Key Insights

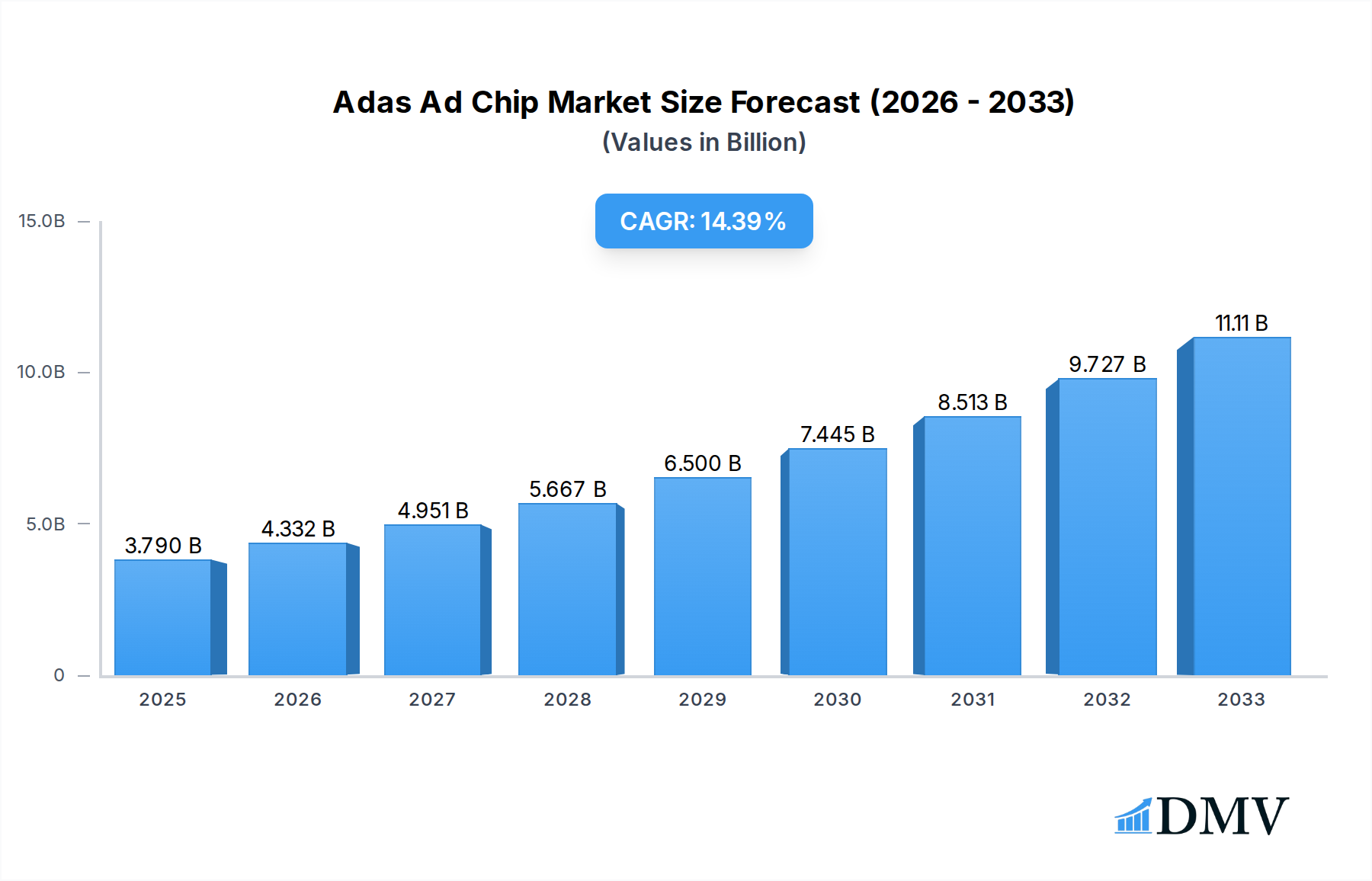

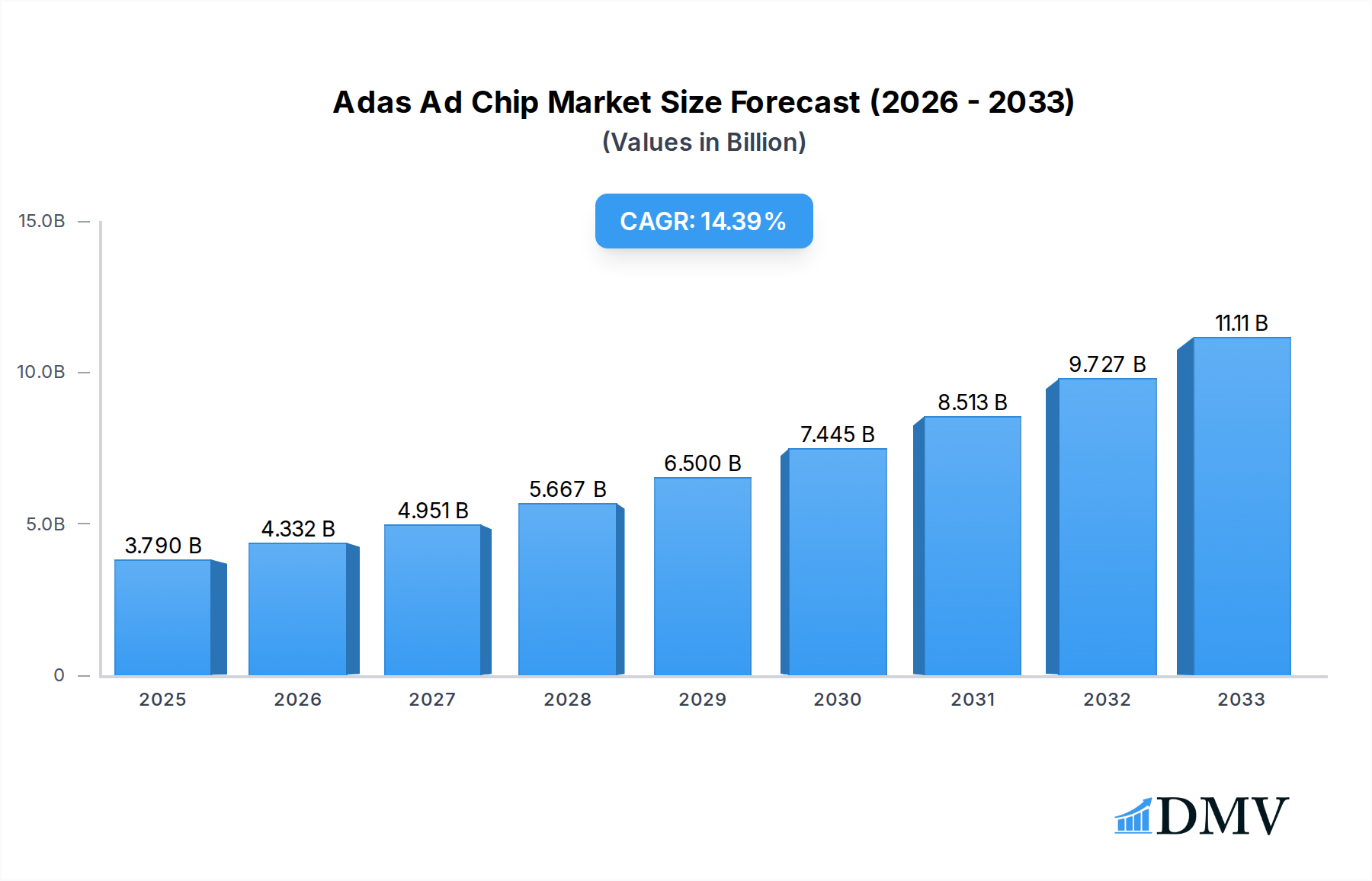

The global ADAS (Advanced Driver-Assistance Systems) AD Chip market is poised for significant expansion, projected to reach an estimated $3.79 billion in 2025. This robust growth is underpinned by a remarkable Compound Annual Growth Rate (CAGR) of 14.3% anticipated from 2025 to 2033. This surge is primarily driven by the escalating demand for enhanced vehicle safety features, the increasing adoption of autonomous driving technologies, and stringent government regulations mandating ADAS functionalities. The continuous innovation in processing power and specialized architectures like GPUs, FPGAs, and ASICs is further fueling market penetration across both commercial vehicles and passenger cars. Key players are heavily investing in research and development to deliver more sophisticated and cost-effective solutions, enabling widespread integration of ADAS features.

Adas Ad Chip Market Size (In Billion)

Emerging trends such as the integration of AI and machine learning into ADAS chips, the development of sensor fusion capabilities for improved environmental perception, and the evolution towards higher levels of automation are shaping the competitive landscape. The market's growth trajectory is also supported by increasing consumer awareness and demand for advanced safety and convenience features. While the market benefits from strong drivers, potential restraints include the high cost of development and implementation of cutting-edge ADAS technologies, as well as challenges related to data security and privacy concerns. Despite these hurdles, the overarching push towards safer and more intelligent mobility solutions, coupled with significant technological advancements, ensures a dynamic and promising future for the ADAS AD Chip market.

Adas Ad Chip Company Market Share

This in-depth report offers a definitive analysis of the ADAS AD Chip market, projecting its trajectory from 2019 through 2033, with a base and estimated year of 2025 and a forecast period from 2025 to 2033. Delve into the intricate market dynamics, from technology evolution and regional dominance to the strategic plays of key industry giants. Our research encompasses the entire spectrum of ADAS AD Chip applications, including Commercial Vehicle and Passenger Car segments, and analyzes the impact of various chip types such as GPU, FPGA, ASIC, and Others. Discover the critical trends shaping this multi-billion dollar industry and gain actionable insights for your business strategy.

Adas Ad Chip Market Composition & Trends

The ADAS AD Chip market is characterized by a dynamic composition driven by relentless innovation and evolving regulatory landscapes. Market concentration is a key feature, with dominant players like NVIDIA, Qualcomm, and Mobileye spearheading technological advancements. The study meticulously examines innovation catalysts, including the increasing demand for sophisticated sensor fusion, AI-driven decision-making, and enhanced processing power for autonomous driving features. Regulatory frameworks across major automotive markets are increasingly mandating advanced safety features, directly impacting ADAS AD Chip adoption. Substitute products, while present, are largely outpaced by the specialized performance offered by dedicated ADAS chips. End-user profiles are diverse, ranging from major OEMs focused on integrating advanced driver-assistance systems into their latest models to Tier 1 suppliers developing modular solutions. Merger and acquisition (M&A) activities are significant, with multi-billion dollar deals reshaping the competitive ecosystem as companies seek to consolidate expertise and expand market reach. For instance, M&A deal values in the past five years have collectively amounted to over xxx billion, indicating a robust consolidation trend. Key players are strategically acquiring smaller, innovative firms to bolster their portfolios and accelerate time-to-market for next-generation ADAS solutions. The market share distribution highlights the intense competition and the constant pursuit of technological superiority.

Adas Ad Chip Industry Evolution

The evolution of the ADAS AD Chip industry is a compelling narrative of technological ambition and market expansion, projected to reach astronomical figures within the forecast period. From 2019 to 2024, the industry witnessed significant foundational growth, fueled by increasing consumer awareness of vehicle safety and the initial rollout of advanced driver-assistance features. The base year of 2025 marks a pivotal point, with the market projected to be valued at approximately xxx billion, driven by the widespread adoption of Level 2 and Level 3 autonomous driving functionalities. Technological advancements have been the primary engine of this evolution. The transition from simpler processing units to highly integrated System-on-Chips (SoCs) incorporating powerful GPUs, NPUs (Neural Processing Units), and specialized ASICs has enabled more complex algorithms for object detection, path planning, and decision-making. Furthermore, advancements in deep learning and artificial intelligence have unlocked new capabilities, allowing ADAS systems to interpret intricate environmental data with unprecedented accuracy. Consumer demand has shifted dramatically, with a growing preference for vehicles equipped with advanced safety features becoming a key purchasing criterion. This demand is further amplified by the escalating pursuit of higher levels of vehicle autonomy, pushing the boundaries of what ADAS technologies can achieve. By 2033, the market is anticipated to reach an astounding xxx billion, reflecting the full integration of sophisticated ADAS capabilities across the automotive spectrum and paving the way for widespread Level 4 and Level 5 autonomy. The average annual growth rate for the forecast period is estimated at xx.xx%, underscoring the sustained upward trajectory of this critical sector.

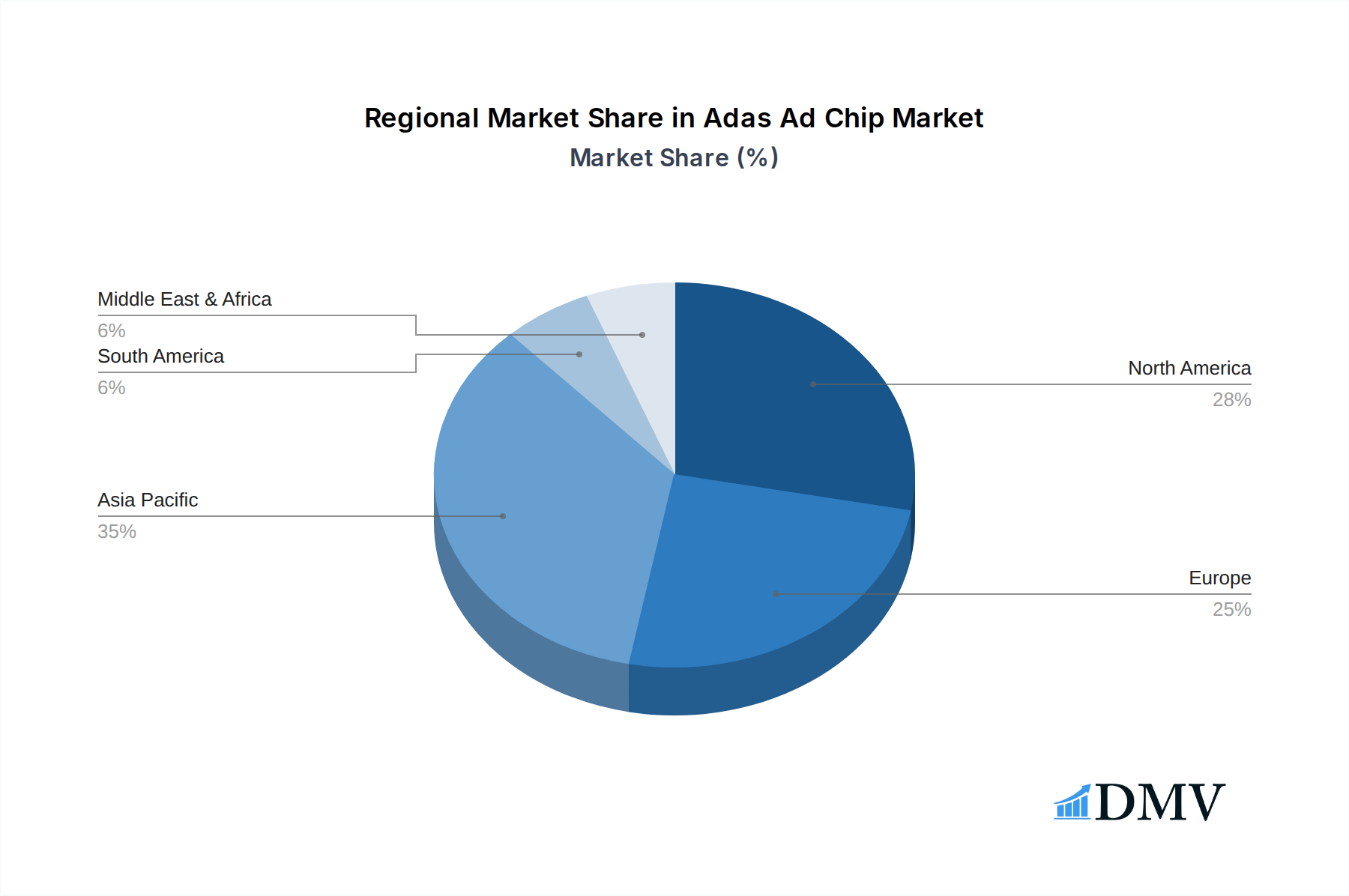

Leading Regions, Countries, or Segments in Adas Ad Chip

The global ADAS AD Chip market demonstrates distinct leadership across various regions and segments, driven by a confluence of technological investment, supportive regulatory environments, and robust consumer adoption. North America stands out as a leading region, characterized by significant investment trends from major automotive manufacturers and a strong consumer appetite for cutting-edge automotive technology. The country's proactive stance on vehicle safety standards and a well-established automotive research and development ecosystem have fostered rapid adoption of ADAS features. Within the Application segment, Passenger Car dominates the market, accounting for an estimated xx% of the total market share in 2025. This dominance is attributed to the high volume of passenger vehicle production and the increasing integration of ADAS functionalities as standard or optional features across various trim levels. The consumer preference for enhanced safety and convenience in personal vehicles acts as a powerful catalyst. In terms of Type, ASIC chips are emerging as a dominant force, projected to capture over xx% of the market by 2033. Their specialized architecture, optimized for specific ADAS tasks like object recognition and sensor fusion, offers superior performance and power efficiency compared to general-purpose processors. Key drivers for ASIC dominance include their ability to handle complex AI algorithms efficiently, crucial for real-time decision-making in autonomous systems, and their cost-effectiveness in high-volume production scenarios. Regulatory support, exemplified by evolving safety mandates and incentive programs for adopting advanced automotive technologies, further solidifies the leadership of these segments. Continuous R&D investment by companies like NVIDIA, Qualcomm, and Mobileye in developing more powerful and efficient ASICs specifically for ADAS applications is a critical factor propelling their market penetration. The substantial growth in the Commercial Vehicle segment, however, is also noteworthy, driven by safety regulations and the potential for operational efficiency gains through autonomous driving technologies.

Adas Ad Chip Product Innovations

Product innovation in the ADAS AD Chip market is characterized by a relentless pursuit of enhanced processing power, improved energy efficiency, and greater integration of artificial intelligence capabilities. Companies are developing sophisticated SoCs that integrate multiple processing units, including high-performance GPUs for real-time image processing and NPUs optimized for deep learning inference. These advancements enable ADAS systems to process vast amounts of sensor data from cameras, radar, and LiDAR with unprecedented speed and accuracy, leading to more robust object detection, tracking, and prediction. The unique selling propositions of these next-generation chips lie in their ability to support higher levels of autonomy, reduce latency, and minimize power consumption, crucial for mass-market adoption. Specific technological advancements include the development of specialized neural network accelerators and the implementation of advanced power management techniques. The focus is on creating comprehensive, scalable solutions that can support a wide range of ADAS features, from basic driver assistance to fully autonomous driving capabilities.

Propelling Factors for Adas Ad Chip Growth

The growth of the ADAS AD Chip market is propelled by a confluence of critical factors. Technological advancements are paramount, with continuous innovation in AI, machine learning, and sensor fusion enabling more sophisticated and reliable ADAS functionalities. The increasing demand for vehicle safety is a significant driver, as governments and consumers alike prioritize features that reduce accidents and enhance occupant protection. Economic factors, including the growing disposable income in key markets and the decreasing cost of advanced electronics, are making ADAS features more accessible. Furthermore, supportive regulatory landscapes worldwide, with mandates for advanced safety systems, are accelerating adoption. The pursuit of autonomous driving, from partial to full autonomy, is a long-term catalyst, pushing the boundaries of ADAS chip capabilities. Investments by major automotive OEMs and Tier 1 suppliers in R&D further fuel this growth trajectory.

Obstacles in the Adas Ad Chip Market

Despite its robust growth, the ADAS AD Chip market faces several obstacles. Regulatory challenges persist, with varying standards and certification processes across different regions creating complexity for global manufacturers. Supply chain disruptions, as witnessed in recent years, can significantly impact production and lead times, leading to cost overruns and project delays. Intense competitive pressures necessitate substantial R&D investments, making it challenging for smaller players to compete with established giants. The high cost of advanced ADAS chips can also be a barrier to widespread adoption, particularly in price-sensitive segments. Furthermore, consumer perception and trust regarding the reliability and safety of autonomous driving technologies need continuous cultivation. Addressing these challenges effectively will be crucial for sustained market expansion.

Future Opportunities in Adas Ad Chip

The ADAS AD Chip market is poised for significant future opportunities. The ongoing evolution towards higher levels of autonomous driving (Level 4 and Level 5) presents a substantial growth avenue, requiring even more sophisticated and powerful processing capabilities. The expansion of ADAS into emerging markets, where vehicle safety regulations are becoming more stringent, offers vast untapped potential. The development of specialized ADAS chips for specific applications, such as commercial vehicles, last-mile delivery robots, and even off-road machinery, will open new market niches. Furthermore, the integration of V2X (Vehicle-to-Everything) communication capabilities into ADAS chips will enable enhanced situational awareness and cooperative driving. Opportunities also lie in the development of more energy-efficient chips to support the growing trend of electric vehicles and in providing software-defined ADAS solutions that can be updated remotely.

Major Players in the Adas Ad Chip Ecosystem

- NVIDIA

- Qualcomm

- Mobileye

- Tesla

- Huawei

- Horizon Robotics

- Black Sesame Technologies

- SemiDrive

- TI

- Renesas

- Infineon

- SiEngine Technology

Key Developments in Adas Ad Chip Industry

- 2023/08: NVIDIA announces new generation of automotive SoCs with advanced AI capabilities, boosting performance for autonomous driving systems.

- 2023/07: Qualcomm launches its next-generation Snapdragon Ride platform, focusing on scalable ADAS solutions for a wider range of vehicles.

- 2023/06: Mobileye unveils its EyeQ Ultra™ chip, designed for Level 4 and Level 5 autonomous driving, featuring over 130 TOPS of processing power.

- 2023/05: Huawei showcases its advanced automotive chip solutions, emphasizing its commitment to the intelligent vehicle ecosystem.

- 2023/04: Horizon Robotics partners with a major Chinese automaker to integrate its ADAS solutions into upcoming vehicle models.

- 2023/03: Black Sesame Technologies announces a strategic collaboration to accelerate the development of high-performance automotive processors.

- 2023/02: SemiDrive releases new automotive-grade microcontrollers designed for safety-critical ADAS applications.

- 2023/01: Texas Instruments (TI) expands its portfolio of ADAS-focused processors, offering enhanced performance and power efficiency.

- 2022/12: Renesas Electronics announces advancements in its R-Car system-on-chips, enhancing capabilities for advanced driver-assistance systems.

- 2022/11: Infineon Technologies strengthens its position in automotive sensing and processing with new product introductions for ADAS.

- 2022/10: SiEngine Technology unveils its latest automotive SoC, targeting the burgeoning intelligent driving market.

Strategic Adas Ad Chip Market Forecast

The strategic ADAS AD Chip market forecast indicates a future driven by accelerating technological advancements, increasing regulatory mandates, and a robust consumer demand for enhanced safety and convenience. The forecast period (2025–2033) is expected to witness exponential growth, fueled by the widespread adoption of Level 3 and higher autonomous driving capabilities in both passenger cars and commercial vehicles. Key growth catalysts include continued innovation in AI and machine learning, leading to more predictive and responsive ADAS systems. The expanding ecosystem of automotive suppliers and OEMs actively investing in next-generation intelligent vehicle technologies will further solidify market expansion. Emerging opportunities in vehicle-to-everything (V2X) communication and specialized ADAS applications will create new revenue streams. The market is anticipated to reach unprecedented valuation, driven by the inherent value proposition of safer, more efficient, and increasingly autonomous transportation.

Adas Ad Chip Segmentation

-

1. Application

- 1.1. Commercial Vehicle

- 1.2. Passenger Car

-

2. Type

- 2.1. GPU

- 2.2. FPGA

- 2.3. ASIC

- 2.4. Others

Adas Ad Chip Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Adas Ad Chip Regional Market Share

Geographic Coverage of Adas Ad Chip

Adas Ad Chip REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Commercial Vehicle

- 5.1.2. Passenger Car

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. GPU

- 5.2.2. FPGA

- 5.2.3. ASIC

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Adas Ad Chip Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Commercial Vehicle

- 6.1.2. Passenger Car

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. GPU

- 6.2.2. FPGA

- 6.2.3. ASIC

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Adas Ad Chip Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Commercial Vehicle

- 7.1.2. Passenger Car

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. GPU

- 7.2.2. FPGA

- 7.2.3. ASIC

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Adas Ad Chip Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Commercial Vehicle

- 8.1.2. Passenger Car

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. GPU

- 8.2.2. FPGA

- 8.2.3. ASIC

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Adas Ad Chip Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Commercial Vehicle

- 9.1.2. Passenger Car

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. GPU

- 9.2.2. FPGA

- 9.2.3. ASIC

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Adas Ad Chip Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Commercial Vehicle

- 10.1.2. Passenger Car

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. GPU

- 10.2.2. FPGA

- 10.2.3. ASIC

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Adas Ad Chip Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Commercial Vehicle

- 11.1.2. Passenger Car

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. GPU

- 11.2.2. FPGA

- 11.2.3. ASIC

- 11.2.4. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 NVIDIA

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Qualcomm

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Mobileye

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Tesla

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Huawei

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Horizon Robotics

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Black Sesame Technologies

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 SemiDrive

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 TI

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Renesas

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Infineon

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 SiEngine Technology

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 NVIDIA

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Adas Ad Chip Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Adas Ad Chip Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Adas Ad Chip Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Adas Ad Chip Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Adas Ad Chip Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Adas Ad Chip Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Adas Ad Chip Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Adas Ad Chip Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Adas Ad Chip Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Adas Ad Chip Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Adas Ad Chip Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Adas Ad Chip Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Adas Ad Chip Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Adas Ad Chip Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Adas Ad Chip Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Adas Ad Chip Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Adas Ad Chip Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Adas Ad Chip Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Adas Ad Chip Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Adas Ad Chip Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Adas Ad Chip Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Adas Ad Chip Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Adas Ad Chip Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Adas Ad Chip Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Adas Ad Chip Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Adas Ad Chip Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Adas Ad Chip Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Adas Ad Chip Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Adas Ad Chip Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Adas Ad Chip Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Adas Ad Chip Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Adas Ad Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Adas Ad Chip Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Adas Ad Chip Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Adas Ad Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Adas Ad Chip Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Adas Ad Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Adas Ad Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Adas Ad Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Adas Ad Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Adas Ad Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Adas Ad Chip Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Adas Ad Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Adas Ad Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Adas Ad Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Adas Ad Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Adas Ad Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Adas Ad Chip Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Adas Ad Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Adas Ad Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Adas Ad Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Adas Ad Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Adas Ad Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Adas Ad Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Adas Ad Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Adas Ad Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Adas Ad Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Adas Ad Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Adas Ad Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Adas Ad Chip Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Adas Ad Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Adas Ad Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Adas Ad Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Adas Ad Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Adas Ad Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Adas Ad Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Adas Ad Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Adas Ad Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Adas Ad Chip Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Adas Ad Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Adas Ad Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Adas Ad Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Adas Ad Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Adas Ad Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Adas Ad Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Adas Ad Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Adas Ad Chip Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Adas Ad Chip?

The projected CAGR is approximately 14.3%.

2. Which companies are prominent players in the Adas Ad Chip?

Key companies in the market include NVIDIA, Qualcomm, Mobileye, Tesla, Huawei, Horizon Robotics, Black Sesame Technologies, SemiDrive, TI, Renesas, Infineon, SiEngine Technology.

3. What are the main segments of the Adas Ad Chip?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Adas Ad Chip," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Adas Ad Chip report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Adas Ad Chip?

To stay informed about further developments, trends, and reports in the Adas Ad Chip, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence