Key Insights

The neuromorphic computing chip market is set for substantial growth, propelled by the increasing demand for AI-driven solutions across various sectors. With an estimated market size of USD 125.39 billion in 2025, the sector is projected to achieve a compelling Compound Annual Growth Rate (CAGR) of 67.3% from 2025 to 2033. This accelerated expansion is attributed to the inherent advantages of neuromorphic chips, including their energy efficiency and brain-like data processing capabilities. Key applications in Artificial Intelligence, Medical Equipment, Robotics, and Communications are primary growth engines. The evolution of AI algorithms and the need for real-time processing and edge computing are creating significant opportunities for neuromorphic technology. Innovations in manufacturing, such as advanced chip architectures, are enhancing performance and accessibility.

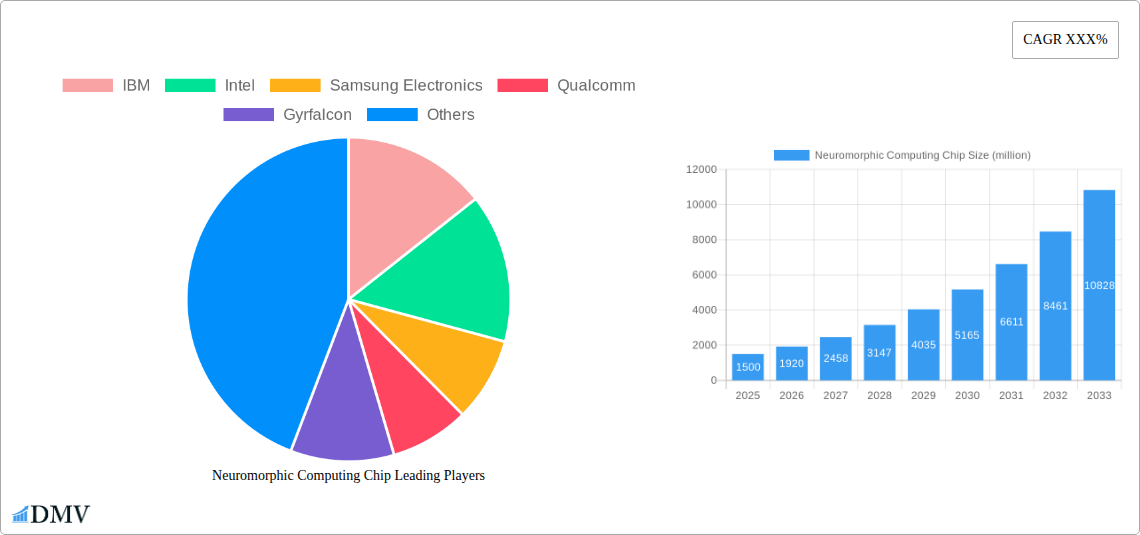

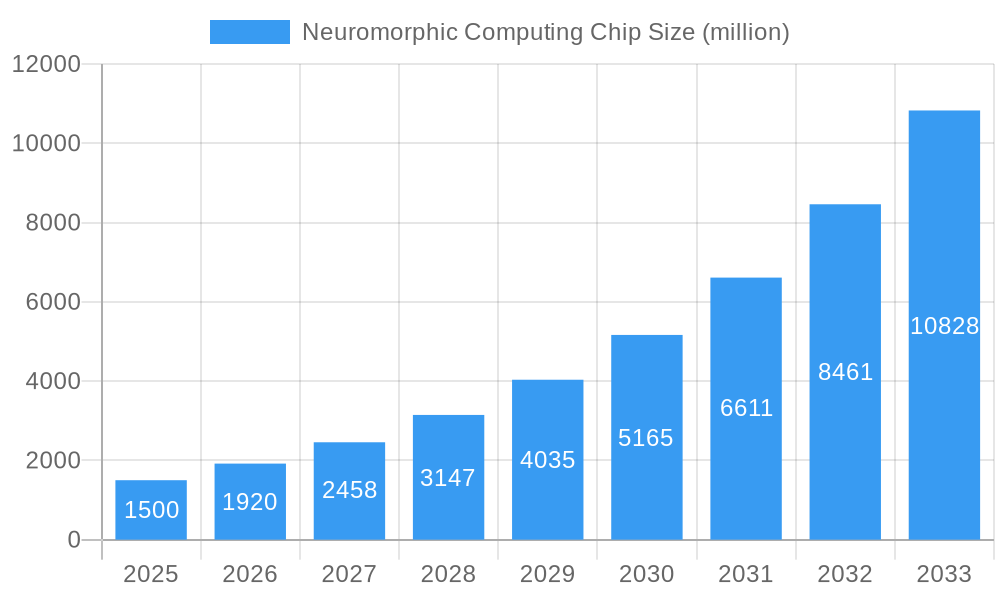

Neuromorphic Computing Chip Market Size (In Billion)

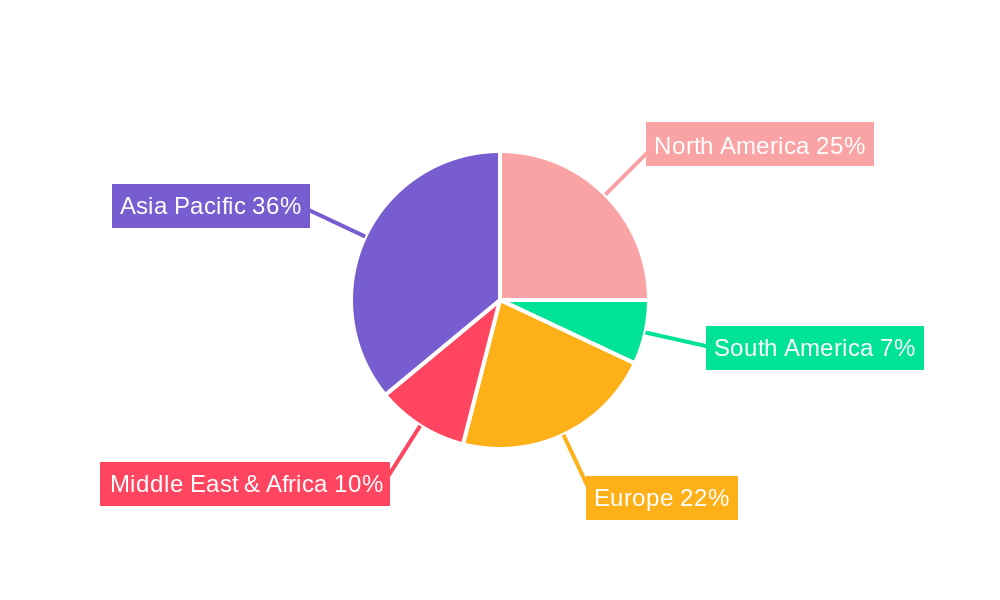

Market dynamics are shaped by both growth drivers and challenges. While AI advancements and IoT adoption are strong contributors, high initial investment and specialized expertise requirements pose hurdles. However, the shift towards brain-inspired computing and continuous innovation from industry leaders like IBM, Intel, Samsung Electronics, and Qualcomm are expected to mitigate these challenges. Emerging companies are introducing novel solutions, intensifying competition and innovation. Geographically, the Asia Pacific region, led by China and Japan, is anticipated to lead market growth, supported by robust government investment in AI R&D and manufacturing infrastructure. North America and Europe remain significant markets due to strong R&D and advanced technology adoption. The development of specialized neuromorphic chips for medical equipment and communications will be a crucial growth avenue.

Neuromorphic Computing Chip Company Market Share

Neuromorphic Computing Chip Market Composition & Trends

The global neuromorphic computing chip market is a dynamic landscape, characterized by intense innovation and strategic collaborations among industry giants and emerging innovators. Market concentration is notable, with key players like IBM, Intel, Samsung Electronics, and Qualcomm investing heavily in research and development to capture a significant share of the burgeoning Artificial Intelligence and Robotics sectors. Innovation catalysts are primarily driven by the pursuit of power-efficient, high-performance computing solutions that mimic the human brain’s architecture. This includes advancements in spiking neural networks and analog computing paradigms. The regulatory landscape, while still evolving, is increasingly focused on ethical AI development and data security, indirectly influencing the design and adoption of neuromorphic solutions. Substitute products, such as conventional GPUs and TPUs, continue to offer competition, but neuromorphic chips present a distinct advantage in low-power, real-time processing for edge AI applications. End-user profiles are diverse, ranging from Medical Equipment manufacturers seeking sophisticated diagnostic tools to the Communications Industry demanding more intelligent network infrastructure. Mergers and acquisitions (M&A) are a significant trend, with a projected total deal value of over 500 million in the historical period (2019-2024), indicating consolidation and strategic integration of specialized technologies. For instance, acquisitions of startups with unique analog neuromorphic IP are crucial for established players to accelerate their product roadmaps. The market share distribution is projected to see significant shifts, with companies demonstrating superior energy efficiency and adaptability gaining prominence by 2025.

- Market Concentration: Dominated by a few key players, with significant strategic investments in R&D.

- Innovation Catalysts: Advancements in Spiking Neural Networks (SNNs), analog computing, and ultra-low power processing.

- Regulatory Influence: Growing emphasis on ethical AI, data privacy, and responsible innovation.

- Substitute Products: Conventional GPUs, TPUs, and ASICs, presenting a competitive but differentiated market.

- End-User Segments: AI, Medical Devices, Robotics, Communications, and emerging IoT applications.

- M&A Activity: Active consolidation, with projected M&A deal values exceeding 500 million during the historical period.

Neuromorphic Computing Chip Industry Evolution

The neuromorphic computing chip industry is poised for exponential growth, fundamentally reshaping the landscape of computing by emulating the human brain's efficiency and learning capabilities. Over the study period of 2019–2033, the market is projected to witness a compound annual growth rate (CAGR) of approximately 45%, driven by escalating demand for AI acceleration at the edge and in data centers. The base year of 2025 marks a pivotal point, with the market estimated to reach a valuation of 2,500 million, a substantial increase from its nascent stages. This evolution is underpinned by relentless technological advancements, particularly in the development of novel hardware architectures that enable parallel processing and event-driven computation. For instance, the transition from traditional von Neumann architectures to in-memory computing and crossbar arrays, which are fundamental to neuromorphic design, has dramatically improved energy efficiency, with some chips achieving performance metrics of over 1,000 giga-operations per watt.

Shifting consumer demands are also a significant propellant. The proliferation of smart devices, autonomous systems, and the Internet of Things (IoT) necessitates on-device AI processing that is both power-efficient and latency-free. Neuromorphic chips are uniquely positioned to fulfill these requirements, offering the potential for continuous learning and adaptation without constant cloud connectivity. Adoption metrics are steadily rising, with early adopters in specialized fields like advanced sensor processing, real-time object recognition in robotics, and personalized medical diagnostics showing significant performance gains. The forecast period of 2025–2033 anticipates a widespread integration of neuromorphic technology across various industries, moving beyond niche applications to mainstream adoption. This growth trajectory is further fueled by substantial R&D investments, estimated to be in the billions of dollars, from leading technology firms and venture capitalists alike. The industry’s evolution is a testament to the growing recognition of the limitations of conventional computing paradigms for complex, dynamic AI tasks, and the compelling advantages offered by brain-inspired architectures.

Leading Regions, Countries, or Segments in Neuromorphic Computing Chip

The Artificial Intelligence application segment is undeniably the dominant force driving the neuromorphic computing chip market. This segment's ascendancy is fueled by the insatiable demand for intelligent systems capable of complex pattern recognition, predictive analytics, and real-time decision-making. Within AI, the use of neuromorphic chips in advanced machine learning algorithms, deep learning inference at the edge, and natural language processing applications is experiencing unprecedented growth. The inherent parallelism and energy efficiency of neuromorphic architectures make them ideal for accelerating these computationally intensive tasks, particularly in power-constrained environments like mobile devices and autonomous vehicles.

- Dominant Application Segment: Artificial Intelligence.

- Key Drivers: Exponential growth in AI research and deployment, need for energy-efficient AI inference, development of sophisticated AI algorithms.

- Impact: Drives innovation in chip design, fosters collaboration between AI researchers and hardware manufacturers.

- Market Share: Expected to command over 70% of the total neuromorphic chip market by 2025.

- Examples: Real-time object detection in autonomous driving, anomaly detection in cybersecurity, personalized recommendation engines.

In terms of chip type, the 12nm and 28nm process technologies are currently leading the market, offering a favorable balance between performance, power efficiency, and manufacturing maturity. These nodes allow for higher transistor density and improved power management, crucial for deploying neuromorphic processors in a wide range of devices.

- Leading Chip Types: 12nm and 28nm.

- Key Drivers: Established manufacturing ecosystems, cost-effectiveness, optimized performance for current neuromorphic designs.

- Impact: Facilitates wider adoption and commercialization of neuromorphic chips.

- Market Share: Combined, these nodes are projected to hold approximately 60% of the market by 2025.

- Examples: Enabling on-device AI in smartphones, smart home devices, and industrial IoT sensors.

Regionally, North America and Asia Pacific are emerging as the leading hubs for neuromorphic computing chip development and adoption. North America, particularly the United States, benefits from extensive investments in AI research from both private sector giants and government initiatives, coupled with a robust startup ecosystem. Asia Pacific, spearheaded by countries like China, South Korea, and Japan, is witnessing rapid growth driven by its massive consumer electronics market, strong manufacturing capabilities, and increasing government support for advanced semiconductor technologies. Significant investments in AI infrastructure and the rapid deployment of smart technologies are propelling the adoption of neuromorphic solutions in these regions.

- Leading Regions: North America and Asia Pacific.

- North America Drivers: Strong R&D investment, presence of major AI technology companies, supportive government policies.

- Asia Pacific Drivers: Large consumer electronics market, advanced manufacturing capabilities, rapid digitalization, government initiatives for AI adoption.

- Impact: Drive global market growth, foster strategic partnerships and supply chain development.

Neuromorphic Computing Chip Product Innovations

Neuromorphic computing chips are revolutionizing computation with unique product innovations that mimic the brain's efficiency. Innovations focus on asynchronous, event-driven processing, enabling ultra-low power consumption for edge AI. Companies are developing chips with integrated analog memory and processing elements, significantly reducing data movement and latency. Performance metrics are staggering, with some chips achieving over 1,000 giga-operations per second while consuming mere milliwatts of power, a breakthrough for battery-powered devices. Unique selling propositions include real-time learning capabilities, fault tolerance, and inherent parallelism, making them ideal for applications requiring continuous adaptation and responsiveness, such as advanced robotics and sensor fusion.

Propelling Factors for Neuromorphic Computing Chip Growth

The growth of the neuromorphic computing chip market is propelled by a confluence of powerful factors. The relentless demand for Artificial Intelligence capabilities, especially at the edge, where power and latency are critical constraints, is a primary driver. Advancements in AI algorithms, particularly spiking neural networks, are creating hardware requirements that conventional architectures struggle to meet efficiently. Economically, the increasing need for energy-efficient computing solutions in data centers and mobile devices translates to significant cost savings and environmental benefits, making neuromorphic chips an attractive proposition. Furthermore, government initiatives and funding in countries like the United States and China are accelerating research and development, fostering a competitive yet collaborative ecosystem. The development of novel materials and fabrication techniques is also enabling the creation of smaller, faster, and more power-efficient neuromorphic processors.

Obstacles in the Neuromorphic Computing Chip Market

Despite the immense potential, the neuromorphic computing chip market faces several significant obstacles. Regulatory challenges, particularly concerning the standardization and validation of novel AI hardware, can slow down adoption. The inherent complexity of neuromorphic architectures requires specialized software development tools and programming models, leading to a scarcity of skilled developers. Supply chain disruptions, especially in advanced semiconductor manufacturing, can impact production timelines and costs, affecting the availability of these highly specialized chips. Moreover, the initial high cost of development and manufacturing for niche neuromorphic solutions presents a barrier for smaller enterprises looking to integrate them, leading to competitive pressures from more established and cost-effective alternatives for certain applications.

Future Opportunities in Neuromorphic Computing Chip

The future opportunities for neuromorphic computing chips are vast and exciting. The burgeoning Internet of Things (IoT) sector presents a massive market for ultra-low-power, intelligent edge devices. Emerging technologies like brain-computer interfaces (BCIs) offer a revolutionary avenue for neuromorphic integration, enabling seamless interaction between humans and machines. The Medical Equipment industry is ripe for transformation, with neuromorphic chips enabling advanced diagnostics, personalized treatments, and intelligent prosthetics. Furthermore, advancements in materials science and quantum computing integration could unlock entirely new paradigms of neuromorphic processing, pushing performance boundaries beyond current imaginations. The increasing global focus on sustainable technology also positions neuromorphic computing as a key enabler of energy-efficient digital infrastructure.

Major Players in the Neuromorphic Computing Chip Ecosystem

- IBM

- Intel

- Samsung Electronics

- Qualcomm

- Gyrfalcon

- Eta Compute

- Westwell

- Lynxi

- DeepcreatIC

- SynSense

Key Developments in Neuromorphic Computing Chip Industry

- 2023 October: IBM announces advancements in its TrueNorth neuromorphic chip, showcasing improved learning capabilities for AI inference.

- 2023 September: Intel unveils its latest generation of neuromorphic hardware, focusing on enhanced scalability and energy efficiency for enterprise AI solutions.

- 2023 July: Samsung Electronics showcases a novel neuromorphic chip design integrated into its mobile processors, enabling on-device AI for consumer electronics.

- 2023 May: Qualcomm introduces new neuromorphic IP for its Snapdragon platforms, targeting enhanced AI processing in smartphones and IoT devices.

- 2023 March: Gyrfalcon demonstrates its latest AI accelerator chips optimized for neuromorphic workloads, achieving industry-leading performance per watt.

- 2023 January: Eta Compute releases a new generation of low-power neuromorphic microcontrollers for edge AI applications in smart sensors and wearables.

- 2022 November: Westwell introduces a neuromorphic-powered autonomous driving system, demonstrating real-time perception and decision-making capabilities.

- 2022 August: Lynxi develops a novel spiking neural network simulator, accelerating the development and testing of neuromorphic algorithms.

- 2022 June: DeepcreatIC announces a breakthrough in analog neuromorphic circuit design, promising unprecedented energy efficiency.

- 2022 April: SynSense introduces its event-driven vision sensor integrated with a neuromorphic processor for real-time image processing with minimal power consumption.

Strategic Neuromorphic Computing Chip Market Forecast

The strategic forecast for the neuromorphic computing chip market is exceptionally positive, driven by the intrinsic advantages these chips offer for the future of Artificial Intelligence. As AI applications become more pervasive and demand for edge computing intensifies, neuromorphic processors are poised to become indispensable. The increasing focus on energy efficiency and the limitations of traditional computing architectures for complex neural processing will continue to fuel market expansion. Emerging opportunities in areas like advanced robotics, autonomous systems, and next-generation medical devices will further solidify the market's growth trajectory. Investments in R&D and the ongoing development of more accessible software tools will pave the way for wider adoption, making the market’s potential in the coming decade substantial.

Neuromorphic Computing Chip Segmentation

-

1. Application

- 1.1. Artificial Intelligence

- 1.2. Medical Equipment

- 1.3. Robot

- 1.4. Communications Industry

- 1.5. Other

-

2. Type

- 2.1. 12nm

- 2.2. 28nm

- 2.3. Others

Neuromorphic Computing Chip Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Neuromorphic Computing Chip Regional Market Share

Geographic Coverage of Neuromorphic Computing Chip

Neuromorphic Computing Chip REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 67.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Artificial Intelligence

- 5.1.2. Medical Equipment

- 5.1.3. Robot

- 5.1.4. Communications Industry

- 5.1.5. Other

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. 12nm

- 5.2.2. 28nm

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Neuromorphic Computing Chip Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Artificial Intelligence

- 6.1.2. Medical Equipment

- 6.1.3. Robot

- 6.1.4. Communications Industry

- 6.1.5. Other

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. 12nm

- 6.2.2. 28nm

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Neuromorphic Computing Chip Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Artificial Intelligence

- 7.1.2. Medical Equipment

- 7.1.3. Robot

- 7.1.4. Communications Industry

- 7.1.5. Other

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. 12nm

- 7.2.2. 28nm

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Neuromorphic Computing Chip Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Artificial Intelligence

- 8.1.2. Medical Equipment

- 8.1.3. Robot

- 8.1.4. Communications Industry

- 8.1.5. Other

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. 12nm

- 8.2.2. 28nm

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Neuromorphic Computing Chip Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Artificial Intelligence

- 9.1.2. Medical Equipment

- 9.1.3. Robot

- 9.1.4. Communications Industry

- 9.1.5. Other

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. 12nm

- 9.2.2. 28nm

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Neuromorphic Computing Chip Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Artificial Intelligence

- 10.1.2. Medical Equipment

- 10.1.3. Robot

- 10.1.4. Communications Industry

- 10.1.5. Other

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. 12nm

- 10.2.2. 28nm

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Neuromorphic Computing Chip Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Artificial Intelligence

- 11.1.2. Medical Equipment

- 11.1.3. Robot

- 11.1.4. Communications Industry

- 11.1.5. Other

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. 12nm

- 11.2.2. 28nm

- 11.2.3. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 IBM

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Intel

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Samsung Electronics

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Qualcomm

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Gyrfalcon

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Eta Compute

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Westwell

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Lynxi

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 DeepcreatIC

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 SynSense

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 IBM

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Neuromorphic Computing Chip Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Neuromorphic Computing Chip Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Neuromorphic Computing Chip Revenue (billion), by Application 2025 & 2033

- Figure 4: North America Neuromorphic Computing Chip Volume (K), by Application 2025 & 2033

- Figure 5: North America Neuromorphic Computing Chip Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Neuromorphic Computing Chip Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Neuromorphic Computing Chip Revenue (billion), by Type 2025 & 2033

- Figure 8: North America Neuromorphic Computing Chip Volume (K), by Type 2025 & 2033

- Figure 9: North America Neuromorphic Computing Chip Revenue Share (%), by Type 2025 & 2033

- Figure 10: North America Neuromorphic Computing Chip Volume Share (%), by Type 2025 & 2033

- Figure 11: North America Neuromorphic Computing Chip Revenue (billion), by Country 2025 & 2033

- Figure 12: North America Neuromorphic Computing Chip Volume (K), by Country 2025 & 2033

- Figure 13: North America Neuromorphic Computing Chip Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Neuromorphic Computing Chip Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Neuromorphic Computing Chip Revenue (billion), by Application 2025 & 2033

- Figure 16: South America Neuromorphic Computing Chip Volume (K), by Application 2025 & 2033

- Figure 17: South America Neuromorphic Computing Chip Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Neuromorphic Computing Chip Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Neuromorphic Computing Chip Revenue (billion), by Type 2025 & 2033

- Figure 20: South America Neuromorphic Computing Chip Volume (K), by Type 2025 & 2033

- Figure 21: South America Neuromorphic Computing Chip Revenue Share (%), by Type 2025 & 2033

- Figure 22: South America Neuromorphic Computing Chip Volume Share (%), by Type 2025 & 2033

- Figure 23: South America Neuromorphic Computing Chip Revenue (billion), by Country 2025 & 2033

- Figure 24: South America Neuromorphic Computing Chip Volume (K), by Country 2025 & 2033

- Figure 25: South America Neuromorphic Computing Chip Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Neuromorphic Computing Chip Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Neuromorphic Computing Chip Revenue (billion), by Application 2025 & 2033

- Figure 28: Europe Neuromorphic Computing Chip Volume (K), by Application 2025 & 2033

- Figure 29: Europe Neuromorphic Computing Chip Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Neuromorphic Computing Chip Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Neuromorphic Computing Chip Revenue (billion), by Type 2025 & 2033

- Figure 32: Europe Neuromorphic Computing Chip Volume (K), by Type 2025 & 2033

- Figure 33: Europe Neuromorphic Computing Chip Revenue Share (%), by Type 2025 & 2033

- Figure 34: Europe Neuromorphic Computing Chip Volume Share (%), by Type 2025 & 2033

- Figure 35: Europe Neuromorphic Computing Chip Revenue (billion), by Country 2025 & 2033

- Figure 36: Europe Neuromorphic Computing Chip Volume (K), by Country 2025 & 2033

- Figure 37: Europe Neuromorphic Computing Chip Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Neuromorphic Computing Chip Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Neuromorphic Computing Chip Revenue (billion), by Application 2025 & 2033

- Figure 40: Middle East & Africa Neuromorphic Computing Chip Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Neuromorphic Computing Chip Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Neuromorphic Computing Chip Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Neuromorphic Computing Chip Revenue (billion), by Type 2025 & 2033

- Figure 44: Middle East & Africa Neuromorphic Computing Chip Volume (K), by Type 2025 & 2033

- Figure 45: Middle East & Africa Neuromorphic Computing Chip Revenue Share (%), by Type 2025 & 2033

- Figure 46: Middle East & Africa Neuromorphic Computing Chip Volume Share (%), by Type 2025 & 2033

- Figure 47: Middle East & Africa Neuromorphic Computing Chip Revenue (billion), by Country 2025 & 2033

- Figure 48: Middle East & Africa Neuromorphic Computing Chip Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Neuromorphic Computing Chip Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Neuromorphic Computing Chip Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Neuromorphic Computing Chip Revenue (billion), by Application 2025 & 2033

- Figure 52: Asia Pacific Neuromorphic Computing Chip Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Neuromorphic Computing Chip Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Neuromorphic Computing Chip Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Neuromorphic Computing Chip Revenue (billion), by Type 2025 & 2033

- Figure 56: Asia Pacific Neuromorphic Computing Chip Volume (K), by Type 2025 & 2033

- Figure 57: Asia Pacific Neuromorphic Computing Chip Revenue Share (%), by Type 2025 & 2033

- Figure 58: Asia Pacific Neuromorphic Computing Chip Volume Share (%), by Type 2025 & 2033

- Figure 59: Asia Pacific Neuromorphic Computing Chip Revenue (billion), by Country 2025 & 2033

- Figure 60: Asia Pacific Neuromorphic Computing Chip Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Neuromorphic Computing Chip Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Neuromorphic Computing Chip Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Neuromorphic Computing Chip Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Neuromorphic Computing Chip Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Neuromorphic Computing Chip Revenue billion Forecast, by Type 2020 & 2033

- Table 4: Global Neuromorphic Computing Chip Volume K Forecast, by Type 2020 & 2033

- Table 5: Global Neuromorphic Computing Chip Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Neuromorphic Computing Chip Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Neuromorphic Computing Chip Revenue billion Forecast, by Application 2020 & 2033

- Table 8: Global Neuromorphic Computing Chip Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Neuromorphic Computing Chip Revenue billion Forecast, by Type 2020 & 2033

- Table 10: Global Neuromorphic Computing Chip Volume K Forecast, by Type 2020 & 2033

- Table 11: Global Neuromorphic Computing Chip Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global Neuromorphic Computing Chip Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Neuromorphic Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United States Neuromorphic Computing Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Neuromorphic Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Neuromorphic Computing Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Neuromorphic Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Mexico Neuromorphic Computing Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Neuromorphic Computing Chip Revenue billion Forecast, by Application 2020 & 2033

- Table 20: Global Neuromorphic Computing Chip Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Neuromorphic Computing Chip Revenue billion Forecast, by Type 2020 & 2033

- Table 22: Global Neuromorphic Computing Chip Volume K Forecast, by Type 2020 & 2033

- Table 23: Global Neuromorphic Computing Chip Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global Neuromorphic Computing Chip Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Neuromorphic Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Brazil Neuromorphic Computing Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Neuromorphic Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Argentina Neuromorphic Computing Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Neuromorphic Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Neuromorphic Computing Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Neuromorphic Computing Chip Revenue billion Forecast, by Application 2020 & 2033

- Table 32: Global Neuromorphic Computing Chip Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Neuromorphic Computing Chip Revenue billion Forecast, by Type 2020 & 2033

- Table 34: Global Neuromorphic Computing Chip Volume K Forecast, by Type 2020 & 2033

- Table 35: Global Neuromorphic Computing Chip Revenue billion Forecast, by Country 2020 & 2033

- Table 36: Global Neuromorphic Computing Chip Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Neuromorphic Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Neuromorphic Computing Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Neuromorphic Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Germany Neuromorphic Computing Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Neuromorphic Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: France Neuromorphic Computing Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Neuromorphic Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Italy Neuromorphic Computing Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Neuromorphic Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Spain Neuromorphic Computing Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Neuromorphic Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Russia Neuromorphic Computing Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Neuromorphic Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: Benelux Neuromorphic Computing Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Neuromorphic Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Nordics Neuromorphic Computing Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Neuromorphic Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Neuromorphic Computing Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Neuromorphic Computing Chip Revenue billion Forecast, by Application 2020 & 2033

- Table 56: Global Neuromorphic Computing Chip Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Neuromorphic Computing Chip Revenue billion Forecast, by Type 2020 & 2033

- Table 58: Global Neuromorphic Computing Chip Volume K Forecast, by Type 2020 & 2033

- Table 59: Global Neuromorphic Computing Chip Revenue billion Forecast, by Country 2020 & 2033

- Table 60: Global Neuromorphic Computing Chip Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Neuromorphic Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Turkey Neuromorphic Computing Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Neuromorphic Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Israel Neuromorphic Computing Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Neuromorphic Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: GCC Neuromorphic Computing Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Neuromorphic Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 68: North Africa Neuromorphic Computing Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Neuromorphic Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 70: South Africa Neuromorphic Computing Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Neuromorphic Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Neuromorphic Computing Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Neuromorphic Computing Chip Revenue billion Forecast, by Application 2020 & 2033

- Table 74: Global Neuromorphic Computing Chip Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Neuromorphic Computing Chip Revenue billion Forecast, by Type 2020 & 2033

- Table 76: Global Neuromorphic Computing Chip Volume K Forecast, by Type 2020 & 2033

- Table 77: Global Neuromorphic Computing Chip Revenue billion Forecast, by Country 2020 & 2033

- Table 78: Global Neuromorphic Computing Chip Volume K Forecast, by Country 2020 & 2033

- Table 79: China Neuromorphic Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 80: China Neuromorphic Computing Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Neuromorphic Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 82: India Neuromorphic Computing Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Neuromorphic Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 84: Japan Neuromorphic Computing Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Neuromorphic Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 86: South Korea Neuromorphic Computing Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Neuromorphic Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Neuromorphic Computing Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Neuromorphic Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 90: Oceania Neuromorphic Computing Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Neuromorphic Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Neuromorphic Computing Chip Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Neuromorphic Computing Chip?

The projected CAGR is approximately 67.3%.

2. Which companies are prominent players in the Neuromorphic Computing Chip?

Key companies in the market include IBM, Intel, Samsung Electronics, Qualcomm, Gyrfalcon, Eta Compute, Westwell, Lynxi, DeepcreatIC, SynSense.

3. What are the main segments of the Neuromorphic Computing Chip?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 125.39 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Neuromorphic Computing Chip," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Neuromorphic Computing Chip report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Neuromorphic Computing Chip?

To stay informed about further developments, trends, and reports in the Neuromorphic Computing Chip, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence