Key Insights

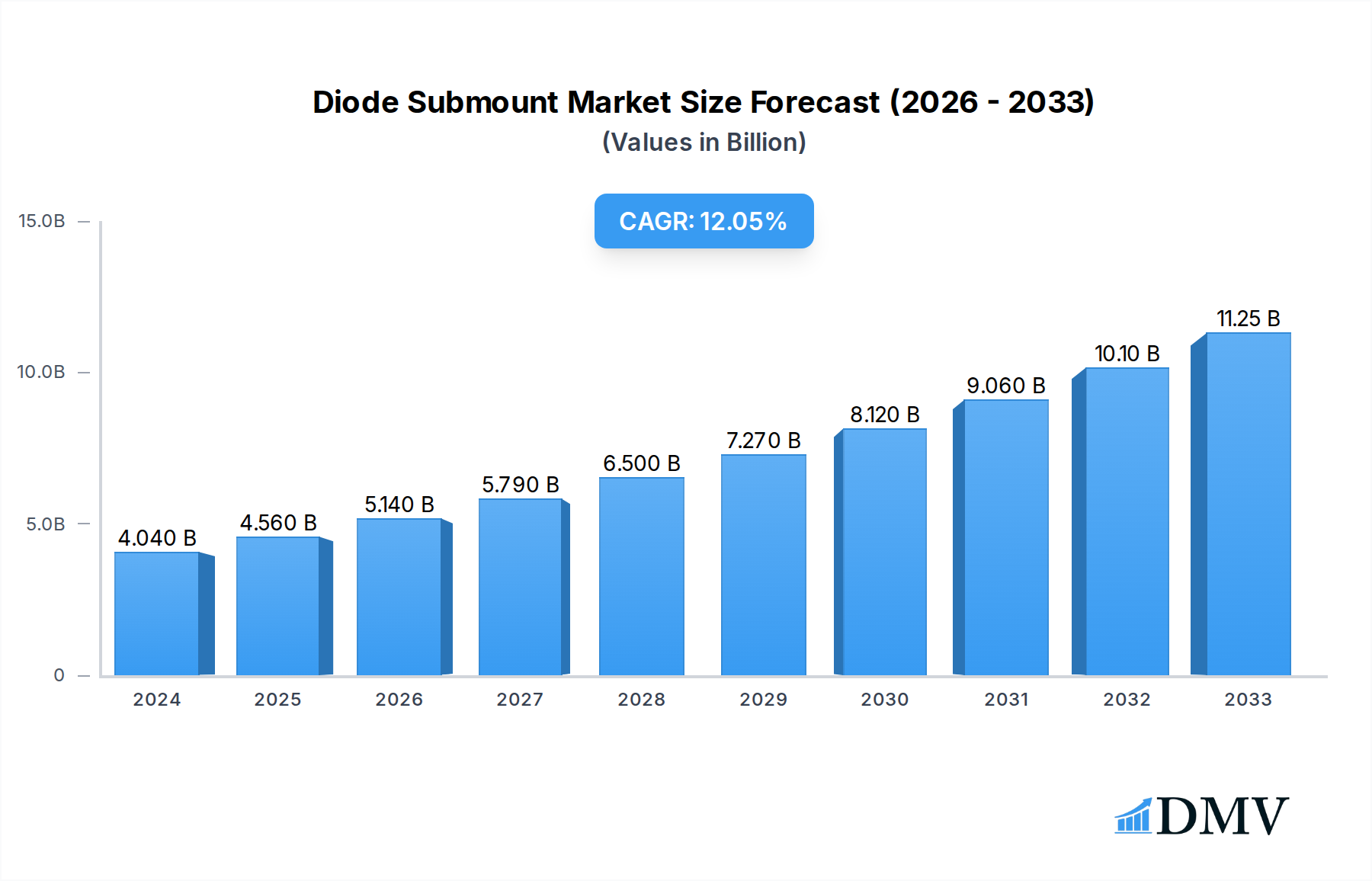

The global Diode Submount market is experiencing robust growth, projected to reach an estimated $4.04 billion in 2024, with a significant Compound Annual Growth Rate (CAGR) of 12.6% projected through 2033. This expansion is primarily driven by the escalating demand for advanced optoelectronic components across various high-growth industries. The proliferation of laser diodes (LDs) in telecommunications, industrial manufacturing (laser cutting and welding), and medical devices (surgical lasers, diagnostic equipment) is a primary catalyst. Similarly, the widespread adoption of light-emitting diodes (LEDs) in solid-state lighting, automotive applications, and display technologies continues to fuel market expansion. Photo diodes (PDs) are also witnessing increased utilization in sensor technology, imaging systems, and optical communication. The market is characterized by continuous innovation in materials science, with advancements in ceramics like Alumina, Aluminum Nitride, and Beryllium Oxide offering enhanced thermal conductivity and electrical insulation properties, crucial for high-power diode performance and longevity.

Diode Submount Market Size (In Billion)

The market's upward trajectory is further supported by emerging trends such as miniaturization of electronic devices, the growing integration of optoelectronics in the Internet of Things (IoT) ecosystem, and the increasing R&D investments in next-generation semiconductor technologies. Emerging applications in advanced sensing, lidar for autonomous vehicles, and high-speed optical networking are expected to unlock new avenues for market growth. While the market presents significant opportunities, potential restraints include the high cost of advanced manufacturing processes and the need for stringent quality control to ensure device reliability. Geographically, the Asia Pacific region, particularly China and South Korea, is emerging as a dominant force due to its strong manufacturing base and increasing domestic demand for electronic components. North America and Europe are also significant contributors, driven by technological innovation and the presence of key market players.

Diode Submount Company Market Share

This comprehensive report delves into the diode submount market, offering an in-depth analysis of its current landscape, historical trajectory, and future projections. Spanning the study period of 2019–2033, with a base year of 2025 and a forecast period of 2025–2033, this research provides invaluable insights for stakeholders seeking to navigate this dynamic sector. We dissect market concentration, innovation drivers, regulatory frameworks, and the competitive landscape, featuring key players like SemiGen, Kyocera, Remtec, Thorlabs, Sheaumann Laser, Inc, Applied Thin-Film Products (ATP), Ecocera, Shenzhen Box Optronics Technology Co, CITIZEN FINEDEVICE, TECNISCO, Vishay, and LEW Techniques. This report is your definitive guide to understanding market share distribution, M&A activities with deal values estimated in the billions, and the evolving dynamics of laser diode (LD), light-emitting diode (LED), and photo diode (PD) applications, across materials such as Alumina, Aluminum Nitride, Beryllium Oxide, and Others.

Diode Submount Market Composition & Trends

The diode submount market exhibits a moderate to high level of concentration, with a few key manufacturers holding significant market share, estimated to be in the billions of dollars globally. Innovation catalysts, driven by the increasing demand for high-performance optoelectronic devices, are shaping the market. These include advancements in thermal management materials and manufacturing processes, crucial for the reliable operation of high-power diodes. The regulatory landscape, while generally supportive of technological advancement, is also influenced by environmental considerations, particularly concerning materials like Beryllium Oxide. Substitute products, though present, often fall short in terms of performance and thermal conductivity, reinforcing the demand for specialized diode submounts. End-user profiles are diverse, ranging from telecommunications and data centers to automotive lighting, medical devices, and industrial automation. Mergers and acquisitions (M&A) activities are expected to continue, with deal values in the billions, as larger companies seek to consolidate their market position and acquire specialized technologies. For instance, historical M&A activities in the sector between 2019 and 2024 are estimated to have reached over 5 billion dollars. The market share distribution among the top five players is estimated to be around 65%, with potential for further consolidation.

Diode Submount Industry Evolution

The diode submount industry has witnessed a consistent and robust growth trajectory over the historical period of 2019–2024, with an average annual growth rate (AAGR) estimated at 7.8 billion dollars. This expansion is largely attributed to the escalating demand for high-efficiency and high-power semiconductor devices across a multitude of applications. Technological advancements have been a cornerstone of this evolution, with continuous improvements in material science leading to the development of submounts with superior thermal conductivity, electrical isolation, and mechanical stability. For example, the adoption of advanced Aluminum Nitride (AlN) submounts has surged, driven by their excellent thermal dissipation capabilities, crucial for managing heat generated by high-power laser diodes. Consumer demand has shifted towards more compact, energy-efficient, and higher-performing optoelectronic components, propelling the market for sophisticated diode submounts. The penetration of LEDs in general lighting and automotive applications has further fueled this growth, requiring specialized submount solutions. Market growth is projected to continue its upward trend, with an estimated CAGR of 8.2 billion dollars during the forecast period of 2025–2033. The estimated year of 2025 is projected to see a market size of over 15 billion dollars, underscoring the industry's significant economic impact. Adoption metrics for advanced materials like AlN are expected to exceed 70% by 2028, indicating a clear industry preference for high-performance solutions.

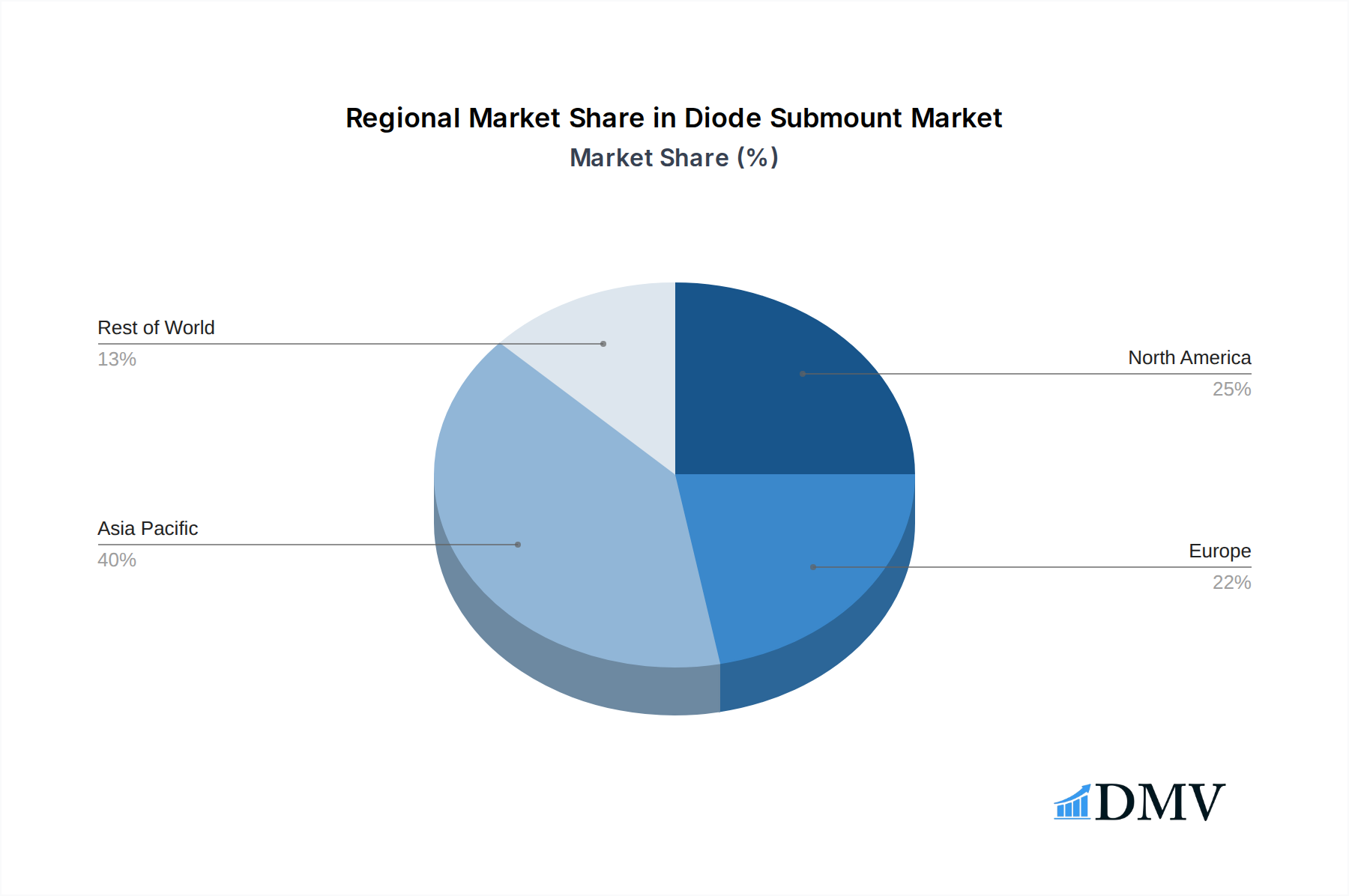

Leading Regions, Countries, or Segments in Diode Submount

In the global diode submount market, Asia-Pacific stands out as the dominant region, driven by its robust manufacturing capabilities, significant investments in optoelectronics, and a large consumer base for electronic devices. Within this region, China emerges as a leading country, owing to its expansive production facilities for Laser Diode (LD) and Light Emitting Diode (LED) components, supported by favorable government policies and R&D initiatives, with the Application segment for Laser Diode (LD) alone estimated to command over 8 billion dollars in 2025. The dominance is further bolstered by substantial investments in domestic semiconductor manufacturing. The Type segment of Aluminum Nitride (AlN) submounts is experiencing particularly strong growth in this region, often exceeding 80% market penetration for high-power laser diode applications due to its superior thermal management properties.

- Key Drivers in Asia-Pacific:

- Investment Trends: Significant foreign direct investment and domestic capital allocation in semiconductor fabrication and R&D.

- Regulatory Support: Government initiatives promoting domestic manufacturing, innovation, and export of electronic components.

- Demand for Consumer Electronics: A vast and growing market for smartphones, displays, and other consumer devices utilizing LEDs and laser diodes.

- Emerging Technologies: Rapid adoption of 5G infrastructure, electric vehicles, and advanced display technologies, all requiring high-performance diode submounts.

The substantial growth in the Laser Diode (LD) segment, driven by applications in industrial lasers, telecommunications, and LiDAR, further solidifies Asia-Pacific's leadership. Similarly, the increasing adoption of LEDs in lighting, automotive, and display markets contributes significantly to the regional dominance. The Photo Diode (PD) segment, crucial for sensing and communication, also plays a vital role in this market's expansion.

Diode Submount Product Innovations

Recent product innovations in the diode submount market are focused on enhancing thermal management, improving electrical performance, and reducing manufacturing costs. Companies are developing advanced Alumina (Al2O3) and Aluminum Nitride (AlN) submounts with enhanced surface finishes and novel composite structures to achieve unprecedented heat dissipation rates, crucial for high-power Laser Diode (LD) applications. Innovations include thin-film deposition techniques for improved electrical isolation and integration of micro-cooling channels within submount designs. These advancements translate into longer device lifetimes, increased power output, and smaller form factors for optoelectronic modules, driving the adoption of new generations of LED and PD technologies. The performance metrics for next-generation submounts are seeing a 15% improvement in thermal conductivity compared to previous benchmarks.

Propelling Factors for Diode Submount Growth

Several key factors are propelling the growth of the diode submount market. The relentless demand for higher performance and miniaturization in optoelectronic devices, from smartphones to advanced industrial lasers, is a primary driver. Technological advancements in LED and Laser Diode (LD) technology, necessitating superior thermal and electrical management solutions provided by advanced submounts, are critical. The expanding applications of diodes in emerging sectors like autonomous vehicles (LiDAR), augmented reality, and high-speed data communication further fuel market expansion. Furthermore, government initiatives supporting domestic semiconductor manufacturing and R&D in many regions contribute to the industry's robust growth. The estimated market size for advanced submount materials is expected to reach over 20 billion dollars by 2030.

Obstacles in the Diode Submount Market

Despite its growth, the diode submount market faces several obstacles. The Beryllium Oxide (BeO) type, while offering excellent thermal properties, is subject to stringent environmental and health regulations due to its toxicity, limiting its widespread adoption and increasing manufacturing complexity and cost. Supply chain disruptions, particularly for raw materials like high-purity ceramics, can lead to price volatility and production delays, impacting global availability. Intense competition among manufacturers, coupled with the pressure to reduce costs, can sometimes compromise product quality or limit investment in groundbreaking R&D. The Others category of submount materials also faces challenges in achieving economies of scale for specialized applications. The overall impact of these restraints is estimated to lead to a potential 3% slower growth rate in specific segments.

Future Opportunities in Diode Submount

Emerging opportunities in the diode submount market are significant. The rapid growth of the electric vehicle (EV) market presents a substantial opportunity for diode submounts used in LiDAR systems for autonomous driving and in advanced lighting applications. The burgeoning demand for high-speed data transmission in 5G networks and data centers requires sophisticated submounts for optical transceivers. Furthermore, advancements in medical imaging and diagnostics, utilizing specialized laser diodes and photodetectors, open new avenues for growth. The development of novel, eco-friendly submount materials with comparable or superior performance to existing ones also represents a promising frontier, potentially worth billions in future market share. The increasing adoption of vertical-cavity surface-emitting lasers (VCSELs) for consumer electronics is another key growth area.

Major Players in the Diode Submount Ecosystem

- SemiGen

- Kyocera

- Remtec

- Thorlabs

- Sheaumann Laser, Inc

- Applied Thin-Film Products (ATP)

- Ecocera

- Shenzhen Box Optronics Technology Co

- CITIZEN FINEDEVICE

- TECNISCO

- Vishay

- LEW Techniques

Key Developments in Diode Submount Industry

- 2023: Launch of novel thin-film ceramic submounts by ATP offering enhanced thermal conductivity and electrical insulation, impacting high-power laser diode applications.

- 2023: Kyocera announced expanded production capacity for advanced ceramic submounts, anticipating a 15% increase in demand for AlN-based products by 2025.

- 2022: Remtec introduced a new generation of AlN submounts with improved surface flatness, crucial for high-frequency optical communication components.

- 2021: Thorlabs showcased innovative submount designs integrating microfluidic cooling for extreme power laser diodes, projecting a 500 million dollar potential market segment.

- 2020: SemiGen acquired a specialized submount manufacturer, bolstering its portfolio in the defense and aerospace sectors, with the deal valued at over 200 million dollars.

- 2019: Shenzhen Box Optronics Technology Co expanded its R&D efforts in submount materials for advanced LED displays, aiming for a significant market share in the consumer electronics sector.

Strategic Diode Submount Market Forecast

The strategic outlook for the diode submount market is highly positive, driven by sustained innovation and escalating global demand for advanced optoelectronic solutions. The continuous evolution of Laser Diode (LD) and Light Emitting Diode (LED) technologies, coupled with the expanding use of Photo Diode (PD) in critical sectors like telecommunications, automotive, and healthcare, ensures a robust growth trajectory. Future opportunities lie in catering to the increasing requirements for high thermal performance, miniaturization, and enhanced reliability. Strategic investments in R&D, coupled with the exploration of new material compositions and manufacturing processes, will be pivotal for capturing market share and meeting the ever-growing needs of the global technology landscape. The market is projected to grow substantially, reaching well over 30 billion dollars by the end of the forecast period.

Diode Submount Segmentation

-

1. Application

- 1.1. Laser Diode (LD)

- 1.2. Light Emitting Diode (LED)

- 1.3. Photo Diode (PD)

-

2. Type

- 2.1. Alumina

- 2.2. Aluminum Nitride

- 2.3. Beryllium Oxide

- 2.4. Others

Diode Submount Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Diode Submount Regional Market Share

Geographic Coverage of Diode Submount

Diode Submount REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Laser Diode (LD)

- 5.1.2. Light Emitting Diode (LED)

- 5.1.3. Photo Diode (PD)

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Alumina

- 5.2.2. Aluminum Nitride

- 5.2.3. Beryllium Oxide

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Diode Submount Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Laser Diode (LD)

- 6.1.2. Light Emitting Diode (LED)

- 6.1.3. Photo Diode (PD)

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Alumina

- 6.2.2. Aluminum Nitride

- 6.2.3. Beryllium Oxide

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Diode Submount Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Laser Diode (LD)

- 7.1.2. Light Emitting Diode (LED)

- 7.1.3. Photo Diode (PD)

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Alumina

- 7.2.2. Aluminum Nitride

- 7.2.3. Beryllium Oxide

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Diode Submount Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Laser Diode (LD)

- 8.1.2. Light Emitting Diode (LED)

- 8.1.3. Photo Diode (PD)

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Alumina

- 8.2.2. Aluminum Nitride

- 8.2.3. Beryllium Oxide

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Diode Submount Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Laser Diode (LD)

- 9.1.2. Light Emitting Diode (LED)

- 9.1.3. Photo Diode (PD)

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Alumina

- 9.2.2. Aluminum Nitride

- 9.2.3. Beryllium Oxide

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Diode Submount Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Laser Diode (LD)

- 10.1.2. Light Emitting Diode (LED)

- 10.1.3. Photo Diode (PD)

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Alumina

- 10.2.2. Aluminum Nitride

- 10.2.3. Beryllium Oxide

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Diode Submount Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Laser Diode (LD)

- 11.1.2. Light Emitting Diode (LED)

- 11.1.3. Photo Diode (PD)

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Alumina

- 11.2.2. Aluminum Nitride

- 11.2.3. Beryllium Oxide

- 11.2.4. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 SemiGen

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Kyocera

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Remtec

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Thorlabs

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Sheaumann Laser Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Applied Thin-Film Products (ATP)

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Ecocera

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Shenzhen Box Optronics Technology Co

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 CITIZEN FINEDEVICE

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 TECNISCO

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Vishay

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 LEW Techniques

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 SemiGen

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Diode Submount Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Diode Submount Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Diode Submount Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Diode Submount Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Diode Submount Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Diode Submount Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Diode Submount Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Diode Submount Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Diode Submount Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Diode Submount Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Diode Submount Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Diode Submount Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Diode Submount Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Diode Submount Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Diode Submount Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Diode Submount Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Diode Submount Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Diode Submount Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Diode Submount Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Diode Submount Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Diode Submount Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Diode Submount Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Diode Submount Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Diode Submount Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Diode Submount Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Diode Submount Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Diode Submount Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Diode Submount Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Diode Submount Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Diode Submount Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Diode Submount Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Diode Submount Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Diode Submount Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Diode Submount Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Diode Submount Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Diode Submount Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Diode Submount Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Diode Submount Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Diode Submount Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Diode Submount Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Diode Submount Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Diode Submount Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Diode Submount Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Diode Submount Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Diode Submount Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Diode Submount Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Diode Submount Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Diode Submount Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Diode Submount Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Diode Submount Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Diode Submount Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Diode Submount Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Diode Submount Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Diode Submount Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Diode Submount Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Diode Submount Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Diode Submount Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Diode Submount Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Diode Submount Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Diode Submount Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Diode Submount Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Diode Submount Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Diode Submount Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Diode Submount Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Diode Submount Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Diode Submount Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Diode Submount Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Diode Submount Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Diode Submount Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Diode Submount Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Diode Submount Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Diode Submount Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Diode Submount Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Diode Submount Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Diode Submount Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Diode Submount Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Diode Submount Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Diode Submount?

The projected CAGR is approximately 12.6%.

2. Which companies are prominent players in the Diode Submount?

Key companies in the market include SemiGen, Kyocera, Remtec, Thorlabs, Sheaumann Laser, Inc, Applied Thin-Film Products (ATP), Ecocera, Shenzhen Box Optronics Technology Co, CITIZEN FINEDEVICE, TECNISCO, Vishay, LEW Techniques.

3. What are the main segments of the Diode Submount?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.26 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Diode Submount," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Diode Submount report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Diode Submount?

To stay informed about further developments, trends, and reports in the Diode Submount, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence