Key Insights

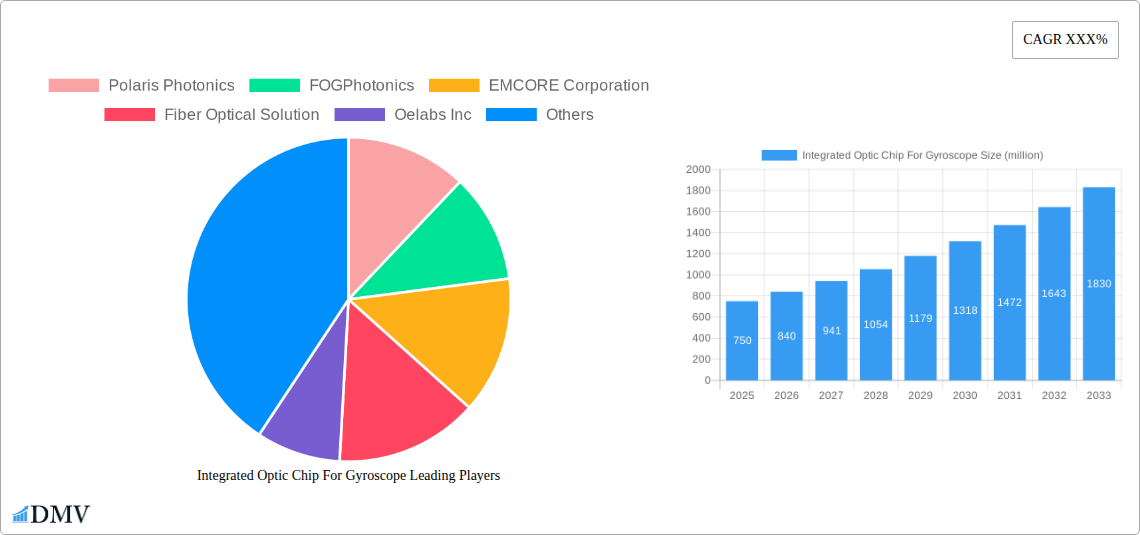

The global market for Integrated Optic Chips for Gyroscopes is poised for substantial growth, projected to reach approximately $750 million in 2025. This expansion is driven by the increasing demand for high-precision navigation and stabilization solutions across a multitude of industries. The aerospace sector, with its stringent requirements for accurate inertial navigation systems in aircraft and spacecraft, remains a primary consumer. Similarly, the automotive industry is witnessing a surge in adoption for advanced driver-assistance systems (ADAS) and autonomous driving technologies, where precise gyro functionality is paramount. The growing sophistication of consumer electronics, including drones and virtual reality headsets, also contributes significantly to market momentum. Furthermore, the ongoing miniaturization and cost reduction of these optic chips are making them more accessible for a wider range of applications, further fueling market penetration.

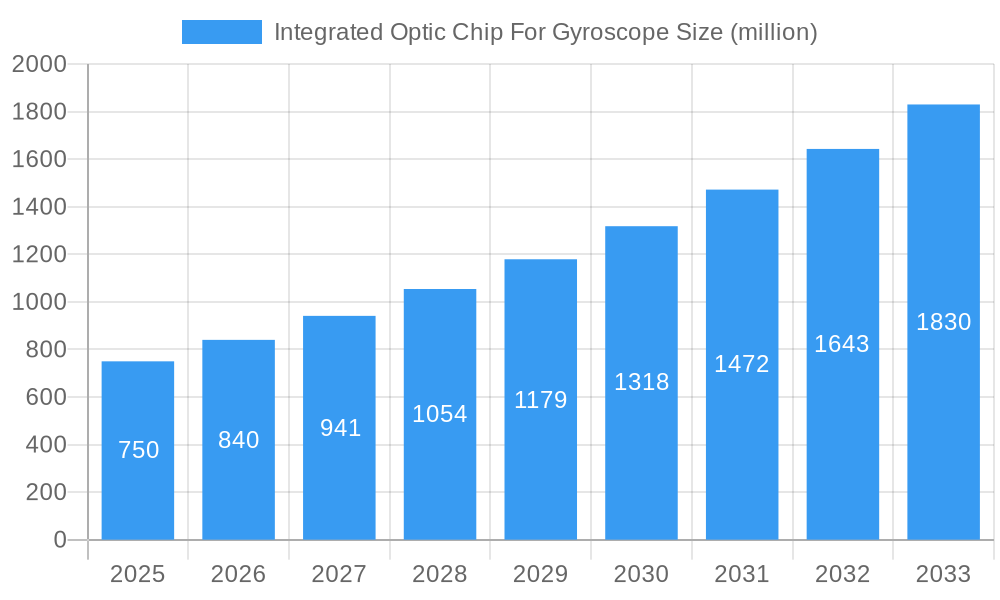

Integrated Optic Chip For Gyroscope Market Size (In Million)

The projected compound annual growth rate (CAGR) of around 12% for the forecast period of 2025-2033 indicates a robust expansion, pushing the market value well beyond $1.5 billion by 2033. Key trends influencing this growth include advancements in silicon photonics, enabling higher integration density and performance, and the development of novel materials for enhanced sensitivity and reduced noise. The increasing emphasis on miniaturized, lightweight, and power-efficient navigation solutions will continue to be a significant driver. However, challenges such as high initial research and development costs and the need for specialized manufacturing expertise could pose some restraints. Despite these hurdles, the inherent advantages of integrated optic gyroscopes – namely their superior accuracy, vibration resistance, and faster response times compared to traditional mechanical gyroscopes – ensure their continued relevance and growing importance across diverse technological landscapes.

Integrated Optic Chip For Gyroscope Company Market Share

Integrated Optic Chip For Gyroscope Market Composition & Trends

This comprehensive report delves into the intricate market composition and evolving trends of the integrated optic chip for gyroscope market. We analyze the landscape of key players, including Polaris Photonics, FOGPhotonics, EMCORE Corporation, Fiber Optical Solution, Oelabs Inc, KVH Industries, Optilab, PANWOO Equpiment Consulting, Box Optronics Technology, OELABS Inc, One Silicon Chip Photonics, and HongKong Liocrebif Technology. The market exhibits a moderate concentration, with innovation catalysts primarily driven by advancements in fiber optic gyroscope (FOG) technology and silicon photonics. Regulatory landscapes, particularly concerning defense and aerospace applications, are significant influencing factors. While direct substitute products are limited, advancements in MEMS gyroscopes present a competitive alternative in certain lower-performance segments. End-user profiles span critical sectors such as aerospace, ship, automotive, and other specialized industrial applications. Mergers and acquisitions (M&A) activities are present, with estimated deal values in the range of $50 million to $500 million within the historical period. Market share distribution is dynamic, with established players holding significant portions, while emerging companies are focusing on niche applications and technological differentiation.

- Market Concentration: Moderate, with key players investing heavily in R&D.

- Innovation Catalysts: Miniaturization, cost reduction, enhanced accuracy, and increased bandwidth.

- Regulatory Landscapes: Stringent quality and performance standards, especially for aerospace and defense.

- Substitute Products: MEMS gyroscopes for cost-sensitive applications.

- End-User Profiles: Defense contractors, satellite manufacturers, autonomous vehicle developers, maritime navigation system providers.

- M&A Activities: Strategic acquisitions aimed at consolidating market share and acquiring specialized technologies. Estimated M&A deal values: $50 million to $500 million.

Integrated Optic Chip For Gyroscope Industry Evolution

The integrated optic chip for gyroscope industry has witnessed a transformative evolution, driven by relentless technological innovation and an expanding array of demanding applications. The Study Period (2019–2033) encapsulates a significant growth trajectory, with the Base Year (2025) and Estimated Year (2025) serving as crucial benchmarks for understanding current market dynamics and future potential. The Forecast Period (2025–2033) projects a robust Compound Annual Growth Rate (CAGR) of approximately 12.5%, fueled by escalating demand for high-precision, compact, and cost-effective gyroscopes.

Technological advancements have been the primary engine of this evolution. The integration of optical components onto a single chip, or integrated optic chip, has dramatically reduced the size, weight, and power consumption of traditional fiber optic gyroscopes. This miniaturization, coupled with enhanced performance metrics such as improved angular rate sensitivity and reduced drift, has unlocked new application possibilities. Early stages saw the adoption of planar optics and bulk components, which were later superseded by advancements in waveguide fabrication and lithography techniques. The transition to silicon photonics has been particularly impactful, enabling mass production at lower costs and facilitating the integration of additional functionalities like signal processing and control electronics directly onto the chip.

Shifting consumer and industry demands have also played a pivotal role. The burgeoning automotive sector's need for advanced driver-assistance systems (ADAS) and autonomous driving capabilities necessitates highly accurate and reliable navigation and stabilization systems. Similarly, the aerospace industry's continuous pursuit of lighter, more efficient, and more robust inertial navigation systems for aircraft, drones, and spacecraft has propelled the demand for integrated optic gyroscopes. The ship and maritime sectors are increasingly adopting these technologies for enhanced navigation, stability control, and platform stabilization in increasingly complex operational environments. The Historical Period (2019–2024) showcases a steady upward trend, with early adopters in defense and aerospace paving the way for broader market penetration. This period was characterized by significant R&D investments, leading to performance breakthroughs and the initial commercialization of chip-scale FOGs. The adoption metrics during this time were primarily driven by specialized high-value applications, with penetration in mainstream markets beginning to accelerate in the latter half of the historical period.

Leading Regions, Countries, or Segments in Integrated Optic Chip For Gyroscope

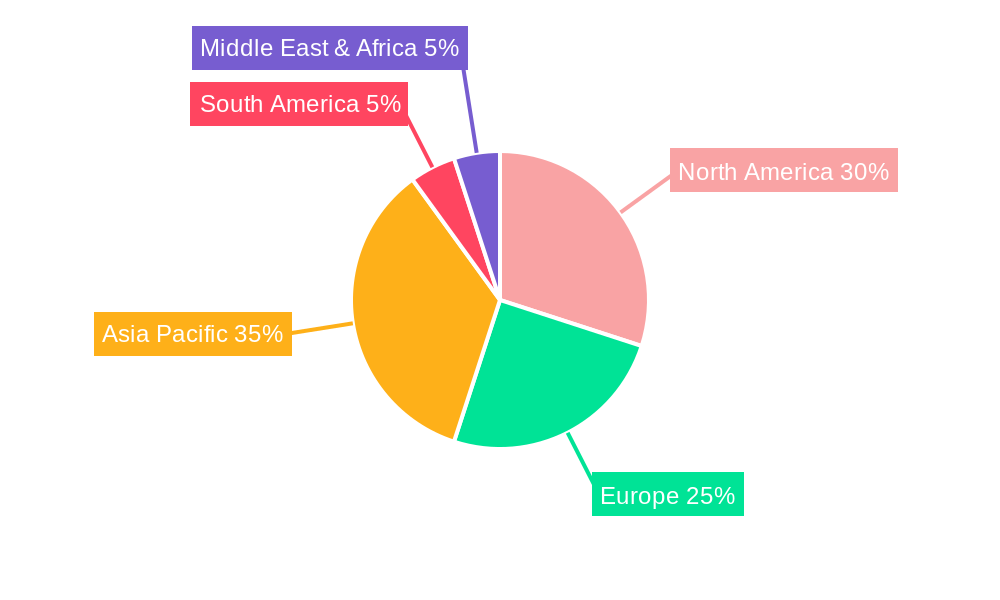

The integrated optic chip for gyroscope market is experiencing significant growth across various regions, with North America currently leading in terms of market share and adoption. This dominance is driven by a confluence of factors including robust government investment in defense and aerospace programs, a thriving automotive industry pushing for ADAS and autonomous driving solutions, and a strong ecosystem of research and development institutions. The region benefits from early-stage adoption of cutting-edge technologies and a proactive regulatory environment that supports innovation.

Within the Application segment, Aerospace remains the most significant contributor to market revenue, accounting for an estimated 45% of the total market share. This is due to the critical need for high-precision, reliable, and miniaturized inertial navigation systems in aircraft, satellites, and unmanned aerial vehicles (UAVs). The stringent performance requirements and high-value nature of aerospace applications drive substantial investment in advanced integrated optic chip technologies. The Automotive segment is emerging as a rapidly growing force, projected to capture 30% of the market share by the end of the forecast period. The increasing adoption of ADAS features and the development of fully autonomous vehicles are creating an insatiable demand for accurate and cost-effective gyroscopes for navigation, stabilization, and sensor fusion. The Ship segment, while smaller at an estimated 20% market share, is also experiencing steady growth, driven by the need for advanced navigation, stabilization systems for offshore platforms, and enhanced maneuverability in commercial and defense vessels. Others, encompassing applications in robotics, industrial automation, and scientific instrumentation, represent the remaining 5% but offer significant potential for niche growth.

In terms of Type, the 1310nm wavelength segment currently holds the largest market share, estimated at 55%. This is attributed to its well-established performance characteristics and compatibility with existing fiber optic infrastructure. The 1550nm segment is gaining traction and is projected to grow at a faster CAGR of approximately 15%, driven by its lower attenuation in optical fibers and suitability for long-haul applications and higher bandwidth requirements. The Others type segment, which includes emerging wavelengths and multi-wavelength solutions, is expected to see substantial growth as new technologies mature and find application-specific advantages.

- Dominant Region: North America

- Key Drivers:

- Significant defense and aerospace R&D spending, with an estimated $150 billion invested historically.

- Leading automotive manufacturers accelerating ADAS and autonomous vehicle development.

- Presence of major integrated optic chip manufacturers and research institutions.

- Supportive government initiatives and grants for photonics innovation.

- Key Drivers:

- Dominant Application Segment: Aerospace

- In-depth Analysis: Critical for aircraft navigation, satellite attitude control, and drone stabilization. High reliability and miniaturization are paramount. Market size estimated at $700 million in the base year.

- Key Drivers:

- Increasing demand for advanced UAVs for surveillance and delivery.

- New satellite constellation deployments requiring precise orientation.

- Stringent safety regulations in commercial aviation.

- Emerging Application Segment: Automotive

- In-depth Analysis: Essential for ADAS, autonomous driving, and electronic stability control. Cost-effectiveness and mass-producibility are key. Market size projected to reach $600 million by 2033.

- Key Drivers:

- Government mandates for ADAS features.

- Consumer demand for safer and more convenient driving experiences.

- Technological advancements in sensor fusion.

- Dominant Type: 1310nm

- In-depth Analysis: Well-established technology offering a good balance of performance and cost. Dominates in existing applications. Market share at 55%.

- Key Drivers:

- Mature manufacturing processes and supply chains.

- Proven reliability in various operational environments.

- Growing Type: 1550nm

- In-depth Analysis: Offers lower optical loss and improved performance in longer fiber lengths, making it suitable for advanced applications. Projected CAGR of 15%.

- Key Drivers:

- Demand for higher bandwidth and longer reach in complex systems.

- Advancements in laser and detector technologies.

Integrated Optic Chip For Gyroscope Product Innovations

Recent product innovations in the integrated optic chip for gyroscope market are revolutionizing performance and miniaturization. Companies are developing chip-scale fiber optic gyroscopes (CS-FOGs) that integrate all optical components onto a single silicon photonic chip. These advancements offer unprecedented size reduction, power efficiency, and cost-effectiveness compared to traditional FOGs. Innovations include improved waveguide designs for enhanced light confinement and reduced optical loss, leading to higher sensitivity and lower drift rates, often achieving bias stability of 0.01°/hour. Furthermore, the integration of on-chip signal processing and calibration algorithms is streamlining deployment and improving accuracy in real-time. These innovations are paving the way for wider adoption in demanding applications like automotive ADAS, advanced drone navigation, and compact inertial measurement units (IMUs). The unique selling proposition lies in achieving near-inertial-grade performance in a fraction of the size and cost.

Propelling Factors for Integrated Optic Chip For Gyroscope Growth

Several key factors are propelling the growth of the integrated optic chip for gyroscope market. Firstly, the relentless demand for miniaturization and reduced SWaP (Size, Weight, and Power) across industries like aerospace, defense, and automotive is a significant driver. Secondly, advancements in silicon photonics and lithography techniques are enabling cost-effective mass production and improved performance metrics, such as bias stability in the range of 0.005°/hour to 0.1°/hour. Thirdly, the increasing complexity of autonomous systems, including autonomous vehicles and drones, necessitates highly accurate and reliable inertial navigation solutions. Finally, government initiatives and defense spending in key regions, particularly for advanced navigation and guidance systems, are providing substantial impetus to market expansion.

Obstacles in the Integrated Optic Chip For Gyroscope Market

Despite the robust growth potential, the integrated optic chip for gyroscope market faces several obstacles. High initial R&D and manufacturing costs for novel silicon photonics processes can be a barrier for smaller players. Stringent qualification and certification processes, especially for aerospace and defense applications, can lengthen time-to-market and add significant expense. Supply chain disruptions for specialized photonic components and raw materials, as witnessed historically, can impact production volumes and lead times. Furthermore, while improving, the performance gap compared to the highest-end traditional FOGs in extremely demanding applications can still limit adoption in certain niche segments.

Future Opportunities in Integrated Optic Chip For Gyroscope

The future of the integrated optic chip for gyroscope market is ripe with opportunities. The burgeoning autonomous vehicle market represents a massive growth avenue, with projected adoption rates reaching millions of units annually. The increasing demand for space-based applications, including satellite constellations and lunar missions, will drive the need for highly reliable and compact gyroscopes. Furthermore, the exploration of new materials and fabrication techniques, such as heterogeneously integrated silicon photonics, promises further performance enhancements and cost reductions. The expansion of industrial automation and robotics requiring precise motion control also presents a significant, albeit fragmented, opportunity.

Major Players in the Integrated Optic Chip For Gyroscope Ecosystem

- Polaris Photonics

- FOGPhotonics

- EMCORE Corporation

- Fiber Optical Solution

- Oelabs Inc

- KVH Industries

- Optilab

- PANWOO Equpiment Consulting

- Box Optronics Technology

- OELABS Inc

- One Silicon Chip Photonics

- HongKong Liocrebif Technology

Key Developments in Integrated Optic Chip For Gyroscope Industry

- 2023 Q4: EMCORE Corporation announces a new generation of integrated optic chip gyroscopes with improved bias stability of 0.008°/hour.

- 2024 Q1: Polaris Photonics unveils a silicon photonic chip-scale FOG for automotive ADAS applications, targeting mass production.

- 2024 Q2: KVH Industries expands its fiber optic gyroscope product line with enhanced temperature compensation for challenging environments.

- 2024 Q3: One Silicon Chip Photonics achieves a breakthrough in waveguide fabrication, enabling smaller footprints and higher integration densities.

- 2024 Q4: FOGPhotonics secures a significant contract for integrated optic chip gyroscopes for a new satellite constellation.

- 2025 Q1: Oelabs Inc demonstrates a novel packaging technology for integrated optic chip gyroscopes, enhancing ruggedness and reliability.

- 2025 Q2: Box Optronics Technology introduces a multi-wavelength integrated optic chip for advanced navigation and sensing.

- 2025 Q3: Fiber Optical Solution announces strategic partnerships to scale up production of its high-performance integrated optic chip gyroscopes.

- 2025 Q4: PANWOO Equpiment Consulting forecasts continued strong growth in the automotive segment for integrated optic chip gyroscopes.

- 2026 Q1: HongKong Liocrebif Technology highlights advancements in hybrid integration for cost-effective chip-scale FOGs.

Strategic Integrated Optic Chip For Gyroscope Market Forecast

The strategic outlook for the integrated optic chip for gyroscope market is exceptionally promising, driven by relentless innovation and expanding applications. The market is projected to experience sustained growth, with a projected market size of $2.5 billion by 2033. Key growth catalysts include the increasing adoption of autonomous systems across automotive, aerospace, and industrial sectors, demanding high-precision navigation. Continued advancements in silicon photonics integration will further drive miniaturization, cost reduction, and performance enhancements, making these gyroscopes accessible for a wider range of applications. Strategic partnerships and acquisitions are expected to consolidate the market and accelerate technological development, ensuring that the integrated optic chip for gyroscope market remains at the forefront of inertial sensing technology.

Integrated Optic Chip For Gyroscope Segmentation

-

1. Application

- 1.1. Aerospace

- 1.2. Ship

- 1.3. Automotive

- 1.4. Others

-

2. Type

- 2.1. 1310nm

- 2.2. 1550nm

- 2.3. Others

Integrated Optic Chip For Gyroscope Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Integrated Optic Chip For Gyroscope Regional Market Share

Geographic Coverage of Integrated Optic Chip For Gyroscope

Integrated Optic Chip For Gyroscope REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XXX% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Aerospace

- 5.1.2. Ship

- 5.1.3. Automotive

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. 1310nm

- 5.2.2. 1550nm

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Integrated Optic Chip For Gyroscope Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Aerospace

- 6.1.2. Ship

- 6.1.3. Automotive

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. 1310nm

- 6.2.2. 1550nm

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Integrated Optic Chip For Gyroscope Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Aerospace

- 7.1.2. Ship

- 7.1.3. Automotive

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. 1310nm

- 7.2.2. 1550nm

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Integrated Optic Chip For Gyroscope Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Aerospace

- 8.1.2. Ship

- 8.1.3. Automotive

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. 1310nm

- 8.2.2. 1550nm

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Integrated Optic Chip For Gyroscope Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Aerospace

- 9.1.2. Ship

- 9.1.3. Automotive

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. 1310nm

- 9.2.2. 1550nm

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Integrated Optic Chip For Gyroscope Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Aerospace

- 10.1.2. Ship

- 10.1.3. Automotive

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. 1310nm

- 10.2.2. 1550nm

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Integrated Optic Chip For Gyroscope Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Aerospace

- 11.1.2. Ship

- 11.1.3. Automotive

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. 1310nm

- 11.2.2. 1550nm

- 11.2.3. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Polaris Photonics

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 FOGPhotonics

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 EMCORE Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Fiber Optical Solution

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Oelabs Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 KVH Industries

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Optilab

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 PANWOO Equpiment Consulting

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Box Optronics Technology

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 OELABS Inc

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 One Silicon Chip Photonics

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 HongKong Liocrebif Technology

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 Polaris Photonics

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Integrated Optic Chip For Gyroscope Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: Global Integrated Optic Chip For Gyroscope Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Integrated Optic Chip For Gyroscope Revenue (million), by Application 2025 & 2033

- Figure 4: North America Integrated Optic Chip For Gyroscope Volume (K), by Application 2025 & 2033

- Figure 5: North America Integrated Optic Chip For Gyroscope Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Integrated Optic Chip For Gyroscope Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Integrated Optic Chip For Gyroscope Revenue (million), by Type 2025 & 2033

- Figure 8: North America Integrated Optic Chip For Gyroscope Volume (K), by Type 2025 & 2033

- Figure 9: North America Integrated Optic Chip For Gyroscope Revenue Share (%), by Type 2025 & 2033

- Figure 10: North America Integrated Optic Chip For Gyroscope Volume Share (%), by Type 2025 & 2033

- Figure 11: North America Integrated Optic Chip For Gyroscope Revenue (million), by Country 2025 & 2033

- Figure 12: North America Integrated Optic Chip For Gyroscope Volume (K), by Country 2025 & 2033

- Figure 13: North America Integrated Optic Chip For Gyroscope Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Integrated Optic Chip For Gyroscope Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Integrated Optic Chip For Gyroscope Revenue (million), by Application 2025 & 2033

- Figure 16: South America Integrated Optic Chip For Gyroscope Volume (K), by Application 2025 & 2033

- Figure 17: South America Integrated Optic Chip For Gyroscope Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Integrated Optic Chip For Gyroscope Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Integrated Optic Chip For Gyroscope Revenue (million), by Type 2025 & 2033

- Figure 20: South America Integrated Optic Chip For Gyroscope Volume (K), by Type 2025 & 2033

- Figure 21: South America Integrated Optic Chip For Gyroscope Revenue Share (%), by Type 2025 & 2033

- Figure 22: South America Integrated Optic Chip For Gyroscope Volume Share (%), by Type 2025 & 2033

- Figure 23: South America Integrated Optic Chip For Gyroscope Revenue (million), by Country 2025 & 2033

- Figure 24: South America Integrated Optic Chip For Gyroscope Volume (K), by Country 2025 & 2033

- Figure 25: South America Integrated Optic Chip For Gyroscope Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Integrated Optic Chip For Gyroscope Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Integrated Optic Chip For Gyroscope Revenue (million), by Application 2025 & 2033

- Figure 28: Europe Integrated Optic Chip For Gyroscope Volume (K), by Application 2025 & 2033

- Figure 29: Europe Integrated Optic Chip For Gyroscope Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Integrated Optic Chip For Gyroscope Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Integrated Optic Chip For Gyroscope Revenue (million), by Type 2025 & 2033

- Figure 32: Europe Integrated Optic Chip For Gyroscope Volume (K), by Type 2025 & 2033

- Figure 33: Europe Integrated Optic Chip For Gyroscope Revenue Share (%), by Type 2025 & 2033

- Figure 34: Europe Integrated Optic Chip For Gyroscope Volume Share (%), by Type 2025 & 2033

- Figure 35: Europe Integrated Optic Chip For Gyroscope Revenue (million), by Country 2025 & 2033

- Figure 36: Europe Integrated Optic Chip For Gyroscope Volume (K), by Country 2025 & 2033

- Figure 37: Europe Integrated Optic Chip For Gyroscope Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Integrated Optic Chip For Gyroscope Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Integrated Optic Chip For Gyroscope Revenue (million), by Application 2025 & 2033

- Figure 40: Middle East & Africa Integrated Optic Chip For Gyroscope Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Integrated Optic Chip For Gyroscope Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Integrated Optic Chip For Gyroscope Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Integrated Optic Chip For Gyroscope Revenue (million), by Type 2025 & 2033

- Figure 44: Middle East & Africa Integrated Optic Chip For Gyroscope Volume (K), by Type 2025 & 2033

- Figure 45: Middle East & Africa Integrated Optic Chip For Gyroscope Revenue Share (%), by Type 2025 & 2033

- Figure 46: Middle East & Africa Integrated Optic Chip For Gyroscope Volume Share (%), by Type 2025 & 2033

- Figure 47: Middle East & Africa Integrated Optic Chip For Gyroscope Revenue (million), by Country 2025 & 2033

- Figure 48: Middle East & Africa Integrated Optic Chip For Gyroscope Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Integrated Optic Chip For Gyroscope Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Integrated Optic Chip For Gyroscope Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Integrated Optic Chip For Gyroscope Revenue (million), by Application 2025 & 2033

- Figure 52: Asia Pacific Integrated Optic Chip For Gyroscope Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Integrated Optic Chip For Gyroscope Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Integrated Optic Chip For Gyroscope Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Integrated Optic Chip For Gyroscope Revenue (million), by Type 2025 & 2033

- Figure 56: Asia Pacific Integrated Optic Chip For Gyroscope Volume (K), by Type 2025 & 2033

- Figure 57: Asia Pacific Integrated Optic Chip For Gyroscope Revenue Share (%), by Type 2025 & 2033

- Figure 58: Asia Pacific Integrated Optic Chip For Gyroscope Volume Share (%), by Type 2025 & 2033

- Figure 59: Asia Pacific Integrated Optic Chip For Gyroscope Revenue (million), by Country 2025 & 2033

- Figure 60: Asia Pacific Integrated Optic Chip For Gyroscope Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Integrated Optic Chip For Gyroscope Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Integrated Optic Chip For Gyroscope Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Integrated Optic Chip For Gyroscope Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Integrated Optic Chip For Gyroscope Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Integrated Optic Chip For Gyroscope Revenue million Forecast, by Type 2020 & 2033

- Table 4: Global Integrated Optic Chip For Gyroscope Volume K Forecast, by Type 2020 & 2033

- Table 5: Global Integrated Optic Chip For Gyroscope Revenue million Forecast, by Region 2020 & 2033

- Table 6: Global Integrated Optic Chip For Gyroscope Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Integrated Optic Chip For Gyroscope Revenue million Forecast, by Application 2020 & 2033

- Table 8: Global Integrated Optic Chip For Gyroscope Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Integrated Optic Chip For Gyroscope Revenue million Forecast, by Type 2020 & 2033

- Table 10: Global Integrated Optic Chip For Gyroscope Volume K Forecast, by Type 2020 & 2033

- Table 11: Global Integrated Optic Chip For Gyroscope Revenue million Forecast, by Country 2020 & 2033

- Table 12: Global Integrated Optic Chip For Gyroscope Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Integrated Optic Chip For Gyroscope Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: United States Integrated Optic Chip For Gyroscope Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Integrated Optic Chip For Gyroscope Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Canada Integrated Optic Chip For Gyroscope Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Integrated Optic Chip For Gyroscope Revenue (million) Forecast, by Application 2020 & 2033

- Table 18: Mexico Integrated Optic Chip For Gyroscope Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Integrated Optic Chip For Gyroscope Revenue million Forecast, by Application 2020 & 2033

- Table 20: Global Integrated Optic Chip For Gyroscope Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Integrated Optic Chip For Gyroscope Revenue million Forecast, by Type 2020 & 2033

- Table 22: Global Integrated Optic Chip For Gyroscope Volume K Forecast, by Type 2020 & 2033

- Table 23: Global Integrated Optic Chip For Gyroscope Revenue million Forecast, by Country 2020 & 2033

- Table 24: Global Integrated Optic Chip For Gyroscope Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Integrated Optic Chip For Gyroscope Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Brazil Integrated Optic Chip For Gyroscope Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Integrated Optic Chip For Gyroscope Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Argentina Integrated Optic Chip For Gyroscope Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Integrated Optic Chip For Gyroscope Revenue (million) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Integrated Optic Chip For Gyroscope Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Integrated Optic Chip For Gyroscope Revenue million Forecast, by Application 2020 & 2033

- Table 32: Global Integrated Optic Chip For Gyroscope Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Integrated Optic Chip For Gyroscope Revenue million Forecast, by Type 2020 & 2033

- Table 34: Global Integrated Optic Chip For Gyroscope Volume K Forecast, by Type 2020 & 2033

- Table 35: Global Integrated Optic Chip For Gyroscope Revenue million Forecast, by Country 2020 & 2033

- Table 36: Global Integrated Optic Chip For Gyroscope Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Integrated Optic Chip For Gyroscope Revenue (million) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Integrated Optic Chip For Gyroscope Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Integrated Optic Chip For Gyroscope Revenue (million) Forecast, by Application 2020 & 2033

- Table 40: Germany Integrated Optic Chip For Gyroscope Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Integrated Optic Chip For Gyroscope Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: France Integrated Optic Chip For Gyroscope Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Integrated Optic Chip For Gyroscope Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: Italy Integrated Optic Chip For Gyroscope Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Integrated Optic Chip For Gyroscope Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Spain Integrated Optic Chip For Gyroscope Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Integrated Optic Chip For Gyroscope Revenue (million) Forecast, by Application 2020 & 2033

- Table 48: Russia Integrated Optic Chip For Gyroscope Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Integrated Optic Chip For Gyroscope Revenue (million) Forecast, by Application 2020 & 2033

- Table 50: Benelux Integrated Optic Chip For Gyroscope Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Integrated Optic Chip For Gyroscope Revenue (million) Forecast, by Application 2020 & 2033

- Table 52: Nordics Integrated Optic Chip For Gyroscope Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Integrated Optic Chip For Gyroscope Revenue (million) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Integrated Optic Chip For Gyroscope Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Integrated Optic Chip For Gyroscope Revenue million Forecast, by Application 2020 & 2033

- Table 56: Global Integrated Optic Chip For Gyroscope Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Integrated Optic Chip For Gyroscope Revenue million Forecast, by Type 2020 & 2033

- Table 58: Global Integrated Optic Chip For Gyroscope Volume K Forecast, by Type 2020 & 2033

- Table 59: Global Integrated Optic Chip For Gyroscope Revenue million Forecast, by Country 2020 & 2033

- Table 60: Global Integrated Optic Chip For Gyroscope Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Integrated Optic Chip For Gyroscope Revenue (million) Forecast, by Application 2020 & 2033

- Table 62: Turkey Integrated Optic Chip For Gyroscope Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Integrated Optic Chip For Gyroscope Revenue (million) Forecast, by Application 2020 & 2033

- Table 64: Israel Integrated Optic Chip For Gyroscope Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Integrated Optic Chip For Gyroscope Revenue (million) Forecast, by Application 2020 & 2033

- Table 66: GCC Integrated Optic Chip For Gyroscope Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Integrated Optic Chip For Gyroscope Revenue (million) Forecast, by Application 2020 & 2033

- Table 68: North Africa Integrated Optic Chip For Gyroscope Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Integrated Optic Chip For Gyroscope Revenue (million) Forecast, by Application 2020 & 2033

- Table 70: South Africa Integrated Optic Chip For Gyroscope Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Integrated Optic Chip For Gyroscope Revenue (million) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Integrated Optic Chip For Gyroscope Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Integrated Optic Chip For Gyroscope Revenue million Forecast, by Application 2020 & 2033

- Table 74: Global Integrated Optic Chip For Gyroscope Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Integrated Optic Chip For Gyroscope Revenue million Forecast, by Type 2020 & 2033

- Table 76: Global Integrated Optic Chip For Gyroscope Volume K Forecast, by Type 2020 & 2033

- Table 77: Global Integrated Optic Chip For Gyroscope Revenue million Forecast, by Country 2020 & 2033

- Table 78: Global Integrated Optic Chip For Gyroscope Volume K Forecast, by Country 2020 & 2033

- Table 79: China Integrated Optic Chip For Gyroscope Revenue (million) Forecast, by Application 2020 & 2033

- Table 80: China Integrated Optic Chip For Gyroscope Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Integrated Optic Chip For Gyroscope Revenue (million) Forecast, by Application 2020 & 2033

- Table 82: India Integrated Optic Chip For Gyroscope Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Integrated Optic Chip For Gyroscope Revenue (million) Forecast, by Application 2020 & 2033

- Table 84: Japan Integrated Optic Chip For Gyroscope Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Integrated Optic Chip For Gyroscope Revenue (million) Forecast, by Application 2020 & 2033

- Table 86: South Korea Integrated Optic Chip For Gyroscope Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Integrated Optic Chip For Gyroscope Revenue (million) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Integrated Optic Chip For Gyroscope Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Integrated Optic Chip For Gyroscope Revenue (million) Forecast, by Application 2020 & 2033

- Table 90: Oceania Integrated Optic Chip For Gyroscope Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Integrated Optic Chip For Gyroscope Revenue (million) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Integrated Optic Chip For Gyroscope Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Integrated Optic Chip For Gyroscope?

The projected CAGR is approximately XXX%.

2. Which companies are prominent players in the Integrated Optic Chip For Gyroscope?

Key companies in the market include Polaris Photonics, FOGPhotonics, EMCORE Corporation, Fiber Optical Solution, Oelabs Inc, KVH Industries, Optilab, PANWOO Equpiment Consulting, Box Optronics Technology, OELABS Inc, One Silicon Chip Photonics, HongKong Liocrebif Technology.

3. What are the main segments of the Integrated Optic Chip For Gyroscope?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Integrated Optic Chip For Gyroscope," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Integrated Optic Chip For Gyroscope report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Integrated Optic Chip For Gyroscope?

To stay informed about further developments, trends, and reports in the Integrated Optic Chip For Gyroscope, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence