Key Insights

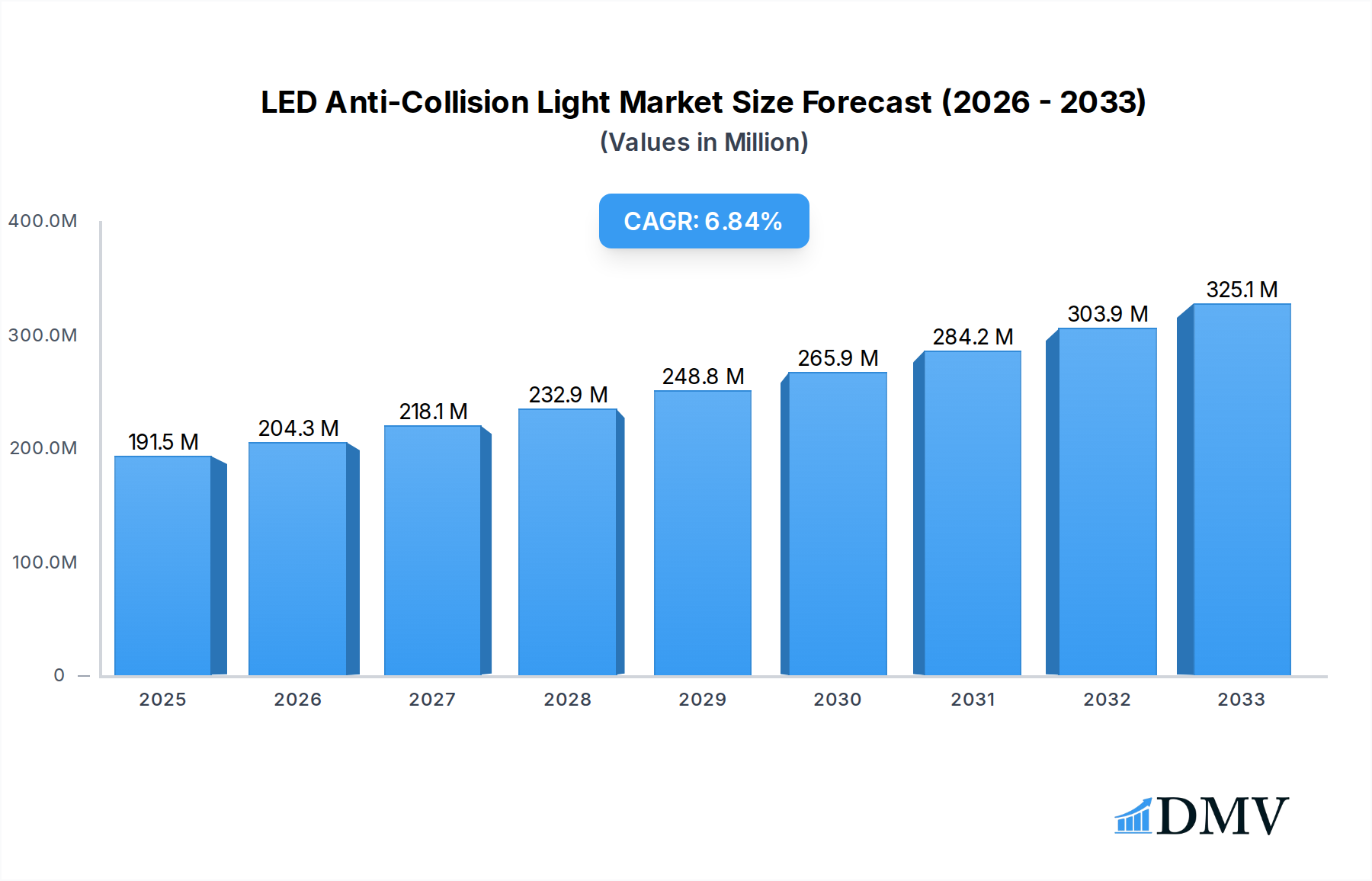

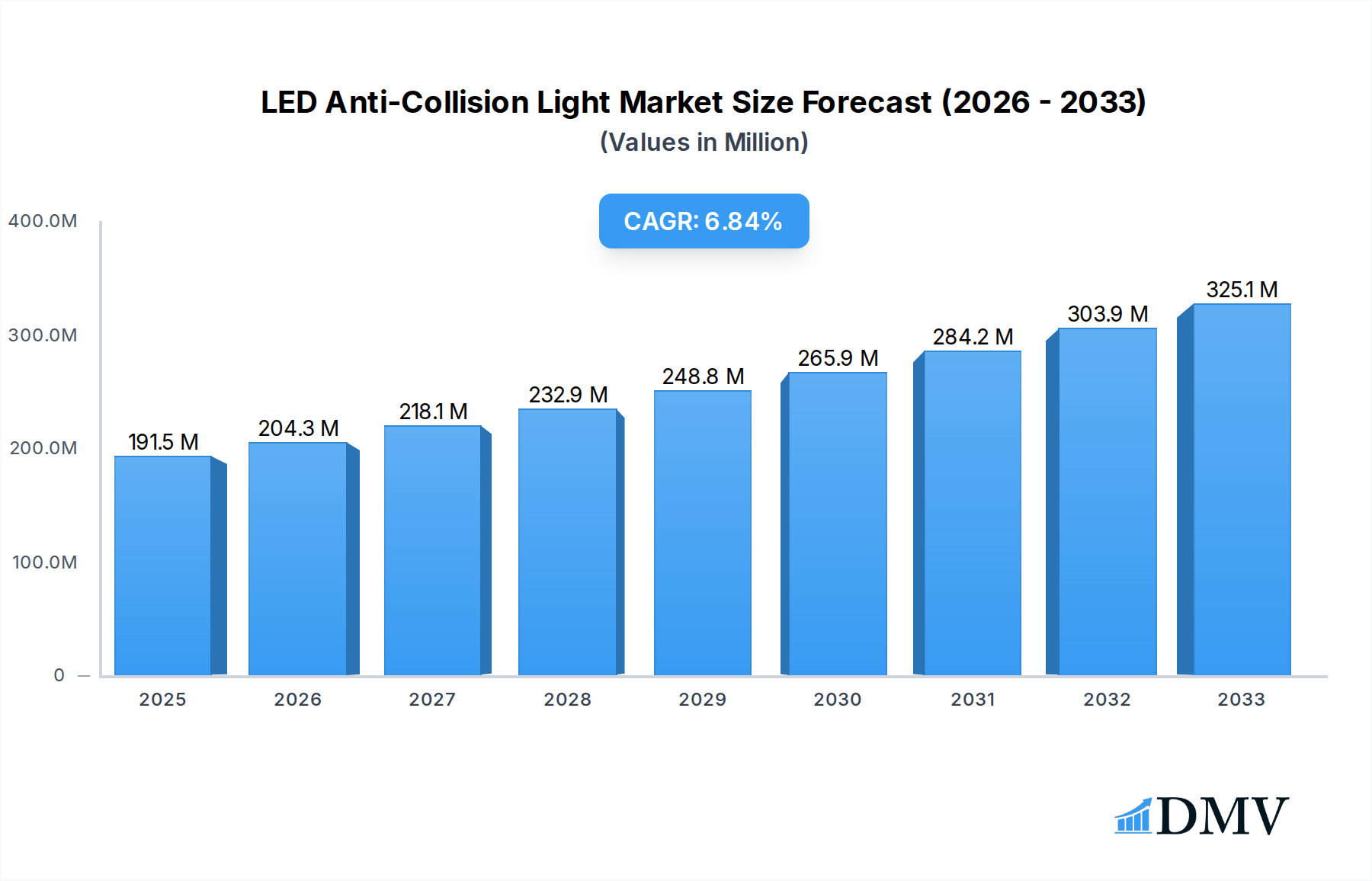

The global LED Anti-Collision Light market is poised for significant expansion, projected to reach $191.5 million by 2025, driven by a robust CAGR of 6.6%. This growth is primarily fueled by the increasing demand for enhanced aviation safety, stringent regulatory mandates for aircraft visibility, and the growing adoption of advanced lighting solutions across various transportation sectors. The inherent advantages of LED technology, such as longer lifespan, energy efficiency, and superior illumination compared to traditional lighting systems, further solidify its position in this market. Emerging economies are also contributing to this upward trajectory as they invest in modernizing their aerospace and transportation infrastructure, necessitating reliable and efficient anti-collision lighting. The market is further stimulated by continuous innovation in LED technology, leading to lighter, more powerful, and cost-effective anti-collision lights that cater to evolving industry needs.

LED Anti-Collision Light Market Size (In Million)

The market is segmented into dual-mode and tri-mode anti-collision lights, with applications spanning aircraft, vessels, vehicles, and other specialized areas. Aircraft applications are expected to dominate due to the critical need for collision avoidance in air travel and the continuous upgrades in avionics and safety equipment. Vessels and vehicles, particularly in commercial and defense sectors, are also witnessing increased adoption owing to heightened safety awareness and regulatory compliance. Key players are investing in research and development to introduce intelligent lighting systems that integrate with existing navigation and communication platforms, further enhancing their competitive edge. While the market benefits from strong drivers, potential restraints include the initial high cost of advanced LED systems and the need for standardization across different regulatory bodies, which could temper the pace of adoption in certain segments.

LED Anti-Collision Light Company Market Share

The global LED anti-collision light market is characterized by a dynamic landscape, currently valued at approximately $XXX million. While not entirely consolidated, key players like Collins Aerospace, Oxley, Whelen, and Honeywell Aerospace hold significant market share, contributing to approximately XX% of the total market value. Innovation remains a critical catalyst, driven by the persistent demand for enhanced aviation safety, marine navigation, and vehicle visibility solutions. Regulatory bodies worldwide, particularly those governing aviation safety, continue to shape market trends by mandating stricter visibility standards, thereby spurring the adoption of advanced LED anti-collision lighting systems. The development of dual-mode anti-collision light and tri-mode anti-collision light technologies signifies this innovation drive, offering more versatile and effective collision avoidance. Substitute products, such as traditional incandescent or halogen-based lights, are rapidly losing ground due to the superior efficiency, longevity, and brightness of LEDs. End-user profiles are diverse, ranging from commercial and military aviation to recreational boating, automotive manufacturers, and even specialized industrial applications. Mergers and acquisitions (M&A) activity is anticipated to remain steady, with projected deal values in the range of $XX million to $XX million over the study period, as larger entities seek to consolidate market presence and acquire innovative technologies from smaller players like AeroLEDs, COBHAM, and SKYFLAR. LFD Limited, Thiesen Electronics Gmbh, and innovative Lighting are actively participating in this evolving ecosystem.

LED Anti-Collision Light Industry Evolution

The LED anti-collision light industry has witnessed a remarkable growth trajectory over the historical period of 2019–2024, with an estimated compound annual growth rate (CAGR) of approximately XX% in market value, reaching an estimated $XXX million by the base year 2025. This robust expansion is directly attributable to escalating concerns surrounding air traffic safety and the imperative to reduce mid-air collisions. The Federal Aviation Administration (FAA) and the European Union Aviation Safety Agency (EASA), among other global regulatory bodies, have played a pivotal role by continuously updating and enforcing stringent visibility and illumination standards for aircraft. This has created a sustained demand for high-performance LED anti-collision lighting systems that offer superior brightness, wider beam angles, and enhanced durability compared to older technologies.

Technological advancements have been a significant driver of this evolution. The transition from incandescent and halogen lighting to solid-state LED technology has offered substantial benefits, including reduced power consumption, lower heat generation, and significantly longer operational lifespans. This translates into reduced maintenance costs and improved reliability for end-users, particularly in the aviation sector where downtime is extremely costly. Furthermore, the miniaturization of LED components has enabled the integration of more sophisticated lighting solutions into smaller platforms, expanding their applicability beyond traditional aircraft to include drones, unmanned aerial vehicles (UAVs), and smaller marine vessels.

Shifting consumer demands, influenced by increased awareness of safety and efficiency, have also contributed to the industry's growth. Operators are increasingly prioritizing systems that offer better performance, lower operating expenses, and compliance with the latest safety regulations. The introduction of dual-mode anti-collision light and tri-mode anti-collision light systems, offering enhanced flexibility and adaptability to varying operational conditions, reflects this evolving demand. Companies like Whelen, Honeywell Aerospace, and Collins Aerospace have been at the forefront of these innovations, investing heavily in research and development to stay ahead of the curve. The market's growth is further underscored by the continuous influx of new entrants and the expansion of existing players into new geographical markets, seeking to capture a larger share of this burgeoning industry. The forecast period of 2025–2033 is expected to see continued strong growth, with an anticipated CAGR of XX%, pushing the market value to an estimated $XXX million by the end of 2033.

Leading Regions, Countries, or Segments in LED Anti-Collision Light

The LED anti-collision light market is currently dominated by the Aircraft segment, showcasing an impressive market share estimated at XX% of the total market value. This dominance is intrinsically linked to the stringent safety regulations governing aviation worldwide. Organizations such as the FAA in the United States and EASA in Europe have continuously mandated the implementation of advanced anti-collision lighting systems to minimize the risk of mid-air collisions. These regulations drive a consistent demand for high-performance LED solutions that offer superior visibility and reliability in all weather conditions and at various altitudes.

Key Drivers in the Aircraft Segment:

- Regulatory Mandates: Continuous updates and enforcement of aviation safety regulations by global aviation authorities are the primary drivers.

- Technological Advancements: The development of more efficient, brighter, and longer-lasting LED anti-collision lights, including dual-mode anti-collision light and tri-mode anti-collision light systems, caters to evolving aircraft needs.

- Fleet Modernization: Airlines and aircraft manufacturers are actively upgrading existing fleets and incorporating advanced lighting solutions into new aircraft to enhance safety and operational efficiency.

- Growth in Air Traffic: The steady increase in global air traffic, both commercial and military, directly translates into a higher demand for safety equipment, including anti-collision lights.

- Increased Focus on Safety: A global heightened awareness and proactive approach towards aviation safety by all stakeholders, including operators, manufacturers, and regulators.

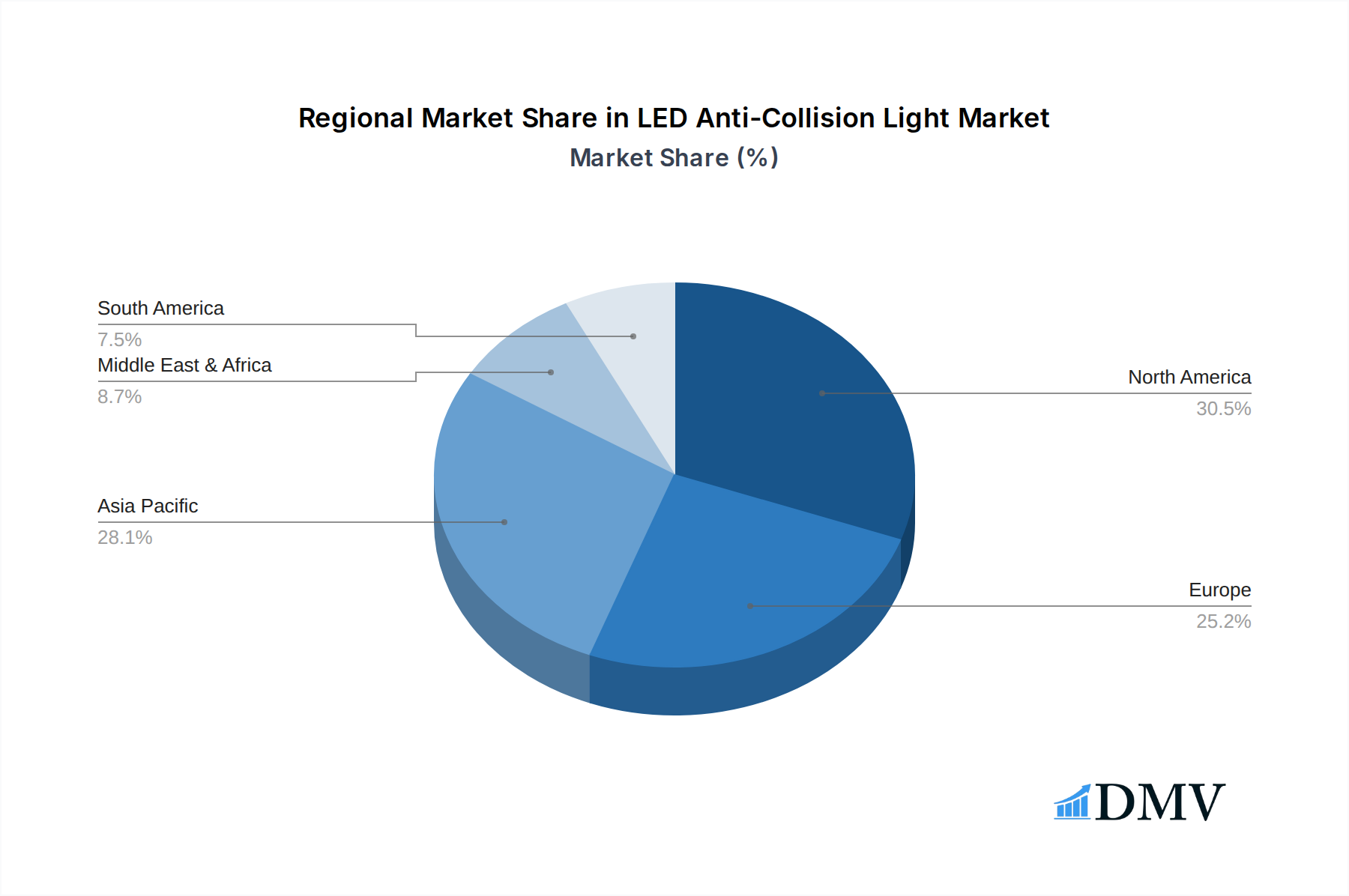

The United States stands out as a leading country within this dominant aircraft segment, accounting for an estimated XX% of the global market share. This leadership is attributed to its vast aerospace industry, significant investment in aviation infrastructure, and the presence of major aerospace manufacturers and regulatory bodies that drive innovation and adoption. North America, as a region, also commands a substantial portion of the market due to the high volume of commercial and military aircraft operations. Companies like Collins Aerospace and Honeywell Aerospace, with significant operations in the US, play a crucial role in shaping the market dynamics within this region. The continuous modernization of the US air traffic control system and the substantial investment in defense and commercial aviation further bolster the demand for advanced LED anti-collision lighting solutions in this key market. The proactive stance on safety and the rapid adoption of new technologies by US-based operators solidify its position as a frontrunner in the LED anti-collision light market.

LED Anti-Collision Light Product Innovations

Product innovations in the LED anti-collision light market are primarily focused on enhancing visibility, reducing power consumption, and increasing the lifespan of these critical safety devices. Manufacturers are developing advanced dual-mode anti-collision light and tri-mode anti-collision light systems that offer dynamic flash patterns and wider illumination angles, significantly improving collision avoidance capabilities for aircraft, vessels, and vehicles. For instance, new product iterations boast an impressive XX% increase in luminous intensity compared to previous generations, coupled with a XX% reduction in power draw. These advancements are driven by the integration of cutting-edge LED chips and sophisticated optical designs, allowing for clearer and more conspicuous signaling, even in challenging environmental conditions. Unique selling propositions often lie in features like integrated diagnostics for real-time performance monitoring, enhanced resistance to vibration and extreme temperatures, and seamless integration with existing avionics and control systems.

Propelling Factors for LED Anti-Collision Light Growth

Several key factors are propelling the growth of the LED anti-collision light market. The relentless pursuit of enhanced safety across aviation, maritime, and automotive sectors is paramount, driving demand for more effective collision avoidance technologies. Stricter regulatory mandates from aviation authorities like the FAA and EASA are forcing widespread adoption of advanced LED anti-collision lighting. Furthermore, the inherent advantages of LED technology, including superior energy efficiency, extended lifespan, and reduced maintenance requirements, contribute significantly to cost savings for end-users. Continuous technological advancements, such as the development of dual-mode anti-collision light and tri-mode anti-collision light systems offering greater versatility, further fuel market expansion. Economic factors, including the growing global aviation industry and increased production of vehicles and vessels, also contribute to the rising demand.

Obstacles in the LED Anti-Collision Light Market

Despite robust growth, the LED anti-collision light market faces several obstacles. Stringent and evolving regulatory compliance can be a significant barrier, requiring substantial investment in research, development, and testing for new products. Supply chain disruptions, as observed in recent global events, can impact the availability of key components and raw materials, leading to production delays and increased costs. Intense competition among established players like Collins Aerospace, Oxley, and Whelen, as well as emerging manufacturers, can lead to price pressures and reduced profit margins. The high initial cost of advanced LED anti-collision systems can also be a deterrent for some smaller operators or in cost-sensitive segments. Furthermore, the need for specialized installation and maintenance expertise can pose challenges for widespread adoption in less developed markets.

Future Opportunities in LED Anti-Collision Light

Emerging opportunities in the LED anti-collision light market are abundant. The rapidly growing drone and UAV sector presents a significant untapped market, requiring specialized and miniaturized anti-collision lighting solutions. The expansion of autonomous vehicle technology in the automotive sector will necessitate sophisticated visual signaling and collision avoidance systems, creating new avenues for LED anti-collision lights. Furthermore, advancements in smart lighting technologies, incorporating features like networked communication and adaptive illumination, offer potential for enhanced safety and operational efficiency. The increasing focus on sustainable and energy-efficient solutions will continue to drive demand for LED-based products across all application segments. The development of even more advanced tri-mode anti-collision light systems with integrated sensors will unlock further market potential.

Major Players in the LED Anti-Collision Light Ecosystem

- Collins Aerospace

- Oxley

- Whelen

- Honeywell Aerospace

- LFD Limited

- AeroLEDs

- COBHAM

- SKYFLAR

- NSE INDUSTRIES

- Soderberg Manufacturing

- NAASCO

- Innovative Lighting

- Thiesen Electronics Gmbh

- Anhang Technology

Key Developments in LED Anti-Collision Light Industry

- 2023: Launch of next-generation tri-mode anti-collision light with enhanced visibility and reduced power consumption by Whelen, significantly impacting aviation safety standards.

- 2022: Collins Aerospace announces a strategic partnership with a leading drone manufacturer to integrate advanced LED anti-collision lighting into their unmanned aerial vehicle platforms, signaling a major expansion into the UAV market.

- 2021: Honeywell Aerospace receives FAA certification for its innovative dual-mode anti-collision light system, enhancing safety for a wide range of commercial aircraft.

- 2020: Oxley expands its manufacturing capabilities to meet the growing global demand for military-grade LED anti-collision lights, securing several large defense contracts.

- 2019: LFD Limited introduces a new line of robust LED anti-collision lights designed for extreme marine environments, addressing a key need in the maritime sector.

Strategic LED Anti-Collision Light Market Forecast

The strategic outlook for the LED anti-collision light market is highly optimistic, driven by an unwavering commitment to safety and continuous technological innovation. The forecast period of 2025–2033 is projected to witness substantial growth, fueled by the increasing adoption of advanced dual-mode anti-collision light and tri-mode anti-collision light systems across aviation, maritime, and automotive sectors. The robust regulatory environment, coupled with the superior performance and cost-efficiency of LED technology, will continue to be key growth catalysts. Emerging applications in the drone and autonomous vehicle markets, along with the ongoing modernization of existing fleets, present significant untapped opportunities. Stakeholders can anticipate sustained innovation and strategic collaborations as companies like Collins Aerospace, Honeywell Aerospace, and Whelen vie for market leadership. The market's trajectory indicates a strong upward trend, promising significant returns for invested parties.

LED Anti-Collision Light Segmentation

-

1. Application

- 1.1. Aircraft

- 1.2. Vessels

- 1.3. Vehicles

- 1.4. Others

-

2. Types

- 2.1. Dual-Mode Anti-Collision Light

- 2.2. Tri-Mode Anti-Collision Light

LED Anti-Collision Light Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

LED Anti-Collision Light Regional Market Share

Geographic Coverage of LED Anti-Collision Light

LED Anti-Collision Light REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global LED Anti-Collision Light Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Aircraft

- 5.1.2. Vessels

- 5.1.3. Vehicles

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Dual-Mode Anti-Collision Light

- 5.2.2. Tri-Mode Anti-Collision Light

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America LED Anti-Collision Light Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Aircraft

- 6.1.2. Vessels

- 6.1.3. Vehicles

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Dual-Mode Anti-Collision Light

- 6.2.2. Tri-Mode Anti-Collision Light

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America LED Anti-Collision Light Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Aircraft

- 7.1.2. Vessels

- 7.1.3. Vehicles

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Dual-Mode Anti-Collision Light

- 7.2.2. Tri-Mode Anti-Collision Light

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe LED Anti-Collision Light Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Aircraft

- 8.1.2. Vessels

- 8.1.3. Vehicles

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Dual-Mode Anti-Collision Light

- 8.2.2. Tri-Mode Anti-Collision Light

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa LED Anti-Collision Light Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Aircraft

- 9.1.2. Vessels

- 9.1.3. Vehicles

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Dual-Mode Anti-Collision Light

- 9.2.2. Tri-Mode Anti-Collision Light

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific LED Anti-Collision Light Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Aircraft

- 10.1.2. Vessels

- 10.1.3. Vehicles

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Dual-Mode Anti-Collision Light

- 10.2.2. Tri-Mode Anti-Collision Light

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Collins Aerospace

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Oxley

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Whelen

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Honeywell Aerospace

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 LFD Limited

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 AeroLEDs

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 COBHAM

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 SKYFLAR

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 NSE INDUSTRIES

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Soderberg Manufacturing

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 NAASCO

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Innovative Lighting

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Thiesen Electronics Gmbh

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Anhang Technology

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.1 Collins Aerospace

List of Figures

- Figure 1: Global LED Anti-Collision Light Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America LED Anti-Collision Light Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America LED Anti-Collision Light Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America LED Anti-Collision Light Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America LED Anti-Collision Light Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America LED Anti-Collision Light Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America LED Anti-Collision Light Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America LED Anti-Collision Light Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America LED Anti-Collision Light Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America LED Anti-Collision Light Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America LED Anti-Collision Light Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America LED Anti-Collision Light Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America LED Anti-Collision Light Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe LED Anti-Collision Light Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe LED Anti-Collision Light Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe LED Anti-Collision Light Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe LED Anti-Collision Light Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe LED Anti-Collision Light Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe LED Anti-Collision Light Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa LED Anti-Collision Light Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa LED Anti-Collision Light Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa LED Anti-Collision Light Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa LED Anti-Collision Light Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa LED Anti-Collision Light Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa LED Anti-Collision Light Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific LED Anti-Collision Light Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific LED Anti-Collision Light Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific LED Anti-Collision Light Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific LED Anti-Collision Light Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific LED Anti-Collision Light Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific LED Anti-Collision Light Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global LED Anti-Collision Light Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global LED Anti-Collision Light Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global LED Anti-Collision Light Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global LED Anti-Collision Light Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global LED Anti-Collision Light Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global LED Anti-Collision Light Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States LED Anti-Collision Light Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada LED Anti-Collision Light Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico LED Anti-Collision Light Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global LED Anti-Collision Light Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global LED Anti-Collision Light Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global LED Anti-Collision Light Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil LED Anti-Collision Light Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina LED Anti-Collision Light Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America LED Anti-Collision Light Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global LED Anti-Collision Light Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global LED Anti-Collision Light Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global LED Anti-Collision Light Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom LED Anti-Collision Light Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany LED Anti-Collision Light Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France LED Anti-Collision Light Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy LED Anti-Collision Light Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain LED Anti-Collision Light Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia LED Anti-Collision Light Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux LED Anti-Collision Light Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics LED Anti-Collision Light Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe LED Anti-Collision Light Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global LED Anti-Collision Light Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global LED Anti-Collision Light Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global LED Anti-Collision Light Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey LED Anti-Collision Light Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel LED Anti-Collision Light Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC LED Anti-Collision Light Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa LED Anti-Collision Light Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa LED Anti-Collision Light Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa LED Anti-Collision Light Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global LED Anti-Collision Light Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global LED Anti-Collision Light Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global LED Anti-Collision Light Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China LED Anti-Collision Light Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India LED Anti-Collision Light Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan LED Anti-Collision Light Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea LED Anti-Collision Light Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN LED Anti-Collision Light Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania LED Anti-Collision Light Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific LED Anti-Collision Light Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the LED Anti-Collision Light?

The projected CAGR is approximately 6.6%.

2. Which companies are prominent players in the LED Anti-Collision Light?

Key companies in the market include Collins Aerospace, Oxley, Whelen, Honeywell Aerospace, LFD Limited, AeroLEDs, COBHAM, SKYFLAR, NSE INDUSTRIES, Soderberg Manufacturing, NAASCO, Innovative Lighting, Thiesen Electronics Gmbh, Anhang Technology.

3. What are the main segments of the LED Anti-Collision Light?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "LED Anti-Collision Light," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the LED Anti-Collision Light report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the LED Anti-Collision Light?

To stay informed about further developments, trends, and reports in the LED Anti-Collision Light, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence