Key Insights

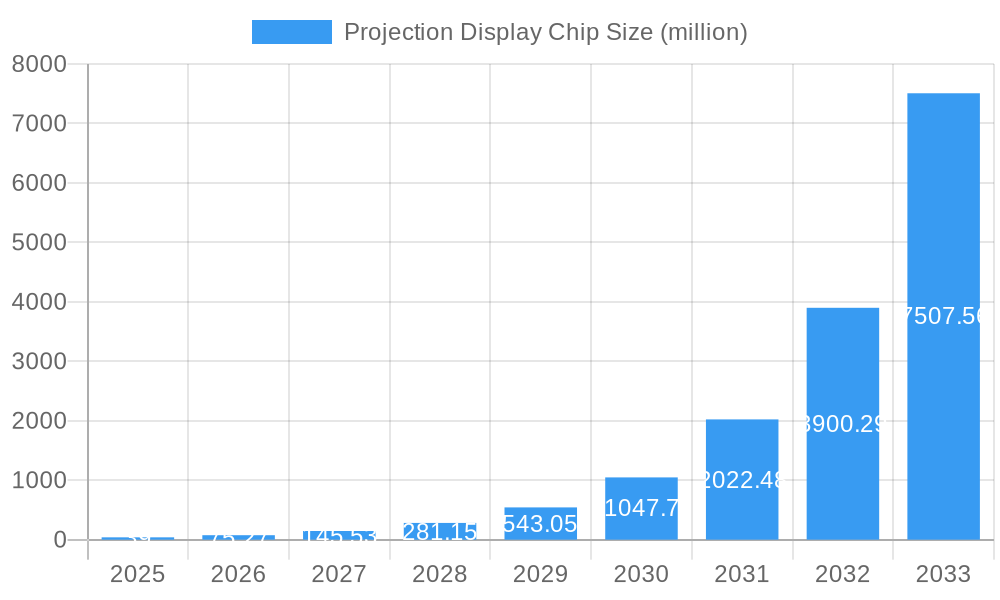

The global Projection Display Chip market is poised for substantial expansion, projected to reach an estimated USD 39 million in 2025, fueled by a remarkable Compound Annual Growth Rate (CAGR) of 93% during the forecast period of 2025-2033. This explosive growth is primarily driven by the increasing demand for innovative display solutions across various sectors. Key applications such as mobile monitors and micro-projection technologies are leading this surge, offering portable and versatile display experiences. The automotive industry is also a significant contributor, integrating advanced projection systems for heads-up displays (HUDs) and infotainment, enhancing driver safety and passenger engagement. Emerging trends like the miniaturization of projection modules and advancements in imaging technologies, particularly CMOS and DMD chips, are further propelling market adoption. These technological leaps are enabling more compact, energy-efficient, and higher-resolution projection devices, making them attractive alternatives to traditional displays.

Projection Display Chip Market Size (In Million)

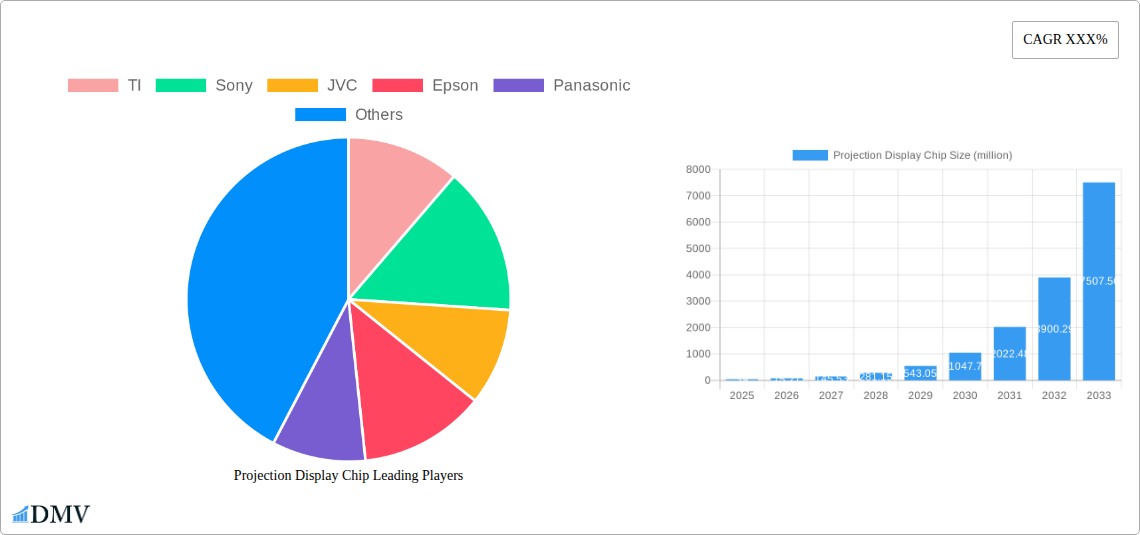

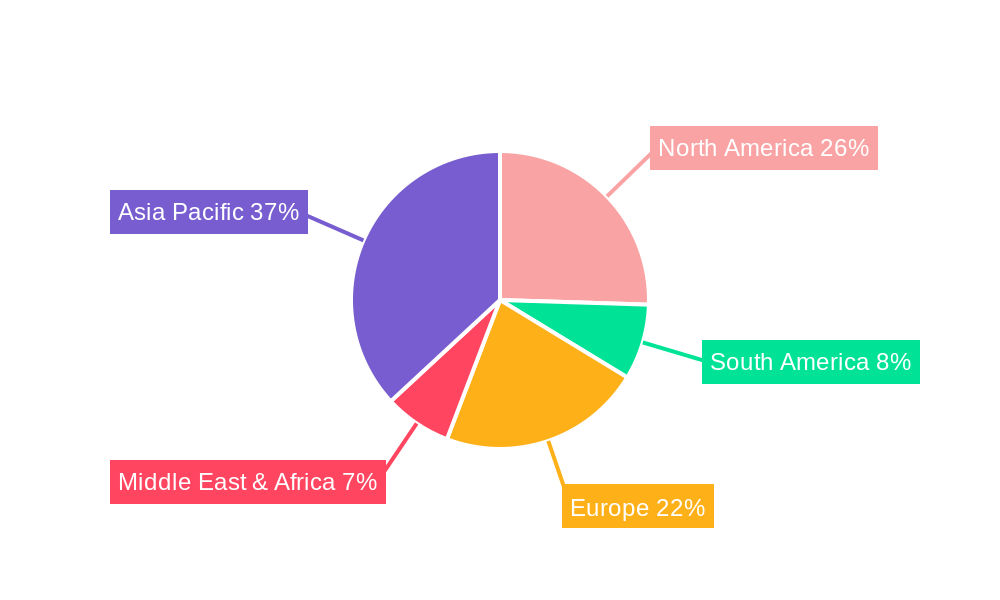

Despite the robust growth trajectory, certain restraints could influence the market's pace. High initial development costs for cutting-edge projection technology and the ongoing competition from established display alternatives like OLED and LCD screens present challenges. However, the unique advantages of projection displays, such as larger screen sizes from smaller devices and improved immersive experiences, are expected to outweigh these limitations. Geographically, Asia Pacific is anticipated to dominate the market due to the strong manufacturing base and rapid adoption of new technologies in countries like China and South Korea. North America and Europe will also witness significant growth, driven by consumer electronics innovation and the increasing integration of projection displays in automotive and enterprise solutions. The competitive landscape is characterized by established players like Texas Instruments, Sony, and Epson, alongside emerging Chinese manufacturers, all vying for market share through continuous product development and strategic collaborations.

Projection Display Chip Company Market Share

Here's the SEO-optimized report description for the Projection Display Chip market, incorporating your specified details and keywords.

Report Title: Global Projection Display Chip Market: Comprehensive Analysis and Future Forecast (2019–2033)

Report Description:

Unlock critical insights into the dynamic global Projection Display Chip market with this in-depth, data-rich report. Spanning 2019 to 2033, this study provides an indispensable resource for stakeholders seeking to navigate the evolving landscape of micro-display technologies. We meticulously analyze market composition, industry evolution, leading regional players, and groundbreaking product innovations. Understand the intricate interplay of CMOS chips and DMD chips, and their pivotal roles in emerging applications like Mobile Monitors, Micro Projection, and the rapidly expanding Automobile Industry. This report offers a granular view of market concentration, innovation catalysts, and the competitive strategies of industry giants such as Texas Instruments (TI), Sony, JVC, Epson, Panasonic, Omnivision Group, Will Semiconductor, Shenzhen Kechuang Digital Display Technology, and Shanghai Huixinchen Industrial. With a base year of 2025 and a comprehensive forecast period extending to 2033, this analysis is your definitive guide to strategic decision-making in the projection display chip sector.

Projection Display Chip Market Composition & Trends

The projection display chip market is characterized by a moderately concentrated landscape, driven by continuous innovation in miniaturization and power efficiency. Key innovation catalysts include the demand for brighter, more compact projection solutions across consumer electronics, automotive displays, and immersive entertainment. The regulatory landscape primarily focuses on safety standards for display technologies and energy efficiency mandates, influencing product design and component selection. Substitute products, while present in some niche applications, have yet to significantly disrupt the core market, primarily due to the unique advantages of projection in terms of screen size and flexibility. End-user profiles are increasingly diverse, ranging from individual consumers seeking portable entertainment solutions to automotive manufacturers integrating advanced heads-up displays (HUDs) and industrial sectors requiring precise visualization. Mergers and acquisitions (M&A) activities are strategic, aimed at consolidating intellectual property, expanding technological capabilities, and securing market share in high-growth segments. For instance, past M&A deals have often involved larger semiconductor companies acquiring specialized micro-display technology firms, bolstering their portfolios in areas like DMD chips and advanced CMOS chips. The overall market share distribution sees a dynamic interplay between established players and emerging innovators, with significant investment flowing into research and development for next-generation projection solutions. The projected M&A deal value in this segment is anticipated to reach approximately $XX million over the forecast period, reflecting the strategic importance of this technology.

Projection Display Chip Industry Evolution

The projection display chip industry has witnessed a remarkable evolution, driven by relentless technological advancements and shifting consumer demands, charting a growth trajectory from its nascent stages to its current significant market position. During the historical period (2019-2024), the market saw steady growth, fueled by the increasing adoption of projection technology in niche applications and the continuous improvement in chip performance. Key technological advancements during this phase included the refinement of CMOS chips for enhanced resolution and power efficiency, and the optimization of DMD chips for superior brightness and contrast ratios. This period also saw the burgeoning interest in Micro Projection devices, which began to find their way into smartphones, pico projectors, and wearable devices, indicating a significant shift in consumer demand towards portable and integrated display solutions. The base year, 2025, marks a pivotal point, with the industry poised for accelerated growth, particularly as the Automobile Industry increasingly integrates advanced projection systems for infotainment and driver assistance.

The forecast period (2025–2033) is projected to experience a compound annual growth rate (CAGR) of approximately XX%, a testament to the sustained innovation and expanding application base. The growth rate is further bolstered by advancements in laser projection technology, which offers greater longevity and energy efficiency, and the development of more sophisticated optical engines. Consumer demand is expected to pivot towards higher resolutions (4K and beyond), greater color accuracy, and more immersive viewing experiences, pushing manufacturers to develop more powerful and versatile projection display chips. The adoption of projection display chips in the Mobile Monitor segment is anticipated to surge, driven by the growing trend of remote work and the need for larger, portable displays. Furthermore, the integration of projection capabilities into augmented reality (AR) and virtual reality (VR) headsets, though still in its early stages, represents a significant future growth avenue, projecting a substantial increase in the adoption of advanced CMOS chips and specialized display technologies. The overall evolution of the industry is thus characterized by a continuous cycle of technological improvement, expanding market applications, and an ever-increasing demand for higher performance and more integrated projection solutions.

Leading Regions, Countries, or Segments in Projection Display Chip

The global Projection Display Chip market exhibits distinct regional dominance and segment leadership, driven by a confluence of technological innovation, robust industrial demand, and strategic government initiatives. In terms of application, the Automobile Industry is emerging as a primary growth driver, with an increasing demand for advanced heads-up displays (HUDs), in-car infotainment systems, and driver monitoring systems leveraging projection display chip technology. This segment's dominance is fueled by significant investments in automotive electronics and the pursuit of enhanced driver safety and passenger experience. Furthermore, the Micro Projection segment continues to show strong potential, propelled by the miniaturization trend in consumer electronics, leading to the integration of projection capabilities into a wider array of devices such as portable projectors, smart home devices, and even smart wearables.

Regionally, Asia-Pacific stands out as the leading market for projection display chips. This leadership is attributed to several key factors:

- Manufacturing Hub: The region is a global epicenter for electronics manufacturing, housing key players like Will Semiconductor, Shenzhen Kechuang Digital Display Technology, and Shanghai Huixinchen Industrial, ensuring robust supply chains and competitive pricing.

- Growing Consumer Market: Rapid urbanization and a burgeoning middle class in countries like China and India create a substantial consumer base for devices incorporating projection technology, including smartphones with integrated projectors and compact home entertainment systems.

- Government Support: Supportive government policies and significant investments in research and development for advanced semiconductor technologies across various Asian nations further bolster market growth.

- Technological Adoption: The region demonstrates a high propensity for adopting new technologies, evident in the rapid uptake of projection display chips in emerging applications.

Within the Type segment, both CMOS Chips and DMD Chips hold significant market share, with their respective strengths catering to different application needs. CMOS Chips are gaining traction due to their cost-effectiveness, lower power consumption, and suitability for high-volume applications like mobile projectors and compact displays. Conversely, DMD Chips, particularly those developed by industry leaders like Texas Instruments, continue to dominate high-performance applications requiring superior brightness, contrast, and resolution, such as professional projectors and advanced automotive displays. Investment trends within these segments show a balanced allocation, with continued R&D focused on improving the performance and efficiency of both technologies. Regulatory support, particularly concerning energy efficiency standards and product safety, is also a key driver shaping the adoption and development of these chip types across different regions.

Projection Display Chip Product Innovations

Product innovations in the projection display chip market are relentlessly pushing the boundaries of miniaturization, brightness, and energy efficiency. Manufacturers are developing advanced CMOS chips with higher pixel densities and improved light-emitting diode (LED) or laser compatibility, enabling smaller and more power-efficient pico projectors for mobile devices and wearables. Simultaneously, advancements in DMD chips are focusing on enhanced durability, wider operating temperature ranges for automotive applications, and higher resolutions to deliver stunning visual experiences. For example, next-generation chips are boasting an impressive luminance output exceeding XX lumens and achieving color gamuts that surpass XX% of the DCI-P3 standard, making them ideal for high-fidelity Micro Projection systems and immersive automotive displays. The unique selling proposition lies in the ability to project large, vibrant images from incredibly compact form factors, revolutionizing how we interact with visual information across various industries.

Propelling Factors for Projection Display Chip Growth

The projection display chip market is propelled by several interconnected factors. Technological advancements are paramount, with continuous improvements in CMOS chips and DMD chips leading to higher resolutions, enhanced brightness, and greater energy efficiency. The expanding applications in the Automobile Industry, particularly for heads-up displays (HUDs) and augmented reality interfaces, represent a significant growth avenue. Furthermore, the growing demand for portable and large-screen viewing experiences in consumer electronics, such as Mobile Monitors and pico projectors, is a major catalyst. Economic factors, including declining manufacturing costs and increasing disposable incomes in emerging markets, also contribute to market expansion. Regulatory support, such as mandates for energy-efficient display technologies, further encourages the adoption of advanced projection solutions.

Obstacles in the Projection Display Chip Market

Despite robust growth, the projection display chip market faces several obstacles. Supply chain disruptions, as evidenced by recent global semiconductor shortages, can impact production and lead to increased component costs, potentially hindering market expansion. Intense competition from alternative display technologies, such as advanced OLED and Mini-LED screens, poses a challenge, especially in segments where cost and form factor are less critical. Regulatory hurdles related to heat dissipation and safety standards in highly integrated devices can also slow down product development and market penetration. Furthermore, the high initial investment required for research and development of cutting-edge projection technologies can be a barrier for smaller companies. The projected impact of these obstacles on market growth is estimated to be around XX% reduction in projected revenue over the forecast period if not adequately addressed.

Future Opportunities in Projection Display Chip

The projection display chip market is ripe with future opportunities. The burgeoning demand for immersive experiences in the Automobile Industry for augmented reality windshield displays presents a substantial growth area for advanced DMD chips and specialized CMOS chips. The continued miniaturization trend in consumer electronics will drive further innovation in Micro Projection technology, enabling integration into an even wider array of portable devices. The development of more energy-efficient and higher-resolution chips will unlock new applications in areas like interactive whiteboards for education and portable medical imaging devices. Emerging markets, with their increasing disposable incomes and adoption of new technologies, offer significant untapped potential for a wide range of projection display chip-enabled products.

Major Players in the Projection Display Chip Ecosystem

- Texas Instruments

- Sony

- JVC

- Epson

- Panasonic

- Omnivision Group

- Will Semiconductor

- Shenzhen Kechuang Digital Display Technology

- Shanghai Huixinchen Industrial

Key Developments in Projection Display Chip Industry

- 2023: Launch of new high-brightness CMOS chips enabling ultra-compact pico projectors with enhanced power efficiency.

- 2023: Introduction of automotive-grade DMD chips with extended temperature ranges for advanced HUD applications.

- 2024: Strategic partnership formed between a leading automotive manufacturer and a projection display chip supplier to co-develop next-generation in-car projection systems.

- 2024: Significant advancements announced in laser projection technology, promising longer lifespan and improved color accuracy for future Micro Projection devices.

- 2024: Increased investment by major players in R&D for higher resolution CMOS chips targeting the burgeoning Mobile Monitor market.

Strategic Projection Display Chip Market Forecast

The strategic forecast for the projection display chip market is exceptionally positive, driven by sustained innovation and expanding application horizons. Growth catalysts include the escalating integration of projection technology within the Automobile Industry, the persistent consumer demand for portable and large-screen Mobile Monitors, and the continuous evolution of Micro Projection solutions. The market's trajectory is further shaped by ongoing advancements in both CMOS chips and DMD chips, promising enhanced performance, reduced power consumption, and greater miniaturization. Emerging economies represent a significant opportunity for market penetration, while the development of novel applications in areas like AR/VR and intelligent signage will fuel long-term growth. The market potential is substantial, poised for continued expansion and technological leadership in the display sector.

Projection Display Chip Segmentation

-

1. Application

- 1.1. Mobile Monitor

- 1.2. Micro Projection

- 1.3. Automobile Industry

- 1.4. Others

-

2. Type

- 2.1. CMOS Chips

- 2.2. DMD Chips

Projection Display Chip Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Projection Display Chip Regional Market Share

Geographic Coverage of Projection Display Chip

Projection Display Chip REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Mobile Monitor

- 5.1.2. Micro Projection

- 5.1.3. Automobile Industry

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. CMOS Chips

- 5.2.2. DMD Chips

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Projection Display Chip Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Mobile Monitor

- 6.1.2. Micro Projection

- 6.1.3. Automobile Industry

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. CMOS Chips

- 6.2.2. DMD Chips

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Projection Display Chip Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Mobile Monitor

- 7.1.2. Micro Projection

- 7.1.3. Automobile Industry

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. CMOS Chips

- 7.2.2. DMD Chips

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Projection Display Chip Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Mobile Monitor

- 8.1.2. Micro Projection

- 8.1.3. Automobile Industry

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. CMOS Chips

- 8.2.2. DMD Chips

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Projection Display Chip Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Mobile Monitor

- 9.1.2. Micro Projection

- 9.1.3. Automobile Industry

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. CMOS Chips

- 9.2.2. DMD Chips

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Projection Display Chip Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Mobile Monitor

- 10.1.2. Micro Projection

- 10.1.3. Automobile Industry

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. CMOS Chips

- 10.2.2. DMD Chips

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Projection Display Chip Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Mobile Monitor

- 11.1.2. Micro Projection

- 11.1.3. Automobile Industry

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. CMOS Chips

- 11.2.2. DMD Chips

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 TI

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Sony

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 JVC

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Epson

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Panasonic

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Omnivision Group

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Will Semiconductor

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Shenzhen Kechuang Digital Display Technology

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Shanghai Huixinchen Industrial

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.1 TI

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Projection Display Chip Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Projection Display Chip Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Projection Display Chip Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Projection Display Chip Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Projection Display Chip Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Projection Display Chip Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Projection Display Chip Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Projection Display Chip Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Projection Display Chip Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Projection Display Chip Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Projection Display Chip Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Projection Display Chip Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Projection Display Chip Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Projection Display Chip Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Projection Display Chip Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Projection Display Chip Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Projection Display Chip Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Projection Display Chip Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Projection Display Chip Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Projection Display Chip Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Projection Display Chip Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Projection Display Chip Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Projection Display Chip Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Projection Display Chip Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Projection Display Chip Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Projection Display Chip Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Projection Display Chip Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Projection Display Chip Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Projection Display Chip Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Projection Display Chip Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Projection Display Chip Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Projection Display Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Projection Display Chip Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Projection Display Chip Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Projection Display Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Projection Display Chip Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Projection Display Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Projection Display Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Projection Display Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Projection Display Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Projection Display Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Projection Display Chip Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Projection Display Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Projection Display Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Projection Display Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Projection Display Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Projection Display Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Projection Display Chip Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Projection Display Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Projection Display Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Projection Display Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Projection Display Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Projection Display Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Projection Display Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Projection Display Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Projection Display Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Projection Display Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Projection Display Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Projection Display Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Projection Display Chip Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Projection Display Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Projection Display Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Projection Display Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Projection Display Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Projection Display Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Projection Display Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Projection Display Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Projection Display Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Projection Display Chip Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Projection Display Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Projection Display Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Projection Display Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Projection Display Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Projection Display Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Projection Display Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Projection Display Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Projection Display Chip Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Projection Display Chip?

The projected CAGR is approximately 5.1%.

2. Which companies are prominent players in the Projection Display Chip?

Key companies in the market include TI, Sony, JVC, Epson, Panasonic, Omnivision Group, Will Semiconductor, Shenzhen Kechuang Digital Display Technology, Shanghai Huixinchen Industrial.

3. What are the main segments of the Projection Display Chip?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Projection Display Chip," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Projection Display Chip report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Projection Display Chip?

To stay informed about further developments, trends, and reports in the Projection Display Chip, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence