Key Insights

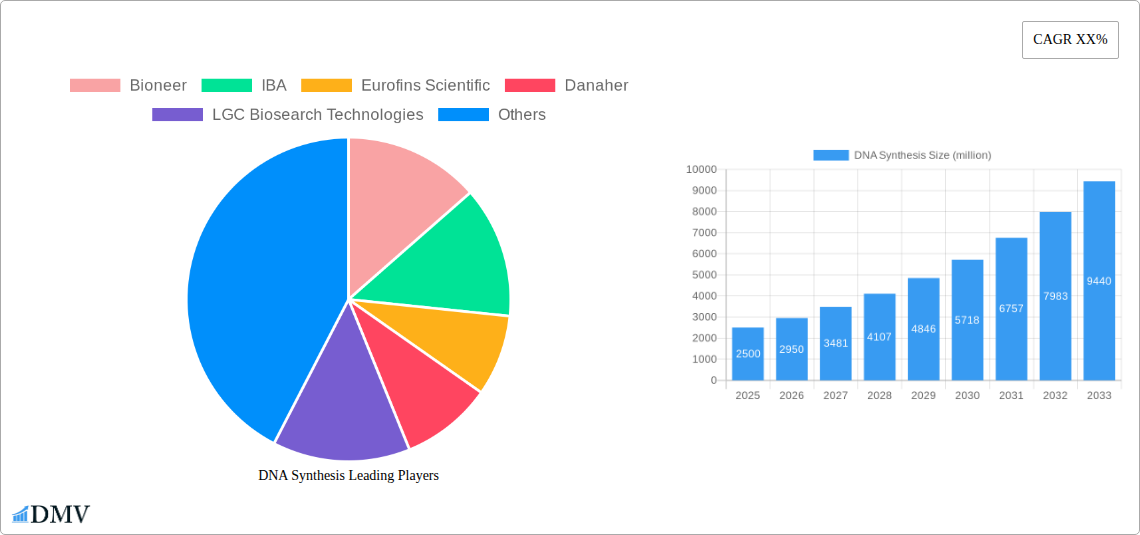

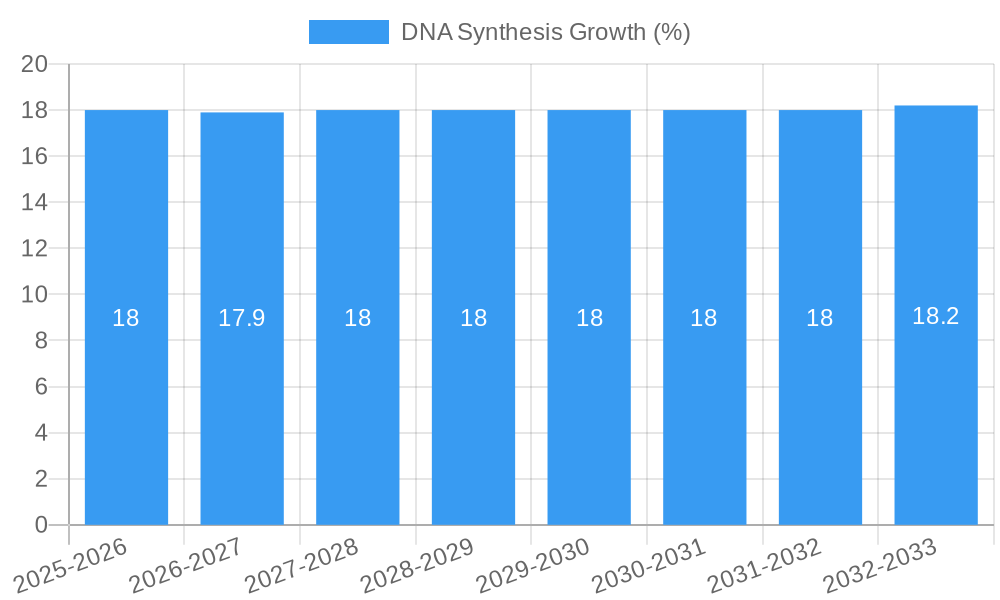

The global DNA synthesis market is poised for significant expansion, projected to reach an estimated \$2,500 million by 2025, with a robust Compound Annual Growth Rate (CAGR) of 18% anticipated through 2033. This impressive growth trajectory is fueled by a confluence of factors, primarily the escalating demand across commercial applications, including diagnostics, drug discovery, and synthetic biology. Academic research also continues to be a strong driver, underpinning fundamental advancements in genomics, molecular biology, and personalized medicine. The market is broadly segmented into oligonucleotide synthesis and gene synthesis, with both segments witnessing substantial uptake due to their critical roles in enabling cutting-edge scientific research and therapeutic development.

Key drivers propelling this market forward include the relentless innovation in DNA sequencing technologies, which paradoxically creates a greater need for synthesized DNA for validation and experimental purposes. Furthermore, the increasing investment in biotechnology and pharmaceutical R&D globally, coupled with the growing awareness and application of gene therapies and advanced diagnostics, are major stimulants. However, the market also faces certain restraints, such as the high cost associated with custom DNA synthesis and the stringent regulatory landscape governing genetic research and its applications. Despite these challenges, emerging trends like the development of more efficient and cost-effective synthesis methods, coupled with the burgeoning field of synthetic biology, are expected to largely offset these limitations, ensuring sustained market growth and innovation.

DNA Synthesis Market Composition & Trends

The global DNA synthesis market is characterized by a dynamic competitive landscape, with a significant presence of both established giants and agile innovators. Market concentration is moderate, driven by continuous innovation and strategic mergers and acquisitions (M&A) aimed at expanding capabilities and market reach. Key innovation catalysts include advancements in next-generation sequencing (NGS), CRISPR technology, and synthetic biology, which are fueling demand for custom DNA sequences for diverse applications. Regulatory landscapes, while evolving, largely support research and development, particularly in areas like personalized medicine and novel therapeutics. Substitute products, such as pre-designed DNA libraries, offer limited competition for highly specialized custom synthesis needs. End-user profiles are diverse, encompassing academic research institutions, pharmaceutical and biotechnology companies, and diagnostic laboratories, all requiring increasingly complex and large-scale DNA constructs. M&A activities have been substantial, with deal values often in the hundreds of millions of dollars, as companies like Thermo Fisher Scientific, Danaher, and GenScript Biotech acquire smaller, specialized firms to consolidate market share and enhance their product portfolios. For instance, the acquisition of LGC Biosearch Technologies by LGC Group aimed to bolster its offerings in genomics and molecular diagnostics. Market share distribution sees major players holding significant portions, but the fragmented nature of custom synthesis also allows for specialized niche players to thrive.

- Market Share Distribution: Dominated by key players with an estimated XXX million in combined market share.

- M&A Deal Values: Average deal values ranging from XXX million to XXX million in recent years.

- Innovation Catalysts: Advancements in NGS, CRISPR, synthetic biology, and mRNA therapeutics.

- Regulatory Landscape: Supportive of R&D, with increasing focus on biosecurity and ethical considerations.

- End-User Segments: Pharmaceutical & Biotechnology (XX% share), Academic & Government Research (XX% share), Diagnostics (XX% share), and others.

DNA Synthesis Industry Evolution

The DNA synthesis industry has witnessed a remarkable evolution, transforming from a niche laboratory technique to a foundational pillar of modern life sciences and biotechnology. The study period from 2019 to 2033, with a base year of 2025, illustrates this trajectory of exponential growth and technological sophistication. Throughout the historical period of 2019–2024, market growth was primarily driven by increasing investments in genomics research, the burgeoning field of gene therapy, and the demand for custom oligonucleotides for PCR and sequencing applications. Companies like Thermo Fisher Scientific and GenScript Biotech emerged as frontrunners, leveraging their extensive R&D capabilities and global distribution networks to capture significant market share.

The forecast period of 2025–2033 is poised to see an accelerated growth rate, estimated to be in the high single digits to low double digits annually, driven by several interconnected factors. Technological advancements in oligo synthesis, such as enhanced phosphoramidite chemistry and the development of novel solid-phase synthesis methods, have drastically improved synthesis speed, accuracy, and the length of obtainable DNA sequences. This has directly impacted the Types segment, with Gene Synthesis experiencing particularly robust expansion as researchers move towards creating custom genes for protein expression, gene editing, and synthetic biology applications.

Furthermore, shifting consumer demands, particularly in the pharmaceutical sector, are reshaping the industry. The rise of mRNA vaccines and therapeutics has created an unprecedented demand for mRNA synthesis, a closely related field that benefits directly from advancements in DNA synthesis technologies. The increasing focus on personalized medicine, diagnostics, and drug discovery also necessitates highly specific and custom-synthesized DNA, further fueling market expansion. The commercial application segment is growing at a faster pace than academic research, reflecting the increasing translation of genomic insights into tangible products and services. The adoption metrics for automated synthesis platforms and cloud-based design tools are steadily rising, indicating a trend towards greater efficiency and accessibility. The industry is not only expanding in terms of output but also in its complexity, with a growing emphasis on delivering longer, error-free DNA constructs with enhanced purity and functionality.

Leading Regions, Countries, or Segments in DNA Synthesis

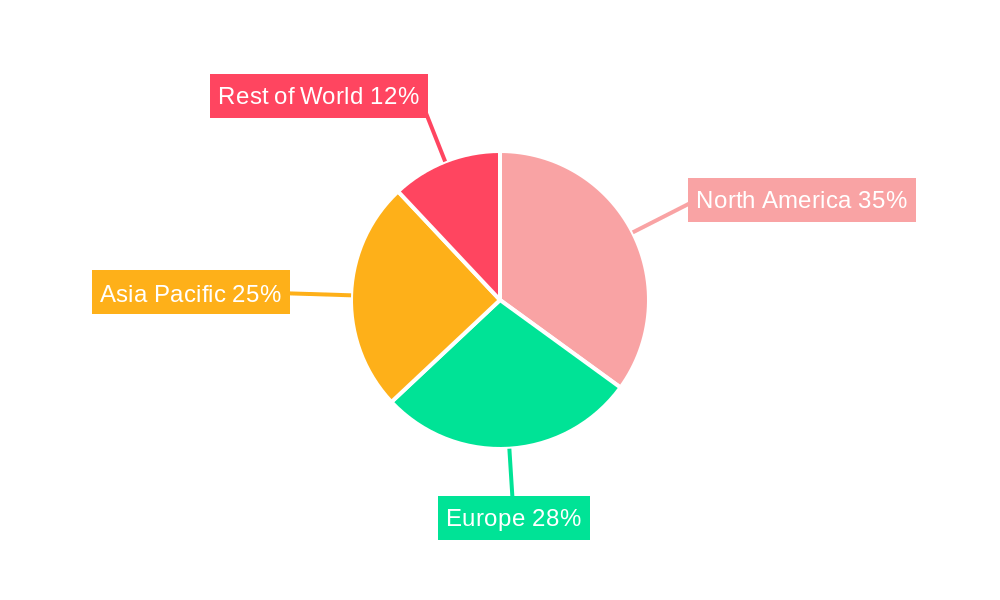

The Gene Synthesis segment stands out as the dominant force in the global DNA synthesis market, showcasing exceptional growth and widespread adoption. This dominance is underpinned by a confluence of factors, including burgeoning advancements in synthetic biology, the accelerating pace of gene therapy development, and the increasing need for custom-designed genes in various research and commercial applications. North America currently leads as the dominant region, driven by substantial investments in biotechnology and pharmaceutical research, a robust academic research infrastructure, and supportive government initiatives.

Key Drivers of Dominance for Gene Synthesis:

- Synthetic Biology Advancements: Gene synthesis is the cornerstone of synthetic biology, enabling the creation of novel biological parts, devices, and systems. The exponential growth in this field, from engineering microbes for biofuels to developing complex gene circuits, directly fuels demand for gene synthesis services.

- Gene Therapy & Cell Therapy Boom: The rapid progress and increasing regulatory approvals for gene therapies and cell therapies represent a massive driver for custom gene synthesis. Companies are requiring large quantities of specific therapeutic genes to be synthesized with high fidelity.

- CRISPR and Gene Editing Applications: The widespread adoption of CRISPR-Cas9 and other gene-editing technologies relies heavily on the availability of precisely synthesized DNA templates and guide RNAs, further boosting the gene synthesis segment.

- Drug Discovery & Development: Pharmaceutical companies are increasingly using gene synthesis to create custom DNA for protein expression, antibody development, and the creation of disease models, accelerating their drug discovery pipelines.

Dominance Factors in North America:

- High R&D Expenditure: The United States, in particular, allocates significant funding to life sciences research, fostering a vibrant ecosystem for gene synthesis demand.

- Strong Biopharmaceutical Hubs: Regions like Boston, San Francisco, and San Diego are global hubs for biotechnology and pharmaceutical innovation, directly translating into high demand for DNA synthesis services.

- Government Funding & Initiatives: Agencies like the National Institutes of Health (NIH) provide substantial funding for genomic research and related technologies, including gene synthesis.

- Presence of Leading Companies: Major players like Thermo Fisher Scientific, Danaher, and GenScript Biotech have significant operations and R&D centers in North America, further solidifying its leadership.

While Gene Synthesis leads in overall impact and growth potential, the Oligonucleotide Synthesis segment remains a critical and consistently growing component of the market, serving foundational needs across diagnostics, PCR, and sequencing. The commercial application segment is rapidly gaining traction, driven by the translation of research findings into commercially viable products and services, outstripping the growth in academic research as the industry matures.

DNA Synthesis Product Innovations

Recent product innovations in DNA synthesis are significantly enhancing capabilities in length, accuracy, and throughput. Advancements in solid-phase synthesis chemistry and automation are enabling the creation of longer, more complex DNA constructs, including custom genes and plasmids, with unprecedented precision and reduced error rates. Companies are also introducing novel delivery systems and specialized synthesis services tailored for emerging applications like mRNA vaccine development and sophisticated gene editing tools. These innovations boast unique selling propositions such as ultra-high fidelity synthesis, rapid turnaround times, and integrated bioinformatics support, directly impacting research efficiency and the development of novel therapeutics and diagnostic solutions. The performance metrics for synthesized DNA are continuously improving, with error rates dropping to single digits per thousand bases and yields increasing, setting new benchmarks for the industry.

Propelling Factors for DNA Synthesis Growth

Several key factors are propelling the growth of the DNA synthesis market. Technological advancements, particularly in phosphoramidite chemistry, solid-phase synthesis, and automated platforms, are enabling higher fidelity, longer sequences, and increased throughput, directly lowering synthesis costs and expanding accessibility. The burgeoning fields of synthetic biology, gene therapy, and personalized medicine are creating an insatiable demand for custom DNA, ranging from simple oligonucleotides to complex genes and genomes. Economic drivers include increasing global R&D investments by pharmaceutical, biotechnology, and academic institutions, fueled by the promise of breakthrough discoveries and novel therapeutics. Regulatory support for gene-based therapies and diagnostics, coupled with the growing commercialization of genomic applications, further stimulates market expansion.

Obstacles in the DNA Synthesis Market

Despite robust growth, the DNA synthesis market faces several obstacles. Stringent regulatory requirements for therapeutic DNA applications, particularly regarding purity and traceability, can increase development timelines and costs. Supply chain disruptions, as witnessed in recent global events, can impact the availability of critical raw materials and reagents, leading to production delays and increased expenses. Intense competitive pressures among established players and emerging companies drive down pricing, potentially impacting profitability. Furthermore, the inherent technical challenges in synthesizing extremely long and complex DNA sequences with absolute fidelity remain a continuous area of development and a potential bottleneck for highly specialized applications.

Future Opportunities in DNA Synthesis

Emerging opportunities in the DNA synthesis market are abundant and diverse. The rapidly expanding field of mRNA therapeutics presents a significant growth avenue, requiring large-scale, high-purity mRNA synthesis, which directly leverages DNA synthesis expertise. The increasing focus on synthetic biology for sustainable solutions, such as biofuels and biomaterials, offers new markets for custom DNA design and synthesis. Advancements in artificial intelligence (AI) and machine learning are paving the way for optimized DNA design and synthesis processes, leading to greater efficiency and novel sequence discovery. The growing demand for advanced diagnostics, including liquid biopsies and gene-based disease screening, also presents substantial opportunities for specialized oligonucleotide and gene synthesis services.

Major Players in the DNA Synthesis Ecosystem

- Bioneer

- IBA

- Eurofins Scientific

- Danaher

- LGC Biosearch Technologies

- Eton Bioscience

- GenScript Biotech

- Kaneka

- Thermo Fisher Scientific

- Quintara Biosciences

Key Developments in DNA Synthesis Industry

- 2023: GenScript Biotech launches its expanded CRISPR gene synthesis platform, offering enhanced speed and accuracy for gene editing applications.

- 2023: Thermo Fisher Scientific announces a significant investment in its oligonucleotide synthesis capabilities to meet growing demand for mRNA therapeutics.

- 2022: Eurofins Scientific acquires a specialized DNA synthesis company, further bolstering its genomics service portfolio.

- 2021: LGC Biosearch Technologies introduces a novel method for synthesizing ultra-long synthetic DNA molecules.

- 2020: Danaher's subsidiaries see increased demand for DNA synthesis services driven by the COVID-19 pandemic and diagnostic assay development.

- 2019: Bioneer reports breakthroughs in high-throughput DNA synthesis, enabling rapid production of custom libraries.

Strategic DNA Synthesis Market Forecast

The strategic DNA synthesis market forecast indicates a trajectory of robust and sustained growth, driven by transformative trends in life sciences and biotechnology. Key growth catalysts include the escalating demand for gene therapies and mRNA-based therapeutics, which necessitate large-scale, high-fidelity DNA synthesis. The rapid advancement and adoption of synthetic biology applications, ranging from sustainable manufacturing to novel biomaterials, will further propel market expansion. Increased global investment in pharmaceutical R&D, particularly in oncology, infectious diseases, and rare genetic disorders, will continue to fuel the need for custom DNA sequences. Emerging markets in diagnostics and personalized medicine, coupled with ongoing technological innovations in synthesis platforms and chemistries, collectively suggest a highly promising and dynamic future for the DNA synthesis industry.

DNA Synthesis Segmentation

-

1. Application

- 1.1. Commercial

- 1.2. Academic Research

-

2. Types

- 2.1. Oligonucleotide Synthesis

- 2.2. Gene Synthesis

DNA Synthesis Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

DNA Synthesis REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global DNA Synthesis Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Commercial

- 5.1.2. Academic Research

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Oligonucleotide Synthesis

- 5.2.2. Gene Synthesis

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America DNA Synthesis Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Commercial

- 6.1.2. Academic Research

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Oligonucleotide Synthesis

- 6.2.2. Gene Synthesis

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America DNA Synthesis Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Commercial

- 7.1.2. Academic Research

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Oligonucleotide Synthesis

- 7.2.2. Gene Synthesis

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe DNA Synthesis Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Commercial

- 8.1.2. Academic Research

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Oligonucleotide Synthesis

- 8.2.2. Gene Synthesis

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa DNA Synthesis Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Commercial

- 9.1.2. Academic Research

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Oligonucleotide Synthesis

- 9.2.2. Gene Synthesis

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific DNA Synthesis Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Commercial

- 10.1.2. Academic Research

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Oligonucleotide Synthesis

- 10.2.2. Gene Synthesis

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Bioneer

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 IBA

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Eurofins Scientific

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Danaher

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 LGC Biosearch Technologies

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Eton Bioscience

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 GenScript Biotech

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Kaneka

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Thermo Fisher Scientific

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Quintara Biosciences

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 Bioneer

List of Figures

- Figure 1: Global DNA Synthesis Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America DNA Synthesis Revenue (million), by Application 2024 & 2032

- Figure 3: North America DNA Synthesis Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America DNA Synthesis Revenue (million), by Types 2024 & 2032

- Figure 5: North America DNA Synthesis Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America DNA Synthesis Revenue (million), by Country 2024 & 2032

- Figure 7: North America DNA Synthesis Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America DNA Synthesis Revenue (million), by Application 2024 & 2032

- Figure 9: South America DNA Synthesis Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America DNA Synthesis Revenue (million), by Types 2024 & 2032

- Figure 11: South America DNA Synthesis Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America DNA Synthesis Revenue (million), by Country 2024 & 2032

- Figure 13: South America DNA Synthesis Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe DNA Synthesis Revenue (million), by Application 2024 & 2032

- Figure 15: Europe DNA Synthesis Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe DNA Synthesis Revenue (million), by Types 2024 & 2032

- Figure 17: Europe DNA Synthesis Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe DNA Synthesis Revenue (million), by Country 2024 & 2032

- Figure 19: Europe DNA Synthesis Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa DNA Synthesis Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa DNA Synthesis Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa DNA Synthesis Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa DNA Synthesis Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa DNA Synthesis Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa DNA Synthesis Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific DNA Synthesis Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific DNA Synthesis Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific DNA Synthesis Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific DNA Synthesis Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific DNA Synthesis Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific DNA Synthesis Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global DNA Synthesis Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global DNA Synthesis Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global DNA Synthesis Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global DNA Synthesis Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global DNA Synthesis Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global DNA Synthesis Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global DNA Synthesis Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States DNA Synthesis Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada DNA Synthesis Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico DNA Synthesis Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global DNA Synthesis Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global DNA Synthesis Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global DNA Synthesis Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil DNA Synthesis Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina DNA Synthesis Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America DNA Synthesis Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global DNA Synthesis Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global DNA Synthesis Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global DNA Synthesis Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom DNA Synthesis Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany DNA Synthesis Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France DNA Synthesis Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy DNA Synthesis Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain DNA Synthesis Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia DNA Synthesis Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux DNA Synthesis Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics DNA Synthesis Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe DNA Synthesis Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global DNA Synthesis Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global DNA Synthesis Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global DNA Synthesis Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey DNA Synthesis Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel DNA Synthesis Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC DNA Synthesis Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa DNA Synthesis Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa DNA Synthesis Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa DNA Synthesis Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global DNA Synthesis Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global DNA Synthesis Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global DNA Synthesis Revenue million Forecast, by Country 2019 & 2032

- Table 41: China DNA Synthesis Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India DNA Synthesis Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan DNA Synthesis Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea DNA Synthesis Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN DNA Synthesis Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania DNA Synthesis Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific DNA Synthesis Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the DNA Synthesis?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the DNA Synthesis?

Key companies in the market include Bioneer, IBA, Eurofins Scientific, Danaher, LGC Biosearch Technologies, Eton Bioscience, GenScript Biotech, Kaneka, Thermo Fisher Scientific, Quintara Biosciences.

3. What are the main segments of the DNA Synthesis?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "DNA Synthesis," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the DNA Synthesis report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the DNA Synthesis?

To stay informed about further developments, trends, and reports in the DNA Synthesis, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence