Key Insights

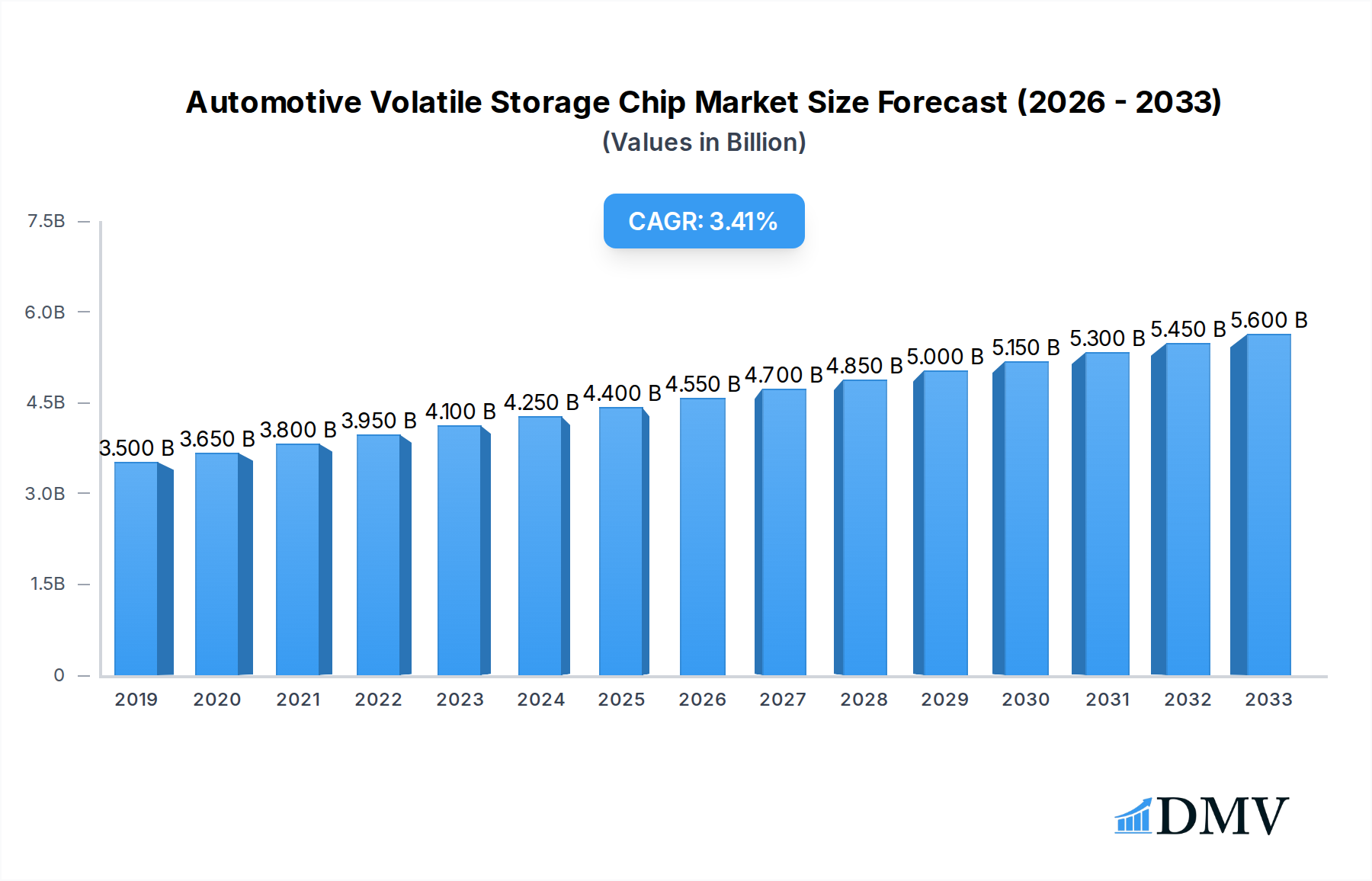

The Automotive Volatile Storage Chip market is poised for significant expansion, projected to reach $5055 million by 2033, demonstrating a robust 3.1% CAGR during the forecast period of 2019-2033. This growth is primarily fueled by the escalating demand for advanced in-vehicle infotainment (IVI) systems and sophisticated Advanced Driver-Assistance Systems (ADAS). As vehicles become increasingly connected and autonomous, the need for high-speed, reliable volatile memory solutions like DRAM and SRAM escalates. These chips are critical for real-time data processing, enabling features such as predictive navigation, complex sensor data analysis for safety systems, and seamless multimedia experiences for drivers and passengers. The continuous innovation in automotive electronics, coupled with stringent safety regulations mandating advanced driver-assistance technologies, directly translates into a heightened requirement for these essential storage components.

Automotive Volatile Storage Chip Market Size (In Billion)

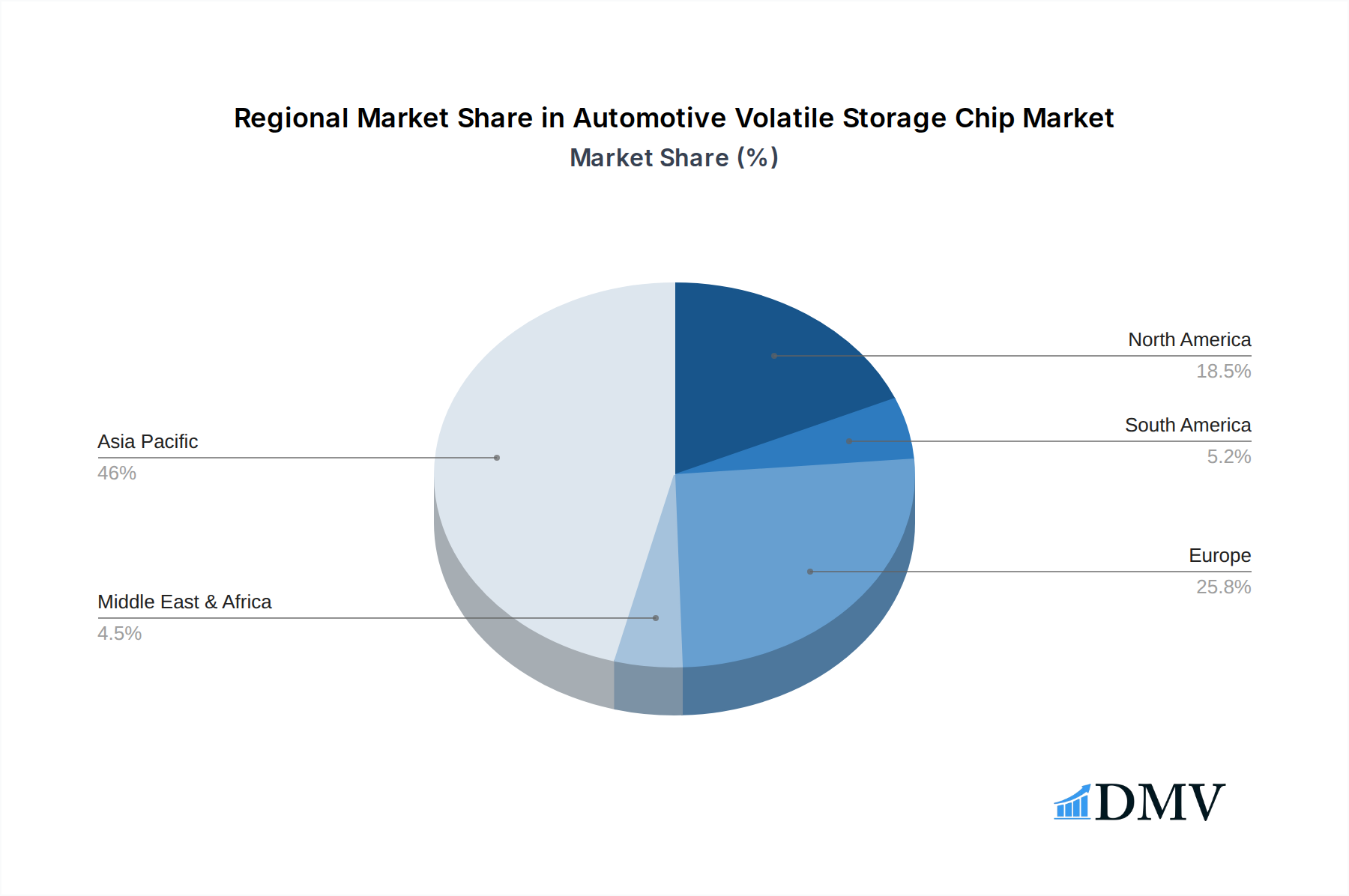

Furthermore, the market is experiencing dynamic shifts driven by technological advancements and evolving consumer expectations. The transition towards electric vehicles (EVs) and the growing complexity of automotive architectures are also contributing factors to this upward trajectory. While the market presents substantial growth opportunities, it is also subject to challenges such as the fluctuating costs of raw materials and the ever-present need for stringent quality control and cybersecurity in automotive applications. Key players like Micron, Samsung, SK Hynix, and Renesas are at the forefront, investing heavily in research and development to offer more efficient and higher-capacity volatile storage solutions. The Asia Pacific region, particularly China and Japan, is expected to lead market growth due to its dominance in automotive manufacturing and rapid adoption of new technologies.

Automotive Volatile Storage Chip Company Market Share

Automotive Volatile Storage Chip Market Composition & Trends

The automotive volatile storage chip market is characterized by a moderate to high concentration, with key players like Micron, Samsung, SK Hynix Semiconductor, and Nanya Technology dominating a significant portion of the market share. This competitive landscape is driven by continuous innovation, particularly in enhancing performance and power efficiency for demanding automotive applications such as In-vehicle IVI and ADAS Systems. The regulatory environment, focusing on safety and data integrity, plays a crucial role in shaping product development and market entry. Substitute products, primarily in the form of non-volatile memory solutions for specific data retention needs, are emerging but have not yet significantly eroded the demand for volatile storage in core real-time processing. End-user profiles are increasingly sophisticated, demanding higher bandwidth and lower latency for advanced functionalities. Mergers and acquisitions are strategically reshaping the market, with recent deals valued in the hundreds of millions, aiming to consolidate technology portfolios and expand market reach. The market share distribution among DRAM and SRAM reveals a clear preference for DRAM due to its higher density and cost-effectiveness for high-capacity storage needs in modern vehicles, while SRAM maintains its niche in high-speed, critical control applications.

Automotive Volatile Storage Chip Industry Evolution

The automotive volatile storage chip industry has witnessed a remarkable evolution, marked by a consistent upward trajectory in market growth and technological innovation throughout the study period (2019–2033). From a base year of 2025, the market has been propelled by a confluence of factors, primarily the escalating demand for advanced automotive electronics. The proliferation of In-vehicle Infotainment (IVI) systems, offering sophisticated entertainment, navigation, and connectivity features, necessitates substantial volatile memory capacity. Simultaneously, the rapid advancement of Automotive Driver-Assistance Systems (ADAS) – encompassing features like adaptive cruise control, lane-keeping assist, and automatic emergency braking – relies heavily on real-time data processing powered by high-speed volatile storage solutions. The historical period (2019–2024) saw initial adoption curves for these technologies, with market growth rates averaging around 15-20% annually. As we move into the forecast period (2025–2033), these rates are projected to sustain, driven by increasing vehicle electrification and the pursuit of autonomous driving capabilities. Technological advancements have been a constant catalyst. The transition from traditional DRAM architectures to more advanced technologies like DDR5 and emerging LPDDR standards has enabled higher data transfer rates and improved power efficiency, crucial for the energy-constrained automotive environment. The development of specialized automotive-grade volatile memory, designed to withstand extreme temperature variations and stringent reliability standards, has further fueled adoption. Consumer demand has shifted significantly, with buyers now expecting a seamless digital experience within their vehicles, mirroring the performance and responsiveness of their personal electronic devices. This has put pressure on automotive manufacturers and their suppliers to integrate higher-performance computing and storage solutions, directly benefiting the volatile storage chip market. The market size in the estimated year of 2025 is projected to reach over $5,000 million, with significant contributions from both DRAM and SRAM segments. The integration of AI and machine learning algorithms in vehicles for predictive maintenance, driver behavior analysis, and enhanced safety features further amplifies the need for faster and more capacious volatile memory.

Leading Regions, Countries, or Segments in Automotive Volatile Storage Chip

The dominance in the automotive volatile storage chip market is clearly established within the ADAS System application segment, driven by its critical role in enabling advanced safety and semi-autonomous driving features. This segment is poised for substantial growth in the forecast period (2025–2033), outpacing other applications like In-vehicle IVI and the broader "Other" category. Several key drivers underpin ADAS System's supremacy.

- Technological Imperative: ADAS functions rely on the rapid processing of massive amounts of sensor data (cameras, radar, lidar) in real-time. Volatile memory, particularly high-speed DRAM and SRAM, is indispensable for buffering this data and facilitating immediate algorithmic computations. The increasing sophistication of ADAS features, moving towards higher levels of autonomy, directly translates to a demand for more powerful and capacious volatile storage solutions.

- Regulatory Push for Safety: Stringent automotive safety regulations worldwide, mandating features like automatic emergency braking and lane departure warnings, are a significant impetus. Governments are actively promoting the adoption of ADAS technologies, creating a robust market for the underlying components, including volatile storage chips. This regulatory support, coupled with the potential to reduce accidents and save lives, makes ADAS a priority for all major automotive markets.

- Investment Trends in R&D: Leading automotive manufacturers and semiconductor companies are investing billions of dollars in the research and development of next-generation ADAS technologies. This includes advancements in sensor fusion, AI algorithms, and the underlying hardware infrastructure, all of which require cutting-edge volatile memory performance. Companies like Renesas, Infineon, and ON Semiconductor are at the forefront of these investments.

- Consumer Demand for Enhanced Safety: While safety might be mandated, there is also a growing consumer awareness and demand for vehicles equipped with advanced driver-assistance features. This growing preference translates into higher sales volumes for vehicles with sophisticated ADAS, consequently driving the demand for the necessary volatile storage chips.

- Technological Advancements in DRAM and SRAM: The evolution of DRAM technologies, such as DDR5 and LPDDR5, offering higher bandwidth and lower power consumption, is perfectly aligned with the performance requirements of ADAS. Similarly, advancements in SRAM for ultra-fast caching and critical control functions are also crucial for the reliable operation of these systems. This synergy between semiconductor innovation and application needs is a hallmark of ADAS dominance.

Analyzing the dominance by Type, DRAM emerges as the primary beneficiary due to its ability to provide high-density, cost-effective storage essential for the data-intensive nature of ADAS and IVI systems. SRAM, while critical for specific high-speed, low-latency applications within ADAS, commands a smaller market share compared to DRAM's broader utility. The estimated market size for volatile storage chips in ADAS Systems alone is projected to exceed $3,000 million in 2025.

Automotive Volatile Storage Chip Product Innovations

Automotive volatile storage chips are experiencing rapid innovation, focusing on enhanced performance, reliability, and specialized functionalities for demanding vehicle environments. Micron, Samsung, and SK Hynix Semiconductor are leading the charge with advanced DRAM solutions, including DDR5 and LPDDR5 variants, offering significantly higher bandwidth and improved power efficiency crucial for ADAS Systems and In-vehicle IVI. These innovations enable faster data processing for complex algorithms and richer multimedia experiences. Furthermore, product developments emphasize automotive-grade reliability, with enhanced temperature resistance (up to 125°C or higher) and adherence to stringent AEC-Q100 standards, ensuring uninterrupted operation under extreme conditions. GSI Technology and AMIC are also contributing with specialized SRAM solutions for critical control units and high-speed cache applications, ensuring millisecond response times essential for safety-critical functions. The unique selling proposition lies in achieving automotive-grade performance and reliability while optimizing for power consumption and cost, enabling the widespread adoption of advanced in-car technologies.

Propelling Factors for Automotive Volatile Storage Chip Growth

Several key factors are propelling the automotive volatile storage chip market. The relentless pursuit of advanced driver-assistance systems (ADAS) and the march towards autonomous driving necessitate significant increases in processing power and, consequently, volatile memory capacity and speed. The growing demand for sophisticated in-vehicle infotainment (IVI) systems, offering seamless connectivity, high-definition displays, and advanced multimedia features, further drives consumption. Electrification of vehicles is also a significant catalyst, as EVs often incorporate more advanced electronics and computational capabilities. Furthermore, increasing stringent safety regulations worldwide are mandating the integration of more safety features, directly boosting the need for robust volatile storage. Technological advancements in DRAM and SRAM, offering higher bandwidth and improved power efficiency, are also critical enablers.

Obstacles in the Automotive Volatile Storage Chip Market

Despite robust growth prospects, the automotive volatile storage chip market faces certain obstacles. Supply chain disruptions, exacerbated by geopolitical events and natural disasters, can lead to component shortages and price volatility, impacting production timelines and costs. The increasing complexity of automotive electronics requires rigorous validation and testing, leading to extended development cycles and higher R&D expenditures. Intensifying competition among established players and emerging manufacturers can put pressure on profit margins. Moreover, the transition to higher memory densities and faster speeds requires significant capital investment in advanced manufacturing facilities, posing a barrier to entry for smaller players. Finally, long product lifecycles and stringent qualification processes in the automotive industry can slow down the adoption of new technologies.

Future Opportunities in Automotive Volatile Storage Chip

Emerging opportunities in the automotive volatile storage chip market are abundant. The expansion of 5G connectivity in vehicles will unlock new possibilities for data-intensive applications and over-the-air updates, requiring greater volatile storage capacity. The growing trend of software-defined vehicles will shift focus towards memory solutions that can support dynamic software configurations and frequent updates. The development of AI-powered vehicle functionalities, such as predictive maintenance and personalized driving experiences, presents a substantial opportunity for high-performance volatile memory. Furthermore, the increasing adoption of edge computing within vehicles for faster local data processing, and the potential for advanced cockpit designs with multiple integrated displays, will continue to fuel demand for innovative volatile storage solutions.

Major Players in the Automotive Volatile Storage Chip Ecosystem

- Micron

- ISSI

- Samsung

- Nanya Technology

- Winbond Electronics

- SK Hynix Semiconductor

- Renesas

- Infineon

- GSI Technology

- ON Semiconductor

- AMIC

Key Developments in Automotive Volatile Storage Chip Industry

- 2023/Q4: Micron announces next-generation automotive-grade DDR5 DRAM, offering significant performance improvements for ADAS and IVI systems.

- 2023/Q3: Samsung expands its portfolio of automotive LPDDR5X DRAM, focusing on enhanced power efficiency for electric vehicles.

- 2023/Q2: SK Hynix Semiconductor unveils its latest high-bandwidth memory (HBM) solutions tailored for AI-driven autonomous driving applications.

- 2023/Q1: Renesas Electronics announces strategic partnerships to integrate advanced volatile storage solutions into its automotive microcontrollers.

- 2022/Q4: Infineon Technologies acquires Cypress Semiconductor, bolstering its offerings in automotive memory and microcontrollers.

- 2022/Q3: Nanya Technology increases production capacity for automotive-grade DRAM to meet growing industry demand.

- 2022/Q2: GSI Technology introduces specialized SRAM solutions for high-speed data buffering in critical automotive control units.

- 2022/Q1: ON Semiconductor enhances its automotive power management ICs to better support high-performance volatile memory integration.

- 2021/Q4: Winbond Electronics expands its NOR Flash offerings, complementary to volatile memory in automotive applications.

- 2021/Q3: AMIC introduces new low-power SRAM solutions designed for energy-constrained automotive ECUs.

Strategic Automotive Volatile Storage Chip Market Forecast

The strategic forecast for the automotive volatile storage chip market is overwhelmingly positive, driven by an unyielding demand for enhanced vehicle intelligence and safety. The projected growth is intrinsically linked to the accelerating adoption of advanced ADAS and the ongoing development of autonomous driving capabilities, creating a sustained need for high-performance, high-capacity volatile memory. The evolution of connected car technologies and the increasing integration of sophisticated in-vehicle infotainment systems further solidify this upward trend. Investments in next-generation memory technologies, focusing on speed, efficiency, and automotive-grade reliability, will continue to be a key growth catalyst. The market is poised to witness significant expansion, with opportunities arising from new applications in AI, edge computing, and software-defined architectures, ensuring a robust and dynamic future for this critical segment of the automotive electronics industry.

Automotive Volatile Storage Chip Segmentation

-

1. Application

- 1.1. In-vehicle IVI

- 1.2. ADAS System

- 1.3. Other

-

2. Type

- 2.1. DRAM

- 2.2. SRAM

Automotive Volatile Storage Chip Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive Volatile Storage Chip Regional Market Share

Geographic Coverage of Automotive Volatile Storage Chip

Automotive Volatile Storage Chip REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. In-vehicle IVI

- 5.1.2. ADAS System

- 5.1.3. Other

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. DRAM

- 5.2.2. SRAM

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Automotive Volatile Storage Chip Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. In-vehicle IVI

- 6.1.2. ADAS System

- 6.1.3. Other

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. DRAM

- 6.2.2. SRAM

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Automotive Volatile Storage Chip Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. In-vehicle IVI

- 7.1.2. ADAS System

- 7.1.3. Other

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. DRAM

- 7.2.2. SRAM

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Automotive Volatile Storage Chip Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. In-vehicle IVI

- 8.1.2. ADAS System

- 8.1.3. Other

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. DRAM

- 8.2.2. SRAM

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Automotive Volatile Storage Chip Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. In-vehicle IVI

- 9.1.2. ADAS System

- 9.1.3. Other

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. DRAM

- 9.2.2. SRAM

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Automotive Volatile Storage Chip Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. In-vehicle IVI

- 10.1.2. ADAS System

- 10.1.3. Other

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. DRAM

- 10.2.2. SRAM

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Automotive Volatile Storage Chip Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. In-vehicle IVI

- 11.1.2. ADAS System

- 11.1.3. Other

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. DRAM

- 11.2.2. SRAM

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Micron

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 ISSI

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Samsung

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Nanya Technology

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Winbond Electronics

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 SK Hynix Semiconductor

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Renesas

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Infineon

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 GSI Technology

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 ON Semiconductor

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 AMIC

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 Micron

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Automotive Volatile Storage Chip Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Automotive Volatile Storage Chip Revenue (million), by Application 2025 & 2033

- Figure 3: North America Automotive Volatile Storage Chip Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automotive Volatile Storage Chip Revenue (million), by Type 2025 & 2033

- Figure 5: North America Automotive Volatile Storage Chip Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Automotive Volatile Storage Chip Revenue (million), by Country 2025 & 2033

- Figure 7: North America Automotive Volatile Storage Chip Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Automotive Volatile Storage Chip Revenue (million), by Application 2025 & 2033

- Figure 9: South America Automotive Volatile Storage Chip Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Automotive Volatile Storage Chip Revenue (million), by Type 2025 & 2033

- Figure 11: South America Automotive Volatile Storage Chip Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Automotive Volatile Storage Chip Revenue (million), by Country 2025 & 2033

- Figure 13: South America Automotive Volatile Storage Chip Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Automotive Volatile Storage Chip Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Automotive Volatile Storage Chip Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Automotive Volatile Storage Chip Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Automotive Volatile Storage Chip Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Automotive Volatile Storage Chip Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Automotive Volatile Storage Chip Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Automotive Volatile Storage Chip Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Automotive Volatile Storage Chip Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Automotive Volatile Storage Chip Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Automotive Volatile Storage Chip Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Automotive Volatile Storage Chip Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Automotive Volatile Storage Chip Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Automotive Volatile Storage Chip Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Automotive Volatile Storage Chip Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Automotive Volatile Storage Chip Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Automotive Volatile Storage Chip Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Automotive Volatile Storage Chip Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Automotive Volatile Storage Chip Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Volatile Storage Chip Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Automotive Volatile Storage Chip Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Automotive Volatile Storage Chip Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Automotive Volatile Storage Chip Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Automotive Volatile Storage Chip Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Automotive Volatile Storage Chip Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Automotive Volatile Storage Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Automotive Volatile Storage Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Automotive Volatile Storage Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Automotive Volatile Storage Chip Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Automotive Volatile Storage Chip Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Automotive Volatile Storage Chip Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Automotive Volatile Storage Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Automotive Volatile Storage Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Automotive Volatile Storage Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Automotive Volatile Storage Chip Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Automotive Volatile Storage Chip Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Automotive Volatile Storage Chip Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Automotive Volatile Storage Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Automotive Volatile Storage Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Automotive Volatile Storage Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Automotive Volatile Storage Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Automotive Volatile Storage Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Automotive Volatile Storage Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Automotive Volatile Storage Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Automotive Volatile Storage Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Automotive Volatile Storage Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Automotive Volatile Storage Chip Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Automotive Volatile Storage Chip Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Automotive Volatile Storage Chip Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Automotive Volatile Storage Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Automotive Volatile Storage Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Automotive Volatile Storage Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Automotive Volatile Storage Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Automotive Volatile Storage Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Automotive Volatile Storage Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Automotive Volatile Storage Chip Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Automotive Volatile Storage Chip Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Automotive Volatile Storage Chip Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Automotive Volatile Storage Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Automotive Volatile Storage Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Automotive Volatile Storage Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Automotive Volatile Storage Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Automotive Volatile Storage Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Automotive Volatile Storage Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Automotive Volatile Storage Chip Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Volatile Storage Chip?

The projected CAGR is approximately 3.1%.

2. Which companies are prominent players in the Automotive Volatile Storage Chip?

Key companies in the market include Micron, ISSI, Samsung, Nanya Technology, Winbond Electronics, SK Hynix Semiconductor, Renesas, Infineon, GSI Technology, ON Semiconductor, AMIC.

3. What are the main segments of the Automotive Volatile Storage Chip?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 5055 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Volatile Storage Chip," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Volatile Storage Chip report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Volatile Storage Chip?

To stay informed about further developments, trends, and reports in the Automotive Volatile Storage Chip, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence