Key Insights

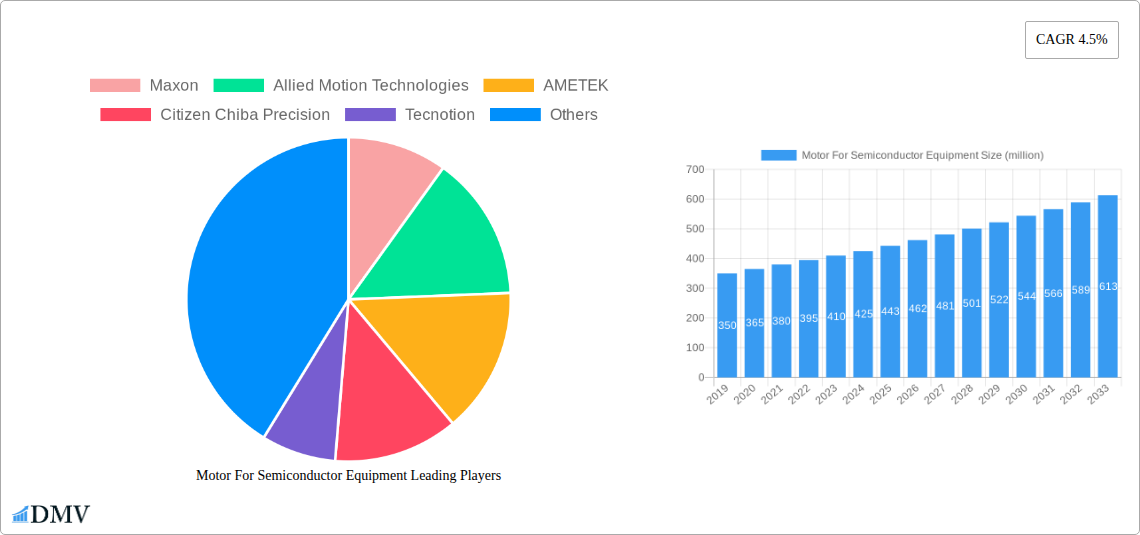

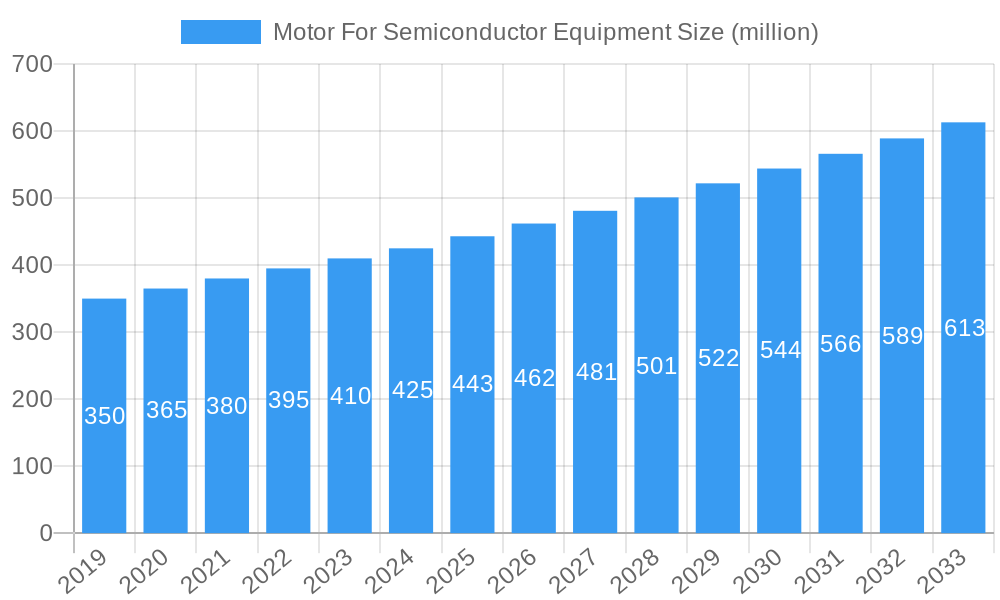

The global market for Motors for Semiconductor Equipment is poised for robust growth, projected to reach an estimated $443 million by 2025. This significant expansion is driven by a Compound Annual Growth Rate (CAGR) of 4.5% over the forecast period of 2025-2033. The escalating demand for advanced semiconductor devices, fueled by the proliferation of 5G technology, artificial intelligence, and the Internet of Things (IoT), is the primary catalyst for this market's upward trajectory. As semiconductor manufacturers strive to produce increasingly complex and miniaturized chips, the need for high-precision, reliable, and efficient motors for critical equipment like lithography machines, wafer inspection systems, thin-film deposition tools, and etching machines becomes paramount. Innovations in motor technology, including the development of coreless and brushless motors offering superior control, speed, and reduced thermal effects, are also key drivers. Furthermore, the ongoing trend of increased automation in semiconductor manufacturing processes necessitates sophisticated motor solutions to ensure seamless operation and enhanced throughput.

Motor For Semiconductor Equipment Market Size (In Million)

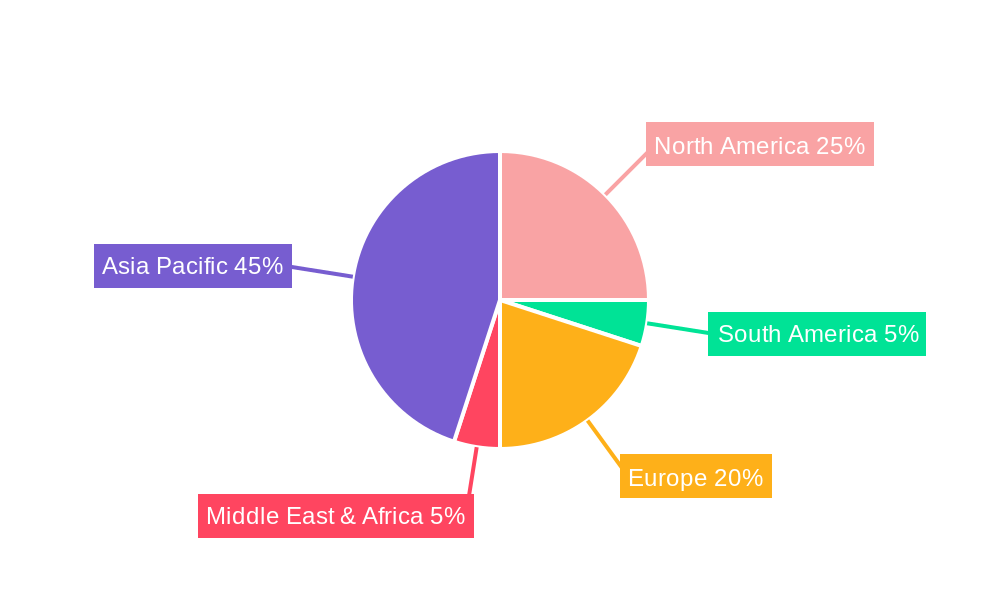

However, certain factors may moderate this growth. The high capital expenditure required for semiconductor manufacturing facilities and the associated equipment, including advanced motor systems, can present a significant barrier to entry for new players and may lead to slower adoption in price-sensitive markets. Additionally, the intricate supply chains and potential geopolitical instabilities can disrupt the availability of raw materials and components, impacting production and costs. Despite these challenges, the market is expected to witness significant expansion in the Asia Pacific region, particularly in China and South Korea, owing to their dominant positions in semiconductor manufacturing and increasing investments in advanced technologies. North America and Europe are also anticipated to contribute substantially to market growth, driven by technological advancements and a strong presence of leading semiconductor equipment manufacturers. The dominant applications are expected to be Lithography Machines and Wafer Inspection Equipment, followed by Thin Film Deposition and Etching Machines, all of which rely heavily on precise motor control.

Motor For Semiconductor Equipment Company Market Share

This in-depth report, "Motor For Semiconductor Equipment Market: Global Outlook & Forecast 2025-2033," delivers critical insights into the dynamic landscape of motors essential for semiconductor manufacturing. Leveraging robust data and expert analysis, this study provides a detailed examination of market composition, industry evolution, regional dominance, product innovations, growth drivers, obstacles, future opportunities, and key players. With a study period spanning 2019–2033, a base year of 2025, and a forecast period of 2025–2033, this report is an indispensable resource for stakeholders seeking to understand and capitalize on the burgeoning demand for high-performance motors in the semiconductor industry.

Motor For Semiconductor Equipment Market Composition & Trends

The global Motor for Semiconductor Equipment market exhibits a moderately consolidated structure, with a few key players dominating significant market share. Innovation remains a primary catalyst, driven by the relentless pursuit of miniaturization, increased precision, and enhanced throughput in semiconductor fabrication processes. Regulatory landscapes, particularly concerning energy efficiency and material compliance, are increasingly shaping product development and adoption. The availability of advanced materials and sophisticated manufacturing techniques has also been instrumental in driving innovation. Substitute products, while present in less demanding applications, struggle to match the stringent performance requirements of core semiconductor equipment. End-user profiles are highly specialized, encompassing Original Equipment Manufacturers (OEMs) of lithography machines, wafer inspection equipment, thin-film deposition equipment, etching machines, ion implanters, and other critical fabrication tools. Mergers and Acquisitions (M&A) activity, valued at approximately $500 million to $800 million annually, plays a crucial role in market consolidation and the acquisition of specialized technologies.

- Market Share Distribution: Leading manufacturers hold a combined market share of approximately 60%, with specialized niche players contributing to the remaining 40%.

- M&A Deal Values: Recent M&A transactions have ranged from $50 million to $200 million, focusing on acquiring intellectual property in high-precision motor technology.

- Innovation Catalysts: Advancements in rare-earth magnet technology and encoder systems are key drivers of product improvement.

- Regulatory Landscape: Emerging environmental regulations in regions like Europe and North America are pushing for motors with higher energy efficiency ratings.

Motor For Semiconductor Equipment Industry Evolution

The Motor for Semiconductor Equipment industry has witnessed remarkable evolution over the historical period of 2019-2024, characterized by consistent year-on-year growth exceeding 8%. This upward trajectory is largely attributed to the exponential increase in demand for advanced semiconductors across diverse sectors, including consumer electronics, automotive, telecommunications, and artificial intelligence. Technological advancements have been at the forefront of this evolution, with a significant shift towards brushless DC motors and AC servo motors due to their superior precision, speed control, and longevity. Coreless motor technology has also gained traction for applications demanding extremely low inertia and high dynamic response, critical for complex wafer handling and precise positioning within lithography machines.

The demand for motors capable of operating in vacuum environments, with ultra-low particle generation and extreme thermal stability, has driven innovation in motor design, materials, and sealing technologies. Furthermore, the increasing complexity of semiconductor manufacturing processes, such as advanced lithography techniques requiring sub-nanometer precision, has necessitated the development of highly integrated motor-driven systems with sophisticated feedback mechanisms. Consumer demand for increasingly powerful and energy-efficient electronic devices directly translates to a higher demand for the semiconductor chips that power them, thereby fueling the growth of the semiconductor equipment market and, consequently, the motor segment.

- Market Growth Trajectories: The market has experienced a compound annual growth rate (CAGR) of approximately 9.5% during the historical period.

- Technological Advancements: The adoption rate of advanced brushless motor technologies has surged by over 70% since 2019.

- Shifting Consumer Demands: The proliferation of 5G technology and the rise of AI have significantly boosted demand for high-performance computing, directly impacting semiconductor production volumes.

- Adoption Metrics: The market share of AC servo motors in wafer inspection equipment has grown from 30% in 2019 to an estimated 55% by 2024.

- Investment Trends: Global investment in semiconductor fabrication plants has exceeded $100 billion, creating substantial demand for new equipment and associated components.

Leading Regions, Countries, or Segments in Motor For Semiconductor Equipment

The Lithography Machine application segment stands as the undisputed leader within the Motor for Semiconductor Equipment market, driven by its paramount importance in defining the intricate patterns on semiconductor wafers. This segment commands a substantial market share, estimated at over 35% of the total application market. The demand for lithography motors is intrinsically linked to the technological advancements in semiconductor nodes, with each new generation requiring increasingly sophisticated and precise motor control.

- Dominant Application Segment: Lithography Machines, due to their critical role in defining chip architectures and the ongoing need for sub-nanometer precision.

- Key Drivers in Lithography:

- Investment Trends: Significant global investments in EUV (Extreme Ultraviolet) lithography technology, estimated at over $20 billion in the last three years, directly boost demand for specialized motors.

- Regulatory Support: Government initiatives and incentives in countries like South Korea, Taiwan, and the United States to bolster domestic semiconductor manufacturing capabilities.

- Technological Advancements: The transition to smaller process nodes (e.g., 3nm, 2nm) necessitates motors with unprecedented precision, low vibration, and high dynamic response.

- Dominant Motor Type within Lithography: Brushless Motors, particularly high-performance AC Servo Motors, are favored for their precision, speed, and torque control capabilities, essential for the rapid and accurate movement of wafer stages. The market share of AC Servo Motors in lithography applications is projected to reach 70% by 2025.

- Geographic Influence: East Asia, particularly Taiwan, South Korea, and Japan, represents the largest consuming region for motors in lithography equipment, driven by the presence of major chip manufacturers. The estimated market value for motors in this segment in East Asia alone exceeds $1.5 billion annually.

Motor For Semiconductor Equipment Product Innovations

Recent product innovations in the Motor for Semiconductor Equipment sector are revolutionizing precision manufacturing. Companies are developing ultra-compact, high-torque density motors with integrated advanced encoder systems for sub-micron positioning accuracy. Innovations in materials, such as advanced ceramic bearings and low-outgassing composites, are enabling motors to perform reliably in ultra-high vacuum (UHV) environments crucial for thin-film deposition and etching. Furthermore, the integration of intelligent control algorithms and predictive maintenance capabilities is enhancing operational efficiency and reducing downtime. These advancements are directly contributing to higher wafer yields and faster fabrication cycles, with performance improvements often exceeding 15% in terms of speed and precision.

Propelling Factors for Motor For Semiconductor Equipment Growth

The Motor for Semiconductor Equipment market is propelled by a confluence of robust growth factors. The insatiable global demand for advanced semiconductors, driven by emerging technologies like 5G, AI, and IoT, directly fuels the need for more sophisticated fabrication equipment. Technological advancements in motor design, including higher precision, increased speed, and enhanced reliability, are critical enablers of next-generation chip manufacturing. Government initiatives and substantial investments aimed at reshoring semiconductor production and fostering technological sovereignty in key regions are creating significant market expansion opportunities. The continuous drive for miniaturization and improved performance in electronic devices also necessitates increasingly complex and precise semiconductor manufacturing processes, thereby boosting demand for specialized motors.

Obstacles in the Motor For Semiconductor Equipment Market

Despite its robust growth, the Motor for Semiconductor Equipment market faces several significant obstacles. Stringent regulatory compliance, particularly regarding environmental standards and material sourcing, can increase manufacturing costs and lead times. Supply chain disruptions, as witnessed in recent years, can impact the availability of critical components and raw materials, leading to production delays and price volatility. Intense competitive pressures among established players and emerging niche manufacturers can lead to price erosion in certain segments. Furthermore, the high cost of research and development for cutting-edge motor technologies can act as a barrier to entry for smaller companies. The lead time for specialized motors, often ranging from 6 to 12 months, can also pose a challenge in meeting rapidly evolving equipment production schedules.

Future Opportunities in Motor For Semiconductor Equipment

Emerging opportunities in the Motor for Semiconductor Equipment market are abundant and poised for significant growth. The expanding market for advanced packaging technologies, requiring highly precise pick-and-place and inspection equipment, presents a substantial opportunity for specialized motors. The increasing adoption of AI and machine learning in semiconductor design and manufacturing creates a demand for more powerful and specialized computing chips, driving further investment in fabrication equipment. The development of next-generation lithography techniques, such as directed self-assembly and multi-beam electron lithography, will necessitate the innovation of novel motor solutions. Furthermore, the growing focus on sustainable manufacturing practices is creating opportunities for energy-efficient motor designs and advanced material solutions, estimated to open up a new market segment valued at over $300 million by 2030.

Major Players in the Motor For Semiconductor Equipment Ecosystem

- Maxon

- Allied Motion Technologies

- AMETEK

- Citizen Chiba Precision

- Tecnotion

- Lin Engineering

- Oriental Motor

Key Developments in Motor For Semiconductor Equipment Industry

- 2024/03: Oriental Motor launched a new series of high-precision stepper motors with enhanced torque and reduced vibration for wafer handling applications.

- 2023/11: AMETEK acquired a leading provider of advanced motion control systems, further strengthening its portfolio for semiconductor equipment.

- 2023/07: Tecnotion introduced a new direct-drive linear motor designed for ultra-high vacuum (UHV) environments, enabling improved wafer inspection accuracy.

- 2022/10: Allied Motion Technologies announced significant investments in R&D for next-generation brushless motors to support advanced lithography demands.

- 2022/05: Maxon unveiled a new generation of miniature coreless motors with exceptional speed and precision, targeting miniaturized semiconductor equipment.

- 2021/09: Lin Engineering expanded its custom motor design capabilities to cater to bespoke requirements for ion implanter equipment.

- 2020/04: Citizen Chiba Precision introduced a new range of compact servo motors optimized for space-constrained thin-film deposition systems.

Strategic Motor For Semiconductor Equipment Market Forecast

The strategic outlook for the Motor for Semiconductor Equipment market remains exceptionally positive, with strong growth anticipated throughout the forecast period of 2025-2033. The relentless pace of technological advancement in the semiconductor industry, coupled with increasing global demand for chips, will continue to be the primary growth catalyst. Key opportunities lie in catering to the evolving needs of lithography, wafer inspection, and thin-film deposition equipment, demanding higher precision, speed, and reliability. Investments in next-generation semiconductor manufacturing technologies and the ongoing trend of semiconductor production expansion in various regions will further bolster market expansion. The market is projected to reach a value exceeding $10 billion by 2033, driven by innovation and the critical role these motors play in enabling the future of electronics.

Motor For Semiconductor Equipment Segmentation

-

1. Application

- 1.1. Lithography Machine

- 1.2. Wafer Inspection Equipment

- 1.3. Thin Film Deposition Equipment

- 1.4. Etching Machine

- 1.5. Ion Implanter

- 1.6. Others

-

2. Type

- 2.1. Coreless Motors

- 2.2. Brushless Motors

- 2.3. AC Servo Motors

- 2.4. Others

Motor For Semiconductor Equipment Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Motor For Semiconductor Equipment Regional Market Share

Geographic Coverage of Motor For Semiconductor Equipment

Motor For Semiconductor Equipment REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Lithography Machine

- 5.1.2. Wafer Inspection Equipment

- 5.1.3. Thin Film Deposition Equipment

- 5.1.4. Etching Machine

- 5.1.5. Ion Implanter

- 5.1.6. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Coreless Motors

- 5.2.2. Brushless Motors

- 5.2.3. AC Servo Motors

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Motor For Semiconductor Equipment Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Lithography Machine

- 6.1.2. Wafer Inspection Equipment

- 6.1.3. Thin Film Deposition Equipment

- 6.1.4. Etching Machine

- 6.1.5. Ion Implanter

- 6.1.6. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Coreless Motors

- 6.2.2. Brushless Motors

- 6.2.3. AC Servo Motors

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Motor For Semiconductor Equipment Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Lithography Machine

- 7.1.2. Wafer Inspection Equipment

- 7.1.3. Thin Film Deposition Equipment

- 7.1.4. Etching Machine

- 7.1.5. Ion Implanter

- 7.1.6. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Coreless Motors

- 7.2.2. Brushless Motors

- 7.2.3. AC Servo Motors

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Motor For Semiconductor Equipment Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Lithography Machine

- 8.1.2. Wafer Inspection Equipment

- 8.1.3. Thin Film Deposition Equipment

- 8.1.4. Etching Machine

- 8.1.5. Ion Implanter

- 8.1.6. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Coreless Motors

- 8.2.2. Brushless Motors

- 8.2.3. AC Servo Motors

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Motor For Semiconductor Equipment Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Lithography Machine

- 9.1.2. Wafer Inspection Equipment

- 9.1.3. Thin Film Deposition Equipment

- 9.1.4. Etching Machine

- 9.1.5. Ion Implanter

- 9.1.6. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Coreless Motors

- 9.2.2. Brushless Motors

- 9.2.3. AC Servo Motors

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Motor For Semiconductor Equipment Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Lithography Machine

- 10.1.2. Wafer Inspection Equipment

- 10.1.3. Thin Film Deposition Equipment

- 10.1.4. Etching Machine

- 10.1.5. Ion Implanter

- 10.1.6. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Coreless Motors

- 10.2.2. Brushless Motors

- 10.2.3. AC Servo Motors

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Motor For Semiconductor Equipment Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Lithography Machine

- 11.1.2. Wafer Inspection Equipment

- 11.1.3. Thin Film Deposition Equipment

- 11.1.4. Etching Machine

- 11.1.5. Ion Implanter

- 11.1.6. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Coreless Motors

- 11.2.2. Brushless Motors

- 11.2.3. AC Servo Motors

- 11.2.4. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Maxon

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Allied Motion Technologies

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 AMETEK

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Citizen Chiba Precision

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Tecnotion

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Lin Engineering

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Oriental Motor

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.1 Maxon

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Motor For Semiconductor Equipment Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Motor For Semiconductor Equipment Revenue (million), by Application 2025 & 2033

- Figure 3: North America Motor For Semiconductor Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Motor For Semiconductor Equipment Revenue (million), by Type 2025 & 2033

- Figure 5: North America Motor For Semiconductor Equipment Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Motor For Semiconductor Equipment Revenue (million), by Country 2025 & 2033

- Figure 7: North America Motor For Semiconductor Equipment Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Motor For Semiconductor Equipment Revenue (million), by Application 2025 & 2033

- Figure 9: South America Motor For Semiconductor Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Motor For Semiconductor Equipment Revenue (million), by Type 2025 & 2033

- Figure 11: South America Motor For Semiconductor Equipment Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Motor For Semiconductor Equipment Revenue (million), by Country 2025 & 2033

- Figure 13: South America Motor For Semiconductor Equipment Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Motor For Semiconductor Equipment Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Motor For Semiconductor Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Motor For Semiconductor Equipment Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Motor For Semiconductor Equipment Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Motor For Semiconductor Equipment Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Motor For Semiconductor Equipment Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Motor For Semiconductor Equipment Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Motor For Semiconductor Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Motor For Semiconductor Equipment Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Motor For Semiconductor Equipment Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Motor For Semiconductor Equipment Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Motor For Semiconductor Equipment Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Motor For Semiconductor Equipment Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Motor For Semiconductor Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Motor For Semiconductor Equipment Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Motor For Semiconductor Equipment Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Motor For Semiconductor Equipment Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Motor For Semiconductor Equipment Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Motor For Semiconductor Equipment Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Motor For Semiconductor Equipment Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Motor For Semiconductor Equipment Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Motor For Semiconductor Equipment Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Motor For Semiconductor Equipment Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Motor For Semiconductor Equipment Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Motor For Semiconductor Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Motor For Semiconductor Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Motor For Semiconductor Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Motor For Semiconductor Equipment Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Motor For Semiconductor Equipment Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Motor For Semiconductor Equipment Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Motor For Semiconductor Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Motor For Semiconductor Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Motor For Semiconductor Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Motor For Semiconductor Equipment Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Motor For Semiconductor Equipment Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Motor For Semiconductor Equipment Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Motor For Semiconductor Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Motor For Semiconductor Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Motor For Semiconductor Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Motor For Semiconductor Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Motor For Semiconductor Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Motor For Semiconductor Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Motor For Semiconductor Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Motor For Semiconductor Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Motor For Semiconductor Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Motor For Semiconductor Equipment Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Motor For Semiconductor Equipment Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Motor For Semiconductor Equipment Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Motor For Semiconductor Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Motor For Semiconductor Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Motor For Semiconductor Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Motor For Semiconductor Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Motor For Semiconductor Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Motor For Semiconductor Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Motor For Semiconductor Equipment Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Motor For Semiconductor Equipment Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Motor For Semiconductor Equipment Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Motor For Semiconductor Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Motor For Semiconductor Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Motor For Semiconductor Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Motor For Semiconductor Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Motor For Semiconductor Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Motor For Semiconductor Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Motor For Semiconductor Equipment Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Motor For Semiconductor Equipment?

The projected CAGR is approximately 4.5%.

2. Which companies are prominent players in the Motor For Semiconductor Equipment?

Key companies in the market include Maxon, Allied Motion Technologies, AMETEK, Citizen Chiba Precision, Tecnotion, Lin Engineering, Oriental Motor.

3. What are the main segments of the Motor For Semiconductor Equipment?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 443 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Motor For Semiconductor Equipment," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Motor For Semiconductor Equipment report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Motor For Semiconductor Equipment?

To stay informed about further developments, trends, and reports in the Motor For Semiconductor Equipment, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence