Key Insights

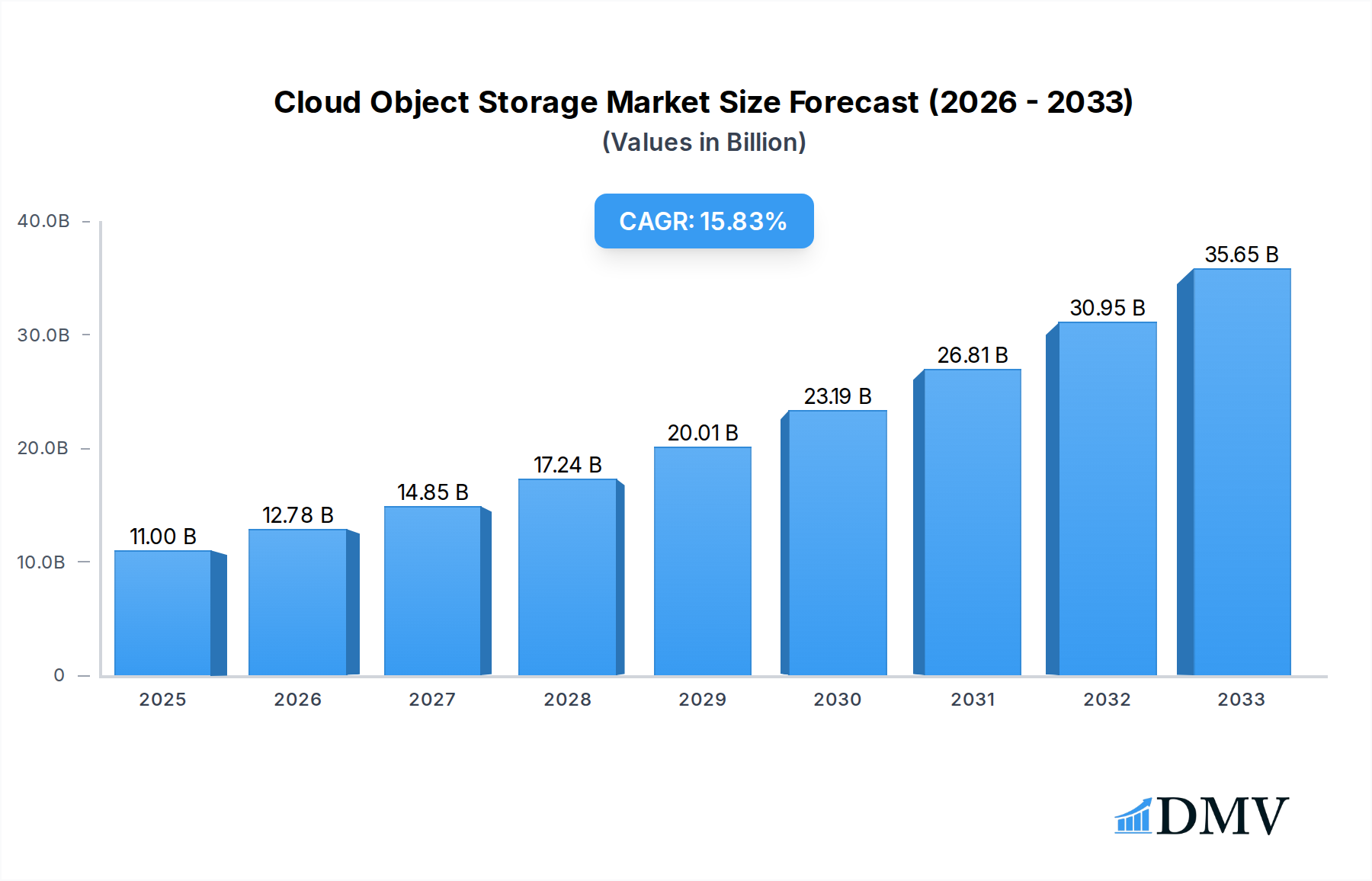

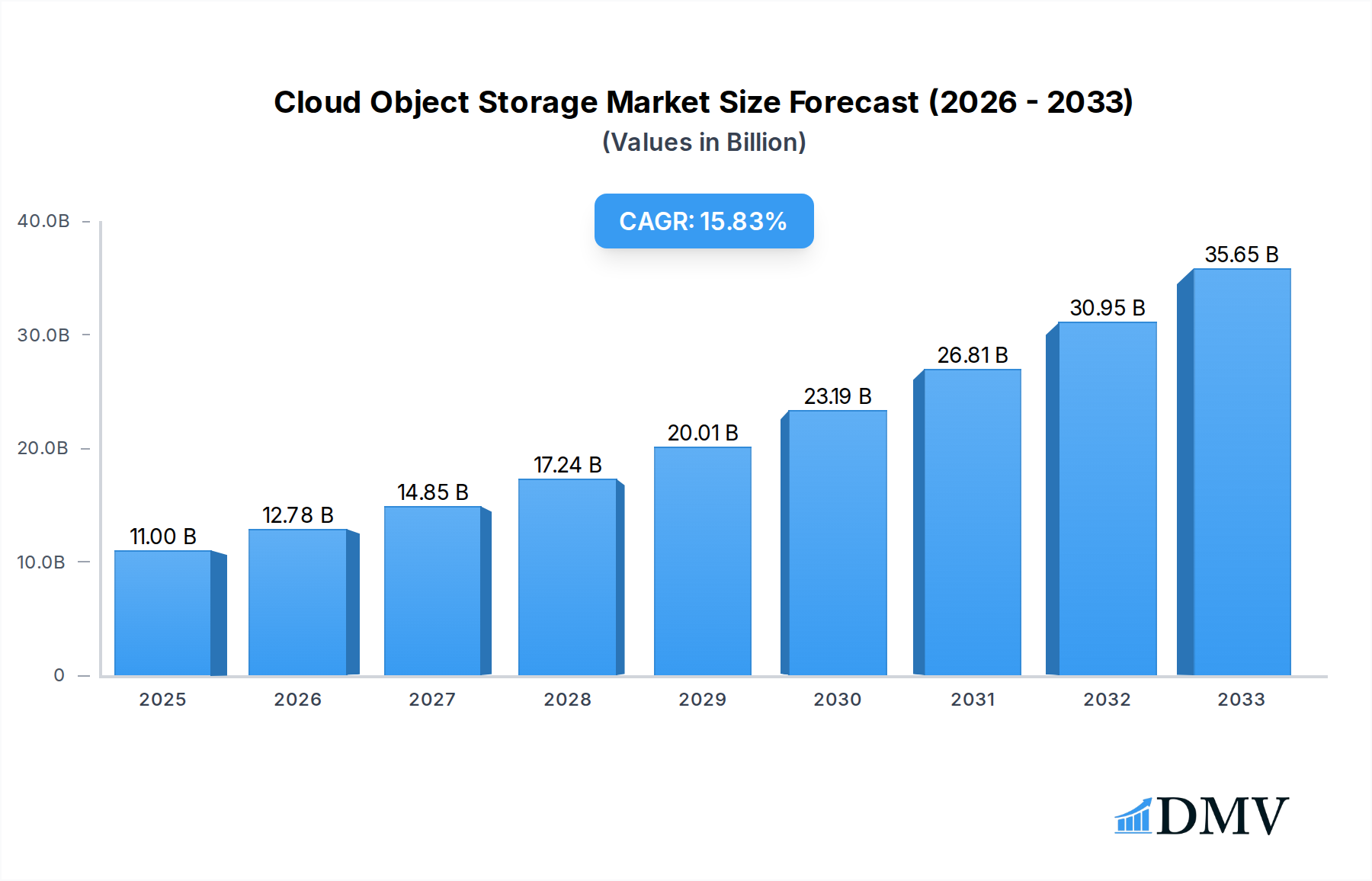

The global Cloud Object Storage market is poised for significant expansion, projected to reach an estimated $11 billion by 2025. This robust growth is fueled by a CAGR of 16.2%, indicating a rapid adoption trajectory that will continue through the forecast period ending in 2033. The burgeoning volume of unstructured data generated by diverse applications, particularly in social media platforms, IT and telecommunication, and the BFSI sector, is a primary catalyst. Organizations are increasingly recognizing the scalability, durability, and cost-effectiveness of object storage solutions for managing these vast datasets. The transition towards hybrid and public cloud deployments further amplifies demand as businesses seek flexible and resilient data management strategies.

Cloud Object Storage Market Size (In Billion)

The market's upward momentum is further supported by emerging trends such as the growing adoption of AI and machine learning, which rely heavily on readily accessible and scalable data repositories. Innovations in data deduplication, compression, and automated tiering are also contributing to the market's expansion by optimizing storage efficiency and reducing operational costs. While the market demonstrates strong growth, potential restraints may include data security concerns and vendor lock-in, though these are being mitigated by advancements in encryption and interoperability standards. Key players like IBM, Microsoft Corporation, and Google are at the forefront, driving innovation and expanding the market's reach across all major regions.

Cloud Object Storage Company Market Share

Comprehensive Cloud Object Storage Market Analysis: Trends, Growth, and Future Outlook (2019-2033)

This in-depth report provides a definitive analysis of the global Cloud Object Storage market, covering historical trends, current dynamics, and future projections. Delve into market composition, industry evolution, regional dominance, product innovations, growth drivers, obstacles, and emerging opportunities. Essential for stakeholders in IT and Telecommunication, BFSI, Social Media Platforms, and other sectors, this report equips you with critical insights to navigate the burgeoning cloud object storage landscape, projected to reach billions in value by 2033.

Cloud Object Storage Market Composition & Trends

The Cloud Object Storage market exhibits a dynamic composition characterized by significant innovation catalysts and evolving regulatory landscapes. Market concentration is influenced by the strategic plays of industry giants like Microsoft Corporation, Google, and IBM, alongside specialized providers such as Caringo Inc. and Datadirect Networks. The market share distribution is a complex interplay of established players and agile newcomers, with International Data Corporation (IDC) reporting significant investments in cloud infrastructure. Regulatory frameworks are increasingly shaping data governance and privacy, impacting adoption rates across various segments, particularly BFSI. Substitute products, such as traditional file storage and block storage, are gradually being superseded by the scalability and cost-effectiveness of object storage solutions, especially for unstructured data. End-user profiles are expanding beyond core IT, encompassing social media platforms demanding vast storage for user-generated content and the burgeoning Internet of Things (IoT) ecosystem. Mergers and acquisitions (M&A) activities are a key trend, with reported deal values in the billions, as companies like Dell, Hewlett-Packard Enterprise (HPE), and NetApp, Inc. strategically consolidate their cloud offerings and expand their market reach. Hitachi Data Systems and Iron Mountain are also key players in this consolidating environment. The market is ripe with opportunities for innovative solutions that address the ever-growing demand for accessible, scalable, and cost-efficient data storage.

Cloud Object Storage Industry Evolution

The Cloud Object Storage industry has witnessed a remarkable evolution driven by relentless technological advancements and a fundamental shift in consumer demands for data management. From its inception, the market has been on a steep growth trajectory, with historical growth rates consistently exceeding billions in expansion. The study period from 2019 to 2024 laid a strong foundation, with the base year of 2025 marking a significant inflection point for accelerated adoption. This evolution is intrinsically linked to the proliferation of unstructured data, fueled by the explosive growth of digital content from social media, streaming services, and an increasingly connected world. The adoption of cloud-native architectures and the rise of big data analytics have further propelled the demand for object storage's inherent scalability, durability, and cost-effectiveness compared to traditional storage paradigms.

Technological advancements have been central to this transformation. Innovations in distributed systems, erasure coding for enhanced data protection, and the development of highly efficient API interfaces have made object storage more accessible and performant. Furthermore, the integration of object storage with other cloud services, such as AI/ML platforms and data analytics tools, has unlocked new use cases and increased its value proposition. Cloud providers have continuously invested in expanding their object storage capacity and improving their service offerings, leading to a highly competitive market.

Shifting consumer demands have also played a pivotal role. Businesses are increasingly prioritizing agility, cost optimization, and the ability to easily access and analyze vast datasets. Object storage's pay-as-you-go model, its ability to handle petabytes of data with ease, and its inherent durability have made it an attractive solution for a wide range of applications, from backup and archiving to content delivery and big data analytics. The forecast period from 2025 to 2033 is expected to witness sustained high growth, with projected market expansion reaching billions, driven by the continued digital transformation initiatives across industries and the ongoing explosion of data creation. Companies like Elastifile and OSNEXUS are contributing to this evolution with specialized solutions.

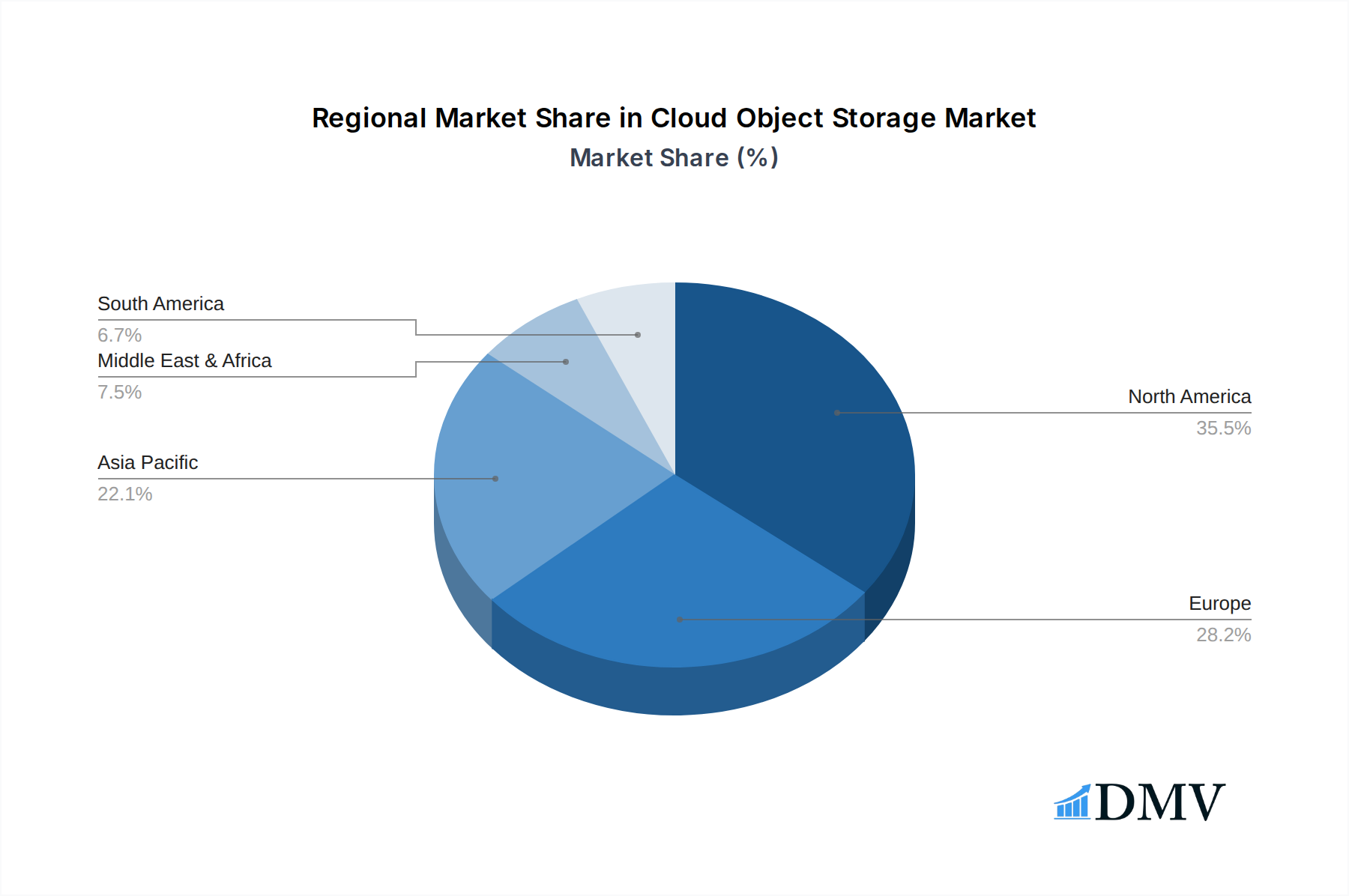

Leading Regions, Countries, or Segments in Cloud Object Storage

The dominance within the Cloud Object Storage market is multifaceted, with North America emerging as a leading region due to substantial investments in cloud infrastructure and a mature technology adoption ecosystem. Within North America, the United States spearheads growth, driven by its thriving technology sector, a high concentration of BFSI institutions, and a significant presence of major cloud providers like Google and Microsoft Corporation.

Application Segments Driving Dominance:

- IT and Telecommunication: This segment represents a cornerstone of cloud object storage adoption. The constant need for storing and managing vast amounts of network data, logs, and customer information makes object storage indispensable. Investment trends show a continuous upgrade of core infrastructure to accommodate the escalating data volumes generated by 5G rollouts and the expansion of digital services. Regulatory support for data localization and security in this sector further bolsters the demand for robust cloud object storage solutions.

- BFSI (Banking, Financial Services, and Insurance): This segment exhibits a strong preference for hybrid cloud and private cloud object storage solutions due to stringent regulatory compliance requirements and the critical need for data security and integrity. Investment trends are geared towards advanced security features, disaster recovery capabilities, and long-term archiving of financial records, often involving values in the billions for infrastructure upgrades. Regulatory support for data retention and privacy laws, such as GDPR and CCPA, significantly influences their adoption strategies.

- Social Media Platforms: These platforms are massive consumers of cloud object storage, requiring highly scalable and cost-effective solutions to manage billions of user-generated photos, videos, and text data. The sheer volume of data necessitates public cloud solutions for their unparalleled elasticity and global reach. Investment trends are focused on optimizing storage costs and improving content delivery speeds to billions of users worldwide.

- Others: This broad category includes industries like media and entertainment, healthcare, and the public sector, all experiencing significant growth in data generation and a corresponding reliance on cloud object storage for archival, backup, and analytics.

Types of Cloud Object Storage Contributing to Dominance:

- Public Cloud: Dominates due to its inherent scalability, cost-effectiveness, and ease of deployment, particularly favored by social media platforms and burgeoning enterprises. Investment trends in public cloud infrastructure by major providers continue to expand capacity and enhance service offerings.

- Hybrid Cloud: Increasingly adopted by BFSI and IT/Telecommunication sectors seeking a balance between the scalability of public cloud and the control and security of private cloud. Investment trends are focused on seamless integration and data mobility between on-premises and cloud environments.

- Private Cloud: Preferred by organizations with highly sensitive data or strict regulatory compliance needs. Investment trends are directed towards enhancing security features, performance, and management capabilities of on-premises object storage solutions.

Cloud Object Storage Product Innovations

Cloud Object Storage product innovation is rapidly advancing, focusing on enhancing scalability, durability, and cost-efficiency for massive unstructured data. Companies are actively developing solutions with enhanced data tiering capabilities, automatically moving less frequently accessed data to lower-cost storage tiers, optimizing operational expenditures in the billions. Performance metrics are being pushed with advancements in low-latency access for active data and the integration of NVMe technologies. Unique selling propositions include immutable storage options for enhanced data security and ransomware protection, advanced data deduplication and compression techniques to reduce storage footprints, and simplified API integrations for seamless application development. Furthermore, the development of distributed object storage systems that can span multiple data centers and regions is a key technological advancement, offering unparalleled resilience and availability for mission-critical applications.

Propelling Factors for Cloud Object Storage Growth

The growth of the Cloud Object Storage market is propelled by several key factors. The exponential increase in unstructured data generation from sources like IoT devices, social media, and video streaming services is a primary driver, creating an insatiable demand for scalable and cost-effective storage solutions. Technological advancements, including improved data compression algorithms, enhanced durability features like erasure coding, and more efficient data retrieval mechanisms, continue to make object storage increasingly attractive. Economically, the pay-as-you-go pricing models offered by cloud providers significantly reduce upfront capital expenditure and allow organizations to scale their storage capacity as needed, leading to substantial cost savings in the billions. Regulatory compliance mandates around data retention and privacy are also compelling organizations to adopt robust and compliant storage solutions.

Obstacles in the Cloud Object Storage Market

Despite its rapid growth, the Cloud Object Storage market faces several obstacles. Security concerns and the perception of increased vulnerability in shared cloud environments can be a deterrent for some organizations, particularly those handling highly sensitive data. The complexity of migrating massive datasets from legacy storage systems to cloud object storage can be technically challenging and resource-intensive, leading to potential project delays and cost overruns. Furthermore, vendor lock-in concerns, where migrating data between different cloud object storage providers can be difficult and expensive, can hinder adoption. Evolving regulatory landscapes and data sovereignty requirements across different geographies can also present compliance challenges. Interoperability issues between different object storage APIs and formats can also create integration hurdles.

Future Opportunities in Cloud Object Storage

The future of Cloud Object Storage is bright with numerous emerging opportunities. The continued growth of AI and Machine Learning workloads will drive demand for object storage as a primary repository for vast datasets used in training and inference. The expansion of edge computing will create new opportunities for distributed object storage solutions that can manage data closer to the source. The increasing adoption of blockchain technology may also present opportunities for immutable and highly secure data storage solutions. Furthermore, the convergence of object storage with data analytics platforms will enable new use cases for real-time data processing and insights, unlocking further value for businesses across all sectors.

Major Players in the Cloud Object Storage Ecosystem

- IBM

- Dell

- Hewlett-Packard Enterprise

- Hitachi Data Systems

- Caringo Inc.

- Datadirect Networks

- International Data Corporation

- Netapp, Inc.

- Microsoft Corporation

- Elastifile

- OSNEXUS

- Iron Mountain

Key Developments in Cloud Object Storage Industry

- 2024: Increased adoption of S3-compatible APIs as a de facto standard, fostering interoperability across different object storage solutions.

- 2023: Significant advancements in erasure coding techniques, reducing storage overhead and improving data durability, leading to cost savings in the billions.

- 2023: Growing focus on immutable object storage for enhanced ransomware protection and data security compliance.

- 2022: Expansion of AI/ML specific object storage solutions to cater to the growing demand for data lakes.

- 2021: Strategic acquisitions by major cloud providers to bolster their object storage portfolios and expand market reach.

- 2020: Introduction of advanced data tiering capabilities, enabling automated cost optimization for long-term archival.

- 2019: Increased adoption of hybrid cloud object storage solutions by enterprises for greater flexibility and control.

Strategic Cloud Object Storage Market Forecast

The strategic outlook for the Cloud Object Storage market is overwhelmingly positive, with continued expansion projected to reach hundreds of billions by 2033. Key growth catalysts include the persistent surge in unstructured data, the accelerating adoption of cloud-native applications, and the indispensable role of object storage in supporting AI/ML workloads. Emerging opportunities in edge computing and the integration with blockchain technology further underscore the market's potential. While challenges related to security and data migration persist, ongoing innovation in data protection, cost optimization, and interoperability will pave the way for sustained growth and market leadership for well-positioned players.

Cloud Object Storage Segmentation

-

1. Application

- 1.1. Social Media Platforms

- 1.2. IT and Telecommunication

- 1.3. BFSI

- 1.4. Others

-

2. Types

- 2.1. Public Cloud

- 2.2. Hybrid Cloud

- 2.3. Private Cloud

Cloud Object Storage Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Cloud Object Storage Regional Market Share

Geographic Coverage of Cloud Object Storage

Cloud Object Storage REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 16.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Social Media Platforms

- 5.1.2. IT and Telecommunication

- 5.1.3. BFSI

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Public Cloud

- 5.2.2. Hybrid Cloud

- 5.2.3. Private Cloud

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Cloud Object Storage Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Social Media Platforms

- 6.1.2. IT and Telecommunication

- 6.1.3. BFSI

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Public Cloud

- 6.2.2. Hybrid Cloud

- 6.2.3. Private Cloud

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Cloud Object Storage Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Social Media Platforms

- 7.1.2. IT and Telecommunication

- 7.1.3. BFSI

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Public Cloud

- 7.2.2. Hybrid Cloud

- 7.2.3. Private Cloud

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Cloud Object Storage Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Social Media Platforms

- 8.1.2. IT and Telecommunication

- 8.1.3. BFSI

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Public Cloud

- 8.2.2. Hybrid Cloud

- 8.2.3. Private Cloud

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Cloud Object Storage Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Social Media Platforms

- 9.1.2. IT and Telecommunication

- 9.1.3. BFSI

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Public Cloud

- 9.2.2. Hybrid Cloud

- 9.2.3. Private Cloud

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Cloud Object Storage Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Social Media Platforms

- 10.1.2. IT and Telecommunication

- 10.1.3. BFSI

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Public Cloud

- 10.2.2. Hybrid Cloud

- 10.2.3. Private Cloud

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Cloud Object Storage Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Social Media Platforms

- 11.1.2. IT and Telecommunication

- 11.1.3. BFSI

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Public Cloud

- 11.2.2. Hybrid Cloud

- 11.2.3. Private Cloud

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 IBM

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Dell

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Hewlett-Packard Enterprise

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Hitachi Data Systems

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Caringo Inc.

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Datadirect Networks

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 International Data Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Netapp

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Inc.

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Microsoft Corporation

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Google

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Elastifile

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 OSNEXUS

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Iron Mountain

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 IBM

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Cloud Object Storage Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Cloud Object Storage Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Cloud Object Storage Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Cloud Object Storage Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Cloud Object Storage Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Cloud Object Storage Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Cloud Object Storage Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Cloud Object Storage Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Cloud Object Storage Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Cloud Object Storage Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Cloud Object Storage Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Cloud Object Storage Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Cloud Object Storage Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Cloud Object Storage Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Cloud Object Storage Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Cloud Object Storage Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Cloud Object Storage Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Cloud Object Storage Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Cloud Object Storage Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Cloud Object Storage Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Cloud Object Storage Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Cloud Object Storage Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Cloud Object Storage Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Cloud Object Storage Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Cloud Object Storage Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Cloud Object Storage Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Cloud Object Storage Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Cloud Object Storage Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Cloud Object Storage Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Cloud Object Storage Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Cloud Object Storage Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Cloud Object Storage Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Cloud Object Storage Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Cloud Object Storage Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Cloud Object Storage Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Cloud Object Storage Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Cloud Object Storage Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Cloud Object Storage Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Cloud Object Storage Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Cloud Object Storage Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Cloud Object Storage Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Cloud Object Storage Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Cloud Object Storage Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Cloud Object Storage Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Cloud Object Storage Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Cloud Object Storage Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Cloud Object Storage Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Cloud Object Storage Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Cloud Object Storage Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Cloud Object Storage Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Cloud Object Storage Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Cloud Object Storage Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Cloud Object Storage Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Cloud Object Storage Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Cloud Object Storage Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Cloud Object Storage Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Cloud Object Storage Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Cloud Object Storage Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Cloud Object Storage Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Cloud Object Storage Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Cloud Object Storage Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Cloud Object Storage Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Cloud Object Storage Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Cloud Object Storage Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Cloud Object Storage Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Cloud Object Storage Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Cloud Object Storage Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Cloud Object Storage Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Cloud Object Storage Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Cloud Object Storage Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Cloud Object Storage Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Cloud Object Storage Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Cloud Object Storage Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Cloud Object Storage Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Cloud Object Storage Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Cloud Object Storage Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Cloud Object Storage Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Cloud Object Storage?

The projected CAGR is approximately 16.2%.

2. Which companies are prominent players in the Cloud Object Storage?

Key companies in the market include IBM, Dell, Hewlett-Packard Enterprise, Hitachi Data Systems, Caringo Inc., Datadirect Networks, International Data Corporation, Netapp, Inc., Microsoft Corporation, Google, Elastifile, OSNEXUS, Iron Mountain.

3. What are the main segments of the Cloud Object Storage?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5600.00, USD 8400.00, and USD 11200.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Cloud Object Storage," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Cloud Object Storage report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Cloud Object Storage?

To stay informed about further developments, trends, and reports in the Cloud Object Storage, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence