Key Insights

The D-Sub data connector market is poised for robust expansion, projected to reach an estimated USD 2.5 billion by 2025 and grow at a Compound Annual Growth Rate (CAGR) of 6.5% through 2033. This growth is propelled by the sustained demand from the Automotive Industry, driven by the increasing integration of advanced driver-assistance systems (ADAS) and infotainment features. The Electronic and Electrical Industry remains a significant consumer, benefiting from the widespread use of D-Sub connectors in consumer electronics, industrial automation, and telecommunications equipment. Furthermore, the Automation Industry's continuous evolution and the petrochemical sector's need for reliable connectivity in harsh environments are key growth accelerators. Emerging applications in specialized entertainment setups and other niche industries are also contributing to the market's upward trajectory, indicating a diversified and resilient demand base for these dependable connectors.

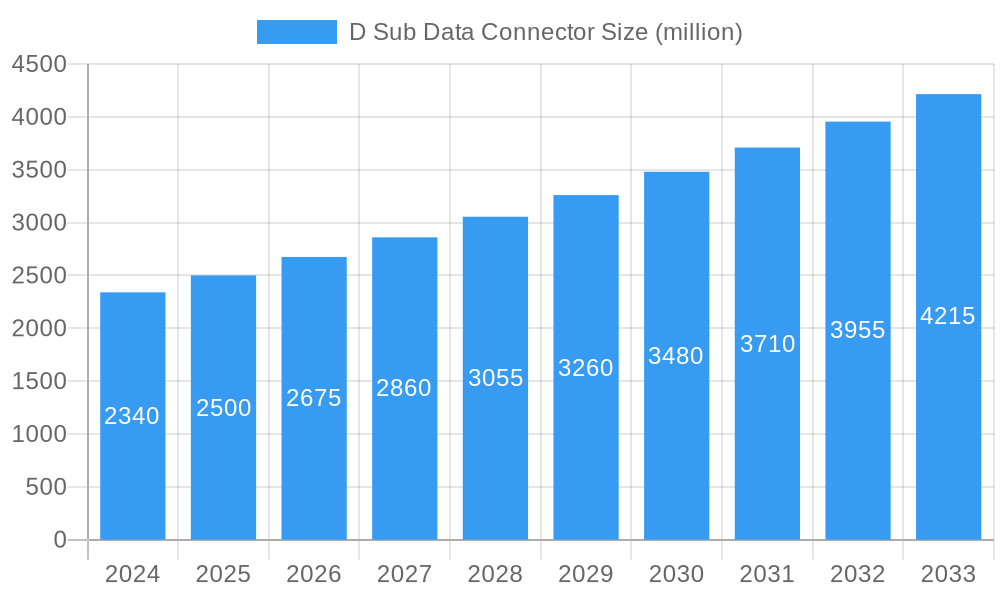

D Sub Data Connector Market Size (In Billion)

The market is characterized by a dynamic competitive landscape with prominent players like TE Connectivity, Souriau-Sunbank, and Murrelektronik vying for market share. Innovations in connector design, focusing on miniaturization, enhanced durability, and improved signal integrity, are shaping product development. The Plug-In and Push-Pull connector types are expected to dominate, catering to ease of use and secure connections. However, the market faces challenges related to the emergence of newer, higher-speed interconnect technologies and the potential obsolescence in certain cutting-edge applications. Despite these restraints, the established reliability, cost-effectiveness, and broad compatibility of D-Sub connectors ensure their continued relevance across a multitude of critical industrial and commercial applications, especially in regions with established manufacturing bases like North America and Europe.

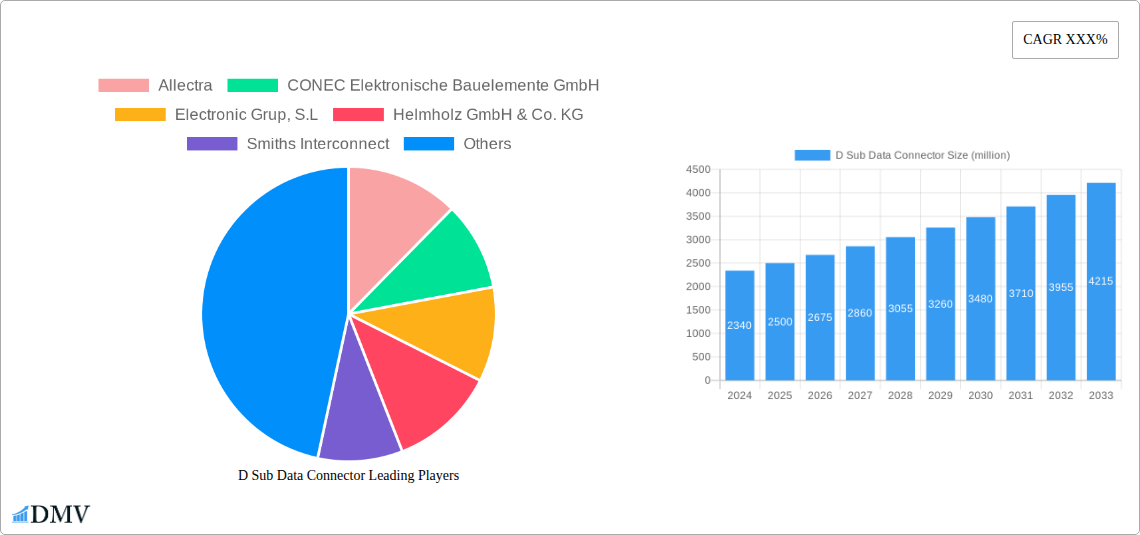

D Sub Data Connector Company Market Share

D Sub Data Connector Market Composition & Trends

The D-sub data connector market, valued at over $XXX million, exhibits a moderately concentrated landscape with key players like TE Connectivity, Souriau-Sunbank, and Smiths Interconnect holding substantial shares. Innovation is primarily driven by demands for higher bandwidth, miniaturization, and enhanced environmental resistance across diverse applications. The regulatory environment, particularly concerning electrical safety standards and material compliance (e.g., RoHS, REACH), significantly influences product development and market entry. Substitute products, such as USB-C and high-speed serial connectors, pose a growing challenge, particularly in consumer electronics, though D-sub connectors retain a strong foothold in industrial and legacy systems due to their robustness and cost-effectiveness. End-user profiles span the Automotive Industry, Electronic and Electrical Industry, Automation Industry, Petrochemical Industry, and Entertainment Industry, each with unique connectivity requirements. Mergers and acquisitions are strategically shaping the market, with recent deals valued at over $XXX million focused on expanding product portfolios and geographical reach.

- Market Share Distribution: Leading players collectively command over 60% of the market.

- M&A Deal Value: Over $XXX million in disclosed M&A transactions during the study period.

- Innovation Catalysts: Miniaturization, high-speed data transfer, and ruggedization.

- Regulatory Impact: Compliance with safety and environmental standards is paramount.

D Sub Data Connector Industry Evolution

The D-sub data connector industry has witnessed a steady evolutionary path driven by persistent technological advancements and evolving application demands. From its origins as a fundamental component for serial communication, the market has adapted to increasingly sophisticated requirements. The study period from 2019 to 2033 encompasses significant shifts. Historically, from 2019 to 2024, the market saw stable growth, bolstered by its entrenched position in industrial automation and legacy equipment. The base year of 2025 represents a pivot point, with an estimated market value exceeding $XXX million. This period is characterized by a growing emphasis on higher data transmission rates and improved signal integrity, prompting manufacturers to enhance connector designs. The forecast period of 2025–2033 anticipates continued expansion, albeit at a more measured pace compared to disruptive newer technologies. This growth is underpinned by the inherent reliability and cost-effectiveness of D-sub connectors, making them indispensable in sectors where durability and proven performance are critical. Technological advancements have focused on material science for enhanced durability and thermal management, as well as improved pin configurations for denser I/O solutions. Consumer demands, while less directly impactful on the core industrial D-sub market, indirectly influence it through the need for interoperability and backward compatibility with older systems. Adoption metrics for newer D-sub variants, such as those with higher pin densities and specialized shielding, are showing a positive upward trend, indicating a sustained relevance. The industry's ability to integrate new features while maintaining its core strengths will be crucial for sustained market relevance.

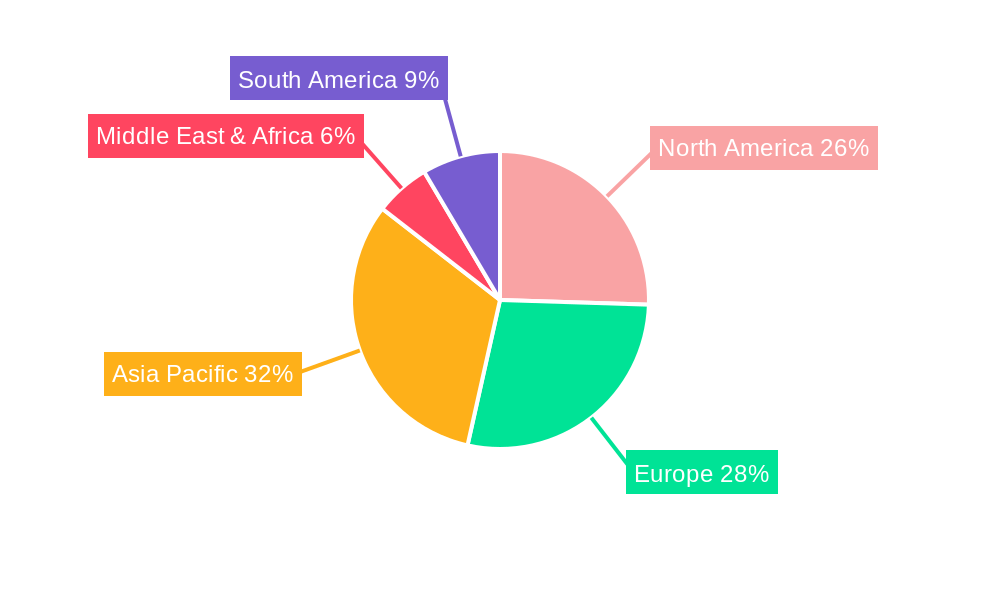

Leading Regions, Countries, or Segments in D Sub Data Connector

The Automation Industry stands out as a dominant segment within the global D-sub data connector market, driven by a confluence of factors that underscore its critical role in modern industrial infrastructure. This dominance is projected to continue throughout the forecast period, with an estimated market contribution exceeding $XXX million in the base year of 2025. The robustness, reliability, and cost-effectiveness of D-sub connectors make them the preferred choice for a wide array of automation applications, from programmable logic controllers (PLCs) and human-machine interfaces (HMIs) to industrial networking and control systems. The Electronic and Electrical Industry follows closely, leveraging D-sub connectors for internal component interconnections and power delivery where stringent reliability is non-negotiable.

Key drivers underpinning the Automation Industry's leadership include:

- Investment Trends: Significant global investments in factory automation, smart manufacturing, and Industry 4.0 initiatives are directly fueling the demand for dependable connectivity solutions like D-sub connectors. Countries with strong manufacturing bases and advanced industrial sectors, such as Germany, China, and the United States, are at the forefront of this investment.

- Regulatory Support: While not specific to D-subs, overall industrial automation standards and safety regulations necessitate highly reliable and certified interconnect components, a niche where D-sub connectors excel.

- Legacy System Integration: A vast installed base of existing automation equipment relies on D-sub connectors, necessitating their continued production and integration into newer systems for backward compatibility. This inertia provides a stable demand.

- Performance Metrics: D-sub connectors offer a proven track record of durability in harsh industrial environments, including resistance to vibration, shock, and temperature fluctuations, crucial for uninterrupted operation in manufacturing settings.

In terms of Type, Plug-In connectors represent the largest sub-segment within the D-sub market, particularly within the Automation and Electronic & Electrical industries. Their ease of installation and disconnection simplifies maintenance and system reconfiguration. The Automotive Industry also presents a significant application area, with D-sub connectors finding use in diagnostic ports and certain in-vehicle electronic systems where robust and secure connections are paramount. While newer connector technologies are emerging, the long-standing integration and proven reliability of D-sub connectors ensure their sustained importance across these vital industrial sectors.

D Sub Data Connector Product Innovations

Product innovations in the D-sub data connector market are primarily focused on enhancing performance and expanding application suitability. Advancements include the development of higher-density pin configurations, improved shielding for superior electromagnetic interference (EMI) resistance, and the integration of new materials for enhanced durability and corrosion resistance. Some manufacturers are also introducing specialized D-sub variants with integrated circuitry or enhanced sealing for extreme environmental conditions. These innovations aim to maintain D-sub connectors' relevance in demanding applications within the Automotive Industry, Automation Industry, and specialized sectors of the Electronic and Electrical Industry, offering reliable, high-performance connectivity solutions.

Propelling Factors for D Sub Data Connector Growth

The D-sub data connector market's growth is propelled by several key factors. Foremost is the sustained demand from the Automation Industry, driven by ongoing investments in smart manufacturing and Industry 4.0, requiring robust and reliable interconnects. The Electronic and Electrical Industry continues to rely on D-sub connectors for their proven performance in power and data transmission applications. Furthermore, the Automotive Industry utilizes these connectors for diagnostic purposes and in certain electronic control units, benefiting from their ruggedness. Technological advancements, while often introducing alternatives, also spur innovation within the D-sub segment, leading to improved versions with higher bandwidth and better signal integrity. The cost-effectiveness and established reliability of D-sub connectors ensure their continued adoption in applications where failure is not an option.

Obstacles in the D Sub Data Connector Market

The D-sub data connector market faces several significant obstacles. Intense competition from newer, high-speed interconnect technologies like USB-C and Thunderbolt poses a substantial threat, particularly in consumer-facing and rapidly evolving electronics segments. Stringent regulatory compliance, including RoHS and REACH directives, adds complexity and cost to manufacturing processes, especially for global supply chains. Supply chain disruptions, as experienced in recent years, can impact raw material availability and lead times, affecting production schedules and pricing. Furthermore, the perceived "legacy" status of D-sub connectors can deter adoption in cutting-edge applications where the latest technological advancements are prioritized.

Future Opportunities in D Sub Data Connector

Emerging opportunities for D-sub data connectors lie in their continued application within specialized industrial environments and niche markets. The growing adoption of the Internet of Things (IoT) in industrial settings presents opportunities for ruggedized D-sub connectors that can withstand harsh conditions and provide reliable data transmission. Developments in electric vehicles (EVs) and advanced driver-assistance systems (ADAS) may also present avenues for specialized D-sub connectors where robustness and EMI shielding are critical. Furthermore, the ongoing need for backward compatibility in legacy systems across various industries ensures a sustained, albeit slower, demand for traditional D-sub connectors. The market can also capitalize on opportunities by developing variants with enhanced environmental sealing and higher pin densities to meet evolving industrial demands.

Major Players in the D Sub Data Connector Ecosystem

- Allectra

- CONEC Elektronische Bauelemente GmbH

- Electronic Grup, S.L

- Helmholz GmbH & Co. KG

- Smiths Interconnect

- Souriau-Sunbank

- TE Connectivity

- Murrelektronik

- U.I. Lapp GmbH

- Dongguan Lianda Precision Products Co. Ltd

- Fischer Elektronik GmbH & Co. KG

- Beijer Electronics

- Douglas Electrical Components

- ERNI Electronics

- GIMATIC

- GLENAIR

- Igus

- ILME

- Japan Aviation Electronics Industries

- PHG

- Wieland Electric

Key Developments in D Sub Data Connector Industry

- 2023: Launch of ruggedized D-sub connectors with enhanced IP ratings for industrial automation by Murrelektronik.

- 2023: Smiths Interconnect announces expansion of their D-sub connector manufacturing capabilities to meet increased global demand.

- 2022: TE Connectivity introduces new high-density D-sub connectors for advanced telecommunications equipment.

- 2022: CONEC Elektronische Bauelemente GmbH acquires a specialized connector manufacturer to broaden its product portfolio.

- 2021: Souriau-Sunbank releases a new series of D-sub connectors with improved EMI shielding for aerospace applications.

- 2020: ILME unveils innovative quick-release mechanisms for D-sub connectors in industrial control panels.

- 2019: GLENAIR acquires a company specializing in custom connector solutions, enhancing their D-sub offerings.

Strategic D Sub Data Connector Market Forecast

The strategic forecast for the D-sub data connector market indicates continued resilience, driven by the indispensable role of these connectors in industrial automation, electronic and electrical systems, and the automotive sector. Growth catalysts include ongoing investments in Industry 4.0, the need for reliable connectivity in harsh environments, and the significant installed base of legacy systems requiring backward compatibility. While facing competition from newer technologies, the market's ability to innovate with higher pin densities and improved environmental resistance will be crucial. Opportunities in specialized applications and the sustained demand from core industrial segments are expected to ensure a stable, albeit moderate, growth trajectory throughout the forecast period, projecting a market value of over $XXX million by 2033.

D Sub Data Connector Segmentation

-

1. Application

- 1.1. Automotive Industry

- 1.2. Electronic and Electrical Industry

- 1.3. Automation Industry

- 1.4. Petrochemical Industry

- 1.5. Entertainment Industry

- 1.6. Other Industries

-

2. Type

- 2.1. Plug-In

- 2.2. Push-Pull

- 2.3. Bayonet

- 2.4. Crimp

- 2.5. Others

D Sub Data Connector Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

D Sub Data Connector Regional Market Share

Geographic Coverage of D Sub Data Connector

D Sub Data Connector REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XXX% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Automotive Industry

- 5.1.2. Electronic and Electrical Industry

- 5.1.3. Automation Industry

- 5.1.4. Petrochemical Industry

- 5.1.5. Entertainment Industry

- 5.1.6. Other Industries

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Plug-In

- 5.2.2. Push-Pull

- 5.2.3. Bayonet

- 5.2.4. Crimp

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global D Sub Data Connector Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Automotive Industry

- 6.1.2. Electronic and Electrical Industry

- 6.1.3. Automation Industry

- 6.1.4. Petrochemical Industry

- 6.1.5. Entertainment Industry

- 6.1.6. Other Industries

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Plug-In

- 6.2.2. Push-Pull

- 6.2.3. Bayonet

- 6.2.4. Crimp

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America D Sub Data Connector Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Automotive Industry

- 7.1.2. Electronic and Electrical Industry

- 7.1.3. Automation Industry

- 7.1.4. Petrochemical Industry

- 7.1.5. Entertainment Industry

- 7.1.6. Other Industries

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Plug-In

- 7.2.2. Push-Pull

- 7.2.3. Bayonet

- 7.2.4. Crimp

- 7.2.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America D Sub Data Connector Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Automotive Industry

- 8.1.2. Electronic and Electrical Industry

- 8.1.3. Automation Industry

- 8.1.4. Petrochemical Industry

- 8.1.5. Entertainment Industry

- 8.1.6. Other Industries

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Plug-In

- 8.2.2. Push-Pull

- 8.2.3. Bayonet

- 8.2.4. Crimp

- 8.2.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe D Sub Data Connector Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Automotive Industry

- 9.1.2. Electronic and Electrical Industry

- 9.1.3. Automation Industry

- 9.1.4. Petrochemical Industry

- 9.1.5. Entertainment Industry

- 9.1.6. Other Industries

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Plug-In

- 9.2.2. Push-Pull

- 9.2.3. Bayonet

- 9.2.4. Crimp

- 9.2.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa D Sub Data Connector Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Automotive Industry

- 10.1.2. Electronic and Electrical Industry

- 10.1.3. Automation Industry

- 10.1.4. Petrochemical Industry

- 10.1.5. Entertainment Industry

- 10.1.6. Other Industries

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Plug-In

- 10.2.2. Push-Pull

- 10.2.3. Bayonet

- 10.2.4. Crimp

- 10.2.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific D Sub Data Connector Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Automotive Industry

- 11.1.2. Electronic and Electrical Industry

- 11.1.3. Automation Industry

- 11.1.4. Petrochemical Industry

- 11.1.5. Entertainment Industry

- 11.1.6. Other Industries

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Plug-In

- 11.2.2. Push-Pull

- 11.2.3. Bayonet

- 11.2.4. Crimp

- 11.2.5. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Allectra

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 CONEC Elektronische Bauelemente GmbH

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Electronic Grup S.L

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Helmholz GmbH & Co. KG

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Smiths Interconnect

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Souriau-Sunbank

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 TE Connectivity

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Murrelektronik

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 U.I. Lapp GmbH

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Dongguan Lianda Precision Products Co. Ltd

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Fischer Elektronik GmbH & Co. KG

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Beijer Electronics

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Douglas Electrical Components

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 ERNI Electronics

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 GIMATIC

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 GLENAIR

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Igus

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 ILME

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 Japan Aviation Electronics Industries

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.20 PHG

- 12.1.20.1. Company Overview

- 12.1.20.2. Products

- 12.1.20.3. Company Financials

- 12.1.20.4. SWOT Analysis

- 12.1.21 Wieland Electric

- 12.1.21.1. Company Overview

- 12.1.21.2. Products

- 12.1.21.3. Company Financials

- 12.1.21.4. SWOT Analysis

- 12.1.1 Allectra

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global D Sub Data Connector Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America D Sub Data Connector Revenue (million), by Application 2025 & 2033

- Figure 3: North America D Sub Data Connector Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America D Sub Data Connector Revenue (million), by Type 2025 & 2033

- Figure 5: North America D Sub Data Connector Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America D Sub Data Connector Revenue (million), by Country 2025 & 2033

- Figure 7: North America D Sub Data Connector Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America D Sub Data Connector Revenue (million), by Application 2025 & 2033

- Figure 9: South America D Sub Data Connector Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America D Sub Data Connector Revenue (million), by Type 2025 & 2033

- Figure 11: South America D Sub Data Connector Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America D Sub Data Connector Revenue (million), by Country 2025 & 2033

- Figure 13: South America D Sub Data Connector Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe D Sub Data Connector Revenue (million), by Application 2025 & 2033

- Figure 15: Europe D Sub Data Connector Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe D Sub Data Connector Revenue (million), by Type 2025 & 2033

- Figure 17: Europe D Sub Data Connector Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe D Sub Data Connector Revenue (million), by Country 2025 & 2033

- Figure 19: Europe D Sub Data Connector Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa D Sub Data Connector Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa D Sub Data Connector Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa D Sub Data Connector Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa D Sub Data Connector Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa D Sub Data Connector Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa D Sub Data Connector Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific D Sub Data Connector Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific D Sub Data Connector Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific D Sub Data Connector Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific D Sub Data Connector Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific D Sub Data Connector Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific D Sub Data Connector Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global D Sub Data Connector Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global D Sub Data Connector Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global D Sub Data Connector Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global D Sub Data Connector Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global D Sub Data Connector Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global D Sub Data Connector Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States D Sub Data Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada D Sub Data Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico D Sub Data Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global D Sub Data Connector Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global D Sub Data Connector Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global D Sub Data Connector Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil D Sub Data Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina D Sub Data Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America D Sub Data Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global D Sub Data Connector Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global D Sub Data Connector Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global D Sub Data Connector Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom D Sub Data Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany D Sub Data Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France D Sub Data Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy D Sub Data Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain D Sub Data Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia D Sub Data Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux D Sub Data Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics D Sub Data Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe D Sub Data Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global D Sub Data Connector Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global D Sub Data Connector Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global D Sub Data Connector Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey D Sub Data Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel D Sub Data Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC D Sub Data Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa D Sub Data Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa D Sub Data Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa D Sub Data Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global D Sub Data Connector Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global D Sub Data Connector Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global D Sub Data Connector Revenue million Forecast, by Country 2020 & 2033

- Table 40: China D Sub Data Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India D Sub Data Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan D Sub Data Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea D Sub Data Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN D Sub Data Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania D Sub Data Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific D Sub Data Connector Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the D Sub Data Connector?

The projected CAGR is approximately XXX%.

2. Which companies are prominent players in the D Sub Data Connector?

Key companies in the market include Allectra, CONEC Elektronische Bauelemente GmbH, Electronic Grup, S.L, Helmholz GmbH & Co. KG, Smiths Interconnect, Souriau-Sunbank, TE Connectivity, Murrelektronik, U.I. Lapp GmbH, Dongguan Lianda Precision Products Co. Ltd, Fischer Elektronik GmbH & Co. KG, Beijer Electronics, Douglas Electrical Components, ERNI Electronics, GIMATIC, GLENAIR, Igus, ILME, Japan Aviation Electronics Industries, PHG, Wieland Electric.

3. What are the main segments of the D Sub Data Connector?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "D Sub Data Connector," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the D Sub Data Connector report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the D Sub Data Connector?

To stay informed about further developments, trends, and reports in the D Sub Data Connector, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence