Key Insights

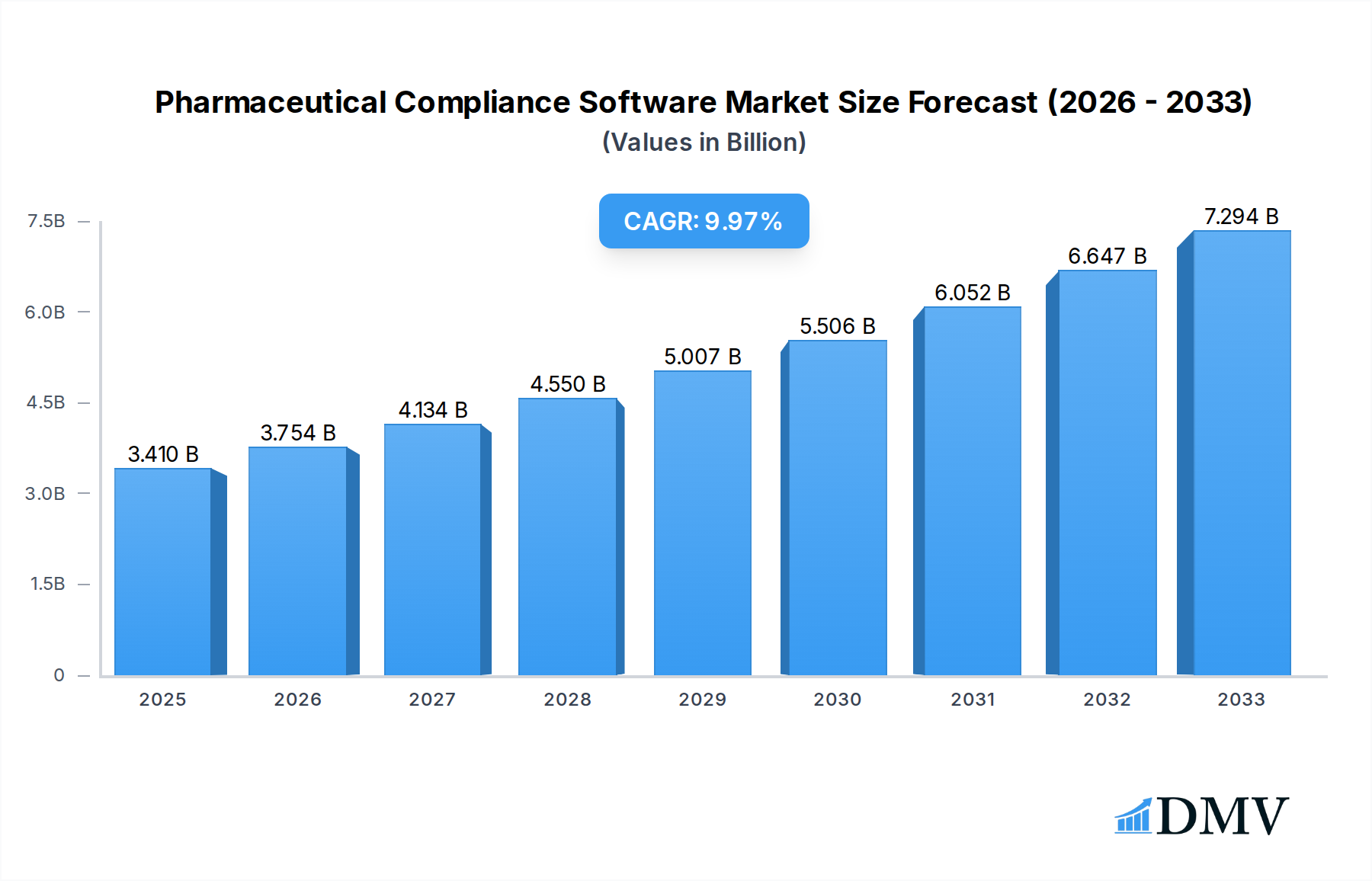

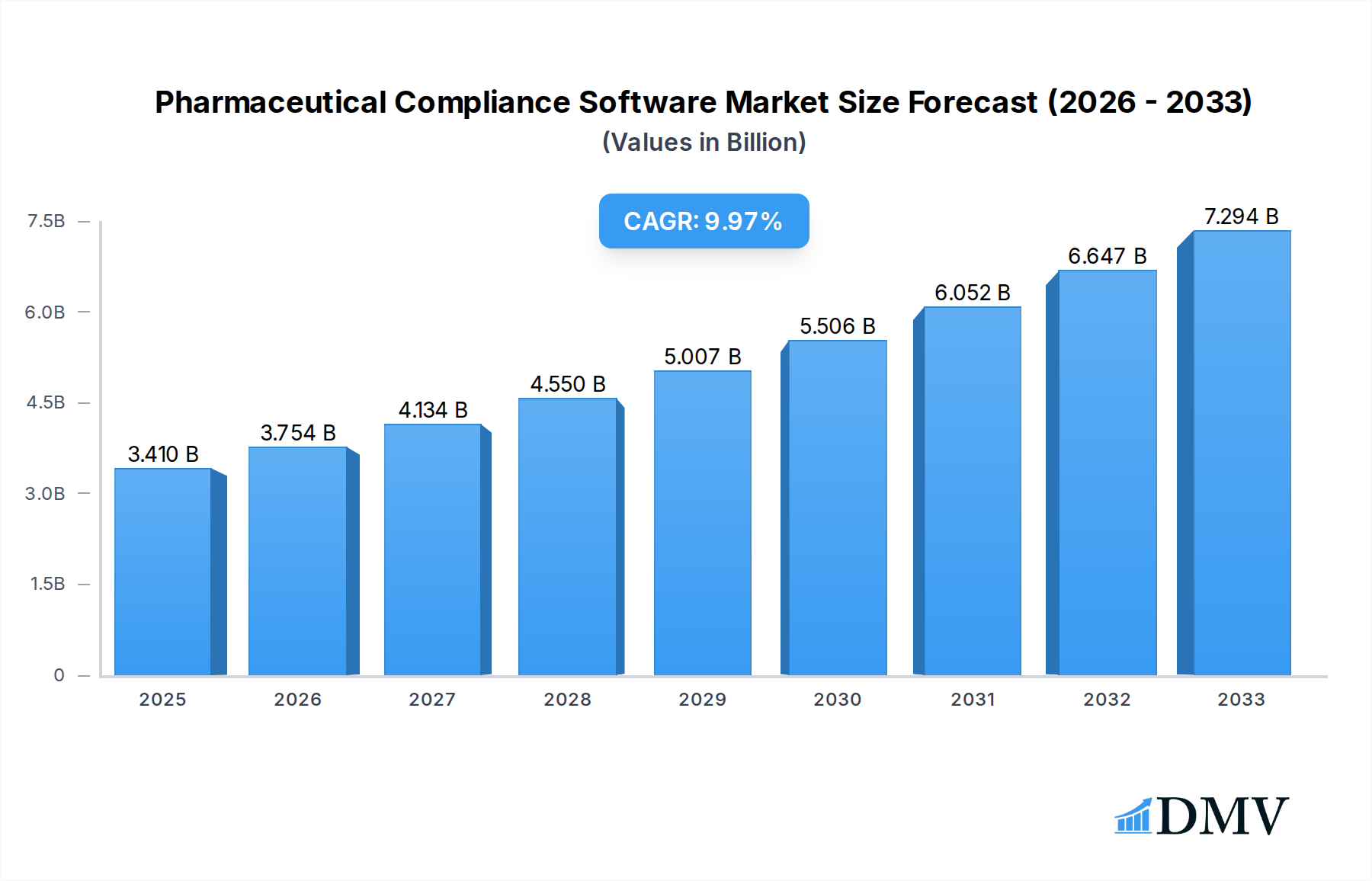

The global Pharmaceutical Compliance Software market is poised for robust expansion, reflecting the increasing stringency of regulatory environments and the pharmaceutical industry's digital transformation imperatives. Valued at 3.41 billion in 2025, the market is projected to grow significantly with a compelling CAGR of 10.1% during the forecast period of 2025-2033. This impressive growth is primarily fueled by a confluence of critical drivers, including the escalating complexity of global pharmaceutical regulations from bodies like the FDA, EMA, and other national health authorities, which necessitates sophisticated solutions for meticulous adherence. Furthermore, the imperative for enhanced data integrity, product traceability, and risk management across the drug lifecycle, from research and development to manufacturing and post-market surveillance, significantly bolsters the demand for these specialized software tools. The industry's accelerating shift towards digital platforms and automation to improve operational efficiencies, reduce human error, and mitigate the substantial financial and reputational risks associated with non-compliance also plays a pivotal role in market expansion.

Pharmaceutical Compliance Software Market Size (In Billion)

Key trends shaping this dynamic market include the accelerating adoption of cloud-based pharmaceutical compliance software, which offers greater flexibility, scalability, and cost-effectiveness compared to traditional on-premise deployments. There's also a growing emphasis on integrating advanced analytics and artificial intelligence (AI) to enable predictive compliance, real-time monitoring, and proactive risk assessment, thereby enhancing decision-making capabilities. While the market's trajectory is overwhelmingly positive, certain challenges, such as the substantial initial investment required for implementation, complexities associated with integrating with existing legacy systems, and the need for specialized training to maximize software utility, pose potential hurdles. Nevertheless, the continuous innovation by leading companies like Ideagen, Wolters Kluwer, and Sparta Systems in developing comprehensive solutions covering Product Information Management (PIM) and Pharmaceutical Electronic Registration, alongside an expanding geographical footprint led by North America and Europe, is expected to overcome these challenges, ensuring sustained market growth and compliance excellence throughout the pharmaceutical sector.

Pharmaceutical Compliance Software Company Market Share

Pharmaceutical Compliance Software Market Composition & Trends

The Pharmaceutical Compliance Software market is currently experiencing a dynamic phase characterized by rapid innovation and strategic consolidation, valued at an estimated xx billion in 2025. While the landscape features a mix of established industry giants and agile specialized providers, market concentration is steadily increasing. The top three companies, including market leaders such as Wolters Kluwer and MasterControl, collectively command an estimated xx billion share of the market, driven by comprehensive offerings and strong brand recognition. Innovation catalysts are predominantly fueled by the pharmaceutical industry’s escalating demand for GxP compliance, data integrity, and efficient quality management systems, pushing software developers to integrate advanced analytics and automation. The regulatory landscape, including stringent FDA, EMA, and other global health authority guidelines, acts as a primary market driver, compelling pharmaceutical companies to adopt robust compliance solutions to mitigate risks and ensure product safety.

Substitute products, primarily manual processes, legacy systems, or generalized enterprise resource planning (ERP) modules with limited compliance functionalities, are rapidly losing ground as the industry demands specialized, real-time compliance capabilities. End-user profiles span pharmaceutical manufacturers, contract research organizations (CROs), and biotechnology firms, all seeking to streamline regulatory submissions, document management, and quality control. Mergers and acquisitions (M&A) activities have been robust, signaling a drive towards expanding solution portfolios and geographic reach. In 2024, the total M&A deal value in the sector reached an estimated xx billion, with notable acquisitions aimed at integrating AI-driven compliance tools and broadening cloud-based offerings. These strategic moves by players like Ideagen and Sparta Systems aim to create more integrated, end-to-end compliance ecosystems, positioning them for sustained growth within a market projected to reach xx billion by 2033. The competitive intensity is moderate, with a clear trend towards differentiation through specialized modules and superior user experience, addressing the evolving needs of a highly regulated industry.

Pharmaceutical Compliance Software Industry Evolution

The Pharmaceutical Compliance Software industry has undergone a remarkable evolution, transitioning from rudimentary document management systems to sophisticated, AI-driven platforms that are indispensable for navigating the complex global regulatory environment. Beginning its historical period from 2019, the market was valued at an estimated xx billion, primarily driven by the foundational need for digital record-keeping and basic regulatory reporting. The subsequent years, through to 2024, witnessed a consistent growth trajectory, propelled by increasing regulatory stringency, particularly in data integrity (ALCOA+ principles) and electronic recordkeeping. This period saw a significant shift from localized, departmental solutions to more integrated enterprise-wide systems.

Technological advancements have been a cornerstone of this evolution. The advent of cloud computing dramatically reshaped deployment models, offering scalability, accessibility, and cost efficiencies that on-premise solutions struggled to match. This led to a substantial surge in cloud-based pharmaceutical compliance software adoption, transforming how companies managed their GxP processes. Furthermore, the integration of Artificial Intelligence (AI) and Machine Learning (ML) began to emerge, enabling predictive analytics for compliance risks, automated document review, and intelligent data analysis to identify potential deviations before they escalate. Blockchain technology also started to gain traction for enhancing supply chain traceability and ensuring data immutability, particularly relevant for drug serialization and anti-counterfeiting measures.

Shifting consumer demands within the pharmaceutical industry have further accelerated this evolution. There's a growing need for proactive compliance, not just reactive reporting. Pharmaceutical companies require solutions that can provide real-time insights, facilitate seamless collaboration across global teams, and adapt quickly to evolving regulations without extensive custom development. The COVID-19 pandemic, from 2020 onwards, underscored the critical importance of robust, agile digital compliance infrastructure, particularly for expedited drug development and global distribution, creating an unprecedented demand for advanced compliance tools. This intensified focus on speed-to-market while maintaining uncompromising quality and safety standards propelled the industry’s growth.

From the base year 2025, with an estimated market size of xx billion, the forecast period extending to 2033 anticipates a robust compound annual growth rate (CAGR) of xx%, reaching a projected xx billion. This growth will be significantly influenced by the continued digital transformation initiatives within pharma, the further maturation of AI/ML applications in compliance, and the increasing adoption of integrated platforms that combine quality management, risk management, and regulatory information management. Adoption metrics show that by 2024, an estimated xx% of large pharmaceutical companies had implemented cloud-based compliance solutions, a figure projected to climb to xx% by 2030, reflecting the undeniable shift towards more agile and scalable software architectures. The industry’s evolution is a testament to its critical role in safeguarding public health while enabling pharmaceutical innovation.

Leading Regions, Countries, or Segments in Pharmaceutical Compliance Software

The Pharmaceutical Compliance Software market exhibits distinct leadership across various segments and geographies, driven by a confluence of regulatory demands, technological adoption, and investment trends. Among the "Types" segments, Cloud-Based Pharmaceutical Compliance Software has unequivocally emerged as the dominant force, overshadowing its On-Premise counterpart. By the estimated year 2025, the cloud-based segment is projected to account for an estimated xx billion of the total market, growing at a robust CAGR of xx% during the forecast period of 2025-2033. This dominance is primarily due to its inherent advantages in scalability, reduced IT infrastructure costs, enhanced accessibility, and seamless updates, which are critical for global pharmaceutical operations requiring agile adaptation to regulatory changes.

Key drivers for the supremacy of Cloud-Based Pharmaceutical Compliance Software include:

- Investment Trends: Significant capital expenditure by major pharmaceutical players shifting towards SaaS models to minimize upfront infrastructure investments and leverage operational expenditures.

- Regulatory Support: Increasing acceptance and development of regulatory guidelines for cloud-based data storage and processing, providing clarity and confidence to adopters.

- Remote Work Enablement: The imperative for remote access and collaborative compliance management, particularly amplified by global events, has accelerated cloud adoption.

- Integration Capabilities: Superior ability of cloud platforms to integrate with other enterprise systems like ERP, QMS, and LIMS, creating a unified data ecosystem.

Within the "Application" segments, Product Information Management (PIM) is a leading category, representing a substantial portion of the market, with an estimated market value of xx billion in 2025. PIM software is crucial for managing the vast and complex data associated with pharmaceutical products, from R&D through to commercialization, ensuring accurate and compliant labeling, packaging, and global submissions. Its importance is underscored by the ever-increasing scrutiny on data integrity and product safety.

Drivers for PIM's prominence include:

- Global Harmonization Efforts: The drive towards global unique device identification (UDI) and product serialization mandates increased demand for robust PIM systems.

- Complex Product Portfolios: Pharmaceutical companies manage thousands of SKUs with region-specific variations, making PIM essential for accurate and controlled information dissemination.

- Risk Mitigation: Effective PIM reduces errors in product information, thereby minimizing the risk of product recalls, regulatory fines, and brand damage.

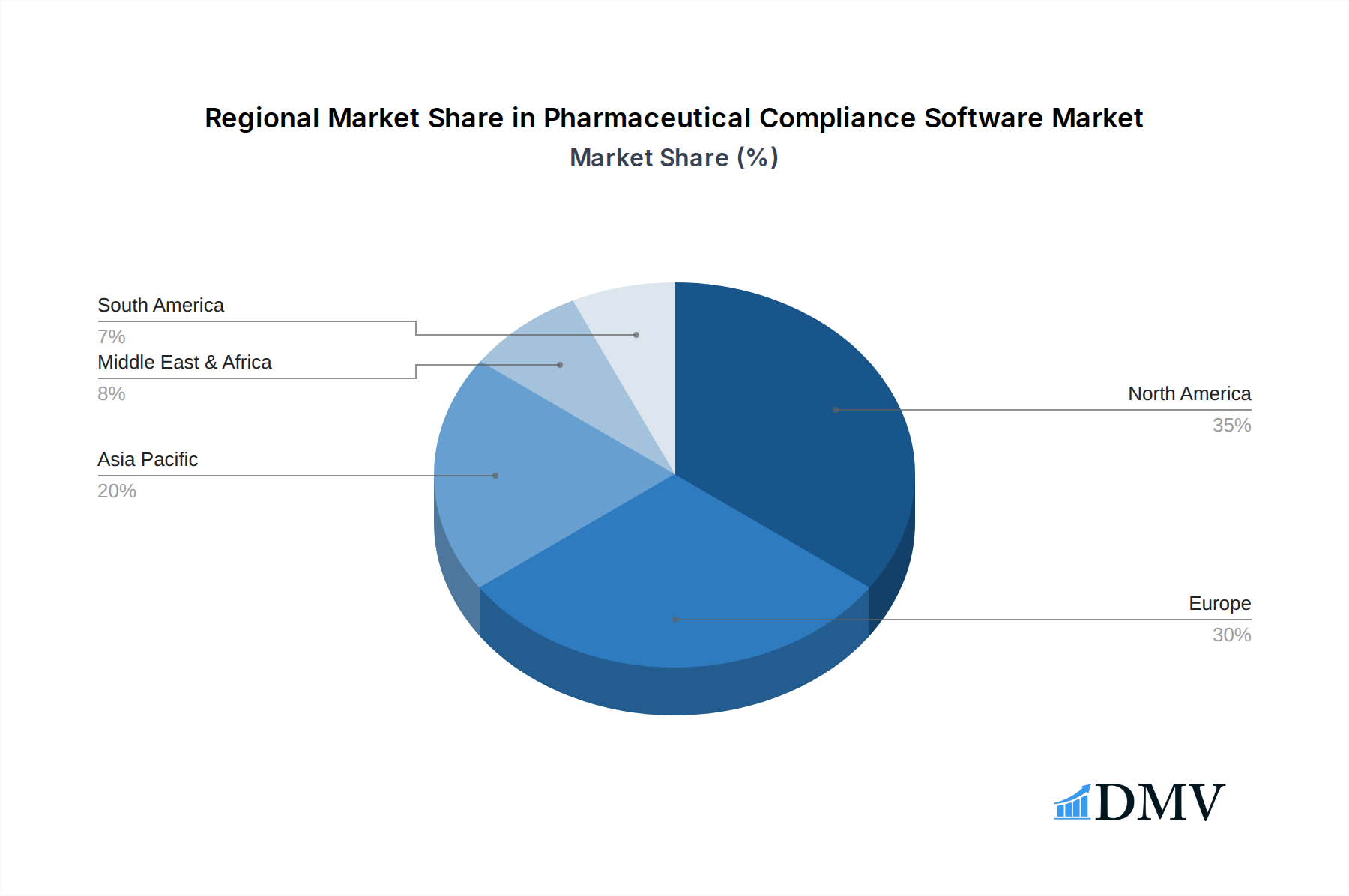

Geographically, North America and Europe collectively dominate the global Pharmaceutical Compliance Software market. North America, especially the United States, holds the largest market share, valued at an estimated xx billion in 2025. This leadership is attributable to the presence of a vast and highly regulated pharmaceutical industry, stringent FDA regulations (e.g., 21 CFR Part 11, GxP), high R&D investment, and early adoption of advanced digital solutions. Europe follows closely, driven by the equally stringent EMA guidelines and a robust pharmaceutical manufacturing base. These regions' sophisticated regulatory environments and a strong emphasis on data quality and integrity compel pharmaceutical companies to invest heavily in advanced compliance software, making them the primary demand generators for both cloud-based solutions and specialized PIM applications.

Pharmaceutical Compliance Software Product Innovations

Product innovations in Pharmaceutical Compliance Software are fundamentally transforming how the industry manages regulatory adherence and quality. Leading solutions now integrate Artificial Intelligence (AI) and Machine Learning (ML) to offer predictive analytics, automating the identification of potential compliance risks before they manifest. For instance, platforms from MasterControl and Wolters Kluwer are leveraging AI for intelligent document review, significantly reducing manual effort and improving accuracy in managing GxP documents. Real-time analytics dashboards provide instant visibility into compliance status across the entire value chain, while advanced data integrity features, sometimes incorporating blockchain, ensure auditability and immutability of critical records. Unique selling propositions revolve around seamless integration capabilities with existing enterprise systems, offering a unified platform for quality, risk, and regulatory information management. These technological advancements not only enhance performance by drastically reducing non-compliance incidents (estimated xx% reduction) but also empower pharmaceutical companies to achieve proactive, rather than reactive, compliance.

Propelling Factors for Pharmaceutical Compliance Software Growth

Several potent factors are propelling the growth of the Pharmaceutical Compliance Software market. Regulatory stringency remains paramount; evolving global GxP regulations, stricter data integrity requirements (e.g., FDA's 21 CFR Part 11, EU Annex 11), and an intensified focus on patient safety necessitate robust software solutions. For example, the need for enhanced serialization and traceability under the Drug Supply Chain Security Act (DSCSA) in the US and the Falsified Medicines Directive (FMD) in Europe drives demand for compliance platforms. Technologically, the digital transformation wave sweeping the pharmaceutical industry encourages adoption of cloud-based, AI-powered systems for efficiency and scalability. Economically, the globalization of pharmaceutical supply chains increases complexity, making integrated compliance software essential to manage diverse regulations across multiple jurisdictions, thereby mitigating substantial financial penalties and operational disruptions. Furthermore, the increasing volume of data generated by R&D and manufacturing demands sophisticated tools for effective management and analysis.

Obstacles in the Pharmaceutical Compliance Software Market

Despite significant growth, the Pharmaceutical Compliance Software market faces notable obstacles. A primary barrier is the high initial implementation cost and the complexity of integrating new software with legacy systems, which can involve expenditures of several billion for large enterprises. This often creates resistance to change, especially within organizations reliant on outdated, but deeply entrenched, processes. Another significant challenge is data migration, as transferring vast amounts of sensitive historical data into new systems can be technically complex, time-consuming, and carry inherent risks of data integrity compromise. Furthermore, regulatory fragmentation across different countries and regions presents a hurdle; software must be adaptable to a myriad of specific local requirements, complicating development and deployment. Competitive pressures from both established vendors and emerging niche players, coupled with the need for continuous software updates to match evolving regulations, can strain resources. Cybersecurity risks associated with handling highly sensitive pharmaceutical data also necessitate continuous, substantial investment, potentially slowing market expansion by an estimated xx billion in opportunity during the forecast period due to cautious adoption.

Future Opportunities in Pharmaceutical Compliance Software

The Pharmaceutical Compliance Software market is poised for significant future opportunities, driven by technological advancements and evolving industry needs. A major opportunity lies in the deeper integration of Artificial Intelligence (AI) and Machine Learning (ML) for predictive compliance, allowing pharmaceutical companies to anticipate and prevent regulatory issues proactively, rather than reactively. This includes AI-driven anomaly detection in quality control and automated regulatory intelligence gathering. Secondly, the expansion into emerging markets (e.g., Asia-Pacific, Latin America) presents substantial growth potential, as these regions rapidly develop their pharmaceutical industries and implement stricter regulatory frameworks, necessitating advanced compliance solutions. Another key opportunity is the leveraging of blockchain technology for enhanced supply chain traceability and data immutability, which can significantly bolster anti-counterfeiting measures and ensure transparent, verifiable drug provenance. Furthermore, the increasing trend towards personalized medicine and gene therapies will create new compliance complexities, demanding highly flexible and specialized software solutions capable of managing novel data sets and expedited regulatory pathways, opening new market niches for innovation and specialized compliance offerings.

Major Players in the Pharmaceutical Compliance Software Ecosystem

- Ideagen

- ACUTA

- Wolters Kluwer

- Lachman Consultant Services

- Sparta Systems

- Intagras

- LogicManager

- LogicGate

- Bwise

- Qordata

- Qualsys

- Axway

- Med-Script

- QUMAS

- MasterControl

Key Developments in Pharmaceutical Compliance Software Industry

- 2024/Q3: MasterControl launched an enhanced AI-powered module for automated document control, significantly reducing review times by xx% and improving audit readiness for pharmaceutical manufacturing sites.

- 2023/Q4: Ideagen acquired a specialist in Pharmacovigilance software, expanding its comprehensive GxP compliance suite to better address drug safety and adverse event reporting, aiming for an estimated xx billion increase in market reach.

- 2023/Q1: Wolters Kluwer introduced a new cloud-native regulatory intelligence platform, providing real-time updates on global pharmaceutical regulations, enabling proactive compliance strategy development for its global client base.

- 2022/Q2: Sparta Systems announced a strategic partnership with a leading blockchain provider to integrate distributed ledger technology for enhanced supply chain traceability and data integrity within its Quality Management System (QMS) offerings.

- 2021/Q3: QUMAS (now part of Dassault Systèmes) saw significant enhancements in its electronic document management capabilities, facilitating seamless submission of regulatory information to health authorities globally and contributing to a xx billion increase in platform utility.

Strategic Pharmaceutical Compliance Software Market Forecast

The Pharmaceutical Compliance Software market is poised for significant and sustained growth, fueled by an escalating global regulatory landscape and the relentless pursuit of digital transformation within the life sciences sector. Future opportunities are largely concentrated around the integration of cutting-edge technologies like AI, machine learning, and blockchain, which promise to revolutionize compliance from reactive to predictive. The increasing complexity of global supply chains and the stringent demand for data integrity will continue to drive investments in robust, cloud-based solutions. With a projected market value reaching xx billion by 2033, the market potential is enormous, catering to the industry's critical need for efficiency, risk mitigation, and unwavering adherence to quality and safety standards. Strategic collaborations and continuous innovation will be pivotal for companies looking to capitalize on this dynamic and essential market segment.

Pharmaceutical Compliance Software Segmentation

-

1. Application

- 1.1. Product Information Management

- 1.2. Pharmaceutical Electronic Registration

-

2. Types

- 2.1. Cloud-Based Pharmaceutical Compliance Software

- 2.2. On-Premise Pharmaceutical Compliance Software

Pharmaceutical Compliance Software Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Pharmaceutical Compliance Software Regional Market Share

Geographic Coverage of Pharmaceutical Compliance Software

Pharmaceutical Compliance Software REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Product Information Management

- 5.1.2. Pharmaceutical Electronic Registration

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Cloud-Based Pharmaceutical Compliance Software

- 5.2.2. On-Premise Pharmaceutical Compliance Software

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Pharmaceutical Compliance Software Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Product Information Management

- 6.1.2. Pharmaceutical Electronic Registration

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Cloud-Based Pharmaceutical Compliance Software

- 6.2.2. On-Premise Pharmaceutical Compliance Software

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Pharmaceutical Compliance Software Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Product Information Management

- 7.1.2. Pharmaceutical Electronic Registration

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Cloud-Based Pharmaceutical Compliance Software

- 7.2.2. On-Premise Pharmaceutical Compliance Software

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Pharmaceutical Compliance Software Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Product Information Management

- 8.1.2. Pharmaceutical Electronic Registration

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Cloud-Based Pharmaceutical Compliance Software

- 8.2.2. On-Premise Pharmaceutical Compliance Software

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Pharmaceutical Compliance Software Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Product Information Management

- 9.1.2. Pharmaceutical Electronic Registration

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Cloud-Based Pharmaceutical Compliance Software

- 9.2.2. On-Premise Pharmaceutical Compliance Software

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Pharmaceutical Compliance Software Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Product Information Management

- 10.1.2. Pharmaceutical Electronic Registration

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Cloud-Based Pharmaceutical Compliance Software

- 10.2.2. On-Premise Pharmaceutical Compliance Software

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Pharmaceutical Compliance Software Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Product Information Management

- 11.1.2. Pharmaceutical Electronic Registration

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Cloud-Based Pharmaceutical Compliance Software

- 11.2.2. On-Premise Pharmaceutical Compliance Software

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Ideagen

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 ACUTA

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Wolters Kluwer

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Lachman Consultant Services

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Sparta Systems

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Intagras

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 LogicManager

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 LogicGate

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Bwise

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Qordata

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Qualsys

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Axway

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Med-Script

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 QUMAS

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 MasterControl

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 Ideagen

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Pharmaceutical Compliance Software Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Pharmaceutical Compliance Software Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Pharmaceutical Compliance Software Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Pharmaceutical Compliance Software Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Pharmaceutical Compliance Software Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Pharmaceutical Compliance Software Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Pharmaceutical Compliance Software Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Pharmaceutical Compliance Software Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Pharmaceutical Compliance Software Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Pharmaceutical Compliance Software Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Pharmaceutical Compliance Software Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Pharmaceutical Compliance Software Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Pharmaceutical Compliance Software Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Pharmaceutical Compliance Software Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Pharmaceutical Compliance Software Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Pharmaceutical Compliance Software Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Pharmaceutical Compliance Software Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Pharmaceutical Compliance Software Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Pharmaceutical Compliance Software Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Pharmaceutical Compliance Software Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Pharmaceutical Compliance Software Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Pharmaceutical Compliance Software Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Pharmaceutical Compliance Software Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Pharmaceutical Compliance Software Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Pharmaceutical Compliance Software Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Pharmaceutical Compliance Software Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Pharmaceutical Compliance Software Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Pharmaceutical Compliance Software Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Pharmaceutical Compliance Software Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Pharmaceutical Compliance Software Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Pharmaceutical Compliance Software Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Pharmaceutical Compliance Software Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Pharmaceutical Compliance Software Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Pharmaceutical Compliance Software Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Pharmaceutical Compliance Software Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Pharmaceutical Compliance Software Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Pharmaceutical Compliance Software Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Pharmaceutical Compliance Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Pharmaceutical Compliance Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Pharmaceutical Compliance Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Pharmaceutical Compliance Software Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Pharmaceutical Compliance Software Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Pharmaceutical Compliance Software Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Pharmaceutical Compliance Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Pharmaceutical Compliance Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Pharmaceutical Compliance Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Pharmaceutical Compliance Software Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Pharmaceutical Compliance Software Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Pharmaceutical Compliance Software Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Pharmaceutical Compliance Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Pharmaceutical Compliance Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Pharmaceutical Compliance Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Pharmaceutical Compliance Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Pharmaceutical Compliance Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Pharmaceutical Compliance Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Pharmaceutical Compliance Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Pharmaceutical Compliance Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Pharmaceutical Compliance Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Pharmaceutical Compliance Software Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Pharmaceutical Compliance Software Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Pharmaceutical Compliance Software Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Pharmaceutical Compliance Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Pharmaceutical Compliance Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Pharmaceutical Compliance Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Pharmaceutical Compliance Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Pharmaceutical Compliance Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Pharmaceutical Compliance Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Pharmaceutical Compliance Software Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Pharmaceutical Compliance Software Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Pharmaceutical Compliance Software Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Pharmaceutical Compliance Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Pharmaceutical Compliance Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Pharmaceutical Compliance Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Pharmaceutical Compliance Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Pharmaceutical Compliance Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Pharmaceutical Compliance Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Pharmaceutical Compliance Software Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Pharmaceutical Compliance Software?

The projected CAGR is approximately 10.4%.

2. Which companies are prominent players in the Pharmaceutical Compliance Software?

Key companies in the market include Ideagen, ACUTA, Wolters Kluwer, Lachman Consultant Services, Sparta Systems, Intagras, LogicManager, LogicGate, Bwise, Qordata, Qualsys, Axway, Med-Script, QUMAS, MasterControl.

3. What are the main segments of the Pharmaceutical Compliance Software?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.2 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4350.00, USD 6525.00, and USD 8700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Pharmaceutical Compliance Software," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Pharmaceutical Compliance Software report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Pharmaceutical Compliance Software?

To stay informed about further developments, trends, and reports in the Pharmaceutical Compliance Software, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence