Key Insights

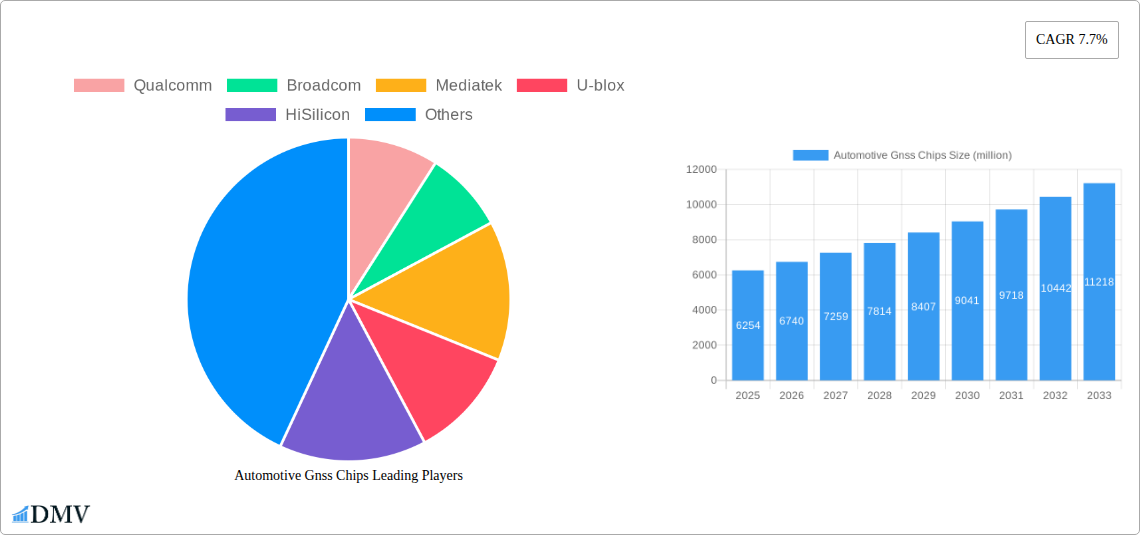

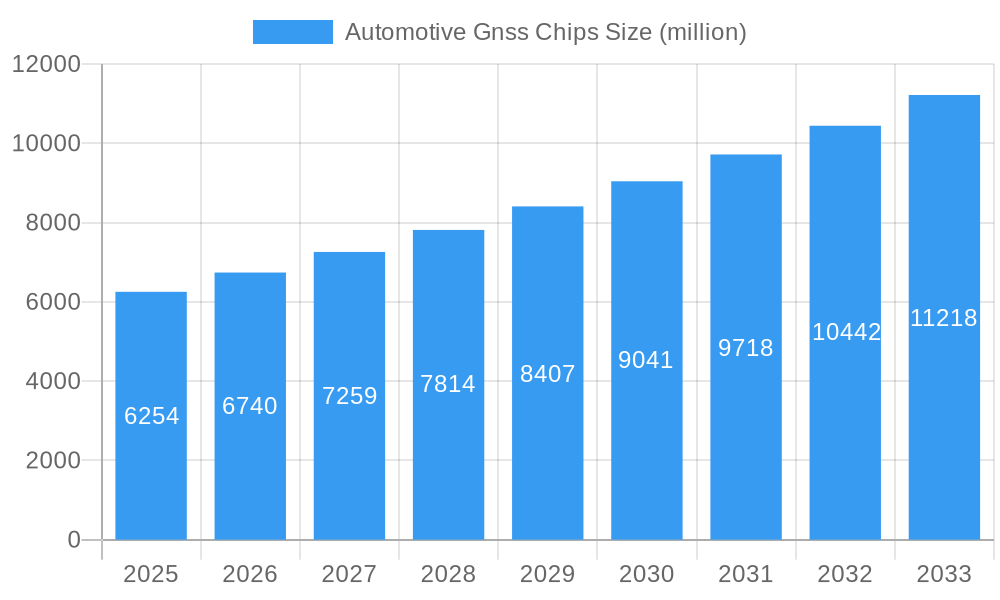

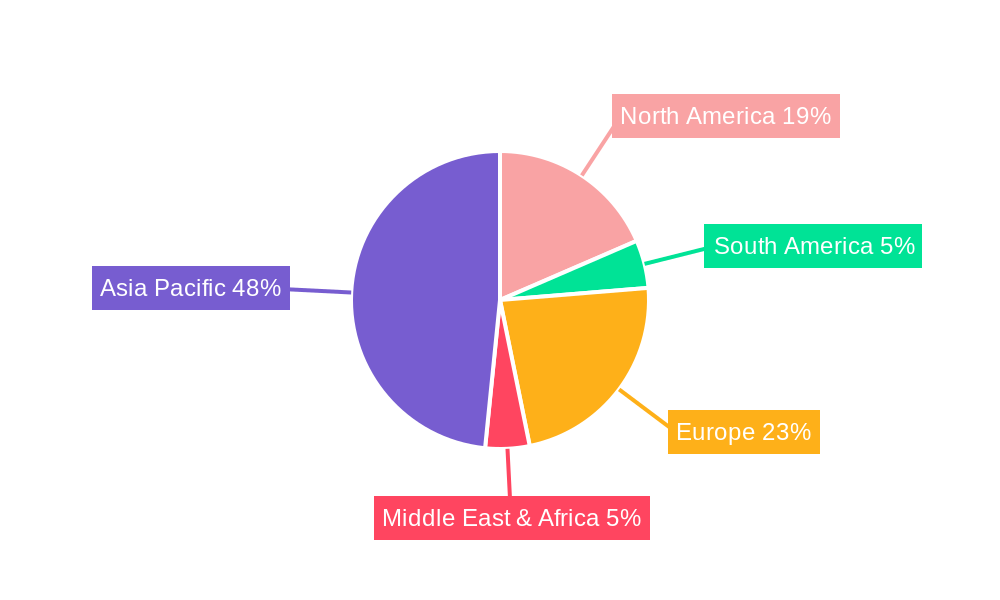

The global Automotive GNSS Chips market is poised for significant expansion, projected to reach a valuation of approximately USD 6,254 million by 2025. This robust growth is fueled by a Compound Annual Growth Rate (CAGR) of 7.7% throughout the forecast period extending to 2033. The increasing integration of advanced navigation and positioning systems in both passenger cars and commercial vehicles is a primary driver, enhancing functionalities such as real-time traffic updates, precise location services for autonomous driving, and advanced driver-assistance systems (ADAS). The demand for High Precision GNSS Chips is escalating, driven by the stringent accuracy requirements for safety-critical automotive applications, including lane-keeping assist, automated parking, and the burgeoning field of vehicle-to-everything (V2X) communication. Standard Precision GNSS Chips will continue to cater to essential navigation and infotainment systems, maintaining a steady demand. Geographically, the Asia Pacific region, particularly China and Japan, is anticipated to dominate the market, owing to its advanced automotive manufacturing capabilities and rapid adoption of new vehicle technologies. North America and Europe are also substantial markets, driven by stringent safety regulations and a growing consumer preference for connected and autonomous vehicles.

Automotive Gnss Chips Market Size (In Billion)

The market landscape is characterized by intense competition, with key players like Qualcomm, Broadcom, Mediatek, and U-blox leading the innovation in GNSS chip technology. These companies are focusing on developing smaller, more power-efficient, and highly accurate GNSS solutions. Emerging trends include the adoption of multi-constellation GNSS receivers capable of utilizing signals from Galileo, GLONASS, BeiDou, and GPS simultaneously, leading to enhanced reliability and accuracy. The miniaturization of GNSS modules and the integration of GNSS functionality with other sensors, such as inertial measurement units (IMUs), are also critical trends shaping the market. Despite the promising growth trajectory, certain factors could pose challenges. The complexity of integrating GNSS chips with existing vehicle electronics and the potential for signal interference in urban canyons or tunnels might present development hurdles. Furthermore, the evolving regulatory landscape surrounding data privacy and security for connected vehicles will necessitate continuous adaptation from manufacturers. Nonetheless, the overarching trend towards increasingly intelligent and connected vehicles ensures a dynamic and expanding future for the Automotive GNSS Chips market.

Automotive Gnss Chips Company Market Share

This comprehensive market research report delves deep into the Automotive GNSS Chips market, providing an in-depth analysis of its current state, historical trajectory, and future projections. Designed to equip stakeholders with actionable insights, this report covers market composition, industry evolution, regional dominance, product innovations, growth drivers, market obstacles, emerging opportunities, major players, key developments, and strategic market forecasts. The study spans the Study Period: 2019–2033, with a Base Year: 2025, Estimated Year: 2025, and Forecast Period: 2025–2033, building upon the Historical Period: 2019–2024. We meticulously analyze the impact of High Precision GNSS Chips and Standard Precision GNSS Chips across Passenger Cars and Commercial Vehicles, offering a panoramic view of this critical automotive technology segment.

Automotive Gnss Chips Market Composition & Trends

The Automotive GNSS Chips market exhibits a dynamic composition characterized by a moderate level of concentration, with key players like Qualcomm, Broadcom, Mediatek, U-blox, and STMicroelectronics holding significant market share. Innovation catalysts are primarily driven by the increasing demand for advanced driver-assistance systems (ADAS), autonomous driving features, and enhanced in-vehicle infotainment. The integration of multi-constellation GNSS receivers (GPS, GLONASS, Galileo, BeiDou) and the development of chipsets with enhanced accuracy, reliability, and lower power consumption are shaping innovation trends. Regulatory landscapes, particularly those mandating enhanced safety features and data privacy, indirectly influence GNSS chip development, pushing for more robust and secure solutions. While direct substitute products are limited, the increasing sophistication of inertial navigation systems (INS) and visual odometry offers complementary positioning capabilities that can augment or, in specific scenarios, reduce reliance on GNSS. End-user profiles are predominantly automotive OEMs and Tier-1 suppliers who integrate these chips into their vehicle platforms. Merger and acquisition (M&A) activities, though not at a frenzied pace, are strategic, aimed at consolidating expertise, expanding product portfolios, and securing market access. For instance, recent M&A deals, with an estimated aggregate value of over XXX million, indicate a trend towards inorganic growth. The market share distribution shows the top 5 players commanding approximately XX% of the market in 2024.

Automotive Gnss Chips Industry Evolution

The Automotive GNSS Chips industry has witnessed a significant evolution driven by relentless technological advancements and the escalating demand for sophisticated navigation and positioning solutions within vehicles. From rudimentary GPS receivers for basic navigation, the industry has transitioned to highly integrated chipsets capable of providing centimeter-level accuracy, crucial for autonomous driving and advanced ADAS functionalities. The growth trajectory of this market has been consistently upward, fueled by the increasing adoption of connected car technologies and the growing sophistication of in-car electronics. During the Historical Period: 2019–2024, the market experienced a compound annual growth rate (CAGR) of approximately XX%, driven by the increasing penetration of navigation systems in new vehicle sales.

Technological advancements have been at the forefront of this evolution. The development of multi-band GNSS chipsets, which utilize multiple frequency bands from various satellite constellations, has dramatically improved accuracy and resilience to interference, particularly in challenging urban canyons and tunnels. Furthermore, the integration of complementary sensor fusion capabilities, such as accelerometers, gyroscopes, and magnetometers, within GNSS chipsets has enabled more robust and reliable positioning solutions, especially during GNSS signal outages. The advent of Real-Time Kinematic (RTK) and Precise Point Positioning (PPP) technologies, once confined to surveying and professional applications, is now being integrated into automotive-grade GNSS chips, paving the way for highly precise localization required for Level 3 and above autonomous driving.

Shifting consumer demands have also played a pivotal role. Modern car buyers expect seamless integration of navigation, real-time traffic information, and personalized location-based services. This has compelled automotive manufacturers to incorporate more advanced GNSS solutions. The increasing complexity of vehicle architectures and the drive towards software-defined vehicles further necessitate highly integrated and intelligent GNSS chips. The adoption metric for GNSS systems in new vehicles has risen from approximately XX% in 2019 to an estimated XX% in 2024. The market is projected to continue its robust growth, with an anticipated CAGR of XX% during the Forecast Period: 2025–2033, driven by the escalating adoption of autonomous driving technologies and the increasing prevalence of connected vehicle services.

Leading Regions, Countries, or Segments in Automotive Gnss Chips

The Automotive GNSS Chips market exhibits clear regional and segmental dominance, driven by distinct factors. In terms of geographical influence, North America and Europe currently lead the market, primarily due to their well-established automotive industries, high adoption rates of advanced automotive technologies, and stringent safety regulations that necessitate sophisticated positioning systems.

North America:

- Key Drivers: The strong presence of major automotive OEMs (e.g., Ford, GM, Tesla) and Tier-1 suppliers, coupled with a high consumer appetite for advanced features like ADAS and in-car navigation, fuels demand. Significant investments in autonomous vehicle R&D and testing further boost the need for high-performance High Precision GNSS Chips. Government initiatives and federal mandates promoting vehicle safety standards also contribute to market growth.

- Dominance Factors: The region’s mature automotive ecosystem, robust technological infrastructure, and proactive regulatory environment create a fertile ground for GNSS chip adoption. The focus on integrating GNSS with other sensor technologies for enhanced safety and autonomous driving is a significant differentiator.

Europe:

- Key Drivers: Similar to North America, Europe boasts a strong automotive manufacturing base and a high demand for advanced vehicle features. Stringent European New Car Assessment Programme (Euro NCAP) ratings, which increasingly emphasize safety and driver assistance, push manufacturers to integrate superior GNSS solutions. The ongoing development of intelligent transportation systems (ITS) and connected vehicle infrastructure also plays a crucial role.

- Dominance Factors: European automakers are at the forefront of automotive innovation, particularly in electrification and autonomous driving. The emphasis on data security and privacy within the EU also influences the demand for secure and reliable GNSS chip solutions.

Among the segments, Passenger Cars represent the largest application segment for Automotive GNSS Chips. This is due to the sheer volume of passenger vehicle production globally and the increasing standardization of navigation systems and basic ADAS features in even mid-range vehicles.

- Passenger Cars:

- Key Drivers: The rising consumer expectation for integrated navigation, real-time traffic updates, and smartphone mirroring capabilities (e.g., Apple CarPlay, Android Auto) directly translates into higher demand for GNSS chips. The proliferation of ADAS features like adaptive cruise control, lane-keeping assist, and automatic emergency braking, which increasingly rely on accurate positioning, further propels adoption.

- Dominance Factors: The mass-market appeal and high production volumes of passenger cars make them the primary volume driver for GNSS chip manufacturers. The continuous innovation cycle in passenger vehicle features ensures a sustained demand for updated and more advanced GNSS solutions.

While Commercial Vehicles represent a smaller volume segment, they are critical for the adoption of High Precision GNSS Chips due to their demanding operational requirements, such as fleet management, precise route optimization, and advanced telematics. The growing adoption of these chips in both segments underscores the indispensable role of GNSS technology in the modern automotive landscape.

Automotive Gnss Chips Product Innovations

The Automotive GNSS Chips market is characterized by rapid product innovation focused on enhancing accuracy, reliability, and integration. Leading companies are developing next-generation chipsets that support multi-band reception across all major GNSS constellations (GPS, GLONASS, Galileo, BeiDou), significantly improving accuracy to centimeter-level even in challenging environments like urban canyons. Innovations include advanced interference mitigation techniques to combat jamming and spoofing, crucial for safety-critical applications. Furthermore, the integration of High Precision GNSS Chips with inertial measurement units (IMUs) and sensor fusion algorithms is enabling seamless positioning during GNSS signal outages, a key requirement for autonomous driving. Chips are also being optimized for lower power consumption, reduced form factor, and enhanced security features, ensuring compliance with evolving automotive standards and facilitating easier integration into complex vehicle architectures.

Propelling Factors for Automotive Gnss Chips Growth

Several key factors are propelling the growth of the Automotive GNSS Chips market. Firstly, the accelerating adoption of Advanced Driver-Assistance Systems (ADAS) and the increasing push towards autonomous driving technologies (from Level 1 to Level 4) are paramount. These systems intrinsically rely on precise and reliable positioning data provided by GNSS chips. Secondly, the burgeoning connected car ecosystem, with its demand for real-time location-based services, enhanced navigation, and vehicle-to-everything (V2X) communication, is a significant growth catalyst. Thirdly, government regulations and safety mandates worldwide are increasingly emphasizing the need for robust navigation and positioning systems, thereby driving the adoption of higher-performing GNSS solutions. Finally, the continuous technological advancements in GNSS chipset design, leading to improved accuracy, lower power consumption, and enhanced interference immunity, are making these chips more attractive and cost-effective for automotive applications.

Obstacles in the Automotive Gnss Chips Market

Despite the robust growth, the Automotive GNSS Chips market faces several obstacles. Regulatory complexities and varying standards across different regions can pose challenges for global product deployment. Supply chain disruptions, as evidenced in recent years, can impact the availability and cost of crucial components and raw materials for chip manufacturing. Intense competition among established players and emerging entrants puts pressure on pricing and profit margins. Furthermore, the sensitivity of GNSS signals to environmental factors such as urban canyons, tunnels, and severe weather conditions can impact performance, necessitating advanced mitigation techniques which add to cost and complexity. The high cost of R&D and validation for automotive-grade components also presents a barrier, particularly for smaller players.

Future Opportunities in Automotive Gnss Chips

Emerging opportunities in the Automotive GNSS Chips market are diverse and promising. The continued development and widespread adoption of Level 4 and Level 5 autonomous driving will necessitate ultra-high precision and redundant positioning systems, creating a substantial market for advanced GNSS solutions. The expansion of V2X communication technologies offers opportunities for GNSS chips to play a central role in enabling safer and more efficient traffic management. Furthermore, the growth of the automotive aftermarket, with demand for retrofitting advanced navigation and safety features in older vehicles, presents another avenue for market expansion. The increasing integration of GNSS with other sensor technologies and AI-driven localization algorithms is opening up new possibilities for context-aware positioning and intelligent navigation.

Major Players in the Automotive Gnss Chips Ecosystem

- Qualcomm

- Broadcom

- Mediatek

- U-blox

- HiSilicon

- STMicroelectronics

- Furuno Electric

- Mengxin Technology

- Bynav

- Unistrong

- Techtotop

- UNISOC

- Goke Microelectronics

- ALLYSTAR Technology

- HangZhou ZhongKe Microelectronics

Key Developments in Automotive Gnss Chips Industry

- 2023 Q4: Qualcomm introduces new automotive GNSS platform with enhanced multi-band capabilities and integrated AI features for improved positioning accuracy.

- 2023 Q3: U-blox launches a new series of automotive-grade GNSS modules designed for robust performance in challenging environments.

- 2023 Q2: Broadcom announces advancements in its GNSS chipset technology, focusing on increased immunity to jamming and spoofing.

- 2023 Q1: Mediatek showcases its latest GNSS solutions optimized for next-generation connected car applications.

- 2022 Q4: STMicroelectronics partners with an ADAS supplier to integrate its GNSS chips into advanced driver assistance systems.

- 2022 Q3: HiSilicon releases updated GNSS chipsets with improved support for BeiDou and Galileo constellations.

- 2022 Q2: Bynav demonstrates centimeter-level positioning accuracy for autonomous driving using its proprietary GNSS technology.

- 2022 Q1: Mengxin Technology announces significant advancements in multi-frequency GNSS receivers for automotive applications.

- 2021 Q4: UNISOC expands its automotive GNSS portfolio with cost-effective solutions for mass-market vehicles.

- 2021 Q3: Goke Microelectronics unveils GNSS chipsets with integrated safety mechanisms for automotive functional safety.

Strategic Automotive Gnss Chips Market Forecast

The strategic forecast for the Automotive GNSS Chips market points towards sustained and robust growth, driven by the unstoppable march towards autonomous driving and the ever-increasing connectivity of vehicles. The continued demand for enhanced safety features, precise navigation, and seamless location-based services will fuel the adoption of increasingly sophisticated High Precision GNSS Chips. Technological advancements in multi-constellation support, interference mitigation, and sensor fusion will be critical enablers. The market's future potential is immense, with new opportunities arising from the evolving automotive landscape, including the integration of GNSS with emerging technologies like AI and 5G, and the expansion into new geographical markets. The market is projected to reach a valuation of approximately XXX billion by 2033, with a CAGR of XX% during the forecast period.

Automotive Gnss Chips Segmentation

-

1. Application

- 1.1. Passenger Cars

- 1.2. Commercial Vehicles

-

2. Type

- 2.1. High Precision GNSS Chips

- 2.2. Standard Precision GNSS Chips

Automotive Gnss Chips Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive Gnss Chips Regional Market Share

Geographic Coverage of Automotive Gnss Chips

Automotive Gnss Chips REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Cars

- 5.1.2. Commercial Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. High Precision GNSS Chips

- 5.2.2. Standard Precision GNSS Chips

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Automotive Gnss Chips Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Cars

- 6.1.2. Commercial Vehicles

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. High Precision GNSS Chips

- 6.2.2. Standard Precision GNSS Chips

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Automotive Gnss Chips Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Cars

- 7.1.2. Commercial Vehicles

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. High Precision GNSS Chips

- 7.2.2. Standard Precision GNSS Chips

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Automotive Gnss Chips Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Cars

- 8.1.2. Commercial Vehicles

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. High Precision GNSS Chips

- 8.2.2. Standard Precision GNSS Chips

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Automotive Gnss Chips Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Cars

- 9.1.2. Commercial Vehicles

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. High Precision GNSS Chips

- 9.2.2. Standard Precision GNSS Chips

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Automotive Gnss Chips Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Cars

- 10.1.2. Commercial Vehicles

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. High Precision GNSS Chips

- 10.2.2. Standard Precision GNSS Chips

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Automotive Gnss Chips Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Passenger Cars

- 11.1.2. Commercial Vehicles

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. High Precision GNSS Chips

- 11.2.2. Standard Precision GNSS Chips

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Qualcomm

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Broadcom

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Mediatek

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 U-blox

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 HiSilicon

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 STMicroelectronics

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Furuno Electric

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Mengxin Technology

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Bynav

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Unistrong

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Techtotop

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 UNISOC

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Goke Microelectronics

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 ALLYSTAR Technology

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 HangZhou ZhongKe Microelectronics

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 Qualcomm

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Automotive Gnss Chips Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Automotive Gnss Chips Revenue (million), by Application 2025 & 2033

- Figure 3: North America Automotive Gnss Chips Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automotive Gnss Chips Revenue (million), by Type 2025 & 2033

- Figure 5: North America Automotive Gnss Chips Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Automotive Gnss Chips Revenue (million), by Country 2025 & 2033

- Figure 7: North America Automotive Gnss Chips Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Automotive Gnss Chips Revenue (million), by Application 2025 & 2033

- Figure 9: South America Automotive Gnss Chips Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Automotive Gnss Chips Revenue (million), by Type 2025 & 2033

- Figure 11: South America Automotive Gnss Chips Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Automotive Gnss Chips Revenue (million), by Country 2025 & 2033

- Figure 13: South America Automotive Gnss Chips Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Automotive Gnss Chips Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Automotive Gnss Chips Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Automotive Gnss Chips Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Automotive Gnss Chips Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Automotive Gnss Chips Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Automotive Gnss Chips Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Automotive Gnss Chips Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Automotive Gnss Chips Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Automotive Gnss Chips Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Automotive Gnss Chips Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Automotive Gnss Chips Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Automotive Gnss Chips Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Automotive Gnss Chips Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Automotive Gnss Chips Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Automotive Gnss Chips Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Automotive Gnss Chips Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Automotive Gnss Chips Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Automotive Gnss Chips Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Gnss Chips Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Automotive Gnss Chips Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Automotive Gnss Chips Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Automotive Gnss Chips Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Automotive Gnss Chips Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Automotive Gnss Chips Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Automotive Gnss Chips Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Automotive Gnss Chips Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Automotive Gnss Chips Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Automotive Gnss Chips Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Automotive Gnss Chips Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Automotive Gnss Chips Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Automotive Gnss Chips Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Automotive Gnss Chips Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Automotive Gnss Chips Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Automotive Gnss Chips Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Automotive Gnss Chips Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Automotive Gnss Chips Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Automotive Gnss Chips Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Automotive Gnss Chips Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Automotive Gnss Chips Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Automotive Gnss Chips Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Automotive Gnss Chips Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Automotive Gnss Chips Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Automotive Gnss Chips Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Automotive Gnss Chips Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Automotive Gnss Chips Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Automotive Gnss Chips Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Automotive Gnss Chips Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Automotive Gnss Chips Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Automotive Gnss Chips Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Automotive Gnss Chips Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Automotive Gnss Chips Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Automotive Gnss Chips Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Automotive Gnss Chips Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Automotive Gnss Chips Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Automotive Gnss Chips Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Automotive Gnss Chips Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Automotive Gnss Chips Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Automotive Gnss Chips Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Automotive Gnss Chips Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Automotive Gnss Chips Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Automotive Gnss Chips Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Automotive Gnss Chips Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Automotive Gnss Chips Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Automotive Gnss Chips Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Gnss Chips?

The projected CAGR is approximately 7.7%.

2. Which companies are prominent players in the Automotive Gnss Chips?

Key companies in the market include Qualcomm, Broadcom, Mediatek, U-blox, HiSilicon, STMicroelectronics, Furuno Electric, Mengxin Technology, Bynav, Unistrong, Techtotop, UNISOC, Goke Microelectronics, ALLYSTAR Technology, HangZhou ZhongKe Microelectronics.

3. What are the main segments of the Automotive Gnss Chips?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 6254 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Gnss Chips," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Gnss Chips report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Gnss Chips?

To stay informed about further developments, trends, and reports in the Automotive Gnss Chips, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence