Key Insights

The global pet food market is a dynamic and expanding sector, projected to reach a substantial size driven by several key factors. The rising pet ownership globally, coupled with increasing humanization of pets, fuels demand for premium and specialized pet food products. Consumers are increasingly concerned about pet health and nutrition, leading to a surge in demand for high-quality ingredients, functional foods addressing specific health needs (e.g., weight management, allergies), and natural or organic options. This trend is particularly evident in the premium pet food segment, which commands higher prices and drives significant market growth. The convenience factor also plays a crucial role, with online channels experiencing rapid expansion, providing consumers with seamless access to a wide variety of products. While the market faces challenges like fluctuating raw material costs and increased competition, the overall outlook remains positive due to the enduring human-animal bond and sustained growth in pet ownership. Market segmentation reveals significant opportunities in specialized diets for pets with health conditions, further enhancing market complexity and growth. Key players like Mars Incorporated, Nestlé Purina, and Hill's Pet Nutrition continue to dominate the market, leveraging strong brand recognition and extensive distribution networks. However, smaller, specialized brands focusing on niche markets (e.g., organic, hypoallergenic) are also gaining traction, driving innovation and market diversification.

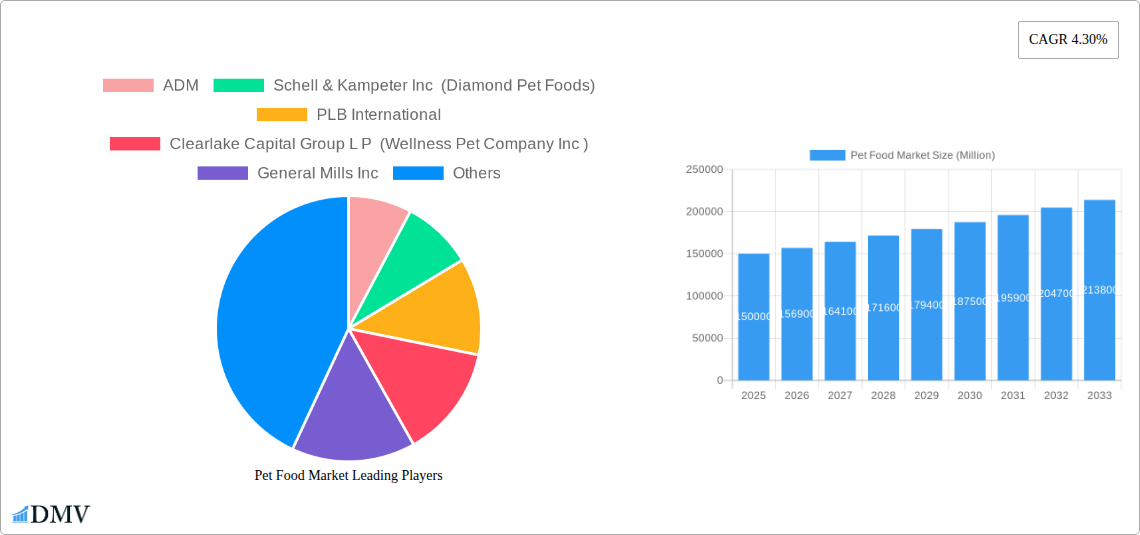

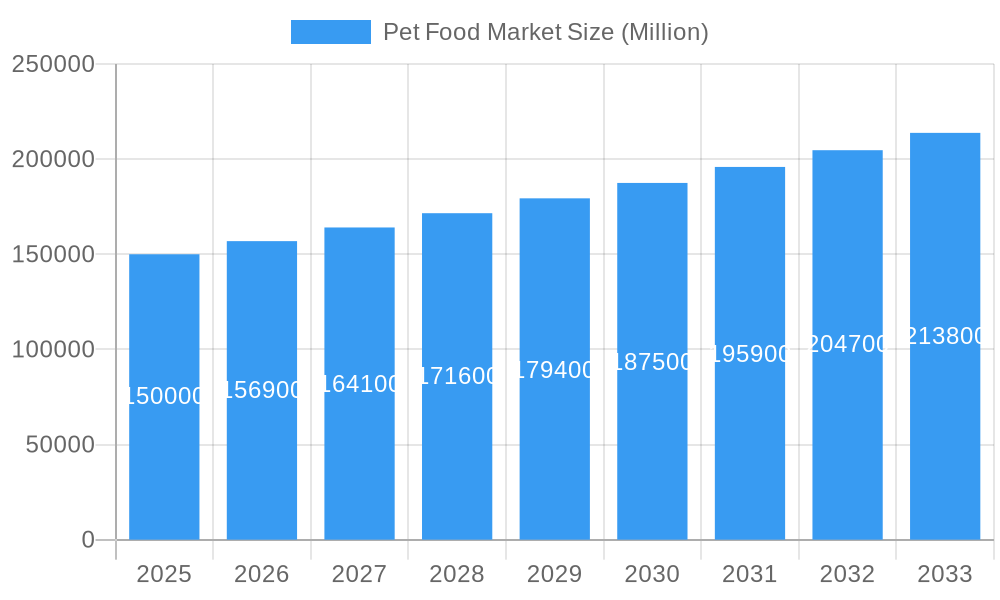

Pet Food Market Market Size (In Billion)

This growth is further supported by expanding geographical markets, particularly in developing economies experiencing rising middle-class populations and increased pet ownership rates. The competitive landscape is characterized by both established multinational corporations and smaller, agile companies, leading to ongoing innovation in product development and marketing strategies. The market's expansion is also influenced by evolving consumer preferences towards sustainable and ethically sourced ingredients, putting pressure on manufacturers to adopt responsible sourcing practices. The integration of technology in the sector, including personalized nutrition plans based on pet profiles and data-driven insights, will continue to shape the future of the pet food market, creating new opportunities for growth and market consolidation. While challenges related to supply chain management and regulatory compliance persist, the long-term prospects for the pet food market remain robust, underpinned by a steadily growing global pet population and increasing consumer spending on pet care.

Pet Food Market Company Market Share

Pet Food Market: A Comprehensive Report (2019-2033)

This insightful report provides a detailed analysis of the global pet food market, encompassing historical data (2019-2024), current estimates (2025), and future forecasts (2025-2033). It delves into market dynamics, competitive landscapes, and emerging trends, offering valuable insights for stakeholders across the industry. The market is projected to reach xx Million by 2033, presenting significant opportunities for growth and investment.

Pet Food Market Market Composition & Trends

This section examines the intricate structure of the pet food market, encompassing market concentration, innovation drivers, regulatory frameworks, substitute products, end-user demographics, and the influence of mergers and acquisitions (M&A). The report analyzes the market share distribution among key players, revealing a moderately concentrated market with significant opportunities for both established players and emerging entrants. M&A activity in the pet food sector is evaluated, providing insights into deal values and strategic implications. Factors like increasing pet ownership, rising disposable incomes, and the growing humanization of pets are explored in detail, alongside their impact on market growth. Regulatory changes concerning pet food safety and labeling are also investigated to determine their effects on the overall market landscape. Finally, the report delves into the types of substitute products available and the extent to which they impact market share.

- Market Concentration: The market is moderately concentrated, with top players holding xx% of the market share in 2025.

- Innovation Catalysts: Growing demand for premium and specialized pet foods drives innovation.

- Regulatory Landscape: Stringent regulations regarding pet food safety and labeling influence market dynamics.

- Substitute Products: Limited substitute products exist, primarily homemade pet food, which pose minimal threat.

- End-User Profiles: The report segments end-users by pet type (dogs, cats, other pets) and their preferences for different food types.

- M&A Activities: Significant M&A activity, with deal values exceeding xx Million in the past five years, indicating market consolidation.

Pet Food Market Industry Evolution

This section details the evolutionary trajectory of the pet food industry, highlighting significant growth patterns, technological advancements, and evolving consumer preferences. The report showcases historical growth rates, pinpointing key factors contributing to expansion. Technological innovations like improved food processing, packaging, and formulation technologies are analyzed alongside their influence on market growth. The shift in consumer demand towards premium, functional, and specialized pet foods is also examined. Specific data points, such as the growth rates of premium pet food segments and the adoption rate of novel pet food technologies are used to illustrate these trends. The report also explores the impact of changing lifestyles and pet ownership patterns on the industry's growth trajectory.

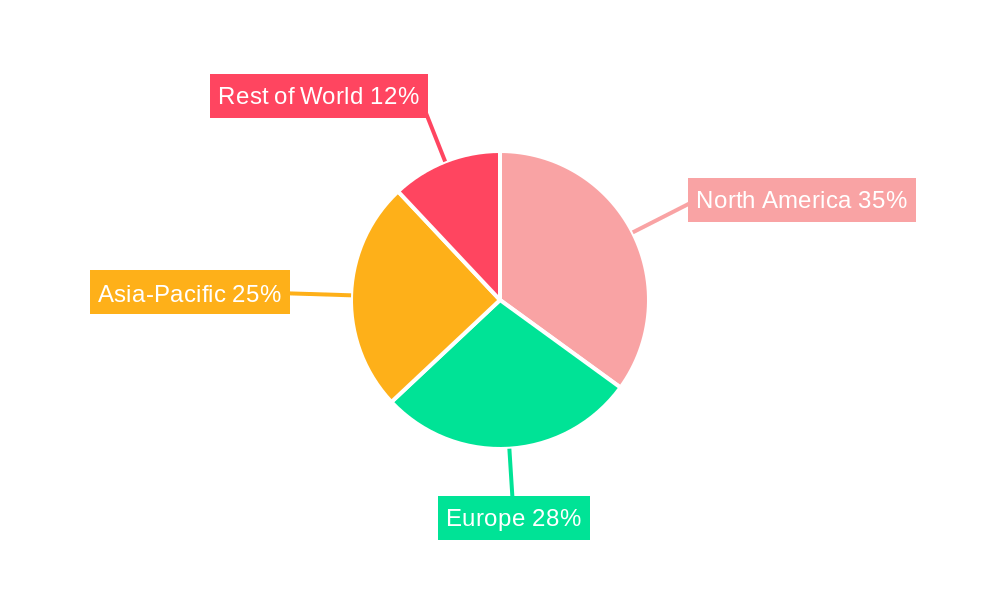

Leading Regions, Countries, or Segments in Pet Food Market

This segment identifies the leading regions, countries, and market segments within the pet food industry. The analysis pinpoints the most dominant areas, considering factors like pet ownership rates, consumer spending habits, and regulatory environments. This section provides a detailed explanation of the factors contributing to their dominance. Both quantitative data (market size, growth rates) and qualitative insights (consumer preferences, market dynamics) are employed.

- Dominant Region: North America (xx Million in 2025)

- Key Drivers for North America's Dominance: High pet ownership rates, high disposable incomes, strong regulatory framework, and robust distribution channels.

- Dominant Pet Type: Dogs (xx Million in 2025)

- Key Drivers for Dog Food Dominance: Higher pet ownership and willingness to spend more on dog food.

- Dominant Distribution Channel: Supermarkets/Hypermarkets (xx Million in 2025)

- Key Drivers for Supermarket/Hypermarket Dominance: Wide reach, established infrastructure, and convenience.

Pet Food Market Product Innovations

The pet food market witnesses continuous innovation, driven by consumer demand for specialized products catering to specific pet needs and health concerns. Recent innovations include the development of novel ingredients (like insect protein), functional foods addressing specific health issues (e.g., sensitive stomachs), and technologically advanced formulations improving digestibility and nutrient absorption. These innovations are characterized by unique selling propositions such as enhanced palatability, improved digestibility, and functional benefits (e.g., joint health support).

Propelling Factors for Pet Food Market Growth

Several factors contribute to the expansion of the pet food market. The increasing humanization of pets leads to higher spending on pet care, including food. Technological advancements improve product quality, safety, and nutrition, stimulating demand. Economic factors like rising disposable incomes in emerging markets boost pet ownership and spending. Supportive government regulations ensure food safety and quality, fostering market growth.

Obstacles in the Pet Food Market Market

The pet food market faces challenges, including fluctuating raw material prices impacting production costs and profit margins. Supply chain disruptions due to geopolitical events or natural calamities can impact product availability. Intense competition among established players and emerging brands creates pricing pressure and necessitates continuous innovation. Stricter regulatory standards may increase compliance costs for manufacturers.

Future Opportunities in Pet Food Market

The future of the pet food market holds promising opportunities. The expansion into emerging markets with growing pet ownership presents significant potential. Technological innovations, such as personalized nutrition and advanced food formulations, offer avenues for growth. The growing demand for sustainable and ethically sourced pet food creates opportunities for eco-conscious brands.

Major Players in the Pet Food Market Ecosystem

- ADM

- Schell & Kampeter Inc (Diamond Pet Foods)

- PLB International

- Clearlake Capital Group L P (Wellness Pet Company Inc)

- General Mills Inc

- Heristo Aktiengesellschaft

- Mars Incorporated

- Nestle (Purina)

- Colgate-Palmolive Company (Hill's Pet Nutrition Inc)

- The J M Smucker Company

Key Developments in Pet Food Market Industry

- May 2023: Nestle Purina launched new cat treats under the Friskies "Friskies Playfuls - treats" brand.

- June 2023: Mars Incorporated launched its premium cat brand SHEBA in Canada.

- July 2023: Hill's Pet Nutrition introduced its new MSC (Marine Stewardship Council) certified pollock and insect protein products.

Strategic Pet Food Market Market Forecast

The pet food market is poised for robust growth, driven by sustained demand for premium and specialized pet foods. Technological innovations and expansion into new markets will further fuel market expansion. The increasing focus on pet health and wellness will continue to drive demand for functional and nutritious pet food products. The market's future is bright, with significant potential for growth and profitability across various segments.

Pet Food Market Segmentation

-

1. Pet Food Product

-

1.1. By Sub Product

-

1.1.1. Dry Pet Food

-

1.1.1.1. By Sub Dry Pet Food

- 1.1.1.1.1. Kibbles

- 1.1.1.1.2. Other Dry Pet Food

-

1.1.1.1. By Sub Dry Pet Food

- 1.1.2. Wet Pet Food

-

1.1.1. Dry Pet Food

-

1.2. Pet Nutraceuticals/Supplements

- 1.2.1. Milk Bioactives

- 1.2.2. Omega-3 Fatty Acids

- 1.2.3. Probiotics

- 1.2.4. Proteins and Peptides

- 1.2.5. Vitamins and Minerals

- 1.2.6. Other Nutraceuticals

-

1.3. Pet Treats

- 1.3.1. Crunchy Treats

- 1.3.2. Dental Treats

- 1.3.3. Freeze-dried and Jerky Treats

- 1.3.4. Soft & Chewy Treats

- 1.3.5. Other Treats

-

1.4. Pet Veterinary Diets

- 1.4.1. Diabetes

- 1.4.2. Digestive Sensitivity

- 1.4.3. Oral Care Diets

- 1.4.4. Renal

- 1.4.5. Urinary tract disease

- 1.4.6. Other Veterinary Diets

-

1.1. By Sub Product

-

2. Pets

- 2.1. Cats

- 2.2. Dogs

- 2.3. Other Pets

-

3. Distribution Channel

- 3.1. Convenience Stores

- 3.2. Online Channel

- 3.3. Specialty Stores

- 3.4. Supermarkets/Hypermarkets

- 3.5. Other Channels

Pet Food Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Pet Food Market Regional Market Share

Geographic Coverage of Pet Food Market

Pet Food Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Pet Food Product

- 5.1.1. By Sub Product

- 5.1.1.1. Dry Pet Food

- 5.1.1.1.1. By Sub Dry Pet Food

- 5.1.1.1.1.1. Kibbles

- 5.1.1.1.1.2. Other Dry Pet Food

- 5.1.1.1.1. By Sub Dry Pet Food

- 5.1.1.2. Wet Pet Food

- 5.1.1.1. Dry Pet Food

- 5.1.2. Pet Nutraceuticals/Supplements

- 5.1.2.1. Milk Bioactives

- 5.1.2.2. Omega-3 Fatty Acids

- 5.1.2.3. Probiotics

- 5.1.2.4. Proteins and Peptides

- 5.1.2.5. Vitamins and Minerals

- 5.1.2.6. Other Nutraceuticals

- 5.1.3. Pet Treats

- 5.1.3.1. Crunchy Treats

- 5.1.3.2. Dental Treats

- 5.1.3.3. Freeze-dried and Jerky Treats

- 5.1.3.4. Soft & Chewy Treats

- 5.1.3.5. Other Treats

- 5.1.4. Pet Veterinary Diets

- 5.1.4.1. Diabetes

- 5.1.4.2. Digestive Sensitivity

- 5.1.4.3. Oral Care Diets

- 5.1.4.4. Renal

- 5.1.4.5. Urinary tract disease

- 5.1.4.6. Other Veterinary Diets

- 5.1.1. By Sub Product

- 5.2. Market Analysis, Insights and Forecast - by Pets

- 5.2.1. Cats

- 5.2.2. Dogs

- 5.2.3. Other Pets

- 5.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.3.1. Convenience Stores

- 5.3.2. Online Channel

- 5.3.3. Specialty Stores

- 5.3.4. Supermarkets/Hypermarkets

- 5.3.5. Other Channels

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. South America

- 5.4.3. Europe

- 5.4.4. Middle East & Africa

- 5.4.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Pet Food Product

- 6. Global Pet Food Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Pet Food Product

- 6.1.1. By Sub Product

- 6.1.1.1. Dry Pet Food

- 6.1.1.1.1. By Sub Dry Pet Food

- 6.1.1.1.1.1. Kibbles

- 6.1.1.1.1.2. Other Dry Pet Food

- 6.1.1.1.1. By Sub Dry Pet Food

- 6.1.1.2. Wet Pet Food

- 6.1.1.1. Dry Pet Food

- 6.1.2. Pet Nutraceuticals/Supplements

- 6.1.2.1. Milk Bioactives

- 6.1.2.2. Omega-3 Fatty Acids

- 6.1.2.3. Probiotics

- 6.1.2.4. Proteins and Peptides

- 6.1.2.5. Vitamins and Minerals

- 6.1.2.6. Other Nutraceuticals

- 6.1.3. Pet Treats

- 6.1.3.1. Crunchy Treats

- 6.1.3.2. Dental Treats

- 6.1.3.3. Freeze-dried and Jerky Treats

- 6.1.3.4. Soft & Chewy Treats

- 6.1.3.5. Other Treats

- 6.1.4. Pet Veterinary Diets

- 6.1.4.1. Diabetes

- 6.1.4.2. Digestive Sensitivity

- 6.1.4.3. Oral Care Diets

- 6.1.4.4. Renal

- 6.1.4.5. Urinary tract disease

- 6.1.4.6. Other Veterinary Diets

- 6.1.1. By Sub Product

- 6.2. Market Analysis, Insights and Forecast - by Pets

- 6.2.1. Cats

- 6.2.2. Dogs

- 6.2.3. Other Pets

- 6.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.3.1. Convenience Stores

- 6.3.2. Online Channel

- 6.3.3. Specialty Stores

- 6.3.4. Supermarkets/Hypermarkets

- 6.3.5. Other Channels

- 6.1. Market Analysis, Insights and Forecast - by Pet Food Product

- 7. North America Pet Food Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Pet Food Product

- 7.1.1. By Sub Product

- 7.1.1.1. Dry Pet Food

- 7.1.1.1.1. By Sub Dry Pet Food

- 7.1.1.1.1.1. Kibbles

- 7.1.1.1.1.2. Other Dry Pet Food

- 7.1.1.1.1. By Sub Dry Pet Food

- 7.1.1.2. Wet Pet Food

- 7.1.1.1. Dry Pet Food

- 7.1.2. Pet Nutraceuticals/Supplements

- 7.1.2.1. Milk Bioactives

- 7.1.2.2. Omega-3 Fatty Acids

- 7.1.2.3. Probiotics

- 7.1.2.4. Proteins and Peptides

- 7.1.2.5. Vitamins and Minerals

- 7.1.2.6. Other Nutraceuticals

- 7.1.3. Pet Treats

- 7.1.3.1. Crunchy Treats

- 7.1.3.2. Dental Treats

- 7.1.3.3. Freeze-dried and Jerky Treats

- 7.1.3.4. Soft & Chewy Treats

- 7.1.3.5. Other Treats

- 7.1.4. Pet Veterinary Diets

- 7.1.4.1. Diabetes

- 7.1.4.2. Digestive Sensitivity

- 7.1.4.3. Oral Care Diets

- 7.1.4.4. Renal

- 7.1.4.5. Urinary tract disease

- 7.1.4.6. Other Veterinary Diets

- 7.1.1. By Sub Product

- 7.2. Market Analysis, Insights and Forecast - by Pets

- 7.2.1. Cats

- 7.2.2. Dogs

- 7.2.3. Other Pets

- 7.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.3.1. Convenience Stores

- 7.3.2. Online Channel

- 7.3.3. Specialty Stores

- 7.3.4. Supermarkets/Hypermarkets

- 7.3.5. Other Channels

- 7.1. Market Analysis, Insights and Forecast - by Pet Food Product

- 8. South America Pet Food Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Pet Food Product

- 8.1.1. By Sub Product

- 8.1.1.1. Dry Pet Food

- 8.1.1.1.1. By Sub Dry Pet Food

- 8.1.1.1.1.1. Kibbles

- 8.1.1.1.1.2. Other Dry Pet Food

- 8.1.1.1.1. By Sub Dry Pet Food

- 8.1.1.2. Wet Pet Food

- 8.1.1.1. Dry Pet Food

- 8.1.2. Pet Nutraceuticals/Supplements

- 8.1.2.1. Milk Bioactives

- 8.1.2.2. Omega-3 Fatty Acids

- 8.1.2.3. Probiotics

- 8.1.2.4. Proteins and Peptides

- 8.1.2.5. Vitamins and Minerals

- 8.1.2.6. Other Nutraceuticals

- 8.1.3. Pet Treats

- 8.1.3.1. Crunchy Treats

- 8.1.3.2. Dental Treats

- 8.1.3.3. Freeze-dried and Jerky Treats

- 8.1.3.4. Soft & Chewy Treats

- 8.1.3.5. Other Treats

- 8.1.4. Pet Veterinary Diets

- 8.1.4.1. Diabetes

- 8.1.4.2. Digestive Sensitivity

- 8.1.4.3. Oral Care Diets

- 8.1.4.4. Renal

- 8.1.4.5. Urinary tract disease

- 8.1.4.6. Other Veterinary Diets

- 8.1.1. By Sub Product

- 8.2. Market Analysis, Insights and Forecast - by Pets

- 8.2.1. Cats

- 8.2.2. Dogs

- 8.2.3. Other Pets

- 8.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.3.1. Convenience Stores

- 8.3.2. Online Channel

- 8.3.3. Specialty Stores

- 8.3.4. Supermarkets/Hypermarkets

- 8.3.5. Other Channels

- 8.1. Market Analysis, Insights and Forecast - by Pet Food Product

- 9. Europe Pet Food Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Pet Food Product

- 9.1.1. By Sub Product

- 9.1.1.1. Dry Pet Food

- 9.1.1.1.1. By Sub Dry Pet Food

- 9.1.1.1.1.1. Kibbles

- 9.1.1.1.1.2. Other Dry Pet Food

- 9.1.1.1.1. By Sub Dry Pet Food

- 9.1.1.2. Wet Pet Food

- 9.1.1.1. Dry Pet Food

- 9.1.2. Pet Nutraceuticals/Supplements

- 9.1.2.1. Milk Bioactives

- 9.1.2.2. Omega-3 Fatty Acids

- 9.1.2.3. Probiotics

- 9.1.2.4. Proteins and Peptides

- 9.1.2.5. Vitamins and Minerals

- 9.1.2.6. Other Nutraceuticals

- 9.1.3. Pet Treats

- 9.1.3.1. Crunchy Treats

- 9.1.3.2. Dental Treats

- 9.1.3.3. Freeze-dried and Jerky Treats

- 9.1.3.4. Soft & Chewy Treats

- 9.1.3.5. Other Treats

- 9.1.4. Pet Veterinary Diets

- 9.1.4.1. Diabetes

- 9.1.4.2. Digestive Sensitivity

- 9.1.4.3. Oral Care Diets

- 9.1.4.4. Renal

- 9.1.4.5. Urinary tract disease

- 9.1.4.6. Other Veterinary Diets

- 9.1.1. By Sub Product

- 9.2. Market Analysis, Insights and Forecast - by Pets

- 9.2.1. Cats

- 9.2.2. Dogs

- 9.2.3. Other Pets

- 9.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.3.1. Convenience Stores

- 9.3.2. Online Channel

- 9.3.3. Specialty Stores

- 9.3.4. Supermarkets/Hypermarkets

- 9.3.5. Other Channels

- 9.1. Market Analysis, Insights and Forecast - by Pet Food Product

- 10. Middle East & Africa Pet Food Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Pet Food Product

- 10.1.1. By Sub Product

- 10.1.1.1. Dry Pet Food

- 10.1.1.1.1. By Sub Dry Pet Food

- 10.1.1.1.1.1. Kibbles

- 10.1.1.1.1.2. Other Dry Pet Food

- 10.1.1.1.1. By Sub Dry Pet Food

- 10.1.1.2. Wet Pet Food

- 10.1.1.1. Dry Pet Food

- 10.1.2. Pet Nutraceuticals/Supplements

- 10.1.2.1. Milk Bioactives

- 10.1.2.2. Omega-3 Fatty Acids

- 10.1.2.3. Probiotics

- 10.1.2.4. Proteins and Peptides

- 10.1.2.5. Vitamins and Minerals

- 10.1.2.6. Other Nutraceuticals

- 10.1.3. Pet Treats

- 10.1.3.1. Crunchy Treats

- 10.1.3.2. Dental Treats

- 10.1.3.3. Freeze-dried and Jerky Treats

- 10.1.3.4. Soft & Chewy Treats

- 10.1.3.5. Other Treats

- 10.1.4. Pet Veterinary Diets

- 10.1.4.1. Diabetes

- 10.1.4.2. Digestive Sensitivity

- 10.1.4.3. Oral Care Diets

- 10.1.4.4. Renal

- 10.1.4.5. Urinary tract disease

- 10.1.4.6. Other Veterinary Diets

- 10.1.1. By Sub Product

- 10.2. Market Analysis, Insights and Forecast - by Pets

- 10.2.1. Cats

- 10.2.2. Dogs

- 10.2.3. Other Pets

- 10.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.3.1. Convenience Stores

- 10.3.2. Online Channel

- 10.3.3. Specialty Stores

- 10.3.4. Supermarkets/Hypermarkets

- 10.3.5. Other Channels

- 10.1. Market Analysis, Insights and Forecast - by Pet Food Product

- 11. Asia Pacific Pet Food Market Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Pet Food Product

- 11.1.1. By Sub Product

- 11.1.1.1. Dry Pet Food

- 11.1.1.1.1. By Sub Dry Pet Food

- 11.1.1.1.1.1. Kibbles

- 11.1.1.1.1.2. Other Dry Pet Food

- 11.1.1.1.1. By Sub Dry Pet Food

- 11.1.1.2. Wet Pet Food

- 11.1.1.1. Dry Pet Food

- 11.1.2. Pet Nutraceuticals/Supplements

- 11.1.2.1. Milk Bioactives

- 11.1.2.2. Omega-3 Fatty Acids

- 11.1.2.3. Probiotics

- 11.1.2.4. Proteins and Peptides

- 11.1.2.5. Vitamins and Minerals

- 11.1.2.6. Other Nutraceuticals

- 11.1.3. Pet Treats

- 11.1.3.1. Crunchy Treats

- 11.1.3.2. Dental Treats

- 11.1.3.3. Freeze-dried and Jerky Treats

- 11.1.3.4. Soft & Chewy Treats

- 11.1.3.5. Other Treats

- 11.1.4. Pet Veterinary Diets

- 11.1.4.1. Diabetes

- 11.1.4.2. Digestive Sensitivity

- 11.1.4.3. Oral Care Diets

- 11.1.4.4. Renal

- 11.1.4.5. Urinary tract disease

- 11.1.4.6. Other Veterinary Diets

- 11.1.1. By Sub Product

- 11.2. Market Analysis, Insights and Forecast - by Pets

- 11.2.1. Cats

- 11.2.2. Dogs

- 11.2.3. Other Pets

- 11.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.3.1. Convenience Stores

- 11.3.2. Online Channel

- 11.3.3. Specialty Stores

- 11.3.4. Supermarkets/Hypermarkets

- 11.3.5. Other Channels

- 11.1. Market Analysis, Insights and Forecast - by Pet Food Product

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 ADM

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Schell & Kampeter Inc (Diamond Pet Foods)

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 PLB International

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Clearlake Capital Group L P (Wellness Pet Company Inc )

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 General Mills Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Heristo Aktiengesellschaft

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Mars Incorporated

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Nestle (Purina)

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Colgate-Palmolive Company (Hill's Pet Nutrition Inc )

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 The J M Smucker Compan

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 ADM

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Pet Food Market Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Pet Food Market Revenue (undefined), by Pet Food Product 2025 & 2033

- Figure 3: North America Pet Food Market Revenue Share (%), by Pet Food Product 2025 & 2033

- Figure 4: North America Pet Food Market Revenue (undefined), by Pets 2025 & 2033

- Figure 5: North America Pet Food Market Revenue Share (%), by Pets 2025 & 2033

- Figure 6: North America Pet Food Market Revenue (undefined), by Distribution Channel 2025 & 2033

- Figure 7: North America Pet Food Market Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 8: North America Pet Food Market Revenue (undefined), by Country 2025 & 2033

- Figure 9: North America Pet Food Market Revenue Share (%), by Country 2025 & 2033

- Figure 10: South America Pet Food Market Revenue (undefined), by Pet Food Product 2025 & 2033

- Figure 11: South America Pet Food Market Revenue Share (%), by Pet Food Product 2025 & 2033

- Figure 12: South America Pet Food Market Revenue (undefined), by Pets 2025 & 2033

- Figure 13: South America Pet Food Market Revenue Share (%), by Pets 2025 & 2033

- Figure 14: South America Pet Food Market Revenue (undefined), by Distribution Channel 2025 & 2033

- Figure 15: South America Pet Food Market Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 16: South America Pet Food Market Revenue (undefined), by Country 2025 & 2033

- Figure 17: South America Pet Food Market Revenue Share (%), by Country 2025 & 2033

- Figure 18: Europe Pet Food Market Revenue (undefined), by Pet Food Product 2025 & 2033

- Figure 19: Europe Pet Food Market Revenue Share (%), by Pet Food Product 2025 & 2033

- Figure 20: Europe Pet Food Market Revenue (undefined), by Pets 2025 & 2033

- Figure 21: Europe Pet Food Market Revenue Share (%), by Pets 2025 & 2033

- Figure 22: Europe Pet Food Market Revenue (undefined), by Distribution Channel 2025 & 2033

- Figure 23: Europe Pet Food Market Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 24: Europe Pet Food Market Revenue (undefined), by Country 2025 & 2033

- Figure 25: Europe Pet Food Market Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East & Africa Pet Food Market Revenue (undefined), by Pet Food Product 2025 & 2033

- Figure 27: Middle East & Africa Pet Food Market Revenue Share (%), by Pet Food Product 2025 & 2033

- Figure 28: Middle East & Africa Pet Food Market Revenue (undefined), by Pets 2025 & 2033

- Figure 29: Middle East & Africa Pet Food Market Revenue Share (%), by Pets 2025 & 2033

- Figure 30: Middle East & Africa Pet Food Market Revenue (undefined), by Distribution Channel 2025 & 2033

- Figure 31: Middle East & Africa Pet Food Market Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 32: Middle East & Africa Pet Food Market Revenue (undefined), by Country 2025 & 2033

- Figure 33: Middle East & Africa Pet Food Market Revenue Share (%), by Country 2025 & 2033

- Figure 34: Asia Pacific Pet Food Market Revenue (undefined), by Pet Food Product 2025 & 2033

- Figure 35: Asia Pacific Pet Food Market Revenue Share (%), by Pet Food Product 2025 & 2033

- Figure 36: Asia Pacific Pet Food Market Revenue (undefined), by Pets 2025 & 2033

- Figure 37: Asia Pacific Pet Food Market Revenue Share (%), by Pets 2025 & 2033

- Figure 38: Asia Pacific Pet Food Market Revenue (undefined), by Distribution Channel 2025 & 2033

- Figure 39: Asia Pacific Pet Food Market Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 40: Asia Pacific Pet Food Market Revenue (undefined), by Country 2025 & 2033

- Figure 41: Asia Pacific Pet Food Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Pet Food Market Revenue undefined Forecast, by Pet Food Product 2020 & 2033

- Table 2: Global Pet Food Market Revenue undefined Forecast, by Pets 2020 & 2033

- Table 3: Global Pet Food Market Revenue undefined Forecast, by Distribution Channel 2020 & 2033

- Table 4: Global Pet Food Market Revenue undefined Forecast, by Region 2020 & 2033

- Table 5: Global Pet Food Market Revenue undefined Forecast, by Pet Food Product 2020 & 2033

- Table 6: Global Pet Food Market Revenue undefined Forecast, by Pets 2020 & 2033

- Table 7: Global Pet Food Market Revenue undefined Forecast, by Distribution Channel 2020 & 2033

- Table 8: Global Pet Food Market Revenue undefined Forecast, by Country 2020 & 2033

- Table 9: United States Pet Food Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Canada Pet Food Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 11: Mexico Pet Food Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 12: Global Pet Food Market Revenue undefined Forecast, by Pet Food Product 2020 & 2033

- Table 13: Global Pet Food Market Revenue undefined Forecast, by Pets 2020 & 2033

- Table 14: Global Pet Food Market Revenue undefined Forecast, by Distribution Channel 2020 & 2033

- Table 15: Global Pet Food Market Revenue undefined Forecast, by Country 2020 & 2033

- Table 16: Brazil Pet Food Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 17: Argentina Pet Food Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 18: Rest of South America Pet Food Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 19: Global Pet Food Market Revenue undefined Forecast, by Pet Food Product 2020 & 2033

- Table 20: Global Pet Food Market Revenue undefined Forecast, by Pets 2020 & 2033

- Table 21: Global Pet Food Market Revenue undefined Forecast, by Distribution Channel 2020 & 2033

- Table 22: Global Pet Food Market Revenue undefined Forecast, by Country 2020 & 2033

- Table 23: United Kingdom Pet Food Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Germany Pet Food Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: France Pet Food Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Italy Pet Food Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Spain Pet Food Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Russia Pet Food Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 29: Benelux Pet Food Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 30: Nordics Pet Food Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 31: Rest of Europe Pet Food Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Global Pet Food Market Revenue undefined Forecast, by Pet Food Product 2020 & 2033

- Table 33: Global Pet Food Market Revenue undefined Forecast, by Pets 2020 & 2033

- Table 34: Global Pet Food Market Revenue undefined Forecast, by Distribution Channel 2020 & 2033

- Table 35: Global Pet Food Market Revenue undefined Forecast, by Country 2020 & 2033

- Table 36: Turkey Pet Food Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Israel Pet Food Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 38: GCC Pet Food Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 39: North Africa Pet Food Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 40: South Africa Pet Food Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: Rest of Middle East & Africa Pet Food Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Global Pet Food Market Revenue undefined Forecast, by Pet Food Product 2020 & 2033

- Table 43: Global Pet Food Market Revenue undefined Forecast, by Pets 2020 & 2033

- Table 44: Global Pet Food Market Revenue undefined Forecast, by Distribution Channel 2020 & 2033

- Table 45: Global Pet Food Market Revenue undefined Forecast, by Country 2020 & 2033

- Table 46: China Pet Food Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 47: India Pet Food Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 48: Japan Pet Food Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 49: South Korea Pet Food Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 50: ASEAN Pet Food Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 51: Oceania Pet Food Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 52: Rest of Asia Pacific Pet Food Market Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Pet Food Market?

The projected CAGR is approximately 4.3%.

2. Which companies are prominent players in the Pet Food Market?

Key companies in the market include ADM, Schell & Kampeter Inc (Diamond Pet Foods), PLB International, Clearlake Capital Group L P (Wellness Pet Company Inc ), General Mills Inc, Heristo Aktiengesellschaft, Mars Incorporated, Nestle (Purina), Colgate-Palmolive Company (Hill's Pet Nutrition Inc ), The J M Smucker Compan.

3. What are the main segments of the Pet Food Market?

The market segments include Pet Food Product, Pets, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

Increased Demand for Meat; Initiatives By the Key Players; Focus on Animal nutrition and Health.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Shift Toward Vegan- Based Diet; Changing Raw Material Prices and Strict Government Rules to Restrict Market Growth.

8. Can you provide examples of recent developments in the market?

July 2023: Hill's Pet Nutrition introduced its new MSC (Marine Stewardship Council) certified pollock and insect protein products for pets with sensitive stomachs and skin lines. They contain vitamins, omega-3 fatty acids, and antioxidants.June 2023: Mars Incorporated launched its premium cat brand SHEBA in Canada, offering cat parents wet formulas through its SHEBA BISTRO line.May 2023: Nestle Purina launched new cat treats under the Friskies "Friskies Playfuls - treats" brand. These treats are round in shape and are available in chicken and liver and salmon and shrimp flavors for adult cats.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Pet Food Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Pet Food Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Pet Food Market?

To stay informed about further developments, trends, and reports in the Pet Food Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence