Key Insights

The Asia-Pacific dog food market is poised for significant expansion, driven by escalating pet ownership, rising disposable incomes, and a heightened focus on pet health and nutrition across the region. The market, valued at $17.85 billion in the base year 2025, is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.11% between 2025 and 2033. Key growth catalysts include the increasing 'humanization' of pets, which spurs higher expenditure on premium and specialized dog food offerings. This trend is prominently observed in mature economies like Japan and Australia, and is rapidly gaining traction in emerging markets such as India and Vietnam, propelled by a growing middle class. The market segmentation by product type (dry, wet, treats), distribution channel (supermarkets, online retailers, specialty stores), and country offers diverse avenues for growth, with convenience and online channels experiencing particularly strong momentum as consumers seek accessible and varied product selections. Despite potential challenges from fluctuating raw material prices and regional economic uncertainties, the overall market outlook remains highly positive. The competitive landscape, featuring established international brands and agile regional players, fosters innovation and a wider array of consumer choices and price points.

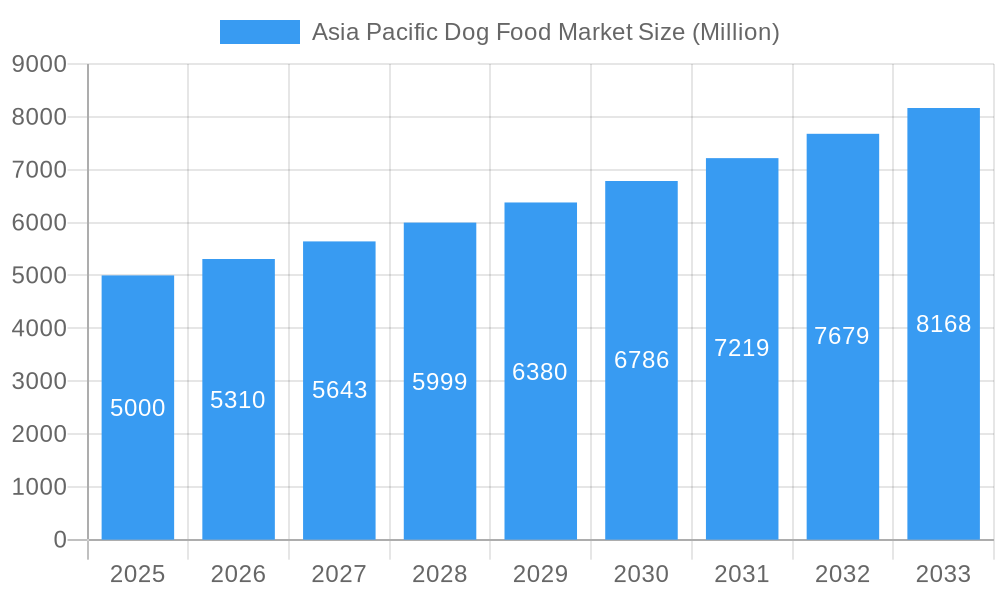

Asia Pacific Dog Food Market Market Size (In Billion)

The inherent diversity of the Asia-Pacific region presents both strategic opportunities and operational challenges. Significant markets like China, India, and Japan are characterized by large populations and expanding pet ownership. However, distinct consumer preferences and regulatory frameworks necessitate localized marketing and product development strategies. The burgeoning demand for premium and functional dog foods, addressing specific dietary requirements such as allergies or digestive sensitivities, represents a key growth segment. Moreover, the increasing prevalence of online pet food retailers broadens customer reach, reducing dependence on traditional retail. Sustained market growth will depend on navigating emerging market pricing sensitivities and ensuring supply chain resilience. Success will favor market participants who adeptly manage regional specificities, capitalize on digital marketing channels, and innovate with high-quality, bespoke product solutions.

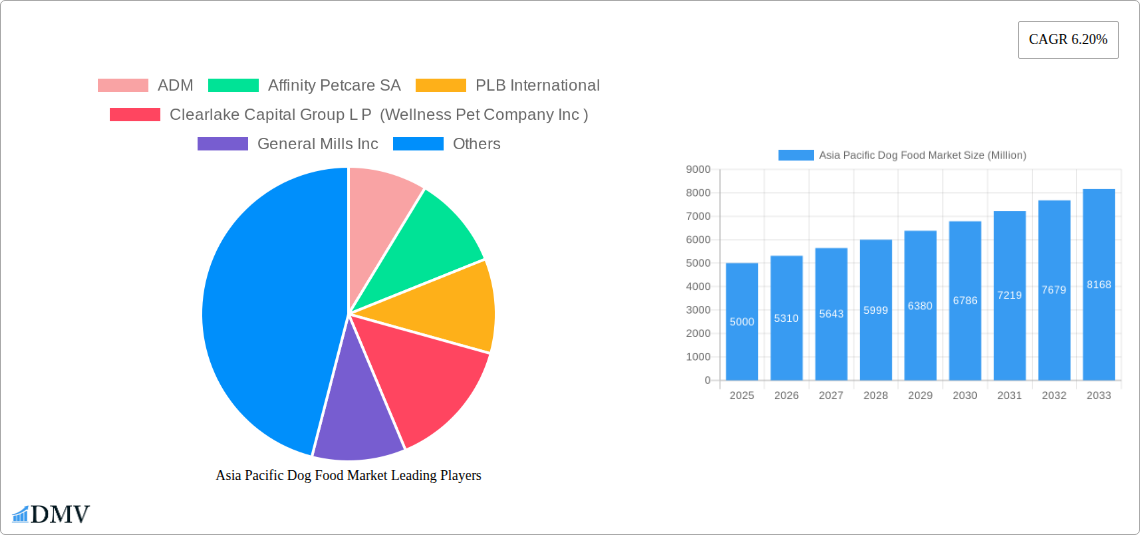

Asia Pacific Dog Food Market Company Market Share

Asia Pacific Dog Food Market: A Comprehensive Report (2019-2033)

This insightful report provides a detailed analysis of the Asia Pacific dog food market, encompassing historical data (2019-2024), current estimates (2025), and future projections (2025-2033). It offers crucial insights for stakeholders, including manufacturers, distributors, investors, and regulatory bodies, seeking to understand market dynamics, growth opportunities, and competitive landscapes within this rapidly expanding sector. The market is valued at xx Million in 2025 and is projected to reach xx Million by 2033, exhibiting a CAGR of xx%.

Asia Pacific Dog Food Market Composition & Trends

This section delves into the intricate composition of the Asia Pacific dog food market, examining key aspects that influence its trajectory. We analyze market concentration, revealing the dominance of key players like Mars Incorporated and Nestle (Purina), and quantify their market share. The report explores innovation catalysts, including the rise of premium and specialized dog foods catering to specific dietary needs and preferences. The impact of regulatory landscapes, varying across different Asia-Pacific countries, is carefully assessed, alongside the influence of substitute products and emerging trends in pet ownership. End-user profiles are segmented by factors such as income levels, pet breed preferences, and lifestyle choices. Furthermore, the report documents significant M&A activities, including deal values and their implications for market consolidation.

- Market Concentration: Highly concentrated, with top 5 players holding xx% market share in 2025.

- Innovation Catalysts: Premiumization, functional foods (e.g., hypoallergenic, weight management), and sustainable sourcing.

- Regulatory Landscape: Varied across nations, impacting labeling, ingredient regulations, and import/export.

- Substitute Products: Limited, but increasing awareness of homemade diets poses a potential threat.

- M&A Activity: Significant activity observed in the historical period (2019-2024), with deal values totaling xx Million. Examples include [Insert specific examples if available, otherwise state "Specific deals are detailed within the report"].

Asia Pacific Dog Food Market Industry Evolution

This section traces the evolution of the Asia Pacific dog food market, analyzing its growth trajectories, technological advancements, and evolving consumer preferences. It provides granular data on growth rates, adoption of new technologies, and shifts in consumer purchasing behavior across different segments. The report examines how technological advancements in pet food manufacturing, such as precision feeding and customized formulations, are influencing product development and market expansion. We explore the rising demand for premium and specialized dog food, driven by increasing pet humanization and a greater focus on pet health and nutrition. Detailed analysis of the growth trajectory from 2019 to 2024, showcasing specific growth rates for each year, is presented within. The impact of changing demographics, including rising disposable incomes and urbanization in key markets, on consumer spending on pet food is also analyzed.

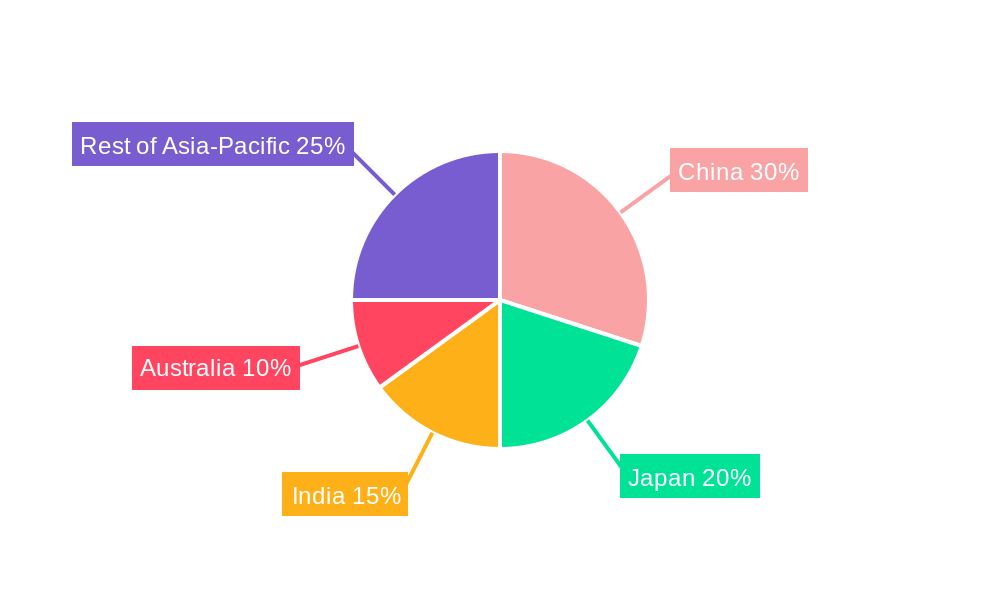

Leading Regions, Countries, or Segments in Asia Pacific Dog Food Market

This segment provides an in-depth analysis of the most influential regions, countries, and market segments within the dynamic Asia Pacific dog food landscape. We meticulously examine the contributing factors behind their leadership, including evolving investment patterns, supportive regulatory frameworks, and shifting consumer preferences. A comprehensive comparative overview of pivotal markets such as China, Japan, and Australia is presented, taking into account critical indicators like pet ownership penetration, prevailing economic conditions, and the sophistication of distribution networks.

- Dominant Region: China continues its reign, propelled by a burgeoning middle class, escalating disposable incomes, and a significant surge in pet ownership, making it a cornerstone of the Asia Pacific market.

- Key Countries with High Growth Potential: Beyond China, Japan, Australia, and India are emerging as critical growth hubs, each exhibiting unique market dynamics and consumer demands. South Korea and Southeast Asian nations are also showing promising traction.

- Leading Distribution Channels: While Supermarkets/Hypermarkets maintain the largest distribution channel share due to convenience and accessibility, Specialty Pet Stores are rapidly gaining prominence, offering curated selections and expert advice. The rise of E-commerce platforms is also a significant trend, revolutionizing accessibility and consumer choice.

- Dominant Product Segment: Dry dog food continues to command the largest market share, owing to its convenience, shelf-life, and cost-effectiveness. However, wet dog food and specialized functional foods (e.g., grain-free, organic, breed-specific) are experiencing robust growth, catering to evolving consumer demands for premiumization and health-focused options.

- Key Growth Drivers (China): The rapid expansion of the middle class, coupled with increasing urbanization and a growing desire for companionship, fuels high pet ownership rates. Rising disposable incomes translate to greater spending on premium pet nutrition, while the pervasive influence of e-commerce platforms simplifies purchasing.

- Key Growth Drivers (Japan): A deeply ingrained culture of pet companionship, coupled with a sophisticated consumer base, drives strong demand for premium, specialized, and highly functional dog foods, including those focusing on health benefits and gourmet ingredients.

- Key Growth Drivers (Australia): The concept of "pet humanization" is exceptionally strong, leading to a significant emphasis on pet health and nutrition. Consumers are increasingly discerning, seeking high-quality ingredients, transparent sourcing, and products that contribute to their dogs' long-term well-being.

Asia Pacific Dog Food Market Product Innovations

Recent years have witnessed significant product innovations in the Asia Pacific dog food market. Manufacturers are focusing on developing specialized diets, incorporating functional ingredients like probiotics, prebiotics, and omega-3 fatty acids, to cater to specific dietary needs and health concerns. The rise of novel protein sources, including insect protein and alternative meat sources, is also gaining traction. The emphasis is on improving palatability, digestibility, and overall nutritional value, leading to premiumization and increased consumer spending.

Propelling Factors for Asia Pacific Dog Food Market Growth

Several factors propel the growth of the Asia Pacific dog food market. These include rising pet ownership rates across the region, particularly in rapidly developing economies, coupled with increased disposable incomes and shifting consumer preferences toward premium pet food products. Favorable government regulations and supportive policies also contribute to market growth. Technological advancements in pet food manufacturing and packaging enhance product quality and shelf life. Furthermore, the growing adoption of online channels and e-commerce platforms offers convenient access to a wide variety of products, boosting market expansion.

Obstacles in the Asia Pacific Dog Food Market Market

Despite positive growth prospects, several challenges hinder the Asia Pacific dog food market's expansion. These include fluctuating raw material prices, supply chain disruptions, and intense competition among established and emerging players. Varying regulatory requirements across countries pose complexities for manufacturers operating across different markets. Consumer preference shifts and evolving dietary trends also present constant challenges, demanding continuous innovation and adaptation. Counterfeit products and concerns regarding ingredient safety and sustainability impact consumer confidence.

Future Opportunities in Asia Pacific Dog Food Market

The Asia Pacific dog food market presents several lucrative opportunities. The growth of the pet humanization trend and a rising middle class are key factors. Expansion into underserved markets, particularly in Southeast Asia, holds enormous potential. Innovation in functional pet foods, such as specialized diets for pets with specific health conditions, presents a major opportunity. Adoption of sustainable and ethical sourcing practices and packaging solutions is increasingly important, contributing to growth.

Major Players in the Asia Pacific Dog Food Market Ecosystem

- ADM (Archer Daniels Midland)

- Affinity Petcare SA

- PLB International

- Clearlake Capital Group L.P. (operating Wellness Pet Company Inc.)

- General Mills Inc. (including Blue Buffalo)

- IB Group (Drools Pet Food Pvt Ltd)

- Mars Incorporated (including Royal Canin, Pedigree, Whiskas)

- Nestlé S.A. (Purina PetCare) [Nestlé]

- Colgate-Palmolive Company (Hill's Pet Nutrition Inc.) [Hill's Pet Nutrition]

- Schell & Kampeter, Inc. (Diamond Pet Foods)

- Champion Petfoods LP (Orijen, Acana)

- Unicharm Corporation

- Local and regional players emerging with niche offerings.

Key Developments in Asia Pacific Dog Food Market Industry

- July 2023: Hill's Pet Nutrition launched innovative MSC-certified pollock and insect protein-based products, strategically catering to the rising demand for sustainable sourcing and hypoallergenic options for sensitive pets across the Asia Pacific region.

- April 2023: Mars Incorporated inaugurated its first dedicated pet food Research & Development center in the APAC region, underscoring its commitment to localized innovation, product development tailored to regional tastes and needs, and strengthening its market presence.

- March 2023: Blue Buffalo (part of General Mills Inc.) expanded its product portfolio with the introduction of its BLUE Wilderness Premier Blend, emphasizing a strong market trend towards high-protein formulations and natural ingredients to meet the evolving nutritional demands of pets.

- Ongoing Trend: Increasing investment in e-commerce and direct-to-consumer (DTC) channels by both global giants and emerging brands to enhance accessibility, personalize customer engagement, and leverage data analytics for market insights.

- Growing Focus: Significant investment in the development of functional dog foods, addressing specific health concerns such as digestive health, joint support, skin and coat condition, and cognitive function, driven by heightened consumer awareness of pet well-being.

Strategic Asia Pacific Dog Food Market Forecast

The Asia Pacific dog food market is poised for robust growth, driven by rising pet ownership, increasing disposable incomes, and a growing preference for premium and specialized pet foods. The market's future success hinges on manufacturers' ability to adapt to evolving consumer trends, embrace sustainable practices, and navigate regional regulatory landscapes effectively. Continuous innovation in product formulation, packaging, and distribution channels will be crucial for achieving sustained growth throughout the forecast period.

Asia Pacific Dog Food Market Segmentation

-

1. Pet Food Product

-

1.1. By Sub Product

-

1.1.1. Dry Pet Food

-

1.1.1.1. By Sub Dry Pet Food

- 1.1.1.1.1. Kibbles

- 1.1.1.1.2. Other Dry Pet Food

-

1.1.1.1. By Sub Dry Pet Food

- 1.1.2. Wet Pet Food

-

1.1.1. Dry Pet Food

-

1.2. Pet Nutraceuticals/Supplements

- 1.2.1. Milk Bioactives

- 1.2.2. Omega-3 Fatty Acids

- 1.2.3. Probiotics

- 1.2.4. Proteins and Peptides

- 1.2.5. Vitamins and Minerals

- 1.2.6. Other Nutraceuticals

-

1.3. Pet Treats

- 1.3.1. Crunchy Treats

- 1.3.2. Dental Treats

- 1.3.3. Freeze-dried and Jerky Treats

- 1.3.4. Soft & Chewy Treats

- 1.3.5. Other Treats

-

1.4. Pet Veterinary Diets

- 1.4.1. Diabetes

- 1.4.2. Digestive Sensitivity

- 1.4.3. Oral Care Diets

- 1.4.4. Renal

- 1.4.5. Urinary tract disease

- 1.4.6. Other Veterinary Diets

-

1.1. By Sub Product

-

2. Distribution Channel

- 2.1. Convenience Stores

- 2.2. Online Channel

- 2.3. Specialty Stores

- 2.4. Supermarkets/Hypermarkets

- 2.5. Other Channels

Asia Pacific Dog Food Market Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. Japan

- 1.3. South Korea

- 1.4. India

- 1.5. Australia

- 1.6. New Zealand

- 1.7. Indonesia

- 1.8. Malaysia

- 1.9. Singapore

- 1.10. Thailand

- 1.11. Vietnam

- 1.12. Philippines

Asia Pacific Dog Food Market Regional Market Share

Geographic Coverage of Asia Pacific Dog Food Market

Asia Pacific Dog Food Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.11% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Pet Food Product

- 5.1.1. By Sub Product

- 5.1.1.1. Dry Pet Food

- 5.1.1.1.1. By Sub Dry Pet Food

- 5.1.1.1.1.1. Kibbles

- 5.1.1.1.1.2. Other Dry Pet Food

- 5.1.1.1.1. By Sub Dry Pet Food

- 5.1.1.2. Wet Pet Food

- 5.1.1.1. Dry Pet Food

- 5.1.2. Pet Nutraceuticals/Supplements

- 5.1.2.1. Milk Bioactives

- 5.1.2.2. Omega-3 Fatty Acids

- 5.1.2.3. Probiotics

- 5.1.2.4. Proteins and Peptides

- 5.1.2.5. Vitamins and Minerals

- 5.1.2.6. Other Nutraceuticals

- 5.1.3. Pet Treats

- 5.1.3.1. Crunchy Treats

- 5.1.3.2. Dental Treats

- 5.1.3.3. Freeze-dried and Jerky Treats

- 5.1.3.4. Soft & Chewy Treats

- 5.1.3.5. Other Treats

- 5.1.4. Pet Veterinary Diets

- 5.1.4.1. Diabetes

- 5.1.4.2. Digestive Sensitivity

- 5.1.4.3. Oral Care Diets

- 5.1.4.4. Renal

- 5.1.4.5. Urinary tract disease

- 5.1.4.6. Other Veterinary Diets

- 5.1.1. By Sub Product

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Convenience Stores

- 5.2.2. Online Channel

- 5.2.3. Specialty Stores

- 5.2.4. Supermarkets/Hypermarkets

- 5.2.5. Other Channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Pet Food Product

- 6. Asia Pacific Dog Food Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Pet Food Product

- 6.1.1. By Sub Product

- 6.1.1.1. Dry Pet Food

- 6.1.1.1.1. By Sub Dry Pet Food

- 6.1.1.1.1.1. Kibbles

- 6.1.1.1.1.2. Other Dry Pet Food

- 6.1.1.1.1. By Sub Dry Pet Food

- 6.1.1.2. Wet Pet Food

- 6.1.1.1. Dry Pet Food

- 6.1.2. Pet Nutraceuticals/Supplements

- 6.1.2.1. Milk Bioactives

- 6.1.2.2. Omega-3 Fatty Acids

- 6.1.2.3. Probiotics

- 6.1.2.4. Proteins and Peptides

- 6.1.2.5. Vitamins and Minerals

- 6.1.2.6. Other Nutraceuticals

- 6.1.3. Pet Treats

- 6.1.3.1. Crunchy Treats

- 6.1.3.2. Dental Treats

- 6.1.3.3. Freeze-dried and Jerky Treats

- 6.1.3.4. Soft & Chewy Treats

- 6.1.3.5. Other Treats

- 6.1.4. Pet Veterinary Diets

- 6.1.4.1. Diabetes

- 6.1.4.2. Digestive Sensitivity

- 6.1.4.3. Oral Care Diets

- 6.1.4.4. Renal

- 6.1.4.5. Urinary tract disease

- 6.1.4.6. Other Veterinary Diets

- 6.1.1. By Sub Product

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Convenience Stores

- 6.2.2. Online Channel

- 6.2.3. Specialty Stores

- 6.2.4. Supermarkets/Hypermarkets

- 6.2.5. Other Channels

- 6.1. Market Analysis, Insights and Forecast - by Pet Food Product

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 ADM

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Affinity Petcare SA

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 PLB International

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Clearlake Capital Group L P (Wellness Pet Company Inc )

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 General Mills Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 IB Group (Drools Pet Food Pvt Ltd )

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Mars Incorporated

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Nestle (Purina)

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Colgate-Palmolive Company (Hill's Pet Nutrition Inc )

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Schell & Kampeter Inc (Diamond Pet Foods

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 ADM

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Asia Pacific Dog Food Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Asia Pacific Dog Food Market Share (%) by Company 2025

List of Tables

- Table 1: Asia Pacific Dog Food Market Revenue billion Forecast, by Pet Food Product 2020 & 2033

- Table 2: Asia Pacific Dog Food Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 3: Asia Pacific Dog Food Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Asia Pacific Dog Food Market Revenue billion Forecast, by Pet Food Product 2020 & 2033

- Table 5: Asia Pacific Dog Food Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 6: Asia Pacific Dog Food Market Revenue billion Forecast, by Country 2020 & 2033

- Table 7: China Asia Pacific Dog Food Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Japan Asia Pacific Dog Food Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: South Korea Asia Pacific Dog Food Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: India Asia Pacific Dog Food Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Australia Asia Pacific Dog Food Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: New Zealand Asia Pacific Dog Food Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Indonesia Asia Pacific Dog Food Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Malaysia Asia Pacific Dog Food Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Singapore Asia Pacific Dog Food Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Thailand Asia Pacific Dog Food Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Vietnam Asia Pacific Dog Food Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Philippines Asia Pacific Dog Food Market Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia Pacific Dog Food Market?

The projected CAGR is approximately 10.11%.

2. Which companies are prominent players in the Asia Pacific Dog Food Market?

Key companies in the market include ADM, Affinity Petcare SA, PLB International, Clearlake Capital Group L P (Wellness Pet Company Inc ), General Mills Inc, IB Group (Drools Pet Food Pvt Ltd ), Mars Incorporated, Nestle (Purina), Colgate-Palmolive Company (Hill's Pet Nutrition Inc ), Schell & Kampeter Inc (Diamond Pet Foods.

3. What are the main segments of the Asia Pacific Dog Food Market?

The market segments include Pet Food Product, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 17.85 billion as of 2022.

5. What are some drivers contributing to market growth?

Increased Demand for Meat; Initiatives By the Key Players; Focus on Animal nutrition and Health.

6. What are the notable trends driving market growth?

China and Japan were the major countries with increasing usage of commercial pet foods in the region.

7. Are there any restraints impacting market growth?

Shift Toward Vegan- Based Diet; Changing Raw Material Prices and Strict Government Rules to Restrict Market Growth.

8. Can you provide examples of recent developments in the market?

July 2023: Hill's Pet Nutrition introduced its new MSC (Marine Stewardship Council) certified pollock and insect protein products for pets with sensitive stomachs and skin lines. They contain vitamins, omega-3 fatty acids, and antioxidants.April 2023: Mars Incorporated opened its first pet food research and development center in Asia-Pacific. This new facility, called the APAC pet center, will support the company's product development.March 2023: Blue Buffalo, a subsidiary of General Mills Inc., launched its new high-protein dry dog food line, BLUE Wilderness Premier Blend. It is formulated with chicken and a blend of antioxidants, vitamins, and minerals.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia Pacific Dog Food Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia Pacific Dog Food Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia Pacific Dog Food Market?

To stay informed about further developments, trends, and reports in the Asia Pacific Dog Food Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence