Key Insights

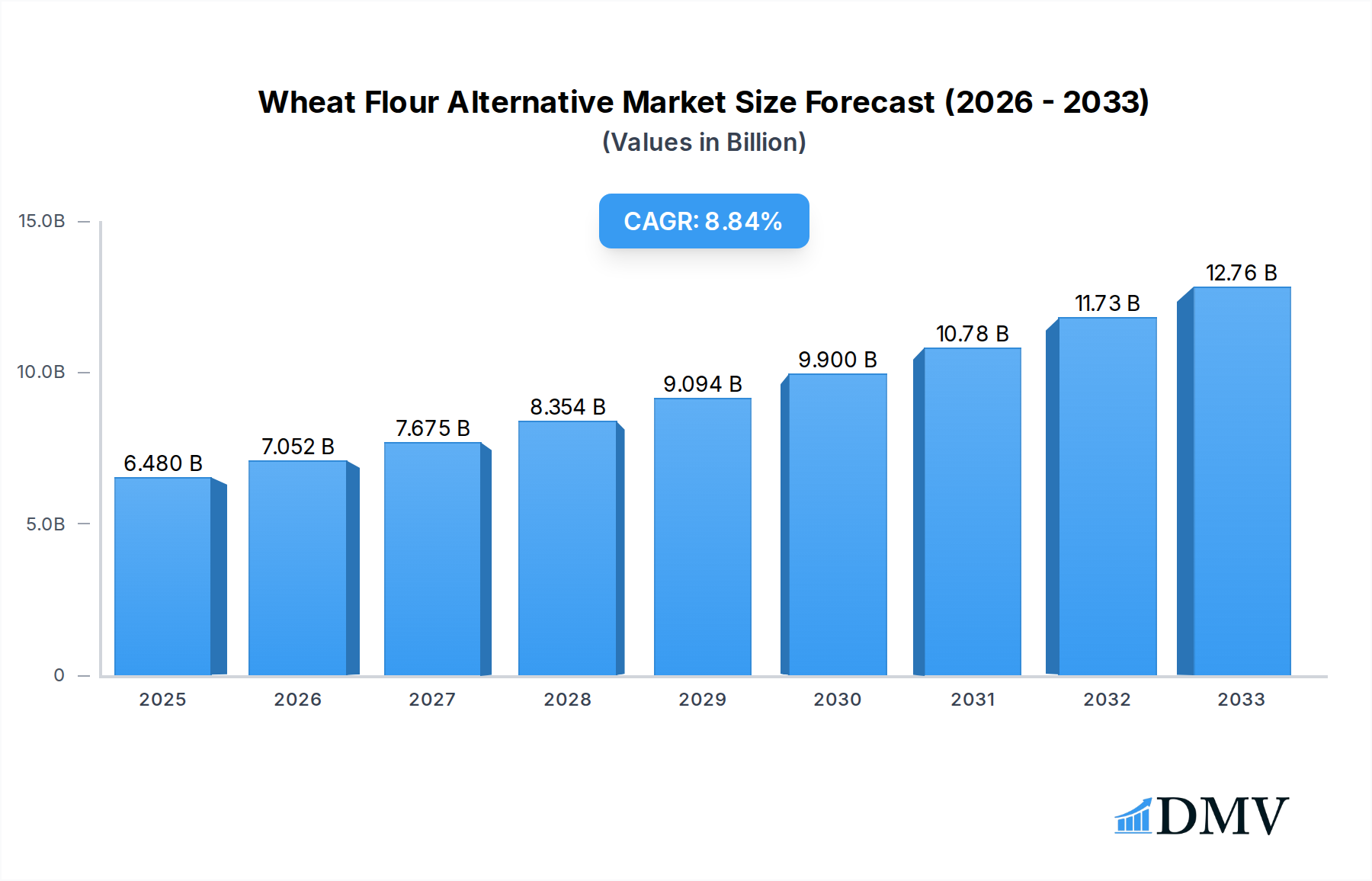

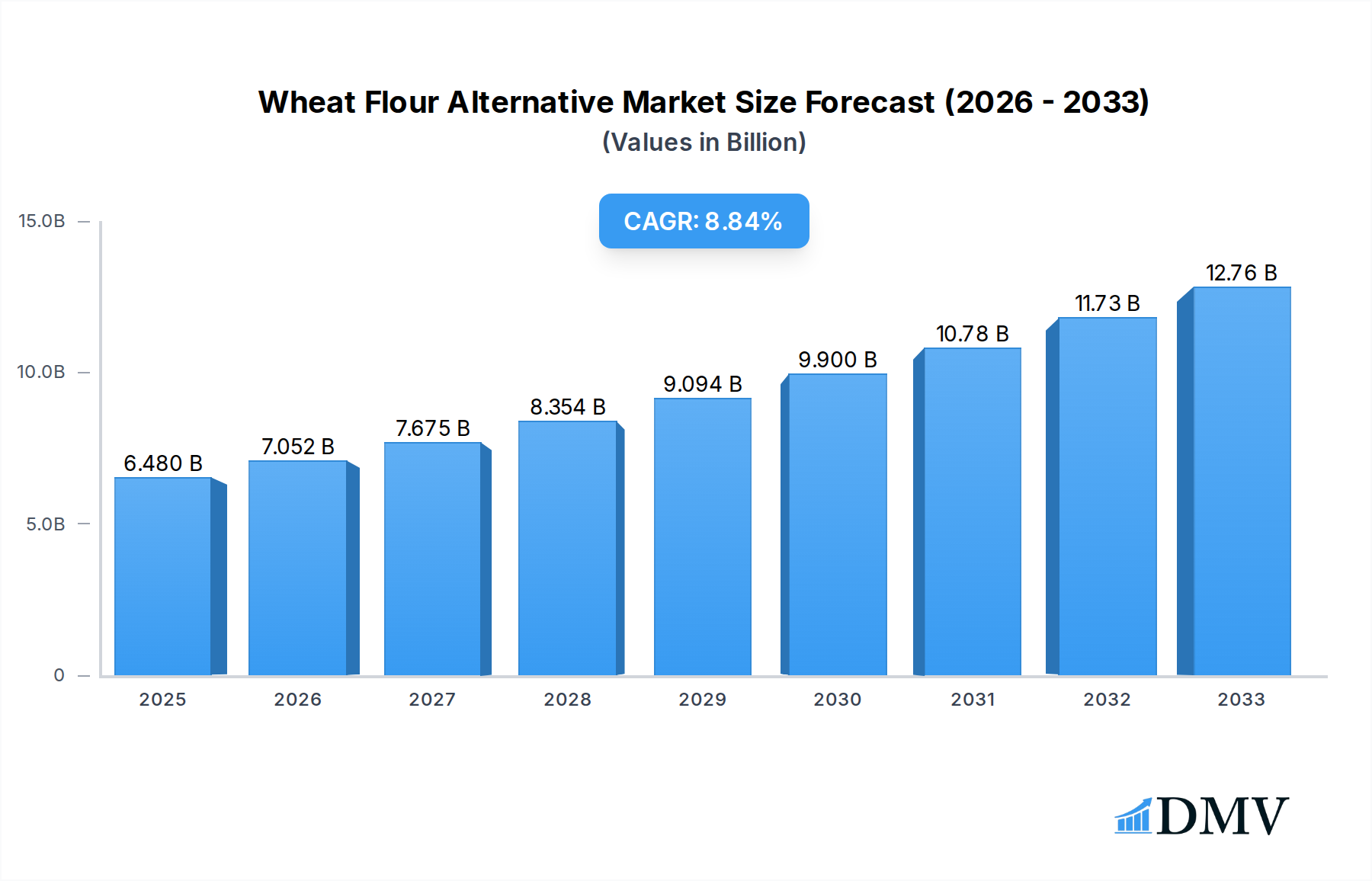

The global wheat flour alternative market is experiencing robust expansion, driven by a confluence of evolving consumer preferences and dietary shifts. Valued at an estimated $6.48 billion in 2025, this market is projected to grow at an impressive Compound Annual Growth Rate (CAGR) of 8.85% through 2033. A primary catalyst for this surge is the increasing awareness and diagnosis of gluten intolerance and celiac disease, propelling demand for gluten-free options. Simultaneously, the rising popularity of plant-based diets, ketogenic lifestyles, and general healthy eating trends has broadened the appeal for diverse flour types beyond traditional wheat. Innovations in product development by leading companies, alongside a growing appreciation for functional food ingredients, are further fueling market momentum, particularly in applications like baked goods, noodles, pastries, and fried foods where alternative flours offer distinct nutritional and textural benefits.

Wheat Flour Alternative Market Size (In Billion)

Key market trends point towards a significant diversification in product offerings, with specialty flours such as quinoa, almond, sweet potato, and ancient grain varieties gaining considerable traction. Consumers are increasingly seeking clean label products and natural ingredients, which alternative flours often provide. While the higher cost of these specialty flours compared to conventional wheat and the challenges in replicating the precise functional properties of gluten in some applications pose minor restraints, ongoing research and development are consistently improving their versatility and performance. Major industry players like ADM, Bunge, Cargill, and Wilmar International, alongside specialized ingredient providers such as NorQuin and Andean Valley Corporation, are actively innovating and expanding their portfolios to meet this escalating demand across North America, Europe, and the rapidly growing Asia Pacific region.

Wheat Flour Alternative Company Market Share

SEO Keywords: Wheat Flour Alternative Market, Gluten-Free Flour, Plant-Based Flour, Healthy Eating Trends, Food Industry Analysis, Market Growth Forecast, Consumer Preferences, Sustainable Food, Food Innovation, Corn Flour, Rice Flour, Sweet Potato Flour, Quinoa Flour, Almond Flour, Global Food Market, Future Food Trends, Baking Ingredients.

The global demand for Wheat Flour Alternative products is surging, driven by evolving consumer dietary preferences, increased awareness of gluten sensitivities, and a robust push towards healthier, plant-based lifestyles. This comprehensive report meticulously dissects the multifaceted Wheat Flour Alternative Market, offering unparalleled insights into its current landscape and future trajectories. From the rising popularity of gluten-free flour to the innovative applications across various food segments like Baked Goods, Noodles, and Pastry, stakeholders across the food ecosystem are seeking definitive data to navigate this dynamic market. Our analysis spans the Study Period: 2019–2033, with a Base Year: 2025, an Estimated Year: 2025, and a robust Forecast Period: 2025–2033, leveraging Historical Period: 2019–2024 data to project future growth with precision.

This report is an indispensable resource for producers, investors, food innovators, and policymakers seeking to capitalize on the plant-based food movement. It explores critical market dynamics, pinpoints growth opportunities, and illuminates potential challenges, ensuring a strategic advantage in a competitive and rapidly expanding industry. Discover the pivotal role of Corn Flour, Rice Flour, Sweet Potato Flour, Quinoa Flour, and Almond Flour in shaping consumer choices and driving market expansion.

Wheat Flour Alternative Market Composition & Trends

The Wheat Flour Alternative Market exhibits a diverse and evolving composition, characterized by intense innovation and a gradual shift in market concentration. While the market has traditionally seen dominance from a few large players like ADM and Cargill, a surge of specialized producers such as Milne MicroDried and Carolina Innovative Food Ingredients are rapidly gaining traction, fostering a more fragmented yet highly competitive landscape. Innovation catalysts include advancements in processing technologies that enhance texture and flavor profiles of alternative flours, coupled with a strong regulatory push towards transparent labeling and healthier food options. The market is also heavily influenced by the rise of substitute products beyond traditional wheat, with novel legume and seed flours constantly emerging. End-user profiles are expanding, moving beyond individuals with celiac disease to a broader demographic seeking wellness and dietary diversity.

- Market Concentration: The top five players, including ADM, Bunge, and Cargill, collectively commanded an estimated market value of xx billion in 2025, representing a significant but decreasing share as smaller, agile companies innovate.

- Innovation Catalysts: Investment in R&D for enhanced sensory attributes and nutritional fortification has exceeded xx billion annually, driving new product introductions.

- Regulatory Landscapes: Global regulations concerning gluten-free certification and ingredient sourcing have fostered consumer trust, contributing to a market value increase of xx billion.

- Substitute Products: The introduction of flours from novel sources like ancient grains and root vegetables has diversified consumer choices, impacting traditional alternative flour segments by xx billion annually.

- End-User Profiles: The segment of health-conscious consumers without specific dietary restrictions now accounts for an estimated xx billion in market revenue, indicating a broad appeal beyond allergen avoidance.

- M&A Activities: The Historical Period: 2019–2024 witnessed over 15 significant mergers and acquisitions, with deal values collectively exceeding xx billion, aimed at consolidating supply chains, expanding product portfolios, and capturing niche markets. A notable acquisition in 2023 was valued at xx billion, signifying growing investor confidence.

Wheat Flour Alternative Industry Evolution

The Wheat Flour Alternative Industry is undergoing a profound evolution, marked by accelerated market growth trajectories, groundbreaking technological advancements, and rapidly shifting consumer demands. Historically, the market was primarily driven by the niche needs of individuals with celiac disease or gluten intolerance. However, the last decade, particularly during the Historical Period: 2019–2024, has seen a dramatic expansion, propelled by a broader consumer embrace of healthier eating, sustainable food practices, and experimental culinary trends. The market size, valued at an estimated xx billion in 2025, is projected to reach xx billion by 2033, demonstrating a Compound Annual Growth Rate (CAGR) of xx%. This robust growth is not merely volumetric but also reflects a deepening market penetration across various geographies and demographic segments.

Technological advancements have been pivotal in this evolution. Innovations in milling techniques now allow for finer textures and improved functional properties in alternative flours, closely mimicking the baking characteristics of wheat flour. For instance, advanced processing of Rice Flour and Almond Flour has significantly enhanced their applicability in mainstream baking. Furthermore, the development of blends that combine the best attributes of different alternative flours (e.g., the elasticity of Corn Flour with the nutrient profile of Quinoa Flour) has unlocked new product possibilities. Enzyme technology and fermentation processes are also being leveraged to improve the sensory profiles and shelf life of these flours, addressing previous limitations. These technological leaps have reduced the cost of production for certain alternatives, making them more accessible and competitive.

Shifting consumer demands are the ultimate engine driving this evolution. Beyond gluten-free, consumers are actively seeking products that offer additional health benefits, such as high protein content, increased fiber, and lower glycemic index. The demand for naturally sourced, non-GMO, and organic alternative flours has surged, with the premium segment growing by xx billion annually. The rise of veganism and flexitarian diets has further fueled the adoption of plant-based flour options. Consumers are also becoming more adventurous in their culinary choices, experimenting with exotic flours like Sweet Potato Flour and seeking products that offer unique flavor profiles and textures. Digital platforms and social media have played a significant role in disseminating information about these alternative flours, leading to higher adoption metrics. The online retail adoption rate for specialty alternative flours has seen an increase of xx% over the past five years, contributing an additional xx billion to market revenue, demonstrating a clear shift in purchasing habits and market engagement during the Forecast Period: 2025–2033.

Leading Regions, Countries, or Segments in Wheat Flour Alternative

The Wheat Flour Alternative Market exhibits distinct leadership across various dimensions, with the Baked Goods application segment, particularly in North America, currently holding a dominant position. This segment, encompassing breads, cakes, cookies, and pastries made with alternatives like Rice Flour, Almond Flour, and Quinoa Flour, represents the largest revenue share, estimated at xx billion in 2025, and is projected to maintain its lead throughout the Forecast Period: 2025–2033. The widespread consumer demand for gluten-free baked goods, coupled with continuous innovation from manufacturers like GoodMills Group and Jinshahe Group, underpins this dominance.

- Key Drivers for Baked Goods Dominance:

- High Consumer Acceptance: Baked goods are a primary entry point for consumers experimenting with wheat flour alternatives, driven by familiar product forms.

- Extensive R&D: Significant investment in developing blends and processing techniques to replicate the texture and flavor of traditional wheat-based baked goods.

- Retail Accessibility: A robust distribution network ensures wide availability in supermarkets, specialty stores, and online platforms.

- Marketing & Education: Effective campaigns have raised awareness about the health benefits and culinary versatility of alternative flours in baking.

- Investment Trends: Venture capital and private equity investments in gluten-free bakeries and ingredient suppliers have collectively surpassed xx billion during the Historical Period: 2019–2024.

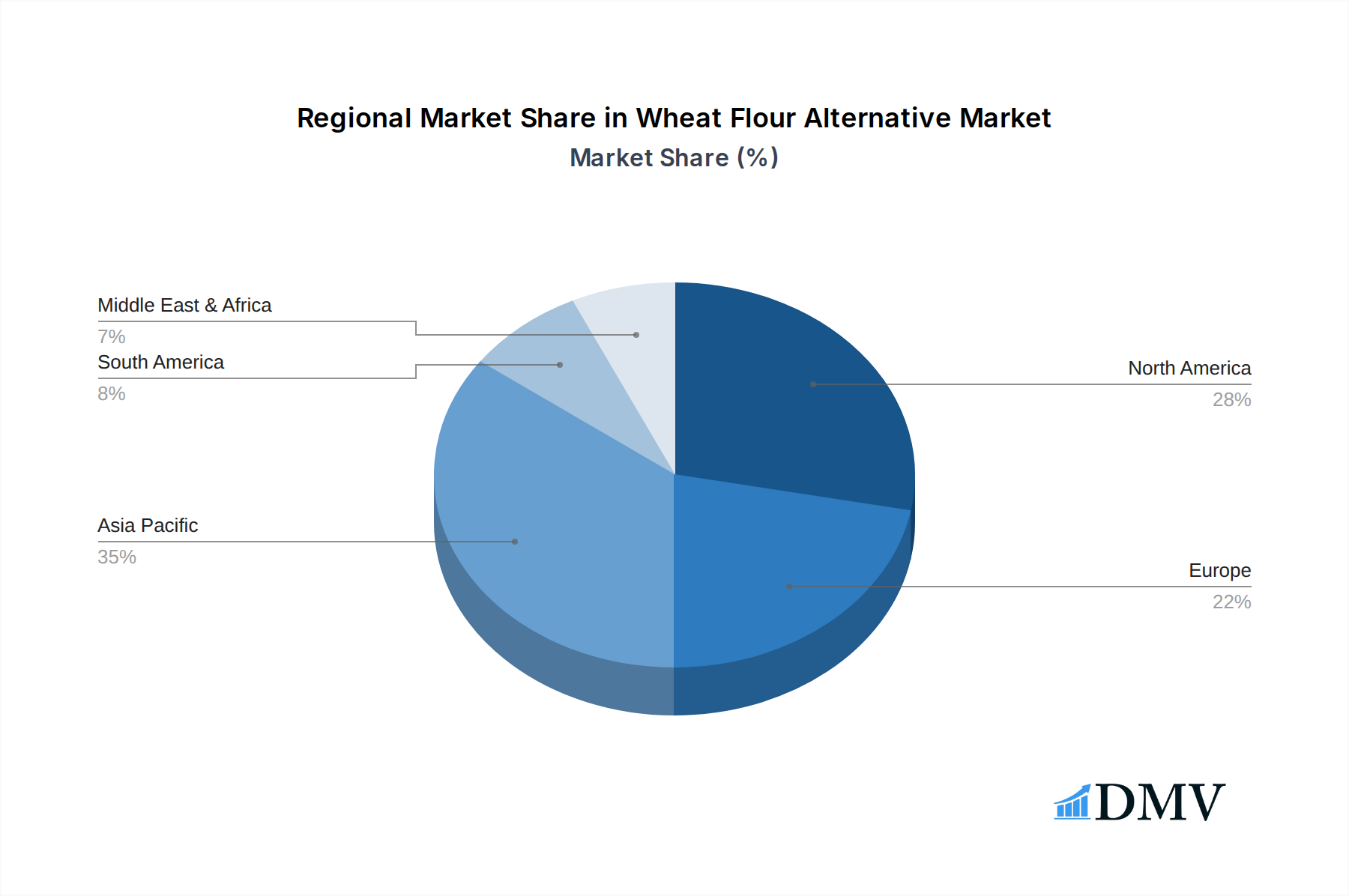

Geographically, North America, specifically the United States, stands out as a leading market. This is attributable to a high prevalence of celiac disease and gluten sensitivity, coupled with a strong health and wellness trend. Regulatory support for gluten-free labeling and extensive marketing by major food companies have further bolstered market penetration. Consumers in the region are highly receptive to new product introductions and are willing to pay a premium for perceived health benefits. The market here is also characterized by strong purchasing power and a vibrant ecosystem of health food stores and online retailers. The revenue generated from North America alone is estimated at xx billion in 2025, with a projected growth to xx billion by 2033. The continuous innovation by regional players like Carolina Innovative Food Ingredients and NorQuin has cemented this leadership.

Among the types of flours, Rice Flour and Almond Flour are currently the leading segments, collectively accounting for an estimated market value of xx billion. Rice flour benefits from its neutral flavor, versatility, and cost-effectiveness, making it a staple in many gluten-free products. Almond flour, while more expensive, is highly valued for its nutrient density, low glycemic index, and superior baking properties, especially in premium and keto-friendly products. These segments are supported by consistent consumer demand and continuous product refinement by leading suppliers.

Wheat Flour Alternative Product Innovations

The Wheat Flour Alternative Market is a hotbed of innovation, continually introducing novel flours and blends designed to overcome traditional limitations while enhancing nutritional profiles and sensory experiences. Recent advancements focus on improving texture, elasticity, and flavor neutrality, making alternative flours increasingly indistinguishable from their wheat counterparts in various applications. For instance, advanced milling techniques for Sweet Potato Flour have yielded finer grinds that integrate seamlessly into Pastry and Fried Food, offering natural sweetness and a vibrant color without compromising structural integrity. Companies like Milne MicroDried are pioneering proprietary drying methods to create highly functional fruit and vegetable flours with extended shelf life and enhanced nutrient retention. The development of multi-grain and seed-based blends, often featuring Quinoa Flour and specialized Corn Flour varieties, provides unique selling propositions by delivering comprehensive amino acid profiles and high fiber content. Performance metrics are consistently improving, with new formulations achieving up to xx% better rise in baked goods and xx% greater crispness in fried applications, thereby expanding their culinary versatility and appealing to a broader consumer base seeking both health and uncompromising taste.

Propelling Factors for Wheat Flour Alternative Growth

The growth of the Wheat Flour Alternative Market is propelled by a confluence of powerful drivers. Technologically, innovations in processing, such as micronization and fermentation, are enhancing the functional properties and sensory profiles of alternative flours, making them more palatable and versatile for applications in Baked Goods and Noodles. Economically, rising disposable incomes in emerging markets and increasing consumer willingness to pay a premium for healthier, specialty food items are significantly boosting market value, contributing an estimated xx billion to annual growth. Furthermore, the growing awareness of celiac disease, gluten sensitivity, and other food intolerances is expanding the consumer base exponentially. Regulatory influences, including clearer labeling requirements for gluten-free products across major economies, instill consumer trust and facilitate market entry for new products. The surging global demand for plant-based food options and the widespread adoption of specific diets (e.g., keto, paleo) that often exclude wheat, are also primary catalysts, collectively driving market expansion by an additional xx billion.

Obstacles in the Wheat Flour Alternative Market

Despite its robust growth, the Wheat Flour Alternative Market faces several significant obstacles. Regulatory challenges, particularly concerning ingredient sourcing and allergen cross-contamination, can impede product development and market expansion. Stringent labeling requirements, though beneficial for consumers, can increase compliance costs for manufacturers by an estimated xx million annually. Supply chain disruptions, often due to climate change impacting crop yields for ingredients like almonds or quinoa, lead to price volatility and inconsistent availability, potentially causing xx billion in lost sales across the industry during peak demand. Moreover, the higher production costs and complex processing often associated with alternative flours result in premium pricing compared to conventional wheat flour, deterring price-sensitive consumers. Intense competitive pressures from established brands and new entrants, coupled with the ongoing need to replicate the unique functional properties of wheat gluten, present considerable R&D hurdles, requiring investments of over xx billion to develop superior product formulations.

Future Opportunities in Wheat Flour Alternative

The Wheat Flour Alternative Market is ripe with future opportunities, driven by evolving consumer trends and technological advancements. Untapped markets in developing regions, where awareness of gluten-free and plant-based diets is growing, present immense potential, offering an estimated market expansion of xx billion by 2033. Breakthroughs in biotechnology and precision agriculture promise to yield novel flour sources with enhanced nutritional profiles and functional properties, opening doors for entirely new product categories. The increasing demand for sustainable and ethically sourced ingredients will create significant opportunities for companies investing in regenerative farming practices and transparent supply chains, potentially adding xx billion to market value. Furthermore, the burgeoning demand for personalized nutrition and functional foods offers avenues for developing alternative flours fortified with specific vitamins, minerals, or probiotics, catering to highly targeted consumer segments and creating premium product lines.

Major Players in the Wheat Flour Alternative Ecosystem

- ADM

- Bunge

- Cargill

- Louis Dreyfus

- COFCO Group

- Wilmar International

- Jinshahe Group

- GoodMills Group

- Milne MicroDried

- Carolina Innovative Food Ingredients

- Liuxu Food

- Live Glean

- NorQuin

- Andean Valley Corporation

Key Developments in Wheat Flour Alternative Industry

- January 2023: ADM acquired a specialty ingredients company for xx billion, significantly expanding its portfolio of Rice Flour and Sweet Potato Flour offerings, strengthening its position in the gluten-free bakery segment.

- March 2024: NorQuin launched a new line of high-protein Quinoa Flour blends, specifically targeting the sports nutrition and health supplement markets, estimated to add xx billion in annual revenue.

- June 2023: Carolina Innovative Food Ingredients announced a xx million investment in a new facility to scale up production of its unique sweet potato-based flours, addressing growing demand from the Fried Food and Pastry sectors.

- August 2022: GoodMills Group introduced an innovative Corn Flour variant with improved binding properties, opening new applications in gluten-free pasta and Noodles, aiming for xx billion market share increase.

- November 2024: Live Glean partnered with a major retail chain to distribute its upcycled alternative flours, leveraging food waste streams to create sustainable products and capture an estimated xx billion in the eco-conscious consumer market.

Strategic Wheat Flour Alternative Market Forecast

The Wheat Flour Alternative Market is poised for unprecedented expansion during the Forecast Period: 2025–2033, driven by a powerful confluence of strategic growth catalysts. Future opportunities are largely centered on innovation in functional properties and targeted nutrition, with specialized flours like Almond Flour and Quinoa Flour seeing sustained premium demand. The burgeoning plant-based food movement will continue to fuel the adoption of these alternatives across all application segments, from Baked Goods to Fried Food, projecting a market value exceeding xx billion by 2033. Strategic investments in R&D to enhance flavor, texture, and shelf-life, coupled with expanding distribution channels in emerging economies, will unlock vast market potential. Furthermore, sustainable sourcing practices and transparent supply chains will become increasingly crucial, appealing to an environmentally conscious consumer base and generating an additional xx billion in revenue from responsible consumption patterns.

Wheat Flour Alternative Segmentation

-

1. Application

- 1.1. Baked Goods

- 1.2. Noodles

- 1.3. Pastry

- 1.4. Fried Food

- 1.5. Others

-

2. Type

- 2.1. Corn Flour

- 2.2. Rice Flour

- 2.3. Sweet Potato Flour

- 2.4. Quinoa Flour

- 2.5. Almond Flour

- 2.6. Others

Wheat Flour Alternative Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Wheat Flour Alternative Regional Market Share

Geographic Coverage of Wheat Flour Alternative

Wheat Flour Alternative REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.85% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Baked Goods

- 5.1.2. Noodles

- 5.1.3. Pastry

- 5.1.4. Fried Food

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Corn Flour

- 5.2.2. Rice Flour

- 5.2.3. Sweet Potato Flour

- 5.2.4. Quinoa Flour

- 5.2.5. Almond Flour

- 5.2.6. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Wheat Flour Alternative Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Baked Goods

- 6.1.2. Noodles

- 6.1.3. Pastry

- 6.1.4. Fried Food

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Corn Flour

- 6.2.2. Rice Flour

- 6.2.3. Sweet Potato Flour

- 6.2.4. Quinoa Flour

- 6.2.5. Almond Flour

- 6.2.6. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Wheat Flour Alternative Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Baked Goods

- 7.1.2. Noodles

- 7.1.3. Pastry

- 7.1.4. Fried Food

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Corn Flour

- 7.2.2. Rice Flour

- 7.2.3. Sweet Potato Flour

- 7.2.4. Quinoa Flour

- 7.2.5. Almond Flour

- 7.2.6. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Wheat Flour Alternative Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Baked Goods

- 8.1.2. Noodles

- 8.1.3. Pastry

- 8.1.4. Fried Food

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Corn Flour

- 8.2.2. Rice Flour

- 8.2.3. Sweet Potato Flour

- 8.2.4. Quinoa Flour

- 8.2.5. Almond Flour

- 8.2.6. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Wheat Flour Alternative Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Baked Goods

- 9.1.2. Noodles

- 9.1.3. Pastry

- 9.1.4. Fried Food

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Corn Flour

- 9.2.2. Rice Flour

- 9.2.3. Sweet Potato Flour

- 9.2.4. Quinoa Flour

- 9.2.5. Almond Flour

- 9.2.6. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Wheat Flour Alternative Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Baked Goods

- 10.1.2. Noodles

- 10.1.3. Pastry

- 10.1.4. Fried Food

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Corn Flour

- 10.2.2. Rice Flour

- 10.2.3. Sweet Potato Flour

- 10.2.4. Quinoa Flour

- 10.2.5. Almond Flour

- 10.2.6. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Wheat Flour Alternative Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Baked Goods

- 11.1.2. Noodles

- 11.1.3. Pastry

- 11.1.4. Fried Food

- 11.1.5. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Corn Flour

- 11.2.2. Rice Flour

- 11.2.3. Sweet Potato Flour

- 11.2.4. Quinoa Flour

- 11.2.5. Almond Flour

- 11.2.6. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 ADM

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Bunge

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Cargill

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Louis Dreyfus

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 COFCO Group

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Wilmar International

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Jinshahe Group

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 GoodMills Group

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Milne MicroDried

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Carolina Innovative Food Ingredients

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Liuxu Food

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Live Glean

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 NorQuin

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Andean Valley Corporation

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 ADM

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Wheat Flour Alternative Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Wheat Flour Alternative Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Wheat Flour Alternative Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Wheat Flour Alternative Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Wheat Flour Alternative Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Wheat Flour Alternative Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Wheat Flour Alternative Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Wheat Flour Alternative Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Wheat Flour Alternative Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Wheat Flour Alternative Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Wheat Flour Alternative Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Wheat Flour Alternative Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Wheat Flour Alternative Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Wheat Flour Alternative Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Wheat Flour Alternative Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Wheat Flour Alternative Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Wheat Flour Alternative Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Wheat Flour Alternative Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Wheat Flour Alternative Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Wheat Flour Alternative Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Wheat Flour Alternative Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Wheat Flour Alternative Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Wheat Flour Alternative Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Wheat Flour Alternative Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Wheat Flour Alternative Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Wheat Flour Alternative Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Wheat Flour Alternative Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Wheat Flour Alternative Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Wheat Flour Alternative Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Wheat Flour Alternative Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Wheat Flour Alternative Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Wheat Flour Alternative Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Wheat Flour Alternative Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Wheat Flour Alternative Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Wheat Flour Alternative Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Wheat Flour Alternative Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Wheat Flour Alternative Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Wheat Flour Alternative Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Wheat Flour Alternative Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Wheat Flour Alternative Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Wheat Flour Alternative Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Wheat Flour Alternative Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Wheat Flour Alternative Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Wheat Flour Alternative Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Wheat Flour Alternative Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Wheat Flour Alternative Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Wheat Flour Alternative Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Wheat Flour Alternative Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Wheat Flour Alternative Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Wheat Flour Alternative Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Wheat Flour Alternative Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Wheat Flour Alternative Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Wheat Flour Alternative Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Wheat Flour Alternative Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Wheat Flour Alternative Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Wheat Flour Alternative Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Wheat Flour Alternative Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Wheat Flour Alternative Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Wheat Flour Alternative Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Wheat Flour Alternative Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Wheat Flour Alternative Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Wheat Flour Alternative Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Wheat Flour Alternative Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Wheat Flour Alternative Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Wheat Flour Alternative Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Wheat Flour Alternative Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Wheat Flour Alternative Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Wheat Flour Alternative Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Wheat Flour Alternative Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Wheat Flour Alternative Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Wheat Flour Alternative Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Wheat Flour Alternative Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Wheat Flour Alternative Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Wheat Flour Alternative Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Wheat Flour Alternative Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Wheat Flour Alternative Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Wheat Flour Alternative Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Wheat Flour Alternative?

The projected CAGR is approximately 8.85%.

2. Which companies are prominent players in the Wheat Flour Alternative?

Key companies in the market include ADM, Bunge, Cargill, Louis Dreyfus, COFCO Group, Wilmar International, Jinshahe Group, GoodMills Group, Milne MicroDried, Carolina Innovative Food Ingredients, Liuxu Food, Live Glean, NorQuin, Andean Valley Corporation.

3. What are the main segments of the Wheat Flour Alternative?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.48 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Wheat Flour Alternative," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Wheat Flour Alternative report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Wheat Flour Alternative?

To stay informed about further developments, trends, and reports in the Wheat Flour Alternative, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence