Key Insights into Mobile Satellite Services Market

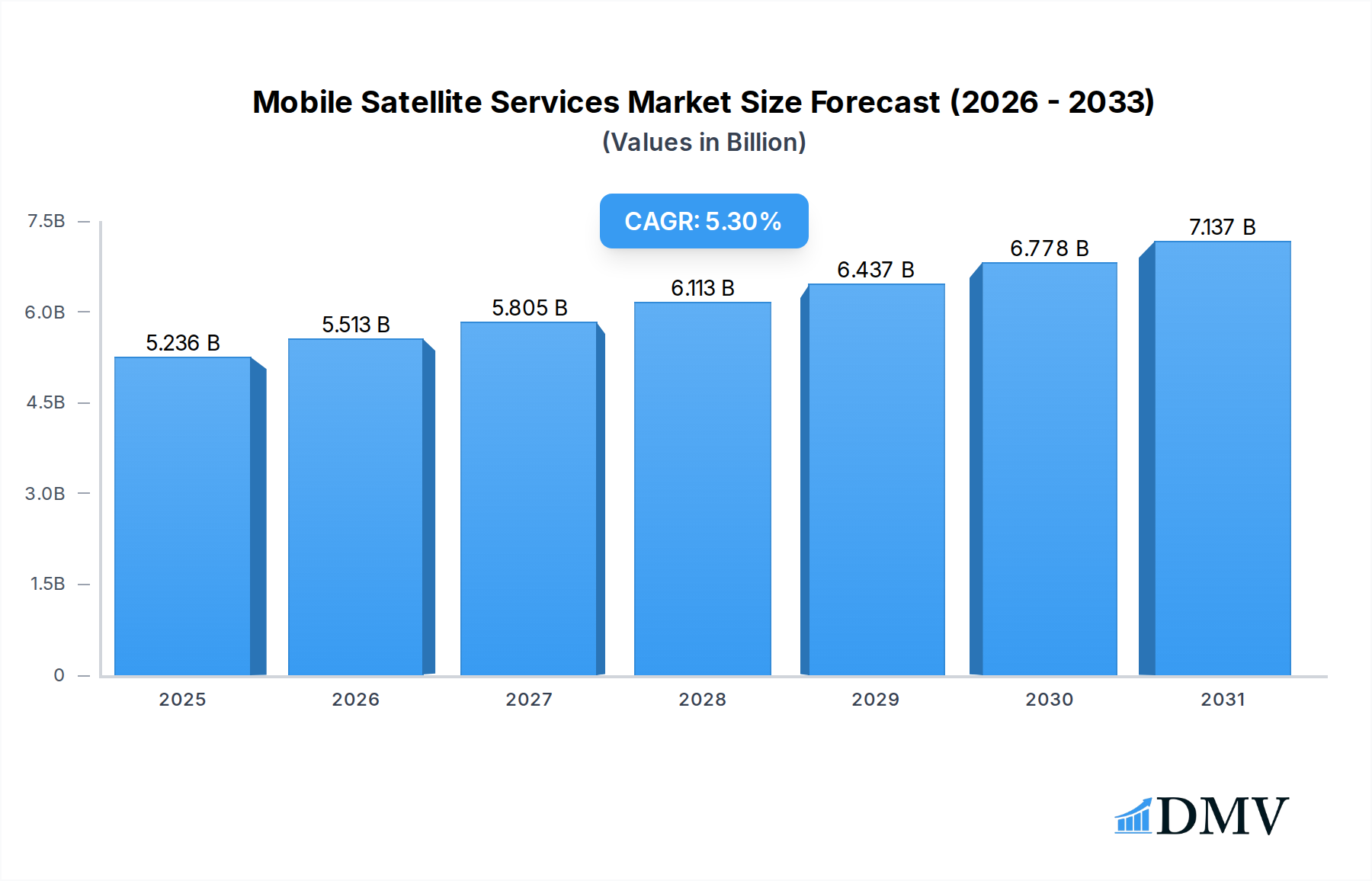

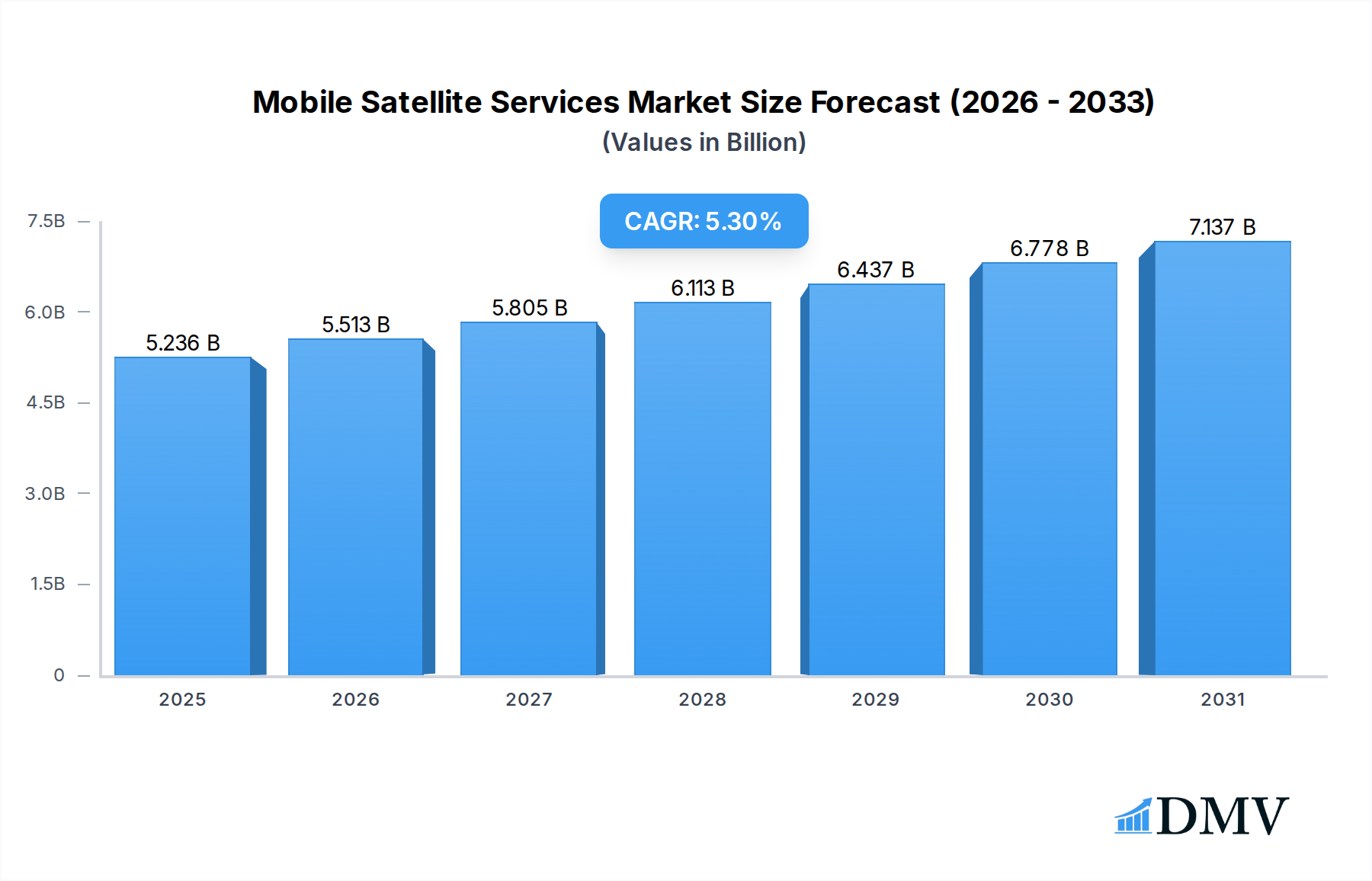

The Mobile Satellite Services Market is currently valued at an impressive $4972.1 million and is poised for substantial expansion, projecting a compound annual growth rate (CAGR) of 5.3% through 2032. This robust growth is primarily fueled by the escalating global demand for ubiquitous connectivity, particularly in remote and underserved regions, as well as critical applications where terrestrial networks are insufficient or non-existent. Key demand drivers include the proliferation of IoT and M2M communication, requiring seamless connectivity for diverse applications such as remote monitoring and asset tracking across various industries. The increasing reliance on satellite-based solutions for disaster relief, emergency services, and defense operations further underpins market expansion. Furthermore, the growth of the Maritime Industry Market and the burgeoning demand from the Aerospace and Defense Market for reliable communication systems are significant macro tailwinds.

Mobile Satellite Services Market Size (In Billion)

The evolution of satellite technology, notably the deployment of advanced Low Earth Orbit Satellite Market constellations, is revolutionizing service delivery, offering lower latency and higher bandwidth capabilities. This technological leap is enabling new applications and enhancing existing ones, making satellite services more competitive against traditional terrestrial options. The market is witnessing a strategic shift towards integrated solutions that combine satellite and terrestrial networks, offering hybrid connectivity models to optimize performance and cost. Innovation in terminal equipment, miniaturization, and improved power efficiency are also broadening the addressable market by making satellite connectivity more accessible and affordable for a wider range of end-users. The outlook for the Mobile Satellite Services Market remains highly positive, driven by sustained investment in next-generation satellite infrastructure and the continuous expansion of application use cases across commercial, government, and consumer segments.

Mobile Satellite Services Company Market Share

Data Services Dominance in Mobile Satellite Services Market

The Data Services segment unequivocally holds the largest revenue share within the Mobile Satellite Services Market, a dominance underscored by the accelerating global demand for real-time information exchange and persistent connectivity. This segment's prevalence is primarily driven by the exponential growth of the Internet of Things (IoT) and Machine-to-Machine (M2M) communication, which inherently rely on satellite networks for transmitting critical data from geographically dispersed assets. Industries such as oil & gas, mining, agriculture, and transportation & logistics are heavy consumers of satellite data services for applications like remote monitoring, predictive maintenance, and operational efficiency improvements. For instance, sensors deployed on pipelines, remote machinery, or vast agricultural fields transmit essential operational data via satellite, enabling proactive management and reducing downtime. The burgeoning Satellite Communication Market, particularly for broadband access in remote areas, also contributes significantly to this segment's lead.

Key players in the Mobile Satellite Services Market, including Iridium Communications, Inmarsat, and Viasat, are heavily investing in enhancing their data service capabilities, rolling out higher bandwidth solutions and developing specialized platforms for various vertical markets. The introduction of advanced L-Band and Ka-Band systems, coupled with the emergence of Low Earth Orbit Satellite Market constellations, is driving a new era of high-throughput satellite (HTS) data services, capable of supporting bandwidth-intensive applications such as video streaming and large file transfers. This technological progression is allowing satellite data services to not only serve niche markets but also to compete more effectively with terrestrial networks in certain regions. While the Voice Services Market remains vital for critical communications, particularly in maritime and emergency scenarios, its growth trajectory is outpaced by the robust expansion of data consumption across nearly all end-user industries. The sheer volume and diversity of data applications, from global Asset Tracking Market solutions to extensive remote sensing networks, ensure the continued leadership and growth consolidation of the Data Services segment in the Mobile Satellite Services Market, further solidifying its critical role in modern global infrastructure.

Key Market Drivers and Constraints in Mobile Satellite Services Market

The Mobile Satellite Services Market expansion is underpinned by several potent drivers. A primary impetus is the escalating demand for pervasive connectivity in remote and underserved regions, where terrestrial infrastructure is either non-existent or economically unviable. This driver is quantified by the projected 50% increase in global IoT connections in remote areas by 2028, a significant portion of which will rely on satellite links. Another critical driver is the increasing adoption of satellite solutions for disaster resilience and emergency communication. For example, during natural disasters, ground-based communication networks are often compromised, making satellite systems the sole means of communication for first responders and relief efforts. The imperative for resilient communication infrastructure is amplified by the observed 15% annual rise in extreme weather events globally over the last decade, directly stimulating demand for robust Mobile Satellite Services Market offerings.

Conversely, several constraints impede the market's growth. The high initial capital expenditure associated with launching and maintaining satellite constellations remains a significant barrier, requiring substantial investment in ground infrastructure and satellite procurement. This is evident in the multi-billion dollar costs incurred by new Low Earth Orbit Satellite Market entrants. Regulatory complexities and licensing hurdles across different nations also present substantial challenges, with varying spectrum allocation policies and legal frameworks often delaying market entry and operational expansion. Furthermore, intense competition from expanding terrestrial cellular and fiber networks, particularly in semi-urban and rural areas, poses a constraint. While satellite offers global reach, terrestrial networks often provide higher bandwidth and lower latency at a competitive price point in populated regions, compelling satellite operators to focus on niche markets or specialized hybrid solutions. The Telecommunication Services Market is highly dynamic, and while satellite has a unique value proposition, cost-effectiveness remains a constant challenge against terrestrial alternatives.

Competitive Ecosystem of Mobile Satellite Services Market

The Mobile Satellite Services Market is characterized by a mix of established global operators and innovative new entrants, all vying for market share through technological advancements and diversified service offerings.

- Iridium Communications: A leading provider of global voice and data communications, leveraging its unique constellation of 66 cross-linked Low Earth Orbit (LEO) satellites. Iridium specializes in mission-critical applications for maritime, aviation, government, and land mobile users, known for its truly global coverage and robust capabilities for the Voice Services Market and low-latency data transmission.

- Inmarsat: A prominent player offering a diverse portfolio of global mobile satellite communication services, including broadband internet, voice, and safety services across land, sea, and air. Inmarsat is particularly strong in the Maritime Industry Market and aviation sectors, providing critical connectivity solutions and driving innovation in high-throughput satellite (HTS) technologies.

- Viasat: Known for its advanced satellite broadband services, Viasat focuses on delivering high-speed, high-capacity connectivity to commercial and government customers worldwide. The company's strategy involves developing ultra-high capacity satellites to address increasing demand for Data Services Market, particularly in areas like in-flight connectivity and remote enterprise solutions.

- Globalstar: Offers satellite voice and data services, including Asset Tracking Market and M2M solutions, through its LEO satellite constellation. Globalstar is recognized for its personal communications devices and robust services for remote monitoring and asset management across various industrial sectors.

- Thuraya Telecommunications Company: A UAE-based satellite operator providing mobile satellite voice and data services across Europe, Africa, Asia, and Australia. Thuraya emphasizes handheld satellite phones and broadband terminals, catering to government, energy, media, and maritime users with reliable communication solutions.

- EchoStar Corporation: A global provider of satellite communication solutions, including a significant presence in the consumer broadband market through its HughesNet service, and enterprise satellite services. EchoStar's strategy encompasses both geostationary and, increasingly, multi-orbit satellite solutions to meet varied customer needs in the Satellite Communication Market.

- Orbcomm: Specializes in M2M and IoT solutions, providing global satellite and cellular connectivity for Asset Tracking Market, monitoring, and control of fixed and mobile assets. Orbcomm's services are crucial for sectors like transportation, heavy equipment, maritime, and oil & gas, facilitating operational efficiency and data-driven decision-making.

- Omnispace: An innovative company focused on developing a hybrid satellite and terrestrial 5G network, aiming to deliver seamless mobile connectivity directly to standard 5G devices. This approach seeks to broaden the reach of the Telecommunication Services Market by integrating non-terrestrial networks (NTN) with existing terrestrial infrastructure.

- AST SpaceMobile: Developing a space-based cellular broadband network designed to connect directly to standard, unmodified mobile phones. AST SpaceMobile aims to eliminate coverage gaps for cellular users globally, potentially disrupting traditional Mobile Satellite Services Market models by offering direct-to-device connectivity.

Recent Developments & Milestones in Mobile Satellite Services Market

- March 2024: Iridium Communications announced a strategic partnership with a major maritime analytics firm to integrate its Certus broadband service for enhanced ship-to-shore data transmission, improving real-time operational insights for the Maritime Industry Market.

- February 2024: Inmarsat revealed plans to launch new high-throughput satellite (HTS) payloads in 2026 as part of its ORCHESTRA network, aiming to boost capacity and lower latency for global Data Services Market, particularly in aviation and enterprise segments.

- January 2024: Viasat completed its acquisition of Inmarsat, creating a new global leader in satellite communications. This merger is expected to yield significant synergies and accelerate innovation in both Mobile Satellite Services Market and broadband segments.

- November 2023: Globalstar announced the successful deployment of new ground infrastructure to support its next-generation LEO constellation, enhancing coverage and service reliability for its Asset Tracking Market and Voice Services Market customers worldwide.

- September 2023: AST SpaceMobile successfully conducted its first-ever two-way voice call using its BlueWalker 3 test satellite and unmodified smartphones, marking a significant milestone towards direct-to-device satellite connectivity and a new era for the Mobile Satellite Services Market.

- July 2023: The European Space Agency (ESA) initiated new funding programs for 5G Non-Terrestrial Network (NTN) research and development, aiming to integrate satellite capabilities more closely with the broader Telecommunication Services Market infrastructure.

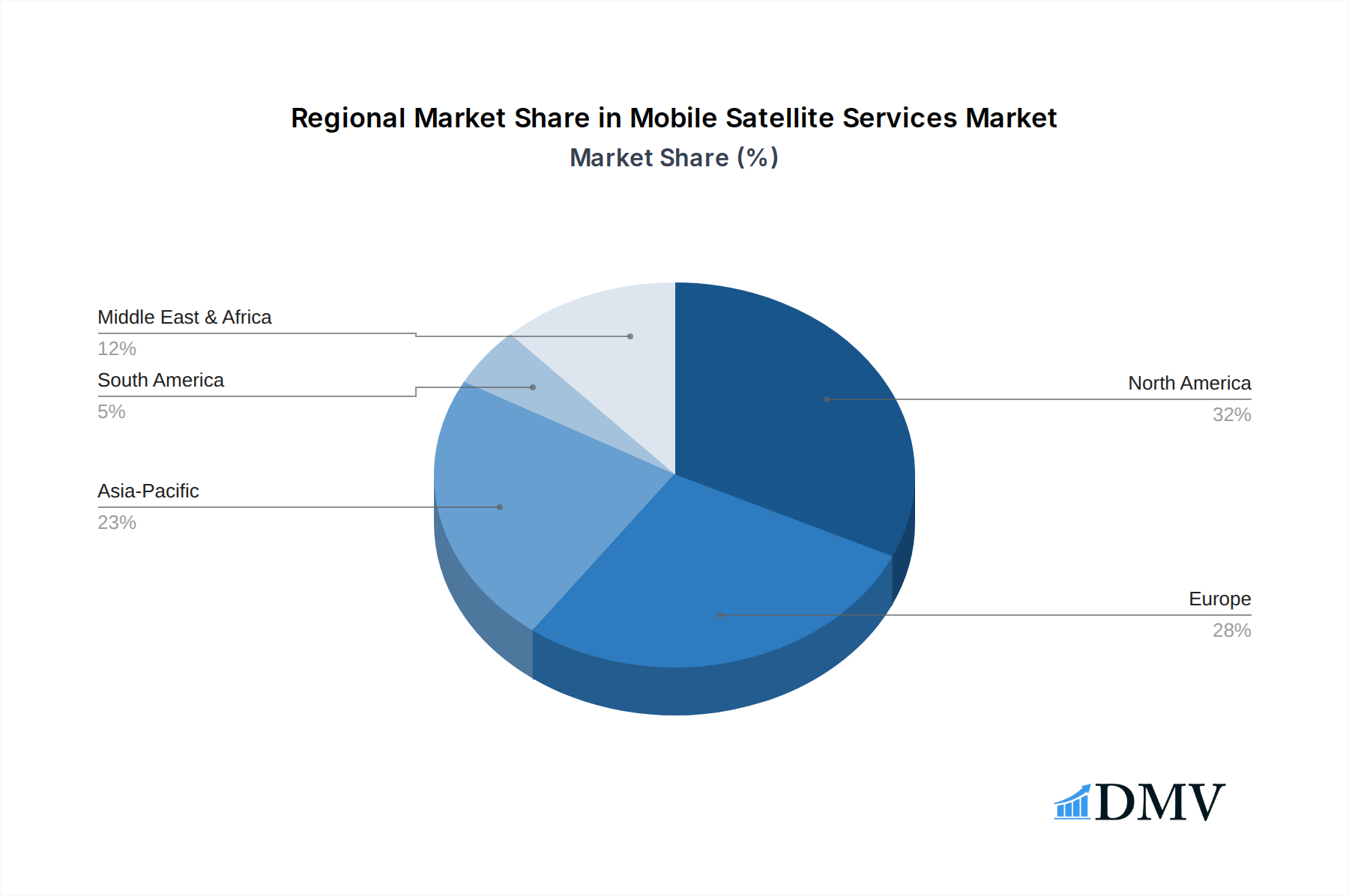

Regional Market Breakdown for Mobile Satellite Services Market

Geographically, the Mobile Satellite Services Market exhibits diverse growth patterns and maturity levels across key regions. North America remains a dominant force, contributing an estimated 35% of the global revenue share. This region's strength is driven by significant government & defense spending, early adoption of advanced satellite technologies, and a robust private sector demanding secure and reliable connectivity for remote operations. The demand from the Aerospace and Defense Market and specialized industrial applications in oil & gas and mining are primary drivers. North America is characterized by a mature market with high penetration, focusing on technological upgrades and specialized high-value services.

Europe follows with a substantial market share, estimated at 28%, propelled by strong maritime and aviation sectors, as well as increasing demand for data services in critical infrastructure management. Countries like the UK, Germany, and France are investing in satellite communication for security, emergency services, and broadband access in rural areas. The region is seeing steady growth, with a focus on integrating satellite services into 5G ecosystems and expanding the use of Low Earth Orbit Satellite Market constellations for enhanced data transmission.

Asia Pacific is identified as the fastest-growing region, projected to register the highest CAGR above the global average, driven by rapid economic development, expanding industrialization, and significant investments in connectivity infrastructure. This region's large underserved population and increasing urbanization create immense opportunities for both Voice Services Market and Data Services Market. Countries like China, India, and ASEAN nations are rapidly adopting satellite solutions for remote area connectivity, disaster management, and the growth of the Asset Tracking Market in transportation and logistics. The region's vast geographical spread makes satellite a crucial component of its Telecommunication Services Market.

Middle East & Africa also demonstrate robust growth, particularly in the oil & gas, mining, and maritime sectors. The demand for reliable communication in remote operational sites and for fleet management within the Maritime Industry Market are key drivers. Investment in satellite infrastructure is increasing to bridge connectivity gaps and support economic diversification initiatives. While starting from a smaller base, this region is experiencing significant expansion as foundational infrastructure is deployed.

Mobile Satellite Services Regional Market Share

Technology Innovation Trajectory in Mobile Satellite Services Market

The Mobile Satellite Services Market is undergoing a profound technological transformation, driven by several disruptive innovations. One of the most significant is the proliferation of Low Earth Orbit (LEO) and Medium Earth Orbit (MEO) satellite constellations. Unlike traditional geostationary (GEO) satellites, LEO/MEO systems offer significantly lower latency (down to 20-50ms) and higher bandwidth capacities, making them ideal for latency-sensitive applications like real-time video conferencing, cloud access, and gaming. Companies like Iridium, OneWeb, and Starlink (SpaceX) are at the forefront of this shift. R&D investments in these constellations are in the tens of billions of dollars, with adoption timelines accelerating; many LEO services are already commercially available, and global coverage is expanding rapidly. This innovation directly threatens incumbent GEO operators by offering superior performance for a growing range of applications, while also reinforcing the overall Mobile Satellite Services Market by expanding its addressable use cases beyond traditional verticals. The Low Earth Orbit Satellite Market is fundamentally reshaping competitive dynamics.

Another critical innovation is the integration of 5G Non-Terrestrial Networks (NTN). This involves designing satellite systems to be compatible with 5G standards, enabling seamless connectivity between terrestrial 5G networks and satellite infrastructure. This aims to extend 5G coverage to rural, remote, and maritime areas, and provide robust connectivity for the Asset Tracking Market and critical communications. R&D efforts are focused on developing compatible modems, network architectures, and spectrum allocation strategies. Adoption is projected to gain significant traction between 2025 and 2030, as 3GPP standards evolve to fully support NTN. This technology primarily reinforces incumbent Mobile Satellite Services Market business models by enabling them to become an integral part of the broader Telecommunication Services Market, offering hybrid solutions that leverage the strengths of both terrestrial and satellite networks, rather than operating in isolation.

Furthermore, Artificial Intelligence (AI) and Machine Learning (ML) for network optimization are emerging as vital technologies. AI/ML algorithms are being employed to dynamically manage satellite constellations, optimize resource allocation, predict network failures, and enhance cybersecurity. These technologies are crucial for managing the complexity of multi-orbit, multi-band satellite networks and ensuring efficient spectrum utilization for the Data Services Market. While adoption is already underway for internal network management, its full potential in customer-facing services is expected to materialize over the next 5-7 years. AI/ML primarily reinforces incumbent business models by enabling more efficient operations, reducing costs, and improving service quality, thus enhancing profitability and competitive advantage in the increasingly complex Mobile Satellite Services Market.

Pricing Dynamics & Margin Pressure in Mobile Satellite Services Market

The pricing dynamics in the Mobile Satellite Services Market are complex, influenced by a combination of technological advancements, competitive intensity, and the specific value proposition offered. Historically, average selling prices (ASPs) for satellite connectivity have been relatively high due to the significant capital expenditure involved in launching and maintaining satellite infrastructure. However, the advent of High-Throughput Satellites (HTS) and particularly the proliferation of Low Earth Orbit Satellite Market constellations are exerting downward pressure on per-megabit pricing, especially for Data Services Market. Newer LEO providers are adopting a direct-to-consumer or direct-to-enterprise model with subscription-based pricing, offering significantly lower monthly costs and higher bandwidth tiers compared to traditional GEO offerings, leading to increased price-to-performance ratios.

Margin structures across the value chain vary considerably. Satellite operators typically enjoy higher gross margins, reflecting their substantial investment in infrastructure, but these are offset by high operational expenditures (OpEx) for ground segment maintenance, network management, and regulatory compliance. Service providers, who bundle satellite capacity with value-added services such as managed networks, cybersecurity, or specialized applications for the Maritime Industry Market or Asset Tracking Market, often operate with thinner margins but benefit from recurring revenue streams and customer stickiness. The key cost levers include launch services, satellite manufacturing, ground segment development, and spectrum licensing fees. Innovations in reusable rocket technology have begun to reduce launch costs, impacting the overall cost structure of new constellations.

Competitive intensity is escalating due to new entrants with extensive LEO capacity, leading to margin pressure for established players, particularly in the broadband connectivity sector. To counter this, many incumbents are diversifying their offerings into higher-value, specialized services, focusing on niche markets where terrestrial alternatives are non-existent or inadequate, such as the Aerospace and Defense Market or remote enterprise connectivity. Furthermore, the integration of satellite services into hybrid 5G networks, as part of the broader Telecommunication Services Market, creates new opportunities for revenue streams and strategic partnerships, potentially mitigating some of the pricing erosion seen in commodity data services. The market's future will likely see a continued trend towards tiered pricing models based on bandwidth, latency, and service level agreements (SLAs), alongside a growing emphasis on value-added services to differentiate offerings and preserve margins.

Mobile Satellite Services Segmentation

-

1. Service Type

- 1.1. Voice Services

- 1.2. Data Services

- 1.3. Video Services

- 1.4. Tracking & Monitoring Services

- 1.5. Others

-

2. Frequency Band

- 2.1. L-Band

- 2.2. S-Band

- 2.3. Ku-Band

- 2.4. Ka-Band

- 2.5. Others

-

3. Application

- 3.1. Satellite Communication

- 3.2. Fleet Management

- 3.3. Asset Tracking

- 3.4. Remote Monitoring

- 3.5. Others

-

4. End User Industry

- 4.1. Aerospace and Defense

- 4.2. Government & Defense

- 4.3. Maritime

- 4.4. Oil & Gas

- 4.5. Mining

- 4.6. Transportation & Logistics

- 4.7. Agriculture

- 4.8. Energy & Utilities

- 4.9. Others

Mobile Satellite Services Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Mobile Satellite Services Regional Market Share

Geographic Coverage of Mobile Satellite Services

Mobile Satellite Services REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Service Type

- 5.1.1. Voice Services

- 5.1.2. Data Services

- 5.1.3. Video Services

- 5.1.4. Tracking & Monitoring Services

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Frequency Band

- 5.2.1. L-Band

- 5.2.2. S-Band

- 5.2.3. Ku-Band

- 5.2.4. Ka-Band

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Satellite Communication

- 5.3.2. Fleet Management

- 5.3.3. Asset Tracking

- 5.3.4. Remote Monitoring

- 5.3.5. Others

- 5.4. Market Analysis, Insights and Forecast - by End User Industry

- 5.4.1. Aerospace and Defense

- 5.4.2. Government & Defense

- 5.4.3. Maritime

- 5.4.4. Oil & Gas

- 5.4.5. Mining

- 5.4.6. Transportation & Logistics

- 5.4.7. Agriculture

- 5.4.8. Energy & Utilities

- 5.4.9. Others

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. South America

- 5.5.3. Europe

- 5.5.4. Middle East & Africa

- 5.5.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Service Type

- 6. Global Mobile Satellite Services Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Service Type

- 6.1.1. Voice Services

- 6.1.2. Data Services

- 6.1.3. Video Services

- 6.1.4. Tracking & Monitoring Services

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Frequency Band

- 6.2.1. L-Band

- 6.2.2. S-Band

- 6.2.3. Ku-Band

- 6.2.4. Ka-Band

- 6.2.5. Others

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Satellite Communication

- 6.3.2. Fleet Management

- 6.3.3. Asset Tracking

- 6.3.4. Remote Monitoring

- 6.3.5. Others

- 6.4. Market Analysis, Insights and Forecast - by End User Industry

- 6.4.1. Aerospace and Defense

- 6.4.2. Government & Defense

- 6.4.3. Maritime

- 6.4.4. Oil & Gas

- 6.4.5. Mining

- 6.4.6. Transportation & Logistics

- 6.4.7. Agriculture

- 6.4.8. Energy & Utilities

- 6.4.9. Others

- 6.1. Market Analysis, Insights and Forecast - by Service Type

- 7. North America Mobile Satellite Services Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Service Type

- 7.1.1. Voice Services

- 7.1.2. Data Services

- 7.1.3. Video Services

- 7.1.4. Tracking & Monitoring Services

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Frequency Band

- 7.2.1. L-Band

- 7.2.2. S-Band

- 7.2.3. Ku-Band

- 7.2.4. Ka-Band

- 7.2.5. Others

- 7.3. Market Analysis, Insights and Forecast - by Application

- 7.3.1. Satellite Communication

- 7.3.2. Fleet Management

- 7.3.3. Asset Tracking

- 7.3.4. Remote Monitoring

- 7.3.5. Others

- 7.4. Market Analysis, Insights and Forecast - by End User Industry

- 7.4.1. Aerospace and Defense

- 7.4.2. Government & Defense

- 7.4.3. Maritime

- 7.4.4. Oil & Gas

- 7.4.5. Mining

- 7.4.6. Transportation & Logistics

- 7.4.7. Agriculture

- 7.4.8. Energy & Utilities

- 7.4.9. Others

- 7.1. Market Analysis, Insights and Forecast - by Service Type

- 8. South America Mobile Satellite Services Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Service Type

- 8.1.1. Voice Services

- 8.1.2. Data Services

- 8.1.3. Video Services

- 8.1.4. Tracking & Monitoring Services

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Frequency Band

- 8.2.1. L-Band

- 8.2.2. S-Band

- 8.2.3. Ku-Band

- 8.2.4. Ka-Band

- 8.2.5. Others

- 8.3. Market Analysis, Insights and Forecast - by Application

- 8.3.1. Satellite Communication

- 8.3.2. Fleet Management

- 8.3.3. Asset Tracking

- 8.3.4. Remote Monitoring

- 8.3.5. Others

- 8.4. Market Analysis, Insights and Forecast - by End User Industry

- 8.4.1. Aerospace and Defense

- 8.4.2. Government & Defense

- 8.4.3. Maritime

- 8.4.4. Oil & Gas

- 8.4.5. Mining

- 8.4.6. Transportation & Logistics

- 8.4.7. Agriculture

- 8.4.8. Energy & Utilities

- 8.4.9. Others

- 8.1. Market Analysis, Insights and Forecast - by Service Type

- 9. Europe Mobile Satellite Services Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Service Type

- 9.1.1. Voice Services

- 9.1.2. Data Services

- 9.1.3. Video Services

- 9.1.4. Tracking & Monitoring Services

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Frequency Band

- 9.2.1. L-Band

- 9.2.2. S-Band

- 9.2.3. Ku-Band

- 9.2.4. Ka-Band

- 9.2.5. Others

- 9.3. Market Analysis, Insights and Forecast - by Application

- 9.3.1. Satellite Communication

- 9.3.2. Fleet Management

- 9.3.3. Asset Tracking

- 9.3.4. Remote Monitoring

- 9.3.5. Others

- 9.4. Market Analysis, Insights and Forecast - by End User Industry

- 9.4.1. Aerospace and Defense

- 9.4.2. Government & Defense

- 9.4.3. Maritime

- 9.4.4. Oil & Gas

- 9.4.5. Mining

- 9.4.6. Transportation & Logistics

- 9.4.7. Agriculture

- 9.4.8. Energy & Utilities

- 9.4.9. Others

- 9.1. Market Analysis, Insights and Forecast - by Service Type

- 10. Middle East & Africa Mobile Satellite Services Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Service Type

- 10.1.1. Voice Services

- 10.1.2. Data Services

- 10.1.3. Video Services

- 10.1.4. Tracking & Monitoring Services

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Frequency Band

- 10.2.1. L-Band

- 10.2.2. S-Band

- 10.2.3. Ku-Band

- 10.2.4. Ka-Band

- 10.2.5. Others

- 10.3. Market Analysis, Insights and Forecast - by Application

- 10.3.1. Satellite Communication

- 10.3.2. Fleet Management

- 10.3.3. Asset Tracking

- 10.3.4. Remote Monitoring

- 10.3.5. Others

- 10.4. Market Analysis, Insights and Forecast - by End User Industry

- 10.4.1. Aerospace and Defense

- 10.4.2. Government & Defense

- 10.4.3. Maritime

- 10.4.4. Oil & Gas

- 10.4.5. Mining

- 10.4.6. Transportation & Logistics

- 10.4.7. Agriculture

- 10.4.8. Energy & Utilities

- 10.4.9. Others

- 10.1. Market Analysis, Insights and Forecast - by Service Type

- 11. Asia Pacific Mobile Satellite Services Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Service Type

- 11.1.1. Voice Services

- 11.1.2. Data Services

- 11.1.3. Video Services

- 11.1.4. Tracking & Monitoring Services

- 11.1.5. Others

- 11.2. Market Analysis, Insights and Forecast - by Frequency Band

- 11.2.1. L-Band

- 11.2.2. S-Band

- 11.2.3. Ku-Band

- 11.2.4. Ka-Band

- 11.2.5. Others

- 11.3. Market Analysis, Insights and Forecast - by Application

- 11.3.1. Satellite Communication

- 11.3.2. Fleet Management

- 11.3.3. Asset Tracking

- 11.3.4. Remote Monitoring

- 11.3.5. Others

- 11.4. Market Analysis, Insights and Forecast - by End User Industry

- 11.4.1. Aerospace and Defense

- 11.4.2. Government & Defense

- 11.4.3. Maritime

- 11.4.4. Oil & Gas

- 11.4.5. Mining

- 11.4.6. Transportation & Logistics

- 11.4.7. Agriculture

- 11.4.8. Energy & Utilities

- 11.4.9. Others

- 11.1. Market Analysis, Insights and Forecast - by Service Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Iridium Communications

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Inmarsat

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Viasat

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Globalstar

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Thuraya Telecommunications Company

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 EchoStar Corporation

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Orbcomm

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Space42

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Omnispace

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 AST SpaceMobile

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Ligado Networks

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 Iridium Communications

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Mobile Satellite Services Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: Global Mobile Satellite Services Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Mobile Satellite Services Revenue (million), by Service Type 2025 & 2033

- Figure 4: North America Mobile Satellite Services Volume (K), by Service Type 2025 & 2033

- Figure 5: North America Mobile Satellite Services Revenue Share (%), by Service Type 2025 & 2033

- Figure 6: North America Mobile Satellite Services Volume Share (%), by Service Type 2025 & 2033

- Figure 7: North America Mobile Satellite Services Revenue (million), by Frequency Band 2025 & 2033

- Figure 8: North America Mobile Satellite Services Volume (K), by Frequency Band 2025 & 2033

- Figure 9: North America Mobile Satellite Services Revenue Share (%), by Frequency Band 2025 & 2033

- Figure 10: North America Mobile Satellite Services Volume Share (%), by Frequency Band 2025 & 2033

- Figure 11: North America Mobile Satellite Services Revenue (million), by Application 2025 & 2033

- Figure 12: North America Mobile Satellite Services Volume (K), by Application 2025 & 2033

- Figure 13: North America Mobile Satellite Services Revenue Share (%), by Application 2025 & 2033

- Figure 14: North America Mobile Satellite Services Volume Share (%), by Application 2025 & 2033

- Figure 15: North America Mobile Satellite Services Revenue (million), by End User Industry 2025 & 2033

- Figure 16: North America Mobile Satellite Services Volume (K), by End User Industry 2025 & 2033

- Figure 17: North America Mobile Satellite Services Revenue Share (%), by End User Industry 2025 & 2033

- Figure 18: North America Mobile Satellite Services Volume Share (%), by End User Industry 2025 & 2033

- Figure 19: North America Mobile Satellite Services Revenue (million), by Country 2025 & 2033

- Figure 20: North America Mobile Satellite Services Volume (K), by Country 2025 & 2033

- Figure 21: North America Mobile Satellite Services Revenue Share (%), by Country 2025 & 2033

- Figure 22: North America Mobile Satellite Services Volume Share (%), by Country 2025 & 2033

- Figure 23: South America Mobile Satellite Services Revenue (million), by Service Type 2025 & 2033

- Figure 24: South America Mobile Satellite Services Volume (K), by Service Type 2025 & 2033

- Figure 25: South America Mobile Satellite Services Revenue Share (%), by Service Type 2025 & 2033

- Figure 26: South America Mobile Satellite Services Volume Share (%), by Service Type 2025 & 2033

- Figure 27: South America Mobile Satellite Services Revenue (million), by Frequency Band 2025 & 2033

- Figure 28: South America Mobile Satellite Services Volume (K), by Frequency Band 2025 & 2033

- Figure 29: South America Mobile Satellite Services Revenue Share (%), by Frequency Band 2025 & 2033

- Figure 30: South America Mobile Satellite Services Volume Share (%), by Frequency Band 2025 & 2033

- Figure 31: South America Mobile Satellite Services Revenue (million), by Application 2025 & 2033

- Figure 32: South America Mobile Satellite Services Volume (K), by Application 2025 & 2033

- Figure 33: South America Mobile Satellite Services Revenue Share (%), by Application 2025 & 2033

- Figure 34: South America Mobile Satellite Services Volume Share (%), by Application 2025 & 2033

- Figure 35: South America Mobile Satellite Services Revenue (million), by End User Industry 2025 & 2033

- Figure 36: South America Mobile Satellite Services Volume (K), by End User Industry 2025 & 2033

- Figure 37: South America Mobile Satellite Services Revenue Share (%), by End User Industry 2025 & 2033

- Figure 38: South America Mobile Satellite Services Volume Share (%), by End User Industry 2025 & 2033

- Figure 39: South America Mobile Satellite Services Revenue (million), by Country 2025 & 2033

- Figure 40: South America Mobile Satellite Services Volume (K), by Country 2025 & 2033

- Figure 41: South America Mobile Satellite Services Revenue Share (%), by Country 2025 & 2033

- Figure 42: South America Mobile Satellite Services Volume Share (%), by Country 2025 & 2033

- Figure 43: Europe Mobile Satellite Services Revenue (million), by Service Type 2025 & 2033

- Figure 44: Europe Mobile Satellite Services Volume (K), by Service Type 2025 & 2033

- Figure 45: Europe Mobile Satellite Services Revenue Share (%), by Service Type 2025 & 2033

- Figure 46: Europe Mobile Satellite Services Volume Share (%), by Service Type 2025 & 2033

- Figure 47: Europe Mobile Satellite Services Revenue (million), by Frequency Band 2025 & 2033

- Figure 48: Europe Mobile Satellite Services Volume (K), by Frequency Band 2025 & 2033

- Figure 49: Europe Mobile Satellite Services Revenue Share (%), by Frequency Band 2025 & 2033

- Figure 50: Europe Mobile Satellite Services Volume Share (%), by Frequency Band 2025 & 2033

- Figure 51: Europe Mobile Satellite Services Revenue (million), by Application 2025 & 2033

- Figure 52: Europe Mobile Satellite Services Volume (K), by Application 2025 & 2033

- Figure 53: Europe Mobile Satellite Services Revenue Share (%), by Application 2025 & 2033

- Figure 54: Europe Mobile Satellite Services Volume Share (%), by Application 2025 & 2033

- Figure 55: Europe Mobile Satellite Services Revenue (million), by End User Industry 2025 & 2033

- Figure 56: Europe Mobile Satellite Services Volume (K), by End User Industry 2025 & 2033

- Figure 57: Europe Mobile Satellite Services Revenue Share (%), by End User Industry 2025 & 2033

- Figure 58: Europe Mobile Satellite Services Volume Share (%), by End User Industry 2025 & 2033

- Figure 59: Europe Mobile Satellite Services Revenue (million), by Country 2025 & 2033

- Figure 60: Europe Mobile Satellite Services Volume (K), by Country 2025 & 2033

- Figure 61: Europe Mobile Satellite Services Revenue Share (%), by Country 2025 & 2033

- Figure 62: Europe Mobile Satellite Services Volume Share (%), by Country 2025 & 2033

- Figure 63: Middle East & Africa Mobile Satellite Services Revenue (million), by Service Type 2025 & 2033

- Figure 64: Middle East & Africa Mobile Satellite Services Volume (K), by Service Type 2025 & 2033

- Figure 65: Middle East & Africa Mobile Satellite Services Revenue Share (%), by Service Type 2025 & 2033

- Figure 66: Middle East & Africa Mobile Satellite Services Volume Share (%), by Service Type 2025 & 2033

- Figure 67: Middle East & Africa Mobile Satellite Services Revenue (million), by Frequency Band 2025 & 2033

- Figure 68: Middle East & Africa Mobile Satellite Services Volume (K), by Frequency Band 2025 & 2033

- Figure 69: Middle East & Africa Mobile Satellite Services Revenue Share (%), by Frequency Band 2025 & 2033

- Figure 70: Middle East & Africa Mobile Satellite Services Volume Share (%), by Frequency Band 2025 & 2033

- Figure 71: Middle East & Africa Mobile Satellite Services Revenue (million), by Application 2025 & 2033

- Figure 72: Middle East & Africa Mobile Satellite Services Volume (K), by Application 2025 & 2033

- Figure 73: Middle East & Africa Mobile Satellite Services Revenue Share (%), by Application 2025 & 2033

- Figure 74: Middle East & Africa Mobile Satellite Services Volume Share (%), by Application 2025 & 2033

- Figure 75: Middle East & Africa Mobile Satellite Services Revenue (million), by End User Industry 2025 & 2033

- Figure 76: Middle East & Africa Mobile Satellite Services Volume (K), by End User Industry 2025 & 2033

- Figure 77: Middle East & Africa Mobile Satellite Services Revenue Share (%), by End User Industry 2025 & 2033

- Figure 78: Middle East & Africa Mobile Satellite Services Volume Share (%), by End User Industry 2025 & 2033

- Figure 79: Middle East & Africa Mobile Satellite Services Revenue (million), by Country 2025 & 2033

- Figure 80: Middle East & Africa Mobile Satellite Services Volume (K), by Country 2025 & 2033

- Figure 81: Middle East & Africa Mobile Satellite Services Revenue Share (%), by Country 2025 & 2033

- Figure 82: Middle East & Africa Mobile Satellite Services Volume Share (%), by Country 2025 & 2033

- Figure 83: Asia Pacific Mobile Satellite Services Revenue (million), by Service Type 2025 & 2033

- Figure 84: Asia Pacific Mobile Satellite Services Volume (K), by Service Type 2025 & 2033

- Figure 85: Asia Pacific Mobile Satellite Services Revenue Share (%), by Service Type 2025 & 2033

- Figure 86: Asia Pacific Mobile Satellite Services Volume Share (%), by Service Type 2025 & 2033

- Figure 87: Asia Pacific Mobile Satellite Services Revenue (million), by Frequency Band 2025 & 2033

- Figure 88: Asia Pacific Mobile Satellite Services Volume (K), by Frequency Band 2025 & 2033

- Figure 89: Asia Pacific Mobile Satellite Services Revenue Share (%), by Frequency Band 2025 & 2033

- Figure 90: Asia Pacific Mobile Satellite Services Volume Share (%), by Frequency Band 2025 & 2033

- Figure 91: Asia Pacific Mobile Satellite Services Revenue (million), by Application 2025 & 2033

- Figure 92: Asia Pacific Mobile Satellite Services Volume (K), by Application 2025 & 2033

- Figure 93: Asia Pacific Mobile Satellite Services Revenue Share (%), by Application 2025 & 2033

- Figure 94: Asia Pacific Mobile Satellite Services Volume Share (%), by Application 2025 & 2033

- Figure 95: Asia Pacific Mobile Satellite Services Revenue (million), by End User Industry 2025 & 2033

- Figure 96: Asia Pacific Mobile Satellite Services Volume (K), by End User Industry 2025 & 2033

- Figure 97: Asia Pacific Mobile Satellite Services Revenue Share (%), by End User Industry 2025 & 2033

- Figure 98: Asia Pacific Mobile Satellite Services Volume Share (%), by End User Industry 2025 & 2033

- Figure 99: Asia Pacific Mobile Satellite Services Revenue (million), by Country 2025 & 2033

- Figure 100: Asia Pacific Mobile Satellite Services Volume (K), by Country 2025 & 2033

- Figure 101: Asia Pacific Mobile Satellite Services Revenue Share (%), by Country 2025 & 2033

- Figure 102: Asia Pacific Mobile Satellite Services Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Mobile Satellite Services Revenue million Forecast, by Service Type 2020 & 2033

- Table 2: Global Mobile Satellite Services Volume K Forecast, by Service Type 2020 & 2033

- Table 3: Global Mobile Satellite Services Revenue million Forecast, by Frequency Band 2020 & 2033

- Table 4: Global Mobile Satellite Services Volume K Forecast, by Frequency Band 2020 & 2033

- Table 5: Global Mobile Satellite Services Revenue million Forecast, by Application 2020 & 2033

- Table 6: Global Mobile Satellite Services Volume K Forecast, by Application 2020 & 2033

- Table 7: Global Mobile Satellite Services Revenue million Forecast, by End User Industry 2020 & 2033

- Table 8: Global Mobile Satellite Services Volume K Forecast, by End User Industry 2020 & 2033

- Table 9: Global Mobile Satellite Services Revenue million Forecast, by Region 2020 & 2033

- Table 10: Global Mobile Satellite Services Volume K Forecast, by Region 2020 & 2033

- Table 11: Global Mobile Satellite Services Revenue million Forecast, by Service Type 2020 & 2033

- Table 12: Global Mobile Satellite Services Volume K Forecast, by Service Type 2020 & 2033

- Table 13: Global Mobile Satellite Services Revenue million Forecast, by Frequency Band 2020 & 2033

- Table 14: Global Mobile Satellite Services Volume K Forecast, by Frequency Band 2020 & 2033

- Table 15: Global Mobile Satellite Services Revenue million Forecast, by Application 2020 & 2033

- Table 16: Global Mobile Satellite Services Volume K Forecast, by Application 2020 & 2033

- Table 17: Global Mobile Satellite Services Revenue million Forecast, by End User Industry 2020 & 2033

- Table 18: Global Mobile Satellite Services Volume K Forecast, by End User Industry 2020 & 2033

- Table 19: Global Mobile Satellite Services Revenue million Forecast, by Country 2020 & 2033

- Table 20: Global Mobile Satellite Services Volume K Forecast, by Country 2020 & 2033

- Table 21: United States Mobile Satellite Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: United States Mobile Satellite Services Volume (K) Forecast, by Application 2020 & 2033

- Table 23: Canada Mobile Satellite Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Canada Mobile Satellite Services Volume (K) Forecast, by Application 2020 & 2033

- Table 25: Mexico Mobile Satellite Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Mexico Mobile Satellite Services Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Global Mobile Satellite Services Revenue million Forecast, by Service Type 2020 & 2033

- Table 28: Global Mobile Satellite Services Volume K Forecast, by Service Type 2020 & 2033

- Table 29: Global Mobile Satellite Services Revenue million Forecast, by Frequency Band 2020 & 2033

- Table 30: Global Mobile Satellite Services Volume K Forecast, by Frequency Band 2020 & 2033

- Table 31: Global Mobile Satellite Services Revenue million Forecast, by Application 2020 & 2033

- Table 32: Global Mobile Satellite Services Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Mobile Satellite Services Revenue million Forecast, by End User Industry 2020 & 2033

- Table 34: Global Mobile Satellite Services Volume K Forecast, by End User Industry 2020 & 2033

- Table 35: Global Mobile Satellite Services Revenue million Forecast, by Country 2020 & 2033

- Table 36: Global Mobile Satellite Services Volume K Forecast, by Country 2020 & 2033

- Table 37: Brazil Mobile Satellite Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 38: Brazil Mobile Satellite Services Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Argentina Mobile Satellite Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 40: Argentina Mobile Satellite Services Volume (K) Forecast, by Application 2020 & 2033

- Table 41: Rest of South America Mobile Satellite Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Rest of South America Mobile Satellite Services Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Global Mobile Satellite Services Revenue million Forecast, by Service Type 2020 & 2033

- Table 44: Global Mobile Satellite Services Volume K Forecast, by Service Type 2020 & 2033

- Table 45: Global Mobile Satellite Services Revenue million Forecast, by Frequency Band 2020 & 2033

- Table 46: Global Mobile Satellite Services Volume K Forecast, by Frequency Band 2020 & 2033

- Table 47: Global Mobile Satellite Services Revenue million Forecast, by Application 2020 & 2033

- Table 48: Global Mobile Satellite Services Volume K Forecast, by Application 2020 & 2033

- Table 49: Global Mobile Satellite Services Revenue million Forecast, by End User Industry 2020 & 2033

- Table 50: Global Mobile Satellite Services Volume K Forecast, by End User Industry 2020 & 2033

- Table 51: Global Mobile Satellite Services Revenue million Forecast, by Country 2020 & 2033

- Table 52: Global Mobile Satellite Services Volume K Forecast, by Country 2020 & 2033

- Table 53: United Kingdom Mobile Satellite Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 54: United Kingdom Mobile Satellite Services Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Germany Mobile Satellite Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 56: Germany Mobile Satellite Services Volume (K) Forecast, by Application 2020 & 2033

- Table 57: France Mobile Satellite Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 58: France Mobile Satellite Services Volume (K) Forecast, by Application 2020 & 2033

- Table 59: Italy Mobile Satellite Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 60: Italy Mobile Satellite Services Volume (K) Forecast, by Application 2020 & 2033

- Table 61: Spain Mobile Satellite Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 62: Spain Mobile Satellite Services Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Russia Mobile Satellite Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 64: Russia Mobile Satellite Services Volume (K) Forecast, by Application 2020 & 2033

- Table 65: Benelux Mobile Satellite Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 66: Benelux Mobile Satellite Services Volume (K) Forecast, by Application 2020 & 2033

- Table 67: Nordics Mobile Satellite Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 68: Nordics Mobile Satellite Services Volume (K) Forecast, by Application 2020 & 2033

- Table 69: Rest of Europe Mobile Satellite Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 70: Rest of Europe Mobile Satellite Services Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Global Mobile Satellite Services Revenue million Forecast, by Service Type 2020 & 2033

- Table 72: Global Mobile Satellite Services Volume K Forecast, by Service Type 2020 & 2033

- Table 73: Global Mobile Satellite Services Revenue million Forecast, by Frequency Band 2020 & 2033

- Table 74: Global Mobile Satellite Services Volume K Forecast, by Frequency Band 2020 & 2033

- Table 75: Global Mobile Satellite Services Revenue million Forecast, by Application 2020 & 2033

- Table 76: Global Mobile Satellite Services Volume K Forecast, by Application 2020 & 2033

- Table 77: Global Mobile Satellite Services Revenue million Forecast, by End User Industry 2020 & 2033

- Table 78: Global Mobile Satellite Services Volume K Forecast, by End User Industry 2020 & 2033

- Table 79: Global Mobile Satellite Services Revenue million Forecast, by Country 2020 & 2033

- Table 80: Global Mobile Satellite Services Volume K Forecast, by Country 2020 & 2033

- Table 81: Turkey Mobile Satellite Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 82: Turkey Mobile Satellite Services Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Israel Mobile Satellite Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 84: Israel Mobile Satellite Services Volume (K) Forecast, by Application 2020 & 2033

- Table 85: GCC Mobile Satellite Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 86: GCC Mobile Satellite Services Volume (K) Forecast, by Application 2020 & 2033

- Table 87: North Africa Mobile Satellite Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 88: North Africa Mobile Satellite Services Volume (K) Forecast, by Application 2020 & 2033

- Table 89: South Africa Mobile Satellite Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 90: South Africa Mobile Satellite Services Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Middle East & Africa Mobile Satellite Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 92: Rest of Middle East & Africa Mobile Satellite Services Volume (K) Forecast, by Application 2020 & 2033

- Table 93: Global Mobile Satellite Services Revenue million Forecast, by Service Type 2020 & 2033

- Table 94: Global Mobile Satellite Services Volume K Forecast, by Service Type 2020 & 2033

- Table 95: Global Mobile Satellite Services Revenue million Forecast, by Frequency Band 2020 & 2033

- Table 96: Global Mobile Satellite Services Volume K Forecast, by Frequency Band 2020 & 2033

- Table 97: Global Mobile Satellite Services Revenue million Forecast, by Application 2020 & 2033

- Table 98: Global Mobile Satellite Services Volume K Forecast, by Application 2020 & 2033

- Table 99: Global Mobile Satellite Services Revenue million Forecast, by End User Industry 2020 & 2033

- Table 100: Global Mobile Satellite Services Volume K Forecast, by End User Industry 2020 & 2033

- Table 101: Global Mobile Satellite Services Revenue million Forecast, by Country 2020 & 2033

- Table 102: Global Mobile Satellite Services Volume K Forecast, by Country 2020 & 2033

- Table 103: China Mobile Satellite Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 104: China Mobile Satellite Services Volume (K) Forecast, by Application 2020 & 2033

- Table 105: India Mobile Satellite Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 106: India Mobile Satellite Services Volume (K) Forecast, by Application 2020 & 2033

- Table 107: Japan Mobile Satellite Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 108: Japan Mobile Satellite Services Volume (K) Forecast, by Application 2020 & 2033

- Table 109: South Korea Mobile Satellite Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 110: South Korea Mobile Satellite Services Volume (K) Forecast, by Application 2020 & 2033

- Table 111: ASEAN Mobile Satellite Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 112: ASEAN Mobile Satellite Services Volume (K) Forecast, by Application 2020 & 2033

- Table 113: Oceania Mobile Satellite Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 114: Oceania Mobile Satellite Services Volume (K) Forecast, by Application 2020 & 2033

- Table 115: Rest of Asia Pacific Mobile Satellite Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 116: Rest of Asia Pacific Mobile Satellite Services Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Mobile Satellite Services?

The projected CAGR is approximately 5.3%.

2. Which companies are prominent players in the Mobile Satellite Services?

Key companies in the market include Iridium Communications, Inmarsat, Viasat, Globalstar, Thuraya Telecommunications Company, EchoStar Corporation, Orbcomm, Space42, Omnispace, AST SpaceMobile, Ligado Networks, .

3. What are the main segments of the Mobile Satellite Services?

The market segments include Service Type, Frequency Band, Application, End User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 4972.1 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Mobile Satellite Services," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Mobile Satellite Services report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Mobile Satellite Services?

To stay informed about further developments, trends, and reports in the Mobile Satellite Services, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence