Key Insights

The United States cardiovascular devices market is a significant and rapidly expanding sector, projected to reach a substantial size over the forecast period (2025-2033). Driven by an aging population, increasing prevalence of cardiovascular diseases like coronary artery disease, heart failure, and arrhythmias, and advancements in minimally invasive surgical techniques and device technology, the market demonstrates robust growth. The 7.80% CAGR indicates a consistently high demand for innovative diagnostic and therapeutic devices, including pacemakers, implantable cardioverter-defibrillators (ICDs), stents, and cardiac valves. The market is segmented into diagnostic and monitoring devices (e.g., electrocardiograms, echocardiography equipment) and therapeutic and surgical devices, with the latter segment expected to dominate due to the rising number of procedures requiring interventional cardiology and cardiac surgery. Key players like Medtronic, Abbott Laboratories, and Boston Scientific Corporation are heavily invested in R&D, leading to continuous product innovation and market consolidation. However, factors like high device costs, stringent regulatory approvals, and the potential for complications associated with device implantation act as restraints on market expansion. Nevertheless, the long-term outlook remains positive, fueled by ongoing technological advancements and increasing healthcare expenditure.

The North American region, particularly the United States, holds a major share of the global cardiovascular devices market due to its advanced healthcare infrastructure, high prevalence of cardiovascular diseases, and strong regulatory frameworks supporting medical device development and adoption. The market's future growth will likely be shaped by several factors including the development and adoption of telemonitoring technologies, the rise of personalized medicine approaches in cardiovascular care, and an increasing focus on improving patient outcomes and reducing healthcare costs. The ongoing focus on improving the longevity and reliability of implanted devices will continue to drive innovation and reshape the competitive landscape. Furthermore, strategic partnerships and collaborations between device manufacturers and healthcare providers are expected to facilitate wider market penetration and streamline device deployment. Competitive advantages are likely to accrue to companies prioritizing data-driven analytics, improved patient support services, and a strong emphasis on product safety and efficacy.

United States Cardiovascular Devices Market: A Comprehensive Report (2019-2033)

This insightful report provides a detailed analysis of the United States cardiovascular devices market, offering a comprehensive overview of market trends, leading players, and future growth opportunities. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report is an invaluable resource for stakeholders seeking to understand and capitalize on this dynamic market. The market is valued at xx Million in 2025 and is projected to reach xx Million by 2033.

United States Cardiovascular Devices Market Composition & Trends

This section delves into the competitive landscape of the US cardiovascular devices market, examining market concentration, innovation drivers, regulatory influences, substitute products, end-user profiles, and mergers & acquisitions (M&A) activity. The market is characterized by a high degree of consolidation, with key players such as Medtronic, Abbott Laboratories, and Boston Scientific holding significant market share. However, smaller, innovative companies are also contributing significantly to advancements in the field.

- Market Share Distribution: Medtronic holds an estimated xx% market share, followed by Abbott Laboratories at xx% and Boston Scientific at xx%. The remaining market share is distributed among other key players and smaller participants.

- Innovation Catalysts: Continuous advancements in minimally invasive procedures, telemedicine integration, and the development of AI-driven diagnostic tools are driving significant innovation.

- Regulatory Landscape: The FDA's regulatory framework plays a crucial role, shaping product development and market entry. Stringent regulatory approvals influence the speed of innovation and market penetration.

- Substitute Products: While limited, alternative treatment methods and lifestyle changes pose some level of competition.

- End-User Profiles: The primary end-users include hospitals, cardiac care centers, and ambulatory surgical centers. Growth in the aging population significantly contributes to market demand.

- M&A Activities: Recent years have witnessed significant M&A activity, exemplified by Royal Philips' acquisition of Cardiologs in November 2021 for an estimated xx Million. These deals reflect the industry's consolidation trend and the pursuit of technological advancements. Average deal values are estimated at xx Million.

United States Cardiovascular Devices Market Industry Evolution

The US cardiovascular devices market has experienced robust growth from 2019 to 2024, fueled by a confluence of factors: the escalating prevalence of cardiovascular diseases (CVDs), substantial increases in healthcare expenditure, and groundbreaking technological advancements. While precise CAGR figures require further specification, the market demonstrated a significant expansion during this period. Minimally invasive procedures, enabled by technological progress, have dramatically improved patient outcomes, driving market demand. This trend is further amplified by the growing adoption of sophisticated imaging technologies and data analytics, facilitating more accurate diagnoses and personalized treatment strategies. A notable shift in consumer preferences towards less invasive, cost-effective, and home-based care options also significantly influences market dynamics. The forecast period (2025-2033) projects continued, accelerated growth driven by these factors, further fueled by the rapid adoption of innovative technologies. However, it's crucial to acknowledge that growth rates and adoption metrics will vary considerably across different device types and market segments. A projected CAGR of [Insert Projected CAGR]% is anticipated for the forecast period.

Leading Regions, Countries, or Segments in United States Cardiovascular Devices Market

Growth and adoption rates within the US cardiovascular devices market exhibit regional variations. However, substantial market presence is observed across diverse regions, reflecting the widespread distribution of healthcare facilities and the pervasive nature of CVDs nationwide. Currently, the Therapeutic and Surgical Devices segment commands a larger market share than the Diagnostic and Monitoring Devices segment, primarily due to the higher demand for interventional procedures. This disparity is expected to persist, albeit with potential shifts driven by technological advancements in diagnostic and remote monitoring capabilities.

Key Drivers for Therapeutic and Surgical Devices Segment Dominance:

- Soaring Prevalence of Cardiovascular Diseases: The high and increasing incidence of conditions requiring interventions directly fuels demand for therapeutic and surgical devices.

- Rapid Technological Advancements: Innovations in minimally invasive techniques and sophisticated device designs significantly enhance adoption rates.

- Robust Investment in Healthcare Infrastructure: Continued and substantial investment in healthcare infrastructure provides a strong foundation for this segment's growth.

- Improved Treatment Outcomes: Minimally invasive procedures often lead to faster recovery times and reduced hospital stays, contributing to increased adoption.

Key Drivers for Diagnostic and Monitoring Devices Segment Growth:

- Growing Emphasis on Early and Preventative Diagnosis: Early detection and proactive disease management are increasing the utilization of diagnostic devices and remote monitoring solutions.

- Advancements in Remote Patient Monitoring (RPM): The expanding adoption of RPM technologies empowers continuous patient monitoring, leading to improved disease management and reduced hospital readmissions.

- Data-driven insights: The use of data analytics and AI to interpret diagnostic data allows for earlier detection and improved treatment planning.

United States Cardiovascular Devices Market Product Innovations

The US cardiovascular devices market has witnessed a remarkable surge in product innovation in recent years. These innovations consistently prioritize enhanced device performance, improved patient outcomes, and reduced invasiveness. Examples include the development of bioabsorbable stents, sophisticated drug-eluting stents, and minimally invasive surgical instruments. These advancements leverage cutting-edge materials, advanced sensors, and sophisticated data analytics to optimize treatment efficacy and patient comfort. Key selling points often center around improved precision, shorter procedure times, and accelerated patient recovery. The integration of artificial intelligence (AI) and machine learning (ML) is rapidly transforming the field, paving the way for more sophisticated diagnostic and therapeutic devices, including AI-powered diagnostic tools and personalized treatment algorithms.

Propelling Factors for United States Cardiovascular Devices Market Growth

Several key factors drive the growth of the US cardiovascular devices market. Technological advancements, such as minimally invasive procedures and improved device designs, significantly impact market expansion. The aging population, with its higher risk of cardiovascular diseases, increases demand. Favorable regulatory policies and increased healthcare spending further contribute to market growth. The growing adoption of telemedicine and remote patient monitoring solutions adds another layer of growth. These factors collectively contribute to a favorable market environment.

Obstacles in the United States Cardiovascular Devices Market

Despite significant growth potential, the US cardiovascular devices market confronts several challenges. Stringent regulatory hurdles, particularly FDA approvals, can impede product launches and increase development costs substantially. Supply chain disruptions and fluctuating raw material prices pose significant risks to profitability. Furthermore, intense competition amongst established and emerging players exerts considerable price pressure. These factors collectively present obstacles to sustained market growth, necessitating well-defined and adaptable management strategies for sustained success. Other challenges may include the high cost of new technologies, reimbursement limitations and the increasing scrutiny of healthcare costs.

Future Opportunities in United States Cardiovascular Devices Market

The US cardiovascular devices market presents numerous opportunities for growth. Emerging technologies like AI and machine learning hold immense potential for improved diagnostics and personalized treatments. Expanding into new markets, such as home healthcare and remote monitoring, offers significant growth potential. Developing innovative devices for underserved patient populations also presents a lucrative opportunity. The shift towards preventative care and personalized medicine will further fuel market expansion.

Major Players in the United States Cardiovascular Devices Market Ecosystem

- Biotronik

- GE Healthcare

- Abbott Laboratories

- Cardinal Health Inc

- Siemens Healthineers AG

- Medtronic PLC

- Edwards Lifesciences

- Boston Scientific Corporation

- W L Gore & Associates Inc

Key Developments in United States Cardiovascular Devices Market Industry

- November 2021: Royal Philips acquired Cardiologs, expanding its cardiac diagnostics and monitoring portfolio.

- March 2021: The FDA approved a non-surgical heart valve for pediatric and adult patients.

- June 1, 2020: Boston Scientific launched DIRECTSENSE Technology for monitoring RF energy delivery during cardiac ablation.

Strategic United States Cardiovascular Devices Market Forecast

The US cardiovascular devices market is poised for continued growth, driven by technological advancements, a rising prevalence of cardiovascular diseases, and increased healthcare spending. Future opportunities lie in the development of innovative, minimally invasive devices, the integration of AI and machine learning, and the expansion into new markets such as home healthcare and remote patient monitoring. The market's potential is substantial, with significant growth expected throughout the forecast period.

United States Cardiovascular Devices Market Segmentation

-

1. Device Type

-

1.1. Diagnostic and Monitoring Devices

- 1.1.1. Electrocardiogram (ECG)

- 1.1.2. Remote Cardiac Monitoring

- 1.1.3. Other Diagnostic and Monitoring Devices

-

1.2. Therapeutic and Surgical Devices

- 1.2.1. Cardiac Assist Devices

- 1.2.2. Cardiac Rhythm Management Device

- 1.2.3. Catheter

- 1.2.4. Grafts

- 1.2.5. Heart Valves

- 1.2.6. Stents

- 1.2.7. Other Therapeutic and Surgical Devices

-

1.1. Diagnostic and Monitoring Devices

United States Cardiovascular Devices Market Segmentation By Geography

- 1. United States

United States Cardiovascular Devices Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

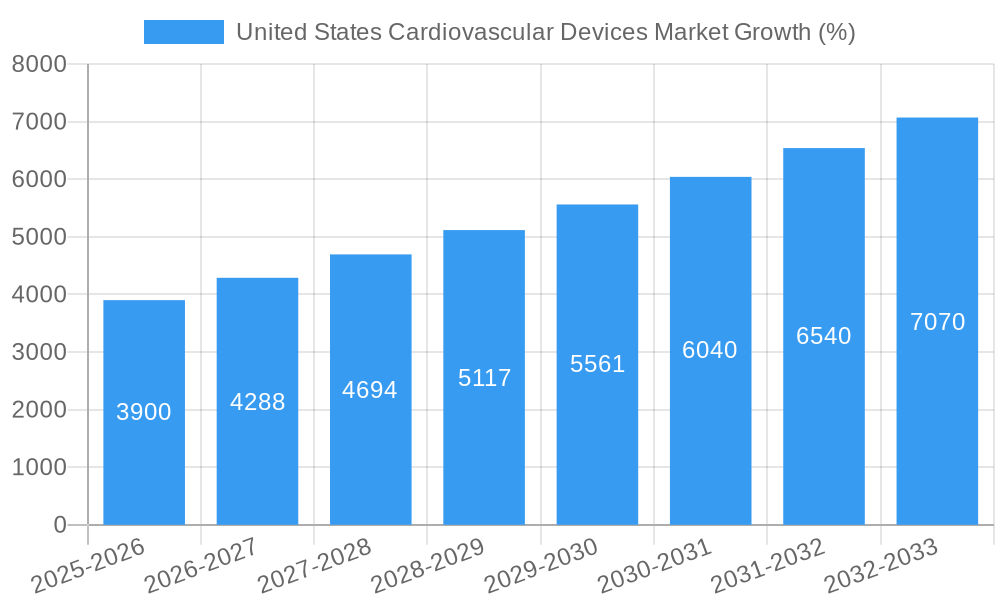

| Growth Rate | CAGR of 7.80% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rapid Technological Advancements; Increasing Burden of Cardiovascular Diseases; Increased Preference of Minimally Invasive Procedures

- 3.3. Market Restrains

- 3.3.1. Stringent Regulatory Policies; High Cost of Instruments and Procedures

- 3.4. Market Trends

- 3.4.1. Electrocardiogram (ECG) is Expected to Dominate the Diagnostic And Monitoring Segment Over the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. United States Cardiovascular Devices Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Device Type

- 5.1.1. Diagnostic and Monitoring Devices

- 5.1.1.1. Electrocardiogram (ECG)

- 5.1.1.2. Remote Cardiac Monitoring

- 5.1.1.3. Other Diagnostic and Monitoring Devices

- 5.1.2. Therapeutic and Surgical Devices

- 5.1.2.1. Cardiac Assist Devices

- 5.1.2.2. Cardiac Rhythm Management Device

- 5.1.2.3. Catheter

- 5.1.2.4. Grafts

- 5.1.2.5. Heart Valves

- 5.1.2.6. Stents

- 5.1.2.7. Other Therapeutic and Surgical Devices

- 5.1.1. Diagnostic and Monitoring Devices

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. United States

- 5.1. Market Analysis, Insights and Forecast - by Device Type

- 6. United States United States Cardiovascular Devices Market Analysis, Insights and Forecast, 2019-2031

- 7. Canada United States Cardiovascular Devices Market Analysis, Insights and Forecast, 2019-2031

- 8. Mexico United States Cardiovascular Devices Market Analysis, Insights and Forecast, 2019-2031

- 9. Competitive Analysis

- 9.1. Market Share Analysis 2024

- 9.2. Company Profiles

- 9.2.1 Biotronik

- 9.2.1.1. Overview

- 9.2.1.2. Products

- 9.2.1.3. SWOT Analysis

- 9.2.1.4. Recent Developments

- 9.2.1.5. Financials (Based on Availability)

- 9.2.2 GE Healthcare

- 9.2.2.1. Overview

- 9.2.2.2. Products

- 9.2.2.3. SWOT Analysis

- 9.2.2.4. Recent Developments

- 9.2.2.5. Financials (Based on Availability)

- 9.2.3 Abbott Laboratories

- 9.2.3.1. Overview

- 9.2.3.2. Products

- 9.2.3.3. SWOT Analysis

- 9.2.3.4. Recent Developments

- 9.2.3.5. Financials (Based on Availability)

- 9.2.4 Cardinal Health Inc

- 9.2.4.1. Overview

- 9.2.4.2. Products

- 9.2.4.3. SWOT Analysis

- 9.2.4.4. Recent Developments

- 9.2.4.5. Financials (Based on Availability)

- 9.2.5 Siemens Healthineers AG

- 9.2.5.1. Overview

- 9.2.5.2. Products

- 9.2.5.3. SWOT Analysis

- 9.2.5.4. Recent Developments

- 9.2.5.5. Financials (Based on Availability)

- 9.2.6 Medtronic PLC

- 9.2.6.1. Overview

- 9.2.6.2. Products

- 9.2.6.3. SWOT Analysis

- 9.2.6.4. Recent Developments

- 9.2.6.5. Financials (Based on Availability)

- 9.2.7 Edwards Lifesciences

- 9.2.7.1. Overview

- 9.2.7.2. Products

- 9.2.7.3. SWOT Analysis

- 9.2.7.4. Recent Developments

- 9.2.7.5. Financials (Based on Availability)

- 9.2.8 Boston Scientific Corporation

- 9.2.8.1. Overview

- 9.2.8.2. Products

- 9.2.8.3. SWOT Analysis

- 9.2.8.4. Recent Developments

- 9.2.8.5. Financials (Based on Availability)

- 9.2.9 W L Gore & Associates Inc

- 9.2.9.1. Overview

- 9.2.9.2. Products

- 9.2.9.3. SWOT Analysis

- 9.2.9.4. Recent Developments

- 9.2.9.5. Financials (Based on Availability)

- 9.2.1 Biotronik

List of Figures

- Figure 1: United States Cardiovascular Devices Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: United States Cardiovascular Devices Market Share (%) by Company 2024

List of Tables

- Table 1: United States Cardiovascular Devices Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: United States Cardiovascular Devices Market Volume K Units Forecast, by Region 2019 & 2032

- Table 3: United States Cardiovascular Devices Market Revenue Million Forecast, by Device Type 2019 & 2032

- Table 4: United States Cardiovascular Devices Market Volume K Units Forecast, by Device Type 2019 & 2032

- Table 5: United States Cardiovascular Devices Market Revenue Million Forecast, by Region 2019 & 2032

- Table 6: United States Cardiovascular Devices Market Volume K Units Forecast, by Region 2019 & 2032

- Table 7: United States Cardiovascular Devices Market Revenue Million Forecast, by Country 2019 & 2032

- Table 8: United States Cardiovascular Devices Market Volume K Units Forecast, by Country 2019 & 2032

- Table 9: United States United States Cardiovascular Devices Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: United States United States Cardiovascular Devices Market Volume (K Units) Forecast, by Application 2019 & 2032

- Table 11: Canada United States Cardiovascular Devices Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Canada United States Cardiovascular Devices Market Volume (K Units) Forecast, by Application 2019 & 2032

- Table 13: Mexico United States Cardiovascular Devices Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Mexico United States Cardiovascular Devices Market Volume (K Units) Forecast, by Application 2019 & 2032

- Table 15: United States Cardiovascular Devices Market Revenue Million Forecast, by Device Type 2019 & 2032

- Table 16: United States Cardiovascular Devices Market Volume K Units Forecast, by Device Type 2019 & 2032

- Table 17: United States Cardiovascular Devices Market Revenue Million Forecast, by Country 2019 & 2032

- Table 18: United States Cardiovascular Devices Market Volume K Units Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the United States Cardiovascular Devices Market?

The projected CAGR is approximately 7.80%.

2. Which companies are prominent players in the United States Cardiovascular Devices Market?

Key companies in the market include Biotronik, GE Healthcare, Abbott Laboratories, Cardinal Health Inc, Siemens Healthineers AG, Medtronic PLC, Edwards Lifesciences, Boston Scientific Corporation, W L Gore & Associates Inc .

3. What are the main segments of the United States Cardiovascular Devices Market?

The market segments include Device Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Rapid Technological Advancements; Increasing Burden of Cardiovascular Diseases; Increased Preference of Minimally Invasive Procedures.

6. What are the notable trends driving market growth?

Electrocardiogram (ECG) is Expected to Dominate the Diagnostic And Monitoring Segment Over the Forecast Period.

7. Are there any restraints impacting market growth?

Stringent Regulatory Policies; High Cost of Instruments and Procedures.

8. Can you provide examples of recent developments in the market?

In November 2021, the company Royal Philips announced the acquisition of Cardiologs to expand its cardiac diagnostics and monitoring portfolio

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Units.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "United States Cardiovascular Devices Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the United States Cardiovascular Devices Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the United States Cardiovascular Devices Market?

To stay informed about further developments, trends, and reports in the United States Cardiovascular Devices Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence