Key Insights

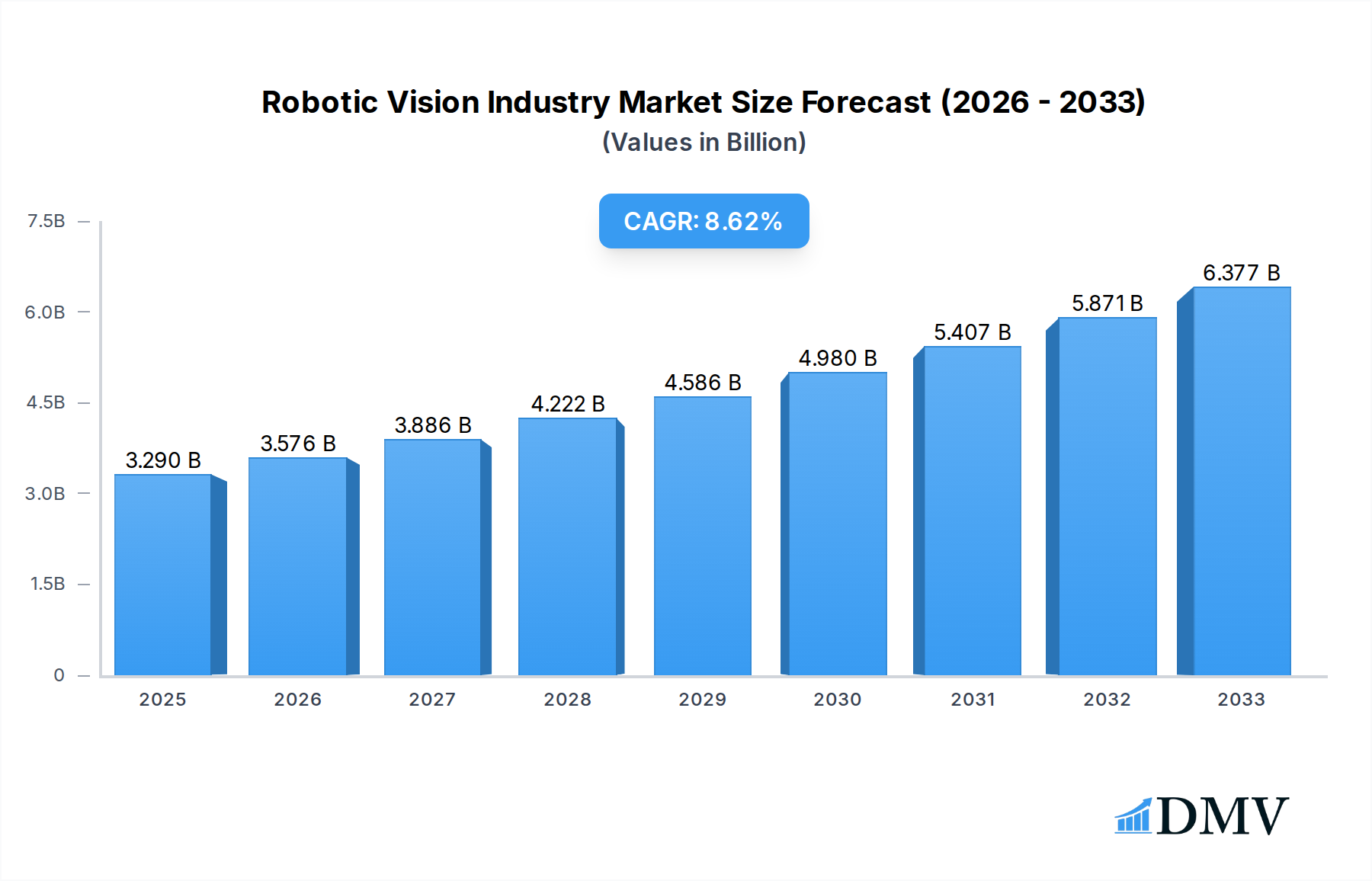

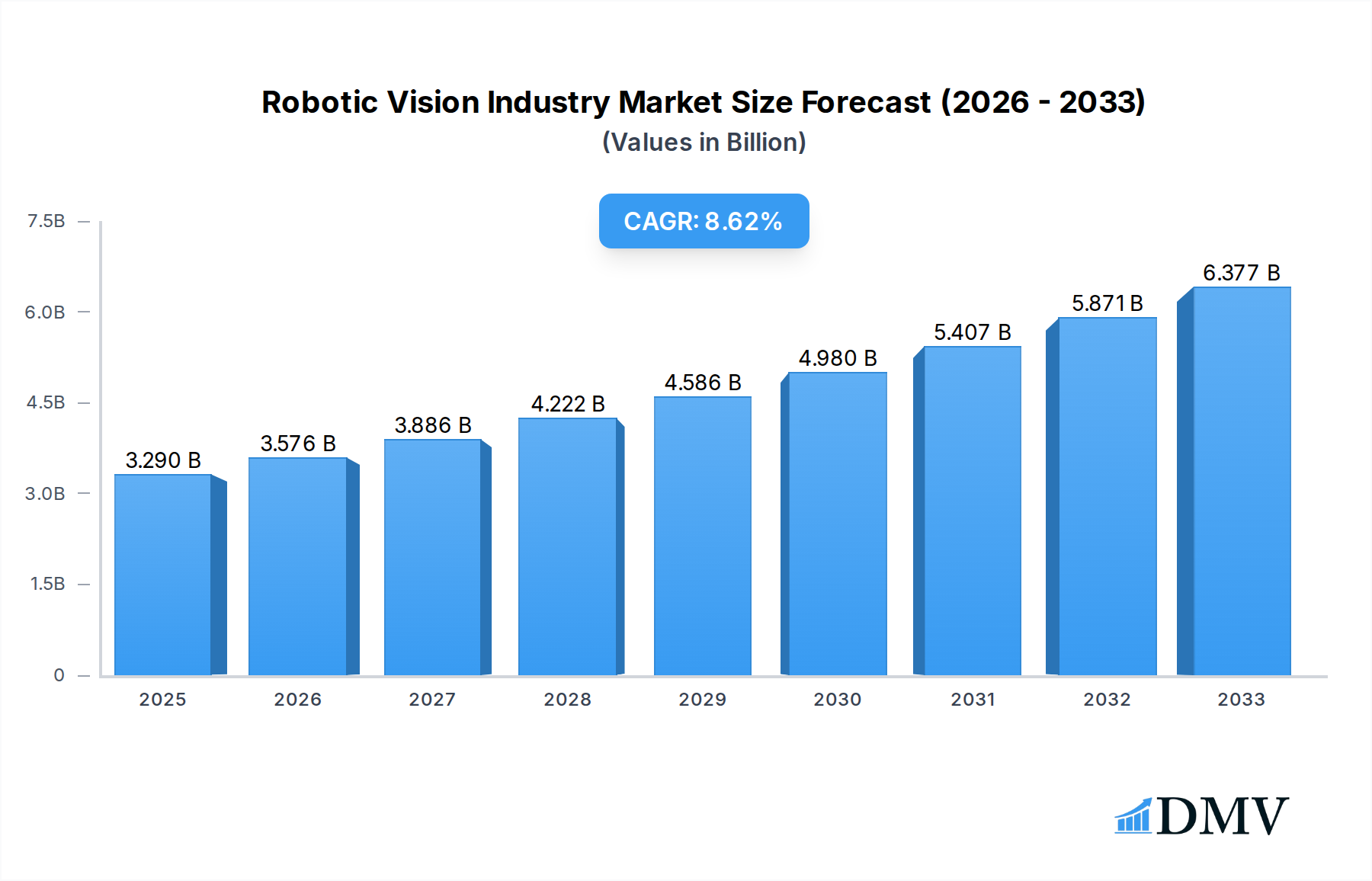

The global Robotic Vision Industry is poised for substantial expansion, projected to reach a market size of $3.29 billion in 2025, with an impressive Compound Annual Growth Rate (CAGR) of 8.7% from 2019 to 2033. This robust growth is propelled by several key drivers, including the increasing demand for automation across manufacturing sectors, the growing need for quality control and inspection, and the advancements in artificial intelligence and machine learning that enhance the capabilities of robotic vision systems. The integration of 2D and 3D vision technologies allows robots to perceive and interact with their environment with greater precision, facilitating complex tasks that were previously impossible. Trends such as the adoption of collaborative robots (cobots) equipped with advanced vision systems and the rise of Industry 4.0 initiatives are further fueling market penetration.

Robotic Vision Industry Market Size (In Billion)

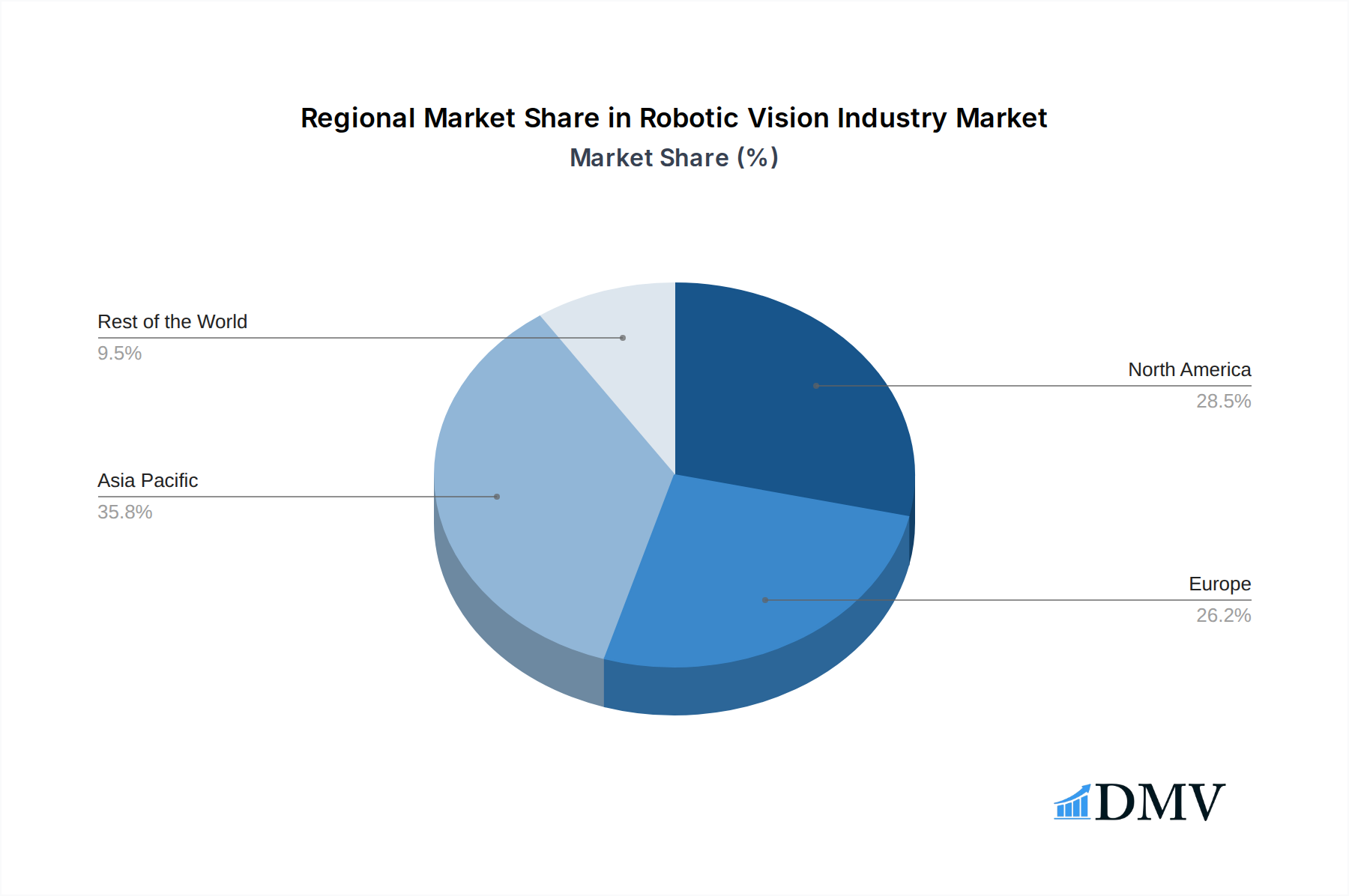

Despite the strong growth trajectory, certain restraints could temper the pace of expansion. High initial investment costs for sophisticated robotic vision systems and a shortage of skilled personnel to operate and maintain these technologies present challenges. However, the widespread adoption of robotic vision in industries like automotive, electronics, aerospace, food and beverage, and pharmaceuticals is expected to offset these limitations. The expanding applications, from intricate assembly tasks in electronics to precise inspection in food packaging, underscore the versatility and indispensable nature of robotic vision. Asia Pacific is anticipated to be a dominant region, driven by its extensive manufacturing base and rapid technological adoption, followed closely by North America and Europe, which are investing heavily in automation to maintain competitive advantages.

Robotic Vision Industry Company Market Share

Here is an SEO-optimized report description for the Robotic Vision Industry, designed to boost search visibility and captivate stakeholders.

Robotic Vision Industry Market Report: Comprehensive Analysis & Forecast (2019–2033)

Unlock critical insights into the rapidly expanding Robotic Vision Industry with this definitive market research report. Covering the historical period from 2019–2024, with a base year of 2025 and a forecast period extending to 2033, this analysis provides an in-depth exploration of market dynamics, technological advancements, and future growth trajectories. Discover the transformative power of machine vision, industrial robotics, and AI in manufacturing across key sectors like Automotive, Electronics, and Aerospace. This report is essential for understanding the global robotic vision market size, 2D vision, 3D vision technologies, and the strategies of major players including Keyence Corporation, FANUC Corporation, National Instruments Corporation, Cognex Corporation, Teledyne Dalsa Inc, Sick AG, ABB Group, Qualcomm Technologies Inc, Hexagon AB, and Omron Adept Technology Inc.

Robotic Vision Industry Market Composition & Trends

The Robotic Vision Industry is characterized by dynamic market concentration driven by continuous innovation and strategic mergers and acquisitions. While a few dominant players command significant market share, a burgeoning ecosystem of specialized technology providers fuels competitive growth. Innovation catalysts include advancements in deep learning for machine vision, edge computing for robotics, and the increasing demand for intelligent automation. The regulatory landscape, while evolving, is largely supportive of automation technologies, particularly those enhancing safety and efficiency. Substitute products are minimal, as robotic vision offers unique capabilities that are difficult to replicate. End-user profiles are diverse, ranging from large-scale automotive manufacturers seeking robot vision inspection to pharmaceutical companies requiring precision in their automated quality control. M&A activities are a significant trend, with deals valued in the billions of dollars, as companies seek to integrate complementary technologies and expand their market reach. For instance, the acquisition of mobile robot companies by larger automation firms underscores a strategic push towards integrated robotic solutions. The market's growth is further shaped by its capacity to address complex industrial challenges with advanced computer vision and robot guidance systems.

Robotic Vision Industry Industry Evolution

The Robotic Vision Industry has witnessed a profound evolution, transforming from niche applications to a cornerstone of modern industrial automation. Over the study period of 2019–2033, and particularly from the historical period of 2019–2024, the market has experienced exponential growth driven by relentless technological innovation and an increasing demand for sophisticated automation solutions. The base year of 2025 marks a pivotal point, with the market poised for sustained expansion throughout the forecast period of 2025–2033. This growth trajectory is underpinned by the continuous refinement of 2D vision and the rapid ascent of 3D vision technologies, enabling robots to perceive and interact with their environments with unprecedented accuracy. Shifting consumer demands for higher quality products, faster production cycles, and increased customization have amplified the need for robotic guidance systems and machine vision inspection. Adoption metrics indicate a significant uptake across diverse industries. For example, the automotive sector, a traditional leader, continues to invest heavily in vision-guided robotics for assembly and quality control, expecting growth rates in the high single digits. Similarly, the electronics industry's demand for precision and miniaturization in PCB inspection and component placement is a major growth driver, with adoption rates exceeding 15% annually in specific sub-segments. The integration of AI and machine learning into robotic vision systems has moved them beyond simple data acquisition to intelligent decision-making, further accelerating their adoption. The ability to perform complex tasks such as defect detection, object recognition, and precise manipulation has made robotic vision indispensable for companies aiming to enhance operational efficiency, reduce waste, and maintain a competitive edge. The market's evolution is not just about technological advancement but also about the democratization of these powerful tools, making them accessible to a wider range of businesses.

Leading Regions, Countries, or Segments in Robotic Vision Industry

The Robotic Vision Industry exhibits distinct leadership across various segments and geographical regions, driven by a confluence of technological adoption, industrial demand, and supportive ecosystems. In terms of Technology, 3D Vision is emerging as a dominant segment, rapidly gaining traction due to its superior depth perception and spatial understanding capabilities, crucial for complex automation tasks. This contrasts with the continued strength of 2D Vision, which remains a foundational technology, particularly for inspection and identification applications where cost-effectiveness and established performance are paramount.

Across End User Industries, the Automotive sector consistently leads the adoption of robotic vision. Key drivers include:

- High Volume Production Needs: The automotive industry's sheer scale necessitates efficient, high-speed automation for assembly, welding, painting, and quality inspection.

- Stringent Quality Standards: The demand for flawless vehicle components and assemblies drives the need for advanced vision inspection systems to detect even minute defects.

- Electrification and Advanced Manufacturing: The shift towards electric vehicles (EVs) and the integration of new materials and complex battery systems create new challenges and opportunities for robotic vision in manufacturing.

- Investment Trends: Significant capital investment by major automotive manufacturers in advanced manufacturing technologies, including robotics and automation, directly fuels the robotic vision market.

The Electronics industry also represents a substantial and rapidly growing segment. Drivers here include:

- Miniaturization and Complexity: The continuous trend towards smaller, more complex electronic components requires highly precise robot guidance and vision inspection for tasks like SMT placement and solder joint inspection.

- High-Value Products: The high value of electronic components makes robust defect detection and quality assurance through robotic vision economically crucial.

- Rapid Product Lifecycles: The fast pace of innovation in consumer electronics necessitates agile and efficient production lines, where robotic vision plays a vital role in speed and accuracy.

While Aerospace and Food & Beverage also represent significant markets with specific needs for inspection and quality control, and Pharmaceutical utilizes it for critical safety and compliance, the sheer volume of integration and investment in the Automotive and Electronics sectors places them at the forefront of current robotic vision market dominance. Geographically, North America and Europe are mature markets with high adoption rates, driven by established industrial bases and strong R&D capabilities. However, the Asia-Pacific region, particularly China, is experiencing the most rapid growth, fueled by a booming manufacturing sector and government initiatives promoting industrial automation. The integration of AI in manufacturing further accelerates the dominance of these key segments and regions, as they are quickest to adopt and leverage these advanced capabilities.

Robotic Vision Industry Product Innovations

Product innovations in the Robotic Vision Industry are centered on enhancing intelligence, speed, and versatility. Advanced deep learning algorithms are now embedded directly into vision hardware, enabling real-time defect detection and object recognition with unprecedented accuracy. Innovations in 3D sensing technology, including structured light and time-of-flight cameras, are providing richer environmental data for more sophisticated robot navigation and manipulation. Novel camera designs with higher resolutions, faster frame rates, and improved low-light performance are also key, allowing for the inspection of finer details and faster production lines. Furthermore, the integration of edge AI processing within vision systems reduces latency and the need for constant cloud connectivity, making robotic vision solutions more robust and efficient for applications like guided robotics and autonomous mobile robots (AMRs). These advancements are crucial for applications ranging from intricate assembly inspection to the precise guidance of robots in complex logistics environments.

Propelling Factors for Robotic Vision Industry Growth

Several key factors are propelling the growth of the Robotic Vision Industry. Technologically, continuous advancements in AI and machine learning, particularly in deep learning for computer vision, are enabling more intelligent and autonomous robotic systems. The increasing demand for enhanced quality control and inspection across all manufacturing sectors, driven by consumer expectations and regulatory requirements, is a major catalyst. Economically, the drive for increased productivity, reduced operational costs, and improved efficiency in manufacturing operations makes industrial automation and robotic vision an attractive investment. Furthermore, government initiatives and incentives promoting Industry 4.0 adoption and smart manufacturing are creating a favorable environment for market expansion. The development of more affordable and user-friendly machine vision systems is also democratizing access to these technologies, further fueling growth.

Obstacles in the Robotic Vision Industry Market

Despite robust growth, the Robotic Vision Industry faces several obstacles. High initial investment costs for sophisticated robotic vision systems and integrated solutions can be a barrier for small and medium-sized enterprises (SMEs). A significant shortage of skilled personnel capable of designing, implementing, and maintaining these advanced systems poses a persistent challenge. Supply chain disruptions, particularly for specialized components, can impact production timelines and cost-effectiveness. Furthermore, the complexity of integrating robotic vision into existing legacy manufacturing infrastructure requires substantial engineering effort and can lead to longer implementation cycles. Cybersecurity concerns associated with increasingly connected industrial automation systems also represent a growing area of focus and potential restraint.

Future Opportunities in Robotic Vision Industry

The Robotic Vision Industry is ripe with future opportunities. The expansion of 3D vision technologies into new applications, such as advanced metrology and augmented reality for maintenance, presents significant potential. The growth of the e-commerce logistics sector demands more sophisticated vision systems for sorting, picking, and packing. The increasing adoption of autonomous mobile robots (AMRs) in warehousing and manufacturing environments will drive demand for enhanced navigation and object recognition capabilities. Furthermore, the burgeoning fields of robotics in healthcare and agriculture are opening up entirely new markets for specialized robotic vision solutions. The continued miniaturization and cost reduction of sensors and processing power will also enable wider adoption in previously underserved markets.

Major Players in the Robotic Vision Industry Ecosystem

- Keyence Corporation

- FANUC Corporation

- National Instruments Corporation

- Cognex Corporation

- Teledyne Dalsa Inc

- Sick AG

- ABB Group

- Qualcomm Technologies Inc

- Hexagon AB

- Omron Adept Technology Inc

Key Developments in Robotic Vision Industry Industry

- September 2022: ABB launches its first line of branded Autonomous Mobile Robots (AMRs) following its 2021 acquisition of ASTI Mobile Robotics, showcasing a fully integrated offering of robots, AMRs, and machine automation solutions. ABB's automation system, including robots and vision function packages, was used in a UK collaboration with Expert Technology Group to develop a complete assembly line based on AMRs for EV vehicle drivetrain part production.

- August 2022: Visionary.ai and Innoviz announce a partnership to integrate Visionary.ai's image signal processor (ISP) technology with Innoviz's LiDAR sensors and perception software. This collaboration aims to enhance 3D machine vision performance for robots and drones.

Strategic Robotic Vision Industry Market Forecast

The strategic Robotic Vision Industry market forecast indicates a period of sustained and accelerated growth. The increasing demand for intelligent automation, driven by the need for enhanced productivity, quality, and flexibility, will continue to be a primary growth catalyst. Advancements in AI and deep learning will further empower robotic vision systems, enabling them to tackle more complex tasks and operate in dynamic environments. The expansion of 3D vision and its integration with other sensing technologies will unlock new application areas across industries. Emerging markets, coupled with the ongoing digital transformation of manufacturing globally, represent significant untapped potential. Companies that focus on developing integrated, intelligent, and adaptable robotic vision solutions are well-positioned to capitalize on the substantial market opportunities ahead, with the global market expected to reach billions in value by 2033.

Robotic Vision Industry Segmentation

-

1. Technology

- 1.1. 2D Vision

- 1.2. 3D Vision

-

2. End User Industry

- 2.1. Automotive

- 2.2. Electronics

- 2.3. Aerospace

- 2.4. Food and Beverage

- 2.5. Pharmaceutical

- 2.6. Other End User Industries

Robotic Vision Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Rest of the World

Robotic Vision Industry Regional Market Share

Geographic Coverage of Robotic Vision Industry

Robotic Vision Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 5.1.1. 2D Vision

- 5.1.2. 3D Vision

- 5.2. Market Analysis, Insights and Forecast - by End User Industry

- 5.2.1. Automotive

- 5.2.2. Electronics

- 5.2.3. Aerospace

- 5.2.4. Food and Beverage

- 5.2.5. Pharmaceutical

- 5.2.6. Other End User Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 6. Global Robotic Vision Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Technology

- 6.1.1. 2D Vision

- 6.1.2. 3D Vision

- 6.2. Market Analysis, Insights and Forecast - by End User Industry

- 6.2.1. Automotive

- 6.2.2. Electronics

- 6.2.3. Aerospace

- 6.2.4. Food and Beverage

- 6.2.5. Pharmaceutical

- 6.2.6. Other End User Industries

- 6.1. Market Analysis, Insights and Forecast - by Technology

- 7. North America Robotic Vision Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Technology

- 7.1.1. 2D Vision

- 7.1.2. 3D Vision

- 7.2. Market Analysis, Insights and Forecast - by End User Industry

- 7.2.1. Automotive

- 7.2.2. Electronics

- 7.2.3. Aerospace

- 7.2.4. Food and Beverage

- 7.2.5. Pharmaceutical

- 7.2.6. Other End User Industries

- 7.1. Market Analysis, Insights and Forecast - by Technology

- 8. Europe Robotic Vision Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Technology

- 8.1.1. 2D Vision

- 8.1.2. 3D Vision

- 8.2. Market Analysis, Insights and Forecast - by End User Industry

- 8.2.1. Automotive

- 8.2.2. Electronics

- 8.2.3. Aerospace

- 8.2.4. Food and Beverage

- 8.2.5. Pharmaceutical

- 8.2.6. Other End User Industries

- 8.1. Market Analysis, Insights and Forecast - by Technology

- 9. Asia Pacific Robotic Vision Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Technology

- 9.1.1. 2D Vision

- 9.1.2. 3D Vision

- 9.2. Market Analysis, Insights and Forecast - by End User Industry

- 9.2.1. Automotive

- 9.2.2. Electronics

- 9.2.3. Aerospace

- 9.2.4. Food and Beverage

- 9.2.5. Pharmaceutical

- 9.2.6. Other End User Industries

- 9.1. Market Analysis, Insights and Forecast - by Technology

- 10. Rest of the World Robotic Vision Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Technology

- 10.1.1. 2D Vision

- 10.1.2. 3D Vision

- 10.2. Market Analysis, Insights and Forecast - by End User Industry

- 10.2.1. Automotive

- 10.2.2. Electronics

- 10.2.3. Aerospace

- 10.2.4. Food and Beverage

- 10.2.5. Pharmaceutical

- 10.2.6. Other End User Industries

- 10.1. Market Analysis, Insights and Forecast - by Technology

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Keyence Corporation

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 FANUC Corporation

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 National Instruments Corporation

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Cognex Corporation

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Teledyne Dalsa Inc

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Sick AG

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 ABB Group

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Qualcomm Technologies Inc

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Hexagon A

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Omron Adept Technology Inc

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.1 Keyence Corporation

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Robotic Vision Industry Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Robotic Vision Industry Revenue (undefined), by Technology 2025 & 2033

- Figure 3: North America Robotic Vision Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 4: North America Robotic Vision Industry Revenue (undefined), by End User Industry 2025 & 2033

- Figure 5: North America Robotic Vision Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 6: North America Robotic Vision Industry Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Robotic Vision Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Robotic Vision Industry Revenue (undefined), by Technology 2025 & 2033

- Figure 9: Europe Robotic Vision Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 10: Europe Robotic Vision Industry Revenue (undefined), by End User Industry 2025 & 2033

- Figure 11: Europe Robotic Vision Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 12: Europe Robotic Vision Industry Revenue (undefined), by Country 2025 & 2033

- Figure 13: Europe Robotic Vision Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Robotic Vision Industry Revenue (undefined), by Technology 2025 & 2033

- Figure 15: Asia Pacific Robotic Vision Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 16: Asia Pacific Robotic Vision Industry Revenue (undefined), by End User Industry 2025 & 2033

- Figure 17: Asia Pacific Robotic Vision Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 18: Asia Pacific Robotic Vision Industry Revenue (undefined), by Country 2025 & 2033

- Figure 19: Asia Pacific Robotic Vision Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Rest of the World Robotic Vision Industry Revenue (undefined), by Technology 2025 & 2033

- Figure 21: Rest of the World Robotic Vision Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 22: Rest of the World Robotic Vision Industry Revenue (undefined), by End User Industry 2025 & 2033

- Figure 23: Rest of the World Robotic Vision Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 24: Rest of the World Robotic Vision Industry Revenue (undefined), by Country 2025 & 2033

- Figure 25: Rest of the World Robotic Vision Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Robotic Vision Industry Revenue undefined Forecast, by Technology 2020 & 2033

- Table 2: Global Robotic Vision Industry Revenue undefined Forecast, by End User Industry 2020 & 2033

- Table 3: Global Robotic Vision Industry Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Robotic Vision Industry Revenue undefined Forecast, by Technology 2020 & 2033

- Table 5: Global Robotic Vision Industry Revenue undefined Forecast, by End User Industry 2020 & 2033

- Table 6: Global Robotic Vision Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: Global Robotic Vision Industry Revenue undefined Forecast, by Technology 2020 & 2033

- Table 8: Global Robotic Vision Industry Revenue undefined Forecast, by End User Industry 2020 & 2033

- Table 9: Global Robotic Vision Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 10: Global Robotic Vision Industry Revenue undefined Forecast, by Technology 2020 & 2033

- Table 11: Global Robotic Vision Industry Revenue undefined Forecast, by End User Industry 2020 & 2033

- Table 12: Global Robotic Vision Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Global Robotic Vision Industry Revenue undefined Forecast, by Technology 2020 & 2033

- Table 14: Global Robotic Vision Industry Revenue undefined Forecast, by End User Industry 2020 & 2033

- Table 15: Global Robotic Vision Industry Revenue undefined Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Robotic Vision Industry?

The projected CAGR is approximately 8.7%.

2. Which companies are prominent players in the Robotic Vision Industry?

Key companies in the market include Keyence Corporation, FANUC Corporation, National Instruments Corporation, Cognex Corporation, Teledyne Dalsa Inc, Sick AG, ABB Group, Qualcomm Technologies Inc, Hexagon A, Omron Adept Technology Inc.

3. What are the main segments of the Robotic Vision Industry?

The market segments include Technology, End User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

Increased Adoption of Cognitive Humanoid Robots; Growing Demand from End - User Segments like Automotive Industry.

6. What are the notable trends driving market growth?

Growing Demand from End-User Segments like Automotive Industry Drives the Market Growth.

7. Are there any restraints impacting market growth?

High Investments.

8. Can you provide examples of recent developments in the market?

September 2022 - Following the 2021 acquisition of mobile robot company ASTI Mobile Robotics, ABB has launched its first line of branded Autonomous Mobile Robots (AMRs). ABB has a fully integrated offering of robots, AMRs, and machine automation solutions. ABB, which already provides AMR solutions for client projects, has collaborated with crucial partner Expert Technology Group in the UK to develop a complete assembly line based on AMRs for a technology startup creating breakthrough parts for EV vehicle drive trains. ABB's automation system uses ABB robots, vision function packages, and AMRs to transport products between robotic automation cells and human assembly stations.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Robotic Vision Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Robotic Vision Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Robotic Vision Industry?

To stay informed about further developments, trends, and reports in the Robotic Vision Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence