Key Insights

The Silicon Carbide (SiC) Power Chip market is projected for significant expansion, driven by the escalating demand for enhanced energy efficiency, superior power density, and robust performance across diverse applications. The market is anticipated to achieve a compound annual growth rate (CAGR) of 25.7%. This growth is primarily propelled by the electric vehicle (EV) and hybrid EV (HEV) sectors, where SiC technology enables extended driving range, faster charging capabilities, and improved overall vehicle efficiency. The development of EV charging infrastructure and the adoption of SiC in industrial motor drives and power supplies further reinforce this growth trajectory. Photovoltaic (PV) systems, energy storage solutions, and wind power generation are also increasingly integrating SiC, contributing to its widespread adoption and solidifying its position as the material of choice for advanced power electronics due to its higher breakdown voltage, reduced switching losses, and superior thermal conductivity compared to traditional silicon.

Silicon Carbide Power Chip Market Size (In Billion)

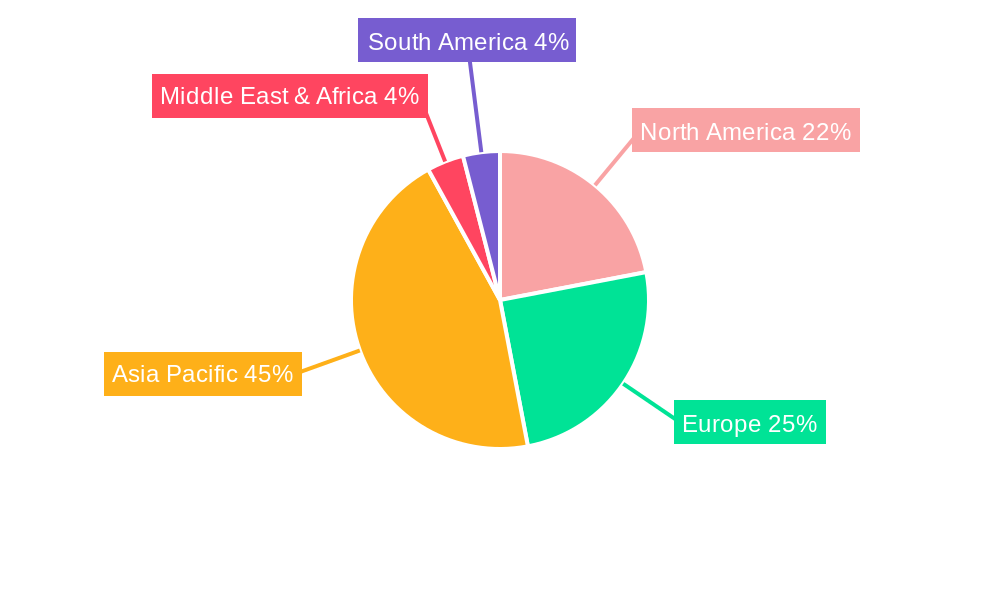

The SiC Power Chip market features a dynamic application landscape, with Automotive & EV/HEV leading, followed by substantial contributions from EV Charging, Industrial Motor/Drive, and PV segments. Key product types include SiC MOSFET Modules and SiC MOSFET Discretes. Geographically, the Asia Pacific region, particularly China, is expected to be a pivotal market for both production and consumption, driven by its leadership in EV manufacturing and renewable energy deployment. North America and Europe are also exhibiting strong growth, influenced by stringent emission regulations and a commitment to sustainable energy solutions. The competitive environment is characterized by established industry leaders and innovative emerging players, all focused on R&D, capacity expansion, and technological innovation to secure market share in this rapidly expanding domain.

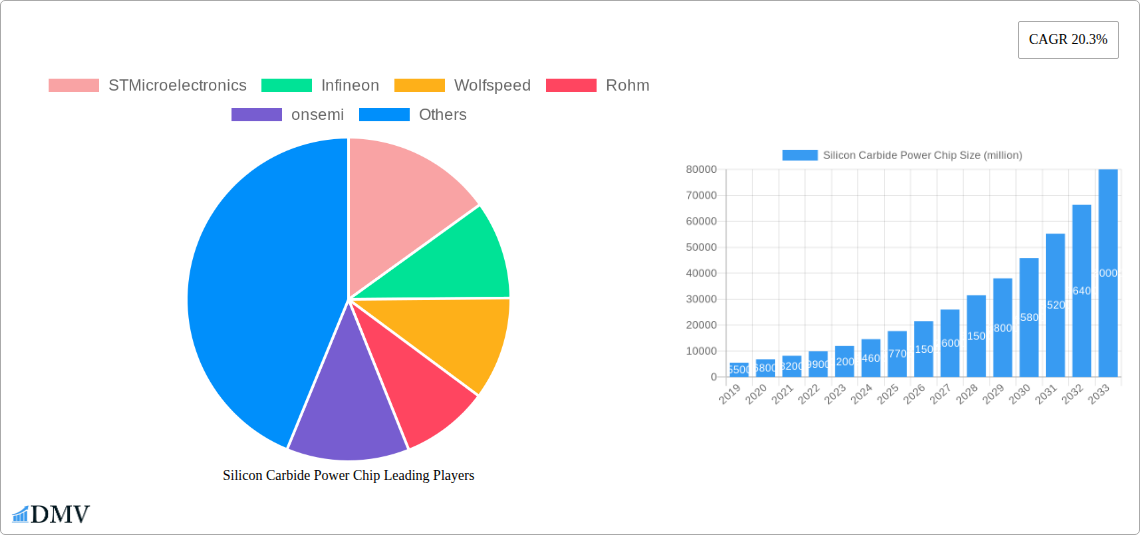

Silicon Carbide Power Chip Company Market Share

This comprehensive market research report provides an in-depth analysis of the global Silicon Carbide (SiC) Power Chip market, a crucial technology revolutionizing power electronics across numerous industries. With a base year of 2025 and projecting forward, the report offers strategic insights into market size, growth drivers, challenges, and emerging trends. The market size is estimated at 3.83 billion by 2025. This analysis equips stakeholders with the essential knowledge to navigate and capitalize on opportunities within this rapidly evolving sector.

Silicon Carbide Power Chip Market Composition & Trends

The global Silicon Carbide (SiC) Power Chip market is characterized by a dynamic interplay of innovation, strategic investments, and evolving regulatory frameworks. Market concentration, while influenced by leading players, is progressively diversifying as new entrants leverage technological breakthroughs and expanding application landscapes. Innovation catalysts are primarily driven by the quest for higher efficiency, increased power density, and enhanced thermal performance, directly addressing the growing demands of high-performance applications. Regulatory landscapes, particularly concerning energy efficiency standards and carbon emission reduction targets, are acting as significant tailwinds for SiC adoption. Substitute products, while present, are increasingly being outpaced by the superior performance characteristics of SiC. End-user profiles are expanding from niche industrial and automotive applications to mainstream consumer electronics and renewable energy infrastructure. Mergers and acquisitions (M&A) are a notable trend, with significant deal values indicating consolidation and strategic positioning by key players aiming to secure intellectual property and market share. For instance, M&A activities in the historical period are valued in the hundreds of millions. Market share distribution is highly competitive, with the top five players holding approximately 60-70% of the global market.

Silicon Carbide Power Chip Industry Evolution

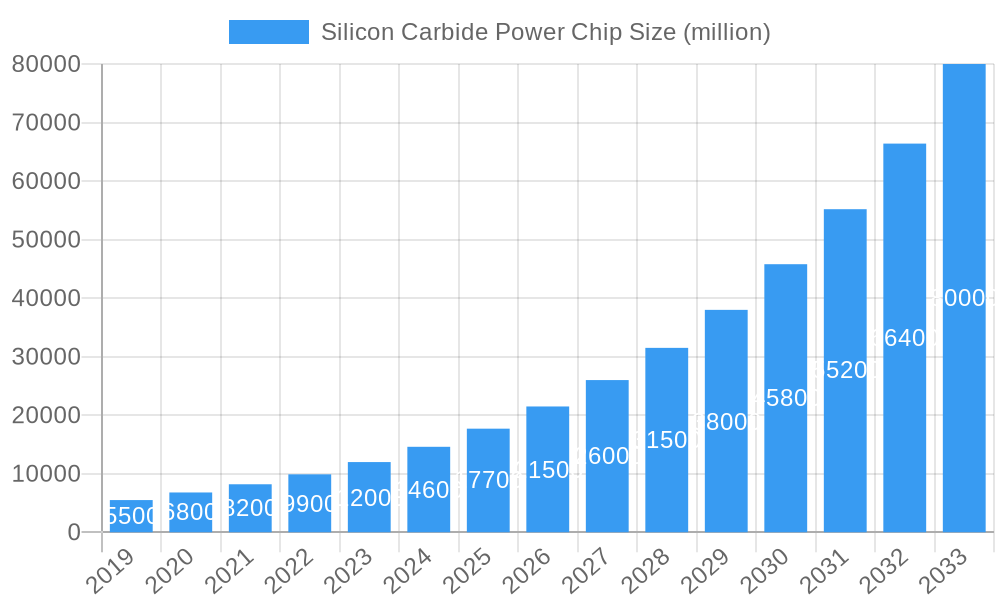

The Silicon Carbide (SiC) Power Chip industry has witnessed a dramatic evolution, transforming from a specialized, high-cost technology into a mainstream enabler of next-generation power solutions. The historical period (2019–2024) saw significant acceleration in SiC adoption, driven by the burgeoning electric vehicle (EV) market and the urgent need for greater energy efficiency in industrial processes and renewable energy systems. Technological advancements have been the bedrock of this evolution. Early iterations focused on improving the fundamental material quality of SiC substrates, leading to reduced defect densities and consequently, higher device reliability and performance. This was followed by significant progress in device design and manufacturing processes for both SiC MOSFETs (Metal-Oxide-Semiconductor Field-Effect Transistors) and SiC diodes, enabling them to handle higher voltages and currents with lower power losses. The transition from silicon-based power devices to SiC has been characterized by a consistent upward trajectory in growth rates, averaging around 25-30% year-on-year during the historical period. Consumer demand has shifted towards more sustainable and energy-efficient solutions, making SiC a highly desirable material. The ability of SiC devices to operate at higher switching frequencies translates into smaller, lighter, and more cost-effective power supply designs, further fueling adoption. For example, in the automotive sector, the integration of SiC in inverters and onboard chargers has enabled longer EV range and faster charging times, directly addressing key consumer pain points. The industrial sector benefits from reduced energy consumption and increased operational efficiency in motor drives and power supplies. The renewable energy sector, including solar photovoltaics (PV) and wind power, is leveraging SiC to maximize energy harvest and grid integration. The forecast period (2025–2033) is expected to witness an even more pronounced growth phase, with sustained double-digit compound annual growth rates (CAGR) in the range of 20-25%, propelled by continued technological maturation, expanding manufacturing capacity, and increasing cost-competitiveness. The market size is projected to reach several tens of billions of dollars by the end of the forecast period, a substantial increase from the tens of millions recorded in the early historical years. The increasing adoption metrics, such as the percentage of new inverter designs featuring SiC, are steadily rising, reflecting a fundamental shift in the power electronics landscape.

Leading Regions, Countries, or Segments in Silicon Carbide Power Chip

The Silicon Carbide (SiC) Power Chip market's dominance is a multifaceted phenomenon, with key regions, countries, and application segments emerging as pivotal growth engines.

Dominant Application Segments:

- Automotive & EV/HEV: This segment is undeniably the leading driver of SiC power chip demand. The insatiable appetite for electrification in the automotive industry, coupled with stringent fuel economy and emission regulations worldwide, has made SiC indispensable for inverters, onboard chargers, and DC-DC converters. The drive for longer EV ranges, faster charging capabilities, and improved overall vehicle efficiency directly translates into massive adoption of SiC MOSFET modules and SiC MOSFET discretes. Investments in this sector are in the billions, driven by both established automotive manufacturers and burgeoning EV startups.

- EV Charging: Closely intertwined with the automotive sector, EV charging infrastructure is a significant growth area. Higher efficiency and power density offered by SiC enable faster and more compact charging stations, reducing installation costs and improving user experience. This segment is witnessing substantial government support and private investment in the hundreds of millions to scale up charging networks globally.

- Industrial Motor/Drive: The industrial sector is increasingly recognizing the energy savings and performance enhancements offered by SiC. Variable frequency drives (VFDs) for industrial motors, leveraging SiC MOSFETs, can significantly reduce energy consumption, leading to substantial operational cost savings. The push for industrial automation and energy efficiency has spurred investments in the hundreds of millions for upgrades and new installations.

- PV & Energy Storage: In renewable energy, SiC is crucial for maximizing the efficiency of solar inverters and battery energy storage systems (BESS). Higher conversion efficiencies mean more energy harvested from solar panels and more efficient power management in storage solutions. Investments here are in the hundreds of millions, driven by climate change mitigation efforts and the pursuit of grid independence.

Leading Regions and Countries:

- Asia Pacific (APAC): This region, particularly China, has emerged as the dominant force in the SiC power chip market. Its leadership is fueled by several key factors:

- Massive Domestic Demand: China's unparalleled leadership in EV production and adoption, coupled with its extensive industrial base and ambitious renewable energy targets, creates an enormous domestic market for SiC.

- Government Support and Policy: Strong government initiatives and subsidies promoting indigenous semiconductor manufacturing and the adoption of new energy vehicles provide a robust ecosystem for SiC growth. Investment in the SiC supply chain by Chinese entities is in the tens of billions.

- Growing Manufacturing Capabilities: Significant investments in local SiC wafer manufacturing and device fabrication facilities are rapidly expanding production capacity, making SiC more accessible and cost-competitive.

- Emerging Players: The region hosts a growing number of SiC chip manufacturers, fostering healthy competition and innovation.

- North America & Europe: These regions are also critical markets, characterized by substantial investments in EV infrastructure, advanced industrial applications, and renewable energy projects. Regulatory frameworks supporting decarbonization and technological innovation are strong drivers. Investments in these regions are in the billions.

Dominant Device Type:

- SiC MOSFET Modules: These modules are increasingly preferred for high-power applications due to their integrated design, ease of implementation, and superior thermal management capabilities. Their dominance is particularly pronounced in the automotive and industrial sectors where reliability and performance are paramount.

Silicon Carbide Power Chip Product Innovations

Product innovation in Silicon Carbide (SiC) power chips is rapidly advancing, focusing on enhanced performance and broader application integration. Innovations include the development of SiC MOSFETs with lower on-resistance and gate charge, leading to improved efficiency and faster switching speeds, crucial for applications like electric vehicle inverters and industrial motor drives. SiC Schottky Barrier Diodes (SBDs) are also seeing advancements, offering lower leakage current and higher surge current capabilities. New module designs are integrating more functionalities, such as gate drivers and protection circuits, simplifying system design and improving reliability. Performance metrics like breakdown voltage exceeding tens of kilovolts, operating temperatures pushing past 200°C, and switching frequencies reaching hundreds of kilohertz are becoming standard. These advancements are critical for achieving higher power density and reducing the overall system size and weight in power conversion applications.

Propelling Factors for Silicon Carbide Power Chip Growth

Several key factors are propelling the growth of the Silicon Carbide (SiC) power chip market. Technological advancements are at the forefront, with continuous improvements in SiC wafer quality, device fabrication processes, and packaging technologies leading to higher performance, greater reliability, and reduced costs. The economic benefits are substantial, driven by the superior energy efficiency of SiC devices, which translates into significant operational cost savings in applications like electric vehicles, industrial motor drives, and data centers. Furthermore, the regulatory push for decarbonization and increased energy efficiency across various sectors worldwide is a powerful catalyst, mandating the adoption of more efficient power electronics solutions. The burgeoning electric vehicle (EV) market, with its immense demand for efficient power conversion components, is arguably the single largest growth driver. Finally, growing consumer awareness and demand for sustainable and energy-efficient products are indirectly fueling the market by encouraging manufacturers to adopt advanced technologies like SiC.

Obstacles in the Silicon Carbide Power Chip Market

Despite robust growth, the Silicon Carbide (SiC) power chip market faces several obstacles. High manufacturing costs remain a significant barrier, particularly for SiC wafer production and device fabrication, making SiC devices more expensive than their silicon counterparts in certain applications. Supply chain disruptions, including limited raw material availability for SiC substrates and bottlenecks in manufacturing capacity, can lead to price volatility and extended lead times, impacting production schedules. Technological challenges persist in areas like packaging to handle higher operating temperatures and voltages effectively, and ensuring long-term reliability in demanding environments. Competition from advanced silicon-based technologies, such as IGBTs and GaN, also presents a challenge in cost-sensitive market segments. Furthermore, lack of widespread standardization in certain SiC device specifications can create integration complexities for system designers.

Future Opportunities in Silicon Carbide Power Chip

The future for Silicon Carbide (SiC) power chips is replete with promising opportunities. The continued expansion of the electric vehicle (EV) market, including commercial vehicles and heavy-duty trucks, presents a massive untapped potential. Growth in renewable energy integration, such as advanced solar inverters and grid-scale energy storage, will further drive demand. The increasing power requirements and efficiency mandates in data centers and telecommunications infrastructure offer significant growth avenues. Emerging opportunities also lie in high-voltage direct current (HVDC) transmission systems and advanced industrial automation. Furthermore, advancements in SiC-based sensor technologies and power management ICs for specialized applications could unlock new market segments. The development of lower-cost manufacturing processes and innovative packaging solutions will accelerate adoption across a broader spectrum of applications.

Major Players in the Silicon Carbide Power Chip Ecosystem

- STMicroelectronics

- Infineon Technologies AG

- Wolfspeed, Inc.

- Rohm Semiconductor

- onsemi

- BYD Semiconductor

- Microchip Technology (formerly Microsemi)

- Mitsubishi Electric Corporation (Vincotech)

- Semikron Danfoss

- Fuji Electric Co., Ltd.

- Navitas Semiconductor (GeneSiC)

- Toshiba Corporation

- Qorvo (UnitedSiC)

- San'an Optoelectronics

- Littelfuse, Inc. (IXYS)

- CETC 55

- WeEn Semiconductors

- BASiC Semiconductor

- SemiQ

- Diodes Incorporated

- SanRex Corporation

- Alpha & Omega Semiconductor

- Robert Bosch GmbH

- KEC Corporation

- PANJIT Group

- Nexperia

- Vishay Intertechnology, Inc.

- Zhuzhou CRRC Times Electric Co., Ltd.

- China Resources Microelectronics Limited

- StarPower Semiconductor Ltd.

- Yangzhou Yangjie Electronic Technology Co., Ltd.

- Guangdong AccoPower Semiconductor Co., Ltd.

- Changzhou Galaxy Century Microelectronics Co., Ltd.

- Hangzhou Silan Microelectronics Co., Ltd.

- Cissoid SA

- SK powertech

- InventChip Technology

- Hebei Sinopack Electronic Technology Co., Ltd.

- Oriental Semiconductor

- Jilin Sino-Microelectronics Co., Ltd.

- PN Junction Semiconductor (Hangzhou) Co., Ltd.

- United Nova Technology Co., Ltd.

Key Developments in Silicon Carbide Power Chip Industry

- 2019: Wolfspeed announces its 200mm SiC wafer production facility, significantly increasing capacity and driving down costs.

- 2020: Infineon Technologies acquires Cypress Semiconductor, bolstering its automotive and industrial power solutions portfolio, including SiC.

- 2021: STMicroelectronics launches a new generation of SiC MOSFETs with improved performance and reliability for automotive applications.

- 2021: Rohm Semiconductor expands its SiC device offerings for EV powertrains and industrial applications.

- 2022: ON Semiconductor completes the acquisition of Silex Microsystems, enhancing its SiC fabrication capabilities.

- 2022: Navitas Semiconductor’s GeneSiC technology gains significant traction in EV charging and industrial power systems.

- 2023: BYD Semiconductor ramps up production of its SiC power modules, catering to its massive in-house EV production needs.

- 2023: Qorvo expands its SiC portfolio with the acquisition of UnitedSiC, strengthening its presence in high-performance power solutions.

- 2024: Several manufacturers announce advancements in SiC module packaging, enabling higher power density and thermal performance.

- 2024: Emerging players like CISSOID introduce ultra-high temperature SiC power modules for demanding applications.

Strategic Silicon Carbide Power Chip Market Forecast

The strategic Silicon Carbide (SiC) power chip market forecast indicates sustained robust growth, driven by the ongoing global transition towards electrification and energy efficiency. The market is projected to witness continued expansion fueled by increasing adoption in the automotive sector, particularly for electric vehicles and charging infrastructure, alongside significant penetration in industrial motor drives, renewable energy systems, and data centers. Technological innovations leading to enhanced performance, reduced costs, and improved reliability will further accelerate market penetration. Emerging opportunities in areas like HVDC transmission and advanced industrial automation are expected to contribute significantly to future growth. The forecast predicts a market size reaching tens of billions of dollars by 2033, with a compelling CAGR of over 20%, underscoring the transformative potential of SiC in the global power electronics landscape.

Silicon Carbide Power Chip Segmentation

-

1. Application

- 1.1. Automotive & EV/HEV

- 1.2. EV Charging

- 1.3. Industrial Motor/Drive

- 1.4. PV, Energy Storage, Wind Power

- 1.5. UPS, Data Center & Server

- 1.6. Rail Transport

- 1.7. Others

-

2. Type

- 2.1. SiC MOSFET Modules

- 2.2. SiC MOSFET Discretes

- 2.3. SiC Diode/SBD

Silicon Carbide Power Chip Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Silicon Carbide Power Chip Regional Market Share

Geographic Coverage of Silicon Carbide Power Chip

Silicon Carbide Power Chip REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 25.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Automotive & EV/HEV

- 5.1.2. EV Charging

- 5.1.3. Industrial Motor/Drive

- 5.1.4. PV, Energy Storage, Wind Power

- 5.1.5. UPS, Data Center & Server

- 5.1.6. Rail Transport

- 5.1.7. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. SiC MOSFET Modules

- 5.2.2. SiC MOSFET Discretes

- 5.2.3. SiC Diode/SBD

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Silicon Carbide Power Chip Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Automotive & EV/HEV

- 6.1.2. EV Charging

- 6.1.3. Industrial Motor/Drive

- 6.1.4. PV, Energy Storage, Wind Power

- 6.1.5. UPS, Data Center & Server

- 6.1.6. Rail Transport

- 6.1.7. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. SiC MOSFET Modules

- 6.2.2. SiC MOSFET Discretes

- 6.2.3. SiC Diode/SBD

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Silicon Carbide Power Chip Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Automotive & EV/HEV

- 7.1.2. EV Charging

- 7.1.3. Industrial Motor/Drive

- 7.1.4. PV, Energy Storage, Wind Power

- 7.1.5. UPS, Data Center & Server

- 7.1.6. Rail Transport

- 7.1.7. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. SiC MOSFET Modules

- 7.2.2. SiC MOSFET Discretes

- 7.2.3. SiC Diode/SBD

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Silicon Carbide Power Chip Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Automotive & EV/HEV

- 8.1.2. EV Charging

- 8.1.3. Industrial Motor/Drive

- 8.1.4. PV, Energy Storage, Wind Power

- 8.1.5. UPS, Data Center & Server

- 8.1.6. Rail Transport

- 8.1.7. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. SiC MOSFET Modules

- 8.2.2. SiC MOSFET Discretes

- 8.2.3. SiC Diode/SBD

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Silicon Carbide Power Chip Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Automotive & EV/HEV

- 9.1.2. EV Charging

- 9.1.3. Industrial Motor/Drive

- 9.1.4. PV, Energy Storage, Wind Power

- 9.1.5. UPS, Data Center & Server

- 9.1.6. Rail Transport

- 9.1.7. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. SiC MOSFET Modules

- 9.2.2. SiC MOSFET Discretes

- 9.2.3. SiC Diode/SBD

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Silicon Carbide Power Chip Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Automotive & EV/HEV

- 10.1.2. EV Charging

- 10.1.3. Industrial Motor/Drive

- 10.1.4. PV, Energy Storage, Wind Power

- 10.1.5. UPS, Data Center & Server

- 10.1.6. Rail Transport

- 10.1.7. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. SiC MOSFET Modules

- 10.2.2. SiC MOSFET Discretes

- 10.2.3. SiC Diode/SBD

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Silicon Carbide Power Chip Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Automotive & EV/HEV

- 11.1.2. EV Charging

- 11.1.3. Industrial Motor/Drive

- 11.1.4. PV, Energy Storage, Wind Power

- 11.1.5. UPS, Data Center & Server

- 11.1.6. Rail Transport

- 11.1.7. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. SiC MOSFET Modules

- 11.2.2. SiC MOSFET Discretes

- 11.2.3. SiC Diode/SBD

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 STMicroelectronics

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Infineon

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Wolfspeed

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Rohm

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 onsemi

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 BYD Semiconductor

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Microchip (Microsemi)

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Mitsubishi Electric (Vincotech)

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Semikron Danfoss

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Fuji Electric

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Navitas (GeneSiC)

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Toshiba

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Qorvo (UnitedSiC)

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 San'an Optoelectronics

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Littelfuse (IXYS)

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 CETC 55

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 WeEn Semiconductors

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 BASiC Semiconductor

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 SemiQ

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.20 Diodes Incorporated

- 12.1.20.1. Company Overview

- 12.1.20.2. Products

- 12.1.20.3. Company Financials

- 12.1.20.4. SWOT Analysis

- 12.1.21 SanRex

- 12.1.21.1. Company Overview

- 12.1.21.2. Products

- 12.1.21.3. Company Financials

- 12.1.21.4. SWOT Analysis

- 12.1.22 Alpha & Omega Semiconductor

- 12.1.22.1. Company Overview

- 12.1.22.2. Products

- 12.1.22.3. Company Financials

- 12.1.22.4. SWOT Analysis

- 12.1.23 Bosch

- 12.1.23.1. Company Overview

- 12.1.23.2. Products

- 12.1.23.3. Company Financials

- 12.1.23.4. SWOT Analysis

- 12.1.24 KEC Corporation

- 12.1.24.1. Company Overview

- 12.1.24.2. Products

- 12.1.24.3. Company Financials

- 12.1.24.4. SWOT Analysis

- 12.1.25 PANJIT Group

- 12.1.25.1. Company Overview

- 12.1.25.2. Products

- 12.1.25.3. Company Financials

- 12.1.25.4. SWOT Analysis

- 12.1.26 Nexperia

- 12.1.26.1. Company Overview

- 12.1.26.2. Products

- 12.1.26.3. Company Financials

- 12.1.26.4. SWOT Analysis

- 12.1.27 Vishay Intertechnology

- 12.1.27.1. Company Overview

- 12.1.27.2. Products

- 12.1.27.3. Company Financials

- 12.1.27.4. SWOT Analysis

- 12.1.28 Zhuzhou CRRC Times Electric

- 12.1.28.1. Company Overview

- 12.1.28.2. Products

- 12.1.28.3. Company Financials

- 12.1.28.4. SWOT Analysis

- 12.1.29 China Resources Microelectronics Limited

- 12.1.29.1. Company Overview

- 12.1.29.2. Products

- 12.1.29.3. Company Financials

- 12.1.29.4. SWOT Analysis

- 12.1.30 StarPower

- 12.1.30.1. Company Overview

- 12.1.30.2. Products

- 12.1.30.3. Company Financials

- 12.1.30.4. SWOT Analysis

- 12.1.31 Yangzhou Yangjie Electronic Technology

- 12.1.31.1. Company Overview

- 12.1.31.2. Products

- 12.1.31.3. Company Financials

- 12.1.31.4. SWOT Analysis

- 12.1.32 Guangdong AccoPower Semiconductor

- 12.1.32.1. Company Overview

- 12.1.32.2. Products

- 12.1.32.3. Company Financials

- 12.1.32.4. SWOT Analysis

- 12.1.33 Changzhou Galaxy Century Microelectronics

- 12.1.33.1. Company Overview

- 12.1.33.2. Products

- 12.1.33.3. Company Financials

- 12.1.33.4. SWOT Analysis

- 12.1.34 Hangzhou Silan Microelectronics

- 12.1.34.1. Company Overview

- 12.1.34.2. Products

- 12.1.34.3. Company Financials

- 12.1.34.4. SWOT Analysis

- 12.1.35 Cissoid

- 12.1.35.1. Company Overview

- 12.1.35.2. Products

- 12.1.35.3. Company Financials

- 12.1.35.4. SWOT Analysis

- 12.1.36 SK powertech

- 12.1.36.1. Company Overview

- 12.1.36.2. Products

- 12.1.36.3. Company Financials

- 12.1.36.4. SWOT Analysis

- 12.1.37 InventChip Technology

- 12.1.37.1. Company Overview

- 12.1.37.2. Products

- 12.1.37.3. Company Financials

- 12.1.37.4. SWOT Analysis

- 12.1.38 Hebei Sinopack Electronic Technology

- 12.1.38.1. Company Overview

- 12.1.38.2. Products

- 12.1.38.3. Company Financials

- 12.1.38.4. SWOT Analysis

- 12.1.39 Oriental Semiconductor

- 12.1.39.1. Company Overview

- 12.1.39.2. Products

- 12.1.39.3. Company Financials

- 12.1.39.4. SWOT Analysis

- 12.1.40 Jilin Sino-Microelectronics

- 12.1.40.1. Company Overview

- 12.1.40.2. Products

- 12.1.40.3. Company Financials

- 12.1.40.4. SWOT Analysis

- 12.1.41 PN Junction Semiconductor (Hangzhou)

- 12.1.41.1. Company Overview

- 12.1.41.2. Products

- 12.1.41.3. Company Financials

- 12.1.41.4. SWOT Analysis

- 12.1.42 United Nova Technology

- 12.1.42.1. Company Overview

- 12.1.42.2. Products

- 12.1.42.3. Company Financials

- 12.1.42.4. SWOT Analysis

- 12.1.1 STMicroelectronics

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Silicon Carbide Power Chip Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Silicon Carbide Power Chip Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Silicon Carbide Power Chip Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Silicon Carbide Power Chip Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Silicon Carbide Power Chip Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Silicon Carbide Power Chip Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Silicon Carbide Power Chip Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Silicon Carbide Power Chip Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Silicon Carbide Power Chip Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Silicon Carbide Power Chip Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Silicon Carbide Power Chip Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Silicon Carbide Power Chip Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Silicon Carbide Power Chip Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Silicon Carbide Power Chip Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Silicon Carbide Power Chip Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Silicon Carbide Power Chip Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Silicon Carbide Power Chip Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Silicon Carbide Power Chip Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Silicon Carbide Power Chip Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Silicon Carbide Power Chip Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Silicon Carbide Power Chip Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Silicon Carbide Power Chip Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Silicon Carbide Power Chip Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Silicon Carbide Power Chip Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Silicon Carbide Power Chip Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Silicon Carbide Power Chip Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Silicon Carbide Power Chip Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Silicon Carbide Power Chip Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Silicon Carbide Power Chip Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Silicon Carbide Power Chip Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Silicon Carbide Power Chip Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Silicon Carbide Power Chip Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Silicon Carbide Power Chip Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Silicon Carbide Power Chip Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Silicon Carbide Power Chip Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Silicon Carbide Power Chip Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Silicon Carbide Power Chip Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Silicon Carbide Power Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Silicon Carbide Power Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Silicon Carbide Power Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Silicon Carbide Power Chip Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Silicon Carbide Power Chip Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Silicon Carbide Power Chip Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Silicon Carbide Power Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Silicon Carbide Power Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Silicon Carbide Power Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Silicon Carbide Power Chip Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Silicon Carbide Power Chip Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Silicon Carbide Power Chip Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Silicon Carbide Power Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Silicon Carbide Power Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Silicon Carbide Power Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Silicon Carbide Power Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Silicon Carbide Power Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Silicon Carbide Power Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Silicon Carbide Power Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Silicon Carbide Power Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Silicon Carbide Power Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Silicon Carbide Power Chip Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Silicon Carbide Power Chip Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Silicon Carbide Power Chip Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Silicon Carbide Power Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Silicon Carbide Power Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Silicon Carbide Power Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Silicon Carbide Power Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Silicon Carbide Power Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Silicon Carbide Power Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Silicon Carbide Power Chip Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Silicon Carbide Power Chip Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Silicon Carbide Power Chip Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Silicon Carbide Power Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Silicon Carbide Power Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Silicon Carbide Power Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Silicon Carbide Power Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Silicon Carbide Power Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Silicon Carbide Power Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Silicon Carbide Power Chip Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Silicon Carbide Power Chip?

The projected CAGR is approximately 25.7%.

2. Which companies are prominent players in the Silicon Carbide Power Chip?

Key companies in the market include STMicroelectronics, Infineon, Wolfspeed, Rohm, onsemi, BYD Semiconductor, Microchip (Microsemi), Mitsubishi Electric (Vincotech), Semikron Danfoss, Fuji Electric, Navitas (GeneSiC), Toshiba, Qorvo (UnitedSiC), San'an Optoelectronics, Littelfuse (IXYS), CETC 55, WeEn Semiconductors, BASiC Semiconductor, SemiQ, Diodes Incorporated, SanRex, Alpha & Omega Semiconductor, Bosch, KEC Corporation, PANJIT Group, Nexperia, Vishay Intertechnology, Zhuzhou CRRC Times Electric, China Resources Microelectronics Limited, StarPower, Yangzhou Yangjie Electronic Technology, Guangdong AccoPower Semiconductor, Changzhou Galaxy Century Microelectronics, Hangzhou Silan Microelectronics, Cissoid, SK powertech, InventChip Technology, Hebei Sinopack Electronic Technology, Oriental Semiconductor, Jilin Sino-Microelectronics, PN Junction Semiconductor (Hangzhou), United Nova Technology.

3. What are the main segments of the Silicon Carbide Power Chip?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.83 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Silicon Carbide Power Chip," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Silicon Carbide Power Chip report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Silicon Carbide Power Chip?

To stay informed about further developments, trends, and reports in the Silicon Carbide Power Chip, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence