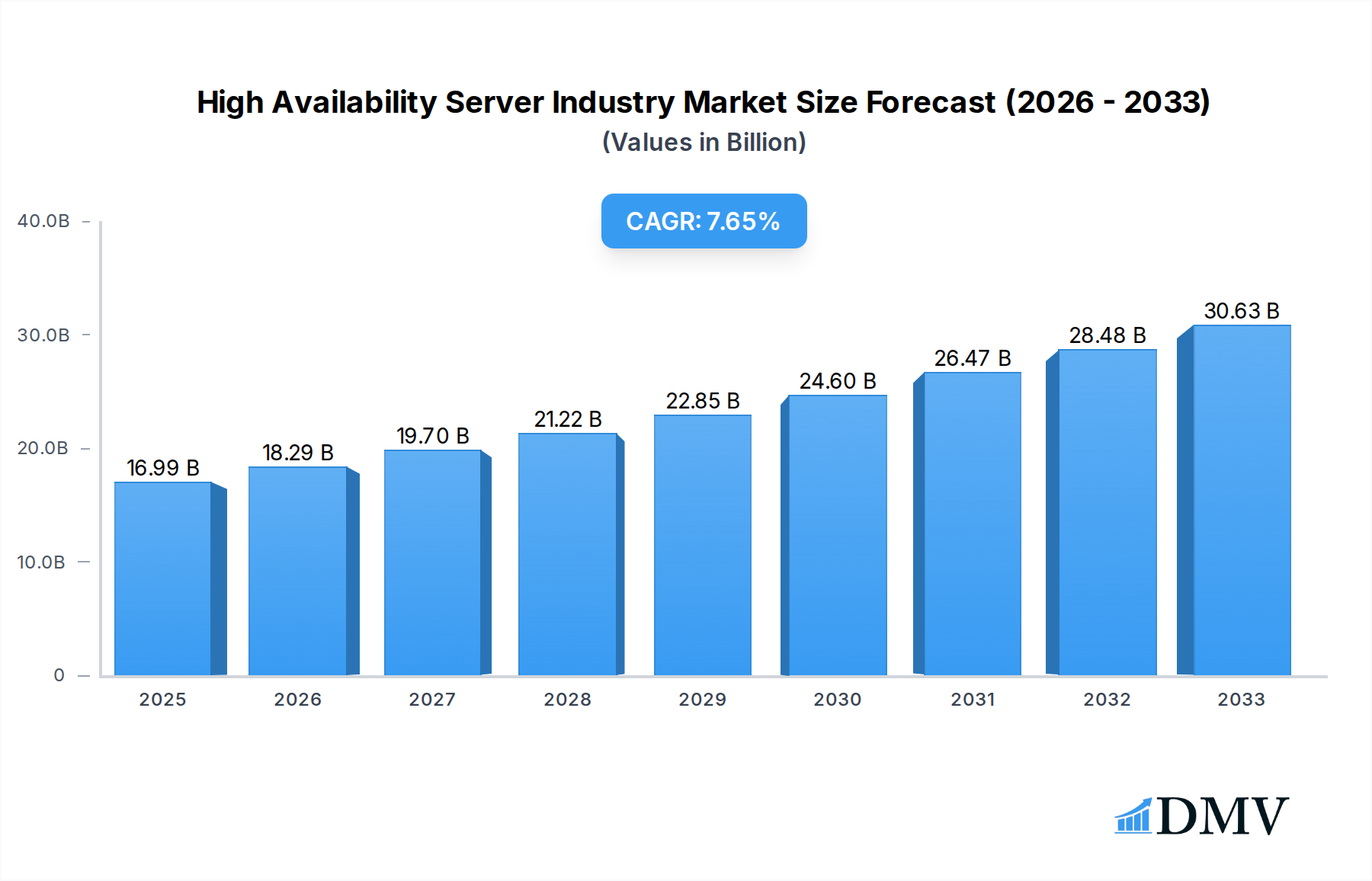

The High Availability Server Industry is poised for significant expansion, with a robust projected market size of $16.99 billion in 2025. This growth is underpinned by an impressive Compound Annual Growth Rate (CAGR) of 7.71%, indicating sustained and dynamic market momentum throughout the forecast period of 2025-2033. The escalating demand for uninterrupted business operations across all sectors is the primary catalyst. Industries such as IT & Telecommunication, BFSI, Retail, and Healthcare are heavily reliant on continuous uptime to maintain customer trust, ensure data integrity, and prevent substantial financial losses stemming from outages. The increasing adoption of cloud-based solutions, driven by their scalability and cost-effectiveness, is a major trend, although on-premise deployments continue to hold relevance for specific security and compliance needs. The proliferation of digital services, e-commerce, and the critical need for resilient IT infrastructure in an increasingly connected world are further fueling this upward trajectory.

High Availability Server Industry Market Size (In Billion)

The market is characterized by strong growth drivers, including the relentless digital transformation initiatives across enterprises, the growing complexity of IT environments, and the ever-present threat of cyberattacks and natural disasters that necessitate robust disaster recovery and business continuity plans. Emerging trends such as the integration of AI and machine learning for predictive maintenance of server hardware, advancements in virtualization technologies, and the rise of edge computing are expected to further stimulate market penetration. However, the industry faces certain restraints, including the high initial investment costs associated with implementing comprehensive high availability solutions, potential complexities in integration with existing legacy systems, and the ongoing challenge of finding skilled IT professionals to manage and maintain these sophisticated infrastructures. Nevertheless, the overarching imperative for operational resilience and the continuous innovation in server technology are expected to outweigh these challenges, ensuring a healthy and expanding market.

High Availability Server Industry Company Market Share

High Availability Server Industry Report: Unlocking Uninterrupted Performance and Business Continuity

Gain unparalleled insights into the High Availability Server Industry with this comprehensive market research report. Spanning the study period 2019–2033, our analysis dives deep into the critical factors driving sustained business operations and digital resilience. We provide a robust base year of 2025 and an estimated year of 2025, followed by a meticulous forecast period of 2025–2033, building upon a detailed historical period from 2019–2024. This report is an indispensable resource for stakeholders seeking to navigate the evolving landscape of mission-critical server infrastructure, disaster recovery solutions, and enterprise-grade computing.

High Availability Server Industry Market Composition & Trends

The High Availability Server Industry is characterized by a dynamic market composition driven by relentless innovation and increasing demand for zero-downtime operations. Market concentration is moderate, with key players like IBM Corp, Hewlett Packard Enterprise Development LP, Dell Inc, and Oracle Corp holding significant, yet fragmented, market shares. Innovation catalysts are primarily focused on enhancing server redundancy, improving fault tolerance mechanisms, and integrating advanced AI-driven predictive maintenance to preempt failures. Regulatory landscapes, particularly in sectors like BFSI and Healthcare, are increasingly mandating stringent uptime requirements, further fueling market growth. Substitute products, such as lower-cost, less resilient server options, face diminishing appeal as the cost of downtime escalates. End-user profiles reveal a growing reliance on high availability across IT & Telecommunication, Retail, and Industrial sectors, driven by the imperative to maintain customer engagement and operational continuity. Merger and acquisition (M&A) activities are on the rise, with substantial deal values in the multi-billion dollar range, indicating consolidation and strategic expansion. For instance, recent M&A activities have seen companies investing billions to acquire specialized high availability solutions providers.

- Market Share Distribution: The top 5 players hold approximately 60% of the market share, with the remaining distributed among mid-tier and niche providers.

- M&A Deal Values: Average M&A deal values in the last three years have exceeded $5 billion, reflecting intense strategic acquisitions.

- Innovation Focus: Key areas include active-active configurations, hot-standby systems, and software-defined high availability.

- Regulatory Impact: Mandates for service level agreements (SLAs) with uptime guarantees of 99.999% are a significant growth driver.

High Availability Server Industry Industry Evolution

The High Availability Server Industry has witnessed a remarkable evolution, transforming from basic redundancy solutions to sophisticated, intelligent systems designed to guarantee continuous business operations. Throughout the historical period (2019–2024), the market experienced steady growth, fueled by the increasing digitalization of businesses and the inherent risks associated with single points of failure. Early adoption was primarily concentrated within large enterprises in the IT & Telecommunication and BFSI sectors, where the financial implications of downtime were most severe. However, the landscape has shifted dramatically, with cloud-based high availability server solutions emerging as a dominant force. This shift has democratized access to robust uptime capabilities, making them accessible to small and medium-sized businesses as well. Technological advancements have been pivotal, moving from hardware-based failover to more agile and cost-effective software-defined solutions. The introduction of containerization and microservices architectures has further necessitated resilient infrastructure, with high availability becoming an integral component of modern application deployment. Consumer demands have also evolved; customers now expect seamless, uninterrupted access to services, with any downtime leading to immediate dissatisfaction and potential customer churn. This has pushed companies to prioritize mission-critical infrastructure that can withstand unexpected disruptions. The market growth trajectory has been consistently upward, with an average annual growth rate of approximately 8% during the historical period. Adoption metrics for advanced high availability features, such as real-time data replication and automated failover orchestration, have surged by over 40% in the last two years alone. The base year of 2025 represents a critical juncture, with market participants increasingly investing in AI and machine learning for predictive failure analysis and proactive threat mitigation, aiming to achieve an unprecedented level of system reliability and operational resilience throughout the forecast period of 2025–2033. The increasing adoption of Linux operating systems in server environments, coupled with the robust capabilities of cloud-based deployments, are key indicators of this ongoing transformation.

Leading Regions, Countries, or Segments in High Availability Server Industry

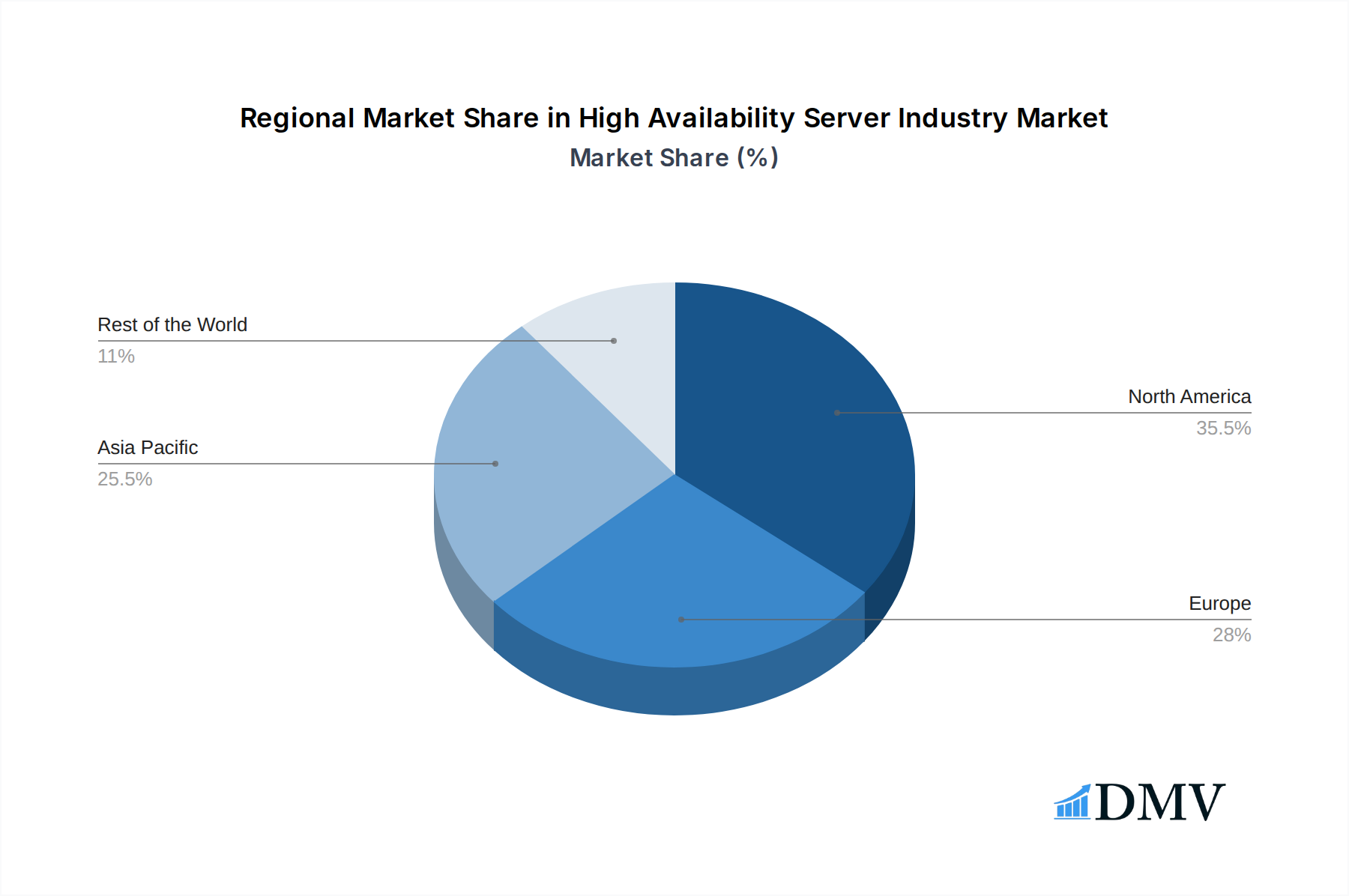

The High Availability Server Industry is experiencing significant regional dominance and segment growth, with North America and Europe leading the charge in adoption and investment. These regions benefit from a mature technological infrastructure, a high concentration of enterprises in critical sectors, and robust regulatory frameworks that mandate stringent uptime requirements. The IT & Telecommunication and BFSI sectors are consistently the largest end-user industries, driving substantial demand for enterprise-grade high availability servers. Within the deployment segment, Cloud-based solutions are rapidly overtaking On-premise deployments, especially in the forecast period, due to their scalability, flexibility, and cost-effectiveness. This shift is particularly pronounced in the North American market, where cloud adoption rates are exceptionally high. The Linux operating system holds a dominant position in server environments, offering unparalleled performance, security, and flexibility for high availability configurations, outperforming Windows and Other Operating System categories like UNIX and BSD in terms of new deployments and upgrades. Investment trends in these leading regions are heavily skewed towards research and development of advanced fault tolerance technologies, disaster recovery planning, and data replication strategies. Regulatory support, such as data residency laws and cybersecurity mandates, indirectly bolsters the demand for highly available and resilient systems, as compliance often necessitates robust infrastructure. For instance, in the BFSI sector, regulatory bodies impose strict uptime requirements, pushing financial institutions to invest billions in redundant server architectures and failover solutions. The Retail sector is also increasingly adopting high availability to ensure uninterrupted e-commerce operations and in-store point-of-sale systems, especially during peak shopping seasons, with projected investments in this segment exceeding $10 billion annually by 2027. The Healthcare industry's adoption is driven by the critical need for continuous access to patient records and medical systems, with investments in this area projected to reach $8 billion by 2028.

- Dominant Region: North America, driven by technological leadership and significant investments from major cloud providers and enterprises.

- Key Segment Drivers (Deployment): Cloud-based solutions are favored for scalability, cost efficiency, and rapid deployment.

- Key Segment Drivers (Operating System): Linux dominates due to its open-source nature, performance, and extensive support for high availability features.

- Key Segment Drivers (End-user Industry): IT & Telecommunication and BFSI lead due to inherent criticality and regulatory pressures; Retail and Healthcare show rapidly growing adoption.

- Investment Trends: Billions are being invested in R&D for AI-driven predictive maintenance and automated disaster recovery.

High Availability Server Industry Product Innovations

Product innovation in the High Availability Server Industry is centered on enhancing performance, reliability, and ease of management. Key advancements include the development of active-active server clusters that distribute workload seamlessly across multiple nodes, providing near-instantaneous failover. Enhanced data replication technologies now offer real-time synchronization with minimal latency, ensuring data integrity even during catastrophic events. Innovations in software-defined networking (SDN) and storage virtualization are also crucial, enabling greater flexibility and agility in configuring and managing HA environments. Performance metrics are consistently improving, with average failover times now measured in milliseconds. Unique selling propositions often lie in integrated AI-powered predictive analytics that can anticipate hardware failures before they occur, reducing unplanned downtime and associated costs.

Propelling Factors for High Availability Server Industry Growth

The High Availability Server Industry is experiencing robust growth fueled by several key factors. The escalating threat of cyberattacks and the increasing sophistication of ransomware attacks necessitate uninterrupted system operations and swift recovery capabilities. The growing adoption of cloud computing and the demand for 24/7 service availability across all industries, from e-commerce to essential services, are paramount. Digital transformation initiatives are driving businesses to rely more heavily on their IT infrastructure, making downtime a significant business risk. Furthermore, the increasing volume of data generation and the need for real-time analytics require highly available platforms. Regulatory compliance mandates in sectors like finance and healthcare are also crucial drivers. Investments in R&D are leading to more advanced and cost-effective disaster recovery solutions.

- Cybersecurity Threats: The constant risk of cyberattacks compels organizations to invest in resilient systems.

- Cloud Adoption: The widespread shift to cloud environments relies heavily on underlying high availability infrastructure.

- Digital Transformation: Businesses' increasing dependence on digital operations makes uptime critical.

- Regulatory Compliance: Mandates for data integrity and service availability in sensitive sectors are key.

- Data Growth: The exponential increase in data requires robust and always-on processing capabilities.

Obstacles in the High Availability Server Industry Market

Despite its growth, the High Availability Server Industry faces several obstacles. The complexity of implementation and management of advanced HA solutions can be a significant barrier for smaller organizations, requiring specialized expertise. The high initial capital investment for robust hardware and software can also be prohibitive, although cloud-based models are mitigating this. Interoperability issues between different vendor solutions can create integration challenges. Furthermore, potential single points of failure in network infrastructure or shared services can undermine even the most sophisticated server HA strategies. Supply chain disruptions, as seen in recent global events, can impact the availability and cost of critical hardware components. Competitive pressures from lower-cost, less resilient alternatives, although diminishing, still exist in some market segments.

- Implementation Complexity: Requires specialized IT skills and significant planning.

- High Initial Costs: Enterprise-grade HA hardware and software can represent a substantial upfront investment.

- Interoperability Challenges: Integrating solutions from multiple vendors can be complex.

- Network Dependencies: Reliance on stable network connectivity is crucial.

- Supply Chain Volatility: Global events can disrupt hardware availability and pricing.

Future Opportunities in High Availability Server Industry

The High Availability Server Industry is ripe with future opportunities. The expanding adoption of edge computing will create new demands for localized HA solutions. The integration of artificial intelligence (AI) and machine learning (ML) for predictive maintenance and automated self-healing capabilities presents a significant growth avenue. The increasing prevalence of the Internet of Things (IoT) will generate massive data streams that require resilient infrastructure for processing. Furthermore, emerging markets in developing economies are poised for rapid growth as they digitize their operations. The development of more energy-efficient and sustainable HA server technologies will also open new markets. The ongoing evolution of containerization and microservices will continue to drive the need for highly available orchestration layers.

- Edge Computing: Demand for localized HA solutions in distributed environments.

- AI/ML Integration: Predictive analytics and self-healing capabilities as key differentiators.

- IoT Data Processing: Robust infrastructure for handling massive data volumes.

- Emerging Markets: Significant growth potential in developing economies undergoing digitalization.

- Sustainable Technologies: Focus on energy-efficient and eco-friendly HA solutions.

Major Players in the High Availability Server Industry Ecosystem

- IBM Corp

- Hewlett Packard Enterprise Development LP

- Dell Inc

- Oracle Corp

- Amazon Web Services Inc

- Microsoft Corp

- Alibaba Cloud Computing Company

- Juniper Networks Inc

- Fujitsu Limited

- NEC Corp

- Unisys Corporation

- CenterServ International Ltd

Key Developments in High Availability Server Industry Industry

- 2023 Q4: Launch of AI-powered predictive failure analysis tools by major vendors, significantly reducing unplanned downtime.

- 2024 Q1: Increased M&A activity in the disaster recovery as a service (DRaaS) space, with deals valued in the multi-billion dollar range.

- 2024 Q2: Introduction of new software-defined HA solutions offering enhanced flexibility and lower TCO.

- 2024 Q3: Significant advancements in real-time data replication technologies, achieving sub-millisecond latency.

- 2024 Q4: Growing adoption of hybrid cloud HA strategies, combining on-premise resilience with cloud scalability.

- 2025 Q1: Major cloud providers announce enhanced SLA guarantees of 99.999% for their HA offerings.

Strategic High Availability Server Industry Market Forecast

The High Availability Server Industry is projected for robust and sustained growth, driven by an escalating global reliance on digital services and the imperative for uninterrupted business operations. The forecast period (2025–2033) will witness accelerated adoption of cloud-native HA solutions and the increasing integration of AI for proactive fault management. The demand for disaster recovery and business continuity planning will remain paramount, particularly in the wake of rising cybersecurity threats and unpredictable global events. Emerging markets present substantial untapped potential, and technological advancements in areas like edge computing and IoT will further diversify the market. Strategic investments in fault-tolerant architectures and resilient infrastructure will be crucial for businesses aiming to maintain competitive advantage and customer trust in the evolving digital landscape. The market is expected to continue its upward trajectory, with continuous innovation ensuring that high availability servers remain a cornerstone of modern enterprise IT.

High Availability Server Industry Segmentation

-

1. Deployment

- 1.1. Cloud-based

- 1.2. On-premise

-

2. Operating System

- 2.1. Windows

- 2.2. Linux

- 2.3. Other Operating System ( (UNIX, BSD)

-

3. End-user Industry

- 3.1. IT & Telecommunication

- 3.2. BFSI

- 3.3. Retail

- 3.4. Healthcare

- 3.5. Industrial

- 3.6. Other End-user Industries

High Availability Server Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Rest of the World

High Availability Server Industry Regional Market Share

Geographic Coverage of High Availability Server Industry

High Availability Server Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.71% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Deployment

- 5.1.1. Cloud-based

- 5.1.2. On-premise

- 5.2. Market Analysis, Insights and Forecast - by Operating System

- 5.2.1. Windows

- 5.2.2. Linux

- 5.2.3. Other Operating System ( (UNIX, BSD)

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. IT & Telecommunication

- 5.3.2. BFSI

- 5.3.3. Retail

- 5.3.4. Healthcare

- 5.3.5. Industrial

- 5.3.6. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Deployment

- 6. Global High Availability Server Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Deployment

- 6.1.1. Cloud-based

- 6.1.2. On-premise

- 6.2. Market Analysis, Insights and Forecast - by Operating System

- 6.2.1. Windows

- 6.2.2. Linux

- 6.2.3. Other Operating System ( (UNIX, BSD)

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. IT & Telecommunication

- 6.3.2. BFSI

- 6.3.3. Retail

- 6.3.4. Healthcare

- 6.3.5. Industrial

- 6.3.6. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Deployment

- 7. North America High Availability Server Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Deployment

- 7.1.1. Cloud-based

- 7.1.2. On-premise

- 7.2. Market Analysis, Insights and Forecast - by Operating System

- 7.2.1. Windows

- 7.2.2. Linux

- 7.2.3. Other Operating System ( (UNIX, BSD)

- 7.3. Market Analysis, Insights and Forecast - by End-user Industry

- 7.3.1. IT & Telecommunication

- 7.3.2. BFSI

- 7.3.3. Retail

- 7.3.4. Healthcare

- 7.3.5. Industrial

- 7.3.6. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Deployment

- 8. Europe High Availability Server Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Deployment

- 8.1.1. Cloud-based

- 8.1.2. On-premise

- 8.2. Market Analysis, Insights and Forecast - by Operating System

- 8.2.1. Windows

- 8.2.2. Linux

- 8.2.3. Other Operating System ( (UNIX, BSD)

- 8.3. Market Analysis, Insights and Forecast - by End-user Industry

- 8.3.1. IT & Telecommunication

- 8.3.2. BFSI

- 8.3.3. Retail

- 8.3.4. Healthcare

- 8.3.5. Industrial

- 8.3.6. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Deployment

- 9. Asia Pacific High Availability Server Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Deployment

- 9.1.1. Cloud-based

- 9.1.2. On-premise

- 9.2. Market Analysis, Insights and Forecast - by Operating System

- 9.2.1. Windows

- 9.2.2. Linux

- 9.2.3. Other Operating System ( (UNIX, BSD)

- 9.3. Market Analysis, Insights and Forecast - by End-user Industry

- 9.3.1. IT & Telecommunication

- 9.3.2. BFSI

- 9.3.3. Retail

- 9.3.4. Healthcare

- 9.3.5. Industrial

- 9.3.6. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Deployment

- 10. Rest of the World High Availability Server Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Deployment

- 10.1.1. Cloud-based

- 10.1.2. On-premise

- 10.2. Market Analysis, Insights and Forecast - by Operating System

- 10.2.1. Windows

- 10.2.2. Linux

- 10.2.3. Other Operating System ( (UNIX, BSD)

- 10.3. Market Analysis, Insights and Forecast - by End-user Industry

- 10.3.1. IT & Telecommunication

- 10.3.2. BFSI

- 10.3.3. Retail

- 10.3.4. Healthcare

- 10.3.5. Industrial

- 10.3.6. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Deployment

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Unisys Corporation

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 CenterServ International Ltd

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Alibaba Cloud Computing Company

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 NEC Corp

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Hewlett Packard Enterprise Development LP

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 IBM Corp

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Fujitsu Limited

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Juniper Networks Inc

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Amazon Web Services Inc

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Dell Inc

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 Cisco System Inc

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.12 Oracle Corp

- 11.1.12.1. Company Overview

- 11.1.12.2. Products

- 11.1.12.3. Company Financials

- 11.1.12.4. SWOT Analysis

- 11.1.1 Unisys Corporation

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global High Availability Server Industry Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America High Availability Server Industry Revenue (undefined), by Deployment 2025 & 2033

- Figure 3: North America High Availability Server Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 4: North America High Availability Server Industry Revenue (undefined), by Operating System 2025 & 2033

- Figure 5: North America High Availability Server Industry Revenue Share (%), by Operating System 2025 & 2033

- Figure 6: North America High Availability Server Industry Revenue (undefined), by End-user Industry 2025 & 2033

- Figure 7: North America High Availability Server Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 8: North America High Availability Server Industry Revenue (undefined), by Country 2025 & 2033

- Figure 9: North America High Availability Server Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe High Availability Server Industry Revenue (undefined), by Deployment 2025 & 2033

- Figure 11: Europe High Availability Server Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 12: Europe High Availability Server Industry Revenue (undefined), by Operating System 2025 & 2033

- Figure 13: Europe High Availability Server Industry Revenue Share (%), by Operating System 2025 & 2033

- Figure 14: Europe High Availability Server Industry Revenue (undefined), by End-user Industry 2025 & 2033

- Figure 15: Europe High Availability Server Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 16: Europe High Availability Server Industry Revenue (undefined), by Country 2025 & 2033

- Figure 17: Europe High Availability Server Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific High Availability Server Industry Revenue (undefined), by Deployment 2025 & 2033

- Figure 19: Asia Pacific High Availability Server Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 20: Asia Pacific High Availability Server Industry Revenue (undefined), by Operating System 2025 & 2033

- Figure 21: Asia Pacific High Availability Server Industry Revenue Share (%), by Operating System 2025 & 2033

- Figure 22: Asia Pacific High Availability Server Industry Revenue (undefined), by End-user Industry 2025 & 2033

- Figure 23: Asia Pacific High Availability Server Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 24: Asia Pacific High Availability Server Industry Revenue (undefined), by Country 2025 & 2033

- Figure 25: Asia Pacific High Availability Server Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Rest of the World High Availability Server Industry Revenue (undefined), by Deployment 2025 & 2033

- Figure 27: Rest of the World High Availability Server Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 28: Rest of the World High Availability Server Industry Revenue (undefined), by Operating System 2025 & 2033

- Figure 29: Rest of the World High Availability Server Industry Revenue Share (%), by Operating System 2025 & 2033

- Figure 30: Rest of the World High Availability Server Industry Revenue (undefined), by End-user Industry 2025 & 2033

- Figure 31: Rest of the World High Availability Server Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 32: Rest of the World High Availability Server Industry Revenue (undefined), by Country 2025 & 2033

- Figure 33: Rest of the World High Availability Server Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global High Availability Server Industry Revenue undefined Forecast, by Deployment 2020 & 2033

- Table 2: Global High Availability Server Industry Revenue undefined Forecast, by Operating System 2020 & 2033

- Table 3: Global High Availability Server Industry Revenue undefined Forecast, by End-user Industry 2020 & 2033

- Table 4: Global High Availability Server Industry Revenue undefined Forecast, by Region 2020 & 2033

- Table 5: Global High Availability Server Industry Revenue undefined Forecast, by Deployment 2020 & 2033

- Table 6: Global High Availability Server Industry Revenue undefined Forecast, by Operating System 2020 & 2033

- Table 7: Global High Availability Server Industry Revenue undefined Forecast, by End-user Industry 2020 & 2033

- Table 8: Global High Availability Server Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 9: Global High Availability Server Industry Revenue undefined Forecast, by Deployment 2020 & 2033

- Table 10: Global High Availability Server Industry Revenue undefined Forecast, by Operating System 2020 & 2033

- Table 11: Global High Availability Server Industry Revenue undefined Forecast, by End-user Industry 2020 & 2033

- Table 12: Global High Availability Server Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Global High Availability Server Industry Revenue undefined Forecast, by Deployment 2020 & 2033

- Table 14: Global High Availability Server Industry Revenue undefined Forecast, by Operating System 2020 & 2033

- Table 15: Global High Availability Server Industry Revenue undefined Forecast, by End-user Industry 2020 & 2033

- Table 16: Global High Availability Server Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 17: Global High Availability Server Industry Revenue undefined Forecast, by Deployment 2020 & 2033

- Table 18: Global High Availability Server Industry Revenue undefined Forecast, by Operating System 2020 & 2033

- Table 19: Global High Availability Server Industry Revenue undefined Forecast, by End-user Industry 2020 & 2033

- Table 20: Global High Availability Server Industry Revenue undefined Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the High Availability Server Industry?

The projected CAGR is approximately 7.71%.

2. Which companies are prominent players in the High Availability Server Industry?

Key companies in the market include Unisys Corporation, CenterServ International Ltd, Alibaba Cloud Computing Company, NEC Corp, Hewlett Packard Enterprise Development LP, IBM Corp, Fujitsu Limited, Juniper Networks Inc, Amazon Web Services Inc, Dell Inc, Cisco System Inc, Oracle Corp.

3. What are the main segments of the High Availability Server Industry?

The market segments include Deployment, Operating System, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

; High Adoption Rate of High Availability Server Across BFSI Sector; Growing Demand for Modular & Micro Data Center with the Increasing Application of IoT Devices.

6. What are the notable trends driving market growth?

BFSI Sector is Expected to Have a Significant Growth Rate.

7. Are there any restraints impacting market growth?

; Lack of Awareness Among Professionals; High Cost for Initial Installation/Deployment.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "High Availability Server Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the High Availability Server Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the High Availability Server Industry?

To stay informed about further developments, trends, and reports in the High Availability Server Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence