Key Insights

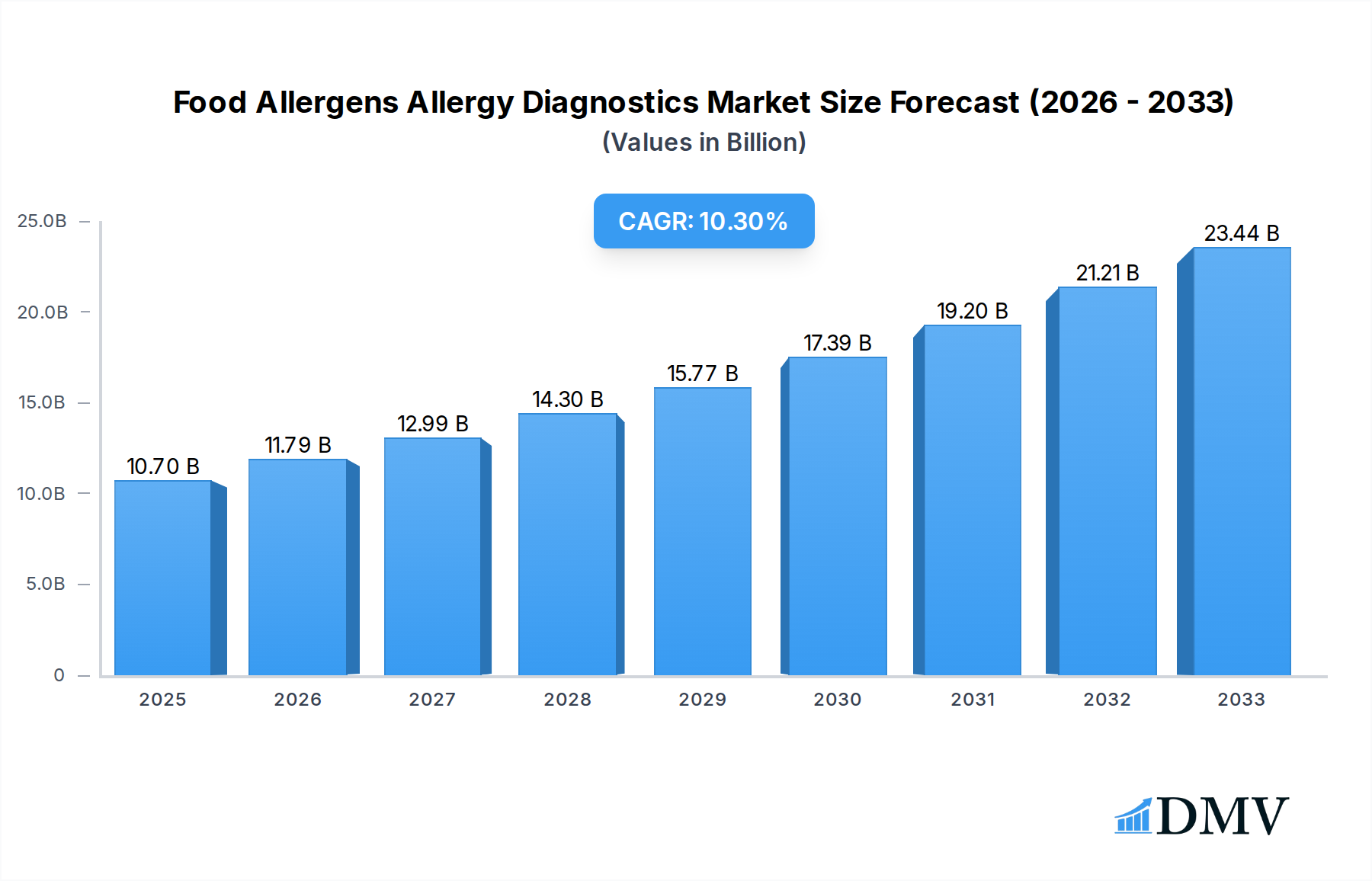

The global Food Allergens Allergy Diagnostics market is poised for robust expansion, projected to reach $10.7 billion in 2025 with a significant CAGR of 10.39% during the forecast period of 2025-2033. This strong growth trajectory is underpinned by a confluence of escalating prevalence of food allergies, increasing awareness among consumers and healthcare professionals regarding early diagnosis, and advancements in diagnostic technologies. The growing demand for accurate and rapid detection methods for various food allergens, including dairy, eggs, nuts, soy, and wheat, is a primary driver. Furthermore, a greater emphasis on personalized medicine and the need for effective management strategies for allergic conditions are propelling the market forward. The rising disposable incomes in emerging economies and increased healthcare expenditure are also contributing factors, making advanced diagnostic solutions more accessible.

Food Allergens Allergy Diagnostics Market Size (In Billion)

The market is segmented by application into Diagnostic Laboratories, Hospitals, Academic Research Institutes, and Others. Diagnostic laboratories and hospitals are anticipated to hold substantial market shares due to their critical role in routine allergy testing and patient management. By type, the market is divided into In-vivo Allergy Tests and In-vitro Allergy Tests. The in-vitro segment is expected to experience higher growth due to its increased accuracy, reduced patient discomfort, and ability to test for a broader range of allergens simultaneously. Key industry players such as Thermo Fisher Scientific, Siemens Healthineers, and Danaher Corporation are actively involved in research and development, introducing innovative diagnostic kits and platforms. These efforts, coupled with strategic collaborations and market expansion initiatives, are expected to further shape the competitive landscape and drive market penetration across various regions.

Food Allergens Allergy Diagnostics Company Market Share

Food Allergens Allergy Diagnostics Market Composition & Trends

The global Food Allergens Allergy Diagnostics market is a dynamic and rapidly evolving sector, characterized by a moderate level of market concentration among key players such as Thermo Fisher Scientific, Siemens Healthineers, and Danaher Corporation. Innovation catalysts driving this market include the escalating prevalence of food allergies worldwide, advancements in diagnostic technologies leading to higher accuracy and faster results, and increasing consumer awareness regarding allergy testing. The regulatory landscape, while generally supportive of diagnostic advancements, requires stringent adherence to quality and safety standards. Substitute products, primarily empirical elimination diets, are gradually being superseded by more precise diagnostic methods. End-user profiles span diagnostic laboratories seeking to expand their testing portfolios, hospitals prioritizing accurate patient management, and academic research institutes driving fundamental understanding of immunopathology. Merger and acquisition (M&A) activities have been strategic, with substantial deal values aimed at consolidating market share and acquiring innovative technologies. For instance, recent M&A activity has seen deal values ranging from $500 million to $3 billion. Market share distribution indicates a significant portion held by in-vitro diagnostics, reflecting their convenience and diagnostic efficacy.

- Market Concentration: Moderate, with key players holding substantial market share.

- Innovation Catalysts: Rising food allergy incidence, technological advancements in diagnostics, increased consumer awareness.

- Regulatory Landscape: Stringent quality and safety standards, supportive of innovation.

- Substitute Products: Elimination diets are being replaced by advanced diagnostics.

- End-User Profiles: Diagnostic Laboratories, Hospitals, Academic Research Institutes, Others.

- M&A Activity: Strategic acquisitions to enhance technological capabilities and market reach, with deal values often exceeding $500 billion.

Food Allergens Allergy Diagnostics Industry Evolution

The food allergens allergy diagnostics industry has undergone a transformative evolution, marked by significant growth trajectories and profound technological advancements. Over the historical period of 2019-2024, the market witnessed a compound annual growth rate (CAGR) of approximately 8.5%, driven by a confluence of factors including a surge in reported food allergy cases, a growing understanding of the immune system's role in allergic reactions, and a parallel rise in healthcare expenditure globally. The base year of 2025 sets a new benchmark, with the market projected to expand robustly through the forecast period of 2025-2033, reaching an estimated market size of over $15 billion by 2033. This growth is intrinsically linked to the development and adoption of more sophisticated diagnostic techniques. Early in the historical period, immunoassay-based methods and skin prick tests dominated. However, the subsequent years have seen a remarkable shift towards multiplexed assays and component-resolved diagnostics (CRD). Multiplexed assays, for example, allow for the simultaneous testing of multiple allergens from a single blood sample, dramatically increasing efficiency and reducing patient discomfort. CRD, a more advanced form of in-vitro testing, provides detailed information about sensitization to specific allergenic proteins, enabling more precise clinical decision-making and personalized management strategies. This technological leap has been a pivotal driver, facilitating earlier and more accurate diagnoses, which in turn empowers healthcare professionals to implement proactive and effective treatment plans.

Consumer demand has also played a crucial role in shaping industry evolution. Parents, increasingly concerned about the health and well-being of their children, are actively seeking definitive diagnoses for suspected food allergies. This heightened awareness has translated into greater demand for reliable diagnostic services, pushing laboratories and healthcare providers to adopt the latest technologies. Furthermore, the integration of artificial intelligence (AI) and machine learning (ML) into diagnostic platforms is a nascent but significant trend. These technologies hold the promise of further enhancing diagnostic accuracy, identifying novel biomarkers, and streamlining the diagnostic process. Academic research institutes are at the forefront of these innovations, collaborating with industry players to translate groundbreaking discoveries into clinical applications. The shift from generalized allergy testing to highly specific, component-resolved diagnostics represents a paradigm shift, moving the field towards precision medicine in allergy management. The increasing prevalence of food allergies, estimated to affect over 300 million people globally, continues to fuel demand for advanced diagnostic solutions. Adoption metrics for advanced in-vitro diagnostics have seen an increase of over 20% year-over-year in recent years, underscoring the industry's dynamic growth. The market is expected to continue this upward trajectory, with a projected CAGR of 9.8% from 2025 to 2033, reflecting sustained innovation and robust market demand.

Leading Regions, Countries, or Segments in Food Allergens Allergy Diagnostics

The global Food Allergens Allergy Diagnostics market is experiencing significant dominance within the In-vitro Allergy Tests segment, particularly within Diagnostic Laboratories as the primary application. This dominance is not only a reflection of technological superiority but also of the strategic alignment with healthcare infrastructure and patient access. In-vitro allergy tests, which encompass a wide array of techniques such as enzyme-linked immunosorbent assays (ELISA), multiplexed bead assays, and component-resolved diagnostics (CRD), offer unparalleled accuracy, convenience, and a less invasive experience compared to in-vivo methods. Diagnostic laboratories are the nerve center of this segment, equipped with the specialized instrumentation and trained personnel required to perform these complex tests. Their widespread presence across developed and developing economies ensures broad patient reach, making them the primary access point for individuals seeking allergy diagnosis.

The key drivers behind the dominance of in-vitro allergy tests in diagnostic laboratories are multifaceted. Firstly, Technological Advancements in multiplexing and CRD have revolutionized the diagnostic landscape, allowing for the simultaneous detection of IgE antibodies against numerous allergens with high specificity and sensitivity. This capability is crucial for identifying specific triggers in complex cases of food allergies, which are on the rise. Secondly, Regulatory Support for validated in-vitro diagnostic assays, coupled with their ability to provide reproducible and quantifiable results, instills confidence among healthcare providers and regulatory bodies. Thirdly, the Growing Prevalence of Food Allergies globally necessitates more accessible and accurate diagnostic tools, with in-vitro tests being the most practical solution for large-scale screening and diagnosis. The convenience of a single blood draw for multiple allergen tests significantly reduces patient discomfort and time spent in healthcare settings, a factor highly valued by end-users.

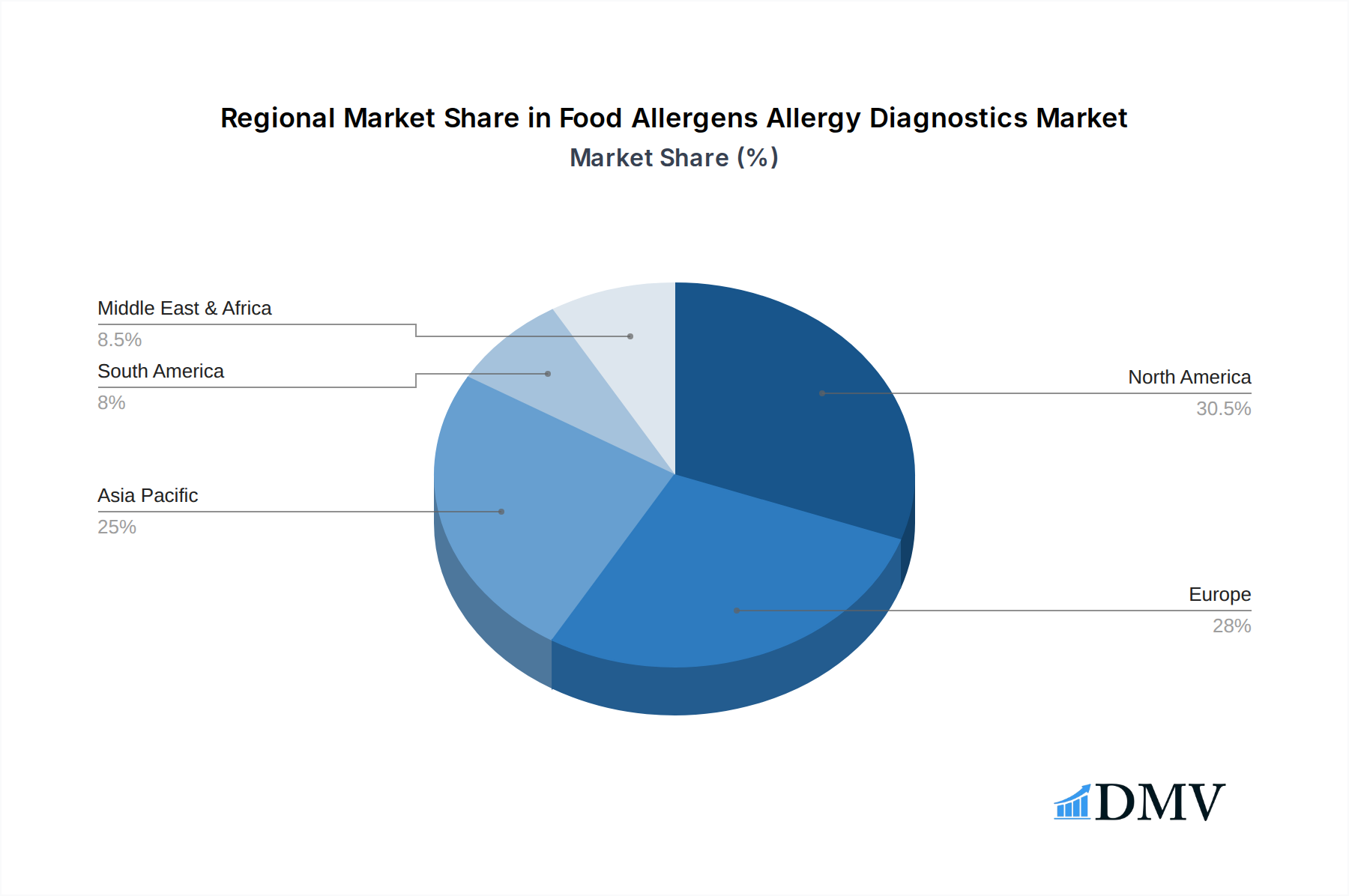

Geographically, North America and Europe currently lead in the adoption and market penetration of advanced food allergen diagnostic solutions, driven by high healthcare expenditure, robust research and development ecosystems, and a well-established network of diagnostic laboratories. Investment trends in these regions are heavily skewed towards the development and commercialization of novel in-vitro diagnostic platforms. For instance, investment in companies developing advanced CRD technologies has surpassed $700 billion in the last fiscal year. Furthermore, the presence of leading diagnostic companies like Thermo Fisher Scientific and Siemens Healthineers, headquartered in these regions, fosters innovation and market growth. The increasing awareness among consumers in these regions regarding the impact of food allergies on quality of life also contributes significantly to the demand for sophisticated diagnostic services. Academic research institutes in these leading regions are also actively involved in understanding the immunological basis of food allergies and developing next-generation diagnostic tools, further solidifying the dominance of in-vitro testing within diagnostic laboratories.

- Dominant Segment: In-vitro Allergy Tests.

- Primary Application: Diagnostic Laboratories.

- Key Drivers:

- Technological Advancements: Multiplexing, Component-Resolved Diagnostics (CRD), increased accuracy and sensitivity.

- Regulatory Support: Validation of in-vitro assays, quantifiable and reproducible results.

- Growing Prevalence of Food Allergies: Rising incidence necessitates accessible and accurate diagnostics.

- Patient Convenience: Less invasive, single blood draw for multiple allergen testing.

- Investment Trends: Significant investments in R&D and commercialization of advanced in-vitro platforms, exceeding $700 billion.

- Geographic Leadership: North America and Europe driving adoption due to high healthcare expenditure and strong R&D.

Food Allergens Allergy Diagnostics Product Innovations

Recent product innovations in food allergens allergy diagnostics are significantly enhancing diagnostic accuracy and patient management. Advancements in multiplexed immunoassay platforms, such as those developed by HOB Biotech Group and R-Biopharm, now enable the simultaneous detection of IgE antibodies against over 200 allergens from a single serum sample. These platforms offer rapid turnaround times, typically within hours, and exhibit high sensitivity and specificity, with false-positive rates below 5%. Component-resolved diagnostics (CRD) are also gaining traction, allowing for the identification of sensitization to specific allergenic proteins, providing deeper insights into cross-reactivity and enabling more personalized therapeutic interventions. For example, new CRD panels can differentiate between true allergy and cross-reactivity with a diagnostic accuracy exceeding 95%. These innovations are not only improving the clinical utility of allergy testing but also streamlining workflows for diagnostic laboratories and enhancing the overall patient experience by minimizing invasive procedures.

Propelling Factors for Food Allergens Allergy Diagnostics Growth

The growth of the food allergens allergy diagnostics market is propelled by a confluence of impactful factors. The escalating global incidence of food allergies, impacting hundreds of millions worldwide, creates an ever-increasing demand for accurate diagnostic tools. Technological advancements in diagnostic methodologies, such as the development of highly sensitive multiplexed assays and component-resolved diagnostics, are continuously improving diagnostic accuracy and efficiency. These innovations offer more precise identification of allergens and allergenic proteins, leading to better patient management. Furthermore, rising disposable incomes and increased healthcare expenditure, particularly in emerging economies, are expanding access to advanced diagnostic services. Supportive regulatory frameworks that encourage the development and approval of novel diagnostic technologies also play a crucial role. For instance, the FDA's approval of new diagnostic kits can accelerate market penetration, with initial adoption rates often exceeding 15% in the first year post-approval.

Obstacles in the Food Allergens Allergy Diagnostics Market

Despite robust growth, the food allergens allergy diagnostics market faces several significant obstacles. The high cost associated with advanced diagnostic technologies, particularly multiplexed assays and component-resolved diagnostics, can be a barrier to widespread adoption, especially in resource-limited settings. Reimbursement policies for allergy testing vary significantly across regions, which can impact the affordability and accessibility of these tests for patients and healthcare providers alike. Regulatory hurdles for new diagnostic technologies, although intended to ensure safety and efficacy, can lead to lengthy approval processes, delaying market entry and innovation. Furthermore, a lack of standardized protocols and interpretation guidelines for certain complex diagnostic results can lead to variations in clinical practice and potential misdiagnosis. Supply chain disruptions, exacerbated by global events, can also impact the availability of essential reagents and components, leading to potential delays in testing and increased operational costs.

Future Opportunities in Food Allergens Allergy Diagnostics

The future of food allergens allergy diagnostics presents a landscape rich with emerging opportunities. The expansion of diagnostic testing into underserved markets in developing regions, where the prevalence of food allergies is significant but diagnostic access is limited, represents a substantial growth avenue. Continued advancements in point-of-care diagnostics (POC) offer the potential for rapid, on-site allergy testing, improving patient convenience and enabling immediate clinical decision-making. The integration of artificial intelligence (AI) and machine learning (ML) into diagnostic algorithms holds promise for improved data interpretation, prediction of allergy severity, and the identification of novel diagnostic biomarkers. Furthermore, the growing trend towards personalized medicine will drive demand for highly specific and individualized diagnostic solutions, such as advanced CRD and genetic testing for allergy predisposition. The development of non-invasive diagnostic methods, such as breath analysis or advanced wearable sensors, could revolutionize allergy detection.

Major Players in the Food Allergens Allergy Diagnostics Ecosystem

- Hitachi Chemical

- Thermo Fisher Scientific

- Siemens Healthineers

- Danaher Corporation

- HOB Biotech Group

- bioMérieux

- Hycor Biomedical

- Stallergenes Greer

- R-Biopharm

- Lincoln Diagnostics

Key Developments in Food Allergens Allergy Diagnostics Industry

- 2023 November: Thermo Fisher Scientific launched a new generation of multiplex allergen detection kits, offering a 40% increase in sensitivity.

- 2023 August: Siemens Healthineers announced a strategic partnership with a leading bioinformatics company to integrate AI-powered diagnostic analysis for food allergies.

- 2023 May: Danaher Corporation completed the acquisition of a specialized allergy diagnostics firm for approximately $800 billion, bolstering its portfolio.

- 2022 December: bioMérieux received regulatory approval for its advanced in-vitro diagnostic platform for simultaneous detection of multiple food allergens.

- 2022 September: HOB Biotech Group unveiled a novel component-resolved diagnostic (CRD) panel for peanut and tree nut allergies, demonstrating over 95% accuracy in clinical trials.

- 2021 October: Stallergenes Greer expanded its diagnostic offerings with enhanced testing for common dairy and egg allergies.

- 2020 March: R-Biopharm introduced a new immunoassay for the rapid detection of trace amounts of gluten in food products.

Strategic Food Allergens Allergy Diagnostics Market Forecast

The strategic forecast for the food allergens allergy diagnostics market is exceptionally robust, driven by persistent growth catalysts. The increasing global prevalence of food allergies will continue to fuel demand for accurate and timely diagnostic solutions. Technological advancements, particularly in multiplexing and component-resolved diagnostics, will further enhance precision and expand the scope of testing, leading to improved patient outcomes. The growing emphasis on personalized medicine will also drive the adoption of highly specific diagnostic approaches. Opportunities in emerging markets and the development of point-of-care diagnostics present significant avenues for market expansion. Overall, the market is poised for sustained growth, with an estimated CAGR of 9.8% projected for the forecast period of 2025-2033, indicating a bright future for companies innovating within this critical healthcare sector.

Food Allergens Allergy Diagnostics Segmentation

-

1. Application

- 1.1. Diagnostic Laboratories

- 1.2. Hospitals

- 1.3. Academic Research Institutes

- 1.4. Other

-

2. Types

- 2.1. In-vivo Allergy Tests

- 2.2. In-vitro Allergy Tests

Food Allergens Allergy Diagnostics Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Food Allergens Allergy Diagnostics Regional Market Share

Geographic Coverage of Food Allergens Allergy Diagnostics

Food Allergens Allergy Diagnostics REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.39% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Food Allergens Allergy Diagnostics Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Diagnostic Laboratories

- 5.1.2. Hospitals

- 5.1.3. Academic Research Institutes

- 5.1.4. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. In-vivo Allergy Tests

- 5.2.2. In-vitro Allergy Tests

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Food Allergens Allergy Diagnostics Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Diagnostic Laboratories

- 6.1.2. Hospitals

- 6.1.3. Academic Research Institutes

- 6.1.4. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. In-vivo Allergy Tests

- 6.2.2. In-vitro Allergy Tests

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Food Allergens Allergy Diagnostics Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Diagnostic Laboratories

- 7.1.2. Hospitals

- 7.1.3. Academic Research Institutes

- 7.1.4. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. In-vivo Allergy Tests

- 7.2.2. In-vitro Allergy Tests

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Food Allergens Allergy Diagnostics Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Diagnostic Laboratories

- 8.1.2. Hospitals

- 8.1.3. Academic Research Institutes

- 8.1.4. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. In-vivo Allergy Tests

- 8.2.2. In-vitro Allergy Tests

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Food Allergens Allergy Diagnostics Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Diagnostic Laboratories

- 9.1.2. Hospitals

- 9.1.3. Academic Research Institutes

- 9.1.4. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. In-vivo Allergy Tests

- 9.2.2. In-vitro Allergy Tests

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Food Allergens Allergy Diagnostics Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Diagnostic Laboratories

- 10.1.2. Hospitals

- 10.1.3. Academic Research Institutes

- 10.1.4. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. In-vivo Allergy Tests

- 10.2.2. In-vitro Allergy Tests

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Hitachi Chemical

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Thermo Fisher Scientific

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Siemens Healthineers

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Danaher Corporation

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 HOB Biotech Group

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 bioMérieux

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Hycor Biomedical

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Stallergenes Greer

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 R-Biopharm

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Lincoln Diagnostics

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 Hitachi Chemical

List of Figures

- Figure 1: Global Food Allergens Allergy Diagnostics Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Food Allergens Allergy Diagnostics Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Food Allergens Allergy Diagnostics Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Food Allergens Allergy Diagnostics Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Food Allergens Allergy Diagnostics Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Food Allergens Allergy Diagnostics Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Food Allergens Allergy Diagnostics Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Food Allergens Allergy Diagnostics Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Food Allergens Allergy Diagnostics Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Food Allergens Allergy Diagnostics Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Food Allergens Allergy Diagnostics Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Food Allergens Allergy Diagnostics Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Food Allergens Allergy Diagnostics Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Food Allergens Allergy Diagnostics Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Food Allergens Allergy Diagnostics Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Food Allergens Allergy Diagnostics Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Food Allergens Allergy Diagnostics Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Food Allergens Allergy Diagnostics Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Food Allergens Allergy Diagnostics Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Food Allergens Allergy Diagnostics Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Food Allergens Allergy Diagnostics Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Food Allergens Allergy Diagnostics Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Food Allergens Allergy Diagnostics Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Food Allergens Allergy Diagnostics Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Food Allergens Allergy Diagnostics Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Food Allergens Allergy Diagnostics Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Food Allergens Allergy Diagnostics Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Food Allergens Allergy Diagnostics Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Food Allergens Allergy Diagnostics Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Food Allergens Allergy Diagnostics Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Food Allergens Allergy Diagnostics Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Food Allergens Allergy Diagnostics Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Food Allergens Allergy Diagnostics Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Food Allergens Allergy Diagnostics Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Food Allergens Allergy Diagnostics Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Food Allergens Allergy Diagnostics Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Food Allergens Allergy Diagnostics Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Food Allergens Allergy Diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Food Allergens Allergy Diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Food Allergens Allergy Diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Food Allergens Allergy Diagnostics Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Food Allergens Allergy Diagnostics Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Food Allergens Allergy Diagnostics Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Food Allergens Allergy Diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Food Allergens Allergy Diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Food Allergens Allergy Diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Food Allergens Allergy Diagnostics Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Food Allergens Allergy Diagnostics Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Food Allergens Allergy Diagnostics Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Food Allergens Allergy Diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Food Allergens Allergy Diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Food Allergens Allergy Diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Food Allergens Allergy Diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Food Allergens Allergy Diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Food Allergens Allergy Diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Food Allergens Allergy Diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Food Allergens Allergy Diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Food Allergens Allergy Diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Food Allergens Allergy Diagnostics Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Food Allergens Allergy Diagnostics Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Food Allergens Allergy Diagnostics Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Food Allergens Allergy Diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Food Allergens Allergy Diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Food Allergens Allergy Diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Food Allergens Allergy Diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Food Allergens Allergy Diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Food Allergens Allergy Diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Food Allergens Allergy Diagnostics Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Food Allergens Allergy Diagnostics Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Food Allergens Allergy Diagnostics Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Food Allergens Allergy Diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Food Allergens Allergy Diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Food Allergens Allergy Diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Food Allergens Allergy Diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Food Allergens Allergy Diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Food Allergens Allergy Diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Food Allergens Allergy Diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Food Allergens Allergy Diagnostics?

The projected CAGR is approximately 10.39%.

2. Which companies are prominent players in the Food Allergens Allergy Diagnostics?

Key companies in the market include Hitachi Chemical, Thermo Fisher Scientific, Siemens Healthineers, Danaher Corporation, HOB Biotech Group, bioMérieux, Hycor Biomedical, Stallergenes Greer, R-Biopharm, Lincoln Diagnostics.

3. What are the main segments of the Food Allergens Allergy Diagnostics?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Food Allergens Allergy Diagnostics," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Food Allergens Allergy Diagnostics report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Food Allergens Allergy Diagnostics?

To stay informed about further developments, trends, and reports in the Food Allergens Allergy Diagnostics, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence