Key Insights

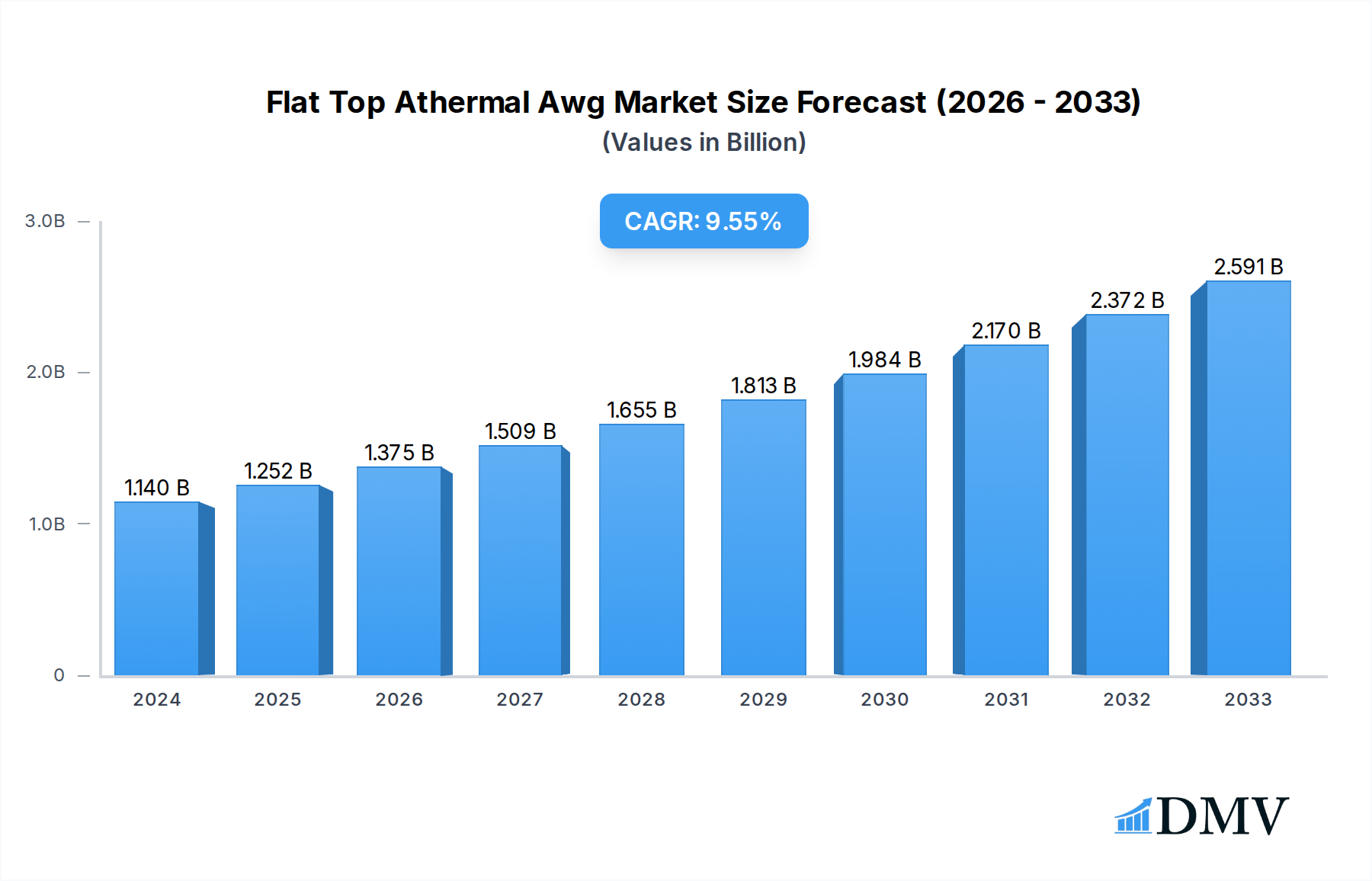

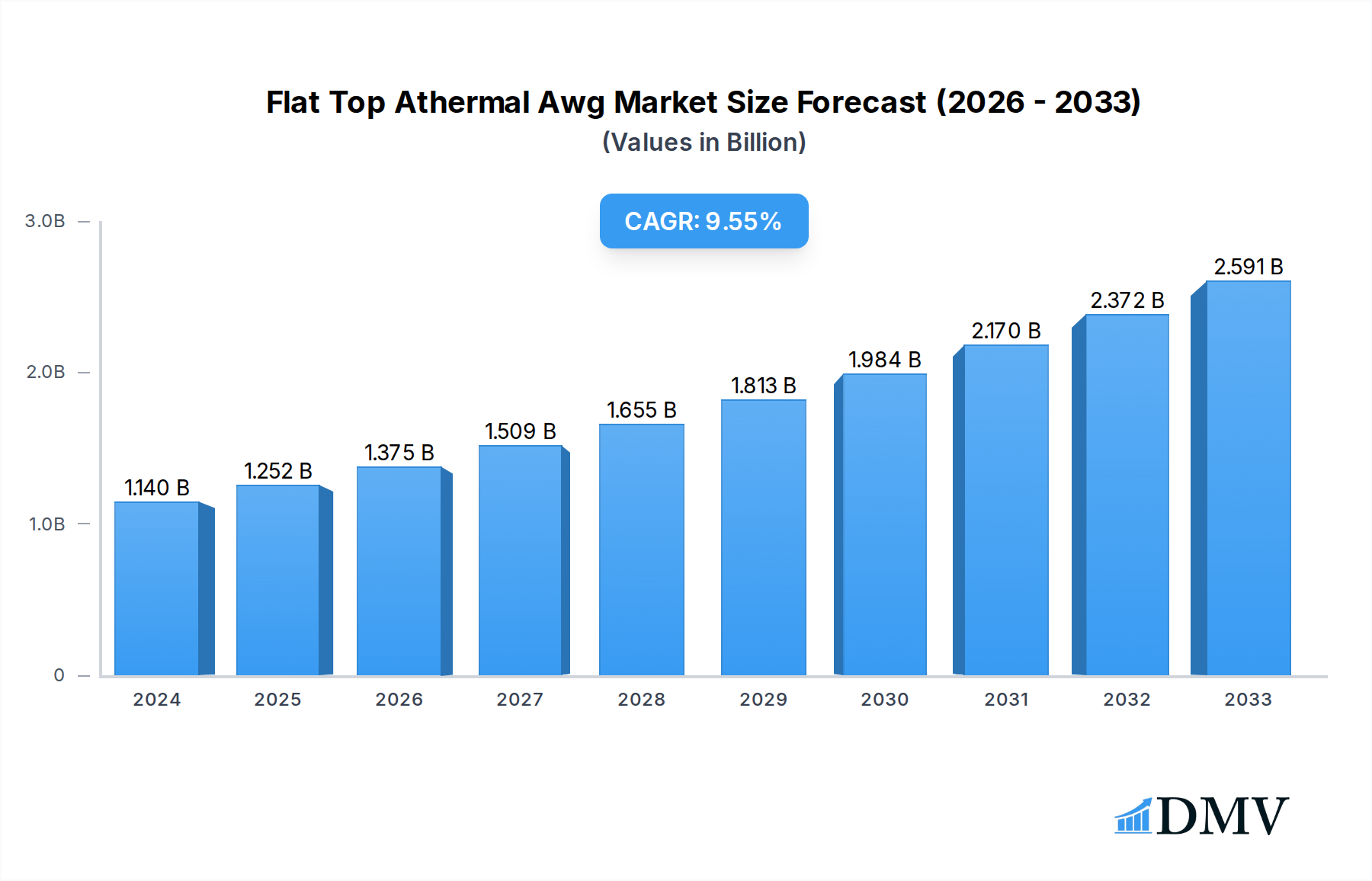

The Flat Top Athermal AWG market is experiencing robust growth, projected to reach an estimated $1.14 billion in 2024. This expansion is driven by an impressive Compound Annual Growth Rate (CAGR) of 9.8% over the forecast period. The increasing demand for higher bandwidth and more efficient optical network infrastructure is a primary catalyst. Key applications like DWDM Transmission, Wavelength Routing, and Optical Add/Drop are witnessing significant adoption of Athermal AWGs, fueling market expansion. Advancements in fiber optic technology, coupled with the growing need for flexible and scalable optical networks in telecommunications, data centers, and enterprise networks, are presenting substantial opportunities. The shift towards higher frequency types, such as 100 GHz and 150 GHz, indicates a move towards more sophisticated and capacity-intensive network solutions.

Flat Top Athermal Awg Market Size (In Billion)

While the market is poised for strong growth, certain factors may present challenges. High initial investment costs for advanced manufacturing processes and the need for specialized technical expertise could act as restraints. Furthermore, the rapid pace of technological evolution necessitates continuous innovation and adaptation to maintain a competitive edge. However, the overarching trend towards increased data consumption, the proliferation of 5G networks, and the expanding cloud computing landscape are expected to outweigh these restraints. Major players like NTT Electronics Corporation, Enablence, and Accelink Technologies are actively investing in research and development to meet these evolving demands, suggesting a dynamic and competitive market landscape with a bright future.

Flat Top Athermal Awg Company Market Share

Flat Top Athermal Awg Market Composition & Trends

The global Flat Top Athermal AWG market is characterized by a dynamic landscape, exhibiting moderate to high concentration with key players actively shaping its trajectory. Innovation remains a significant catalyst, driven by the relentless pursuit of higher channel counts, reduced insertion loss, and enhanced thermal stability for advanced DWDM transmission and wavelength routing applications. Regulatory landscapes, while generally supportive of telecommunications infrastructure development, can influence market entry and product certifications. Substitute products, such as other types of multiplexers and demultiplexers, exist but often lack the precise wavelength selectivity and athermal stability offered by advanced AWG solutions. End-user profiles span telecommunication operators, data centers, research institutions, and enterprise networks, all seeking robust and scalable optical networking solutions. Mergers and acquisitions (M&A) activities are a strategic imperative for consolidation and technology acquisition, with recent deal values in the billion range, indicating significant investment in this sector. For instance, strategic acquisitions aimed at integrating advanced fabrication technologies for higher density AWGs are becoming prevalent.

- Market Share Distribution: Leading entities in the flat top athermal AWG market are estimated to hold significant market shares, with the top 3-5 players potentially accounting for over billion in revenue.

- M&A Deal Values: Recent M&A activities within the optical components industry, including those relevant to AWG technology, have seen valuations exceeding billion, reflecting strategic consolidation.

Flat Top Athermal Awg Industry Evolution

The Flat Top Athermal AWG industry has undergone a remarkable evolution, driven by the exponential growth in data traffic and the increasing demand for high-capacity optical networks. From its inception, the market has witnessed a consistent upward trajectory in growth rates, fueled by the indispensable role of AWGs in modern telecommunications. The study period from 2019 to 2033, with a base year of 2025, encapsulates a significant era of technological maturation and market expansion. The historical period (2019-2024) saw foundational advancements in athermalization techniques and waveguide fabrication, paving the way for denser channel counts and improved performance. As we approach and move through the estimated year of 2025, the market is poised for continued robust growth, projected to be in the high single digits to low double digits annually during the forecast period (2025-2033). This growth is intrinsically linked to the expanding deployment of DWDM systems for long-haul and metro networks, essential for supporting services like 5G, cloud computing, and the Internet of Things (IoT).

Technological advancements have been the cornerstone of this evolution. Early athermal AWGs relied on bulk optics and temperature control mechanisms, which were cumbersome and energy-intensive. The advent of planar lightwave circuit (PLC) technology and advanced silica-on-silicon fabrication processes enabled the development of compact, passively athermal devices. This shift dramatically reduced insertion loss, improved channel isolation, and significantly enhanced thermal stability, making them ideal for deployment in a wider range of environmental conditions without active cooling. The demand for higher channel counts, moving from tens to hundreds of channels within a single AWG device, has been a persistent trend, directly responding to the escalating bandwidth requirements. Furthermore, the development of flat-top spectral shapes has become critical, minimizing adjacent channel crosstalk and ensuring superior signal integrity, a crucial factor for advanced modulation formats used in 100G, 400G, and beyond transmission systems. Consumer demand, primarily from network operators and service providers, has consistently pushed for higher performance metrics: lower insertion loss (often below billion dB), wider passbands, tighter channel spacing (e.g., 50 GHz, 75 GHz, 100 GHz, 150 GHz), and greater reliability. The ability to integrate more functionality into smaller footprints, such as multiplexing and demultiplexing capabilities within a single component, has also driven adoption. The market's evolution is a testament to the continuous innovation in material science, optical design, and manufacturing processes, all working in concert to meet the ever-growing demands of the global digital economy.

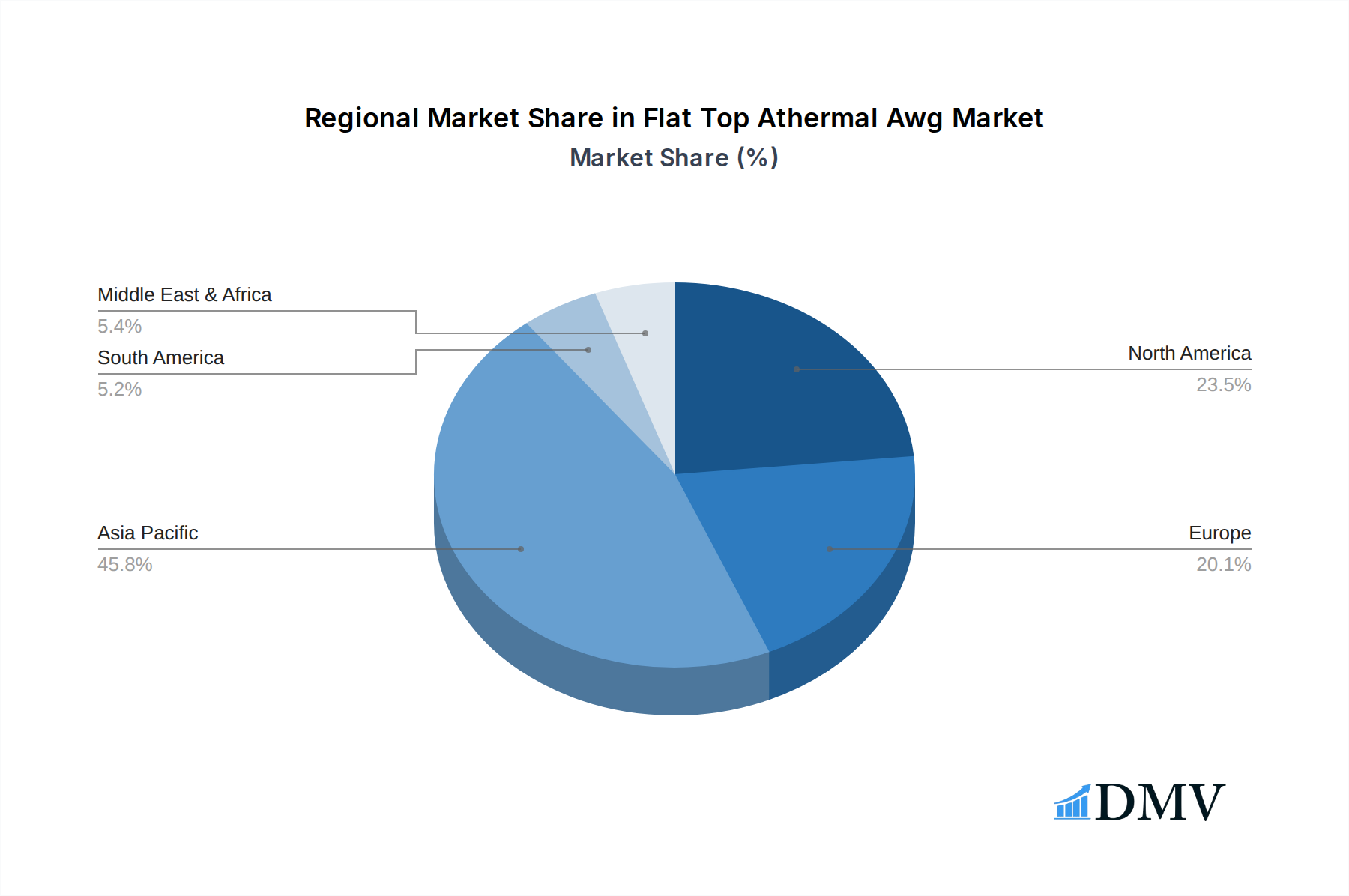

Leading Regions, Countries, or Segments in Flat Top Athermal Awg

The global Flat Top Athermal AWG market is significantly influenced by regional investments in telecommunications infrastructure and the adoption of advanced optical networking technologies. Asia-Pacific, particularly China, stands out as a dominant region, propelled by extensive government initiatives supporting the build-out of 5G networks, fiber-to-the-home (FTTH) deployments, and the rapid expansion of data center capacity. These factors translate into substantial demand for DWDM transmission solutions, where Flat Top Athermal AWGs play a pivotal role. North America and Europe also represent mature and significant markets, characterized by ongoing upgrades to existing networks, the deployment of higher-speed services, and a strong focus on research and development.

Within the Application segment, DWDM Transmission is the undisputed leader, accounting for the largest market share. The increasing need for high-capacity long-haul and metro optical networks to carry ever-growing data traffic directly fuels the demand for AWGs in DWDM systems.

- DWDM Transmission: This segment benefits from massive investments in global and regional backbone networks, facilitating higher data rates and increased spectral efficiency.

- Wavelength Routing: As networks become more complex, the ability of AWGs to precisely route specific wavelengths becomes critical for efficient network management and flexibility.

- Optical Add/Drop: This application is gaining traction as networks evolve towards more flexible architectures, allowing for the selective insertion and removal of channels without disrupting others.

In terms of Type, the market is witnessing a significant shift towards denser channel spacing, driven by the need to maximize fiber capacity.

- 100G Hz: This is a widely adopted channel spacing, offering a good balance between capacity and cost for many DWDM applications.

- 50G Hz: Driven by the push for even higher spectral efficiency, especially in metro and regional networks, 50 GHz AWGs are gaining considerable traction.

- 75G Hz: This spacing offers an intermediate solution, often adopted in specific scenarios where 50 GHz might be overly dense or 100 GHz insufficient.

Key drivers for regional dominance include:

- Government Investment Trends: Significant government funding for telecommunications infrastructure upgrades, particularly in emerging economies, directly stimulates demand for AWG components.

- Regulatory Support: Favorable regulations encouraging broadband deployment and network modernization accelerate market growth.

- Technological Adoption Rates: Regions with a higher propensity to adopt cutting-edge optical technologies, such as advanced modulation formats and higher channel count systems, naturally lead in AWG consumption.

- Presence of Key Manufacturers: The concentration of leading AWG manufacturers in certain regions fosters local ecosystem development and innovation, further solidifying their market position. For example, China's strong domestic manufacturing base, encompassing companies like Accelink Technologies, Broadex Technologies, and HYC, contributes significantly to its leadership in both production and consumption.

Flat Top Athermal Awg Product Innovations

Product innovations in the Flat Top Athermal AWG market are primarily focused on enhancing performance metrics and expanding integration capabilities. Manufacturers are pushing the boundaries of channel density, aiming for ultra-high channel counts exceeding billion channels per device. Innovations in fabrication processes, particularly advancements in silica-on-silicon and silicon photonics, are enabling lower insertion losses, tighter channel spacing (e.g., 50 GHz and 75 GHz), and superior thermal stability across a wider operating temperature range. The development of flat-top spectral shapes with sharper cutoffs is a key differentiator, crucial for minimizing adjacent channel crosstalk in high-speed DWDM systems. Furthermore, integration of advanced features such as integrated optical switches or monitoring ports within a single AWG package represents a significant leap towards more compact and efficient optical networking modules.

Propelling Factors for Flat Top Athermal Awg Growth

The growth of the Flat Top Athermal AWG market is propelled by several key factors. The insatiable demand for bandwidth driven by 5G deployment, cloud computing, AI, and IoT applications necessitates more efficient optical networks. Advances in DWDM technology, enabling higher data rates (e.g., 100GbE, 400GbE, 800GbE), directly translate to increased demand for AWGs. Government initiatives and investments in broadband infrastructure globally, particularly in emerging economies, are creating substantial opportunities. Furthermore, the need for cost-effective and energy-efficient optical solutions favors passively athermal AWGs over traditional active temperature-controlled devices. The continuous push for miniaturization and higher integration within optical transceivers and modules also drives the adoption of compact AWG solutions.

Obstacles in the Flat Top Athermal Awg Market

Despite robust growth, the Flat Top Athermal AWG market faces several obstacles. Intense price competition among manufacturers, particularly in high-volume segments, can lead to shrinking profit margins. Supply chain disruptions, exacerbated by geopolitical factors and raw material availability, can impact production timelines and costs. The rapid pace of technological evolution also presents a challenge, as manufacturers must continually invest in R&D to stay ahead of innovation curves and meet evolving market demands for higher performance. The development of alternative multiplexing technologies, though currently niche, could pose a future threat. Furthermore, the high capital expenditure required for advanced fabrication facilities can act as a barrier to entry for new players.

Future Opportunities in Flat Top Athermal Awg

Emerging opportunities for Flat Top Athermal AWGs are abundant. The expansion of metro and edge data centers, driven by the proliferation of cloud services and the need for lower latency, presents a significant growth avenue. The increasing adoption of coherent optics and advanced modulation formats in a wider range of network segments will further boost demand for high-performance AWGs. The growth of satellite internet constellations and their ground station infrastructure also offers new market potential. Furthermore, the development of novel applications beyond traditional telecommunications, such as in sensing and scientific instrumentation, could open up new revenue streams. The ongoing trend towards silicon photonics integration also presents an opportunity for AWG manufacturers to collaborate and develop next-generation, highly integrated optical engines.

Major Players in the Flat Top Athermal Awg Ecosystem

- NTT Electronics Corporation

- Enablence

- POINTek

- Accelink Technologies

- Broadex Technologies

- Henan Shijia Photons Tech

- Guangzhou Sintai Communication

- HYC

- Shenzhen Gigalight Technology

- DK Photonics

- GEZHI Photonics

- Shenzhen Seacent Photonics

- Wuhan Yilut Technology

- Shenzhen Hilink Technology

- Teosco Technologies

- Shenzhen Optico Communication

- Shenzhen Unifiber Technology

Key Developments in Flat Top Athermal Awg Industry

- 2019: NTT Electronics Corporation announces advancements in planar lightwave circuit (PLC) technology, enabling higher channel count AWGs with improved insertion loss.

- 2020: Accelink Technologies launches a new series of 50 GHz Flat Top Athermal AWGs, targeting high-density DWDM applications.

- 2021: Broadex Technologies expands its manufacturing capacity for athermal AWGs, anticipating increased demand from the 5G rollout.

- 2022: Enablence showcases integration of athermal AWGs with other photonic components for compact transponder modules.

- 2023: POINTek reports a significant increase in orders for its high-performance athermal AWGs from major telecommunication service providers.

- 2023 (Late): HYC develops ultra-low loss AWG modules for advanced coherent transmission systems.

- 2024 (Early): Shenzhen Gigalight Technology introduces a new generation of athermal AWGs with enhanced thermal stability for harsh environments.

- 2024 (Mid): DK Photonics focuses on developing athermal AWGs for data center interconnects (DCI).

- 2024 (Late): GEZHI Photonics announces strategic partnerships to accelerate R&D in next-generation athermal AWG technologies.

Strategic Flat Top Athermal Awg Market Forecast

The Flat Top Athermal AWG market is poised for sustained and robust growth, driven by the unceasing demand for bandwidth in a hyper-connected world. The ongoing 5G rollout, expansion of cloud infrastructure, and the burgeoning IoT ecosystem will continue to fuel the need for high-capacity DWDM transmission, making athermal AWGs indispensable. The shift towards higher channel densities and improved spectral efficiency, such as the increasing adoption of 50 GHz and 75 GHz spacing, represents a significant market opportunity. Investments in optical networking infrastructure, both from governments and private enterprises, will act as a primary growth catalyst. As technology advances, expect continued innovation in miniaturization, integration, and performance enhancements, further solidifying the market's strategic importance in the telecommunications landscape.

Flat Top Athermal Awg Segmentation

-

1. Application

- 1.1. DWDM Transmission

- 1.2. Wavelength Routing

- 1.3. Optical Add/Drop

- 1.4. Others

-

2. Type

- 2.1. 50G Hz

- 2.2. 75G Hz

- 2.3. 100G Hz

- 2.4. 150G Hz

- 2.5. Others

Flat Top Athermal Awg Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Flat Top Athermal Awg Regional Market Share

Geographic Coverage of Flat Top Athermal Awg

Flat Top Athermal Awg REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Flat Top Athermal Awg Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. DWDM Transmission

- 5.1.2. Wavelength Routing

- 5.1.3. Optical Add/Drop

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. 50G Hz

- 5.2.2. 75G Hz

- 5.2.3. 100G Hz

- 5.2.4. 150G Hz

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Flat Top Athermal Awg Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. DWDM Transmission

- 6.1.2. Wavelength Routing

- 6.1.3. Optical Add/Drop

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. 50G Hz

- 6.2.2. 75G Hz

- 6.2.3. 100G Hz

- 6.2.4. 150G Hz

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Flat Top Athermal Awg Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. DWDM Transmission

- 7.1.2. Wavelength Routing

- 7.1.3. Optical Add/Drop

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. 50G Hz

- 7.2.2. 75G Hz

- 7.2.3. 100G Hz

- 7.2.4. 150G Hz

- 7.2.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Flat Top Athermal Awg Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. DWDM Transmission

- 8.1.2. Wavelength Routing

- 8.1.3. Optical Add/Drop

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. 50G Hz

- 8.2.2. 75G Hz

- 8.2.3. 100G Hz

- 8.2.4. 150G Hz

- 8.2.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Flat Top Athermal Awg Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. DWDM Transmission

- 9.1.2. Wavelength Routing

- 9.1.3. Optical Add/Drop

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. 50G Hz

- 9.2.2. 75G Hz

- 9.2.3. 100G Hz

- 9.2.4. 150G Hz

- 9.2.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Flat Top Athermal Awg Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. DWDM Transmission

- 10.1.2. Wavelength Routing

- 10.1.3. Optical Add/Drop

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. 50G Hz

- 10.2.2. 75G Hz

- 10.2.3. 100G Hz

- 10.2.4. 150G Hz

- 10.2.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 NTT Electronics Corporation

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Enablence

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 POINTek

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Accelink Technologies

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Broadex Technologies

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Henan Shijia Photons Tech

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Guangzhou Sintai Communication

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 HYC

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Shenzhen Gigalight Technology

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 DK Photonics

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 GEZHI Photonics

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Shenzhen Seacent Photonics

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Wuhan Yilut Technology

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Shenzhen Hilink Technology

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Teosco Technologies

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Shenzhen Optico Communication

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Shenzhen Unifiber Technology

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.1 NTT Electronics Corporation

List of Figures

- Figure 1: Global Flat Top Athermal Awg Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Flat Top Athermal Awg Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Flat Top Athermal Awg Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Flat Top Athermal Awg Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Flat Top Athermal Awg Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Flat Top Athermal Awg Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Flat Top Athermal Awg Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Flat Top Athermal Awg Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Flat Top Athermal Awg Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Flat Top Athermal Awg Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Flat Top Athermal Awg Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Flat Top Athermal Awg Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Flat Top Athermal Awg Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Flat Top Athermal Awg Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Flat Top Athermal Awg Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Flat Top Athermal Awg Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Flat Top Athermal Awg Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Flat Top Athermal Awg Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Flat Top Athermal Awg Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Flat Top Athermal Awg Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Flat Top Athermal Awg Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Flat Top Athermal Awg Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Flat Top Athermal Awg Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Flat Top Athermal Awg Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Flat Top Athermal Awg Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Flat Top Athermal Awg Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Flat Top Athermal Awg Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Flat Top Athermal Awg Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Flat Top Athermal Awg Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Flat Top Athermal Awg Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Flat Top Athermal Awg Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Flat Top Athermal Awg Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Flat Top Athermal Awg Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Flat Top Athermal Awg Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Flat Top Athermal Awg Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Flat Top Athermal Awg Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Flat Top Athermal Awg Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Flat Top Athermal Awg Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Flat Top Athermal Awg Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Flat Top Athermal Awg Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Flat Top Athermal Awg Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Flat Top Athermal Awg Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Flat Top Athermal Awg Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Flat Top Athermal Awg Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Flat Top Athermal Awg Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Flat Top Athermal Awg Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Flat Top Athermal Awg Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Flat Top Athermal Awg Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Flat Top Athermal Awg Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Flat Top Athermal Awg Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Flat Top Athermal Awg Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Flat Top Athermal Awg Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Flat Top Athermal Awg Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Flat Top Athermal Awg Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Flat Top Athermal Awg Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Flat Top Athermal Awg Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Flat Top Athermal Awg Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Flat Top Athermal Awg Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Flat Top Athermal Awg Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Flat Top Athermal Awg Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Flat Top Athermal Awg Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Flat Top Athermal Awg Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Flat Top Athermal Awg Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Flat Top Athermal Awg Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Flat Top Athermal Awg Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Flat Top Athermal Awg Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Flat Top Athermal Awg Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Flat Top Athermal Awg Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Flat Top Athermal Awg Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Flat Top Athermal Awg Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Flat Top Athermal Awg Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Flat Top Athermal Awg Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Flat Top Athermal Awg Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Flat Top Athermal Awg Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Flat Top Athermal Awg Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Flat Top Athermal Awg Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Flat Top Athermal Awg Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Flat Top Athermal Awg?

The projected CAGR is approximately 9.8%.

2. Which companies are prominent players in the Flat Top Athermal Awg?

Key companies in the market include NTT Electronics Corporation, Enablence, POINTek, Accelink Technologies, Broadex Technologies, Henan Shijia Photons Tech, Guangzhou Sintai Communication, HYC, Shenzhen Gigalight Technology, DK Photonics, GEZHI Photonics, Shenzhen Seacent Photonics, Wuhan Yilut Technology, Shenzhen Hilink Technology, Teosco Technologies, Shenzhen Optico Communication, Shenzhen Unifiber Technology.

3. What are the main segments of the Flat Top Athermal Awg?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Flat Top Athermal Awg," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Flat Top Athermal Awg report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Flat Top Athermal Awg?

To stay informed about further developments, trends, and reports in the Flat Top Athermal Awg, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence