Key Insights

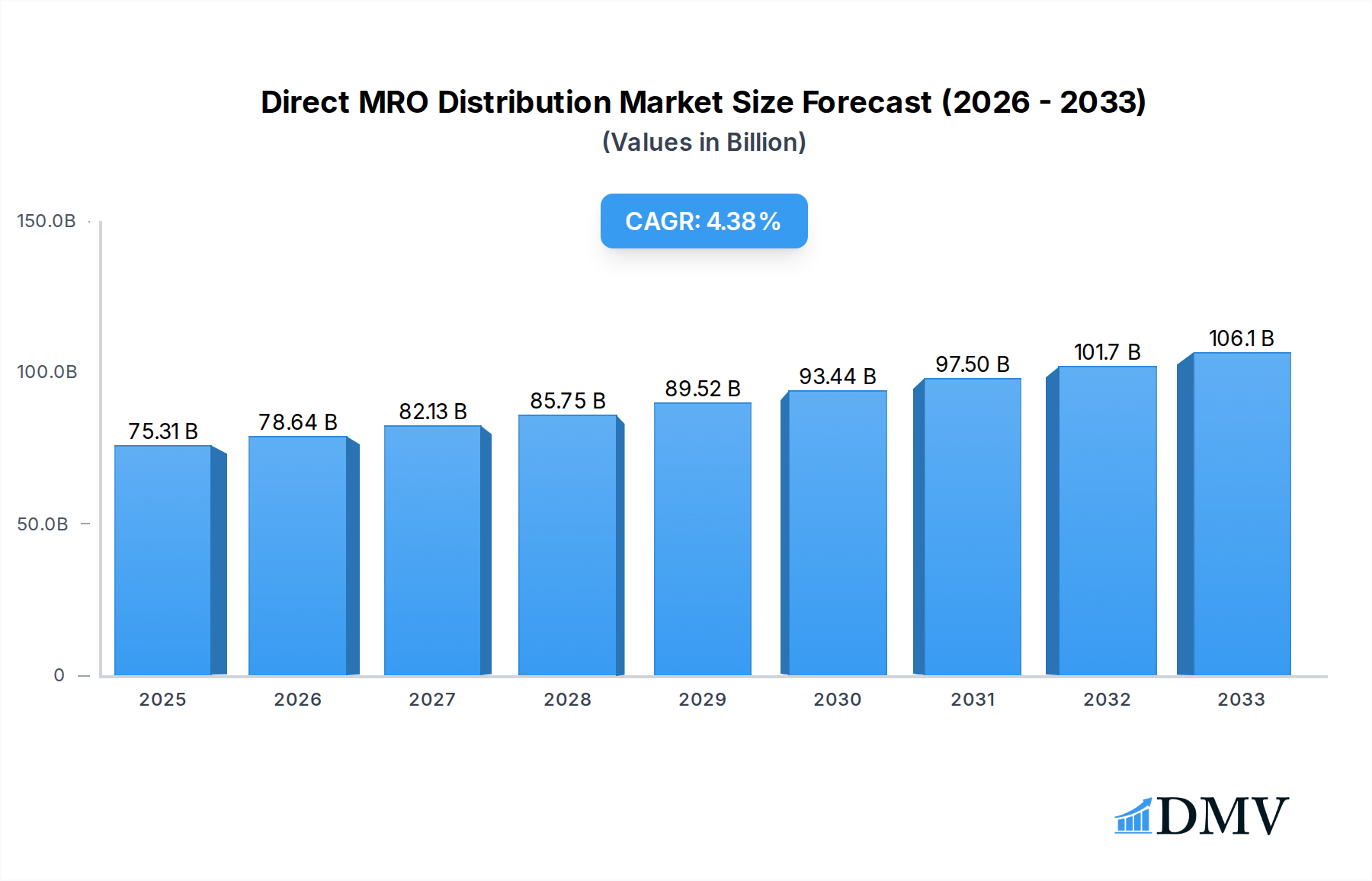

The Direct MRO (Maintenance, Repair, and Operations) Distribution market is poised for substantial growth, projecting a market size of USD 75.31 billion in 2025, with a compound annual growth rate (CAGR) of 4.4% expected to continue through 2033. This robust expansion is primarily driven by increasing industrialization across emerging economies, a growing emphasis on predictive and preventive maintenance strategies to minimize downtime and operational costs, and the continuous adoption of advanced technologies within MRO processes. The demand for efficient and reliable MRO solutions is further fueled by the need to maintain aging infrastructure and the relentless pursuit of operational efficiency across diverse sectors. Industries such as Food, Beverage & Tobacco, Textile, Apparel & Footwear, and Basic Metals & Metal Products are significant contributors to this market, with ongoing investments in upgrading and maintaining their operational capabilities. The shift towards digital MRO solutions, including e-procurement platforms and integrated inventory management systems, is also a significant trend, enhancing accessibility and streamlining the distribution process.

Direct MRO Distribution Market Size (In Billion)

Despite the strong growth trajectory, the market faces certain restraints. These include the volatility in raw material prices, which can impact the cost of MRO supplies, and the complex supply chain logistics inherent in global distribution. Furthermore, the initial investment required for adopting advanced MRO technologies can be a barrier for smaller enterprises. However, the overarching trend of digital transformation, coupled with the increasing awareness of the long-term cost benefits of proactive maintenance, is expected to outweigh these challenges. The market is witnessing consolidation with key players like ABB Group and Schneider Electric expanding their offerings and geographical reach, aiming to capitalize on the burgeoning demand for comprehensive MRO solutions. The segment of Preventive/Scheduled Maintenance is anticipated to see the highest growth, reflecting the strategic importance of minimizing unexpected disruptions in industrial operations.

Direct MRO Distribution Company Market Share

Direct MRO Distribution Market Composition & Trends

The global Direct MRO (Maintenance, Repair, and Operations) Distribution market exhibits a moderately concentrated structure, with key players vying for substantial market share. Innovation is a significant catalyst, driven by the increasing demand for efficient, sustainable, and technologically advanced MRO solutions across diverse industrial sectors. The regulatory landscape, while varying by region, generally favors standardization and safety, indirectly promoting the adoption of high-quality direct distribution channels. Substitute products, such as indirect distribution or in-house procurement, pose a challenge, but direct MRO distribution's advantages in terms of cost control, product expertise, and supply chain optimization often outweigh these alternatives. End-user profiles are broad, encompassing large-scale manufacturing facilities in Food, Beverage & Tobacco, Textile, Apparel & Footwear, Wood & Paper, Mining, Oil & Gas, Basic Metals & Metal Products, Rubber, Plastic and Non-metallic Products, Chemicals, Pharmaceuticals, and Electronics, all seeking seamless access to critical spare parts and operational supplies. Mergers and acquisitions (M&A) are a consistent feature, with deal values in the billions as larger entities consolidate to enhance their product portfolios and geographic reach. For example, the Cromwell Group (Holdings) Limited (Grainger) acquisition was valued at over xx billion. Key market trends include the rise of e-commerce platforms for MRO procurement, the increasing demand for predictive maintenance solutions, and a growing emphasis on sustainable MRO practices. The market share distribution sees dominant players holding significant portions, with opportunities for niche providers to thrive by focusing on specialized product categories or advanced service offerings. The overall market valuation is projected to reach xx billion by 2033, with a Compound Annual Growth Rate (CAGR) of xx%.

- Market Concentration: Moderate to High, driven by strategic M&A and economies of scale.

- Innovation Catalysts: Demand for automation, IoT integration, and sustainable solutions.

- Regulatory Landscapes: Emphasis on safety, environmental compliance, and supply chain transparency.

- Substitute Products: Indirect distribution, direct purchasing from OEMs, and in-house solutions.

- End-User Profiles: Manufacturing, heavy industry, energy, pharmaceuticals, electronics, and automotive.

- M&A Activities: Ongoing consolidation to expand service offerings and market reach, with significant deal values exceeding xx billion annually.

Direct MRO Distribution Industry Evolution

The Direct MRO Distribution industry has undergone a remarkable evolution, transforming from a fragmented and often cumbersome procurement process into a sophisticated, technology-driven ecosystem. The historical period from 2019–2024 witnessed a steady expansion, fueled by the increasing reliance on robust MRO strategies to ensure operational continuity and minimize downtime across various industrial applications. The base year of 2025 is projected to see a market valuation of xx billion, with substantial growth anticipated throughout the forecast period of 2025–2033. This trajectory is primarily propelled by significant technological advancements, including the widespread adoption of digital procurement platforms, the integration of Internet of Things (IoT) sensors for predictive maintenance, and the utilization of advanced analytics for inventory management. These innovations have not only streamlined the MRO supply chain but have also empowered businesses with real-time data for proactive decision-making, thereby reducing unexpected equipment failures and associated costs.

The growth trajectories have been particularly pronounced in sectors requiring continuous operation, such as Mining, Oil & Gas, Basic Metals & Metal Products, and Pharmaceuticals. These industries, characterized by high operational costs and stringent regulatory requirements, have embraced direct MRO distribution as a means to ensure the timely availability of critical spare parts and consumables. The adoption metrics for digital MRO solutions have surged, with an estimated xx% of large enterprises integrating e-procurement portals by 2025. Furthermore, the shift in consumer demands, from a purely transactional relationship to a more service-oriented partnership, has compelled MRO distributors to enhance their value-added offerings. This includes providing technical support, customized stocking solutions, and on-site services, all of which contribute to a stronger competitive advantage.

The study period of 2019–2033 encapsulates a significant transformation, marked by increasing globalization of supply chains and a heightened awareness of supply chain resilience. The COVID-19 pandemic, while presenting initial disruptions, also acted as a potent catalyst for digital transformation and the reinforcement of robust MRO strategies, highlighting the criticality of reliable direct distribution channels. Consequently, the industry has witnessed a substantial increase in the demand for specialized MRO services tailored to specific industry needs. For instance, the ABB Group and Schneider Electric are at the forefront of providing integrated digital solutions that enhance MRO efficiency, impacting the market growth rates significantly. The market is also seeing a rise in companies offering comprehensive MRO solutions, encompassing everything from spare parts management to repair and refurbishment services, further solidifying the direct distribution model. The estimated growth rate for the Direct MRO Distribution market is projected to be a CAGR of xx% during the forecast period, reaching an estimated xx billion by 2033.

Leading Regions, Countries, or Segments in Direct MRO Distribution

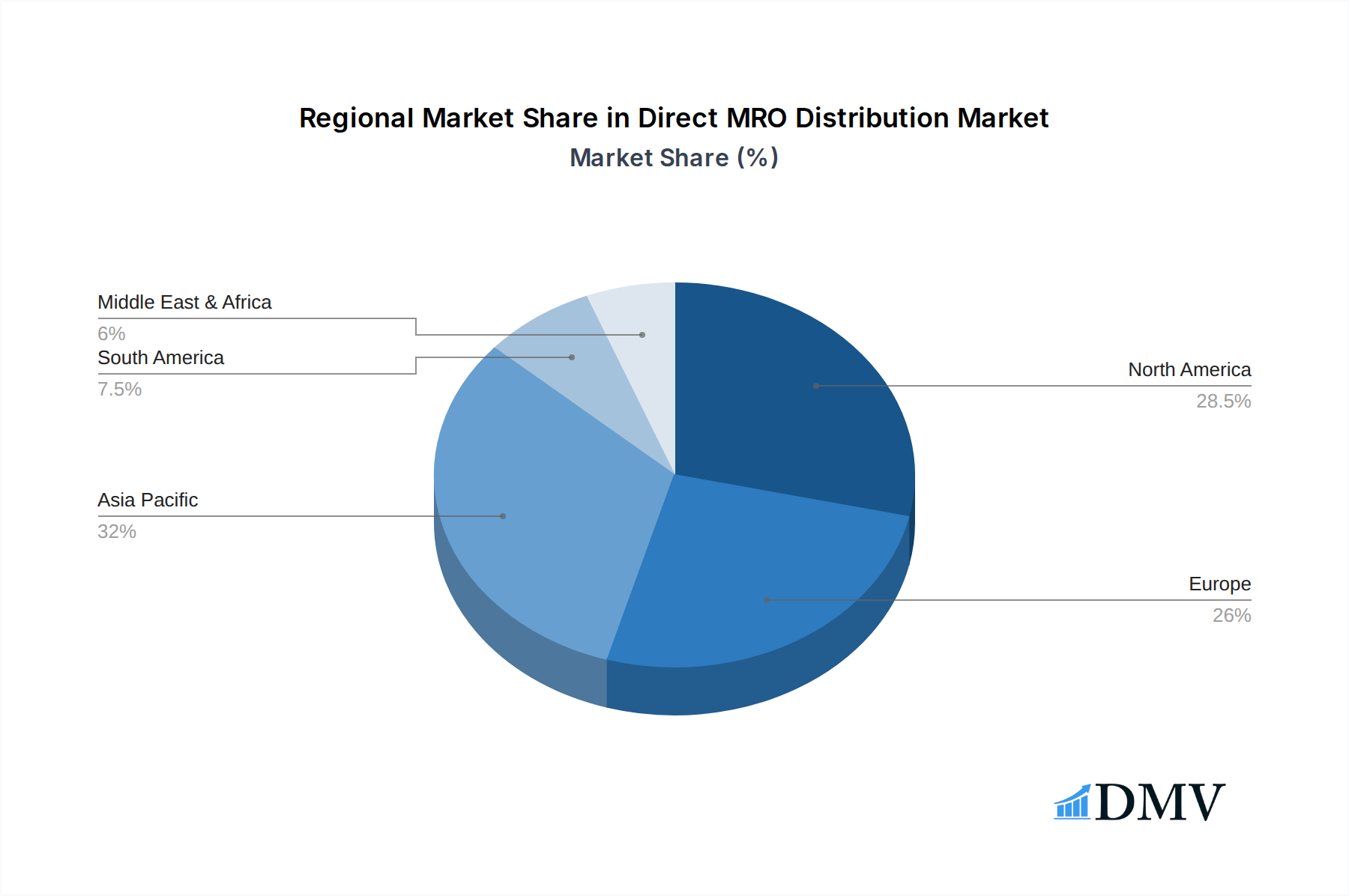

The global Direct MRO Distribution market is characterized by significant regional disparities and segment dominance, driven by a complex interplay of industrial activity, technological adoption, and economic development. North America and Europe currently lead in market share, owing to their well-established industrial bases, high levels of technological integration, and strong emphasis on operational efficiency across sectors like Food, Beverage & Tobacco, Chemicals, and Pharmaceuticals. The Electronics segment, in particular, demonstrates a robust demand for direct MRO due to the rapid pace of technological innovation and the need for specialized, high-precision components. Within North America, the United States is a pivotal market, driven by extensive manufacturing operations and a strong presence of major players like Graco Inc. and ABB Group. In Europe, Germany and the United Kingdom are key contributors, with significant industrial output and a mature MRO distribution network.

The Mining, Oil & Gas and Basic Metals & Metal Products segments, while geographically dispersed, represent substantial markets for direct MRO, particularly in regions with rich natural resources. Countries like Australia, Canada, and several nations in the Middle East exhibit high demand for specialized MRO solutions to maintain critical infrastructure and extraction equipment. The investment trends in these regions are heavily influenced by global commodity prices and infrastructure development projects, leading to significant MRO procurement.

Conversely, the Asia-Pacific region is emerging as a rapidly growing market. China, with its vast manufacturing capabilities spanning nearly all listed segments, including Textile, Apparel & Footwear, Wood & Paper, and Rubber, Plastic and Non-metallic Products, is a key driver of this growth. Increasing industrialization, coupled with government initiatives to promote domestic manufacturing and technological advancement, is fueling the demand for efficient direct MRO distribution. Countries like India and Southeast Asian nations are also witnessing considerable expansion in their MRO needs as their industrial sectors mature.

The application of Preventive/Scheduled Maintenance represents a dominant segment within MRO types. Companies are increasingly prioritizing proactive maintenance strategies to minimize costly unscheduled downtime. This translates into a consistent demand for direct access to genuine spare parts and consumables, as well as expert technical support, which direct MRO distributors are well-positioned to provide. The focus on extending the lifespan of critical assets and optimizing operational performance further solidifies the importance of this maintenance type.

The regulatory support in developed regions, focusing on safety standards and environmental compliance, indirectly boosts the demand for certified and high-quality MRO products, often best sourced through direct channels. The dominance factors are thus a combination of economic prowess, industrial diversification, technological adoption rates, and proactive maintenance strategies. For instance, the Schneider Electric's commitment to energy management and automation solutions directly influences the MRO needs in the Electronics and Basic Metals & Metal Products sectors, highlighting the interconnectedness of industry trends and MRO demand.

Direct MRO Distribution Product Innovations

Direct MRO Distribution is witnessing significant product innovations aimed at enhancing efficiency, extending asset life, and improving operational safety. Companies like Graco Inc. are introducing advanced spraying and coating technologies that offer superior performance and reduced material waste, critical in sectors like Basic Metals & Metal Products and Rubber, Plastic and Non-metallic Products. WABCO (ZF), a key player in commercial vehicle technologies, is innovating in braking and transmission systems, providing direct access to highly reliable and durable components essential for the Mining, Oil & Gas and logistics sectors. Valeo Service UK Ltd is at the forefront of automotive aftermarket MRO, focusing on advanced powertrain and thermal management systems, ensuring vehicles in the Food, Beverage & Tobacco and Textile, Apparel & Footwear logistics chains remain operational. The integration of smart sensors and predictive analytics into MRO components, championed by companies like ABB Group and Rohde & Schwarz, allows for real-time performance monitoring and proactive fault detection, significantly reducing unscheduled downtime and maintenance costs across all industries. These innovations translate to improved mean time between failures (MTBF) and reduced total cost of ownership for end-users, offering unique selling propositions in a competitive market.

Propelling Factors for Direct MRO Distribution Growth

Several key factors are propelling the growth of the Direct MRO Distribution market. Technologically, the increasing integration of the Industrial Internet of Things (IIoT) enables predictive maintenance, reducing unexpected downtime and driving demand for direct access to genuine parts. Economically, the continuous need for operational efficiency and cost optimization across manufacturing and heavy industries encourages businesses to streamline their MRO procurement through direct channels, minimizing intermediaries and their associated markups. Regulatory influences, such as stricter safety standards and environmental mandates in sectors like Chemicals and Pharmaceuticals, also drive the demand for certified, high-quality MRO components, which are best secured through direct distribution. Furthermore, the global expansion of industrial activities, particularly in emerging economies, creates a growing customer base for MRO supplies.

Obstacles in the Direct MRO Distribution Market

Despite robust growth, the Direct MRO Distribution market faces several obstacles. Regulatory challenges, including varying compliance standards across different countries and industries, can complicate international distribution and increase operational costs. Supply chain disruptions, as evidenced by recent global events, can lead to extended lead times and shortages of critical MRO components, impacting operational continuity. Competitive pressures from indirect distributors and direct-to-consumer e-commerce platforms offering lower price points can also pose a challenge, although often at the expense of product authenticity and technical support. The significant capital investment required for maintaining large inventories and sophisticated distribution networks can also be a barrier to entry for smaller players, potentially impacting market concentration.

Future Opportunities in Direct MRO Distribution

The Direct MRO Distribution market is ripe with future opportunities. The burgeoning adoption of Industry 4.0 technologies, including AI and machine learning for inventory forecasting and demand planning, presents a significant avenue for enhancing efficiency and customer service. The increasing focus on sustainability and circular economy principles is creating opportunities for distributors to offer refurbished parts, repair services, and environmentally friendly MRO solutions. Emerging markets in Asia-Pacific and Africa, with their rapidly industrializing economies, represent vast untapped potential for market penetration. Furthermore, the development of specialized MRO solutions tailored to niche industries or specific equipment types, such as those offered by Mento AS for specialized applications, can carve out profitable market segments and cater to evolving customer needs.

Major Players in the Direct MRO Distribution Ecosystem

- Cromwell Group (Holdings) Limited

- Graco Inc.

- WABCO (ZF)

- Mento AS

- Valeo Service UK Ltd

- Ascendum

- Bodo Möller Chemie GmbH

- Lindberg & Lund AS (Biesterfeld)

- Neumo-Egmo Spain SL

- Gazechim Composites Norden AB

- ABB Group

- Rohde & Schwarz

- Schneider Electric

Key Developments in Direct MRO Distribution Industry

- 2023: ABB Group launched an advanced suite of digital MRO solutions integrating AI for predictive maintenance across industrial automation, significantly enhancing asset uptime and reducing operational costs.

- 2023: Graco Inc. expanded its global service network for specialized fluid handling equipment, offering enhanced on-site support and faster delivery of critical spare parts for the Oil & Gas sector.

- 2023: Schneider Electric partnered with several leading industrial manufacturers to create a unified platform for MRO procurement and lifecycle management, simplifying supply chains and improving data visibility.

- 2024: WABCO (ZF) introduced new diagnostic tools for its advanced braking and transmission systems, enabling direct technicians to identify and resolve issues more efficiently, reducing vehicle downtime in the logistics sector.

- 2024: Valeo Service UK Ltd launched an expanded range of electric vehicle components and related MRO solutions, catering to the growing demand for specialized services in the automotive aftermarket.

- 2024: Bodo Möller Chemie GmbH acquired a key distributor in the European adhesives and sealants market, strengthening its position in specialized chemical MRO and expanding its product portfolio for the Rubber, Plastic and Non-metallic Products sector.

- 2024: Lindberg & Lund AS (Biesterfeld) announced a strategic expansion into the Nordic region, enhancing its direct distribution capabilities for a broad range of specialty chemicals and polymers.

- 2024: Rohde & Schwarz unveiled a new generation of test and measurement equipment crucial for the Electronics manufacturing sector, offering improved accuracy and faster diagnostics for complex electronic components.

- 2024: Cromwell Group (Holdings) Limited (Grainger) continued its digital transformation initiatives, optimizing its e-commerce platform to provide a more intuitive and efficient MRO purchasing experience for industrial clients.

- 2024: Neumo-Egmo Spain SL launched a new line of high-performance valves and fittings designed for demanding applications in the Chemicals and Pharmaceuticals industries, emphasizing reliability and corrosion resistance.

Strategic Direct MRO Distribution Market Forecast

The Direct MRO Distribution market is poised for robust growth, fueled by an increasing emphasis on operational efficiency, technological integration, and supply chain resilience. The forecast period anticipates sustained expansion driven by the adoption of Industry 4.0 solutions, particularly IIoT for predictive maintenance, and the growing demand for sustainable MRO practices. Emerging markets offer significant potential for new entrants and expansion by established players. Strategic collaborations and M&A activities are expected to continue shaping the market landscape, leading to consolidation and enhanced service offerings. The market's ability to adapt to evolving industry needs and provide value-added services will be critical for capitalizing on future opportunities and achieving significant market potential.

Direct MRO Distribution Segmentation

-

1. Application

- 1.1. Food, Beverage & Tobacco

- 1.2. Textile, Apparel & Footwear

- 1.3. Wood & Paper

- 1.4. Mining, Oil & Gas

- 1.5. Basic Metals & Metal Products

- 1.6. Rubber, Plastic and Non-metallic Products

- 1.7. Chemicals

- 1.8. Pharmaceuticals

- 1.9. Electronics

- 1.10. Others

-

2. Types

- 2.1. Preventive/Scheduled Maintenance

- 2.2. Corrective Maintenance

Direct MRO Distribution Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Direct MRO Distribution Regional Market Share

Geographic Coverage of Direct MRO Distribution

Direct MRO Distribution REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Direct MRO Distribution Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Food, Beverage & Tobacco

- 5.1.2. Textile, Apparel & Footwear

- 5.1.3. Wood & Paper

- 5.1.4. Mining, Oil & Gas

- 5.1.5. Basic Metals & Metal Products

- 5.1.6. Rubber, Plastic and Non-metallic Products

- 5.1.7. Chemicals

- 5.1.8. Pharmaceuticals

- 5.1.9. Electronics

- 5.1.10. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Preventive/Scheduled Maintenance

- 5.2.2. Corrective Maintenance

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Direct MRO Distribution Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Food, Beverage & Tobacco

- 6.1.2. Textile, Apparel & Footwear

- 6.1.3. Wood & Paper

- 6.1.4. Mining, Oil & Gas

- 6.1.5. Basic Metals & Metal Products

- 6.1.6. Rubber, Plastic and Non-metallic Products

- 6.1.7. Chemicals

- 6.1.8. Pharmaceuticals

- 6.1.9. Electronics

- 6.1.10. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Preventive/Scheduled Maintenance

- 6.2.2. Corrective Maintenance

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Direct MRO Distribution Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Food, Beverage & Tobacco

- 7.1.2. Textile, Apparel & Footwear

- 7.1.3. Wood & Paper

- 7.1.4. Mining, Oil & Gas

- 7.1.5. Basic Metals & Metal Products

- 7.1.6. Rubber, Plastic and Non-metallic Products

- 7.1.7. Chemicals

- 7.1.8. Pharmaceuticals

- 7.1.9. Electronics

- 7.1.10. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Preventive/Scheduled Maintenance

- 7.2.2. Corrective Maintenance

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Direct MRO Distribution Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Food, Beverage & Tobacco

- 8.1.2. Textile, Apparel & Footwear

- 8.1.3. Wood & Paper

- 8.1.4. Mining, Oil & Gas

- 8.1.5. Basic Metals & Metal Products

- 8.1.6. Rubber, Plastic and Non-metallic Products

- 8.1.7. Chemicals

- 8.1.8. Pharmaceuticals

- 8.1.9. Electronics

- 8.1.10. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Preventive/Scheduled Maintenance

- 8.2.2. Corrective Maintenance

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Direct MRO Distribution Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Food, Beverage & Tobacco

- 9.1.2. Textile, Apparel & Footwear

- 9.1.3. Wood & Paper

- 9.1.4. Mining, Oil & Gas

- 9.1.5. Basic Metals & Metal Products

- 9.1.6. Rubber, Plastic and Non-metallic Products

- 9.1.7. Chemicals

- 9.1.8. Pharmaceuticals

- 9.1.9. Electronics

- 9.1.10. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Preventive/Scheduled Maintenance

- 9.2.2. Corrective Maintenance

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Direct MRO Distribution Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Food, Beverage & Tobacco

- 10.1.2. Textile, Apparel & Footwear

- 10.1.3. Wood & Paper

- 10.1.4. Mining, Oil & Gas

- 10.1.5. Basic Metals & Metal Products

- 10.1.6. Rubber, Plastic and Non-metallic Products

- 10.1.7. Chemicals

- 10.1.8. Pharmaceuticals

- 10.1.9. Electronics

- 10.1.10. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Preventive/Scheduled Maintenance

- 10.2.2. Corrective Maintenance

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Cromwell Group (Holdings) Limited (Grainger)

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Graco Inc.

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 WABCO (ZF)

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Mento AS

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Valeo Service UK Ltd

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Ascendum

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Bodo Möller Chemie GmbH

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Lindberg & Lund AS (Biesterfeld)

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Neumo-Egmo Spain SL

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Gazechim Composites Norden AB

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 ABB Group

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Rohde & Schwarz

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Schneider Electric

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.1 Cromwell Group (Holdings) Limited (Grainger)

List of Figures

- Figure 1: Global Direct MRO Distribution Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Direct MRO Distribution Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Direct MRO Distribution Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Direct MRO Distribution Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Direct MRO Distribution Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Direct MRO Distribution Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Direct MRO Distribution Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Direct MRO Distribution Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Direct MRO Distribution Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Direct MRO Distribution Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Direct MRO Distribution Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Direct MRO Distribution Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Direct MRO Distribution Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Direct MRO Distribution Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Direct MRO Distribution Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Direct MRO Distribution Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Direct MRO Distribution Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Direct MRO Distribution Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Direct MRO Distribution Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Direct MRO Distribution Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Direct MRO Distribution Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Direct MRO Distribution Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Direct MRO Distribution Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Direct MRO Distribution Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Direct MRO Distribution Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Direct MRO Distribution Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Direct MRO Distribution Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Direct MRO Distribution Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Direct MRO Distribution Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Direct MRO Distribution Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Direct MRO Distribution Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Direct MRO Distribution Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Direct MRO Distribution Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Direct MRO Distribution Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Direct MRO Distribution Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Direct MRO Distribution Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Direct MRO Distribution Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Direct MRO Distribution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Direct MRO Distribution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Direct MRO Distribution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Direct MRO Distribution Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Direct MRO Distribution Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Direct MRO Distribution Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Direct MRO Distribution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Direct MRO Distribution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Direct MRO Distribution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Direct MRO Distribution Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Direct MRO Distribution Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Direct MRO Distribution Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Direct MRO Distribution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Direct MRO Distribution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Direct MRO Distribution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Direct MRO Distribution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Direct MRO Distribution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Direct MRO Distribution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Direct MRO Distribution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Direct MRO Distribution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Direct MRO Distribution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Direct MRO Distribution Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Direct MRO Distribution Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Direct MRO Distribution Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Direct MRO Distribution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Direct MRO Distribution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Direct MRO Distribution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Direct MRO Distribution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Direct MRO Distribution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Direct MRO Distribution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Direct MRO Distribution Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Direct MRO Distribution Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Direct MRO Distribution Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Direct MRO Distribution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Direct MRO Distribution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Direct MRO Distribution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Direct MRO Distribution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Direct MRO Distribution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Direct MRO Distribution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Direct MRO Distribution Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Direct MRO Distribution?

The projected CAGR is approximately 4.4%.

2. Which companies are prominent players in the Direct MRO Distribution?

Key companies in the market include Cromwell Group (Holdings) Limited (Grainger), Graco Inc., WABCO (ZF), Mento AS, Valeo Service UK Ltd, Ascendum, Bodo Möller Chemie GmbH, Lindberg & Lund AS (Biesterfeld), Neumo-Egmo Spain SL, Gazechim Composites Norden AB, ABB Group, Rohde & Schwarz, Schneider Electric.

3. What are the main segments of the Direct MRO Distribution?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Direct MRO Distribution," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Direct MRO Distribution report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Direct MRO Distribution?

To stay informed about further developments, trends, and reports in the Direct MRO Distribution, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence