Key Insights into the Africa SVOD Market

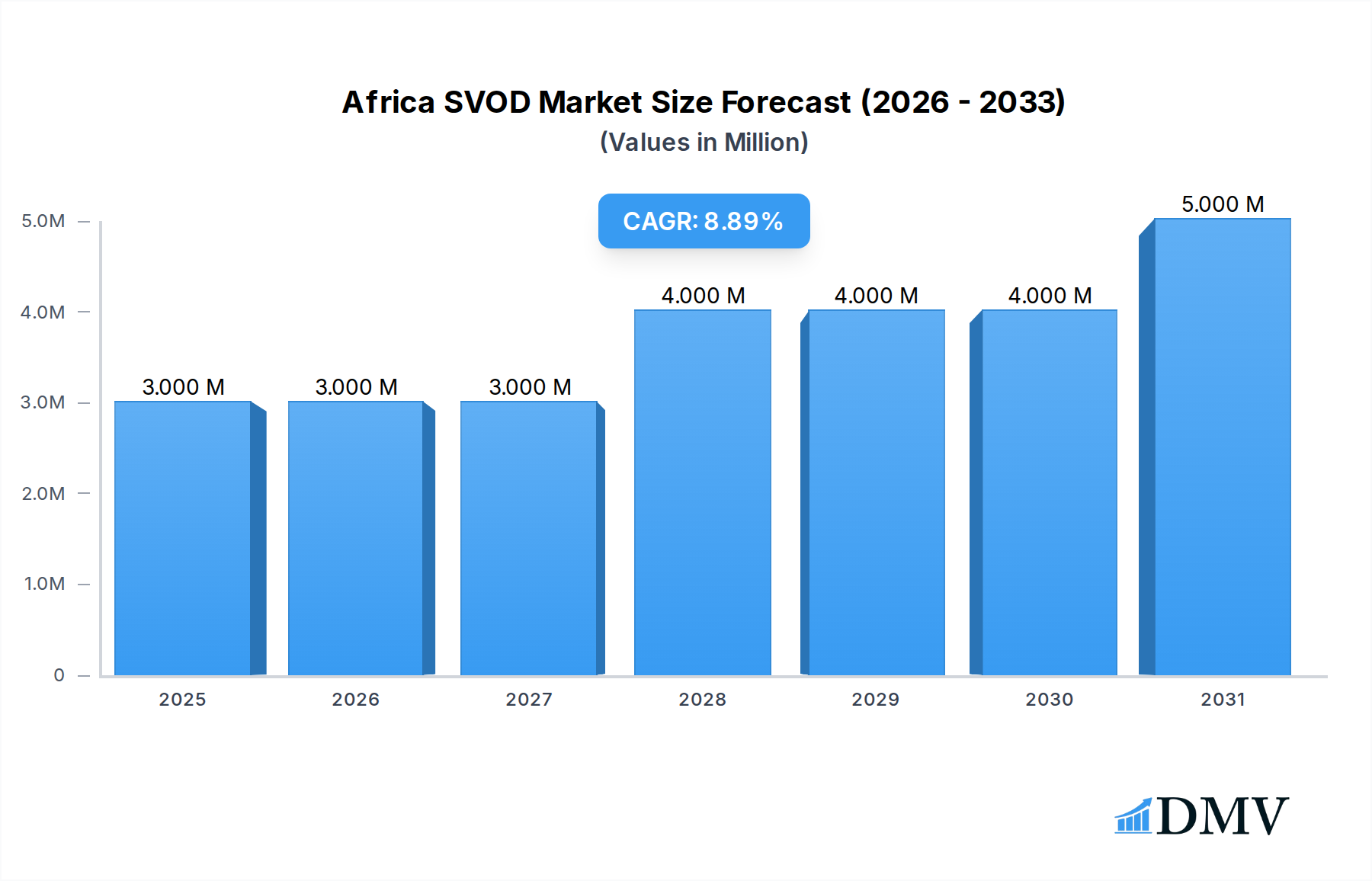

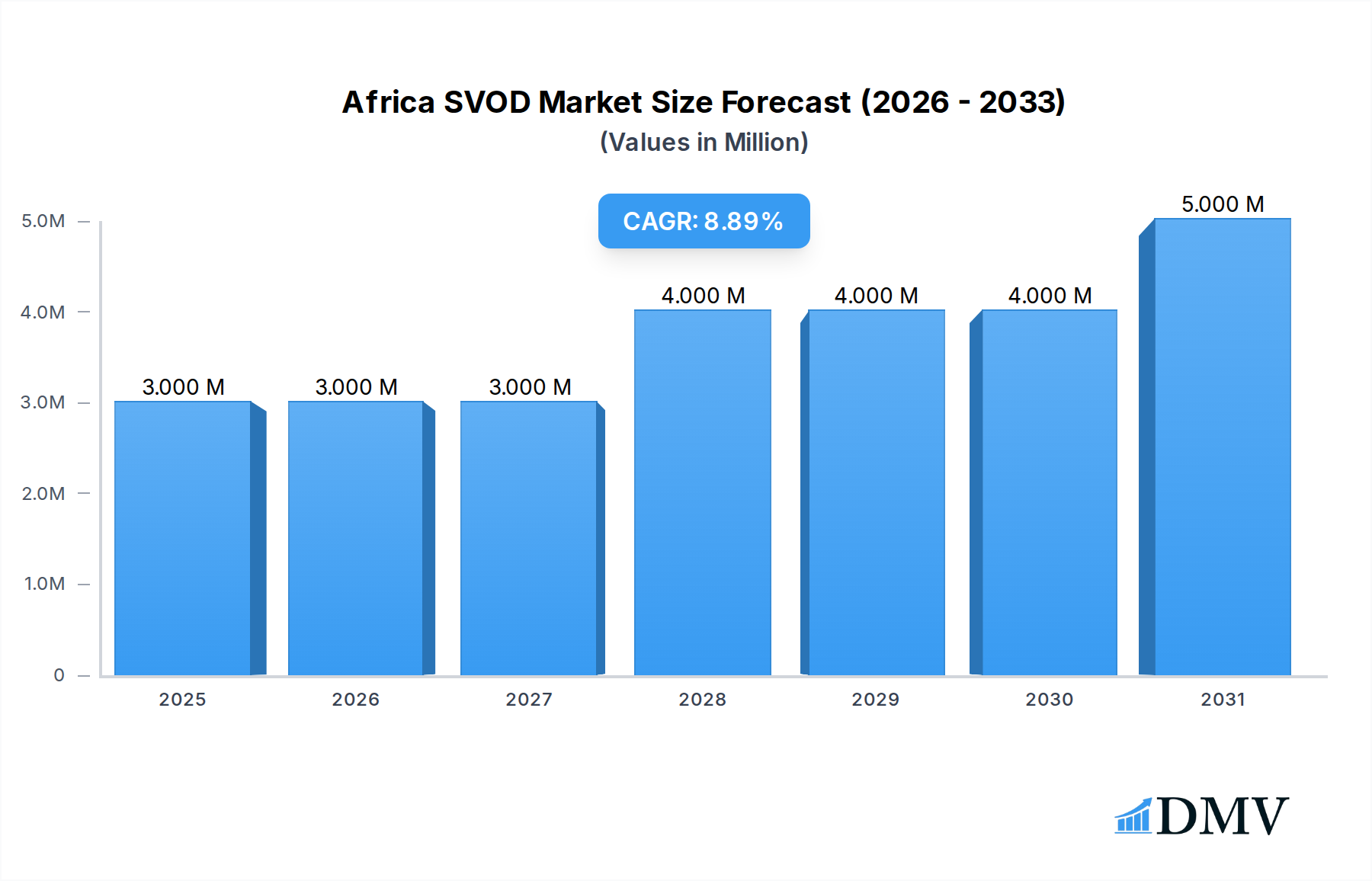

The Africa SVOD Market is poised for significant expansion, driven by a confluence of factors including escalating internet penetration, increasing smartphone adoption, and a growing middle class with disposable income for digital entertainment. Currently valued at $2.10 Million, the market is projected to grow at a robust Compound Annual Growth Rate (CAGR) of 11.29% from 2024 to 2034. This aggressive growth trajectory is underpinned by an intensification of competition, as numerous global players strategically enter the African landscape to capture a nascent, yet rapidly expanding, audience base.

Africa SVOD Market Market Size (In Million)

The strategic thrust by market participants involves enticing marketing strategies, such as offering free mobile plans integrated with SVOD subscriptions and forging regional partnerships to enhance content accessibility and payment flexibility. These initiatives are crucial in overcoming the primary restraint of higher pricing plans, which can act as a significant barrier for adoption in price-sensitive segments. The evolving Broadband Connectivity Market across the continent is a critical enabler, providing the necessary infrastructure for seamless streaming experiences. Furthermore, the Digital Content Market is witnessing a surge in investment, particularly in localized and culturally relevant content, which resonates strongly with African consumers.

Africa SVOD Market Company Market Share

The trend towards drama as a dominant genre is expected to drive substantial growth within the Africa SVOD Market, reflecting consumer preferences for engaging narrative forms. This focus on genre-specific content, coupled with the rising prominence of the Mobile Entertainment Market, positions smartphones as the primary device for content consumption. The continent's youthful demographic and rapid urbanization further contribute to a fertile ground for the expansion of Streaming Services Market. As part of the broader Digital Transformation Market, the Africa SVOD Market is not only a consumer phenomenon but also a significant contributor to the region's digital economy, stimulating local Content Production Market and fostering technological innovation.

Subscription Video on Demand Dominance in Africa SVOD Market

The Subscription Video on Demand (SVOD) revenue model unequivocally dominates the Africa SVOD Market, representing the core mechanism through which consumers access a vast array of digital entertainment. This dominance is not merely coincidental but a strategic outcome of evolving consumer preferences for on-demand access, coupled with the robust market entry strategies of global and regional players. The inherent value proposition of SVOD — unlimited access to a content library for a fixed monthly fee — resonates well with consumers seeking convenience and cost-effectiveness over individual content purchases or ad-supported models. While Transactional Video on Demand (TVOD) offers flexibility for specific premium content, the recurring revenue and broader appeal of SVOD libraries solidify its leading position.

Several factors contribute to SVOD's sustained dominance. Firstly, the expansion of the Broadband Connectivity Market has made reliable internet access more widespread, enabling consistent streaming. Secondly, the proliferation of affordable smartphones and smart TVs has lowered the barrier to entry for digital content consumption, directly fueling the Mobile Entertainment Market. Major players like Netflix Inc., Walt Disney Company (Disney+), and Amazon.com Inc. have aggressively expanded their SVOD offerings, often localizing content and payment options to better suit African market dynamics. Local and regional providers, such as MultiChoice Group Ltd. (Showmax), StarTimes Group (StarTimes ON), and iROKO Partners Ltd. (iROKOtv), have also carved out significant niches by focusing on hyper-local content, which remains a key differentiator.

The competitive landscape within the Africa SVOD Market is characterized by intense battles for subscriber acquisition and retention. Providers are continually enhancing their content libraries, investing heavily in exclusive African originals and popular international titles. The appeal of the Digital Content Market is broadening, and SVOD platforms are at the forefront of this expansion. Furthermore, bundling strategies, often in partnership with telecommunication companies, integrate SVOD subscriptions with data plans, making them more accessible and attractive to a wider consumer base. The long-term growth of the Subscription Services Market across various digital verticals reinforces the viability and continued expansion of SVOD, as consumers become more accustomed to and reliant on subscription-based models for their entertainment needs. This segment's continued innovation in content delivery, personalization, and monetization will be critical in maintaining its leading market share over the coming decade.

Key Market Drivers or Constraints in the Africa SVOD Market

The Africa SVOD Market's trajectory is primarily shaped by a dynamic interplay of potent drivers and significant restraints, each exerting a quantifiable impact on market growth and consumer adoption.

Intensification of Competition as Several Global Players Enter the Market to Capture the Nascent Audience: This driver is a powerful catalyst for market expansion. The entry of major global players like Netflix Inc., Walt Disney Company (Disney+), and Amazon.com Inc. has not only brought substantial investment and a vast content library but also spurred innovation in service delivery. For instance, Netflix's August 2022 announcement of a lineup of new and returning African originals, alongside multi-project collaborations with filmmakers like Mandlakayise Walter Dube, demonstrates the direct impact of this competitive drive on enriching the Digital Content Market. This influx of competition leads to a greater variety of content, improved service quality, and often more aggressive pricing strategies, ultimately benefiting the consumer and expanding the overall Streaming Services Market.

Enticing Marketing Strategies like Free Mobile Plans, Regional Partnerships, etc., are Anticipated to Aid the Long-Term Growth of Market: This driver directly addresses accessibility and affordability, which are crucial in the African context. Telecommunication companies, for example, frequently bundle SVOD subscriptions with mobile data packages, making streaming more accessible to the vast Mobile Entertainment Market. MTN Group Ltd. with Ayoba, and Telkom SA SOC Ltd. with TelkomONE, exemplify regional partnerships designed to lower barriers to entry. Amazon Prime Video's February 2023 multi-picture licensing arrangement with South Africa's Known Associates, making over 20 South African feature films available exclusively, highlights the importance of regional content acquisition as a marketing strategy. Such partnerships expand reach, leverage existing customer bases, and alleviate data cost concerns, thereby significantly aiding the long-term growth of the Africa SVOD Market.

Higher Pricing Plans Act as a Barrier for Adoption: This is the primary restraint curbing broader market penetration. While competition can drive prices down, many SVOD services still present a significant financial outlay for a large portion of the African population, especially when combined with data costs. Even with mobile-first plans, the cumulative cost can be prohibitive, particularly for segments not fully integrated into the formal economy. This restraint necessitates continuous innovation in pricing models and localized payment solutions to improve affordability and encourage wider adoption, allowing more consumers to enter the Subscription Services Market.

Competitive Ecosystem of Africa SVOD Market

The Africa SVOD Market is characterized by a diverse competitive landscape, encompassing global giants, regional powerhouses, and local niche players. Each entity employs unique strategies to capture market share and respond to the specific demands of African consumers, which are largely influenced by the evolving Broadband Connectivity Market and the growing Mobile Entertainment Market.

- Netflix Inc.: A global leader, Netflix has invested heavily in original African content and established multi-project collaborations with local creators, aiming to deepen its appeal to a continent with a rapidly expanding digital audience. Its broad content library and user experience are key differentiators.

- Walt Disney Company (Disney+): Entering the market with its powerful brand and extensive catalog of family-friendly content, Marvel, and Star Wars franchises, Disney+ seeks to attract a significant portion of the African audience, often leveraging existing partnerships or direct-to-consumer models.

- Amazon.com Inc. : Through Amazon Prime Video, the company is strategically acquiring local content and forming licensing agreements, such as its February 2023 deal with South Africa's Known Associates, to enhance its regional content offering and compete effectively in the Digital Content Market.

- MultiChoice Group Ltd. : Operating Showmax, MultiChoice is a dominant regional player, renowned for its strong local content, sports rights, and strategic partnerships with telecommunication providers, giving it a significant footprint in key African markets.

- StarTimes Group (StarTimes ON): This company offers a hybrid model, combining traditional pay-TV with its digital streaming platform, StarTimes ON. It focuses on affordable packages and diverse content, including sports and local productions, appealing to a broad demographic.

- Canal+ Group (MyCanal): A major European player with strong ties to Francophone Africa, Canal+ is expanding its digital offerings through MyCanal, leveraging its extensive content rights and local distribution networks to target specific regional markets.

- iROKO Partners Ltd. (iROKOtv): Often dubbed the "Netflix of Africa," iROKOtv specializes in Nigerian content (Nollywood), demonstrating the power of niche content strategies in attracting and retaining a dedicated subscriber base within the Africa SVOD Market.

- Apple Inc. (Apple TV+): Leveraging its ecosystem of devices, Apple TV+ offers a curated selection of high-quality original programming, aiming for premium subscribers who are integrated into the Apple ecosystem.

- Google LLC (YouTube Premium): While YouTube is primarily an AVOD platform, YouTube Premium offers ad-free viewing, background play, and exclusive content, catering to users willing to pay for an enhanced experience.

- Orange S.A. (Orange VOD): As a major telecommunications operator, Orange integrates VOD services, often bundling them with mobile and internet packages, capitalizing on its extensive subscriber base in various African countries.

- Huawei Technologies Co. Ltd. (Huawei Video): Huawei leverages its strong device presence to offer a content platform, providing an ecosystem play for its smartphone users and contributing to the growing Digital Transformation Market.

- PCCW Media Group (Viu): Focusing on Asian content, particularly K-drama, Viu targets a specific, highly engaged demographic within Africa, showcasing the potential for diverse content preferences.

- MTN Group Ltd. (Ayoba): As a telecommunications giant, MTN offers Ayoba, a super-app that includes messaging, music, games, and basic SVOD content, aiming to leverage its vast mobile subscriber base.

- Telkom SA SOC Ltd. (TelkomONE): A South African telecommunications company, TelkomONE provides a platform for music, video, and gaming, integrating digital entertainment into its service offerings.

Recent Developments & Milestones in Africa SVOD Market

Recent developments in the Africa SVOD Market highlight the aggressive strategies employed by both global and regional players to expand their footprint and enhance content offerings, particularly within the burgeoning Digital Content Market and Mobile Entertainment Market.

- February 2023: Amazon Prime Video announced a multi-picture licensing arrangement with South Africa's Known Associates, the parent company of Johannesburg-based Known Associates Entertainment (KAE) and Cape Town-based Moonlighting Films, during the Joburg Film Festival. This agreement makes over 20 South African feature films, including Zane Meas' "Klip Anker Baai," Marvin-Lee Beukes' "Tickets," Jahmil Qubeka's "You Are My Favourite Place," and Norman Maake's "Piet's Sake 2," available exclusively on Prime Video. This strategic move emphasizes the importance of localized content acquisition in deepening market penetration and addressing regional consumer preferences.

- August 2022: Netflix announced a robust lineup of new and returning African originals slated for late 2022 and early 2023. This extensive roster includes a mix of scripted and unscripted programs, alongside feature films, signaling Netflix's continued commitment to investing in the Content Production Market in Africa. Furthermore, Netflix solidified a multi-project collaboration with acclaimed South African filmmaker Mandlakayise Walter Dube, who previously directed Netflix's first commissioned African film, Silverton Siege. This initiative follows earlier multi-title deals with prominent African creators such as Mo Abudu and her Ebonylife Studios, and Kunle Afolayan and his Nigerian production company KAP, reinforcing Netflix's strategy to bolster local talent and content.

These milestones underscore a clear trend of international SVOD providers actively seeking to localize their content libraries and establish deeper ties with African creative industries, thereby enhancing their competitive edge within the Africa SVOD Market and responding to the unique demands of its rapidly growing subscriber base.

Regional Market Breakdown for Africa SVOD Market

The Africa SVOD Market exhibits varied growth dynamics across its key regional strongholds, each driven by distinct factors related to infrastructure, consumer behavior, and local content ecosystems. While specific CAGR and revenue share data for individual countries are not provided, an analysis of the primary markets—South Africa, Nigeria, and Kenya—along with the broader 'Rest of Africa,' reveals distinct characteristics and growth potential.

South Africa: As one of the most developed economies in Africa, South Africa represents a mature segment within the Africa SVOD Market. It boasts relatively higher internet penetration and a significant middle-class population, making it a lucrative market for global and local SVOD players. The primary demand driver here is the availability of diverse international and high-quality local content, coupled with more established Broadband Connectivity Market infrastructure. Companies like MultiChoice (Showmax) and Netflix have a strong presence, fiercely competing for a subscriber base that is more accustomed to digital payment systems and subscription models. The relatively higher household incomes support premium pricing plans, though competition is intensifying.

Nigeria: Nigeria stands out as potentially the fastest-growing region in terms of sheer subscriber volume, driven by its massive, youthful population and rapidly expanding smartphone adoption. The primary demand driver is the immense popularity of Nigerian content (Nollywood) and the burgeoning Mobile Entertainment Market. While infrastructure can be challenging, the sheer market size attracts significant investment from players like Netflix, which has actively partnered with Nigerian filmmakers. Price sensitivity is high, leading to a focus on mobile-only plans and localized content offerings. The rapid expansion of mobile money services also facilitates the Subscription Services Market here.

Kenya: Kenya is a significant East African hub for the Africa SVOD Market, characterized by its innovative mobile money ecosystem and growing digital literacy. The primary demand driver is the convenience offered by mobile-first SVOD solutions and the increasing availability of affordable internet data. Kenyan consumers are increasingly accessing SVOD services via smartphones, contributing to the expansion of the Digital Content Market. Regional players and global platforms are adapting their strategies to integrate with popular mobile payment methods like M-Pesa to overcome transaction barriers.

Rest of Africa: This encompasses a vast and diverse range of countries, from emerging markets to those with nascent digital infrastructure. While less consolidated than the major three, this segment offers long-term potential. The primary demand drivers here include increasing urbanization, improving Broadband Connectivity Market through initiatives like subsea cables, and rising smartphone penetration in smaller economies. Growth in this segment is often slower but steady, relying on basic, affordable content and mobile-centric delivery models. As internet infrastructure improves and digital literacy rises, these regions will increasingly contribute to the overall expansion of the Africa SVOD Market, fueled by the broader Digital Transformation Market.

Africa SVOD Market Regional Market Share

Regulatory & Policy Landscape Shaping Africa SVOD Market

The regulatory and policy landscape significantly influences the operational framework and growth trajectory of the Africa SVOD Market. Governments across the continent are grappling with how to effectively govern digital streaming services, balancing economic growth, cultural preservation, and consumer protection. Key areas of focus include local content quotas, data privacy, taxation, and licensing.

Many African nations are implementing or considering local content quotas for SVOD platforms. The intent is to promote indigenous languages, cultures, and talent, thereby stimulating the local Content Production Market. For example, countries like South Africa and Nigeria have discussed or proposed regulations that would mandate a certain percentage of content to be locally produced or co-produced. This directly impacts content acquisition strategies for global players and provides opportunities for local studios. Compliance with these quotas can be complex, requiring significant investment in regional creative ecosystems.

Data privacy and protection regulations are also gaining prominence. With the rise of digital services, consumer data collection and usage are under scrutiny. The African Union's Convention on Cybersecurity and Personal Data Protection (Malabo Convention) provides a continental framework, though individual countries like South Africa (POPIA) and Nigeria (NDPR) have their own robust data protection laws. SVOD providers must ensure their data handling practices comply with these varied and evolving regulations, which is crucial for maintaining consumer trust and avoiding penalties within the Digital Transformation Market.

Taxation of digital services, including SVOD, is another critical policy area. Several African countries have introduced or are considering Value Added Tax (VAT) or Digital Service Taxes (DST) on non-resident companies providing digital services to their citizens. This aims to level the playing field for local businesses and generate revenue for governments. These taxes can impact the pricing strategies of SVOD platforms, potentially increasing costs for consumers and influencing market penetration in the Subscription Services Market.

Licensing and censorship also play a role. While often less stringent than for traditional broadcasters, SVOD platforms are expected to adhere to content standards and avoid material deemed offensive or harmful by national authorities. Some countries may require licenses for digital service providers. The nascent and fragmented nature of these regulations means SVOD operators must navigate a complex patchwork of rules, which can pose challenges for pan-African expansion but also presents an opportunity for harmonization as the Streaming Services Market matures.

Export, Trade Flow & Tariff Impact on Africa SVOD Market

The Africa SVOD Market, by its very nature as a digital service, operates within a unique framework concerning export, trade flow, and tariff impacts, distinct from physical goods. Digital content primarily involves the cross-border flow of intellectual property and data rather than tangible products, yet it is still influenced by trade policies, digital service taxes, and data localization trends.

Digital Content Flow: The primary "trade" in the Africa SVOD Market is the cross-border licensing and distribution of Digital Content Market. Global SVOD providers, such as Netflix, Amazon Prime Video, and Disney+, license international content for regional distribution and also export African-produced content to global audiences. This creates a significant "export" of cultural products from Africa, as evidenced by Netflix's investments in Nigerian and South African productions, which are then streamed worldwide. Conversely, the vast majority of content consumed on African SVOD platforms originates from outside the continent, representing a substantial "import" of digital content.

Data Localization and Cross-Border Data Flows: While not a tariff in the traditional sense, emerging data localization policies in some African nations could impact the efficiency and cost of SVOD operations. Requirements to host servers within national borders can increase infrastructure costs for global platforms, potentially affecting service delivery and pricing. Conversely, the free flow of data is essential for the efficient operation of Cloud Computing Market services, which underpin most SVOD platforms. Restrictions on data flow could create non-tariff barriers, complicating seamless regional integration of SVOD services.

Digital Services Taxes (DSTs): Several African countries, including Kenya and Nigeria, have either implemented or are exploring Digital Service Taxes. These taxes are typically levied on the revenue generated by non-resident digital service providers from users within their jurisdiction. While not a customs tariff, a DST directly impacts the profitability and pricing strategies of SVOD providers. These taxes can lead to increased subscription costs for consumers or reduced investment in the local Content Production Market, effectively acting as a trade barrier for digital services if not carefully balanced. The drive for such taxes often stems from a desire to ensure fair taxation of the digital economy and prevent profit shifting by multinational corporations.

Payment Gateway Integration and Foreign Exchange: Cross-border payments are crucial for the Subscription Services Market in Africa. The availability and efficiency of international payment gateways, coupled with foreign exchange rate fluctuations, can impact revenue repatriation for global SVOD players and the affordability of subscriptions for local consumers. Tariffs on financial transactions or capital controls, if present, could indirectly affect the operational viability of these services.

Overall, while traditional tariffs on physical goods are not directly applicable, policies concerning content regulation, data governance, and digital taxation act as de facto trade barriers or facilitators, profoundly shaping the competitive dynamics and growth potential of the Africa SVOD Market. The ongoing evolution of these policies will dictate the ease with which digital content and services can flow across borders within the continent and globally, impacting the overall Digital Transformation Market.

Africa SVOD Market Segmentation

-

1. Content Genre

- 1.1. Drama

- 1.2. Music

- 1.3. Sports

- 1.4. Others

-

2. Revenue Model

- 2.1. Subscription Video on Demand

- 2.2. Transactional Video on Demand

-

3. Device Type

- 3.1. Smartphone

- 3.2. Smart TV

- 3.3. Tablet

- 3.4. PC or Laptop

- 3.5. Others

-

4. User Base

- 4.1. Individual Users

- 4.2. Family Accounts

- 4.3. Corporate Accounts

Africa SVOD Market Segmentation By Geography

- 1. Kenya

- 2. South Africa

- 3. Nigeria

Africa SVOD Market Regional Market Share

Geographic Coverage of Africa SVOD Market

Africa SVOD Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.29% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Content Genre

- 5.1.1. Drama

- 5.1.2. Music

- 5.1.3. Sports

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Revenue Model

- 5.2.1. Subscription Video on Demand

- 5.2.2. Transactional Video on Demand

- 5.3. Market Analysis, Insights and Forecast - by Device Type

- 5.3.1. Smartphone

- 5.3.2. Smart TV

- 5.3.3. Tablet

- 5.3.4. PC or Laptop

- 5.3.5. Others

- 5.4. Market Analysis, Insights and Forecast - by User Base

- 5.4.1. Individual Users

- 5.4.2. Family Accounts

- 5.4.3. Corporate Accounts

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. Kenya

- 5.5.2. South Africa

- 5.5.3. Nigeria

- 5.1. Market Analysis, Insights and Forecast - by Content Genre

- 6. Africa SVOD Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Content Genre

- 6.1.1. Drama

- 6.1.2. Music

- 6.1.3. Sports

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Revenue Model

- 6.2.1. Subscription Video on Demand

- 6.2.2. Transactional Video on Demand

- 6.3. Market Analysis, Insights and Forecast - by Device Type

- 6.3.1. Smartphone

- 6.3.2. Smart TV

- 6.3.3. Tablet

- 6.3.4. PC or Laptop

- 6.3.5. Others

- 6.4. Market Analysis, Insights and Forecast - by User Base

- 6.4.1. Individual Users

- 6.4.2. Family Accounts

- 6.4.3. Corporate Accounts

- 6.1. Market Analysis, Insights and Forecast - by Content Genre

- 7. Kenya Africa SVOD Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Content Genre

- 7.1.1. Drama

- 7.1.2. Music

- 7.1.3. Sports

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Revenue Model

- 7.2.1. Subscription Video on Demand

- 7.2.2. Transactional Video on Demand

- 7.3. Market Analysis, Insights and Forecast - by Device Type

- 7.3.1. Smartphone

- 7.3.2. Smart TV

- 7.3.3. Tablet

- 7.3.4. PC or Laptop

- 7.3.5. Others

- 7.4. Market Analysis, Insights and Forecast - by User Base

- 7.4.1. Individual Users

- 7.4.2. Family Accounts

- 7.4.3. Corporate Accounts

- 7.1. Market Analysis, Insights and Forecast - by Content Genre

- 8. South Africa Africa SVOD Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Content Genre

- 8.1.1. Drama

- 8.1.2. Music

- 8.1.3. Sports

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Revenue Model

- 8.2.1. Subscription Video on Demand

- 8.2.2. Transactional Video on Demand

- 8.3. Market Analysis, Insights and Forecast - by Device Type

- 8.3.1. Smartphone

- 8.3.2. Smart TV

- 8.3.3. Tablet

- 8.3.4. PC or Laptop

- 8.3.5. Others

- 8.4. Market Analysis, Insights and Forecast - by User Base

- 8.4.1. Individual Users

- 8.4.2. Family Accounts

- 8.4.3. Corporate Accounts

- 8.1. Market Analysis, Insights and Forecast - by Content Genre

- 9. Nigeria Africa SVOD Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Content Genre

- 9.1.1. Drama

- 9.1.2. Music

- 9.1.3. Sports

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Revenue Model

- 9.2.1. Subscription Video on Demand

- 9.2.2. Transactional Video on Demand

- 9.3. Market Analysis, Insights and Forecast - by Device Type

- 9.3.1. Smartphone

- 9.3.2. Smart TV

- 9.3.3. Tablet

- 9.3.4. PC or Laptop

- 9.3.5. Others

- 9.4. Market Analysis, Insights and Forecast - by User Base

- 9.4.1. Individual Users

- 9.4.2. Family Accounts

- 9.4.3. Corporate Accounts

- 9.1. Market Analysis, Insights and Forecast - by Content Genre

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 StarTimes Media

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Apple Inc. (Apple TV+)

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 PCCW Media Group (Viu)

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 Orange S.A. (Orange VOD)

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 Huawei Technologies Co. Ltd. (Huawei Video)

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 Walt Disney Company (Disney+)

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 Netflix Inc.

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 StarTimes Group (StarTimes ON)

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.9 Amazon.com Inc.

- 10.1.9.1. Company Overview

- 10.1.9.2. Products

- 10.1.9.3. Company Financials

- 10.1.9.4. SWOT Analysis

- 10.1.10 MTN Group Ltd. (Ayoba)

- 10.1.10.1. Company Overview

- 10.1.10.2. Products

- 10.1.10.3. Company Financials

- 10.1.10.4. SWOT Analysis

- 10.1.11 Google LLC (YouTube Premium)

- 10.1.11.1. Company Overview

- 10.1.11.2. Products

- 10.1.11.3. Company Financials

- 10.1.11.4. SWOT Analysis

- 10.1.12 Canal+ Group (MyCanal)

- 10.1.12.1. Company Overview

- 10.1.12.2. Products

- 10.1.12.3. Company Financials

- 10.1.12.4. SWOT Analysis

- 10.1.13 iROKO Partners Ltd. (iROKOtv)

- 10.1.13.1. Company Overview

- 10.1.13.2. Products

- 10.1.13.3. Company Financials

- 10.1.13.4. SWOT Analysis

- 10.1.14 Telkom SA SOC Ltd. (TelkomONE)

- 10.1.14.1. Company Overview

- 10.1.14.2. Products

- 10.1.14.3. Company Financials

- 10.1.14.4. SWOT Analysis

- 10.1.15 MultiChoice Group Ltd.

- 10.1.15.1. Company Overview

- 10.1.15.2. Products

- 10.1.15.3. Company Financials

- 10.1.15.4. SWOT Analysis

- 10.1.16 Others

- 10.1.16.1. Company Overview

- 10.1.16.2. Products

- 10.1.16.3. Company Financials

- 10.1.16.4. SWOT Analysis

- 10.1.1 StarTimes Media

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: Africa SVOD Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Africa SVOD Market Share (%) by Company 2025

List of Tables

- Table 1: Africa SVOD Market Revenue Million Forecast, by Content Genre 2020 & 2033

- Table 2: Africa SVOD Market Revenue Million Forecast, by Revenue Model 2020 & 2033

- Table 3: Africa SVOD Market Revenue Million Forecast, by Device Type 2020 & 2033

- Table 4: Africa SVOD Market Revenue Million Forecast, by User Base 2020 & 2033

- Table 5: Africa SVOD Market Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Africa SVOD Market Revenue Million Forecast, by Content Genre 2020 & 2033

- Table 7: Africa SVOD Market Revenue Million Forecast, by Revenue Model 2020 & 2033

- Table 8: Africa SVOD Market Revenue Million Forecast, by Device Type 2020 & 2033

- Table 9: Africa SVOD Market Revenue Million Forecast, by User Base 2020 & 2033

- Table 10: Africa SVOD Market Revenue Million Forecast, by Country 2020 & 2033

- Table 11: Africa SVOD Market Revenue Million Forecast, by Content Genre 2020 & 2033

- Table 12: Africa SVOD Market Revenue Million Forecast, by Revenue Model 2020 & 2033

- Table 13: Africa SVOD Market Revenue Million Forecast, by Device Type 2020 & 2033

- Table 14: Africa SVOD Market Revenue Million Forecast, by User Base 2020 & 2033

- Table 15: Africa SVOD Market Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Africa SVOD Market Revenue Million Forecast, by Content Genre 2020 & 2033

- Table 17: Africa SVOD Market Revenue Million Forecast, by Revenue Model 2020 & 2033

- Table 18: Africa SVOD Market Revenue Million Forecast, by Device Type 2020 & 2033

- Table 19: Africa SVOD Market Revenue Million Forecast, by User Base 2020 & 2033

- Table 20: Africa SVOD Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Africa SVOD Market?

The projected CAGR is approximately 11.29%.

2. Which companies are prominent players in the Africa SVOD Market?

Key companies in the market include StarTimes Media, Apple Inc. (Apple TV+), PCCW Media Group (Viu), Orange S.A. (Orange VOD), Huawei Technologies Co. Ltd. (Huawei Video), Walt Disney Company (Disney+), Netflix Inc., StarTimes Group (StarTimes ON), Amazon.com Inc., MTN Group Ltd. (Ayoba), Google LLC (YouTube Premium), Canal+ Group (MyCanal), iROKO Partners Ltd. (iROKOtv), Telkom SA SOC Ltd. (TelkomONE), MultiChoice Group Ltd., Others.

3. What are the main segments of the Africa SVOD Market?

The market segments include Content Genre, Revenue Model, Device Type, User Base.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.10 Million as of 2022.

5. What are some drivers contributing to market growth?

Intensification of Competition as Several Global Players Enter the Market to capture the Nascent audience; Enticing Marketing Strategies like Free Mobile Plans. Regional Partnerships. etc. are anticipated to aid the Long Time Growth of Market.

6. What are the notable trends driving market growth?

Drama Genre is Expected to Drive the Market.

7. Are there any restraints impacting market growth?

Higher Pricing Plans act as a Barrier for Adoption.

8. Can you provide examples of recent developments in the market?

February 2023: Amazon Prime Video announced a multi-picture licensing arrangement with South Africa's Known Associates, the parent company of Johannesburg-based Known Associates Entertainment (KAE) and Cape Town-based Moonlighting Films, during the Joburg Film Festival on Thursday. Over 20 South African feature films, including Zane Meas' "Klip Anker Baai," Marvin-Lee Beukes' "Tickets," Jahmil Qubeka's "You Are My Favourite Place," and Norman Maake's "Piet's Sake 2," will be available exclusively on Prime Video.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Africa SVOD Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Africa SVOD Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Africa SVOD Market?

To stay informed about further developments, trends, and reports in the Africa SVOD Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence